Robotics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

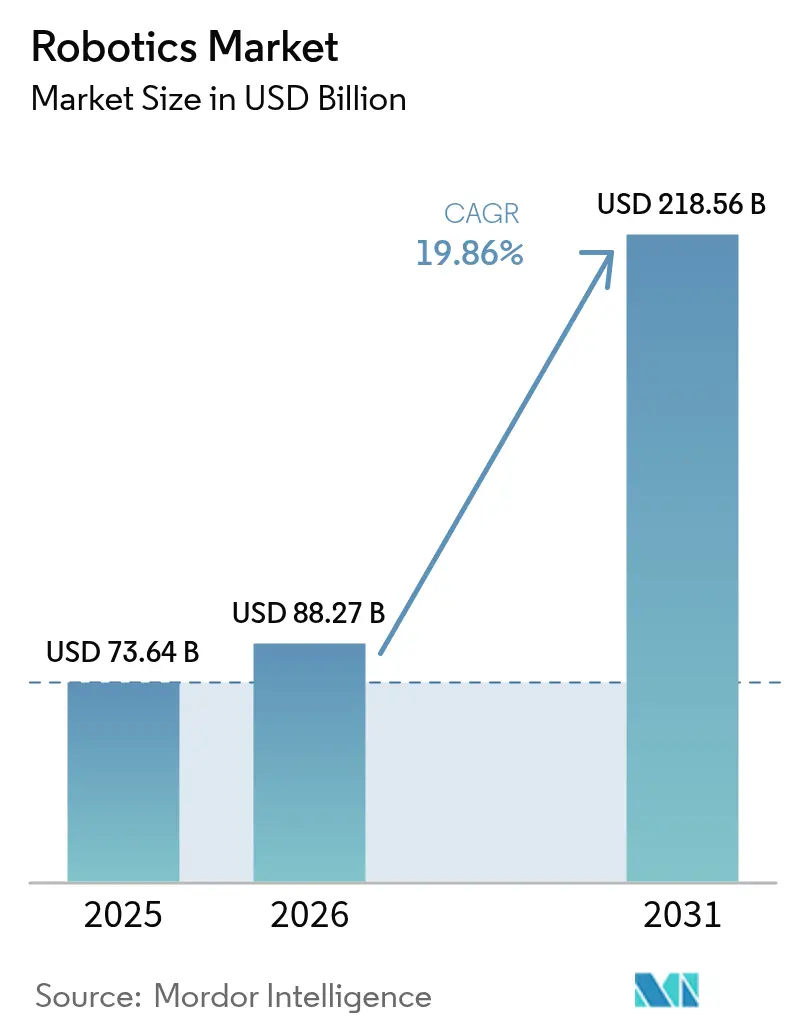

| Market Size (2026) | USD 88.27 Billion |

| Market Size (2031) | USD 218.56 Billion |

| Growth Rate (2026 - 2031) | 19.86% CAGR |

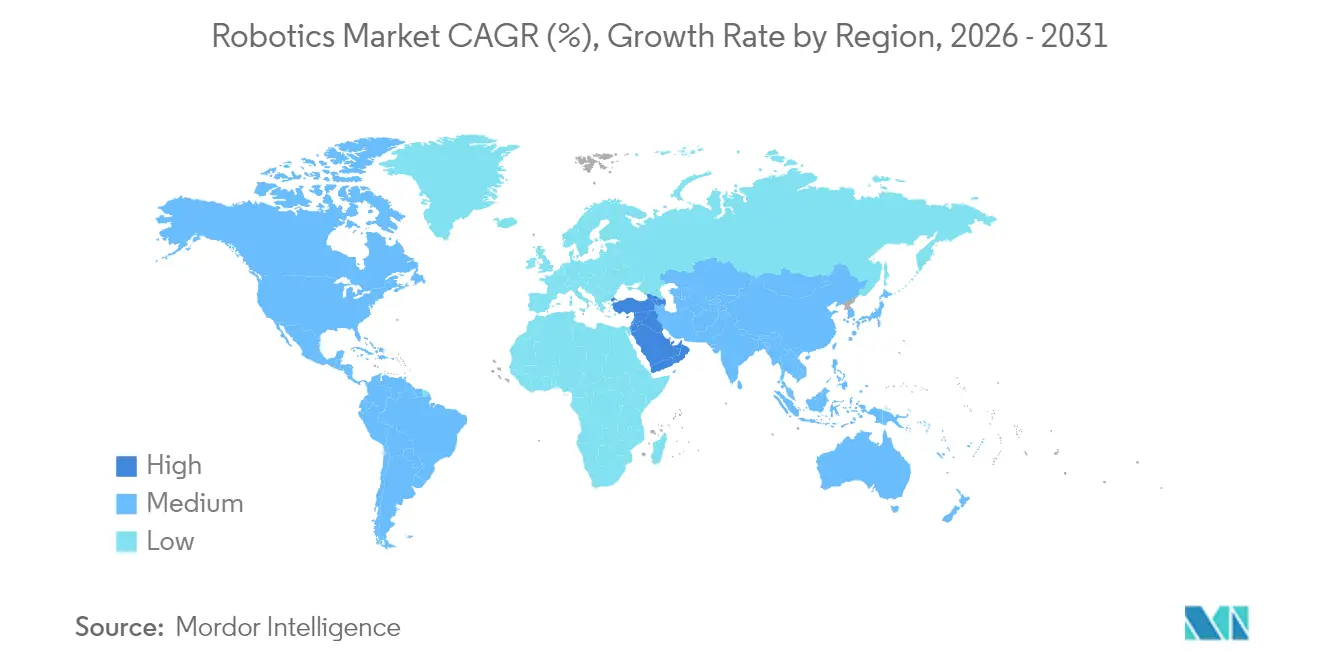

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

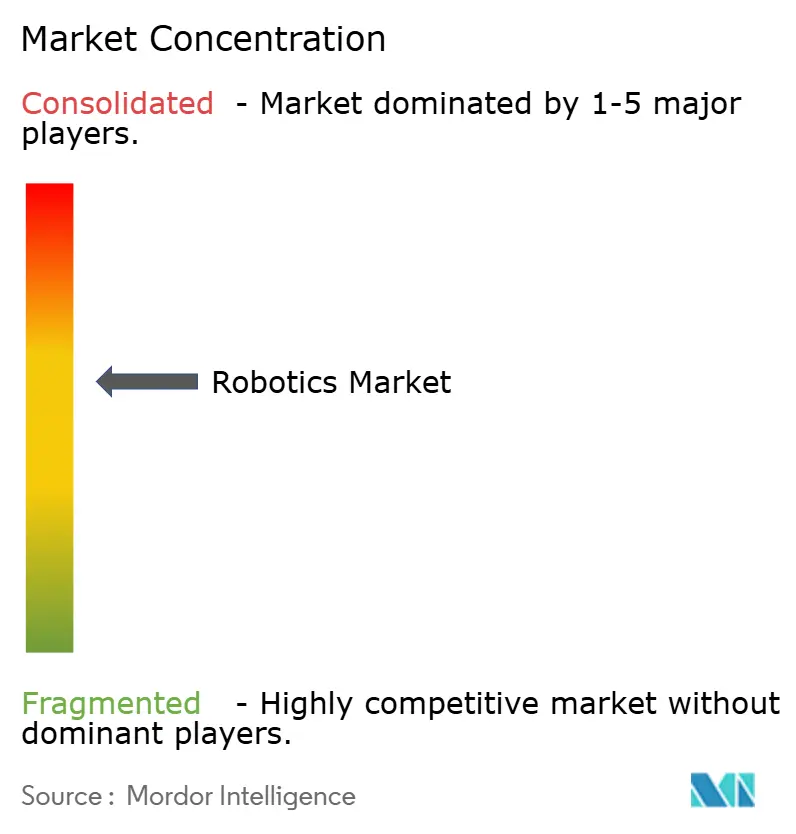

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotics Market Analysis by Mordor Intelligence

Robotics market size in 2026 is estimated at USD 88.27 billion, growing from 2025 value of USD 73.64 billion with 2031 projections showing USD 218.56 billion, growing at 19.86% CAGR over 2026-2031. This growth trajectory reflects structural labor shortages in advanced economies, systematic cost deflation in automation hardware, and government-backed reshoring programs that treat robots as strategic infrastructure rather than optional capital goods. Large enterprises accelerate adoption to stabilise production amid wage pressure, while small and medium firms now gain access through collaborative systems and Robot-as-a-Service contracts. Regional momentum is shifting: Asia-Pacific retains volume leadership, but the Middle East shows the quickest pace as sovereign funds pursue technology-driven diversification. On the supply side, declining component costs and low-code programming platforms reshape the value chain toward software intelligence, setting up recurring revenue streams for vendors that master artificial-intelligence-based control. Cyber-security weaknesses, export-control friction, and skill gaps among smaller users remain braking forces, yet they also open specialist service niches, especially around secure deployment and lifecycle support.

Key Report Takeaways

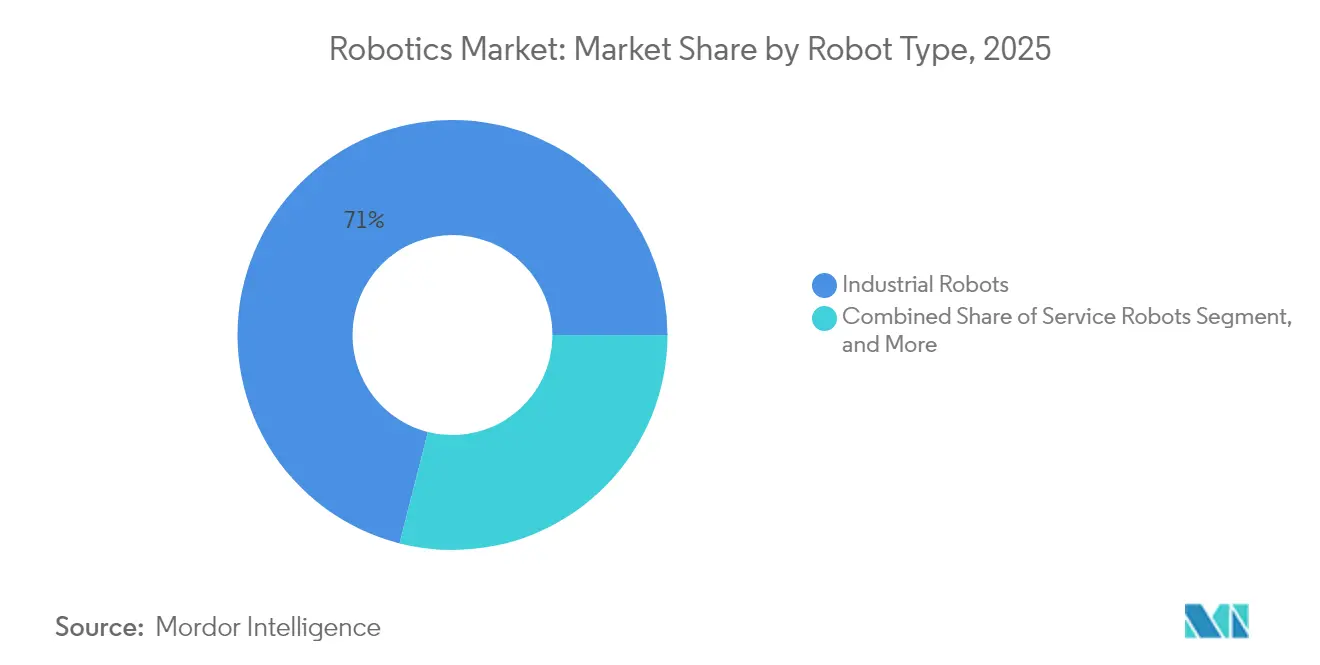

- By robot type, industrial robots led with 71.04% revenue share in 2025; collaborative robots are projected to post a 25.64% CAGR to 2031.

- By component, hardware captured 63.12% of the global robotics market share in 2025, while software is expected to rise at a 22.91% CAGR through 2031.

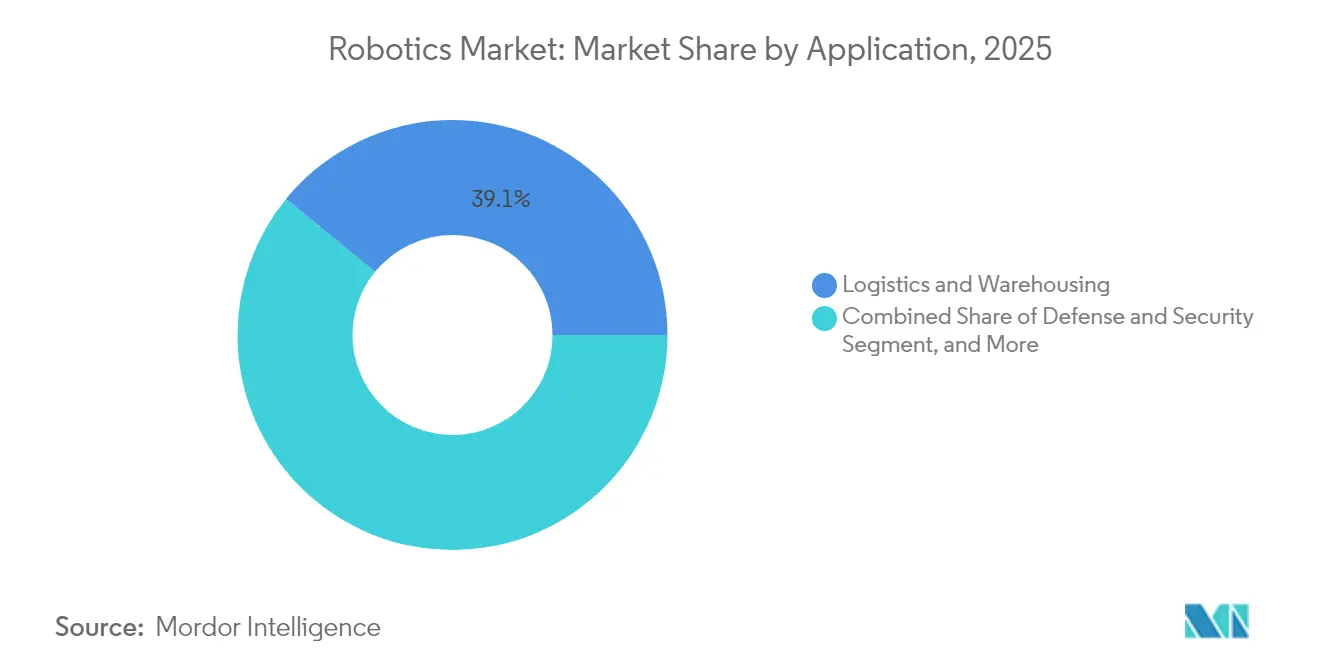

- By application, logistics and warehousing accounted for 39.10% share of the global robotics market size in 2025; medical and surgical robots are advancing at a 21.52% CAGR to 2031.

- By end-user industry, automotive held 28.78% share in 2025, whereas healthcare providers are forecast to expand at a 21.55% CAGR up to 2031.

- By geography, Asia-Pacific commanded 37.72% of the global robotics market share in 2025, while the Middle East registers the fastest expansion at a 21.31% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Robotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising labour-shortage led automation demand | +4.2% | Global, with acute impact in North America, Europe, Japan | Medium term (2-4 years) |

| Declining average robot price per functional hour | +3.8% | Global, particularly emerging markets in APAC and MEA | Short term (≤ 2 years) |

| Proliferation of low-code robot-programming platforms | +2.9% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Fiscal incentives for reshoring manufacturing in G-7 | +3.1% | North America, Europe, Japan | Long term (≥ 4 years) |

| Warehouse AMR roll-outs by e-commerce 3PLs | +3.7% | Global, concentrated in major e-commerce markets | Short term (≤ 2 years) |

| Nation-level humanoid R&D missions | +2.5% | China, Japan, South Korea, with spillover to global markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Labour-Shortage Led Automation Demand

Demographic headwinds in Japan, the United States, and much of Western Europe have shifted automation from cost-saving to capacity-assurance mode. Unfilled factory vacancies topped 2 million roles across G-7 manufacturing in 2024, while Japan’s robot density reached 399 units per 10,000 employees, the highest on record.[1]Asian Robotics Review, “Why So Little Robot Automation in America?,” asianroboticsreview.com Automakers such as Stellantis adopted human-centric robotic cells that trim repetitive strain injuries yet safeguard headcount, signalling a nuanced push toward collaborative deployment.[2]Wall Street Journal, “Robots Are Looking Better to Detroit as Labor Costs Rise,” wsj.com The global robotics market benefits because these structural gaps persist through economic cycles, giving vendors a predictable demand base that decouples from GDP volatility.

Declining Average Robot Price Per Functional Hour

Component commoditisation and scale production cut collaborative robot prices by roughly 15% a year post-2024, while software upgrades doubled performance relative to price.[3]Machinery Market, “Cobot market exceeds USD 1 billion in 2023,” machinery-market.co.uk Chinese suppliers even marketed entry-level humanoids at CNY 199,000 (USD 27,512), placing robots within small-factory capital budgets. As hardware costs slide, adoption curves steepen among small and emerging-market manufacturers, thereby widening the addressable pool for the global robotics market.

Proliferation of Low-Code Robot-Programming Platforms

Low-code interfaces built on Robot Operating System 2 now let domain specialists configure tasks via drag-and-drop tools or speech, compressing deployment cycles from months to weeks and slicing integration bills by roughly 40%. French developer Inbolt logged 70% faster go-lives at SME clients that previously lacked in-house automation engineers. The shift reallocates complexity from plant floors to cloud platforms, raising the software revenue pie within the global robotics market.

Fiscal Incentives for Reshoring Manufacturing in G-7

The USA CHIPS Act funnels USD 52 billion toward domestic semiconductor fabs that embed advanced robotics by mandate, while the EU dedicates 20% of its recovery fund to digital automation. Japan’s Society 5.0 programme grants accelerated depreciation on collaborative systems, prompting a 25% investment jump among enrolled firms. These policy levers inject counter-cyclical demand, sheltering the global robotics market from private-sector slowdowns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent SME integration skill-gap | -2.8% | Global, particularly acute in developing markets | Medium term (2-4 years) |

| Geopolitical export-control on advanced servos | -2.1% | Global, with concentrated impact on China-US trade | Short term (≤ 2 years) |

| Rare-earth magnet price volatility | -1.9% | Global, affecting high-performance robotics | Short term (≤ 2 years) |

| Cyber-security vulnerabilities in ROS deployments | -1.6% | Global, with higher impact in critical infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent SME Integration Skill-Gap

Sixty-eight percent of SMEs still lack engineering talent for robotics deployment, prolonging payback periods and dampening utilisation rates. Integrators cluster in urban hubs, leaving regional firms underserved. Without accelerated skills development or turnkey service models, the global robotics market leaves considerable latent demand untapped.

Geopolitical Export-Control on Advanced Servos

Tightened US chip rules and China’s rare-earth restrictions pushed servo prices up by 15-25% for some western buyers, prompting redesigns or dual-sourcing moves that slow roll-outs. The global robotics market absorbs higher input costs and buffers supply risk through localisation strategies, but near-term friction hampers smooth scaling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Robot Type: Collaborative Upswing Within Industrial Dominance

Industrial robots accounted for 71.04% of the global robotics market in 2025, riding sustained demand from high-throughput automotive and electronics assembly lines. Yet collaborative robots expand at a 25.64% CAGR to 2031, underpinned by safety-certified force-sensing and sub-USD 30,000 price tags that place them within SME budgets. This pivot signals that flexible, human-supervised cells, rather than fenced-off lines, will drive the next deployment wave of the global robotics market.

A surge in Chinese cobot makers lifted their domestic share from 35% to 73% between 2017 and 2024, heightening price competition and accelerating worldwide unit growth. Service-robot niches also flourish: surgical systems surpassed USD 4.18 billion in 2025, reaffirming healthcare as the fastest-rising end-use. This diversification reduces cyclicality for the global robotics market and cushions hardware vendors against single-sector downturns.

By Component: Hardware Leadership Shifts Toward Software Intelligence

Hardware still represented 63.12% of 2025 spending, but software revenue is set to grow 22.91% annually as artificial intelligence becomes the primary value driver. Higher-level control stacks now incorporate cloud analytics and reinforcement learning that deliver 25% faster cycle times with 20% lower electricity use on ABB’s OmniCore platform. The global robotics market size for subscription-based Robot-as-a-Service is projected to treble by 2031 as customers migrate from capital expenditure toward operating expenditure models.

Service revenues, covering integration, remote monitoring, and predictive maintenance, further solidify vendor lock-in. As a result, software and services blur, embedding update rights and cyber-security patches into multi-year contracts. This trend rewires profit pools and raises entry barriers for purely hardware-centric challengers within the global robotics market.

By Application: Logistics Leadership Meets Medical Momentum

E-commerce fulfilment hubs drove logistics and warehousing robots to 39.10% share in 2025, underpinned by autonomous mobile platforms that can be installed without layout overhauls. Meanwhile, medical and surgical systems record 21.52% CAGR thanks to evidence of shorter hospital stays and higher procedural precision compared with laparoscopic methods. The global robotics market size for surgical platforms is on track to hit USD 8.11 billion by 2031, indicating robust health-sector appetite.

Defence programmes, such as DARPA’s RACER Heavy autonomous vehicle, underscore rising demand for off-road and maritime unmanned systems, diversifying application risk. Cleaning and sanitation robots post 30% sales growth as hospitality chains standardise hygiene protocols. This breadth of use cases reinforces long-term momentum for the global robotics market.

By End-User Industry: Automotive Plateau vs Healthcare Surge

Automotive retained 28.78% share in 2025, yet its growth curve flattens as most paint, welding, and assembly lines already employ mature automation. In contrast, hospitals and outpatient centres, propelled by regulatory approvals and demographic necessity, exhibit 21.55% CAGR, positioning healthcare as the new frontier for global robotics market revenue.

Electronics and semiconductor players maintain steady robotics investments to preserve precision and clean-room compliance. Government grants worth JPY 5.15 billion (USD 46 million) to Fab projects in Japan further stimulate uptake. Food and beverage enterprises apply guided changeover modules that cut downtime by 70% and save USD 9,000 per month. This cross-sector mix diversifies cash flows for solution vendors inside the global robotics market.

Geography Analysis

Asia-Pacific secured 37.72% of global robotics market share in 2025, anchored by China’s 430,000 annual industrial-robot installations and two-thirds of worldwide robotics patent grants. Chinese factories integrate robots into lithium-ion battery and consumer-electronics lines, while domestic brands escalate exports, embedding regional cost competitiveness into the global robotics market. Japan posted JPY 180.2 billion (USD 1.64 billion) profit at Fanuc in 2024 on revived Chinese demand and domestic demographic pressure. South Korea’s USD 2.6 billion public-private programme channels humanoid expertise toward battery-plant automation, underscoring strategic prioritisation.

The Middle East registers the highest 21.31% CAGR to 2031 as sovereign wealth vehicles divert hydrocarbons surplus into industrial digitalisation, logistics, and healthcare robotics. Free-trade zones in the United Arab Emirates trial warehouse AMRs to service regional e-commerce flows, reducing over-reliance on seasonal migrant labour. National programmes additionally fund advanced manufacturing hubs that attract global integrators, amplifying the addressable base for the global robotics market.

North American demand remains resilient, propelled by CHIPS-Act-backed fabs and defence contracts such as the USD 642.2 million Navy counter-drone award to Anduril. Europe focuses on safe human–robot collaboration standards and sustainability targets, helped by EUR 69 million (USD 75 million) in annual German funding for artificial-intelligence integration. Both regions increasingly outsource commodity sub-assemblies to Asia while investing in high-value software and integration, reflecting a barbell strategy within the global robotics market.

Mordor Intelligence provides coverage of the robotics market across other key regional markets. Detailed country-level analysis extends to Indonesia incorporating local coverage and market participation, as required.

Regulatory Landscape

Robotics deployments are shaped mainly by machinery safety, workplace safety, and conformity assessment requirements, with additional considerations when AI-enabled control software is embedded in the system. In North America, OSHA guidance and the Nationally Recognized Testing Laboratory (NRTL) ecosystem influence how industrial robot cells are validated. In March 2026, OSHA expanded the scope of recognition for TUVRNA as an NRTL, reinforcing the third-party certification pathways that robot OEMs, integrators, and end users reference when specifying compliant equipment.

In Europe, compliance is increasingly anchored in sector-specific product safety frameworks such as the EU Machinery Regulation (EU) 2023/1230, alongside the EU AI Act, with policy work continuing to reduce overlap for high-risk AI embedded in machinery. Canada also relies on standards-led requirements for industrial robots, with CSA Z434-2026 aligning to ISO 10218-1:2025 and ISO 10218-2:2025 (with Canadian deviations), which affects cell design, safeguarding, and validation in manufacturing and logistics installations. In Asia, national robotics promotion laws continue to shape deployment conditions; South Korea continues to implement the Intelligent Robots Development and Distribution Promotion Act, with enforcement decree updates recorded in 2025.

Value Chain Analysis

The robotics value chain includes upstream components (servo drives and motors, bearings and precision castings, sensors and vision modules, semiconductors, cables, and batteries for mobile platforms), midstream robot manufacturing (mechanical structure, actuation, controllers, safety functions, and factory acceptance testing), and downstream integration and lifecycle services (cell design, end-of-arm tooling, simulation and digital twin work, fleet and workflow software for AMRs, commissioning, training, and maintenance). Revenue capture is shifting toward software intelligence and data-driven optimization, especially in perception, orchestration, and low-code programming layers that shorten deployment time and support recurring service models.

Supply constraints increasingly come from mechanical component availability and supplier qualification rather than software readiness, which makes dual sourcing and regionalization more central to scale-up plans. Vendor activity also shows manufacturers moving upstream through supply-chain partnerships tied to end markets. For example, Apptronik and Jabil (February 2025) collaborated to scale Apollo humanoid production and deploy units in manufacturing operations, while Robust.AI partnered with Foxconn (May 2025) to scale manufacturing of its Carter warehouse robots. Trade tensions and tariffs also reinforce localized production footprints and diversified procurement for semiconductors, sensors, and batteries, while system integrators and RaaS providers bundle hardware, software, and uptime-linked services for logistics and warehousing buyers.

Competitive Landscape

The global robotics market remains moderately fragmented, with top players dominating specific niches yet facing vigorous challenge from focused entrants. Japanese and European incumbents such as Fanuc, ABB, and KUKA continue to control high-payload industrial segments via proprietary servo technology and worldwide service reach. Chinese vendors, aided by scale and state backing, undercut hardware prices and now hold 73% of the domestic cobot market, accelerating export ambitions.

Strategically, leading firms pursue vertical integration and software stacking to defend margins. ABB intends to spin off its robotics division, estimated at USD 2.3 billion 2024 revenue, to unlock balance-sheet flexibility for aggressive acquisition of AI software assets. Fanuc boosts cloud analytics through partnerships to broaden recurring revenue. Meanwhile, service-robot disruptors such as Locus Robotics leverage Robot-as-a-Service contracts to lower customer entry barriers and capture long-run annuity streams, eroding incumbents’ traditional product-sale foothold.

Specialists exploit white-space in medical, defence, and sanitation robots where domain complexity and regulatory burden create protective moats. Intuitive Surgical deepens hospital stickiness through procedural analytics, while Anduril secures multi-year defence contracts that require sovereign-grade cyber-security. Cyber-risk mitigation services and integration consultancies thus emerge as high-margin adjuncts, adding layers of competitiveness to the global robotics market.

Robotics Industry Leaders

Yaskawa Electric Corporation

Denso Corporation

Fanuc Corporation

ABB Ltd.

KUKA AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity is supply-chain localization and capacity additions that shorten lead times for industrial and collaborative robots in North America and Europe, supporting reshoring-linked demand and reducing exposure to cross-border component friction. In 2026, FANUC America announced a USD 90 million investment for an 840,000-square-foot facility in Michigan to expand domestic robot manufacturing capacity. Yaskawa also advanced several footprint moves, including a tax-increment financing district tied to a USD 182 million expansion in Franklin, Wisconsin (April 2026), and a new robotics distribution center and production facility in Kocevje, Slovenia with a USD 31 million investment (July 2026). These actions create whitespace for local system integrators, safety validation partners, and component suppliers to qualify to new regional plants.

Another opportunity is the shift from one-time hardware sales toward software, data infrastructure, and subscription delivery models that reduce integration effort for SMEs. The supporting evidence includes the market-wide move toward low-code platforms and AI-based control stacks, which is already reshaping deployment cycles, and the growing use of Robot-as-a-Service in AMR-heavy logistics workflows where buyers procure uptime and throughput outcomes rather than standalone units. Humanoid and general-purpose robot manufacturing scale-up also supports adjacent demand in testing, certification, and application-layer software, including EngineAI opening a 129,000-square-foot smart factory in Shenzhen (May 2026) and AMC Robotics leasing a 6,150-square-meter manufacturing facility in Bac Ninh, Vietnam (June 2026) for robotic arm production.

Recent Industry Developments

- June 2026: Yaskawa Electric Corporation confirmed full-scale operations for Robot Factory No. 5 in Japan and highlighted efforts to accelerate the start-up of its US flagship facility by FY2027 for small-sized models and collaborative robots. The combination of integrated motor and robot production and added capacity supports lead-time reduction and more resilient supply for high-volume industrial and cobot programs.

- May 2025: ABB announced a plan to list its Robotics division by Q2 2026 to separate the automation business and sharpen strategic focus for investors. A standalone structure increases flexibility for portfolio actions around software and AI control stacks that are becoming central to differentiation beyond hardware platforms.

- March 2024: ABB launched OmniCore, a new generation controller platform positioned to improve motion performance and energy efficiency across supported robot families. The controller refresh strengthens the software and controls layer in the installed base, giving integrators a clearer upgrade path and enabling more advanced application programming and connected maintenance services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the robotics market is defined as the revenue generated from industrial and service robot platforms that are sold or deployed for work in factories, logistics sites, healthcare settings, defense use, and consumer environments, counted on a USD value basis.

Scope exclusions: We exclude adjacent automation items that are typically priced and bought separately, such as standalone sensors, generic software licenses, and non-robot industrial machinery when it is not part of a robot system sale.

Segmentation Overview

- By Robot Type

- Industrial Robots

- Service Robots

- Collaborative (Cobots)

- Mobile/AMR

- By Component

- Hardware

- Software

- Services (Integration, RaaS)

- By Application

- Manufacturing and Assembly

- Logistics and Warehousing

- Medical and Surgical

- Defense and Security

- Inspection and Maintenance

- Cleaning and Sanitation

- By End-User Industry

- Automotive

- Electronics and Semiconductor

- Food and Beverage

- Healthcare Providers

- Military and Defense

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the market and to anchor key demand signals that correlate with robotics spending. We leaned on public and official data series such as IFR publications, ISO standards references, UN Comtrade trade statistics, World Bank and OECD industry indicators, and selected peer reviewed papers that discuss robot density and deployment patterns.

In parallel, we reviewed company filings and investor presentations to map revenue mix, directional product pricing, and regional exposure. To cross-check adoption timing and policy or program changes, we also reviewed reputable press and association websites. For spot checks, a paid subscription covering company financials and another covering shipment-level trade flows were used to cross verify a few revenue and volume assumptions. The sources listed here are illustrative only, and many other public and paid references were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what is actually counted as robotics revenue in purchase cycles, then stress testing our pricing and volume assumptions across industrial and service use cases. We spoke with a mix of robot OEM and component ecosystem contacts, system integrators, distributors, and large end users across APAC, EMEA, and the Americas, so gaps from desk research could be closed and assumptions triangulated against field reality.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 21% | APAC: 50% |

| Mid tier: 46% | Functional/Unit leaders: 32% | EMEA: 31% |

| Smaller Players: 22% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic. We first used macro deployment and production signals to reconstruct the demand pool, then checked it against supplier-side reality.

On the top-down side, indicators such as industrial production trends, robot installation momentum, manufacturing capex direction, warehouse automation adoption, and healthcare procedure volumes were translated into an addressable robotics spend path by region.

That total was corroborated through selective bottom-up approximations, using sampled average selling price (ASP) ranges by robot category, typical order sizes for high volume buyers, and channel checks on service and integration attach rates. Where a direct datapoint was missing for a smaller country or niche application, the gap was handled using proxy ratios such as robot density, wage inflation pressure, and end user mix, and then normalized using interview feedback.

Forecasting relied on scenario analysis supported by variable-level outlook inputs from experts, since robotics demand can swing with factory cycles and logistics investment timing. In the model, ASP logic was updated using observed pricing direction by robot type and component cost trends, and adoption rates were adjusted based on practical constraints such as deployment lead times and integration capacity.

Data Validation & Update Cycle

Outputs were validated by comparing modeled totals with independent signals such as reported installation trends, trade flows for key robot categories, and the implied spend per facility in major end user groups. Any large variances were reviewed step by step, and assumptions were revisited until the driver-level math and the market narrative aligned.

Before sign-off, the work went through internal analyst reviews, and follow-up calls were triggered when a price, volume, or regional split looked out of pattern. The report is refreshed annually, and interim updates are made when material events affect demand, supply, or pricing, followed by a final pre-delivery pass so the numbers reflect the latest available information.

Mordor Intelligence's Robotics Market Estimate Compared With Other Published Estimates

Published robotics market values often look far apart, even when the topic name is the same, because the refresh date, currency timing, and pricing assumptions can shift the final USD total. Differences also come from what is counted as robotics revenue, especially when integration, software, and service contracts are treated inconsistently.

The key gap drivers in robotics tend to be ASP progression methods (for example, mixing premium medical systems with high volume industrial units without a clear weighting) and uneven validation of volume signals such as installations, shipment patterns, or end user deployment cycles. In this report, the refresh cadence and currency conversion timing are held consistent within the forecast window, and the ASP checks are re-run when new pricing or mix signals appear, which explains part of the spread seen versus other figures, a process applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 88.27 B (2026) | |

| Global Consultancy A | USD 61.90 B (2025) | This estimate uses a different base year and a broader headline scope that is not clearly tied to robot type mix, which can compress or expand the total depending on how service and integration revenues are blended and how currency timing is handled. |

| Trade Journal B | USD 28.40 B (2025) | This figure appears closer to a narrower revenue pool that likely emphasizes selected robot categories, and it also reads like a snapshot that may not fully normalize ASP differences across industrial and service platforms or reconcile results against installation and trade signals. |

Looking at the three numbers together, the spread is best explained by scope boundaries, base year choice, and how pricing is carried forward across mixed robot categories. By keeping the inputs traceable to observable demand indicators and by re-checking pricing and mix assumptions during updates, the estimate stays easier to reproduce and compare over time.

Key Questions Answered in the Report

What is the current size of the global robotics market?

The global robotics market stands at USD 88.27 billion in 2026 and is projected to reach USD 218.56 billion by 2031 at a 19.86% CAGR.

Which segment is growing the fastest in the global robotics market?

Collaborative robots show the highest growth, expanding at a 25.64% CAGR through 2031 as safety features, low costs, and ease of programming attract SMEs.

Which region will record the quickest expansion?

The Middle East leads regional growth at a 21.31% CAGR on the back of sovereign-fund automation investments and logistics-hub developments.

Why is software becoming more important than hardware?

Artificial-intelligence control, cloud connectivity, and Robot-as-a-Service contracts deliver performance and continuous updates, shifting value capture to software and recurring services.

What are the biggest barriers for small manufacturers?

Skill shortages in integration and programming, alongside cybersecurity risk and component-supply friction, slow adoption among SMEs despite lower hardware prices.

How fragmented is the vendor landscape?

Top five manufacturers hold around 55% of revenue, indicating moderate concentration; niche entrants thrive in healthcare, defence, and service-robot applications.

Page last updated on: