Industrial Ethernet Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

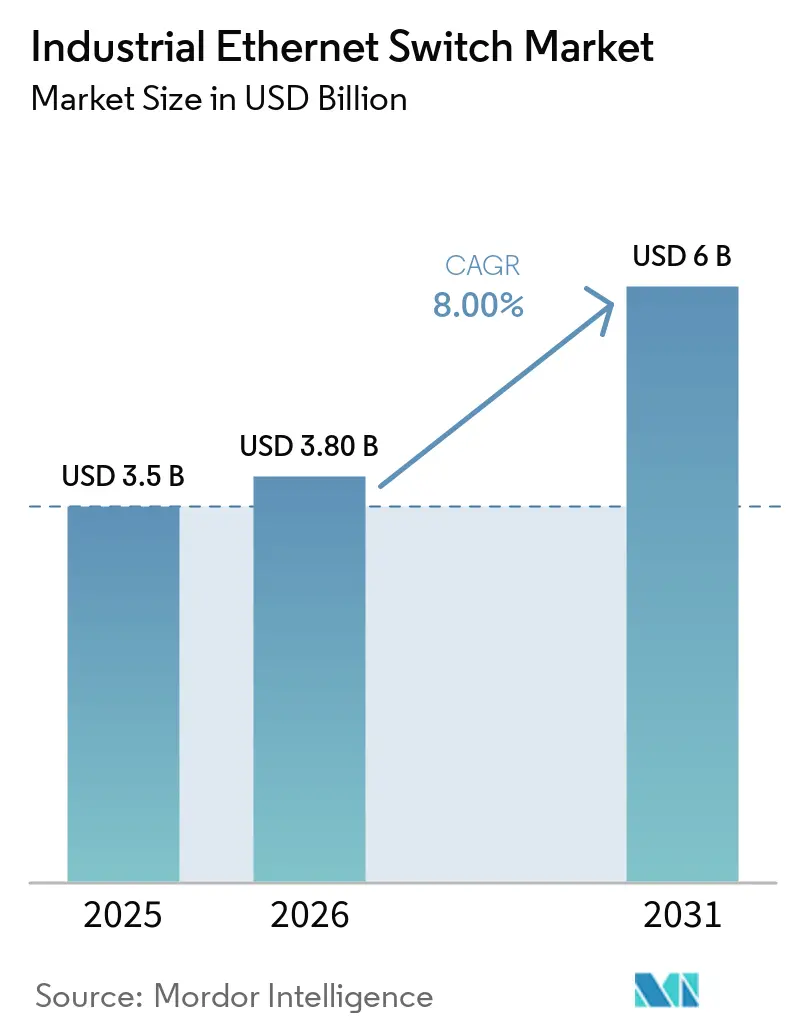

| Market Size (2026) | USD 3.80 Billion |

| Market Size (2031) | USD 6 Billion |

| Growth Rate (2026 - 2031) | 8.00% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Ethernet Switch Market Analysis by Mordor Intelligence

The Industrial Ethernet Switch Market size is expected to increase from USD 3.50 billion in 2025 to USD 3.80 billion in 2026 and reach USD 6.00 billion by 2031, growing at a CAGR of 8% over 2026-2031. Growing demand for deterministic networking in automotive and semiconductor facilities is accelerating the migration from legacy fieldbus to Ethernet architectures that support Time-Sensitive Networking and Ethernet-APL. Heightened cybersecurity regulations, notably IEC 62443 and the European Union’s NIS2 Directive, are pushing end users toward Layer 3 managed platforms with embedded intrusion detection, favoring vendors that integrate security rather than sell commodity hardware. Edge-computing workloads, high-resolution vision systems, and the proliferation of smart sensors are lifting 10 Gigabit adoption and fueling demand for switches with more than 48 ports. Supply-chain tightness for mature-node ASICs is lengthening lead times, while the skills gap in industrial networking is prompting buyers to embrace cloud-managed switches that simplify configuration.

Key Report Takeaways

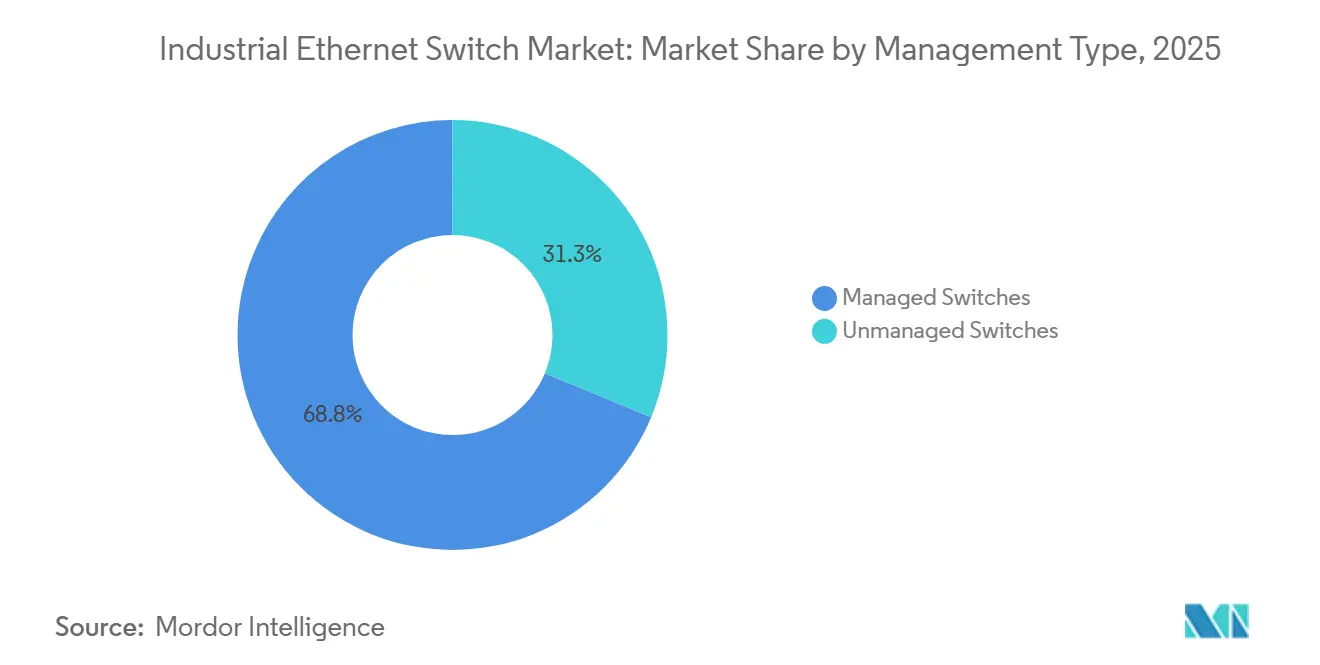

- By management type, managed switches commanded 68.75% of the Industrial Ethernet Switch Market share in 2025 and are forecast to expand at an 11.31% CAGR through 2031.

- By layer capability, Layer 2 hardware held 61.40% share in 2025, while Layer 3 platforms are projected to grow fastest at 11.76% CAGR to 2031.

- By number of ports, the 9-24 port class accounted for 37.85% share in 2025, whereas switches with more than 48 ports represent the fastest-growing bracket at 10.51% CAGR.

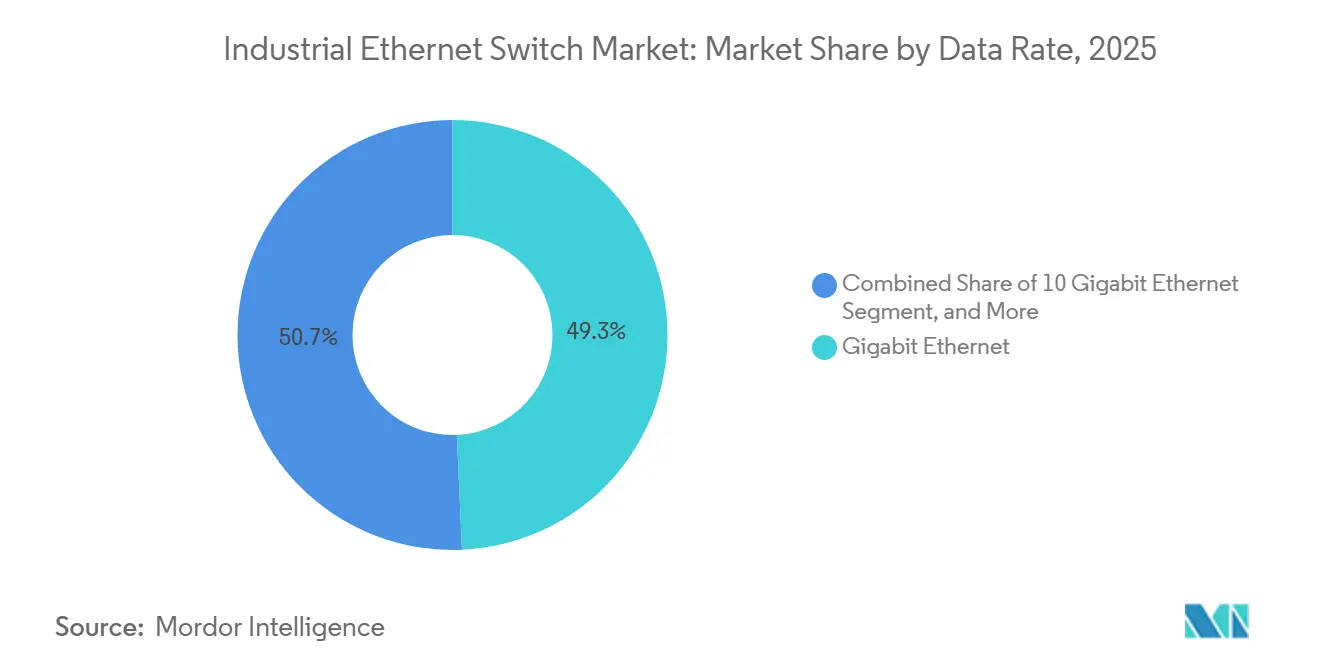

- By data rate, Gigabit Ethernet captured 49.30% share in 2025, yet the 10 Gigabit tier is poised to rise at a 10.88% CAGR through 2031.

- By end-user industry, discrete manufacturing led with 28.60% revenue share in 2025, while government and smart-city deployments are advancing at a 9.25% CAGR to 2031.

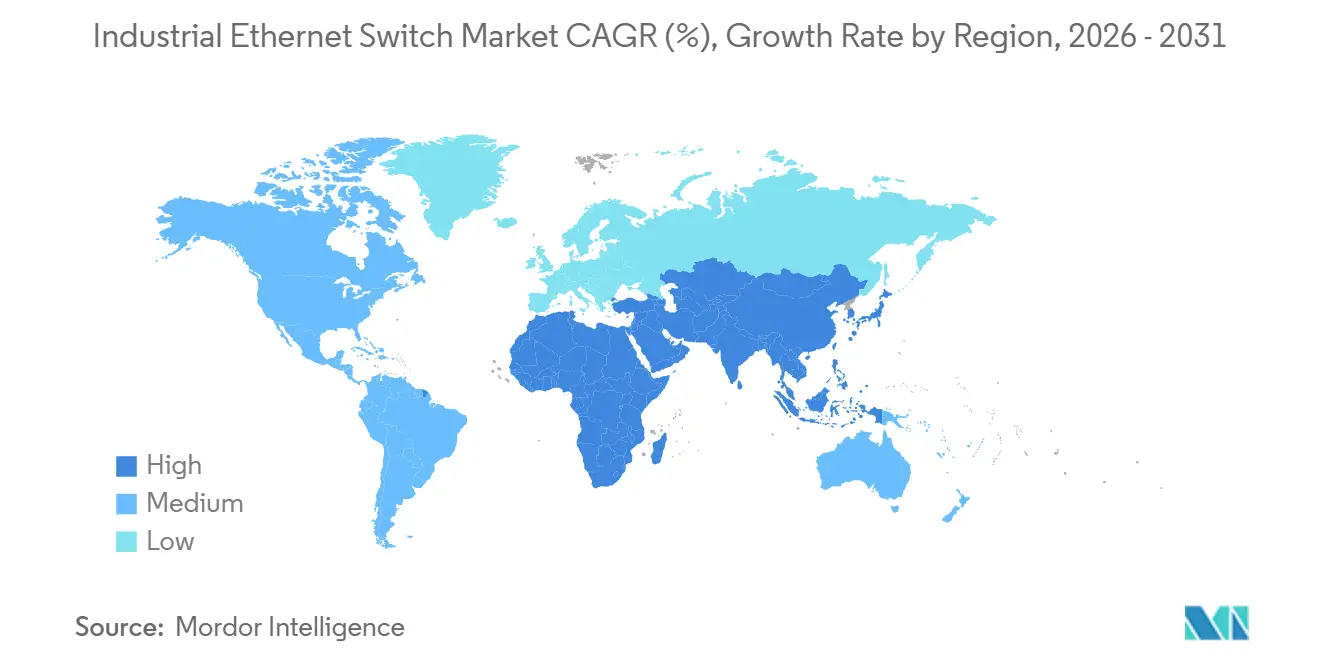

- By geography, Asia-Pacific dominated with 35.12% share in 2025 and is forecast to post a 9.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Ethernet Switch Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid Expansion of IIoT Deployments | +2.1% | Global, led by APAC and North America | Medium term (2–4 years) |

| Rising Demand for Deterministic Networking in Smart Factories | +1.8% | Europe and APAC, spill-over to North America | Medium term (2–4 years) |

| Migration from Fieldbus to Ethernet in Process Industries | +1.5% | Global, concentrated in Europe and North America corridors | Long term (≥4 years) |

| Increasing Adoption of Power over Ethernet for Edge Devices | +1.2% | North America and Europe, early APAC uptake | Short term (≤2 years) |

| Compliance Requirements for Time-Sensitive Networking (TSN) | +1.0% | Europe, APAC, North America | Medium term (2–4 years) |

| Surge in Cyber-Physical Security Investments Post-2025 | +0.9% | Global, regulation-driven in North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of IIoT Deployments

Industrial Internet of Things programs are multiplying Ethernet endpoints in production lines, with industrial Ethernet capturing 76% of new-node installations in 2025. Each smart sensor or edge appliance needs a switch port, and unmanaged daisy chains introduce latency that disrupts 10-50 millisecond control loops. Utilities illustrate the shift; Electricity North West installed rugged switches in United Kingdom substations to stream synchrophasor data at 50 frames per second, traffic that legacy serial links cannot manage. Switch makers now embed IEEE 1588 grandmaster clocks, eliminating standalone timing boxes and trimming bill of materials by roughly 15%. As plant operators see commissioning times fall, demand rises for ports with deterministic forwarding—an anchor trend for the Industrial Ethernet Switch Market.

Rising Demand for Deterministic Networking in Smart Factories

Automotive and semiconductor plants require sub-microsecond synchronization for collaborative robots and vision systems, achievable only with TSN-ready switches. Finalized IEEE 802.1Qbv and 802.1AS standards let devices reserve bandwidth for control traffic, while relegating diagnostics to best-effort queues. European automakers lead adoption after AUTOSAR named Ethernet the in-vehicle backbone in 2024. Siemens updated its SCALANCE XC-300 line in 2025 with IEEE 802.1Qci filtering, insulating networks from rogue traffic.[1]Siemens AG, “SCALANCE XC-300 and XR-300 Industrial Ethernet Switches,” siemens.comDiscrete manufacturers report that TSN shortens commissioning by 30-40%, confirming its pull on Industrial Ethernet Switch Market demand.

Migration from Fieldbus to Ethernet in Process Industries

Chemical and oil-and-gas operators are retiring HART and FOUNDATION Fieldbus in favor of Ethernet-APL, ratified in 2024 to deliver 10 Mbps over 1,000 meters in Zone 1 areas. Ethernet-APL switches integrate intrinsically safe power supplies, cutting cabinet footprints by half. Swiss gas utility Gaznat’s 2025 upgrade reduced cabling costs by 60% and enabled remote firmware updates without hot-work permits. Modular chassis accepting both Ethernet-APL and PROFIBUS modules allow phased migration without downtime, reinforcing the Industrial Ethernet Switch Market’s growth trajectory inside process plants.

Increasing Adoption of Power over Ethernet for Edge Devices

IEEE 802.3bt provides up to 90 watts per port, energizing PTZ cameras, Wi-Fi 6 access points, and compact PLCs without extra wiring. Smart-city rollouts lead: Actelis Networks powered 1,200 streetlights in Chino, California via PoE++ over existing coax in 2025, sidestepping USD 150,000 per mile trenching costs. Industrial sites use PoE to energize explosion-proof cameras and wireless vibration sensors, centralizing UPS protection. Heat dissipation remains a hurdle because a fully loaded 24-port PoE++ switch can generate 600 watts, adding USD 200-300 in enclosure cooling, but the labor savings keep PoE adoption buoyant.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Upfront CAPEX for Ruggedised Switches | -1.2% | Global, acute in APAC and South America | Short term (≤2 years) |

| Lack of Skilled Industrial Networking Personnel | -1.0% | Global, severe in North America and Europe | Medium term (2–4 years) |

| Legacy Equipment Integration Challenges | -0.8% | Global brownfield sites | Long term (≥4 years) |

| Supply Chain Volatility of Specialized ASICs | -0.7% | Global, longest lead times in North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for Ruggedised Switches

Industrial-grade switches with extended temperature ratings and conformal coating cost 200-400% more than commercial gear. A Cisco Industrial Ethernet 5000 with 10 Gigabit uplinks lists at about USD 15,400 against USD 906.50 for an entry-level IE2000, and hazardous-location certifications add USD 500-1,000 per unit.[2]Cisco Systems, “Industrial Ethernet Switch Portfolio and Pricing 2026,” cisco.com Railway and oil-rig projects need EN 50155 or ATEX compliance, inflating budgets and delaying procurement. Leasing models aim to flatten spending, yet customers remain cautious because obsolescence risk reverts to the buyer if products are discontinued mid-term.

Lack of Skilled Industrial Networking Personnel

Only 10% of automation professionals are fluent in both fieldbus and IT protocols, leaving more than 1,000 roles unfilled in early 2026 across North America. Retiring PLC experts compound the gap, and universities have yet to scale curricula. Zero-touch provisioning helps, but it introduces new cyber-risks because persistent internet links reach deep into the shop floor. Misconfigured QoS can add 100 milliseconds of jitter, and diagnosing the problem requires packet analysis skills many electricians lack, slowing Industrial Ethernet Switch Market deployments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Management Type: Cybersecurity Demands Propel Managed Platforms

Managed hardware captured 68.75% of the Industrial Ethernet Switch Market in 2025 and is set to rise at 11.31% CAGR through 2031. Regulatory mandates such as NIS2 oblige operators of essential services to segment networks and maintain audit trails, capabilities only managed devices offer. Process plants prioritize SNMP traps and syslog for centralized monitoring, while discrete lines still use unmanaged units when point-to-point links suffice. “Smart unmanaged” products with read-only dashboards blur boundaries, yet firmware-update requirements in forthcoming Cyber Resilience rules further tilt spending toward fully managed gear. Vendors embedding zero-trust access controls at the port level stand to gain share as end users elevate switches from connectivity devices to critical security assets.

Unmanaged switches retain footholds in machine-mounted clusters where configuration overhead outweighs visibility gains. Rockwell’s Stratix 2100, introduced mid-2025, targets this niche with 5- and 8-port variants. However, as patching obligations expand, brownfield plants are replacing still-functional unmanaged units, enlarging the addressable pool for managed platforms and supporting long-run growth of the Industrial Ethernet Switch Market size for this segment.

By Layer Capability: Routing Comes to the Factory Edge

Layer 2 products held 61.40% share in 2025, yet Layer 3 switches are advancing at 11.76% CAGR as edge computers need inter-VLAN routing for micro-segments. Utilities adopt Layer 3 to carry routed GOOSE messages per IEC 61850 Edition 2.1, letting substations exchange status across wide territories without multicast flooding. Belden’s XTran line, launched in 2025, exemplifies the trend by combining routed GOOSE with MPLS and SD-WAN.

Cost barriers are falling; Broadcom and Marvell chips trimmed 20% since 2024, shrinking the premium between Layer 2 and Layer 3 products. As discrete manufacturers isolate production zones with ACLs on-box, Layer 3 becomes the default upgrade path, boosting the Industrial Ethernet Switch Market size for routing-capable hardware and narrowing appeal for pure Layer 2 devices.

By Number of Ports: High-Density Platforms Aggregate Sensor Tsunamis

Switches sporting 9-24 ports controlled 37.85% share in 2025, but more than 48-port units are expanding at 10.51% CAGR as automotive lines and smart-city poles bundle hundreds of endpoints onto single backplanes. Moxa’s 52-port EDS-4000, shipping since 2024, caters to welding cells hosting 20-30 connections each. Hyperscale colocation providers installing factory-edge compute favor 24-port 10 Gigabit uplink models as aggregation layers, while municipalities load 48-port PoE++ devices into curbside cabinets to feed cameras and 5G small cells.

At the opposite pole, up-to-8-port units reside in wind-turbine nacelles and pumping stations. Advantech’s modular EKI-7000 lets integrators scale from 16 to 32 ports, smoothing multi-phase builds. The polarization in buying patterns squeezes 25-48 port mid-range options, reinforcing divergent demand yet collectively enlarging the Industrial Ethernet Switch Market.

By Data Rate: 10 Gigabit Moves from Luxury to Baseline

Gigabit Ethernet posted 49.30% share in 2025, but 10 Gigabit links are growing at 10.88% CAGR as 12-megapixel cameras stream 5.76 Gbps uncompressed video. NEXCOM’s ISA 142 TSN switch with eight 10 Gigabit ports debuted in 2025, letting vision traffic and control commands coexist. Falling PHY prices cut 10 Gigabit cost per Gig by 35% since 2024, enticing midsize plants to adopt today rather than endure forklifts later.

Sub-100 Mbps remains only where serial gateways persist, while 40 Gigabit uplinks penetrate semiconductor fabs and pharma cleanrooms. Versitron’s SGX75270MA brings 40 Gigabit QSFP+ plus IEEE 1588v2 for sub-100 nanosecond sync. As time-critical workloads rise, 10 Gigabit becomes the new access speed, scaling the Industrial Ethernet Switch Market size for high-bandwidth tiers.

By End-User Industry: Municipal Modernization Sets the Pace

Discrete manufacturing led with 28.60% share in 2025, underpinned by automotive, aerospace, and electronics plants that demand deterministic traffic. Government and smart-city programs are the growth engine at 9.25% CAGR, driven by fiber-to-the-pole builds that require -40 °C to +75 °C switches certified to NEMA TS2. Actelis’ 2025 project in Chino highlights the cost savings of leveraging existing coax runs.

Process industries are converting to Ethernet-APL for hazardous areas, while transportation operators install EN 50155-rated gear aboard rolling stock. Energy utilities specify IEC 61850 hardware with 500,000-hour MTBF and 20 millisecond ring recovery. Each vertical has unique certification hurdles, but all share a push toward higher bandwidth, cybersecurity, and manageability, broadening total Industrial Ethernet Switch Market demand.

Geography Analysis

Asia-Pacific led the Industrial Ethernet Switch Market with 35.12% share in 2025 and is projected to post a 9.89% CAGR to 2031. India’s automation sector is set to climb from USD 3.64 billion in 2026 to USD 13.65 billion by 2034, fueling switch purchases in greenfield factories. China’s EV and semiconductor clusters require TSN-capable gear for ±1 microsecond sync, while Japanese machine-tool builders embed 10 Gigabit switches inside CNC controllers, trimming cabinet footprints by 30%. South Korean shipyards deploy marine-rated fiber backbones to replace proprietary serial lines, and Australian utilities migrate to IEC 61850 Edition 2.1 Layer 3 architectures. Regional labor cost advantages shorten payback periods despite rugged-hardware premiums, and government smart-manufacturing incentives pull forward replacement cycles.

North America holds a strong position, buoyed by reshoring that expands automotive and medical-device capacity. The U.S. CISA’s 2025 guidance on network segmentation compels utilities and transit agencies to retire unmanaged equipment. CenterPoint Energy’s 2025 pipeline backbone cut OPEX by 25% after converging leak-detection telemetry on Ethernet. Canadian mines deploy Class I Division 1 switches tolerant to -40 °C, and Mexican tier-1 suppliers wait 20 weeks for TSN-certified hardware amid ASIC shortages. The region confronts a deep skills shortage, extending median hiring to 120 days and nudging buyers to cloud-managed devices.

Europe commands substantial share thanks to automotive and chemical producers enforcing TSN. NIS2, effective October 2024, pushes managed switches in utilities, transit, and health care. Germany’s Industry 4.0 drive accelerates OPC UA over TSN adoption, with Beckhoff embedding switch fabrics inside control platforms. Electricity North West connected phasor meters via rugged hardware in 2025, and France’s railways standardize on EN 50155 devices with 20 millisecond ring recovery. Lead times for 28-65 nm ASICs top 30 weeks in 2026, spotlighting supply-chain constraints even as smart-grid and factory-modernization budgets expand across Italy and Spain.

Competitive Landscape

The Industrial Ethernet Switch Market is moderately fragmented. Siemens, Rockwell Automation, and Schneider Electric protect installed bases through proprietary configuration suites and bundled multi-year services. Their switches ship pre-configured for native protocols, easing controller integration and justifying premium prices. Specialists such as Moxa, Belden, and Phoenix Contact win transportation and energy niches by offering enclosures pre-certified to EN 50155 or IEC 61850-3, saving users months of compliance work. Cisco and Hewlett Packard Enterprise blur IT and OT lines by layering industrial protocols onto mainstream platforms, a proposition attractive to operators consolidating vendor lists.

Cybersecurity stands out as the new differentiator. UL Solutions certified EtherCAT’s cyber resilience to IEC 62443-4-1/-4-2 Security Level 2 in April 2026, setting a bar many smaller firms cannot match.[3]UL Solutions, “EtherCAT Cyber Resilience Certified 2026,” ul.com Edge-compute convergence opens white space: switches are evolving into nodes that combine compute and storage alongside networking. Belden’s BRS-5G, unveiled in April 2026, merges an eight-port Gigabit switch with an on-board Snapdragon X72 5G modem, offering 10 Gbps downlink where fiber is absent. Patent filings reveal a race to slash MACsec latency below 10 microseconds, crucial for motion control, suggesting intensifying competition in hardware-accelerated encryption.

Supply-chain volatility shapes pricing power. Mature-node ASIC shortages extend industrial switch lead times beyond 30 weeks, and spot premiums climb 300-500%. Vendors with multi-fab sourcing or in-house ASIC design hold an edge, while buyers negotiate longer contracts to lock inventory. Skills scarcity adds another competitive lever; companies offering cloud-based, wizard-driven provisioning lower the barrier for plants lacking networking engineers, capturing incremental Industrial Ethernet Switch Market share.

Industrial Ethernet Switch Industry Leaders

Siemens AG

Schneider Electric SE

Belden Inc.

Moxa Inc.

Rockwell Automation, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Phoenix Contact divested Perle Systems to Hitron Technologies to focus on zero-trust networking and TSN development.

- April 2026: Belden introduced the BRS-5G industrial switch with an integrated Snapdragon X72 5G modem, delivering 10 Gbps downlink for mobile and remote sites.

- April 2026: ABB announced a USD 75 million expansion of its Bengaluru manufacturing campus to add capacity for low-voltage switchgear and control systems.

- March 2026: Phoenix Contact partnered with Xona to embed zero-trust access controls in its EP Raptor switch line.

Global Industrial Ethernet Switch Market Report Scope

The Industrial Ethernet Switch Market caters to rugged industrial settings. These switches ensure dependable, real-time data transmission across sectors like factories, utilities, transportation, and energy. Engineered to endure extreme temperatures, vibrations, electrical noise, and humidity, their demand surges with the rise of industrial automation, IIoT, and smart manufacturing.

The Industrial Ethernet Switch Market Report is Segmented by Management Type (Managed Switches, and Unmanaged Switches), Layer Capability (Layer 2, and Layer 3), Number of Ports (Up to 8 Ports, 9-24 Ports, 25-48 Ports, and More than 48 Ports), Data Rate (≤100 Mbps, Gigabit Ethernet, 10 Gigabit Ethernet, and 40 Gigabit and Above), End-User Industry (Discrete Manufacturing, Process Industries, Transportation and Logistics, Energy and Utilities, Government and Smart Cities, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Managed Switches |

| Unmanaged Switches |

| Layer 2 |

| Layer 3 |

| Up to 8 Ports |

| 9-24 Ports |

| 25–-8 Ports |

| More than 48 Ports |

| ≤100 Mbps |

| Gigabit Ethernet |

| 10 Gigabit Ethernet |

| 40 Gigabit and Above |

| Discrete Manufacturing |

| Process Industries |

| Transportation and Logistics |

| Energy and Utilities |

| Government and Smart Cities |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Management Type | Managed Switches | |

| Unmanaged Switches | ||

| By Layer Capability | Layer 2 | |

| Layer 3 | ||

| By Number of Ports | Up to 8 Ports | |

| 9-24 Ports | ||

| 25–-8 Ports | ||

| More than 48 Ports | ||

| By Data Rate | ≤100 Mbps | |

| Gigabit Ethernet | ||

| 10 Gigabit Ethernet | ||

| 40 Gigabit and Above | ||

| By End-User Industry | Discrete Manufacturing | |

| Process Industries | ||

| Transportation and Logistics | ||

| Energy and Utilities | ||

| Government and Smart Cities | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current Industrial Ethernet Switch Market size and its expected value by 2031?

The Industrial Ethernet Switch Market size stands at USD 3.80 billion in 2026 and is projected to reach USD 6.00 billion by 2031, reflecting an 8% CAGR over 2026-2031.

Which management type is growing fastest within the Industrial Ethernet Switch Market?

Managed switches are advancing at an 11.31% CAGR through 2031 as cybersecurity mandates drive upgrades.

Why is 10 Gigabit Ethernet adoption accelerating in factory networks?

High-resolution machine-vision cameras and edge analytics require multi-gigabit throughput, pushing 10 Gigabit switch demand, which is growing at a 10.88% CAGR.

Which region leads Industrial Ethernet Switch Market demand, and what is its growth outlook?

Asia-Pacific holds 35.12% share and is forecast to expand at a 9.89% CAGR through 2031, propelled by large-scale automation projects in China and India.

How are cybersecurity regulations influencing switch selection?

Standards such as IEC 62443 and the EU NIS2 Directive compel operators to deploy managed, Layer 3 switches with segmentation and intrusion detection, displacing unmanaged hardware.

Page last updated on: