Petroleum Resin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.99 Billion |

| Market Size (2031) | USD 5.31 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Petroleum Resin Market Analysis by Mordor Intelligence

The Petroleum Resin Market size was valued at USD 3.77 billion in 2025 and is estimated to grow from USD 3.99 billion in 2026 to reach USD 5.31 billion by 2031, at a CAGR of 5.88% during the forecast period (2026-2031). Robust e-commerce activity keeps packaging lines running at record speeds, lifting demand for tackifiers that boost hot-melt and pressure-sensitive adhesive performance. Infrastructure investment across India, Vietnam, and Indonesia is opening long-term outlets for road-marking paints that incorporate high-softening-point C5 resins. Concurrently, adhesive formulators in North America and Europe are pivoting toward hydrogenated, low-VOC (volatile organic compounds) grades for hygiene and food-contact products, creating a premium niche that offsets margin pressure in commodity segments. Integrated producers in Asia are adding large cracker and resin units that compress regional pricing but also expand the addressable customer base for specialty grades.

Key Report Takeaways

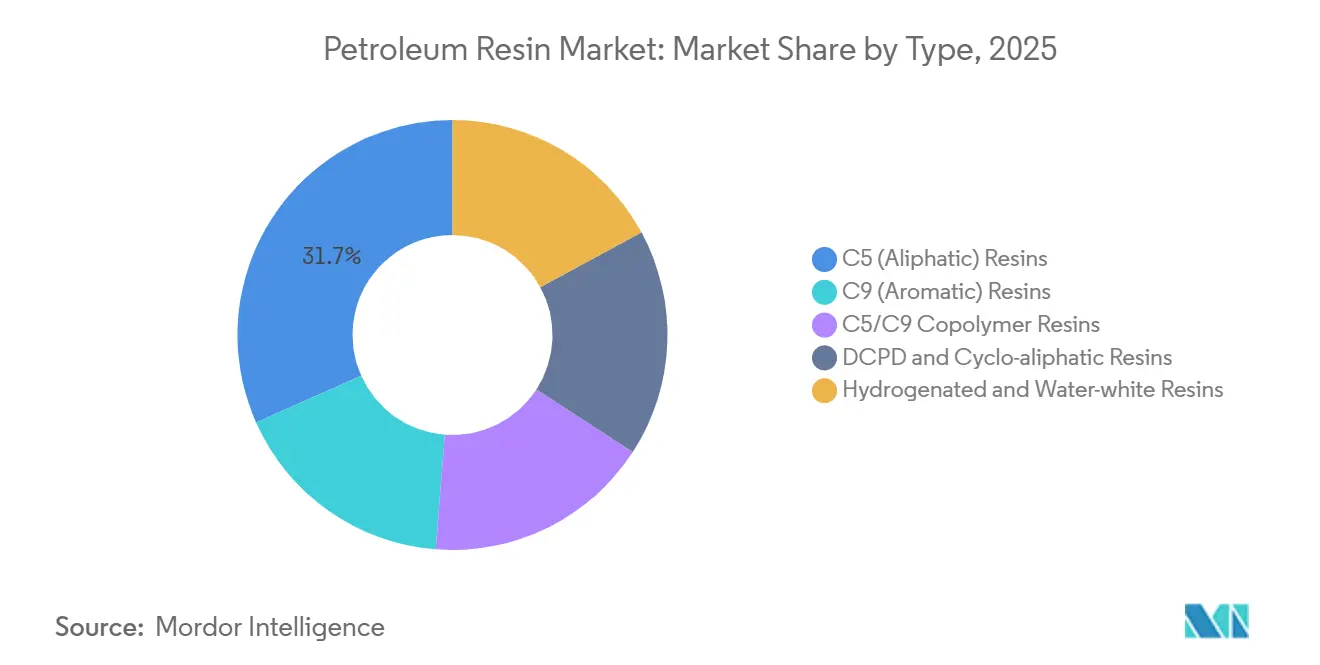

- By type, C5 (aliphatic) resins led with 31.67% revenue share in 2025; hydrogenated and water-white resins are projected to expand at a 6.63% CAGR during the forecast period (2026-2031).

- By application, hot-melt adhesives accounted for 27.72% of the Petroleum Resin market share in 2025, while printing inks and flexible packaging films are advancing at a 6.90% CAGR during the forecast period (2026-2031).

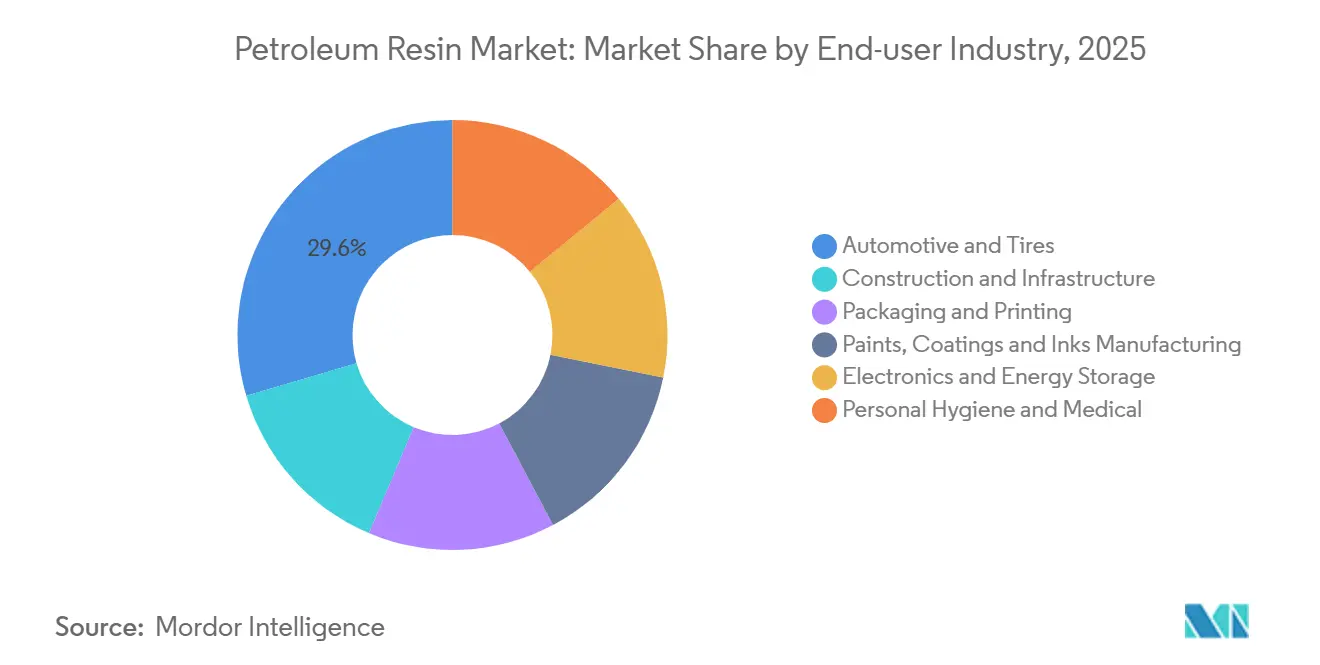

- By end-user industry, automotive and tires captured 29.56% of 2025 revenue, while electronics and energy storage are expected to record the highest projected CAGR at 6.72% during the forecast period (2026-2031).

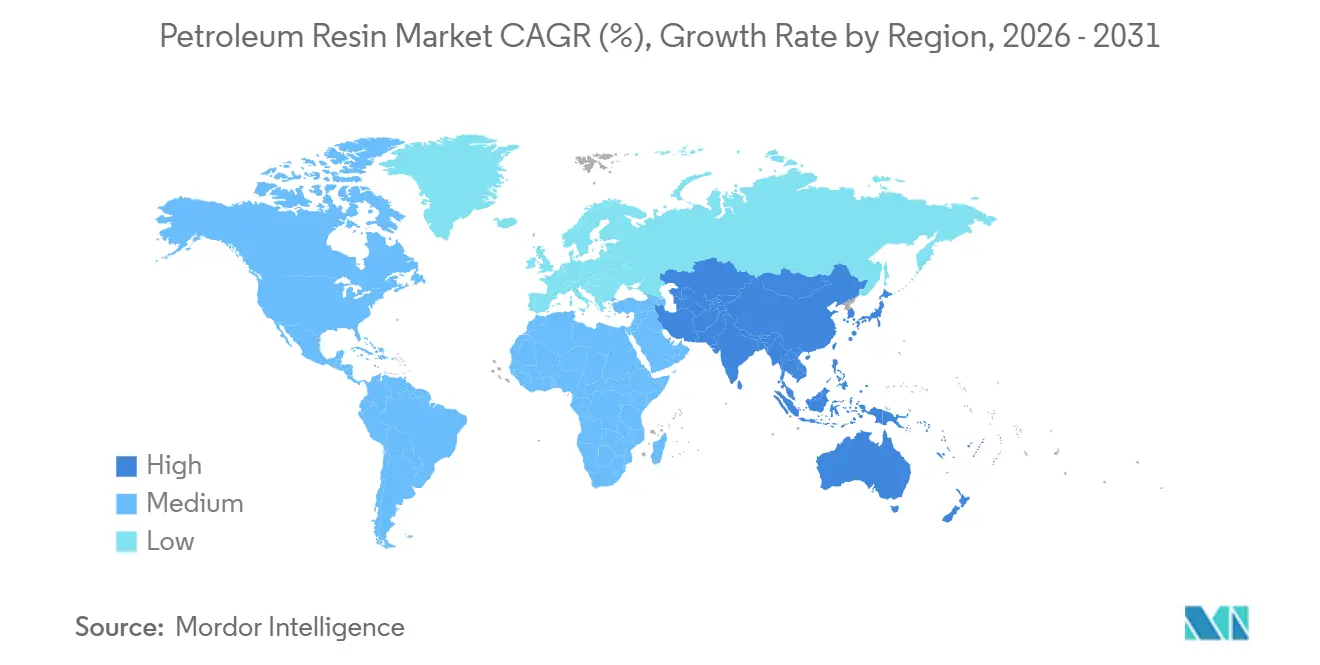

- By geography, Asia-Pacific held a 45.63% share of 2025 revenue, and this share of the region is expected to grow at a 6.88% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Petroleum Resin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-led demand for pressure-sensitive and hot-melt adhesives | +1.2% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Infrastructure build-out in South and Southeast Asia | +0.9% | India, Vietnam, Thailand, Indonesia | Medium term (2-4 years) |

| Capacity expansion by Asian producers lowering resin prices | +0.8% | China, South Korea with global ripple effects | Medium term (2-4 years) |

| Migration toward hydrogenated, low-VOC grades | +0.7% | North America, European Union, export-oriented Asia | Long term (≥ 4 years) |

| Use of petroleum-resin tackifiers in EV battery anode binders | +0.5% | China, South Korea, United States | Long term (≥ 4 years) |

| Commercialization of mixed-C5 advanced recycling | +0.3% | North America, European Union pilot sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand from Pressure-Sensitive and Hot-Melt Adhesives

Parcel volumes generated by online shopping chains, together with high-speed packaging lines that rely on hot-melt systems formulated with hydrocarbon tackifiers. Water-white hydrogenated C5/C9 copolymers maintain tack on thinner recyclable films while keeping color and odor minimal[1]Exxon Mobil Chemical, “Escorez Tackifier Resins,” exxonmobilchemical.com. Peel-strength studies on styrene-block-copolymer pressure-sensitives confirm that aromatic-rich C9 fractions raise thermal stability by nearly 50°C at common 40-60 phr loadings. As e-commerce expands globally, these performance gains outweigh raw-material price swings for converters that prize uptime and package aesthetics.

Infrastructure Boom in South and Southeast Asia

Thermoplastic road-marking paints in India, Thailand, and Vietnam use C5 resins at 10-22 wt% to ensure rapid cure and asphalt adhesion under tropical heat. Chinese supplier Guangdong Bole exports 200-ton-per-day output that meets AASHTO M249 and BS 3262 standards, illustrating cross-border scale and specification diversity. Government highway programs across ASEAN are scheduled to add thousands of lane-kilometers this decade, anchoring consistent consumption even when automotive or consumer-goods cycles soften.

Capacity Expansion by APAC Producers

China’s “oil-to-chemicals” agenda channels refinery streams into high-value polymers, and Sinopec lifted synthetic resin output 9.71% year-on-year to 22.04 million tons in 2025. Zhejiang Petrochemical’s first-phase high-performance resin complex added new LDPE/EVA, ABS, and PMMA lines in late 2025, improving regional availability of feedstocks used by downstream tackifier plants. Wider supply lowers spot prices, enabling formulators to replace more costly terpene or rosin esters in price-sensitive applications.

Shift Toward Hydrogenated, Low-VOC Grades

European Union VOC rules that entered force in mid-2026 tighten limits across adhesive classes, steering converters toward fully hydrogenated resins that eliminate residual aromatics. Rain Carbon’s NOVARES pure series offers water-white clarity and qualifies for direct skin-contact in diapers and feminine products. Hydrogenation retrofit costs add USD 2-5 million per line, yet premiums of 15-25% for food-contact grades justify the spend for suppliers targeting regulated markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-oil and naphtha feedstock costs | -1.1% | Global, most acute in Asia-Pacific | Short term (≤ 2 years) |

| Tightening VOC and odor regulations | -0.6% | North America and EU enforcement | Medium term (2-4 years) |

| Rising competition from bio-based terpene and rosin tackifiers | -0.4% | EU, North America; emerging Asia | Long term (≥ 4 years) |

| Geopolitical risk on Middle-East sea lanes | -0.3% | Import-reliant Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Oil and Naphtha Costs

Spot naphtha surged to almost USD 1,000/ton in March 2026 after shipping through the Strait of Hormuz stalled, forcing Asian crackers to throttle rates below 60% utilization[2]International Energy Agency, “Oil Market Report April 2026,” iea.org. Resin producers without upstream integration saw margins contract 5-8% as C5/C9 fractions became scarce, underscoring the advantage of feed-flex refineries that can swing to ethane or butane when needed.

Tight VOC and Odor Rules

EU directives effective mid-2026 introduced strict thresholds that many solvent-borne adhesives cannot meet without low-odor, hydrogenated tackifiers. Capital outlays for hydrogenation, and the ongoing cost of third-party certification, weigh heaviest on small regional producers, accelerating market share shift toward globally integrated resin suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hydrogenated Grades Capture Premium While C5 Resins Defend Volume

C5 aliphatic resins maintained a 31.67% hold on the petroleum resin market share in 2025, reflecting their affordability and compatibility with natural and synthetic rubber. Hydrogenated and water-white resins, though less voluminous, are registering a brisk 6.63% CAGR for the forecast period (2026-2031) as hygiene and food-contact converters prefer zero-odor profiles that meet MOAH/MOSH limits. Producers lacking hydrogenation capacity risk missing this growth corridor, particularly in Europe, where VOC legislation narrows the addressable pool for aromatic-rich C9 resins.

High-Tg DCPD resins such as LX-3100 are breaking new ground in EV tires, delivering rolling-resistance gains pivotal for extending battery range. C5/C9 copolymers remain the workhorse tackifiers for hot-melt packaging adhesives, balancing pale color with improved cohesion. Specialty cyclo-aliphatic resins carved from refinery DCPD streams occupy a premium tier thanks to thermal stability that surpasses 135°C ring-and-ball softening points, serving specialty tapes and high-temperature masking applications.

By Application: Printing Inks Outpace Hot-Melt Adhesives on Substrate Lightweighting

Hot-melt adhesives sat atop the demand pyramid with 27.72% in 2025, buoyed by corrugated-case sealing and woodworking. Yet printers chasing lighter, mono-material films are steering a projected 6.90% CAGR for ink and flexible-packaging uses that could lift this cohort to one-quarter of total consumption by 2031. Resin makers supplying this segment must tailor molecular-weight distribution that yields balanced wettability and pigment dispersion without compromising lamination bond strength.

Pressure-sensitive adhesives continue to transition toward polymer-rich constructions where tackifiers fine-tune peel and shear in diaper tabs and medical drapes. Road-marking paints, fueled by ASEAN highway builds, remain a steady volume sink for mid-softening-point C5 resins whose price advantage over terpene alternatives widens whenever crude retreats. Rubber compounding, particularly green-tire stock tack, still consumes appreciable tonnage but faces efficiency gains that cap resin loading per tire.

By End-user Industry: Electronics and Energy Storage Surge While Automotive Matures

Automotive and tires accounted for 29.56% of the 2025 offtake, but the segment now tracks plateauing global vehicle builds. Conversely, semiconductor assembly, EV battery plants, and photovoltaic module bonding underpin a 6.72% CAGR during the forecast period (2026-2031) for electronics and energy storage. The petroleum resin market size directed at these advanced manufacturing verticals is forecast to triple its 2025 base by 2031. Converters seek low-ionic-impurity tackifiers that sustain dielectric integrity and thermal cycling, rewarding suppliers with tight process control.

Construction sealants and coatings fluctuate with housing starts, yet remain critical in emerging economies where urbanization still drives cement consumption. Hygiene converters stay loyal to hydrogenated grades for odor-free performance, keeping a stable revenue stream that lends pricing power to fully certified suppliers.

Geography Analysis

Asia-Pacific commands 45.63% of the global demand and is expected to deliver the fastest 6.88% expansion pace during the forecast period (2026-2031) as mega-refinery investments in China unlock abundant C5 and C9 streams. Government-backed expressway grids in India and ASEAN create recurring bids for thermoplastic road-marking paint, anchoring a resilient end-use even when export-oriented manufacturing slows. Integrated Chinese majors use local light-ends surpluses to underprice imports, compelling overseas producers to differentiate on purity and regulatory compliance.

North America leverages the ethane cost advantage that shielded margins during the 2026 naphtha spike. Recent additions at Baytown supply performance polymers that integrate seamlessly with hydrocarbon tackifiers, driving captive downstream demand. Aggressive post-consumer plastics recycling mandates expand access to circular C5 fractions, aligning sustainability credentials with corporate carbon goals.

European growth trails the global average due to subdued industrial activity and tighter VOC ceilings that raise compliance costs. However, premium hydrogenated resins fetch attractive margins, and suppliers that meet EN 71 and REACH restrictions defend share against lower-priced imports. Middle East & Africa and Latin America remain nascent but demonstrate upside where refinery upgrades, such as the Samref conversion into a petrochemical complex, promise localized feedstock pools that shorten logistics chains.

Competitive Landscape

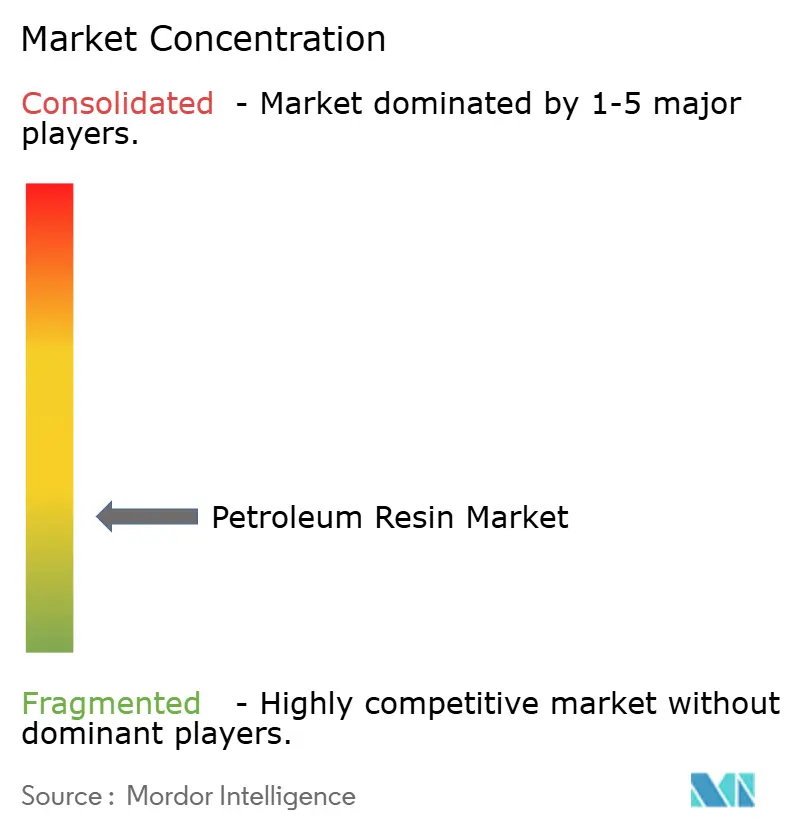

The Petroleum Resin market is fragmented. Consolidation pressure will intensify once the present capacity wave in Asia meets moderating GDP growth. Smaller, stand-alone producers lacking both hydrogenation and bio-hybrid capability may become acquisition targets or exit altogether, nudging the market toward slightly higher concentration by the end of the decade.

Petroleum Resin Industry Leaders

Exxon Mobil Corporation

Eastman Chemical Company

Kolon Industries Inc.

TotalEnergies

Idemitsu Kosan Co.,Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: In its Form 10-K for fiscal year 2025, Exxon Mobil Corporation disclosed that it tripled Proxxima resin blending capacity and plans to scale production to 200,000 tons annually by 2030. Proxxima, a polyolefin thermoset resin, is designed for applications such as construction, coatings, and transportation.

- December 2025: Exxon Mobil Corporation, Saudi Aramco, and Samref signed an agreement to upgrade the Samref refinery in Yanbu, Saudi Arabia, into an integrated petrochemical complex. The project aims to enhance high-quality distillate and chemical production, improve energy efficiency, and reduce emissions. This may result in an increase in the production of petroleum resin.

Global Petroleum Resin Market Report Scope

Petroleum resin (hydrocarbon resin) is a thermoplastic resin derived from petroleum cracking byproducts, used extensively as a tackifier, binder, and modifier in adhesives, coatings, inks, and rubber.

The Petroleum Resin market is segmented by type, application, end-user industry, and geography. By type, the market is segmented into C5 (aliphatic) resins, C9 (aromatic) resins, C5/C9 copolymer resins, dcpd and cyclo-aliphatic resins, and hydrogenated and water-white resins. By application, pressure-sensitive adhesives, hot-melt adhesives, rubber compounding and tires, road-marking paints and industrial coatings, printing inks and flexible packaging films, and EV battery binders. By end-user industry, the market is segmented into construction and infrastructure, automotive and tires, packaging and printing, paints, coatings and inks manufacturing, electronics and energy storage, and personal hygiene and medical. The report also covers the market size and forecasts for petroleum resin in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| C5 (Aliphatic) Resins |

| C9 (Aromatic) Resins |

| C5/C9 Copolymer Resins |

| DCPD and Cyclo-aliphatic Resins |

| Hydrogenated and Water-white Resins |

| Pressure-Sensitive Adhesives |

| Hot-Melt Adhesives |

| Rubber Compounding and Tires |

| Road-Marking Paints and Industrial Coatings |

| Printing Inks and Flexible Packaging Films |

| EV Battery Binders |

| Construction and Infrastructure |

| Automotive and Tires |

| Packaging and Printing |

| Paints, Coatings and Inks Manufacturing |

| Electronics and Energy Storage |

| Personal Hygiene and Medical |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | C5 (Aliphatic) Resins | |

| C9 (Aromatic) Resins | ||

| C5/C9 Copolymer Resins | ||

| DCPD and Cyclo-aliphatic Resins | ||

| Hydrogenated and Water-white Resins | ||

| By Application | Pressure-Sensitive Adhesives | |

| Hot-Melt Adhesives | ||

| Rubber Compounding and Tires | ||

| Road-Marking Paints and Industrial Coatings | ||

| Printing Inks and Flexible Packaging Films | ||

| EV Battery Binders | ||

| By End-user Industry | Construction and Infrastructure | |

| Automotive and Tires | ||

| Packaging and Printing | ||

| Paints, Coatings and Inks Manufacturing | ||

| Electronics and Energy Storage | ||

| Personal Hygiene and Medical | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the petroleum resin market in 2031?

The Petroleum Resin Market size was valued at USD 3.77 billion in 2025 and is estimated to grow from USD 3.99 billion in 2026 to reach USD 5.31 billion by 2031, at a CAGR of 5.88% during the forecast period (2026-2031).

Which region will grow the fastest through 2031?

Asia-Pacific is set to expand at a 6.88% CAGR during the forecast period (2026-2031) owing to infrastructure spending and new resin capacity.

Why are hydrogenated resins gaining popularity?

Low-VOC regulations and hygiene applications favor water-white, odor-free grades obtainable only through hydrogenation.

How are e-commerce trends influencing demand?

Higher parcel volumes require pressure-sensitive and hot-melt adhesives that rely on hydrocarbon tackifiers for fast, clean bonding.

Page last updated on: