Southeast Asia Industrial And Service Robot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

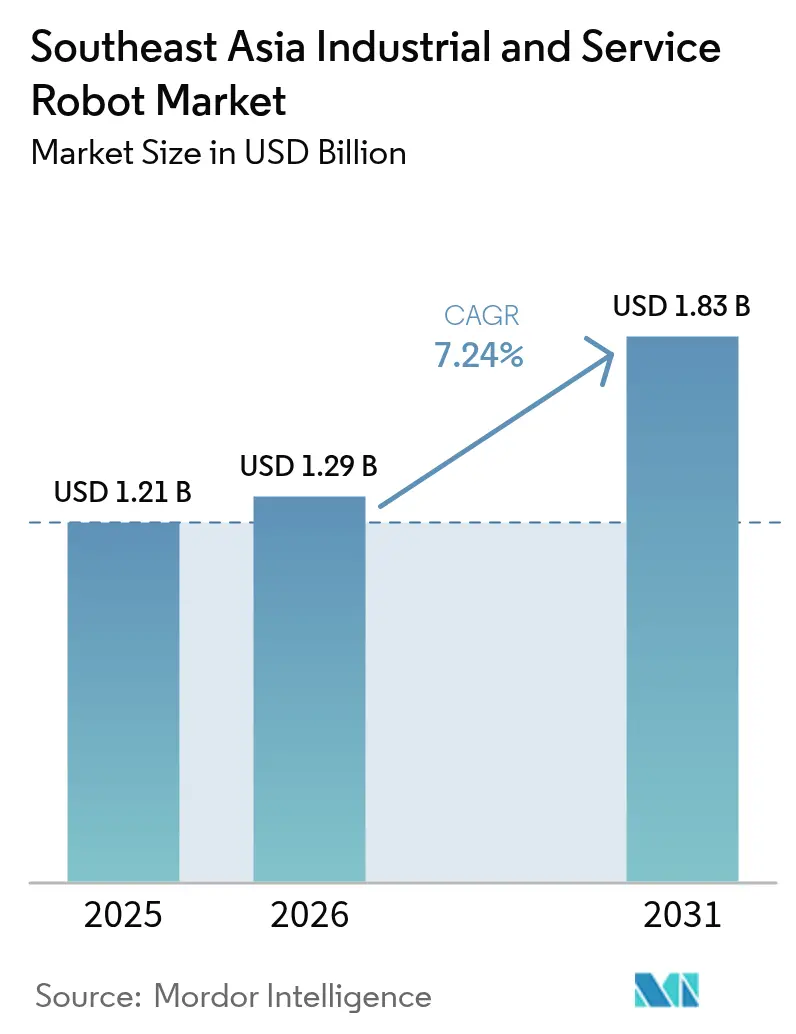

| Base Year Market Size (2025) | USD 1.21 Billion |

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Industrial And Service Robot Market Analysis by Mordor Intelligence

The Southeast Asia industrial and service robot market size was valued at USD 1.29 billion in 2026 and is estimated to grow from USD 1.21 billion in 2025 to reach USD 1.83 billion by 2031, at a CAGR of 7.24% over 2026-2031. Heightened automation incentives, labor scarcity in core manufacturing hubs and the migration of electronics assembly out of coastal China are accelerating first-time deployments across automotive, semiconductor and logistics sites. Collaborative platforms are diffusing fastest because they integrate with legacy lines without caging, cutting typical payback periods from 36 months to 18 months. System integrators now bundle leasing, training and predictive-maintenance software, lowering the entry barrier for small and mid-size factories. Country adoption is polarizing: Vietnam already commands a quarter of regional revenue while the Philippines, still under-penetrated, is advancing above 8% CAGR as e-commerce fulfillment centers embrace autonomous mobile robots.

Key Report Takeaways

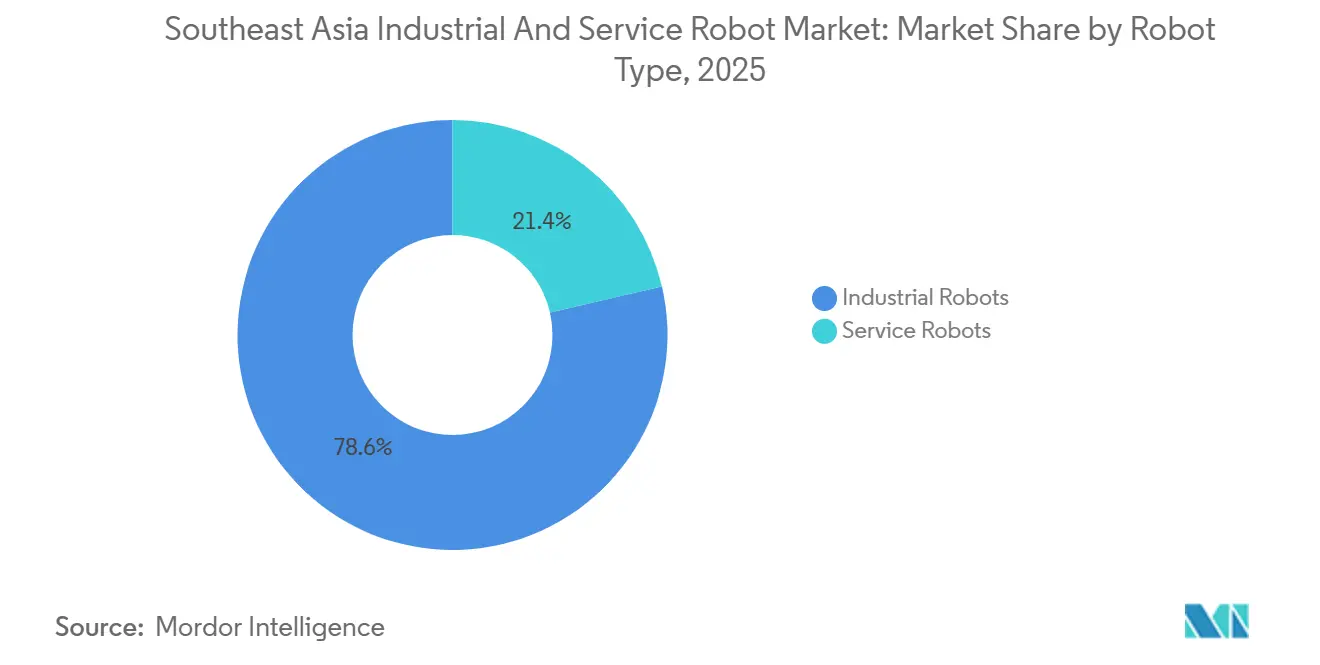

- By robot type, industrial platforms led with 78.63% of Southeast Asia industrial and service robot market share in 2025 while collaborative robot is projected to expand at a 7.93% CAGR through 2031.

- By country, Vietnam accounted for 24.51% of Southeast Asia industrial and service robot market size in 2025, whereas the Philippines is forecast to register the fastest 8.01% CAGR to 2031.

- By payload, 16-60 kg systems captured 42.83% share of the Southeast Asia industrial and service robot market size in 2025, and payloads up to 15 kg is poised to climb at an 8.12% CAGR.

- By component, hardware accounted for 44.12% of the 2025 market share, while service contracts are set to grow at a 7.84% CAGR over 2026-2031.

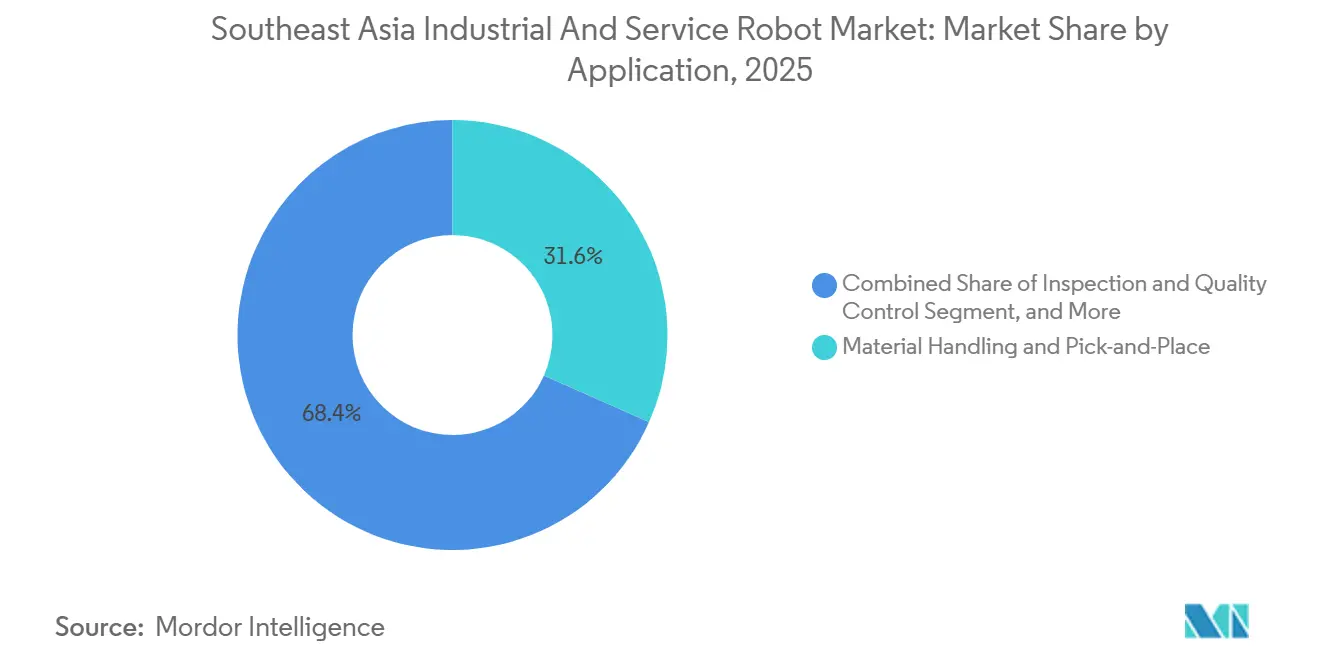

- By application, material handling and pick-and-place secured 31.63% revenue share in 2025, yet inspection and quality control posts the quickest 8.84% CAGR outlook.

- By enterprise size, large enterprises held 59.36% share of the 2025 market share, while small and medium enterprise is projected to expand at a 7.61% CAGR to 2031.

- By end-user industry, electronics and semiconductors commanded 37.48% revenue share in 2025, while healthcare is forecast to expand at a 9.04% CAGR through 2031.

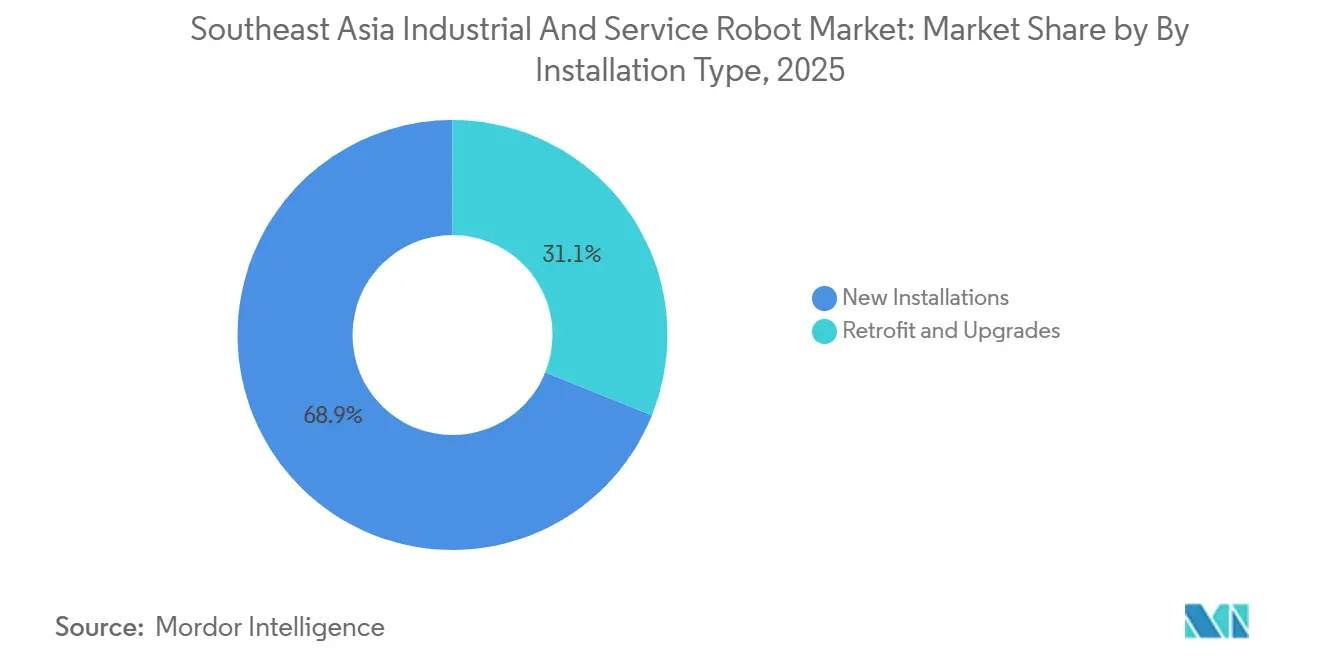

- By installation type, new installs dominated with 68.91% share of 2025 revenue, whereas retrofit and upgrade project is advancing at a 7.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Industrial And Service Robot Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ASEAN Industry 4.0 Subsidy Programmes Accelerating Robot Uptake | +1.2% | Singapore, Malaysia, Thailand, Vietnam | Medium term (2-4 years) |

| Rising Labour Scarcity in Singapore and Thailand Boosting Automation ROI | +1.5% | Singapore, Thailand, with spillover to Malaysia | Short term (≤ 2 years) |

| China-Plus-One Electronics Migration to Vietnam and Malaysia Lifting Precision-Assembly Demand | +1.8% | Vietnam, Malaysia, with secondary gains in Thailand | Medium term (2-4 years) |

| E-Commerce Fulfilment Boom in Indonesia and Philippines Driving Logistics Robots | +1.0% | Indonesia, Philippines, Metro Manila and Jabodetabek corridors | Short term (≤ 2 years) |

| Smart-Hospital Capex in Thailand and Singapore Expanding Service-Robot Adoption | +0.9% | Thailand, Singapore, with pilot projects in Malaysia | Medium term (2-4 years) |

| Growth of Regional System-Integrator Ecosystem Reducing Deployment Barriers for SMEs | +0.7% | Regional, concentrated in Singapore, Malaysia, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ASEAN Industry 4.0 Subsidy Programs Accelerating Robot Uptake

Governments are compressing payback periods by funding up to 70% of qualified automation outlays, cutting the capital needed for a six-axis unit from USD 50 000-70 000 to as low as USD 15 000-25 000.[1]Enterprise Singapore, “Productivity Solutions Grant,” enterprisesg.gov.sg Singapore’s Productivity Solutions Grant, Malaysia’s Smart Manufacturing 4.0 Intervention Fund and Thailand’s eight-year tax holidays collectively backed more than 3 000 new robot cells in 2025. Vietnam’s action plan targets 10 000 automated cells by 2030, while Indonesia set aside IDR 500 billion for smart-factory pilots, signaling long-run policy continuity that should sustain order pipelines.

Rising Labor Scarcity in Singapore and Thailand Boosting Automation ROI

Median manufacturing wages rose 4.8% in Singapore and statutory minimums climbed in Thailand, making the hourly cost of a cobot competitive with human operators.[2]Ministry of Manpower Singapore, “Labour Force Statistics 2025,” mom.gov.sg Foreign-worker quotas tightened, vacancies in welding and inspection breached double digits and aging workforces pushed manufacturers to substitute capital for labor. As a result, body-in-white welding cells and machine-tending cobots proliferated across Rayong, Chonburi, Jurong and Tuas.

China-Plus-One Electronics Migration to Vietnam and Malaysia Lifting Precision Assembly Demand

FDI worth more than USD 13 billion flowed into Vietnamese and Malaysian electronics parks in 2024-2025, bringing SCARA, delta and AI-guided inspection robots onto new smartphone, camera-module and AI-chip assembly lines.[3]Reuters, “Foxconn Expands Vietnam Assembly Lines,” reuters.com Robot density in Vietnamese electronics climbed from 90 to 150 units per 10 000 workers, underlining a shift to automation-first production models that favor zero-defect repeatability over low-cost manual assembly.

E-commerce Fulfillment Boom in Indonesia and Philippines Driving Logistics Robots

Indonesia’s USD 62 billion and the Philippines’ USD 14 billion online retail markets pushed 900 autonomous mobile robots into Metro Manila and Jabodetabek warehouses during 2024-2025. Goods-to-person cycle times fell by two-thirds and labor costs dropped 30%, encouraging third-party logistics firms to bundle robots with real-time inventory software in turnkey contracts worth USD 0.2-0.5 million per 10 000 m² facility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex Versus Low Migrant-Labour Costs Limits ROI in Indonesia and Vietnam | -0.8% | Indonesia, Vietnam, with secondary effects in Philippines | Short term (≤ 2 years) |

| Fragmented Factory Utilities and Floor Conditions Complicate Integration | -0.5% | Indonesia, Philippines, secondary in Vietnam | Medium term (2-4 years) |

| Import Tariffs or Lead-Times for Robot Components Due to Weak Local Supply Base | -0.4% | Regional, most acute in Indonesia, Philippines | Medium term (2-4 years) |

| Shortage of Advanced Robotics Talent Outside Singapore Slows Commissioning and Service | -0.6% | Thailand, Malaysia, Vietnam, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex Versus Low Migrant-Labor Costs Limits ROI in Indonesia and Vietnam

Monthly wages as low as USD 190-315 in garment and footwear zones keep manual processes attractive, especially when cobot leases exceed USD 1 200 per month. Informal recruitment channels and cross-border labor accords further delay the cost-parity point, constraining robot penetration to below 5 units per 10 000 workers in several labor-intensive clusters.

Shortage of Advanced Robotics Talent Outside Singapore Slows Commissioning and Service

Thailand, Malaysia and Vietnam together graduated fewer than 4 000 certified robot technicians in 2024, versus demand for almost 10 000 by 2027. Scarcity inflates day-rates for foreign engineers to USD 1 500-2 500 and extends startup windows by up to three months, eroding some of the productivity gains promised by automation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Robot Type: Collaborative Momentum Recasts Industrial Dominance

The industrial class retained 78.63% of 2025 spending, yet the collaborative subset is advancing 7.93% annually. Large automakers and semiconductor fabs continue installing six-axis workhorses for high-speed welding and wafer handling. In parallel, SMEs are embracing 3-16 kg cobots that bolt onto existing jigs, trimming integration costs 30-40% and unlocking mixed-model production. Service robots accounted for 21.37% of revenue, with mobile platforms for logistics and bedside delivery outpacing domestic vacuums. The Southeast Asia industrial and service robot market for cobots is projected to expand as lease-to-own models proliferate, while articulated incumbents defend market share through digital twin simulation and AI path planning. Collaborative designs already account for half of new cells at Vietnamese electronics vendors, confirming their role as a disruptive bridge between manual lines and fully lights-out factories.

Demand patterns underscore a clear split. Heavy articulated arms still dominate Thai body-in-white welding bays and Malaysian die-attach flows, where duty cycles exceed 20 hours per day. Conversely, Techman, Universal Robots, and ABB GoFa units populate Singaporean precision-machining shops, where operators can re-teach paths in under 10 minutes. Professional service formats AMRs, pharmacy dispensers and UV--disinfection units are outpacing domestic cleaners thanks to hospital and e-commerce funding. As AI-enabled vision packages mature, vendors expect multi-robot orchestration to become the next battleground, weaving cobots and AMRs into unified fleets managed from cloud dashboards.

By Payload Capacity: Lightweight Cells Lead Future Growth

Systems rated 16-60 kg held the largest 42.83% share in 2025, covering welding guns, mid-weight trays and machining blanks. Yet sub-15 kg robots are expanding fastest at 8.12% CAGR as smartphone, wearable and PCB makers favor precision over brute force. Here, the Southeast Asia industrial and service robot market share for lightweight arms benefits from fine-pitch placement accuracy within ±10 µm, a necessity for camera modules and flex connectors. Delta and SCARA variants dominate due to 0.3 second pick cycles and compact footprints.

The heavier 61-225 kg class sits at 18% share, serving palletizing and power-train machining in Thailand and Indonesia, while above-225 kg behemoths handle beverage crates and steel plate. A modular architecture trend lets factories swap wrist assemblies to adjust payload tiers, keeping capital intensity low and supporting high-mix production. As sensor prices fall and safety standards evolve, integrators expect lightweight cobots to infiltrate even legacy stamping lines, trimming ergonomic injuries and night-shift premiums.

By Component: Services Become a Recurring Revenue Anchor

Hardware still commanded 44.12% of the 2025 market share, but service contracts covering design, integration, training, and maintenance are growing 7.84% each year. Integrators now bundle software subscriptions, fleet analytics and predictive-maintenance callouts, generating annuity-style cash flows alongside upfront sales. Manipulators absorb over half of hardware spending, trailed by controllers and drives. Yet sensor and end-effector categories, though smaller, outpace overall growth as AI vision, force-torque feedback and application-specific grippers penetrate pick-and-place and inspection tasks. The Southeast Asia industrial and service robot market size for integration services will continue expanding as SMEs outsource turnkey deployments rather than hiring scarce in-house engineers.

Cloud dashboards that push over-the-air updates cut unplanned downtime 20-30%, cementing software as the glue across mixed fleets. Meanwhile, robot-as-a-service deals price entire cells at USD 1 500-3 000 monthly, aligning cash outflow with productivity gains and smoothing the adoption curve for cash-constrained firms.

By Application: Inspection Surges Under Zero-Defect Mandates

Material handling and pick-and-place retained a 31.63% of market share in 2025, but inspection and quality control is sprinting ahead at 8.84% CAGR. Tier-one electronics buyers now demand six-sigma yields, forcing Vietnamese, Malaysian and Thai suppliers to embed AI-guided vision cells that flag micro-cracks, misalignments and solder voids at 60-unit-per-minute throughputs.

Consequently, the Southeast Asia industrial and service robot market size attached to inspection solutions is set to widen, while commoditization erodes premiums in basic palletizing lines. Welding and soldering, packaging, painting and cutting together cover the remainder, yet each is trending toward higher precision, closed-loop feedback and integrated MES connectivity.

By End-User Industry: Healthcare Outpaces Electronics Expansion

Electronics and semiconductors still control 37.48% of revenue, yet hospital automation is racing ahead at 9.04% CAGR as Thailand, Singapore and Malaysia retrofit pharmacies, operating rooms and linen flows. Service robots now shuttle medication at Singapore General Hospital, slash nurse workload in Bangkok and support minimally invasive surgery with 15% shorter operating times.

Logistics, automotive and food processing round out demand, but each leans on different robot classes AMRs in e-commerce hubs, heavy articulated arms in chassis welding, delta robots in snack packaging. The Southeast Asia industrial and service robot industry sees healthcare as the next frontier where safety, sterility and demographic pressure converge to justify premium unit economics.

By Installation Type: Retrofits Rise on Brownfield Opportunities

New builds captured 68.91% of 2025 revenue as foreign investors erected automation-first electronics fabs, yet retrofit projects are growing 7.57% because legacy automotive, food and plastic lines prefer phased cobot add-ons over full shutdowns.

Upgrade grants covering up to 50% of retrofit bills in Singapore and Thailand shorten ROI below two years, helping SMEs climb the maturity ladder. IoT bolt-ons that connect 2010-vintage robots to modern MES suites further propel the retrofit wave.

By Enterprise Size: Subsidies Propel SME Catch-Up

Large groups still command 59.36% of the market share, leveraging scale to blanket plants with hundreds of articulated arms. However, SMEs are advancing 7.61% annually, catalyzed by subsidies that slash up-front costs and by standard plug-and-play cobot kits priced at USD 30 000-60 000.

Lease models at 3-5% interest further tilt the calculus. As integrator footprints expand beyond capital cities, SMEs' contribution to the Southeast Asia industrial and service robot market will accelerate, diversifying demand across thousands of mid-tier workshops.

Geography Analysis

Vietnam leads regional revenue with 24.51% share in 2025 on the back of USD 142 billion electronics exports and policy tools offering up to 15-year tax holidays for high-tech plants. Robot density in electronics hit 150 units per 10 000 workers, reflecting a decisive pivot toward precision automation. Singapore, though smaller at 18% share, boasts the region’s highest density at 605 units per 10 000 workers, driven by aerospace, pharma and precision engineering upgrades that increasingly focus on retrofitting collaborative cells.

Thailand holds 22% share, supported by 1.9 million-unit vehicle output and 4 500 new robots installed across its Eastern Economic Corridor. Incentives such as eight-year tax holidays and duty exemptions attracted USD 3.2 billion in automation-related FDI. Malaysia follows at 20%, propelled by semiconductor back-end lines in Penang and Johor adding thousands of die-attach and wire-bonding robots.

Indonesia’s 12% slice is climbing at 7.4% CAGR, thanks to AMRs in Jabodetabek fulfillment centers and tier-two automotive components, yet low labor costs still slow full automation in garments and footwear. The Philippines, presently under 10% share, is the fastest grower at 8.01% CAGR as e-commerce corridors around Manila and Clark adopt goods-to-person robots and as tax credits cover half of automation capex.

Cambodia, Laos, Myanmar and Brunei collectively account for roughly 4%, constrained by grid reliability and capital access, but garment cutting and food-processing trials hint at an eventual diffusion as integrators expand support hubs.

Competitive Landscape

Japanese and European majors FANUC, Yaskawa, ABB, KUKA, Kawasaki and Stäubli control an estimated 55-60% of the Southeast Asia industrial and service robot market. Their edge lies in deep distributor networks, multi-decade service records and entrenched links to automotive and electronics multinationals. Taiwanese and South Korean challengers such as Delta Electronics, Techman Robot and Hanwha Robotics together hold 15-20%, carving share in collaborative and lightweight niches by offering 10-week lead times and localized engineering support.

Strategically, incumbents chase high-ticket body-in-white and wafer-handling projects where lifetime service contracts protect 20%+ margins, whereas challengers court first-time adopters with robot-as-a-service bundles priced at USD 1 500-3 000 per month. Chinese entrants, including Siasun and Estun, undercut list prices by up to 30% but are still testing after-sales reach, limiting penetration to low-single digits.

Technology is the new battleground. ABB deployed collision-free multi-robot path planning, Universal Robots scaled its UR+ plug-in marketplace beyond 400 certified peripherals and Yaskawa opened training academies to ease the regional talent crunch. Vertical-specific integrators now bundle food-grade grippers, ISO-10218 safety packages and compliance documentation, compressing proof-of-concept cycles for SMEs and expanding the Southeast Asia industrial and service robot market’s addressable base.

Southeast Asia Industrial And Service Robot Industry Leaders

FANUC Corporation

Yaskawa Electric Corporation

KUKA AG

ABB Ltd

Kawasaki Heavy Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: ABB committed USD 45 million to enlarge its Rayong, Thailand robot plant and open a training center for 500 technicians annually.

- November 2025: Yaskawa and Saigon Automation opened a Ho Chi Minh City integration hub delivering cobot cells to SME electronics firms.

- October 2025: Universal Robots launched the UR20 model across ASEAN, offering a 20 kg payload collaborative arm at USD 55 000.

- September 2025: FANUC inaugurated a robotics academy in Penang, Malaysia to certify 400 programmers each year.

Southeast Asia Industrial And Service Robot Market Report Scope

Industrial robots are automated machines designed to perform manufacturing or production tasks with high precision, speed, and repeatability.

The Southeast Asia Industrial and Service Robot Market Report is Segmented by Robot Type (Industrial Robots including Articulated, SCARA, Cartesian, Delta, Collaborative, and Other Types; Service Robots including Professional and Domestic), Payload Capacity (Up to 15 kg, 16-60 kg, 61-225 kg, Above 225 kg), Component (Hardware, Software, Services), Application (Material Handling, Welding, Assembly, Painting, Packaging, Inspection, Cutting, Other), End-User Industry (Automotive, Electronics, Metals, Plastics, Food and Beverage, Logistics, Healthcare, Retail, Other), Installation Type (New, Retrofit), Enterprise Size (Large, SME), and Country (Indonesia, Malaysia, Singapore, Thailand, Vietnam, Philippines, Rest of SEA). Market Forecasts are Provided in Terms of Value (USD).

| Industrial Robots | Articulated Robots | |

| SCARA Robots | ||

| Cartesian / Gantry Robots | ||

| Parallel / Delta Robots | ||

| Collaborative Robots (Cobots) | ||

| Other Industrial Robot Types | ||

| Service Robots | Professional Service Robots | Logistics and Warehousing |

| Medical and Healthcare | ||

| Agriculture and Field | ||

| Inspection and Maintenance | ||

| Hospitality | ||

| Domestic Service Robots | Cleaning | |

| Companion and Elder-Care | ||

| Lawn and Pool | ||

| Other Domestic Robot Types | ||

| Up to 15 kg |

| 16 - 60 kg |

| 61 - 225 kg |

| Above 225 kg |

| Hardware | Manipulator |

| Controller | |

| Drives | |

| Sensors | |

| End-Effectors | |

| Software | |

| Services | Integration and Deployment |

| Training and Support | |

| Maintenance |

| Material Handling and Pick-and-Place |

| Welding and Soldering |

| Assembly |

| Painting and Dispensing |

| Packaging and Palletising |

| Inspection and Quality Control |

| Cutting and Processing |

| Other Applications |

| Automotive |

| Electronics and Semiconductor |

| Metals and Machinery |

| Plastics and Chemicals |

| Food and Beverage |

| Logistics and Warehousing |

| Healthcare |

| Retail and Hospitality |

| Others (Agriculture, Construction) |

| New Installations |

| Retrofit and Upgrades |

| Large Enterprises |

| Small and Medium Enterprises |

| Indonesia |

| Malaysia |

| Singapore |

| Thailand |

| Vietnam |

| Philippines |

| Rest of Southeast Asia |

| By Robot Type | Industrial Robots | Articulated Robots | |

| SCARA Robots | |||

| Cartesian / Gantry Robots | |||

| Parallel / Delta Robots | |||

| Collaborative Robots (Cobots) | |||

| Other Industrial Robot Types | |||

| Service Robots | Professional Service Robots | Logistics and Warehousing | |

| Medical and Healthcare | |||

| Agriculture and Field | |||

| Inspection and Maintenance | |||

| Hospitality | |||

| Domestic Service Robots | Cleaning | ||

| Companion and Elder-Care | |||

| Lawn and Pool | |||

| Other Domestic Robot Types | |||

| By Payload Capacity (Industrial) | Up to 15 kg | ||

| 16 - 60 kg | |||

| 61 - 225 kg | |||

| Above 225 kg | |||

| By Component | Hardware | Manipulator | |

| Controller | |||

| Drives | |||

| Sensors | |||

| End-Effectors | |||

| Software | |||

| Services | Integration and Deployment | ||

| Training and Support | |||

| Maintenance | |||

| By Application | Material Handling and Pick-and-Place | ||

| Welding and Soldering | |||

| Assembly | |||

| Painting and Dispensing | |||

| Packaging and Palletising | |||

| Inspection and Quality Control | |||

| Cutting and Processing | |||

| Other Applications | |||

| By End-User Industry | Automotive | ||

| Electronics and Semiconductor | |||

| Metals and Machinery | |||

| Plastics and Chemicals | |||

| Food and Beverage | |||

| Logistics and Warehousing | |||

| Healthcare | |||

| Retail and Hospitality | |||

| Others (Agriculture, Construction) | |||

| By Installation Type | New Installations | ||

| Retrofit and Upgrades | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Country | Indonesia | ||

| Malaysia | |||

| Singapore | |||

| Thailand | |||

| Vietnam | |||

| Philippines | |||

| Rest of Southeast Asia | |||

Key Questions Answered in the Report

How large will Southeast Asia’s industrial and service robot demand become by 2031?

It is forecast to reach USD 1.83 billion, expanding at a 7.24% CAGR from 2026-2031.

Which robot segment is growing fastest in Southeast Asia?

Collaborative units, especially those with payloads below 15 kg, are projected to rise at 7.93% CAGR as SMEs adopt flexible automation.

Why is Vietnam the region’s top robot spender?

Electronics and semiconductor FDI above USD 8 billion and generous tax holidays positioned Vietnam to capture 24.51% of 2025 revenue.

What is driving healthcare robot adoption?

Smart-hospital investments in Thailand and Singapore and acute nursing shortages are propelling a 9.04% CAGR in medical service robots.

How do subsidy programs affect SME automation?

Grants covering up to 70% of capex and lease-to-own financing lower entry costs, helping SMEs add cobot cells with payback in under two years.

Page last updated on: