Robotic Software Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

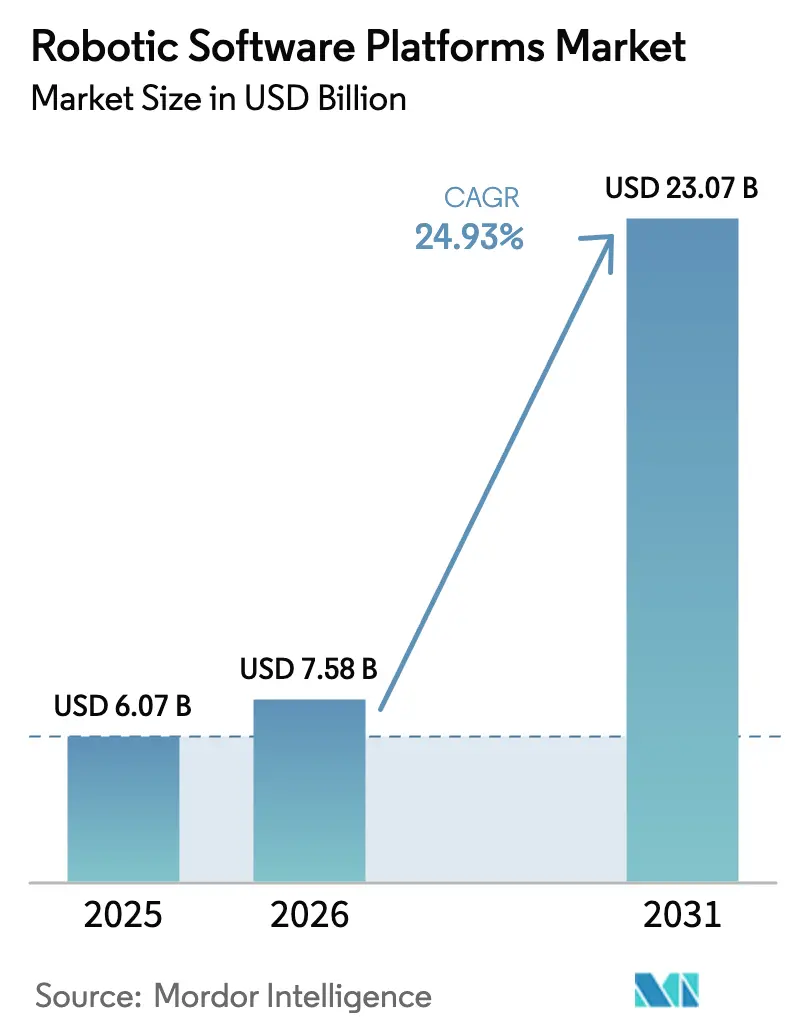

| Market Size (2026) | USD 7.58 Billion |

| Market Size (2031) | USD 23.07 Billion |

| Growth Rate (2026 - 2031) | 24.93% CAGR |

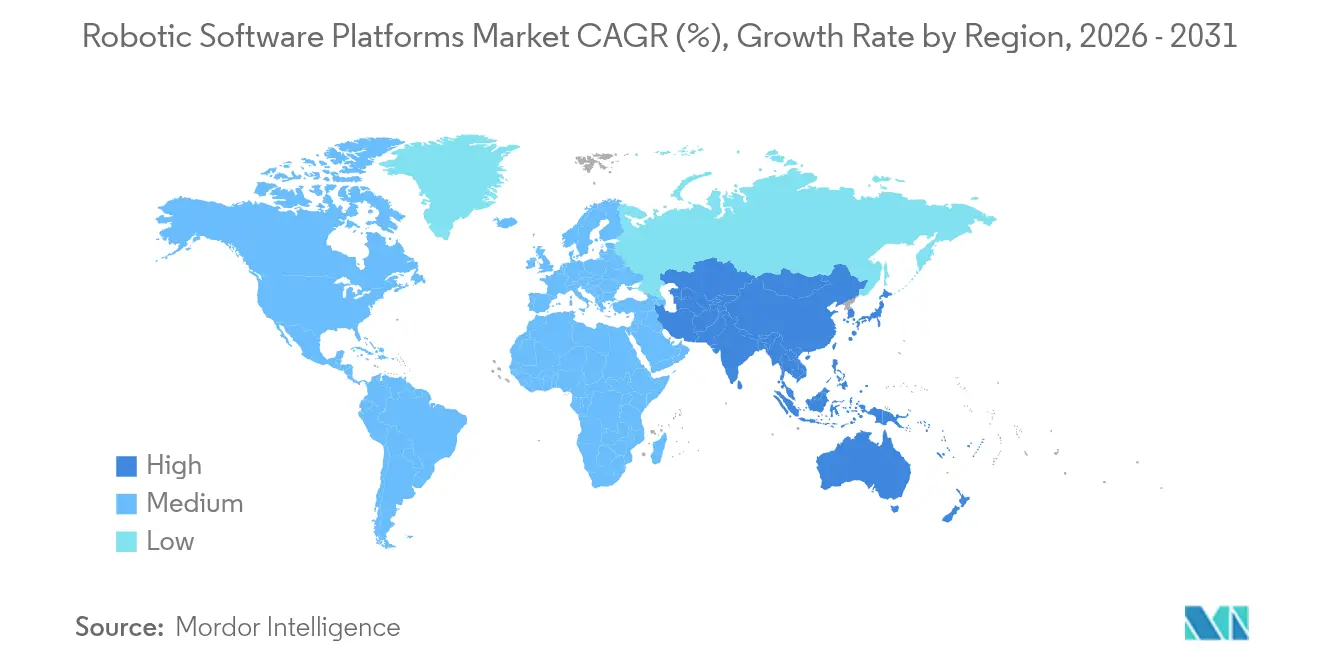

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

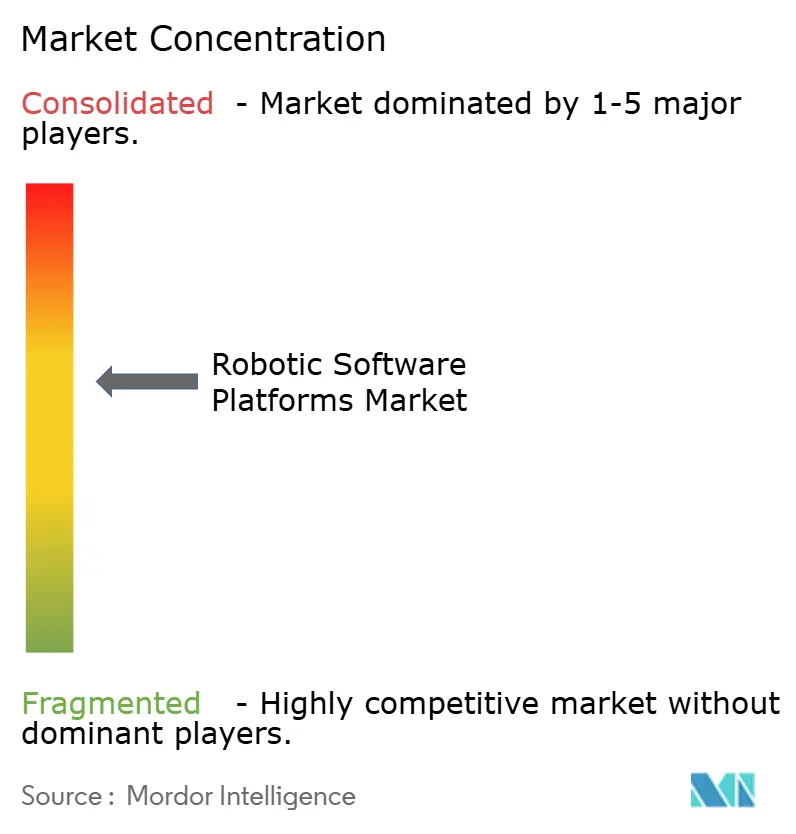

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotic Software Platforms Market Analysis by Mordor Intelligence

The Robotic Software Platforms Market size was valued at USD 6.07 billion in 2025 and estimated to grow from USD 7.58 billion in 2026 to reach USD 23.07 billion by 2031, at a CAGR of 24.93% during the forecast period (2026-2031).

Surging demand stems from enterprises shifting focus from hardware to intelligent code that enables adaptive automation, while generative AI compresses robot-deployment cycles from months to weeks. Industrial-edge AI brings sub-millisecond decision-making on the factory floor, supporting latency-sensitive tasks without constant cloud connectivity. Governments further accelerate uptake, with the US Advanced Manufacturing Investment Credit offering 25% relief on software that modernizes production. Yet legacy industrial protocols and rising vision-AI licensing fees inhibit seamless integration, especially in brownfield sites where equipment dating back decades remains indispensable. [1]Internal Revenue Service, “Inflation Reduction Act—Advanced Manufacturing Investment Credit,” irs.gov

Key Report Takeaways

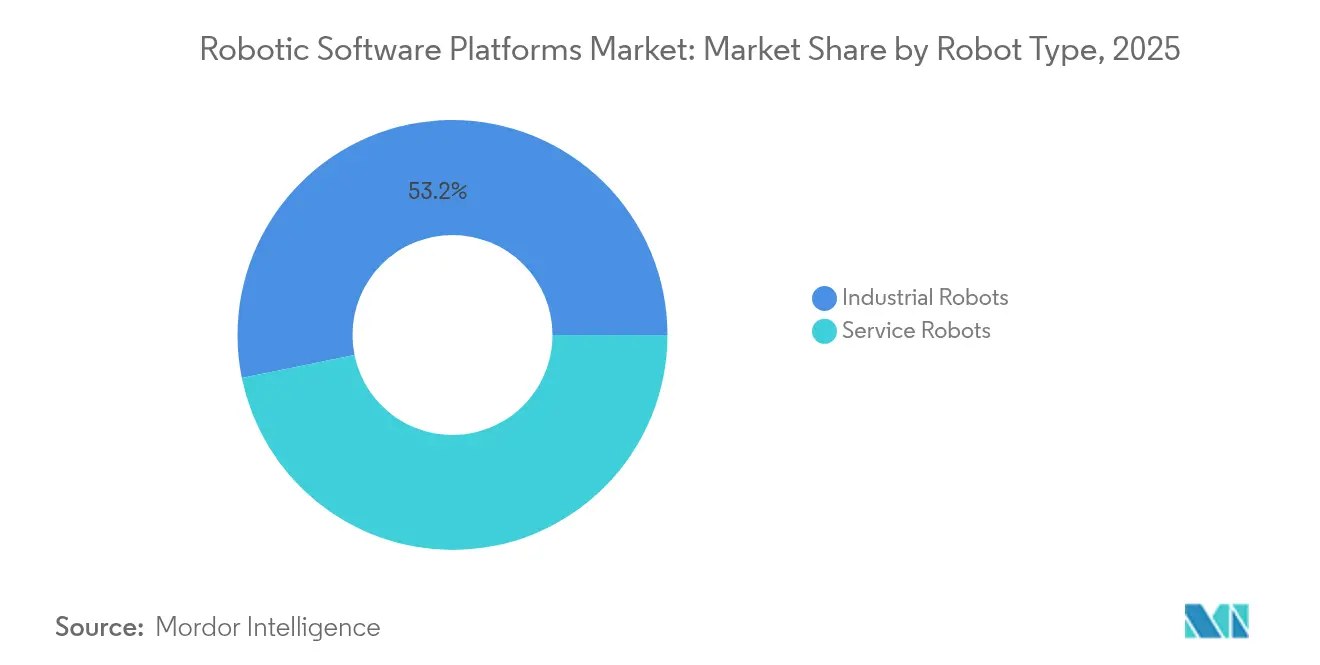

- By robot type, industrial robots commanded 53.20% of the robotic software platforms market share in 2025, while service robots are expanding at a 30.10% CAGR through 2031.

- By software type, simulation and digital-twin tools held 26.50% revenue share of the robotic software platforms market size in 2025; predictive-maintenance platforms lead growth at 31.60% CAGR to 2031.

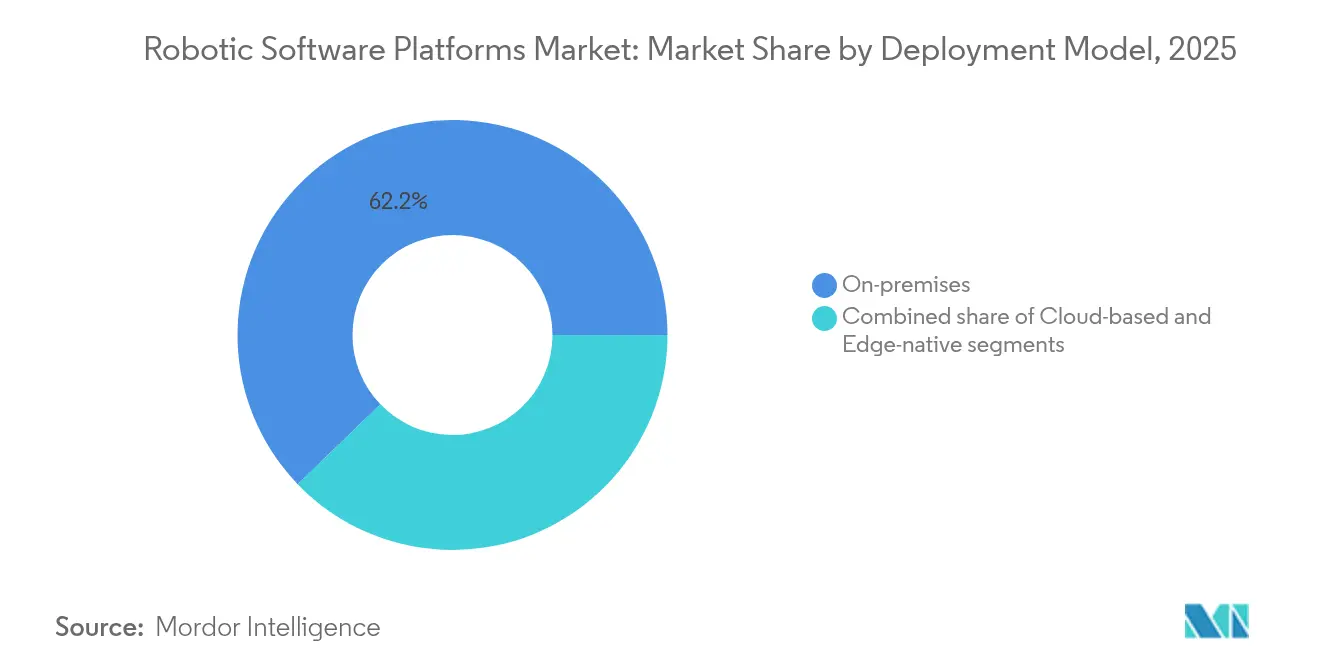

- By deployment model, on-premises installations accounted for a 62.20% share of the robotic software platforms market size in 2025, whereas cloud deployments recorded the fastest 34.10% CAGR through 2031.

- By end-user industry, automotive captured 23.60% of the robotic software platforms market share in 2025, yet healthcare applications are forecast to rise at a 28.80% CAGR to 2031.

- By geography, APAC led with 40.70% revenue share in 2025 and is projected to grow at a 30.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Robotic Software Platforms Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated low-code robot programming tools | +4.20% | Global, with early adoption in North America and EU | Short term (≤ 2 years) |

| Industrial-edge AI enabling on-device autonomy | +6.80% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Collaborative-robot safety certifications harmonising globally | +3.10% | Global, led by EU regulatory framework | Medium term (2-4 years) |

| Robot-as-a-Service uptake among SMEs | +5.40% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Government tax credits for smart-factory software | +2.90% | National, with concentration in US, Germany, China | Short term (≤ 2 years) |

| Cyber-physical security mandates for critical infrastructure robots | +3.70% | Global, with stringent requirements in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Low-Code Robot Programming Tools

Drag-and-drop and natural-language interfaces cut robot programming time by up to 80%, as illustrated by ABB AppStudio’s 2025 launch. The democratization addresses the 2.1 million manufacturing-talent gaps projected for 2030. Mid-market manufacturers gain affordability because fewer specialist engineers are needed. Faster configuration lowers payback periods, enabling robots to handle high-mix, low-volume tasks that once lacked economic justification. Vendors embedding reusable code blocks further shrink commissioning labour. Consequently, low-code capability becomes a must-have feature when buyers shortlist robotic software platforms market offerings. [2]ABB Group, “ABB AppStudio Launch 2025,” global.abb

Industrial-Edge AI Enabling On-Device Autonomy

Shifting inference from cloud to robot improves latency, privacy, and reliability in safety-critical settings such as welding cells that require sub-10 ms reaction windows. NVIDIA’s Isaac platform adoption by Siemens and BYD Electronics reflects mainstream deployment of edge GPUs for perception and path planning. Reduced bandwidth costs help plants in regions with unstable connectivity. Edge AI also supports redundant fail-safe operation during network outages, aligning with insurance requirements for continuous production. As 5G networks mature, edge nodes gain deterministic wireless links, further broadening use cases for adaptive mobile robots inside the robotic software platforms market.

Collaborative-Robot Safety Certifications Harmonizing Globally

Convergence of ISO 3691-4 and ANSI/RIA R15.08 lets vendors design once and sell worldwide, lowering certification overhead. UL Solutions reports growing demand for functional-safety assessments targeting SIL 3 performance. Unified standards also reassure buyers that cobots can work beside staff without cages, driving deployments in food, cosmetics, and electronics assembly. Harmonization accelerates software innovation in dynamic speed and separation monitoring. Improved safety boosts worker acceptance, a soft factor that still decides project approvals in many facilities.

Robot-as-a-Service Uptake Among SMEs

Subscription models eliminate capital-budget barriers, letting SMEs pay per operating hour rather than purchase hardware outright. The RaaS market is projected to reach USD 34 billion by 2026. Brain Corp reports its fleet has covered 250 billion ft², evidencing scale-up under usage-based billing. Providers handle maintenance and software updates, relieving customers of technical complexity. Access to advanced capabilities levels the playing field between small workshops and multinationals, expanding the addressable base of the robotic software platforms market.

Restraints Impact Analysis of Robotic Software Platforms Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy industrial protocols slowing data interoperability | -3.80% | Global, with acute challenges in North America and EU brownfield sites | Medium term (2-4 years) |

| Scarcity of ROS2-skilled engineers | -4.60% | Global, with particular shortages in APAC and North America | Long term (≥ 4 years) |

| Escalating licence costs for vision-AI IP cores | -2.90% | Global, with higher impact on SMEs and emerging market players | Short term (≤ 2 years) |

| Pending EU AI Act liability exposure for autonomous systems | -3.20% | EU core, with spillover effects on global robotics vendors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy Industrial Protocols Slowing Data Interoperability

Modbus, Profibus, and proprietary fieldbuses remain entrenched in decades-old equipment, impeding plug-and-play connectivity with OPC UA and other modern frameworks. Integration often needs protocol gateways that add latency, cost, and maintenance overhead. Plants juggling multiple vendor ecosystems struggle to maintain version parity across controllers. Time-Sensitive Networking promises help, yet its maturity and price keep many firms in pilot mode. Consequently, brownfield sites experience elongated project schedules and higher integration risk, slowing overall robotic software platforms market adoption.

Scarcity of ROS2-Skilled Engineers

ROS2 delivers real-time performance and enhanced security, but the talent pool remains limited. Universities only began updating curricula in 2024, creating a lag that recruiters feel today. Salaries for senior ROS2 developers exceed USD 180,000, inflating project budgets. Platform abstractions like Wind River’s VxWorks integration alleviate some complexity but cannot fully replace deep ROS2 expertise. The shortage is most pronounced in APAC where rapid robot deployment outpaces local workforce development, restraining the robotic software platforms market. [3]RoboticsTomorrow, “ROS2 Talent Shortage,” roboticstomorrow.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Robotic Software Platforms Market Segment Analysis

By Robot Type:

Service Robots Outpace Industrial SystemsIndustrial robots retained 53.20% share of the robotic software platforms market in 2025 because automotive and electronics plants run thousands of articulated arms on deterministic code. However, service robots register a 30.10% CAGR through 2031, far ahead of traditional counterparts. Hospitals expand surgical-assistant fleets, while retailers deploy inventory-scanning units to trim stock-out losses. Johns Hopkins researchers trained surgical robots to learn tasks by watching videos, illustrating how AI deepens software differentiation. Meanwhile, automotive players such as BMW pilot humanoid robots for in-plant logistics, demonstrating convergence between service and industrial paradigms.

Service-robot momentum underscores the value of adaptive perception and human-interaction algorithms versus rigid motion paths. Healthcare buyers rank system intelligence over payload capacity, tilting budgets toward platforms that update continuously via cloud pipelines. Industrial buyers respond by requesting similar capabilities like self-optimizing weld paths. The robotic software platforms market thus shifts toward unified platforms that can support both high-volume manufacturing and low-volume service environments.

By Software Type:

Predictive Maintenance AcceleratesSimulation and digital-twin packages held a 26.50% slice of the robotic software platforms market size in 2025 because they de-risk cell layouts before hardware purchase. Yet predictive-maintenance suites are achieving a 31.60% CAGR through 2031 as downtime avoidance proves a quantifiable benefit. Integrating vibration, temperature, and current sensors into AI models lets operators service robot before failure, extending mean time between repair by 15% on average.

Vendors now bundle AI-powered twins that generate synthetic data to improve fault-detection accuracy. Coupling maintenance insights with spare-parts logistics optimizes warehouse stock levels, delivering cross-functional savings. Escalating licensing fees for proprietary vision IP squeeze margins, prompting software houses to develop open-source or home-grown models. Edge-native inference further shifts value from centralized analytics toward on-device diagnosis. These dynamics reinforce predictive maintenance as the fastest-growing slice of the robotic software platforms market.

By Deployment Model:

Cloud Gains on On-Premises DominanceOn-premises solutions commanded 62.20% of the robotic software platforms market size in 2025, driven by deterministic-control requirements. However, cloud deployments grow at 34.10% CAGR through 2031 as enterprises pursue continuous feature delivery and fleet-level optimization. Vendors now offer hybrid stacks where safety-critical loops run locally, while analytics offload to elastic cloud compute.

CISA guidelines classify robot controllers as OT assets, steering critical-infrastructure operators to edge-native models for security and latency. Meanwhile, mid-tier manufacturers adopt cloud-only offerings to avoid CapEx on servers and redundant power. The net effect is a widening spectrum of deployment choices that customers tailor to process criticality, cementing hybrid frameworks as the mainstream architecture within the robotic software platforms market.

By End-User Industry:

Healthcare Leads GrowthAutomotive held 23.60% of the robotic software platforms market share in 2025, thanks to long-running applications such as welding, painting, and final assembly. Healthcare, though smaller, posts a 28.80% CAGR to 2031, buoyed by aging populations and rising demand for minimally invasive surgery. Surgeons rely on AI guidance for suture placement and tissue classification, pushing vendors to integrate vision and haptic feedback modules.

Telesurgery via 5G expands specialist access in rural regions, while hospitals implement robotic ward assistants for supply delivery. Logistics operators adopt autonomous mobile robots to handle e-commerce peaks, reflecting cross-industry spillovers. Agriculture and food processing eye wash-down compliant robots to counter labour shortages. These diverse use cases highlight how vertical specializations shape purchasing criteria, yet all share a dependency on scalable, secure, and updateable software, reinforcing growth momentum in the robotic software platforms market.

Geography Analysis

APAC Robotic Software Platforms Market

APAC generated 40.70% of global revenue in 2025 and is set to expand at a 30.60% CAGR through 2031, underscoring its manufacturing concentration. China’s USD 138 billion robotic investment pledge catalyses local supplier ecosystems, while Japan and South Korea invest in service robotic for eldercare. Local governments subsidize automation for small exporters, broadening the robotic software platforms market footprint across tier-two cities.

North America Robotic Software Platforms Market

North America benefits from generous tax credits and robust venture funding for AI-native startups. Early adoption of edge architectures supports deployments in automotive, aerospace, and fulfilment centers. Regulatory clarity on collaborative-robot safety gives integrators a stable framework to scale solutions. Canada’s warehouses deploy fleet-management software that optimizes battery utilization and aisle navigation, evidence of cross-border knowledge transfer.

EMEA and LATAM Robotic Software Platforms Market

Europe enforces the AI Act, classifying industrial robots as high-risk systems that must document data provenance and explainability. Compliance adds workload yet raises trust, which local suppliers leverage when exporting to stricter jurisdictions. Central and Eastern European plants modernize to counter labour shortages, while Scandinavian hospitals adopt rehabilitation robots. Emerging markets in Latin America, the Middle East, and Africa adopt RaaS models that bypass capital constraints, slowly diversifying regional demand streams for the robotic software platforms market.

Competitive Landscape

The robotic software platforms market is moderately fragmented, with no vendor covering the whole stack from perception to enterprise orchestration. ABB, KUKA, and FANUC embed tight hardware integration yet accelerate software roadmaps via acquisitions of AI startups. ABB’s 2025 plan to list its robotic unit reflects the strategic value of standalone software revenues.

NVIDIA and Samsung invested USD 35 million in Skild AI, signalling chipmakers’ commitment to build developer ecosystems that sit atop GPU hardware. KUKA enhances its Sunrise.OS with adaptive-path modules learned from cloud training, while FANUC’s ROBOGUIDE v10 adds VR-based offline programming to shorten commissioning. Universal Robots focuses on plug-and-produce APIs that align with SMEs needing rapid deployment.

Startups specializing in natural-language coding, autonomous learning, and edge-native perception secure funding by promising faster ROI. System integrators monetize middleware that bridges ROS2 with legacy PLC networks. Large integrators pursue platform consolidation to simplify sourcing for global manufacturers. Overall, supplier strategies converge on lowering time-to-value and simplifying updates, themes that will shape competitive dynamics in the robotic software platforms market through 2030.

Robotic Software Platforms Industry Leaders

ABB Ltd.

Fanuc Corporation

NVIDIA Corporation

International Business Machines Corporation (IBM)

Brain Corporation

- *Disclaimer: Major Players sorted in no particular order

Robotic Software Platforms Market Companies Covered in this Report

- ABB Ltd.

- AIBrain Inc.

- Brain Corp.

- CloudMinds Technology Inc.

- Cyberbotics Ltd.

- Energid Technologies Corp.

- Fanuc Corp.

- Furhat Robotics AB

- International Business Machines Corp.

- iRobot Corp.

- KUKA AG

- NVIDIA Corp.

- Neurala Inc.

- Realtime Robotics Inc.

- ADLINK Technology Inc.

- Robotic Systems Integration LLC

Recent Industry Developments in Robotic Software Platforms Market

- June 2025: NVIDIA and Samsung invested USD 35 million in Skild AI, valuing the startup at USD 4.5 billion

- May 2025: FANUC released ROBOGUIDE v10 with 64-bit architecture and VR simulation.

- April 2025: ABB announced plans to spin off its robotics division as a public company in 2026.

- March 2025: Mercedes-Benz deployed Apptronik Apollo humanoids for material handling at its Berlin-Marienfelde plant.

Global Robotic Software Platforms Market Report Scope

Robot software is a collection of programmed commands or instructions that inform a mechanical device and an electrical system, known as a robot, what tasks to perform. Robot software is used to perform autonomous activities.

The Robotic Software Platforms Market is segmented by robot type (industrial robots and service robots), by software type (communication management software, data management and analysis software, predictive maintenance software, recognition software, and simulation software), by end-user (automotive, retail and e-commerce, government and defense, healthcare, transportation and logistics, manufacturing, IT and telecommunications, and other end-users verticals) and by geography (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa).

The market sizes and forecasts are in terms of value (USD) for all the above segments.

Segmentation Overview

| Industrial Robots |

| Service Robots |

| Communication Management |

| Data Management and Analytics |

| Predictive Maintenance |

| Recognition / Vision |

| Simulation and Digital Twin |

| On-premises |

| Cloud-based |

| Edge-native |

| Automotive |

| Transportation and Logistics |

| Healthcare |

| Retail and E-commerce |

| Manufacturing (Discrete and Process) |

| Government and Defense |

| ICT and Data-Centers |

| Other Verticals |

| North America | United States | |

| Canada | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Robot Type | Industrial Robots | ||

| Service Robots | |||

| By Software Type | Communication Management | ||

| Data Management and Analytics | |||

| Predictive Maintenance | |||

| Recognition / Vision | |||

| Simulation and Digital Twin | |||

| By Deployment Model | On-premises | ||

| Cloud-based | |||

| Edge-native | |||

| By End-User Industry | Automotive | ||

| Transportation and Logistics | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Manufacturing (Discrete and Process) | |||

| Government and Defense | |||

| ICT and Data-Centers | |||

| Other Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the value of the Robotic software platforms market today and how fast is it growing?

The market stands at USD 7.58 billion in 2026 and is projected to reach USD 23.07 billion by 2031, reflecting a robust 24.93% CAGR.

Which region offers the strongest growth potential for robotic software?

APAC commands 40.70% of 2025 revenue and is forecast to expand at a 30.60% CAGR through 2031, driven by large-scale investments in China, Japan, and South Korea.

What robot category is growing fastest in software demand?

Service robots post the highest 30.10% CAGR to 2031, fueled by healthcare, retail, and hospitality applications, even though industrial robots still hold the largest installed base.

Which software segment is set to outperform others?

Predictive-maintenance platforms lead growth at a 31.60% CAGR because manufacturers prioritize uptime savings over design-phase simulation benefits.

How are deployment models shifting?

Cloud-based deployments grow at 34.10% CAGR as firms seek rapid updates and fleet-level analytics, while hybrid edge architectures handle safety-critical control on-site for latency and security.

What competitive dynamics should executives watch?

The field is moderately fragmented; incumbents like ABB, KUKA, and FANUC increasingly acquire AI-native startups, while chip leaders such as NVIDIA back software specialists to gain ecosystem influence.

Page last updated on: