Piece Picking Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.58 Billion |

| Market Size (2031) | USD 20.78 Billion |

| Growth Rate (2026 - 2031) | 51.78% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Piece Picking Robots Market Analysis by Mordor Intelligence

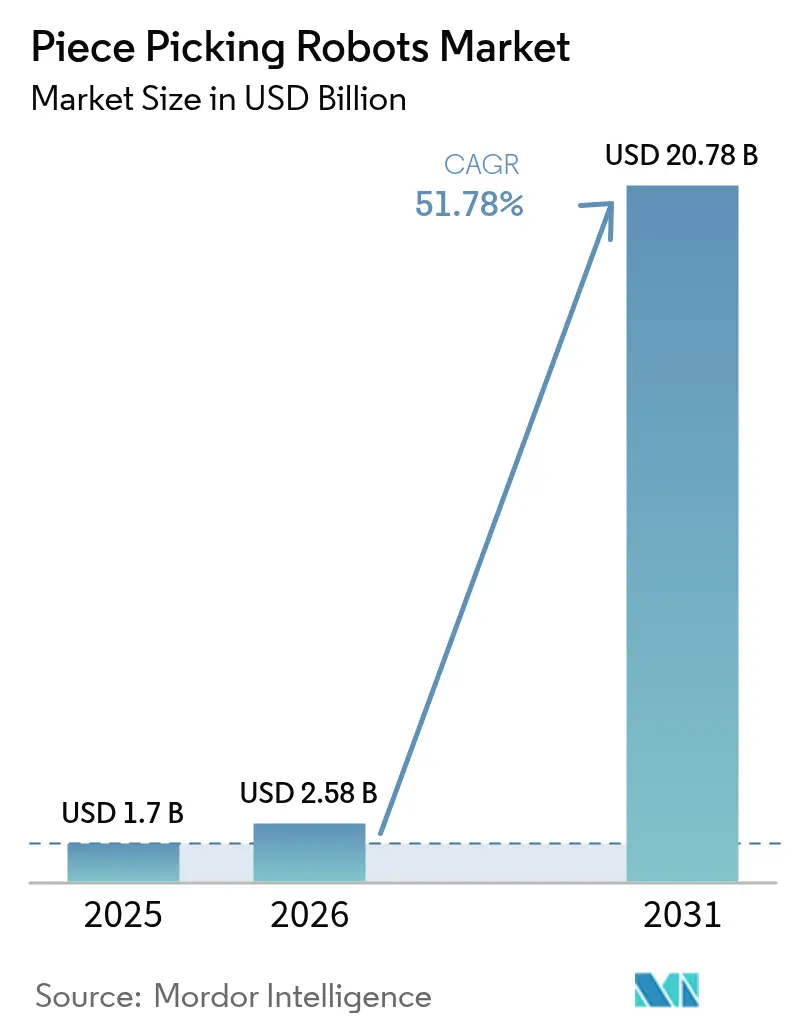

The piece-picking robots market size is expected to grow from USD 1.7 billion in 2025 to USD 2.58 billion in 2026 and is forecast to reach USD 20.78 billion by 2031 at 51.78% CAGR over 2026-2031. Rapid scalability arises from persistent labor shortages, e-commerce parcel growth, and artificial-intelligence breakthroughs that push robotic picking accuracy above 95%. The pace outstrips traditional warehouse automation because manual picking still absorbs up to 60% of fulfillment costs, prompting operators to automate the most labor-intensive workflows. Robots-as-a-Service (RaaS) models lower upfront capital while subscription pricing aligns expenses with seasonal volumes. North America leads adoption, yet Asia-Pacific records the steepest CAGR as aging workforces and wage inflation heighten automation urgency. Competitive positioning now depends less on hardware and more on software that refines grasp planning in real time, underpinning a swift shift toward intelligent, mobile systems that collaborate safely with people.

Key Report Takeaways

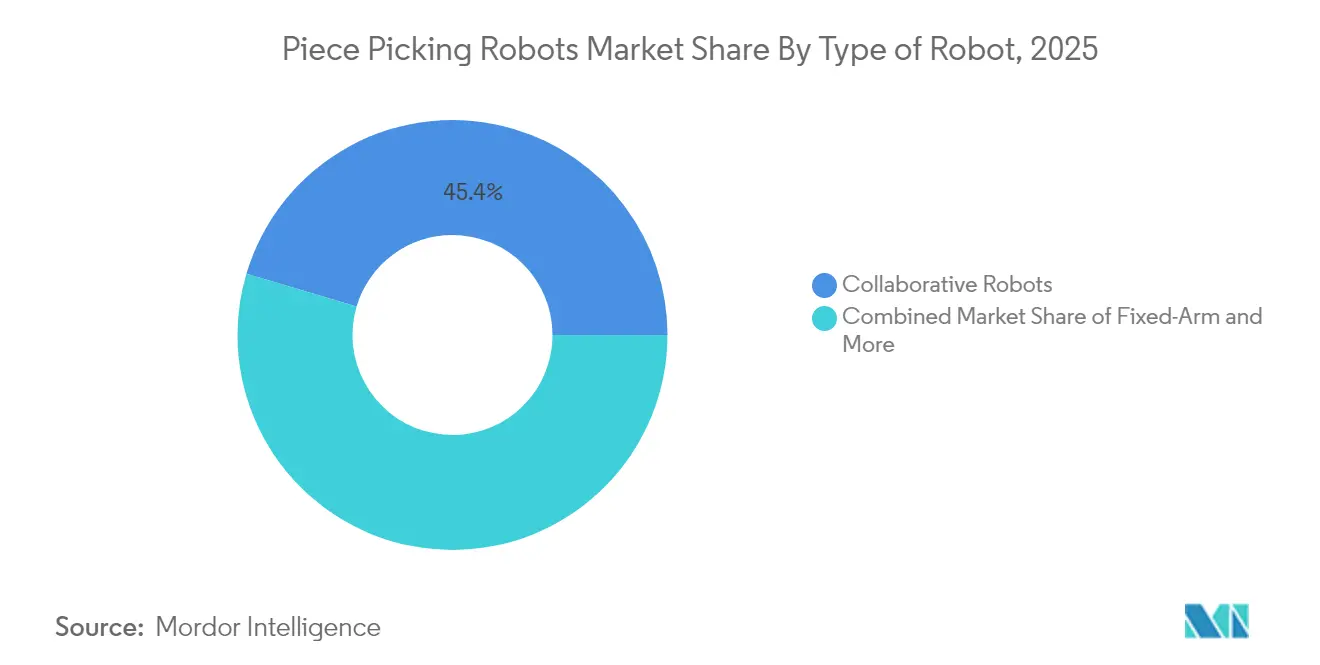

- By robot type, collaborative systems held 45.40% of the piece-picking robots market share in 2025, while mobile AMRs are projected to surge at a 49.2% CAGR to 2031.

- By component, hardware represented 57.10% of 2025 revenue; software is the fastest riser at a 51.3% CAGR through 2031.

- By end-user industry, e-commerce and retail commanded 53.20% of deployments in 2025; grocery and FMCG are expanding at a 55.4% CAGR to 2031.

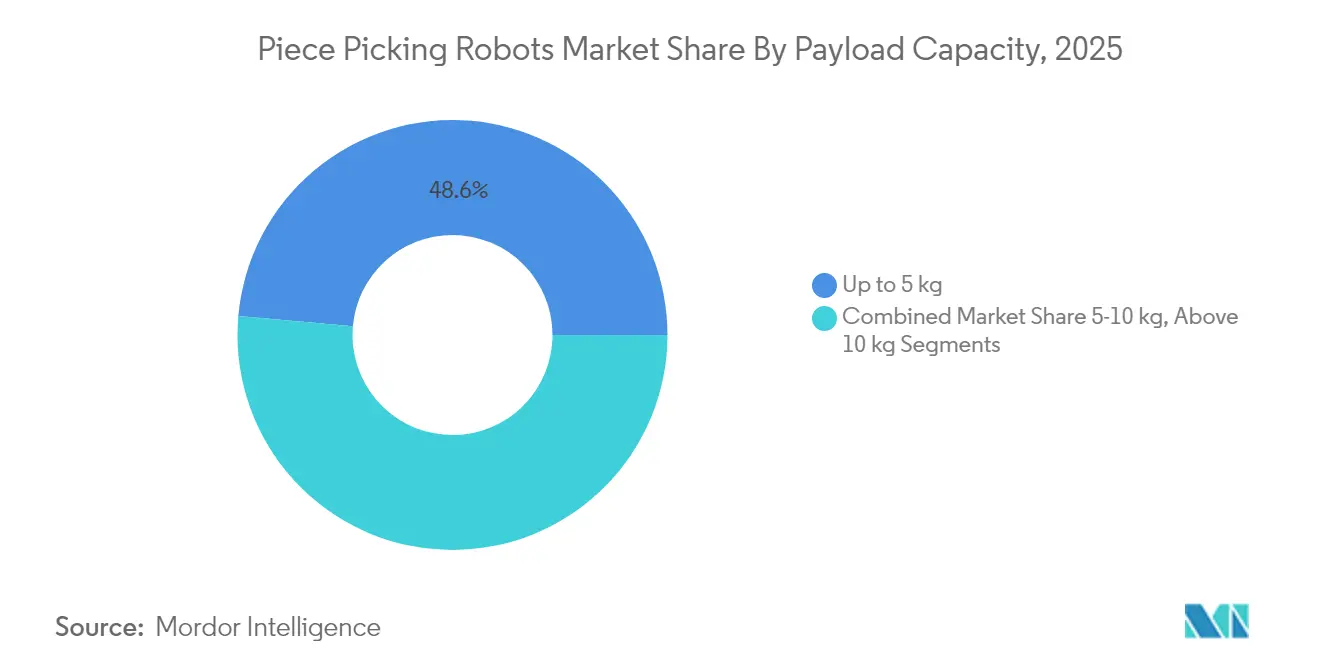

- By payload, the up-to-5 kg class accounted for 48.60% of the piece-picking robots market size in 2025 and is forecast to climb at a 52.9% CAGR through 2031.

- By deployment model, RaaS already represents 60.30% of 2025 installations and is growing at 52.6% annually.

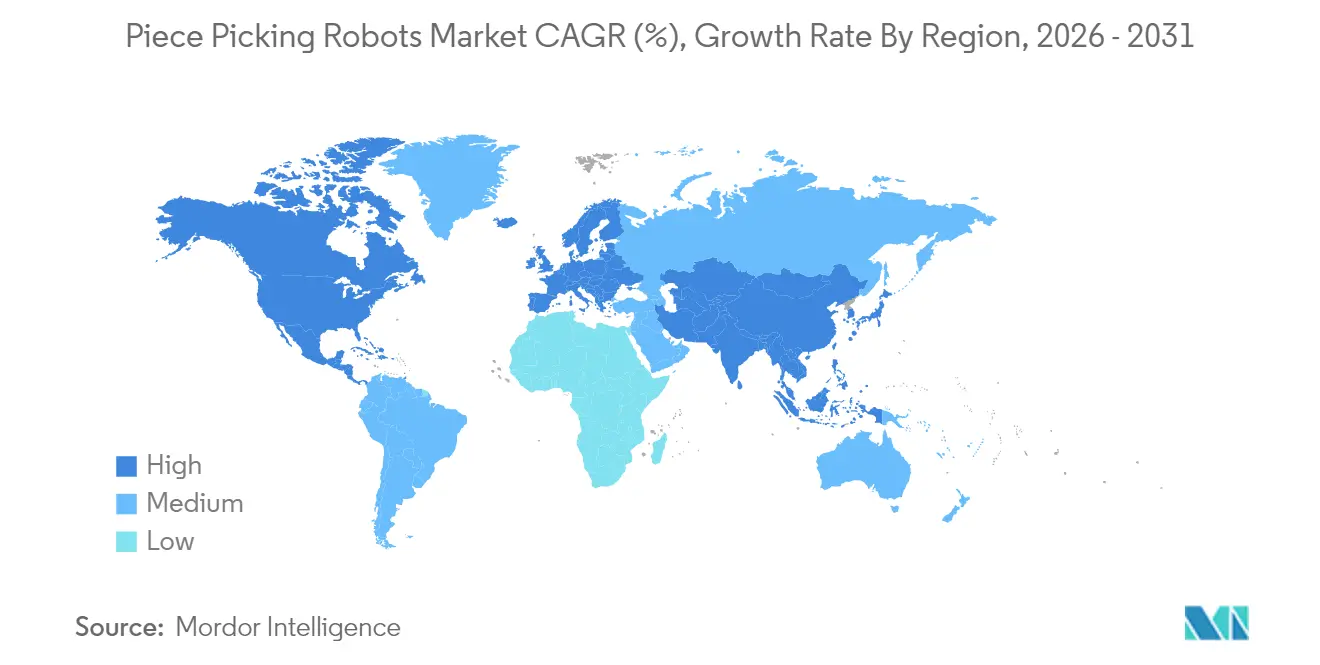

- By geography, North America captured 36.70% revenue share in 2025; Asia-Pacific is advancing at a 54.9% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Piece Picking Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising e-commerce order volumes and SKU proliferation | +12.5% | Global, concentrated in North America & APAC | Medium term (2-4 years) |

| Labour scarcity & wage inflation in mature logistics hubs | +15.2% | North America & EU, spreading to APAC urban centers | Short term (≤ 2 years) |

| Vision-AI breakthroughs enabling ≥ 95% pick accuracy | +8.7% | Global, early adoption in North America & Northern Europe | Medium term (2-4 years) |

| Cost-down in cobot arms (< USD 15,000) widening SME adoption | +6.8% | Global, impactful in APAC & emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising e-commerce order volumes and SKU proliferation

SKU counts are climbing 40% each year at large fulfillment centers, while order sizes fracture into smaller parcels. Piece-picking robots rely on machine-learning algorithms that now handle millions of unique items and reach 1,200 picks per hour. Micro-fulfillment footprints and same-day delivery guarantees intensify the requirement for systems that identify new objects in 0.3 seconds, driving the piece-picking robots market toward AI-rich software.

Labour scarcity and wage inflation in mature logistics hubs

More than 55% of warehouse operators cite labor shortages as the primary trigger for automation. [1]Locus Robotics, “Warehouse Labor Challenges: Automation Solutions,” locusrobotics.com Wage growth in logistics consistently exceeds general inflation, strengthening the investment case for robotics even at current price points. Japan underscores the point, with government programs positioning robotics as essential infrastructure amid a rapidly aging workforce s Robots also mitigate turnover by eliminating repetitive lifting tasks and enabling safer human-robot collaboration.

Vision-AI breakthroughs enabling ≥ 95% pick accuracy

Deep-learning perception now approaches human accuracy for object recognition, while tactile sensors add grip-force intelligence. Amazon’s Vulcan robot has cut damage rates and lifted throughput, highlighting how edge AI enables real-time decision-making at human-reaction speeds

Cost-down in cobot arms (< USD 15,000) widening SME adoption

Entry-level collaborative arms now list below USD 15,000, a sharp fall from 2020 prices that topped USD 50,000. [2]Standard Bots, “How Much Do Robots Cost?,” standardbots.com RaaS models reduce cash-flow hurdles further by spreading costs across pick volumes, letting smaller operations access top-tier capabilities without upfront capex.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent gripper limitations for deformable SKUs | -4.2% | Global, challenging in grocery & FMCG | Medium term (2-4 years) |

| High failure-on-first-pick KPI penalties in grocery | -2.8% | North America & EU grocery chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent gripper limitations for deformable SKUs

Robots still struggle with soft goods and flexible packaging. Success rates drop to 75–80% on deformable items versus 95% on rigid parts, restricting uptake in grocery and FMCG where dexterity matters most .

High failure-on-first-pick KPI penalties in grocery

Grocery fulfilment tolerates error rates below 1%. Robotic mis-picks lead to substitutions and spoilage costs that can exceed an order’s value, so operators remain cautious until accuracy metrics improve for variable produce and chilled inventories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Robot: Mobile AMRs Unlock Flexible Workflows

Mobile autonomous robots are climbing at a 49.2% CAGR and underpin next-generation agility, while collaborative arms retained 45.40% of 2025 revenue. This mix shows the piece-picking robots market shifting from fixed stations toward fleets that navigate dynamic warehouse aisles without heavy infrastructure.

Mobile platforms adapt routing based on live congestion and eliminate conveyance bottlenecks, raising system uptime during peak seasons. Brightpick’s Autopicker lifts items directly from totes and places them into outbound orders, cutting travel cycles and reducing dock-to-ship times. Fixed-arm units remain vital in pharmaceuticals and electronics where micron-level precision outweighs layout flexibility, yet growth is slower than the mobile cohort.

By Component: Software Emerges as the Prime Differentiator

Hardware accounted for 57.10% of 2025 spend, but software is growing 51.3% per year and fast becomes the profit engine. AI-driven stacks refine grasp-planning logic in real time, shrinking pick-cycle latency and expanding SKU coverage. AutoStore’s CarouselAI optimizes sequence selection without human tuning, demonstrating how software outpaces mechanical innovation in value creation .

Service revenues scale alongside software as integrators maintain fleets via cloud diagnostics and predictive maintenance. With over a petabyte of execution data, RightHand Robotics continuously updates algorithms, illustrating that data flywheels lock in customers through compounding accuracy gains

By End-User Industry: Grocery Surge Redefines Demand Profiles

E-commerce and omnichannel retail still deliver 53.20% of deployments, but grocery and FMCG show a 55.4% CAGR as supermarkets target in-store pick stations and dedicated dark stores. AutoStore’s eOperator demonstrates 800 lines per hour while maintaining pharmaceutical-grade accuracy, proving robots can handle temperature-controlled inventories.

Pharmaceutical facilities prize full traceability, embedding barcode scans within each robotic cycle. Third-party logistics providers extend robots across client portfolios, valuing the flexibility to switch SKUs daily without re-engineering grippers or vision pipelines. Automotive parts, apparel, and B2B industrial supplies remain emerging use cases where high mix counts and variable form factors align with maturing AI.

By Payload Capacity: Up to 5 kg Becomes the Norm

The ≤ 5 kg band owned 48.60% of 2025 revenue and advances at a 52.9% CAGR, encapsulating lightweight consumer goods that dominate e-commerce picks. This bracket optimizes speed-to-weight ratios, achieving 1,200 picks per hour with minimal energy draw.

Mid-range 5–10 kg systems serve bulk grocery, power tools, and office supplies, while 10 kg+ robots linger in niche heavy parts and appliance lines where throughput demands differ. Concentrating on the high-volume lightweight tier creates learning-curve effects that keep costs on a downward slope and accelerate the overall piece-picking robots market size.

By Deployment Model: RaaS Reshapes Capital Allocation

RaaS commands 60.30% of installed units and grows 52.6% per year, translating capex into predictable opex and transferring obsolescence risk to vendors. The global RaaS segment is forecast to climb from USD 1.33 billion in 2023 to USD 4.79 billion by 2031. Pay-per-pick pricing aligns cash outflows with revenue, a structure particularly attractive to small and medium warehouses that face volatile order volumes.

Large enterprises still sign direct-purchase contracts when volumes and internal engineering capabilities justify asset ownership. Yet even top-tier retailers deploy hybrid models, leasing extra units for holiday peaks then scaling back fleets to steady-state levels without idle capital.

Geography Analysis

North America captured 36.70% of 2025 turnover by combining mature e-commerce, advanced logistics real estate, and sustained automation budgets. U.S. industrial companies now assign 25-30% of capital investment to automation compared with 15-20% before the pandemic, reinforcing demand for piece-picking solutions. Tax incentives further sweeten returns, and early movers like Staples report measurable productivity gains from intelligent picking cells.

Asia-Pacific is expanding at a 54.9% CAGR and may eclipse North America before 2030. Government-backed initiatives in Japan support robotics as part of national productivity policy, while China’s logistics automation spending surpassed CNY 1.167 trillion (USD 160.5 billion) in 2023. foreign direct investment of USD 230 billion in 2023 fuels new fulfillment hubs that jump directly to advanced automation architectures.

Europe shows steady expansion driven by Germany’s density of 415 robots per 10,000 workers and a venture ecosystem that raised EUR 2 billion (USD 2.2 billion) for robotics in 2023 sifted. Nomagic securing EUR 41.5 million (USD 44.7 million) to broaden AI picking underscores continuing appetite for specialized disruptors. South America and the Middle East & Africa are nascent, yet rising logistics investment and ecommerce adoption signal future inflection once proven solutions drop in cost and complexity.

Competitive Landscape

Innovation and Integration Drive Future Success

Competitive intensity is moderate. No single vendor exceeds a double-digit global share, yet technical moats form around AI algorithms, domain-specific grippers, and integration experience. RightHand Robotics and Covariant apply large operational datasets to refine cloud-delivered brains, while AutoStore, Geek+, and OTTO Motors bundle ASRS, AMRs, and piece-picking arms into turnkey platforms.

Strategic investments mark the path to scale. Rockwell Automation’s March 2025 stake in RightHand Robotics aims to fold best-in-class picking into Rockwell’s controls ecosystem, expanding addressable markets and accelerating time-to-integrate. Midsize innovators focus on niche white spaces. Nexera Robotics secured USD 4.5 million to refine compliant grippers for irregular grocery items, attacking a pain point incumbents have yet to master.

Vertical integration is accelerating. Logistics service giants like DHL commit tens of millions to automated life-science warehouses equipped with Geek+ fleets, locking in proprietary know-how that strengthens client retention. Simultaneously, software-first houses partner with hardware OEMs to ensure end-to-end warranty and maintenance coverage, a tactic that reassures risk-averse customers and compresses vendor selection cycles.

Piece Picking Robots Industry Leaders

-

RightHand Robotics

-

Berkshire Grey

-

Covariant

-

Plus One Robotics

-

Ocado Group (Robotics Solutions)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Rockwell Automation invested in RightHand Robotics to embed piece-picking within Rockwell control stacks, pursuing a platform strategy that broadens solution scope and accelerates deployment speed

- March 2025: AutoStore launched CarouselAI, co-developed with Berkshire Grey, to retrofit intelligent picking into existing cube storage sites and shorten payback periods for brownfield customers

- March 2025: Hy-Tek Intralogistics partnered with Movu Robotics to blend shuttle storage and AMRs, positioning the duo to target high-throughput North American facilities

- February 2025: Nomagic raised EUR 41.5 million (USD 44.7 million) to treble European installations and deepen AI R&D, signaling investor confidence in software-centric differentiation

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the piece-picking robots market as all robotic systems, whether fixed-arm, collaborative, or autonomous mobile, that use machine vision and adaptive gripping to single out, grasp, and place individual stock-keeping units in warehouses, e-commerce fulfillment sites, or distribution hubs, with revenue captured at full-system sale or Robots-as-a-Service contract start. According to Mordor Intelligence, this addressable pool is valued at roughly USD 1.7 billion in 2025.

Scope Exclusion: Case-level palletizers, agricultural fruit harvesters, and micro-laboratory pickers remain outside our sizing.

Segmentation Overview

-

By Type of Robot

- Collaborative

- Fixed-Arm

- Mobile Piece-Picking AMR

- Others

-

By Component

- Hardware

- Software

- Services

-

By End-User Industry

- E-commerce / Retail Fulfilment Centres

- Pharmaceutical & Healthcare

- Grocery and FMCG

- 3PL / Parcel Logistics

- Others

-

By Payload Capacity

- Up to 5 kg

- 5-10 kg

- Above 10 kg

-

By Deployment Model

- Capital Purchase (CapEx)

- Robots-as-a-Service (RaaS)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Colombia

- Rets of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia

- China

- Japan

- South Korea

- India

- Singapore

- Rest of Asia

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We conducted interviews with fulfillment-center engineers, system integrators, and procurement leads across North America, Europe, and Asia-Pacific, supplemented by structured surveys of logistics practitioners. These discussions validated labor-cost inflection points, typical payback cycles, and price-performance breakpoints that public filings rarely reveal.

Desk Research

We begin by extracting shipment and contract data from 10-Ks, investor decks, and vendor presentations, and then align those figures with HS-code trade flows reported by the U.S. Census Bureau, Eurostat Comext, and China Customs. Insight from the International Federation of Robotics, Material Handling Industry briefs, and patent families mined via Questel lets us gauge technology diffusion rates.

Next, our analysts review Warehousing Education & Research Council cost surveys, OSHA injury logs tied to manual picking, and Dow Jones Factiva news on new site build-outs, which refine adoption timelines. These references illustrate but do not exhaust the secondary pool we consult.

Market-Sizing & Forecasting

A top-down reconstruction starts with regional warehouse counts and pick-face densities, converts them into a robot demand pool, and applies observed penetration plus median selling prices to yield annual revenue. Selective bottom-up checks, vendor shipment spot samples and RaaS fleet disclosures, tighten variance. Key inputs include e-commerce parcel growth, warehouse labor inflation, pick-rate improvements, ASP deflation curves, regulatory safety incentives, and capital-spending sentiment. Multivariate regression, followed by scenario analysis, projects the 2025-2030 trajectory.

Data Validation & Update Cycle

Outputs pass anomaly flags, peer review, and management sign-off. We refresh models yearly and issue interim updates when material events, such as major mergers or price shocks, shift the baseline. An analyst completes a final data sweep just before release.

Why Mordor's Piece Picking Robots Baseline Commands Reliability

Published estimates often diverge because firms differ in scope definitions, baseline years, and price-erosion assumptions.

Key gap drivers include exclusion of mobile pickers, bundling of broader pick-and-place systems, or aggressive unit-price discounts not yet visible in contracts. Other publishers cite 2024 values around USD 1.05 billion and USD 1.1 billion, while one places 2025 value as high as USD 4.15 billion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.7 B (2025) | Mordor Intelligence | - |

| USD 1.05 B (2024) | Global Consultancy A | Omits mobile AMR pickers and RaaS revenue; earlier baseline |

| USD 1.10 B (2024) | Global Consultancy B | Blends case-picking and palletizing robots under same scope |

| USD 4.15 B (2025) | Research Firm C | Counts wider automation gear and assumes steep ASP erosion |

These contrasts show that our disciplined scope selection, consistent price logic, and annual refresh cadence give decision-makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current piece-picking robots market size and growth outlook?

The market recorded USD 2.58 billion revenue in 2026 and is on track to reach USD 20.78 billion by 2031, registering a 51.78% CAGR.

Which segment leads the piece-picking robots market share today?

Collaborative robots held 45.40% revenue share in 2025, benefitting from safe human-robot collaboration in mixed workflows.

Why is Asia-Pacific growing faster than other regions?

Aging workforces, rising wages, and high e-commerce penetration push Asia-Pacific to a 54.9% CAGR, the highest among all regions.

How is Robots-as-a-Service changing procurement strategies?

RaaS shifts automation from capex to opex, already accounting for 60.30% of 2025 deployments and letting firms scale fleets during peak demand without buying hardware outright.

What technical hurdle most restricts grocery automation?

Current grippers still struggle with deformable items, keeping success rates around 75–80% and limiting adoption where retailers require near-perfect first-pick accuracy.

Page last updated on: