Robot Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

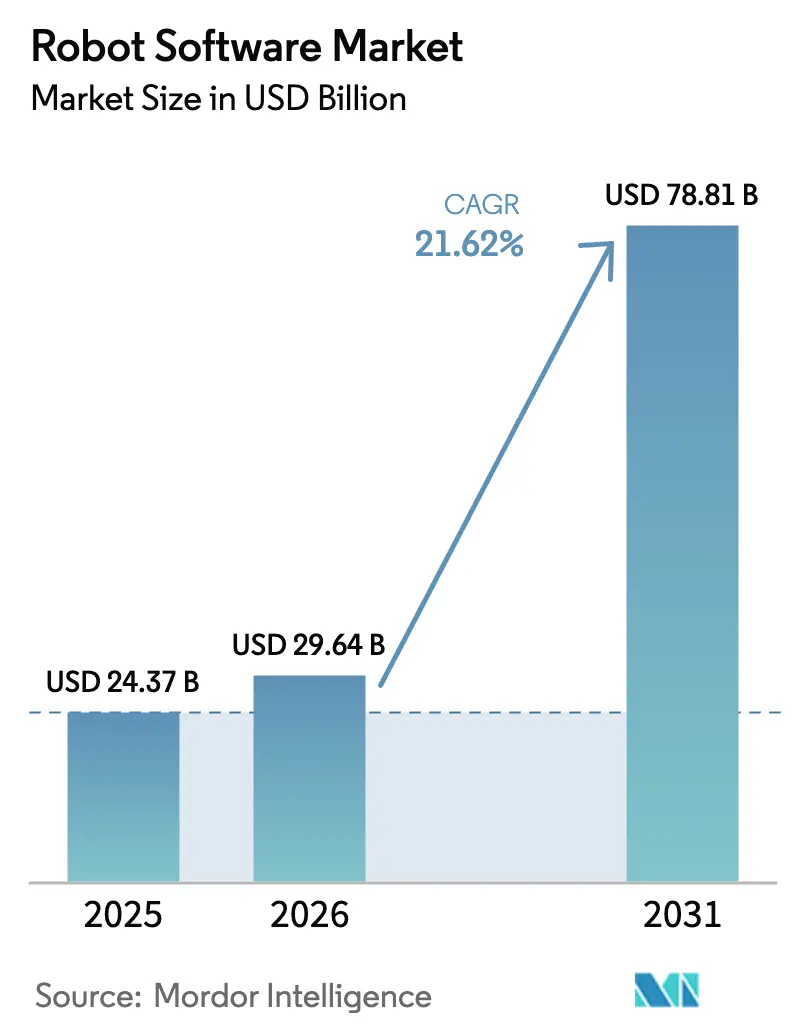

| Market Size (2026) | USD 29.64 Billion |

| Market Size (2031) | USD 78.81 Billion |

| Growth Rate (2026 - 2031) | 21.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robot Software Market Analysis by Mordor Intelligence

The robot software market size is projected to expand from USD 24.37 billion in 2025 to USD 29.64 billion in 2026 and is forecast to reach USD 78.81 billion by 2031, reflecting a 21.62% CAGR, underscoring the momentum behind intelligent automation across factories, hospitals, and warehouses. The transition from proprietary control stacks to open-architecture platforms such as ROS 2 is lowering switching costs, while Robot-as-a-Service contracts convert capital outlays into operating expenses, expanding access for small and medium enterprises. Regulatory tailwinds, notably the European Union Machinery Regulation that mandates virtual safety validation by 2027, are accelerating software demand because compliance now hinges on digital twins and deterministic real-time scheduling. Meanwhile, semiconductor advances exemplified by NVIDIA Jetson Thor are pushing AI inference to the edge, shrinking latency in safety-critical tasks. Venture funding, cloud hyperscaler toolkits, and heightened cybersecurity requirements are collectively reinforcing the value that software adds to physical robots.

Key Report Takeaways

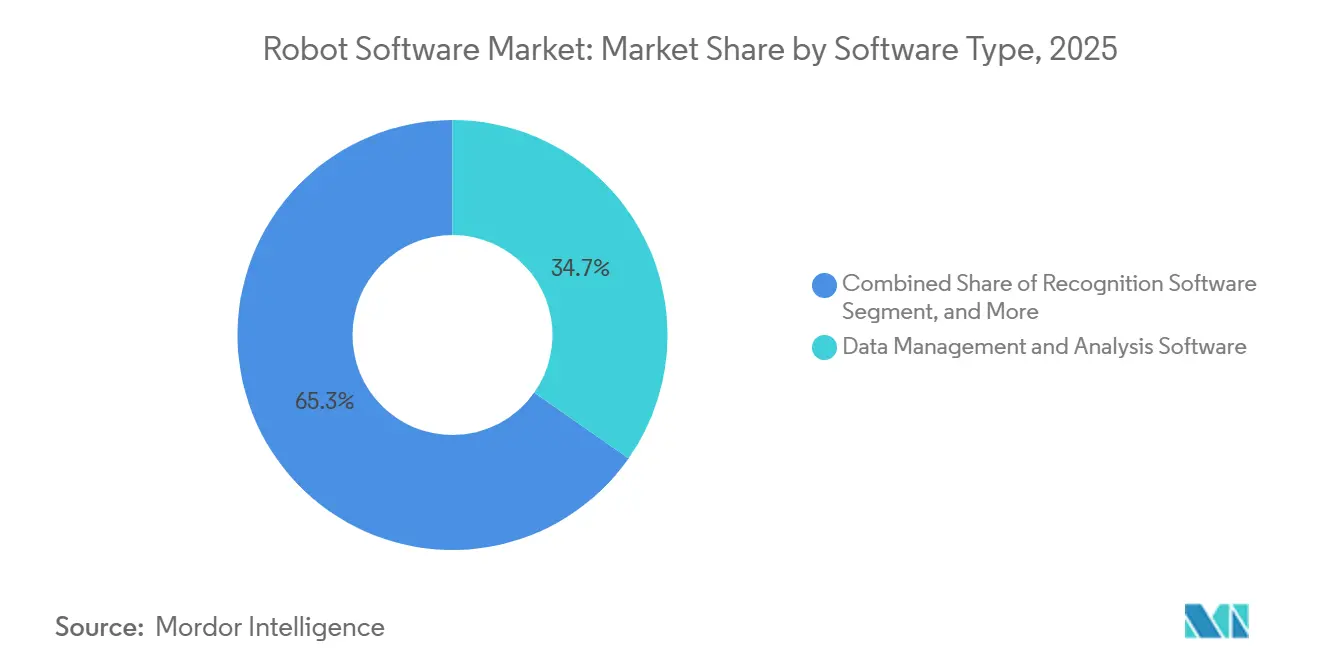

- By software type, data management and analysis led with 34.74% revenue share in 2025, and communication management is projected to expand at a 21.98% CAGR through 2031.

- By robot type, industrial robots accounted for 57.63% of the 2025 base, and service robots are on track for a 23.1% CAGR out to 2031.

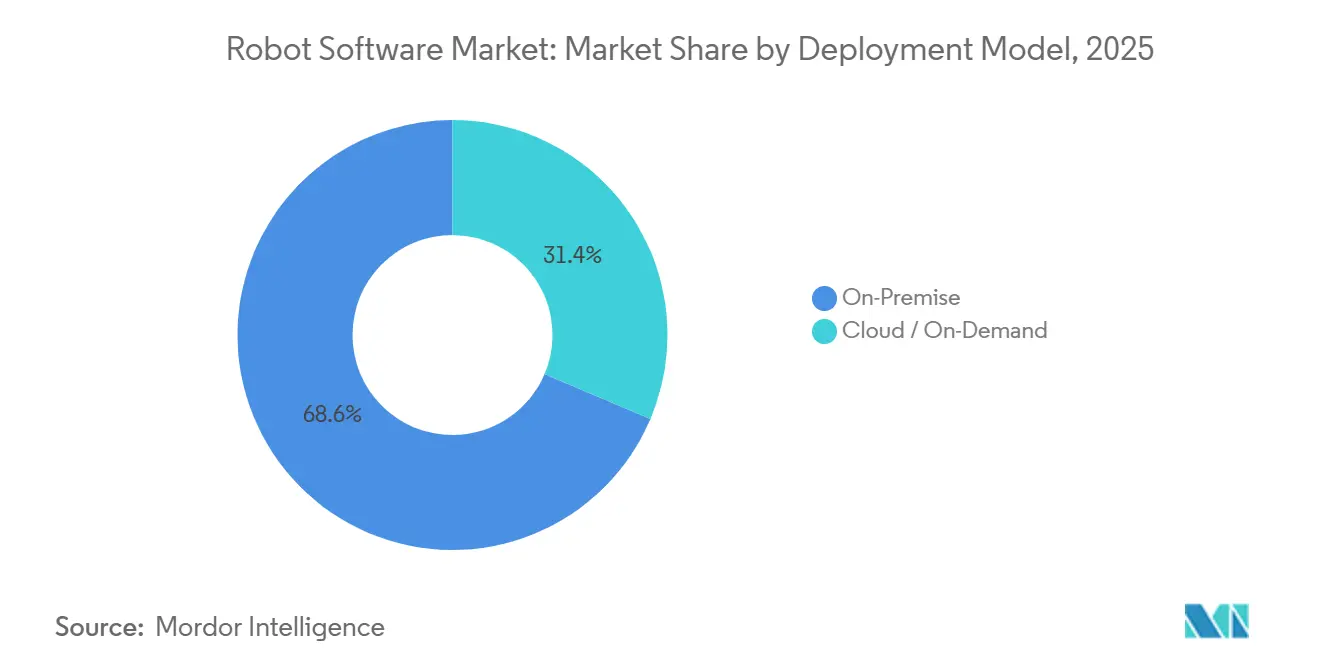

- By deployment model, on-premise installations held 68.62% in 2025, while cloud and on-demand architectures are set to grow at 22.98% through 2031.

- By end-user vertical, manufacturing captured 29.83% in 2025, and healthcare is positioned for a 21.54% CAGR into 2031.

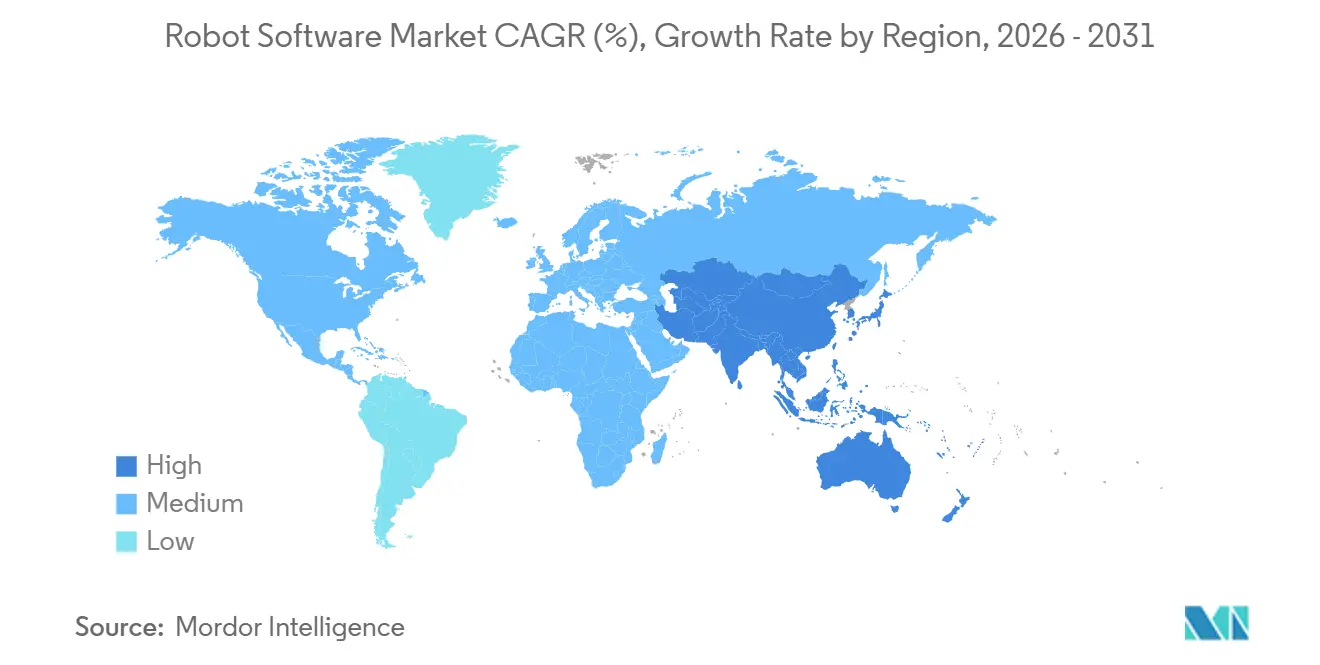

- By geography, North America represented 38.73% revenue in 2025, and Asia-Pacific is forecast to advance at a 22.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Robot Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising need for automation and safety | +4.2% | Global, with concentration in North America, Europe, and Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Rapid SME adoption to cut labor and energy costs | +3.8% | Global, strongest in Asia-Pacific and Europe where labor arbitrage is narrowing | Short term (≤ 2 years) |

| AI and ML integration boosts robot capability | +5.1% | Global, led by North America and China for AI infrastructure investment | Medium term (2-4 years) |

| Low-code and no-code robot-app platforms expand adoption | +3.3% | Global, particularly in SME-dense regions such as Europe and ASEAN | Short term (≤ 2 years) |

| EU safety-driven ROS virtualization mandate (2027) | +2.4% | Europe, with spillover to North America and Asia-Pacific exporters to EU | Medium term (2-4 years) |

| Robot-as-a-Service subscription economics | +4.6% | Global, with early traction in North America and Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI and ML Integration Boosts Robot Capability

Vision language action models now fuse perception and control, allowing robots to follow natural commands and adapt to unseen objects without retraining. The Jetson Thor module provides 2,000 TOPS of on-device compute, enabling humanoid robots to run multimodal models locally and prevent the 100 ms delays that jeopardize surgical precision.[1]NVIDIA Corporation, “NVIDIA Jetson Thor: The Brain for Humanoid Robots,” nvidia.com Intel RealSense SDK added depth-aware segmentation that lets collaborative robots differentiate a human hand from a workpiece, meeting ISO 10218-2 power-and-force thresholds.[2]Intel Corporation, “Intel RealSense SDK 2025 Update: Depth-Aware Object Segmentation,” intel.com Manufacturers benefit because fewer labeled images are required, reducing dataset creation costs. The outcome is faster deployment of flexible cells that can switch product variants within an hour.

Rising Need for Automation and Safety

Aging workforces and low labor participation are structural realities, with Japan reporting a 370,000 manufacturing worker gap in 2025. The updated ISO 10218-1 sets torque and force limits that permit humans and robots to share spaces without cages, thereby increasing software complexity for real-time collision monitoring. UL 3300, the first dedicated safety standard for autonomous mobile robots, mandates redundant braking and lidar-based obstacle detection with a resolution of 0.1 m.[3]UL Solutions, “UL 3300: Standard for Safety of Autonomous Mobile Robots,” ul.com Vendors that embed certified diagnostics and audit logging win share as risk-averse buyers aim to avoid recall costs. Smaller developers lacking compliance budgets are pivoting to platform partners for pre-validated stacks.

Robot-as-a-Service Subscription Economics

Locus Robotics disclosed average monthly fees of USD 3,500 per picking robot in 2025, which now bundle hardware, software, and maintenance. Formic Technologies’ filings show contract terms stretching to 4.2 years, indicating that customers are reluctant to revert once operational. This subscription framing reduces payback anxieties and improves cash flow because payments scale with usage. Vendors update firmware over the air, shortening iteration cycles from quarters to days and ensuring fleets remain security patched. Penetration correlates strongly with reliable broadband, so coverage remains thin in regions where industrial connectivity is sporadic.

EU Safety-Driven ROS Virtualization Mandate (2027)

The EU Machinery Regulation obliges every collaborative robot shipped into the bloc after 2027 to undergo virtual safety validation. ROS 2 adds deterministic scheduling and signed executables, features that simplify auditor sign-off. Gazebo integrated ISO 13849 templates to auto-generate emergency-stop test cases and prove response times below 250 ms. Compliance costs squeeze smaller vendors, prompting acquisitions by larger automation firms that can more easily amortize certification overhead. Exporters to the European market are adopting identical processes, effectively globalizing the mandate.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation cost | -3.9% | Global, most acute in price-sensitive SME segments across Asia-Pacific and South America | Short term (≤ 2 years) |

| Cyber-security and malware threats | -2.7% | Global, with elevated risk in North America and Europe due to higher connectivity rates | Medium term (2-4 years) |

| Shortage of safety-certified software engineers | -1.8% | Global, particularly acute in Europe and North America where certification backlogs exceed 18 months | Long term (≥ 4 years) |

| Vendor lock-in from proprietary OS stacks | -1.4% | Global, most pronounced in legacy industrial automation markets with high installed bases | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation Cost

Total ownership often exceeds USD 200,000 per cell once sensors, networks, and integration are counted, which 58% of manufacturers cited as the biggest hurdle in a 2025 survey. Thin-margin SMEs struggle to amortize expenses because they lack scale. Low-code tools shorten programming cycles, yet hardware and sensor bills are largely inelastic. Finance providers demand creditworthy counterparties, limiting leasing uptake in emerging markets. As interest rates trend higher, cash-flow-sensitive firms delay projects unless subsidies or tax credits offset upfront costs.

Cyber-Security and Malware Threats

Dragos recorded a 30% annual rise in malware campaigns targeting robot controllers during 2024, including ransomware that froze 400 mobile robots at a European automotive supplier for 72 hours. The EU Cyber Resilience Act now requires a software bill of materials and 14-day patch windows, yet only a minority of vendors have automated patch pipelines. Runtime anomaly detection from Claroty or Nozomi baselines motion signatures and flags deviations, but adoption lags due to integration effort. Insurance exclusions for unsegmented networks introduce financial risk, prompting buyers to opt for platforms with built-in security analytics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software Type: Data Orchestration Anchors Largest Share

Data management and analysis software held 34.74% of the 2025 base, demonstrating that users value fleet-wide telemetry aggregation for uptime and energy insights. This slice equated to roughly USD 10.3 billion of the robot software market size in 2025. Predictive maintenance algorithms reading vibration and current signatures now forecast bearing failures weeks ahead, letting procurement plan parts without expedite premiums. Standardized interfaces, such as OPC UA, simplify data extraction from mixed fleets, while transformer models detect anomaly patterns that were previously hidden in high-frequency time series. Communication management is expanding at a 21.98% CAGR because heterogeneous fleets dominate logistics centers where AMRs from several makers negotiate right of way in real time. VDA 5050, released in 2024, underpins this surge by defining a common message taxonomy. Recognition software is converging with transformer vision, enabling robots to achieve human-level detection accuracy. Simulation tools incorporate ISO safety templates, which shorten virtual commissioning. Edge inference is now compulsory in uptime-critical factories because cloud round trips breach deterministic budgets.

Product strategies are coalescing into platform bundles that merge orchestration, recognition, and predictive analytics. Vendors price these suites on a per-robot per-month basis, mirroring SaaS norms. Stand-alone point applications risk marginalization unless they integrate via open APIs. As competitive intensity rises, mergers focus on uniting simulation assets with runtime engines to control the full software lifecycle. The robot software market continues to reward products that convert raw sensor logs into actionable dashboards for line supervisors who lack data-science backgrounds.

By Robot Type: Service Robots Outpace Industrial Growth

Industrial robots owned 57.63% of deployments in 2025, equal to around USD 17.1 billion of robot software market size at that time. The share reflects deep entrenchment in automotive welding, painting, and battery pack assembly. Yet service robots are expanding at 23.1% annually, propelled by healthcare logistics, hospitality, and retail scanning. Intuitive Surgical’s da Vinci platform performed more than two million procedures in 2024, validating clinical acceptance of machine assistance. Service robots must navigate unstructured spaces, interpret social cues, and comply with GDPR. Boston Dynamics’ Spot quadruped now runs autonomous inspection in chemical plants via lidar and stereo fusion, highlighting how perception stacks migrate from labs to hazardous field sites.

Industrial units increasingly feature force-torque sensing, enabling safe human collaboration without cages. Modular designs decouple motion libraries from task logic so engineers swap end effectors without rewriting core code. Service platforms integrate cloud-based language models to enable voice commands at hotel counters. Cross-pollination is evident as Universal Robots ports its URScript environment to mobile bases, allowing integrators to blend manipulation and navigation within a single IDE. The robot software market benefits because each added use case translates into incremental license or subscription revenue rather than one-off sales.

By Deployment Model: Cloud Gains Despite On-Premise Dominance

On-premise installations accounted for 68.62% in 2025, as automotive and aerospace manufacturers demand ultra-low latency for 1-kHz control loops. That slice equated to about USD 20.3 billion of the robot software market size. Cloud and on-demand architectures are rising at 22.98% as developers push training, simulation, and fleet analytics to hyperscale data centers. AWS RoboMaker can now simulate 10,000 robot hours in parallel, significantly reducing validation timelines and costs. Microsoft Azure pairs managed Kubernetes with ROS 2 containers to streamline deployment. Logistics and retail favor cloud because centralized coordination boosts routing efficiency across multiple warehouses. Hybrid edge-cloud topologies prevail, with inference at the edge and model updates synchronized overnight. Cybersecurity rules drive cloud adoption since over-the-air patching is simpler when robots remain continuously online, but the expanded attack surface demands zero-trust segmentation.

On-premise solutions remain relevant in high-IP environments where data sovereignty and air-gapping mitigate espionage risks. Edge gateways bridge real-time control to cloud dashboards through encrypted, rate-limited channels. Vendors bundle service level agreements that guarantee latency budgets, further easing buyer concerns. As 5G private networks mature, bandwidth constraints ease, allowing high resolution vision streams to reach cloud AI services in near real time. The robot software market therefore shows a gradual but clear shift toward hybrid and cloud-first deployments.

By End-User Vertical: Healthcare Accelerates Amid Manufacturing Maturity

Manufacturing accounted for 29.83% in 2025, equivalent to USD 8.9 billion of the robot software market, while healthcare is expected to compound at 21.54% through 2031. Automotive maintains leadership in manufacturing because electric vehicle battery assembly requires sub-0.1 mm-tolerance vision-guided guidance. Electronics plants leverage inspection robots to spot micro-cracks before costly rework. Healthcare’s acceleration stems from FDA clearances for AI-guided surgical suites and reimbursement codes that now cover laparoscopic robotics. CMR Surgical’s Versius gained CE marking in 2024 and boasts a modular footprint that reduces capital outlay for hospitals with constrained theater space. Logistics adds momentum as e-commerce warehouses deploy AMRs that cut pick cycle times by 40%.

Retail chains pilot shelf-scanning and floor-cleaning robots powered by BrainOS, capturing real-time inventory data. Aerospace uses crawler robots for fuel tank inspection, thereby lowering human entry risks. Government agencies run perimeter patrol units that integrate thermal cameras and loudspeakers. Each vertical requires domain-specific compliance, from HIPAA in healthcare to ITAR in defense, complicating sales cycles. Vendors that package vertical templates in their SDKs ease adoption and command premium pricing.

Geography Analysis

North America held 38.73% revenue in 2025, buoyed by early automotive and semiconductor adoption plus a deep robotics talent pool anchored by MIT and Carnegie Mellon. The United States supplies the bulk of demand, with Mexico’s nearshoring boom pulling in high-mix automation projects. Canada leverages AI research clusters to commercialize reinforcement learning that optimizes robot policy updates.

Asia-Pacific is the fastest climber with a 22.44% CAGR through 2031, propelled by China’s plan to deploy 1 million humanoid robots by 2030 and India’s subsidies covering up to 25% of capex for factory automation. Japan combats demographic headwinds with service robots in eldercare, while South Korea intersects automotive heritage with Boston Dynamics mobility know-how. ASEAN nations such as Vietnam attract electronics relocations, nudging small batch manufacturers toward cloud orchestration to compensate for labor gaps.

Europe’s trajectory is shaped by safety and cybersecurity regulations that mandate virtual validation and prompt patching, thereby advantaging vendors with compliance expertise. Germany’s automotive and machinery sectors still dominate installations, but Italy’s SME-focused schemes favor low-code cobots. The United Kingdom and France channel public funds into simulation and AI labs that inform next-generation perception stacks. South America remains emergent, with Brazilian car plants piloting collaborative welding cells. The Middle East leans on logistics hubs in the United Arab Emirates that run AMR fleets in ports and free zones. Africa sees early pilots in mining and agro-processing, though bandwidth and capital bottlenecks slow scaling. Across regions, public incentives, broadband coverage, and security regimes shape uptake and vendor entry strategies.

Competitive Landscape

The robot software market is fragmented because simulation experts, vision providers, fleet managers, and cloud hyperscalers each own slivers of the stack, resulting in no firm controlling more than 8% of global revenue. ABB and FANUC extend proprietary controllers with REST and gRPC APIs so customers integrate modern analytics without abandoning installed machinery. Pure-play newcomers such as Clearpath Robotics and Brain Corporation wrap low-code IDEs around ROS 2, enabling technicians to reconfigure workflows without C++ proficiency.

Robot-as-a-Service shifts revenue toward recurring subscriptions, favoring balance-sheet-strong incumbents that can finance hardware. NVIDIA’s multi-agent reinforcement learning patents hint at coordination algorithms for heterogeneous fleets, a potential moat. The scarcity of TÜV-certified software engineers, with 18-month backlog queues, raises entry barriers and tilts share toward firms with in-house compliance teams. Interoperability standards from IEEE and ISO will commoditize basic motion control, pushing differentiation to cognition, perception, and collaborative intelligence. White-space remains in construction, agriculture, and hospitality where software must parse unstructured settings. M&A accelerates as vendors chase end-to-end platform breadth.

Robot Software Industry Leaders

ABB Ltd.

Clearpath Robotics

NVIDIA Corporation

CloudMinds Technology, Inc.

Liquid Robotics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: NVIDIA launched Isaac Manipulator, a pretrained model that trims robot arm programming time by 70%, with native ROS 2 hooks.

- September 2025: ABB pledged USD 150 million for a Västerås software center targeting predictive maintenance and digital twins.

- August 2025: Universal Robots partnered with Microsoft to embed Azure AI into UR+ so cobots interpret spoken commands.

- July 2025: AWS introduced RoboMaker Fleet Management for real-time AMR orchestration across multi-site warehouse.

Global Robot Software Market Report Scope

Robot software is a set of coded commands or instructions that tell a mechanical device and electronic system, known as a robot, what tasks to perform. Robot software is used to perform autonomous tasks with the use of technologies like Artificial Intelligence. Robot software enables functions for enhanced intelligence, motion, safety, and productivity and gives the power to make the robots see, feel, learn, and maintain safety.

The Robot Software Market Report is Segmented by Software Type (Recognition, Simulation, Predictive Maintenance, Data Management and Analysis, Communication Management), Robot Type (Industrial, Service), Deployment Model (On-Premise, Cloud and On-Demand), End-user Vertical (Automotive, Manufacturing, Healthcare, Transportation and Logistics, Retail and E-commerce, IT and Telecommunications, Government and Defense, BFSI, Aerospace and Defense, Media and Entertainment, Other End-user Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Recognition Software |

| Simulation Software |

| Predictive Maintenance Software |

| Data Management and Analysis Software |

| Communication Management Software |

| Industrial Robots |

| Service Robots |

| On-Premise |

| Cloud / On-Demand |

| Automotive |

| Manufacturing |

| Healthcare |

| Transportation and Logistics |

| Retail and E-commerce |

| IT and Telecommunications |

| Government and Defense |

| BFSI |

| Aerospace and Defense |

| Media and Entertainment |

| Other End-user Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Software Type | Recognition Software | ||

| Simulation Software | |||

| Predictive Maintenance Software | |||

| Data Management and Analysis Software | |||

| Communication Management Software | |||

| By Robot Type | Industrial Robots | ||

| Service Robots | |||

| By Deployment Model | On-Premise | ||

| Cloud / On-Demand | |||

| By End-user Vertical | Automotive | ||

| Manufacturing | |||

| Healthcare | |||

| Transportation and Logistics | |||

| Retail and E-commerce | |||

| IT and Telecommunications | |||

| Government and Defense | |||

| BFSI | |||

| Aerospace and Defense | |||

| Media and Entertainment | |||

| Other End-user Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of global robot software revenue by 2031?

Revenue is forecast to reach USD 78.81 billion in 2031, up from USD 29.64 billion in 2026.

Which geographic region is expected to record the fastest growth through 2031?

Asia-Pacific is projected to advance at a 22.44% compound annual rate, the quickest worldwide.

How fast are service robot software deployments growing compared with industrial ones?

Service-focused deployments are expected to expand at 23.1% annually, outpacing industrial growth.

Why are small and medium enterprises turning to Robot-as-a-Service contracts?

Subscription pricing converts large capital outlays into manageable monthly fees that include maintenance and software updates.

What regulation is driving virtual safety validation requirements in Europe after 2027?

The European Union Machinery Regulation mandates that collaborative systems pass virtual safety tests before shipment.

Page last updated on: