Isoprene Rubber Latex Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

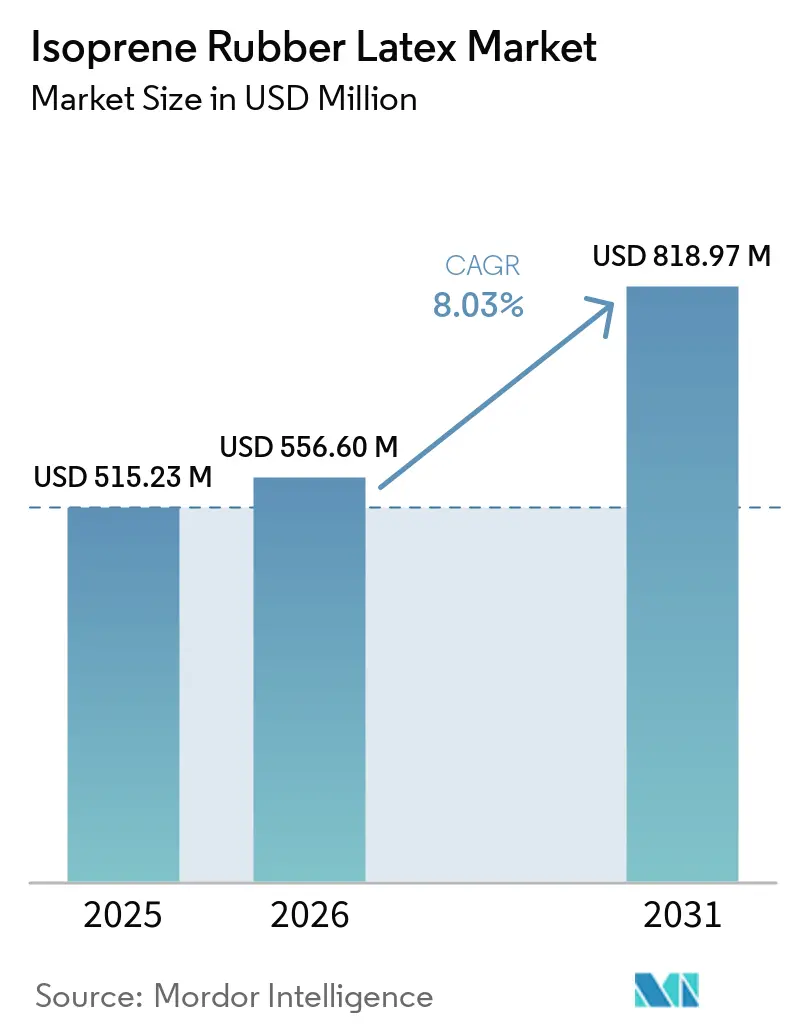

| Market Size (2026) | USD 556.60 Million |

| Market Size (2031) | USD 818.97 Million |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Isoprene Rubber Latex Market Analysis by Mordor Intelligence

The Isoprene Rubber Latex Market size was valued at USD 515.23 million in 2025 and is estimated to grow from USD 556.60 million in 2026 to reach USD 818.97 million by 2031, at a CAGR of 8.03% during the forecast period (2026-2031). Allergy concerns, the phasing out of phthalates, and the implementation of traceability rules have driven the industry's rapid shift from natural rubber to synthetic isoprene latex. This transition is prominently seen in products such as powder-free gloves, catheter balloons, and vaccine vial stoppers. The Asia-Pacific region remains at the forefront, bolstered by Malaysia's strong glove exports and China's growing rubber capacity. Prevulcanized low-solids grades, which meet ASTM D3577 tensile standards, are witnessing a surge in popularity. At the same time, advancements in bio-based isoprene research indicate a commitment to long-term sustainability. Despite challenges such as fluctuating monomer prices and steam-cracker shutdowns impacting margins, consistent demand growth is supported by regulatory endorsements, including ISO 13485:2016 and the FDA's Quality Management System Regulation (QMSR).

Key Report Takeaways

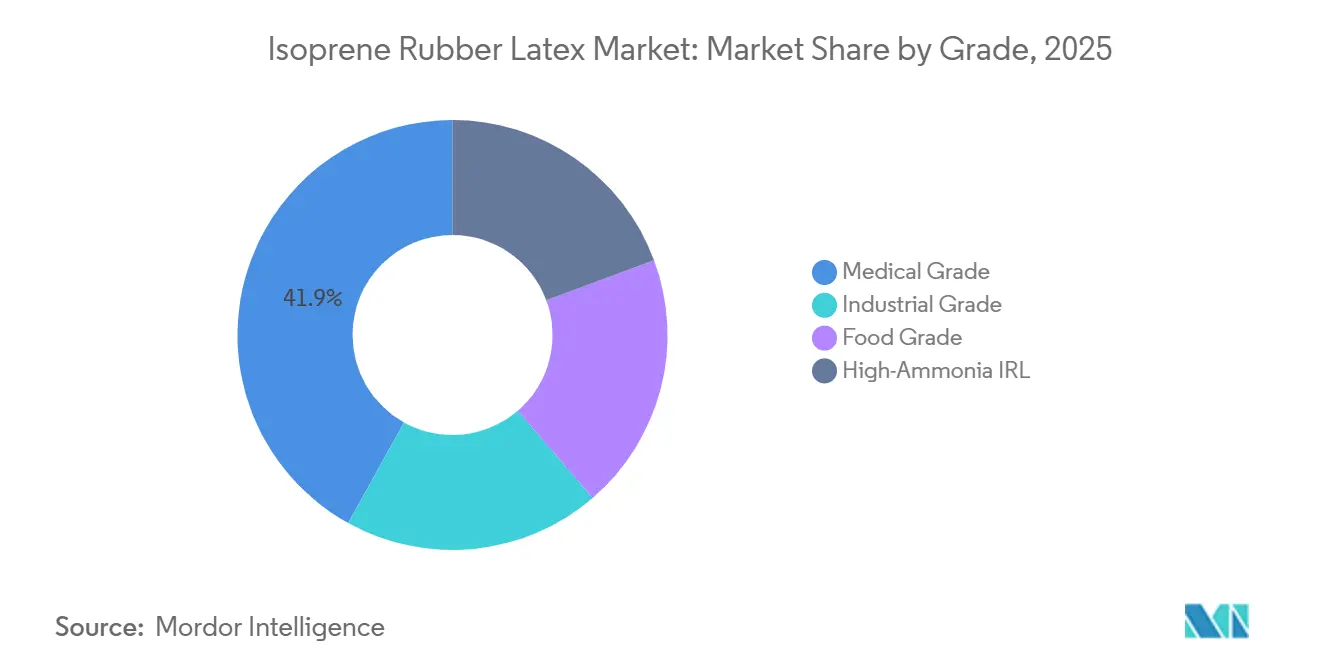

- By grade, medical grade led with 41.94% revenue share in 2025; food grade is projected to expand at an 8.52% CAGR from 2026 to 2031.

- By form, high-solids latex accounted for 63.91% of the Isoprene Rubber Latex market share in 2025; low-solids/prevulcanized latex is advancing at an 8.63% CAGR between 2026 and 2031.

- By application, medical gloves captured 27.56% of the Isoprene Rubber Latex market size in 2025; catheters and balloon devices are forecast to grow at an 8.71% CAGR between 2026 and 2031.

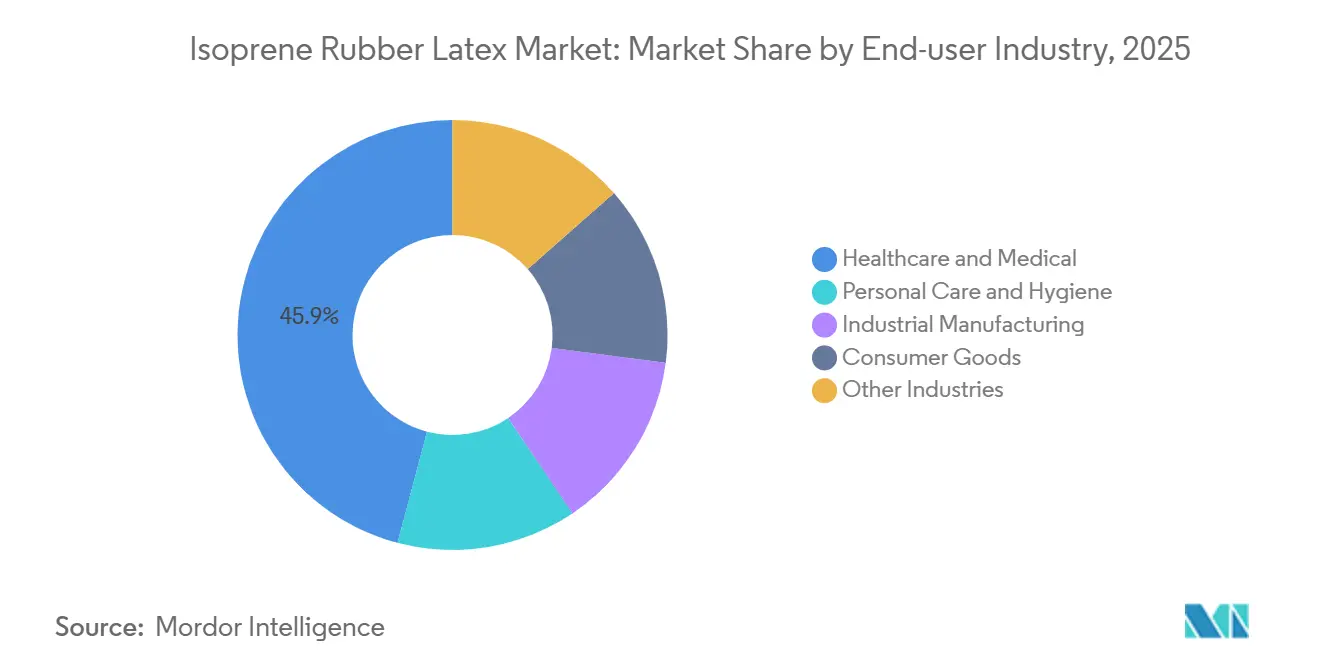

- By end-user industry, healthcare and medical commanded 45.89% share in 2025; personal care and hygiene is set to rise at an 8.51% CAGR between 2026 and 2031.

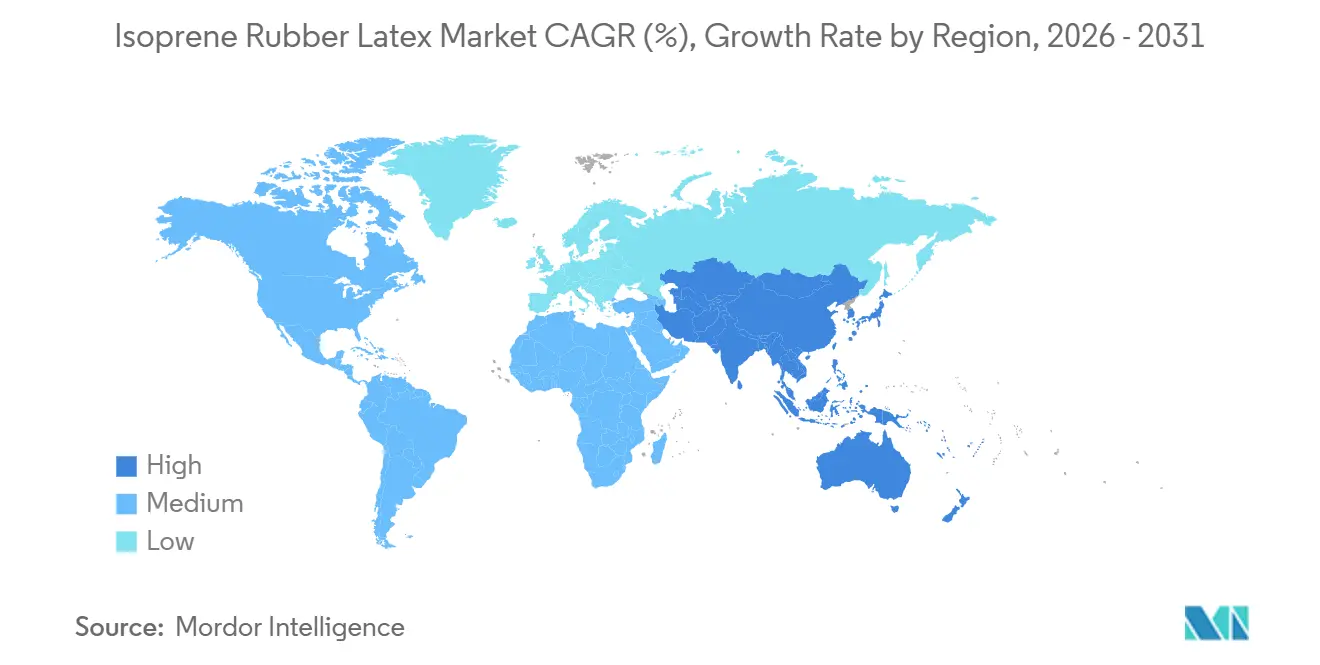

- By geography, Asia-Pacific held 53.37% of the Isoprene Rubber Latex market size in 2025; the region is projected to climb at an 8.99% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Isoprene Rubber Latex Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for powder-free medical gloves | +1.8% | Global, concentrated in Asia-Pacific glove hubs (Malaysia, Thailand, China) | Medium term (2–4 years) |

| Substitution of natural rubber latex amid allergy concerns | +1.5% | Global, with early adoption in North America and EU healthcare systems | Short term (≤2 years) |

| Growth in minimally invasive catheter and balloon procedures | +1.3% | North America, Europe, urban Asia-Pacific | Medium term (2–4 years) |

| DEHP-free device regulation favors IRL catheter balloons | +1.2% | North America (state-level), EU (Regulation 2023/2482) | Long term (≥4 years) |

| Ultra-clean IRL required for mRNA-vaccine vial stoppers | +0.9% | Global, led by North America and the EU, vaccine manufacturing corridors | Short term (≤2 years) |

| Microfluidic-chip elastomer layers needing ultra-pure IRL | +0.3% | North America, Europe, Japan (lab-on-chip R&D centers) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Powder-Free Medical Gloves

In 2017, the U.S. imposed a ban on powdered examination gloves, specifically targeting cornstarch carriers known to disseminate latex allergens. This regulatory shift prompted hospitals to pivot towards hypoallergenic synthetic alternatives. By the forecast period 2026–2031, Malaysia has emerged as a key exporter of surgical gloves, bolstering the demand for isoprene latex. Chinese manufacturer Intco Medical has increased its production capacity and streamlined labor costs, heightening the competitive landscape. Low-protein isoprene grades, containing less than 50 micrograms per gram, are now favored for their ability to reduce type I hypersensitivity, securing a premium position in hospital purchases[1]Centers for Disease Control and Prevention, “Latex Allergy: A Prevention Guide,” cdc.gov. Reflecting this trend, mandates for powder-free gloves have expanded to encompass industrial and food-service sectors, amplifying the market potential for isoprene rubber latex.

Substitution of Natural Rubber Latex Amid Allergy Concerns

Natural-latex allergies affect a significant portion of healthcare workers, prompting occupational safety organizations to classify them as a workplace hazard. The European Pharmacopeia 3.2.9 has banned natural rubber latex in pharmaceutical primary packaging, shifting the focus to synthetic isoprene closures[2]European Directorate for the Quality of Medicines & HealthCare, “European Pharmacopoeia 3.2.9,” edqm.eu. Although guayule rubber and bio-based isoprene report fewer allergy incidents, they still await large-scale validation. Hospitals across North America and Europe have adopted nitrile or synthetic isoprene gloves, with nitrile glove revenues continuing to grow. Due to their identical cis-1,4 polyisoprene backbones, synthetic grades replicate the elasticity of natural rubber. Furthermore, being free from crop-derived proteins, they ensure consistent batches suitable for Class II/III devices.

Growth in Minimally Invasive Catheter and Balloon Procedures

In recent years, U.S. cath-labs have performed a notable number of percutaneous coronary interventions (PCIs). Europe, too, has seen a significant volume of PCIs, underscoring a strong demand for elastomer balloons. Between 2025 and 2026, the FDA approved multiple drug-coated balloons, each requiring elastomer films that can endure high atmospheric pressure without leaching plasticizers. Isoprene latex, celebrated for its high compliance and fatigue resistance, has outshone polyurethane in low-profile delivery systems. In Japan and South Korea, an aging demographic is driving a rise in PAD intervention volumes. To preempt phthalate bans from California's AB 2300 and North Carolina's SB 600, device manufacturers have shifted to DEHP-free isoprene formulations.

DEHP-Free Device Regulation Favors IRL Catheter Balloons

In 2024–2025, California and North Carolina enacted bans on phthalates, while the European Union (EU) extended its DEHP sunset deadline to July 2030. In response, EU scientific committees are now requiring a benefit-risk assessment for CMR/ED phthalates. This change is prompting catheter manufacturers to shift toward plasticizer-free isoprene elastomers. Addressing challenges within the industry, BioPhorum noted that particulate contamination from stoppers has resulted in fill-finish rejections, emphasizing the need for ultra-clean isoprene grades. Additionally, the FDA's QMSR, effective February 2026, incorporates ISO 13485:2016 traceability mandates, benefiting certified synthetic-latex suppliers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost versus NRL | -1.1% | Global, most acute in price-sensitive emerging markets | Medium term (2–4 years) |

| Volatile isoprene-monomer feedstock pricing | -0.9% | Global, concentrated in regions dependent on naphtha crackers | Short term (≤2 years) |

| Steam-cracker outages are limiting polymer-grade isoprene | -0.7% | Asia-Pacific (Singapore, Taiwan), Europe | Medium term (2–4 years) |

| Cold-chain logistics limitations in emerging markets | -0.5% | South America, the Middle-East, and Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Production Cost Versus NRL

By the forecast period 2026–2031, synthetic isoprene latex prices outpace those of natural latex, fueled by the premium trading of polymer-grade monomers over crude C4/C5 streams. While natural rubber prices remain stable, the isoprene monomer market continues to grow steadily. Price-sensitive sectors, including household gloves and industrial dipped goods, still rely on natural latex. In contrast, medical and food-grade segments, benefiting from their hypoallergenic compliance, command premium prices.

Volatile Isoprene-Monomer Feedstock Pricing

ExxonMobil has halted operations at its Singapore cracker, and Formosa Petrochemical has been grappling with an indefinite outage in Taiwan since September 2025. These events have tightened the supply of butadiene. Additionally, the closures of European crackers are further constricting feedstock availability. INEOS Project ONE is introducing ethane-based ethylene, but it is producing only a limited amount of butadiene. As a result, spot prices for isoprene are experiencing quarterly fluctuations, complicating long-term contracts for latex supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Medical Compliance Anchors Premium Pricing

In 2025, medical-grade latex, adhering to FDA 21 CFR 880 standards for gloves and USP 381 standards for closures, commanded 41.94% of the revenue. The market for food-grade isoprene rubber latex, driven by condom manufacturers targeting FDA 21 CFR 177.2600 compliant formulations, is set to expand at a CAGR of 8.52% from 2026 to 2031. Industrial-grade latex finds its application in adhesives and sealants, with liquid polyisoprene grades acting as tackifiers. While high-ammonia grades, known for enhancing shelf life, face scrutiny for EU VOC compliance, there is a noticeable industry shift towards low-ammonia stabilizers. Ultra-low-protein latex, with concentrations below 50 µg/g, is tailored for Class III surgical gloves and specialized medical devices.

Pricing for medical-grade latex remains strong, supported by ISO 13485 traceability and tightening hospital regulations on natural-latex allergens. Food-grade latex is commonly used in pacifiers, baby-bottle nipples, and hypoallergenic condoms, which drives a consistent volume increase. The industrial-grade segment is witnessing growth, especially as electric-vehicle manufacturers lean towards elastomeric bonding, moving away from traditional mechanical fasteners for weight reduction.

By Form: High-Solids Dominance Meets Prevulcanized Innovation

In 2025, high-solids latex, boasting over 50% solids content, commanded 63.91% of the revenue. This high-solids content not only reduced freight costs but also enhanced mechanical stability. Meanwhile, the market share of low-solids prevulcanized latex in the isoprene rubber sector is growing at 8.63% CAGR, from 2026 to 2031. This growth is attributed to radiation-peroxide vulcanization, which has achieved tensile strengths exceeding the ASTM D3577 standard, a benchmark for surgical gloves. Additionally, advancements in room-temperature pre-vulcanization have enabled the production of thin-wall catheter films, eliminating the need for post-cure ovens.

Although high-solids variants continue to dominate, sulfur-free prevulcanized grades are gaining traction. Their appeal lies in a reduced nitrosamine risk and faster production cycles. Glove manufacturing hubs in the Asia-Pacific (Malaysia and Thailand) region are also evolving. They have started integrating hybrid manufacturing models, combining radiation crosslinking with peroxide curing. On the logistics front, players in the supply chain, particularly those proficient in shipping stabilized low-solids latex under stringent cold-chain conditions of 2 to 8 °C, are strategically positioned to capture specialized medical orders during the forecast period of 2026–2031.

By Application: Glove Volume Versus Catheter Value Intensity

In 2025, hospitals widely procured medical gloves, which accounted for 27.56% of application revenue. With rising PCI volumes and the enforcement of phthalate bans, catheters and balloon devices are projected to grow at a CAGR of 8.71% during the forecast period of 2026–2031. The market for isoprene rubber latex, commonly used in adhesives and sealants, grew at an average rate, driven by trends in automotive lightweighting and construction weatherproofing. In the Asia-Pacific region, condom adoption quickly shifted towards hypoallergenic formulations, in line with ISO 4074:2015 standards.

Although automation and reuse trends slowed glove unit growth in developed nations, a transition to ultra-low-protein latex preserved product value. Extended device dwell times and heightened inflation-pressure specifications bolstered catheter demand. Furthermore, the expansion of mRNA plants in North America and Europe is closely tied to the demand for vaccine stoppers.

By End-User Industry: Healthcare Scale Versus Personal-Care Momentum

In 2025, hospitals, adhering to FDA QMSR regulations, predominantly chose powder-free gloves, drapes, and catheters, leading the healthcare sector to command 45.89% of the revenue. Meanwhile, the personal-care sector experienced robust expansion, with a CAGR of 8.51% during the forecast period of 2026–2031. This growth is largely attributed to urban consumers' increasing willingness to invest in premium allergen-free products. In industrial manufacturing, isoprene latex is utilized in elastic threads and sealants, playing a pivotal role in vehicle weatherstripping and carpet backing. This trend aligns with forecasts anticipating a surge in vehicle assemblies by 2030, with a significant emphasis on electric models.

Specific niches within consumer goods, such as sports equipment and rubber bands, are leveraging isoprene's superior fatigue resistance. In the United States, stringent government regulations on baby-product safety, combined with emerging DEHP restrictions in Europe, have heightened the demand for hypoallergenic, plasticizer-free formulations in the personal-care sector.

Geography Analysis

Asia-Pacific, which accounted for 53.37% of the revenue in 2025, is set to reinforce its lead with a projected 8.99% CAGR during the forecast period of 2026–2031. Malaysia has played a significant role in exporting surgical gloves. China, in addition to exporting gloves, is expanding its synthetic-rubber capacity. Both Thailand and Vietnam are increasing production in response to tariff changes affecting Chinese gloves. In February 2026, ARLANXEO launched an HNBR unit in Changzhou, while Zeon's Yonezawa facility is targeting bio-isoprene commercialization by 2034. Additionally, a rising middle class in India and Indonesia is driving increased healthcare spending, highlighting the region's growth potential.

North America and Europe are set to capture a substantial share of 2025's sales. The FDA's QMSR, introduced in 2026, along with state-level bans on phthalates, is driving reforms in catheters and stoppers, leading to increased adoption of synthetic isoprene. At the same time, European steam-cracker shutdowns are limiting local feedstock availability, pushing the region towards imports and driving up latex prices. In North America, the demand for vaccine stoppers remains strong, particularly with the expansion of mRNA fill-finish lines.

South America, the Middle-East, and Africa together make up a smaller portion of the 2025 revenue. The distribution of pre-vulcanized latex, which requires storage between 2°C and 8°C, faces challenges due to cold-chain deficiencies. ARLANXEO aims to complete its Triunfo expansion by 2027 to bolster local supply in Latin America. Meanwhile, the Middle-East's abundant petrochemical feedstock contrasts with its limited downstream latex production capacity, presenting attractive joint-venture opportunities for investors in gloves and catheters.

Competitive Landscape

The isoprene rubber latex market is highly consolidated. Leading petrochemical firms have secured monomer and latex assets, bolstering their supply security. New entrants have been experimenting with fermentation-derived isoprene, aiming to reduce CO₂ emissions and alleviate allergies, although their commercial output remains limited.

Incumbents have been exploring radiation-peroxide prevulcanization technology as a pathway to producing sulfur-free, low-nitrosamine gloves, although they face the challenge of establishing capital-heavy gamma facilities. Additionally, makers of microfluidic devices have been investigating isoprene layers as substitutes for PDMS, which could unlock new markets in specialty laboratories. To gain a competitive edge, firms have been prioritizing ISO 13485 certification, ensuring their supply chains are validated and providing technical support for 510(k) submissions and EU MDR documentation. Suppliers adept at integrating upstream monomer processes with downstream application expertise are strategically positioned to handle feedstock fluctuations and navigate regulatory challenges.

Isoprene Rubber Latex Industry Leaders

Cariflex

Kuraray Co., Ltd.

Zeon Corporation

JSR Corporation

Synthomer plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: ARLANXEO announced a 25% capacity expansion at its Triunfo, Brazil, synthetic-rubber complex, slated for completion by 2027.

- May 2025: Cariflex Pte Ltd inaugurated the world's largest polyisoprene latex manufacturing facility in Singapore. With an investment of USD 355 Million, the new plant marks a significant expansion of the company's global production capacity but also aims to cater to the surging demand in the medical and protective product markets.

Global Isoprene Rubber Latex Market Report Scope

Isoprene rubber latex is a high-performance synthetic colloidal dispersion of polyisoprene polymer particles in water, designed to replicate natural rubber latex without allergenic proteins. It is characterized by superior purity, consistent curing, and excellent tensile strength, making it suitable for specialized dipping and coating applications.

The isoprene rubber latex market is segmented by grade, form, application, end-user industry, and geography. By grade, the market is segmented into medical grade, industrial grade, food grade, and high-ammonia IRL. By form, the market is segmented into personal care and hygiene and low-solids/pre-vulcanized latex. By application, the market is segmented into medical gloves, catheters and balloon devices, condoms, adhesives and sealants, elastic threads and textiles, and other applications (coatings, baby products). By end-user industry, the market is segmented into healthcare and medical, personal care and hygiene, industrial manufacturing, consumer goods, and other industries. The report also covers the market size and forecasts for the market in 19 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Medical Grade |

| Industrial Grade |

| Food Grade |

| High-Ammonia IRL |

| Personal Care and Hygiene |

| Low-Solids/Prevulcanized Latex |

| Medical Gloves |

| Catheters and Balloon Devices |

| Condoms |

| Adhesives and Sealants |

| Elastic Threads and Textiles |

| Other Applications (Coatings, Baby Products) |

| Healthcare and Medical |

| Personal Care and Hygiene |

| Industrial Manufacturing |

| Consumer Goods |

| Other Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Medical Grade | |

| Industrial Grade | ||

| Food Grade | ||

| High-Ammonia IRL | ||

| By Form | Personal Care and Hygiene | |

| Low-Solids/Prevulcanized Latex | ||

| By Application | Medical Gloves | |

| Catheters and Balloon Devices | ||

| Condoms | ||

| Adhesives and Sealants | ||

| Elastic Threads and Textiles | ||

| Other Applications (Coatings, Baby Products) | ||

| By End-user Industry | Healthcare and Medical | |

| Personal Care and Hygiene | ||

| Industrial Manufacturing | ||

| Consumer Goods | ||

| Other Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Which region contributes the most revenue?

Asia-Pacific held 53.37% of 2025 revenue and is expanding at an 8.99% CAGR from 2026 to 2031 on the back of Malaysia’s and China’s capacity additions.

How are phthalate bans influencing catheter materials?

State-level and EU DEHP restrictions are steering catheter balloons toward plasticizer-free synthetic isoprene formulations that meet flexibility targets without leaching.

What is the outlook for bio-based isoprene?

Fermentation routes promise CO₂ savings but are unlikely to achieve commercial scale before the mid-2030s, limiting near-term impact on Isoprene rubber latex supply.

What is the forecast CAGR for Isoprene Rubber Latex between 2026 and 2031?

The market is forecast to rise from USD 556.60 million in 2026 to USD 818.97 million by 2031, reflecting a 8.03% CAGR.

Page last updated on: