Rubber Vulcanization Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.11 Billion |

| Market Size (2031) | USD 5.05 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

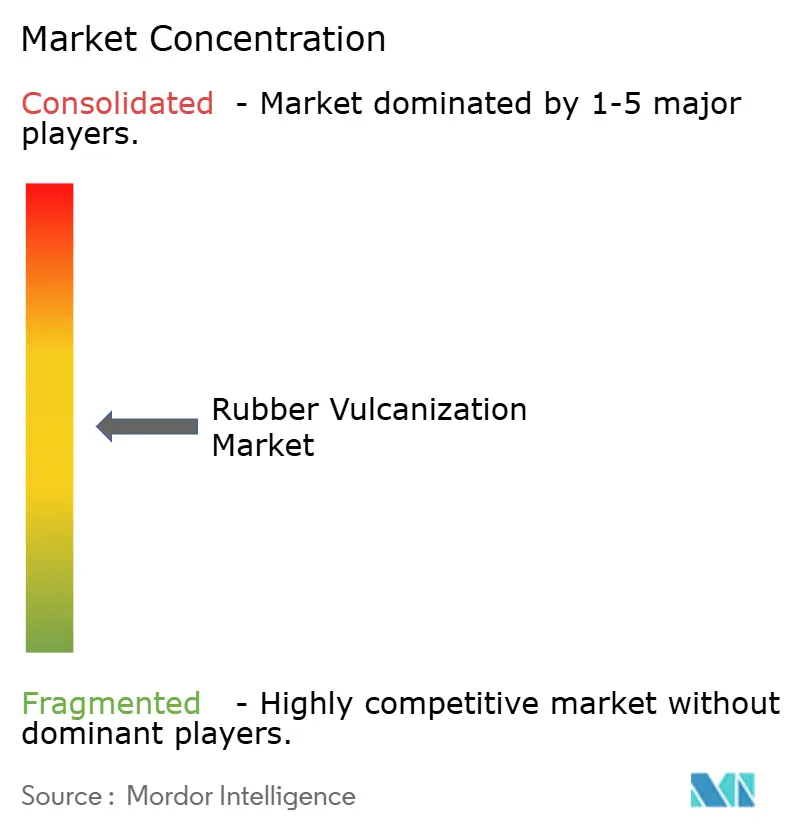

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rubber Vulcanization Market Analysis by Mordor Intelligence

The Rubber Vulcanization Market size was valued at USD 3.94 billion in 2025 and is expected to grow from USD 4.11 billion in 2026 to USD 5.05 billion by 2031, growing at a CAGR of 4.22% from 2026 to 2031. This steady climb reflects several converging forces. Tire makers are switching to low-rolling-resistance compounds that call for ultra-fast accelerators, while industrial users retrofit continuous-line curing to boost throughput. Regionally, Asia-Pacific dominates demand thanks to the sheer scale of Chinese and Indian tire output, and that dominance is widening as local suppliers integrate upstream to cap feedstock costs. On the supply side, sulfur-donor systems and peroxide cures are gaining share because they stretch scarce elemental sulfur and deliver higher cross-link density in high-temperature applications. Real-time analytics and AI-driven formulation tools now let compounders shorten development cycles by half, further stimulating consumption of high-performance curing agents.

Key Report Takeaways

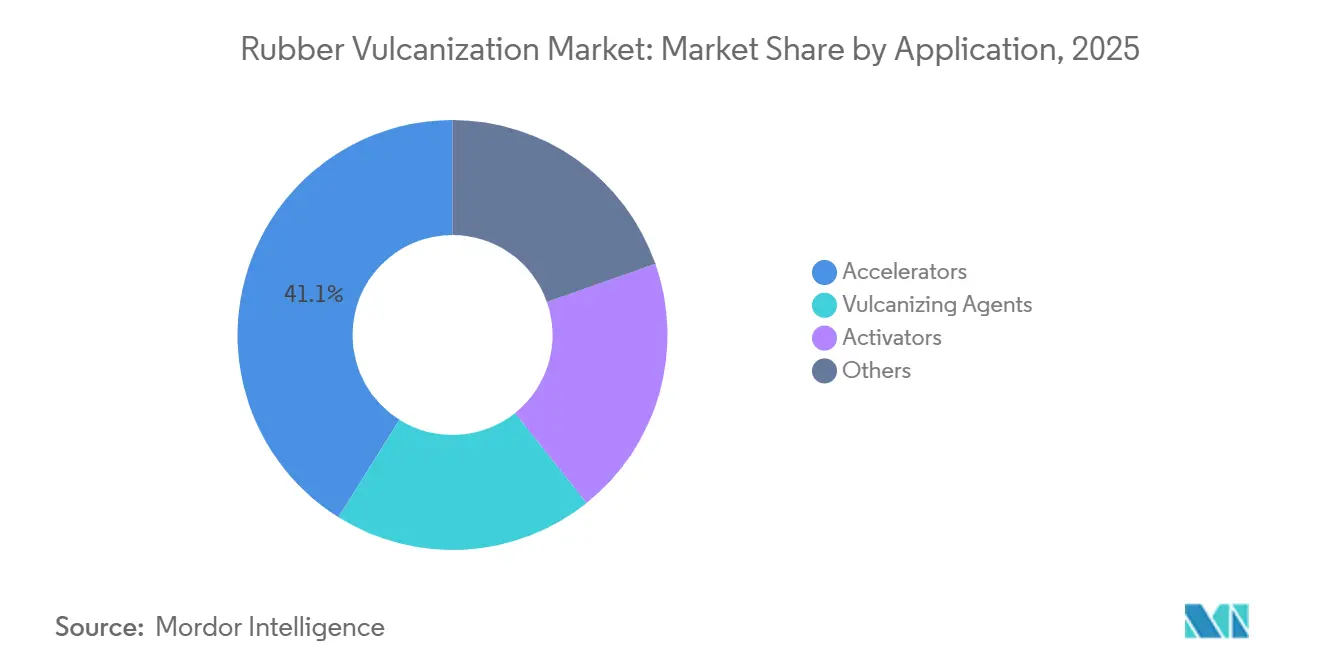

- By product type, accelerators led with 41.11% revenue share in 2025, while vulcanizing agents are forecast to expand at a 4.63% CAGR between 2026 and 2031.

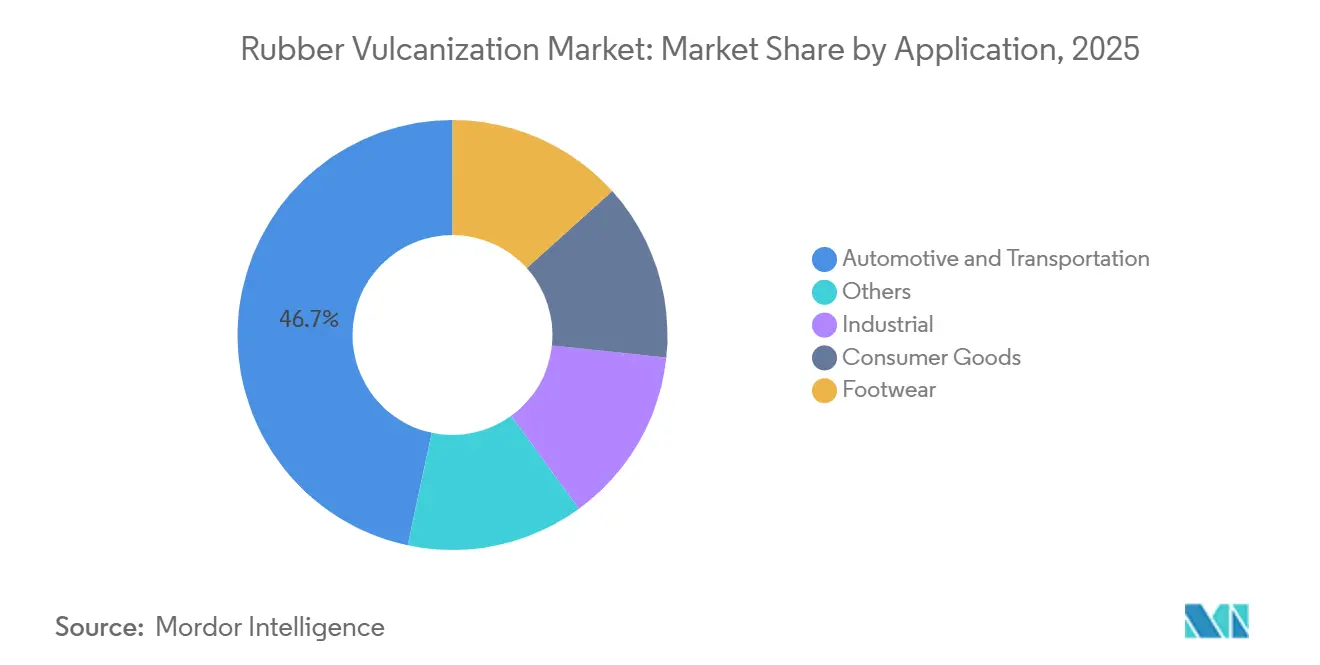

- By application, automotive and transportation accounted for 46.67% of the rubber vulcanization chemicals market share in 2025, yet consumer goods recorded the fastest projected 5.07% CAGR between 2026 and 2031.

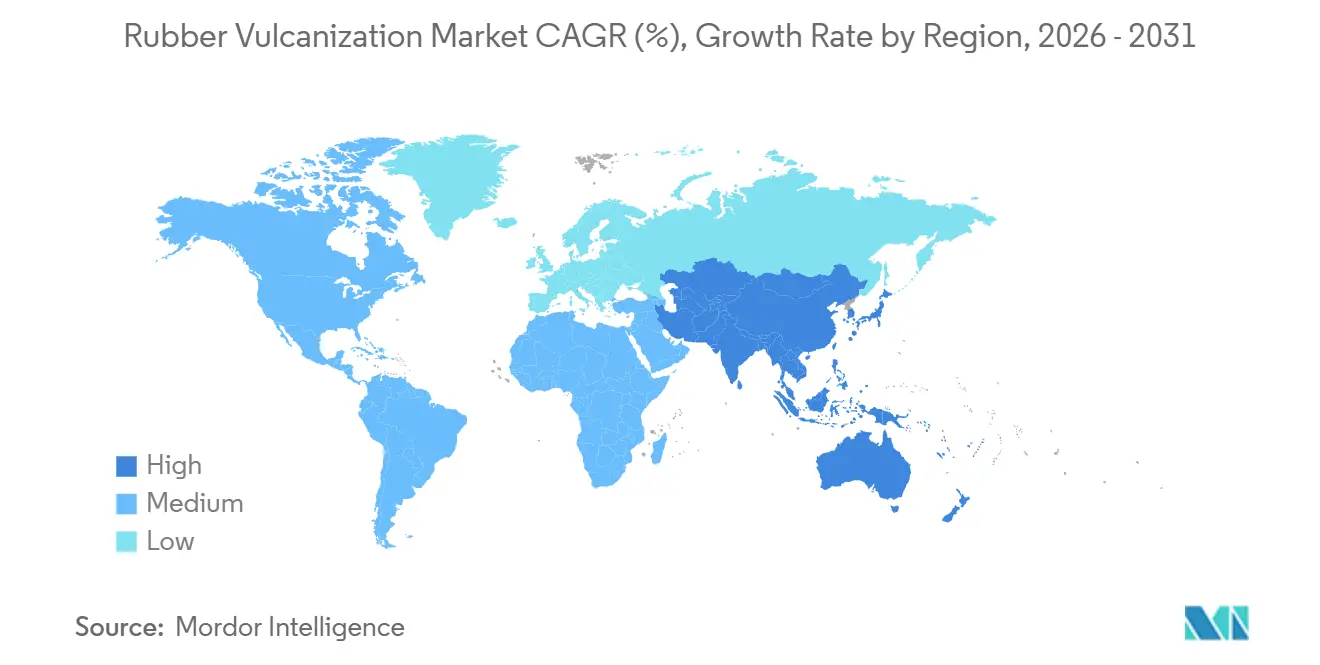

- By geography, Asia-Pacific captured 50.22% of the 2025 value and is advancing at a 5.13% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rubber Vulcanization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward high-performance, low-rolling-resistance rubber compounds | +1.20% | Global, with concentration in the EU, North America, and China | Medium term (2-4 years) |

| Expansion of Asia-Pacific manufacturing and infrastructure spend | +1.50% | APAC core (China, India, ASEAN), spill-over to MEA | Long term (≥ 4 years) |

| Industrial demand for conveyor, hose and belt upgrades | +0.60% | Global, led by mining-intensive regions (Australia, South America, Africa) | Medium term (2-4 years) |

| Microwave and continuous-line vulcanization retrofits slash cure time | +0.50% | APAC and South America, early adoption in India, Thailand, Brazil | Short term (≤ 2 years) |

| AI-driven real-time cure-profile optimization boosting plant yield | +0.40% | Global, concentrated in Tier-1 tire plants and integrated rubber-goods manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward High-Performance, Low-Rolling-Resistance Rubber Compounds

Driven by global mandates on tire energy efficiency, compounders are shifting from carbon black to precipitated silica. This transition necessitates the use of thiuram and sulfenamide accelerators, which can initiate curing at lower temperatures. Continental introduced its EcoContact 7 tire in 2025, achieving a reduction in rolling resistance without compromising wet grip[1]Continental AG, “EcoContact 7 Launch,” continental.com. This was accomplished by blending natural rubber with ultra-fast CBS accelerators. A forthcoming European Union regulation mandates a QR code indicating a product's carbon footprint. This makes low-product-carbon-footprint accelerators a key criterion for original equipment manufacturer procurement. In response, BASF launched a 2026 line of butanediol and PolyTHF with reduced product carbon footprint, enabling formulators to tout significant emission reductions. Additionally, bio-based additives like Kraton's SYLVATRAXX are enhancing these formulations, boosting traction while preserving rebound properties.

Expansion of Asia-Pacific Manufacturing and Infrastructure Spend

In 2025, China accounted for a significant share of global production, manufacturing a substantial number of passenger-car tires. Meanwhile, in 2026, India also recorded notable growth in production compared to the previous year. Both nations are strengthening their greenfield capacities, supported by considerable investments from leading domestic brands. On the upstream front, Kumho Petrochemical and Tosoh are expanding their specialty elastomer lines, which require customized curing packages. Concurrently, LANXESS has significantly increased the output of its Qingdao promoter plant to meet the region's just-in-time demand. This strategic localization highlights the growth of the rubber vulcanization chemicals market, aligning with the expansion of Asia-Pacific's export-driven tire industry.

Industrial Demand for Conveyor, Hose and Belt Upgrades

Mining and infrastructure operators are swapping out older conveyor belts for flame-retardant, high-tensile designs that rely on peroxide or sulfur-donor systems to achieve tight cross-link density. Hydraulic hose manufacturers are now incorporating delayed-action accelerators, providing additional scorch safety to prevent delamination during high-pressure cycles. In underground coal mines, the transition from fabric-reinforced belts to steel-cord ones requires ultra-accelerators capable of achieving a high level of cure in a significantly reduced time, effectively improving press efficiency. While emerging reclaim technologies can process a substantial portion of used belts, they still depend on fresh accelerators to restore mechanical strength, highlighting a continued demand for chemicals despite the increased use of recycled content.

Microwave and Continuous-Line Vulcanization Retrofits Slash Cure Time

Microwave curing modules, operating at a specific frequency, have significantly reduced passenger-tire cure cycles, leading to a notable increase in line output on existing presses. Early adopters in India and Thailand have found the additional electricity costs to be reasonable, particularly when compared to the savings in capital investment. Continuous tunnels for hose and profile extrusion have effectively minimized scrap rates, although they require compounders to adjust zinc-oxide levels to prevent overheating. In response, LANXESS has introduced microwave-compatible Aflux and Aktiplast grades from its South Carolina facility since late 2025, providing tire plants with an efficient solution that simplifies the reformulation process.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility-butadiene, sulfur, zinc oxide | -1.10% | Global, acute in regions dependent on Middle East sulfur and Asia-Pacific butadiene | Short term (≤ 2 years) |

| 6PPD-quinone eco-toxicity scrutiny and potential bans | -0.50% | North America (Washington, California), EU regulatory review underway | Medium term (2-4 years) |

| Sulfur-supply shocks from mining curtailments in 2026-27 | -0.70% | Global, most severe for China and India as net importers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility - Butadiene, Sulfur, Zinc Oxide

In 2025, Chinese butadiene prices experienced an increase. By early 2026, North American contracts also saw a significant rise, creating a challenging price gap for non-integrated accelerator producers, making hedging difficult. During the same period, sulfur prices witnessed a substantial surge due to reduced output from Iranian mines, which resulted in a notable supply deficit. Zinc oxide prices also increased in early 2026 as smelters reduced production because of higher costs. These price dynamics have led to tighter profit margins, with NOCIL's earnings before interest, taxes, depreciation, and amortization declining in the third quarter of the fiscal year 2026. Larger multinational companies have managed to navigate these challenges by leveraging multi-regional sourcing networks, while smaller firms remain constrained by fixed contracts, putting pressure on their working capital.

6PPD-Quinone Eco-Toxicity Scrutiny and Potential Bans

Washington State's legislation requires the gradual elimination of a chemical used in tires unless the leachate complies with strict aquatic-toxicity standards. In 2024, California added the antidegradant to its Safer Consumer Products list, prompting a subsequent notice from the United States federal rulemakers. While Flexsys is experimenting with amine alternatives with significantly lower toxicity levels, it remains tight-lipped about potential launch dates. Tire manufacturers, facing these shifts, are now dual-sourcing replacements, often at higher costs. This pivot has led them to redirect research and development efforts from performance enhancements to meeting regulatory standards, thereby limiting short-term demand growth for conventional antidegradants[2]Flexsys, “6PPD Replacement Program,” flexsys.com .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Accelerators Anchor Revenue, Vulcanizing Agents Lead Growth

Accelerators contributed 41.11% of 2025 sales, confirming their central role in every major rubber recipe. Sulfenamide grades ensure sufficient scorch safety at mixing temperatures and achieve full curing in a short time at press temperatures, solidifying their status as a staple for tires and industrial products. While more expensive, Thiuram accelerators allow for minimal sulfur loadings. This capability is crucial for low-rolling-resistance tread compounds, a feature Continental integrated into its EcoContact 7. While activators like zinc oxide have a slow maturation process, there is a rising demand for magnesium-based variants, which resist thermal hotspots, thanks to microwave retrofits. The market for vulcanizing agents in rubber vulcanization chemicals is projected to surpass that of accelerators. This shift comes as sulfur donors and peroxide systems effectively tackle challenges related to sulfur supply and durability at high temperatures, expanding at a 4.63% CAGR between 2026 and 2031. China Sunsine and NOCIL are doubling down on integrated sulfur-donor packages, aiming to lock in customers that prefer a single-source bundle.

Vulcanizing agents include elemental sulfur, sulfur donors, peroxides, and specialty insoluble sulfur. Insoluble sulfur, which commands a premium, effectively eliminates surface bloom on radial belts. Meanwhile, peroxide curing is gaining traction in ethylene propylene diene monomer hoses, especially for electric-vehicle coolant circuits that operate at higher temperatures than traditional powertrains. Chinese suppliers are now providing combined accelerator-sulfur donor masterbatches, streamlining logistics. This is a service that mid-sized western firms need to match to maintain their market share. Additionally, microwave curing is driving up demand for ultra-fast donors, capable of completing cross-linking in a significantly reduced time. This trend underscores the rubber vulcanization chemicals market's preference for innovation over commoditization.

By Application: Automotive Dominates, Consumer Goods Accelerates

Automotive and transportation used 46.67%. In 2025, the demand for rubber vulcanization chemicals is expected to increase, as radial tires require significant amounts of cure agents and activators. This demand is further driven by electric vehicles, which need lower rolling resistance to balance the weight of their batteries, resulting in higher accelerator content in each tire. Additionally, replacement tires involve greater chemical expenditure compared to original equipment, as aftermarket brands reformulate them to offer extended warranties. While the share of rubber vulcanization chemicals in consumer goods is currently smaller, it is experiencing a faster growth rate, 5.07% CAGR between 2026 and 2031.

In Vietnam and Indonesia, footwear manufacturers are increasingly turning to ethylene-vinyl-acetate blends. These blends require precise sulfur-donor curves to achieve optimal rebound targets and maintain a low compression set. Producing athletic shoes involves significant consumption of accelerators. As global production rises, it's paralleled by increasing middle-class incomes. Additionally, industrial items like conveyor belts and hydraulic hoses account for a consistent share of the demand. This growth is bolstered by upgrades in mining and construction, which prefer peroxide-cured ethylene propylene diene monomer and nitrile rubber for their heat and oil resistance. This preference sustains a diverse demand for various vulcanization chemistries.

Geography Analysis

Asia-Pacific accounted for 50.22% of 2025 revenue and is expected to advance at a 5.13% CAGR through 2026 to 2031. China leads with a significant output of passenger-car tires, followed closely by India. Substantial investments continue to flow into new radial plants. LANXESS has notably increased capacity at its Qingdao facility. Meanwhile, China Sunsine is utilizing its large-scale accelerator line to deliver integrated packages at competitive landed costs. In Japan, Tosoh is expanding its offerings with chloroprene rubber, dependent on imported vulcanization chemicals, signaling a sustained demand in developed Asian markets.

North America and Europe account for a considerable portion of the global demand. Growth remains steady but is tempered by a mature vehicle parc and regulatory challenges, notably the impending limits on certain chemical compounds. LANXESS has commenced production of specialized grades in South Carolina, providing United States tire manufacturers with a local source and reducing freight times. BASF, in a bid to meet emission-labeling standards, has adopted environmentally friendly precursors and transitioned its Verbund site in China to fully renewable energy, offering a compliance edge to European clients.

South America, the Middle-East and Africa collectively account for a smaller share of the market. Brazil has increased its truck-bus-radial output, while Mexico has maintained a notable level of tire production, with both nations heavily reliant on accelerator imports from Asia. Due to reduced sulfur availability from Iran, feedstock supplies have tightened in this region. In response, several Brazilian plants are experimenting with alternative systems that significantly reduce sulfur input. Saudi Arabia is expanding its tire production capacity to cater to regional demand, presenting new opportunities for specialty curing agents once these lines become operational.

Competitive Landscape

The rubber vulcanization market is moderately fragmented. LANXESS, BASF, Eastman Chemical, and China Sunsine together account for a significant portion of the market's revenue, while numerous regional suppliers cater to niche demands. In recent years, LANXESS, operating multiple plants across various countries, increased its promoter output in China to meet rising local demand. China Sunsine, with substantial revenue, leverages vertical integration for cost benefits, sidestepping the volatility of spot butadiene. BASF has raised prices significantly, strategically bundling low-carbon variants favored by original equipment manufacturers in light of new European Union footprint regulations.

Rubber Vulcanization Industry Leaders

Arkema

China Sunsine Chemical Holdings Ltd.

Eastman Chemical Company

KUMHO PETROCHEMICAL

LANXESS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: NOCIL is set to inaugurate its INR 250 crore (approximately USD 30 million) Dahej facility in Gujarat, India. This facility will enhance the production of anti-degradants for tires and industrial rubber, improving durability, performance, and global supply reliability. The expansion will strengthen NOCIL’s position in the Rubber Vulcanization Market by meeting rising domestic and global demand.

- September 2025: LANXESS announced plans to expand its rubber additives production at the Goose Creek facility in South Carolina. The new capacity for processing promoters became operational in November 2025, aiming to cater to the rising United States demand. This development has strengthened supply reliability and enhanced operational efficiency, significantly impacting the United States Rubber Vulcanization Market.

Global Rubber Vulcanization Market Report Scope

Rubber vulcanization is a chemical process that strengthens raw rubber by creating cross-links between polymer chains using heat, pressure, and additives such as sulfur, accelerators, and stabilizers. This transformation enhances elasticity, durability, and resistance to heat, chemicals, and mechanical stress. Vulcanized rubber is essential for tires, seals, hoses, and countless industrial applications, making it a cornerstone of modern manufacturing and performance materials.

The Rubber Vulcanization Market is segmented by product type, application, and geography. By product type, the market is segmented into accelerators, vulcanizing agents, activators, and others. By application, the market is segmented into automotive and transportation, industrial, consumer goods, footwear, and other applications. The report also covers the market size and forecasts for the Rubber Vulcanization Market in 19 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Accelerators |

| Vulcanizing Agents |

| Activators |

| Others |

| Automotive and Transportation |

| Industrial |

| Consumer Goods |

| Footwear |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Accelerators | |

| Vulcanizing Agents | ||

| Activators | ||

| Others | ||

| By Application | Automotive and Transportation | |

| Industrial | ||

| Consumer Goods | ||

| Footwear | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the rubber vulcanization market?

The rubber vulcanization market stands at USD 4.11 billion in 2026 and is forecast to reach USD 5.05 billion by 2031 at a 4.22% CAGR from 2026 to 2031.

Which segment currently holds the largest share of demand?

Automotive and transportation applications held 46.67% of demand in 2025.

Which product type is projected to grow fastest?

Vulcanizing agents are projected to post the highest 4.63% CAGR between 2026 and 2031.

Why is Asia-Pacific dominating consumption?

China and India together produce well over 1 billion tires annually, driving more than half of global chemical demand.

How are feedstock price swings affecting suppliers?

Spikes in sulfur and butadiene have compressed margins, prompting backward integration and diversified sourcing among major producers.

What regulatory trend could reshape antidegradant demand?

Potential bans on 6PPD in the United States and the European Union are pushing tire makers toward low-toxicity alternatives.

Page last updated on: