Thermoplastic Vulcanizate (TPV) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

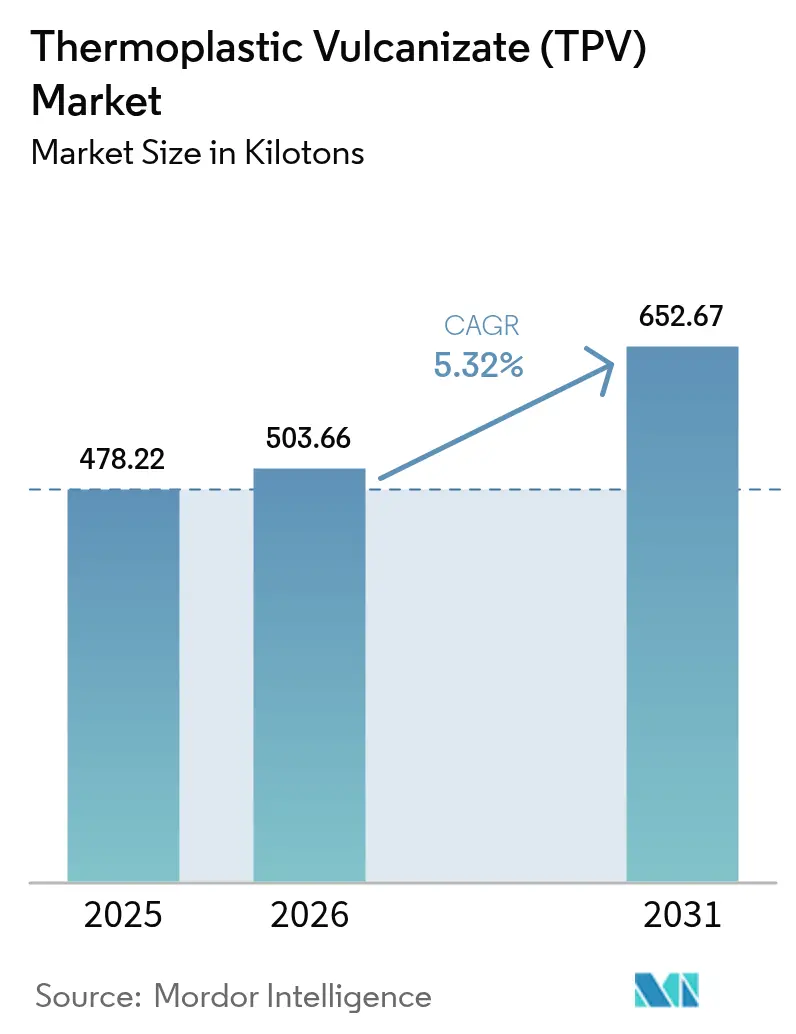

| Market Volume (2026) | 503.66 kilotons |

| Market Volume (2031) | 652.67 kilotons |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

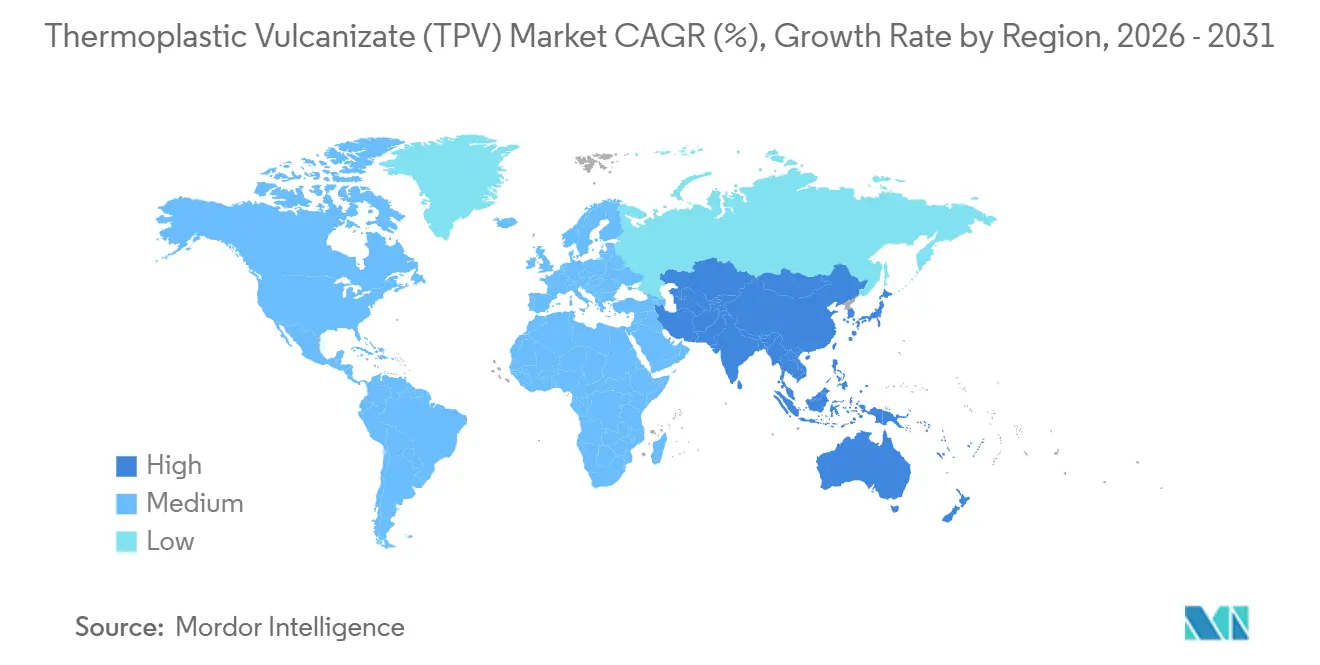

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

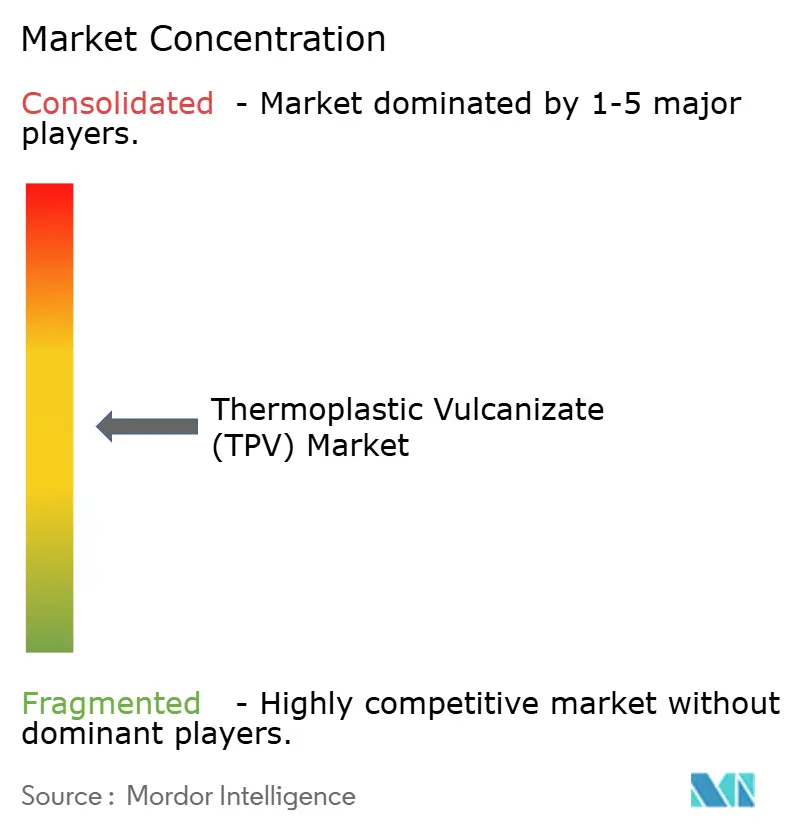

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermoplastic Vulcanizate (TPV) Market Analysis by Mordor Intelligence

The Thermoplastic Vulcanizate Market size is projected to expand from 478.22 kilotons in 2025 and 503.66 kilotons in 2026 to 652.67 kilotons by 2031, registering a CAGR of 5.32% between 2026 to 2031. Strong lightweighting mandates in global automotive platforms, the proliferation of electric-vehicle battery-pack sealing needs, and the rapid substitution of thermoset rubber in recyclable elastomer applications are defining the demand curve. Asia-Pacific maintains leadership because China produces almost one-third of worldwide vehicles, creating critical mass for tier-one suppliers to standardize TPV weatherstrips and under-hood parts. Bio-based grades are moving from pilot scale to commercial adoption as original-equipment manufacturers (OEMs) embed renewable-carbon targets in sourcing scorecards, while healthcare and battery-pack applications diversify end-market exposure. Competitive intensity stays moderate; the top five compounders hold 40%–45% of global capacity, allowing regional specialists to pursue niches such as recycled-content grades and heat-resistant formulations.

Key Report Takeaways

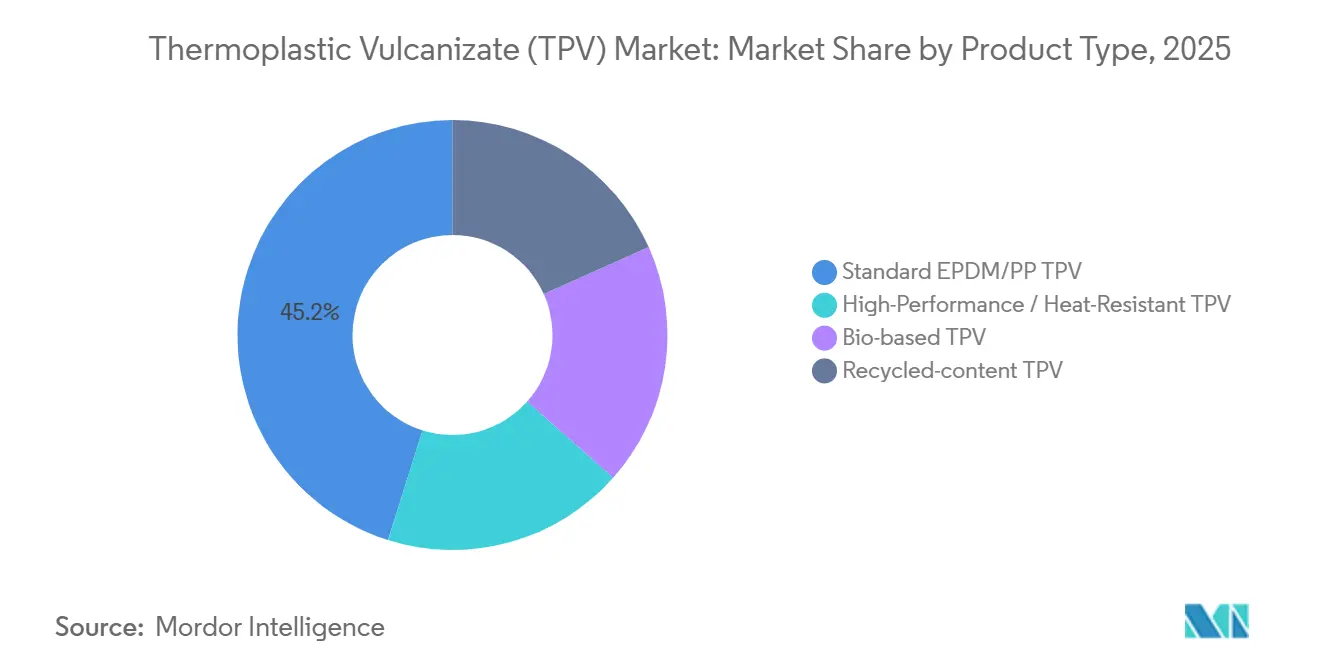

- By product type, standard EPDM/PP compounds represented 45.15% of the Thermoplastic Vulcanizate (TPV) market share in 2025, whereas bio-based grades are projected to post the fastest 6.82% CAGR through 2031.

- By application, sealing systems and weatherstrips led with 41.88% of 2025 volume; medical devices are on track for a 5.69% CAGR to 2031.

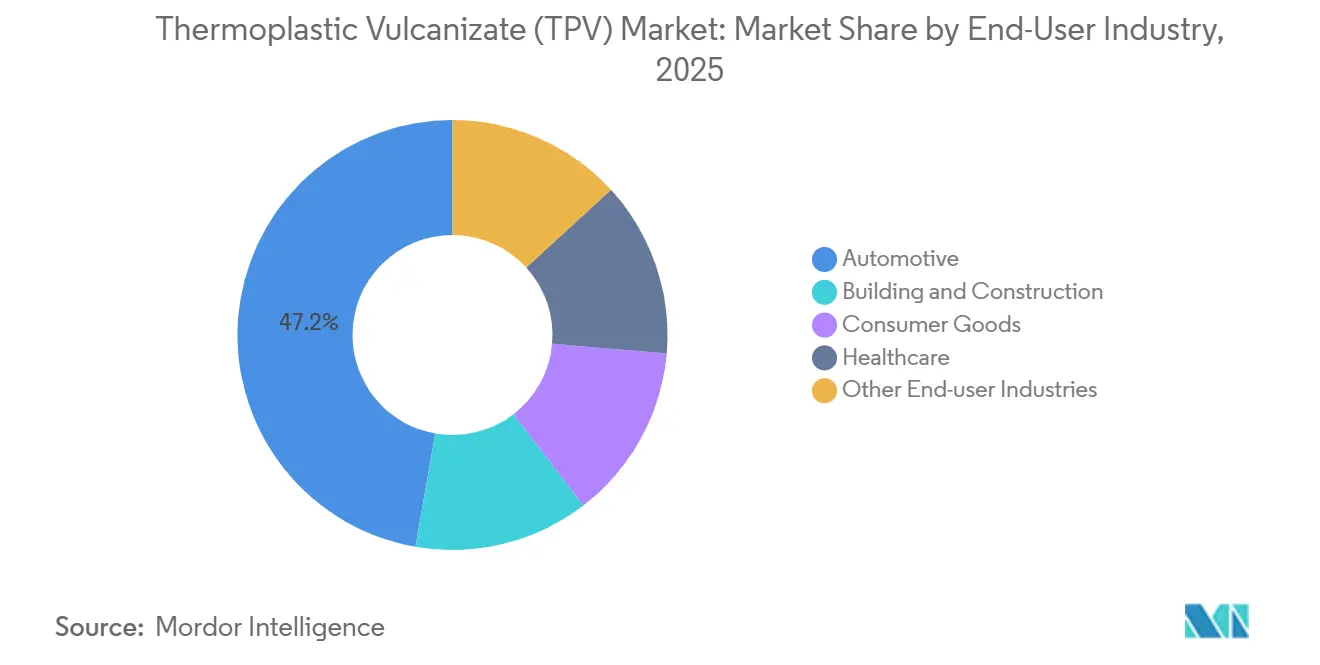

- By end-user, automotive retained 47.24% of 2025 demand, but healthcare is expected to register a 5.62% CAGR over 2026-2031.

- By geography, Asia-Pacific commanded 45.78% of the 2025 volume and is forecast to expand at 6.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermoplastic Vulcanizate (TPV) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising lightweighting demand from automotive OEMs | +1.4% | Global, core in Asia-Pacific with spill-over to North America and Europe | Medium term (2-4 years) |

| Surge in TPV-based soft-touch parts for consumer electronics | +0.8% | China, South Korea, Vietnam, selective North America | Short term (≤ 2 years) |

| OEM pivot toward recyclable elastomers | +1.1% | Europe and North America regulatory push, Asia-Pacific cost focus | Long term (≥ 4 years) |

| Expansion of EV battery-pack sealing uses | +1.3% | China, Germany, United States | Medium term (2-4 years) |

| Emergence of bio-based TPV grades | +0.6% | Europe and North America brand-owner mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Lightweighting Demand From Global Automotive OEMs

Automotive light-weighting goals have cascaded from primary metal structures to elastomeric parts, giving TPV a 20%–24% mass-saving edge over thermoset rubber in door seals and glass-run channels without part redesign[1]Celanese Corporation, “Santoprene TPV Technical Datasheet,” celanese.com. Every 10% curb-weight reduction improves battery-electric range by roughly 6%–8%, an efficiency lever OEMs need to satisfy the European Union’s 2027 fleet CO₂ cap of 93.6 g/km[2]European Automobile Manufacturers Association, “EU Fleet CO₂ Regulations Factsheet 2026,” acea.be. Chinese automakers such as BYD and NIO already integrate multi-material TPV seals on high-volume EV models, while tier-one suppliers Cooper Standard and Toyoda Gosei expanded Wuhan and Tianjin TPV extrusion lines in 2025 to chase 15%-plus compound growth targets. Adoption remains slower in North America, yet Ford retrofitted TPV belt-line seals on the 2025 F-150 Lightning to offset battery-pack mass penalties.

Surge in TPV-Based Soft-Touch Parts for Consumer Electronics

Smartphone, tablet, and wearable OEMs specify Shore A 60-80 TPV overmolds on polycarbonate and ABS housings to eliminate secondary painting and capture a 12%–15% scrap-reduction benefit relative to silicone elastomers. Vietnam and Korea molders that serve Samsung and Xiaomi posted 18% year-on-year TPV volume gains in 2025, buoyed by foldable-phone hinge covers and smartwatch bands requiring high flex fatigue resistance. Premium electronics lines are migrating to renewable-content TPV, whereas cost-sensitive contracts still prefer fossil-derived grades, leaving a 25%-plus price delta. Regulatory pressure is minimal, but voluntary ISO 14001 adoption across the supply chain reinforces a recyclable-thermoplastic preference.

OEM Shift Toward Recyclable Elastomeric Materials

End-of-life (EoL) recyclability clauses have entered OEM purchasing contracts, a development that favors TPV because it can be shredded and re-pelletized without devulcanization. Stellantis requires 15% post-consumer recycled elastomers beginning with 2026 model launches, spurring Avient to commercialize Reborn TPV grades that contain up to 30% recycled content and deliver a 35% carbon-footprint drop versus virgin equivalents. Although chemical recycling could raise recovery rates, capital costs above USD 50 million for a 20 kiloton-per-year pyrolysis line remain a barrier.

Expansion of EV Battery-Pack Sealing Applications

Peroxide-cross-linked TPV grades maintain compression-set resistance under 25% after 1,000 hours at 85 °C and 85% relative humidity, meeting demanding cell-to-pack gasket standards. BYD’s Blade Battery platform uses TPV compression seals that tolerate ± 2 mm expansion differential between aluminum pack trays and steel modules. Coolant manifolds molded from weldable TPV replace multiple hose-and-clamp junctions, cutting assembly time by 30% and leakage risk by double-digit percentages. Supply chains remain taut, with peroxide and flame-retardant lead times stretching to 14-16 weeks in mid-2025.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in propylene and EPDM feedstock prices | -0.9% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Inferior long-term chemical/wear resistance vs. thermoset rubber | -0.7% | North America and Europe automotive, global industrial | Medium term (2-4 years) |

| Lack of closed-loop recycling infrastructure | -0.4% | Europe regulatory pressure, infrastructure gaps elsewhere | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Propylene and EPDM Feedstock Prices

Unplanned cracker outages and fluctuating naphtha costs lifted spot propylene to USD 1,120 per ton in April 2025 before easing later in the year, while European EPDM contracts jumped 12% quarter-over-quarter after capacity curtailments at major producers. TPV compounders normally lock downstream prices for 12-24 months, so rapid feedstock inflation compressed gross margins by up to 300 basis points. The pressure is heaviest in Asia-Pacific, where propylene derivatives account for almost 60% of TPV manufacturing cost.

Inferior Long-Term Chemical/Wear Resistance vs. Thermoset Rubber

Standard TPV grades top out at 135 °C continuous-use temperature and surrender compression-set advantage after prolonged exposure to oils at 150 °C, whereas cross-linked EPDM maintains sealing integrity to 175 °C. Turbocharger air ducts and exhaust-gas recirculation hoses, therefore, still default to thermoset solutions, limiting TPV’s under-hood penetration. DIN abrasion losses of 120-150 mm³ also trail thermoset benchmarks, constraining uptake in mining belts and industrial hoses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bio-Based Grades Accelerate Renewable Transition

Bio-based grades are projected to grow with the highest CAGR of 6.82% CAGR through 2031. Kuraray commercialized SEPTON BIO in 2024 with 80% renewable content and secured Toyota interior-trim contracts for the 2026 model year. Standard EPDM/PP compounds still dominate with 45.15% of 2025 volume because their unit costs of USD 2.80-3.20 per kg undercut renewable alternatives by as much as 30%. High-performance heat-resistant TPV wins critical under-hood hose and turbocharger duct slots, sustaining premium pricing despite more complex peroxide cross-linking. Recycled-content grades depend on feedstock access; fewer than 5% of post-consumer elastomers in North America reenter mechanical recycling streams, forcing compounders to rely on pricier post-industrial scrap.

Standard EPDM/PP grades carry a fossil-derived carbon footprint near 3 kg CO₂-equivalent per kg, exposing OEMs to tightening scope-3 emission audits under the European Corporate Sustainability Reporting Directive. Bio-based alternatives gain share in visible interior trim despite 20%-35% cost premiums because renewable-carbon disclosure provides branding value that offsets higher material expenses. High-performance peroxide-cured grades open battery-pack and turbocharged-engine doors, but reduced re-processability limits recyclability and truncates circular-economy claims. Recycled-content TPV remains capacity-constrained until shredder-residue sorting improves.

By Application: Medical Devices Pace Above-Average Growth

Sealing systems and weatherstrips locked in 41.88% of 2025 demand, illustrating TPV’s roots in automotive weatherproofing. Yet medical devices are forecast to record the highest 5.69% CAGR because single-use diagnostic cartridges, insulin-pen seals, and respiratory-therapy tubes call for gamma-sterilization stability and ISO 10993 biocompatibility, benchmarks met by Teknor Apex’s Medalist TPV series. Interior and exterior automotive trim adopt TPV overmolds to eliminate paint and cut molding cycles 20%-plus, whereas under-hood components rely on heat-stabilized TPV capable of maintaining ≥ 8 MPa tensile strength after 1,000 hours at 125 °C.

Wire-and-cable jackets benefit from halogen-free flame retardancy, and hose/tubing applications now encompass EV coolant manifolds alongside industrial pneumatic lines. Consumer and sporting goods leverage TPV for soft-touch grips but cede high-abrasion niches to thermoplastic polyurethane. Regulatory burden is clearly greatest in medical channels where FDA 21 CFR Part 820 and EU MDR 2017/745 impose rigorous validation, favoring established compounders that hold complete data packets.

By End-User Industry: Healthcare Gains Momentum

Automotive dominated with 47.24% of 2025 volume because global light-vehicle builds surpassed 85 million units and continue to integrate TPV seals to meet CO₂ milestones. Still, healthcare is on track for a 5.62% CAGR as aging demographics spur demand for home-care devices that replace silicone with TPV to improve gamma-sterilization stability. Building and construction growth lags at 4.8%-5.0% because specifiers prefer decades-proven thermoset EPDM window seals. Consumer-goods gains hover around 5% as appliance OEMs adopt TPV gaskets to comply with RoHS substance limits.

Other industrial uses, from conveyor-belt covers to photovoltaic module edge seals, create smaller but profitable micro-niches. Automotive’s scale advantage persists, yet healthcare’s regulatory premiums are reshaping margin profiles for compounders able to satisfy ISO 10993, USP Class VI, and EU MDR data requirements.

Geography Analysis

Asia-Pacific anchored 45.78% of 2025 TPV volume and is projected to grow at 6.18% through 2031. China shipped 5.5 million vehicles abroad in 2024, a 30% rise that has spurred domestic compounders such as Zhejiang Xiantong Rubber to boost TPV nameplate capacity by roughly 20% per year. India, now the world’s third-largest vehicle producer, is adopting TPV on two-wheelers and compact cars to meet rising fuel-economy targets, while Japanese and Korean suppliers Mitsui Chemicals and Kumho Polychem continue to push heat-resistant grades for Toyota, Hyundai, and Kia EV platforms.

North America accounted for significant market demand in 2025. U.S. pickup platforms remain durability-oriented, yet TPV adoption is creeping upward as Ford and General Motors integrate seals on electrified trucks to offset battery weight. Mexico’s 4.1-million-unit assembly base sources local TPV from Teknor Apex’s Matamoros site, giving regional converters supply-chain resilience. Europe’s market growth is driven by bio-based and recycled-content adoption due to EU sustainability directives. Germany, France, and Italy represent 60% of regional TPV needs as Volkswagen, Stellantis, and BMW intensify scope-3 emission audits.

South America market is centered on Brazil, where Fiat and Volkswagen apply TPV weatherstrips on compact models. The Middle East and Africa collectively register nascent growth as Saudi and UAE assembly plants import TPV parts alongside imported kits. Lack of mandatory recycled-content or EPR schemes slows the adoption of renewable or recycled grades in these regions.

Regulatory Landscape

TPV formulation and use are shaped mainly by chemicals management and application-specific requirements, with the most stringent obligations in food contact, medical, and automotive sustainability-linked procurement. In Europe, the European Chemicals Agency (ECHA) process for identifying and managing substances of concern, including PBT/vPvB pathways and authorisation-related activity lists, affects additive and monomer selection and reinforces substitution toward compliant stabilizer, flame-retardant, and processing-aid packages.

A notable 2026 anchor for TPV in regulated applications is Germanys Federal Institute for Risk Assessment (BfR) update that introduced a dedicated TPV guideline for food-contact articles under Recommendation XXI/3, effective June 1, 2026, clarifying compliance criteria for the thermoplastic phase. In the United States, TPV producers and importers also operate under TSCA obligations, where reporting cycles and rulemaking timelines can affect dossiers, data generation, and change management for new or modified chemistries used in TPV compounds.

Value Chain Analysis

The TPV value chain begins with upstream petrochemical and rubber inputs, with polypropylene and EPDM as primary feedstocks, and then moves into specialty compounding via dynamic vulcanization. After pellet distribution, conversion into end products typically happens through extrusion, injection molding, and overmolding. Value is added most consistently at the compounding and application-engineering stages, where formulation know-how, including compression set, heat aging, flame retardancy, and sterilization stability, along with qualification support, helps suppliers secure positions in automotive sealing systems and medical device components.

Operational performance is also constrained by feedstock volatility and manufacturing constraints. The market context shows propylene and EPDM price swings compressing margins for compounders holding 12-24 month pricing commitments. Specialty additives such as peroxide and flame retardants further drive lead times, with EV-oriented grades seeing 14-16 weeks of stretching in mid-2025. Downstream, just-in-time delivery requirements around automotive clusters and the need for controlled, documented material-change processes for medical customers increase the advantage of suppliers with regional production footprints and robust technical service networks.

Competitive Landscape

The Thermoplastic Vulcanizate (TPV) market is moderately consolidated. Specialists such as Teknor Apex and RTP Company invest in medical-grade and flame-retardant portfolios that demand rigorous third-party certifications, erecting qualification barriers. Chinese entrants Shandong Dawn Polymer and LCY Chemical are leveraging 15%-20% cost advantages to penetrate Southeast Asia and Latin America. Innovation centers on reactive extrusion that dynamically vulcanizes EPDM within polypropylene matrices, slashing cycle times by two-thirds and cutting energy consumption 30%-plus. Patent activity in 2024-2025 highlights halogen-free flame-retardant TPV formulations based on aluminum diethylphosphinate and melamine polyphosphate, addressing datacenter and EV-charging cable safety requirements.

Thermoplastic Vulcanizate (TPV) Industry Leaders

Celanese Corporation

Teknor Apex

Mitsui Chemicals Inc.

Avient Corporation

Kumho Polychem

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One key whitespace is electrification-driven thermal management and sealing, where TPV is displacing traditional EPDM rubber in coolant hose, battery-pack sealing, and weldable manifold architectures. In June 2026, Teknor Apex disclosed multi-year validation progress for Sarlink TPV in new energy vehicle coolant hose applications, indicating a route for TPV into high-pressure thermal management systems that must handle new coolant chemistries and tight performance windows. This fits with the report's evidence of TPV expanding from gaskets into coolant manifolds that reduce assembly steps and leakage points.

A second opportunity involves sustainability-credentialed and circular-content TPV for OEM scorecards and interior specifications, covering recycled-content and bio/circular traceability programs. Teknor Apexs May 2026 recycled-solution push for automotive interiors, alongside earlier ISCC PLUS certification activity as referenced in the evidence pack, points to demand for verifiable content claims alongside performance. Avients commercialization of recycled-content TPV grades in the market context also reflects ongoing portfolio build-out. Pricing actions further support continued value capture and cost pass-through dynamics in specialty TPV, with Celanese announcing a global Santoprene TPV price increase effective June 1, 2026, underscoring the importance of supply assurance, qualification lock-in, and differentiated grades rather than commodity substitution alone.

Recent Industry Developments

- June 2026: Teknor Apex announced multi-year validation progress for Sarlink TPV in new energy vehicle coolant hose applications, positioning TPV as an alternative to EPDM rubber in high-pressure thermal management systems. The update highlights deeper collaboration across the coolant-hose value chain, supporting faster specification wins for EV sealing and fluid-handling uses where material qualification cycles are long.

- May 2026: Teknor Apex advanced recycled-content solutions for automotive interiors, including the Crealen R series with up to 70% post-consumer recycled content and alignment to Daimler interior material specifications (DBL 1000, DBL 1224, and DBL 5307.10). The move raises the bar for recycled-content TPV/TPE offerings that must meet OEM-grade aesthetic and performance requirements, not just sustainability targets.

- November 2024: Cooper Standard launched the FlexiCore Thermoplastic Body Seal, a lightweight sealing solution using 100% TPV and polypropylene as an alternative to metal-carrier EPDM seals. The product supports vehicle lightweighting and recyclability goals while expanding the addressable set of body-seal architectures that can be redesigned around thermoplastic processing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the thermoplastic vulcanizate (TPV) market covers TPV materials sold as commercially supplied compounds. These compounds are processed like plastics but used in end-use parts where rubber-like performance is required across major industries.

Scope exclusions: We exclude downstream finished-product revenues and count only TPV material demand at the compound sales level, not the value added from part fabrication.

Segmentation Overview

- By Product Type

- Standard EPDM/PP TPV

- High-Performance / Heat-Resistant TPV

- Bio-based TPV

- Recycled-content TPV

- By Application

- Sealing Systems and Weather-strips

- Interior and Exterior Trim

- Under-the-Hood Components

- Hose and Tubing

- Wire and Cable

- Medical Devices

- Consumer and Sporting Goods Parts

- By End-User Industry

- Automotive

- Building and Construction

- Consumer Goods

- Healthcare

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Malaysia

- Thailand

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordic Countries

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- Qatar

- United Arab Emirates

- Nigeria

- Egypt

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base structure of the TPV demand pool and keep assumptions realistic before interviews started. We relied on public sources such as national statistics agencies for industrial output and vehicle production, UN Comtrade-style customs data for polymer and elastomer trade flows, and environmental agencies for updates linked to recyclability and materials compliance.

To translate those signals into a usable model, we also reviewed peer-reviewed polymer and materials journals, association publications covering plastics and elastomers, and public technical literature that describes typical TPV uses like seals, hoses, and interior trim. Company annual reports, investor presentations, and credible industry press were used to cross-check capacity additions and the direction of pricing. Where needed, we referenced paid subscriptions for company financials and intelligence, patent databases, and shipment-level import/export data to verify timelines and remove obvious outliers. These examples are not exhaustive, and additional public and paid sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with TPV compounders, distributors, converters, and end users that specify TPV in parts, especially for automotive and industrial applications. Since this is a global market, we covered APAC, EMEA, and the Americas so the model could be stress-tested against regional production footprints, application mix shifts, and expected pricing behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 16% | APAC: 52% |

| Mid tier: 45% | Functional/Unit leaders: 27% | EMEA: 29% |

| Smaller Players: 17% | Managers: 57% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs TPV demand from end-use production indicators and application-level penetration, then converts those inputs into material consumption in tons. For example, vehicle production and build mix are mapped to TPV-heavy use areas like sealing systems, hoses and tubing, and interior and exterior trim, then adjusted using regional adoption patterns that came up in interviews.

After forming the demand pool, we corroborate totals with selective bottom-up approximations to keep the outputs grounded, such as sampled supplier roll-ups, distributor channel checks, and ASP x volume checks. Pricing ranges were reviewed against multiple respondent inputs. The model uses inputs including vehicle production trends, lightweighting and substitution rates versus thermoset rubber, regional manufacturing shifts, capacity additions and utilization direction, and observed price movement tied to feedstock and compounding spreads. Where bottom-up visibility is thinner in smaller countries, we use proxy indicators such as manufacturing output and trade flows, followed by expert re-checks.

Forecasting uses scenario analysis supported by short variable-level projections agreed with interviewees, since adoption and pricing can change quickly when EV programs or materials compliance rules shift. Final outputs are expressed in volume for the headline market size, aligned to the report page figures for 2025, 2026, and 2031.

Data Validation & Update Cycle

Model outputs are validated through repeated triangulation across independent signals, and we test for year-to-year jumps that do not match production, trade, or capacity reality. When the variance is too wide, we revisit the underlying assumption and trigger targeted follow-up calls to confirm whether the gap is real or a data artifact.

Before sign-off, results go through analyst review steps that include unit consistency checks (tons and kilotons), regional share sense checks, and a final pass comparing implied consumption against known end-use activity levels. Reports are refreshed annually, and interim updates are added when material events occur, such as major capacity moves or sharp price swings. Right before delivery, a fresh review is completed so clients receive the latest updated view.

Mordor Intelligence's Thermoplastic Vulcanizate Market Estimate Compared With Other Published Estimates

Published market sizes for TPV often differ because firms use different units, different cutoffs for what counts as TPV, and different treatments for how prices progress across regions. Timing also contributes, since some estimates lock assumptions early, while others update after capacity or demand shifts become visible.

Key gaps usually come from mixing value and volume views, and from differences in whether adjacent thermoplastic elastomer families are rolled in. Currency conversion timing, the year selected for comparison, and whether recycled-content and bio-based grades are treated as part of TPV demand can all move the final number, even when the market narrative sounds similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.48 M (2025) | |

| Global Consultancy A | USD 1.62 B (2024) | Reported in value terms and anchored to a different base year, and typical value builds can include broader pricing assumptions and adjacent elastomer blends that are not strictly separated at the compound level. |

| Industry Research Group B | USD 1.90 B (2025) | Value-based sizing and a wider scope treatment where processing-method and grade definitions can broaden what is counted, which tends to inflate totals when converted back to an implied tonnage. |

The table shows a wide spread mainly because the baseline here is expressed in kilotons, and in Mordor Intelligence's model the headline size is tied to TPV compound consumption (2025: 478.22 kilotons) rather than revenue totals that depend heavily on regional ASP assumptions. When the scope is kept at material demand and cross-checked against end-use production signals, the estimate stays easier to reproduce and simpler to validate year over year.

Key Questions Answered in the Report

What is the projected TPV consumption in 2031?

Global demand is expected to reach 652.67 kilotons by 2031, reflecting a 5.32% CAGR over 2026-2031.

Which region leads TPV demand and why?

Asia-Pacific holds nearly 46% of the 2025 volume, mainly due to China’s dominance in vehicle production and aggressive EV rollout.

Why are bio-based TPV grades gaining traction?

They cut life-cycle greenhouse-gas emissions by up to 59% and help OEMs meet renewable-carbon and scope-3 targets despite a 20%-35% price premium.

What restricts TPV use in high-temperature automotive hoses?

Standard TPV continuous-use temperatures cap at 135 °C to 150 °C, below the 175 °C capability of cross-linked EPDM.

How does TPV improve EV battery-pack design?

Weldable TPV gaskets enable one-piece coolant manifolds and withstand compression-set and thermal-runaway requirements, trimming assembly time by about 30%.

What inhibits TPV circularity today?

Less than 8% of post-consumer TPV reenters mechanical recycling because automated sorting infrastructure is limited.

Page last updated on: