Humanoids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

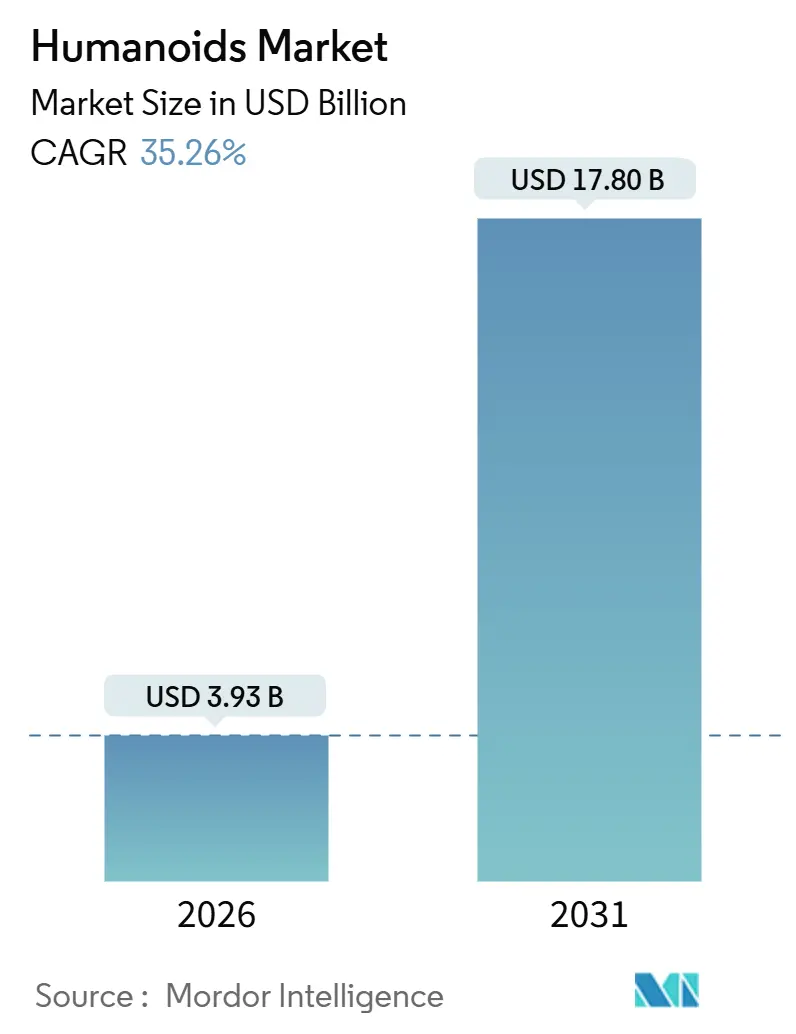

| Market Size (2026) | USD 3.93 Billion |

| Market Size (2031) | USD 17.80 Billion |

| Growth Rate (2026 - 2031) | 35.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Humanoids Market Analysis by Mordor Intelligence

The Humanoids Market size is estimated at USD 3.93 billion in 2026, and is expected to reach USD 17.80 billion by 2031, at a CAGR of 35.26% during the forecast period (2026-2031).

Rapid cost declines in artificial intelligence hardware, demographic ageing in the G7 and China, and widening industrial labour gaps are converging to push humanoid robots from pilot projects to core operational assets across healthcare, manufacturing, and logistics. Venture investment flows exceeding USD 4 billion in 2024–2025, together with China’s and South Korea’s “Humanoid 2025” policies, are accelerating time-to-market for new platforms. Enterprises are prioritising human-scale form factors capable of using existing tools and infrastructure, while software advances turn once-static machines into adaptable co-workers. As these factors reinforce each other, the humanoids market is becoming a pivotal solution for countries seeking productivity gains without expanding their human workforce.

Key Report Takeaways

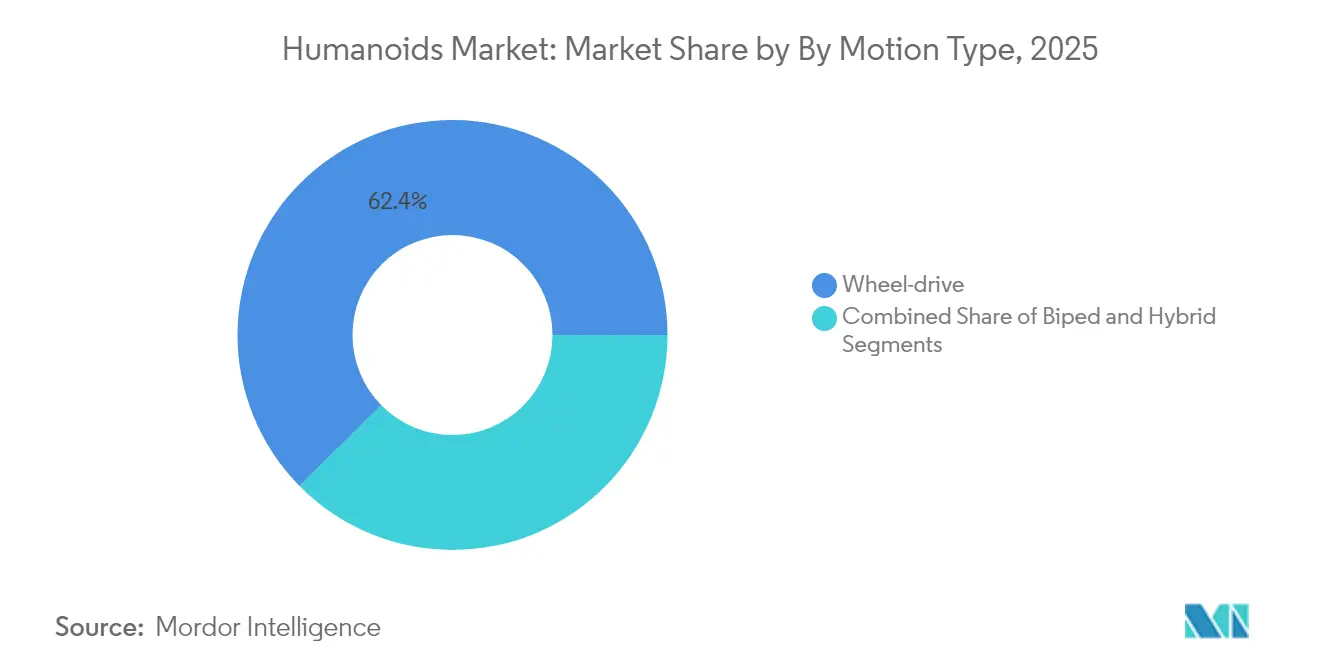

- By motion type, wheel-drive robots held 62.40% of the humanoids market share in 2025, while biped systems are projected to grow at a 57.1% CAGR to 2031.

- By component, hardware accounted for 67.20% share of the humanoids market size in 2025; software is on track for a 55.9% CAGR through 2031.

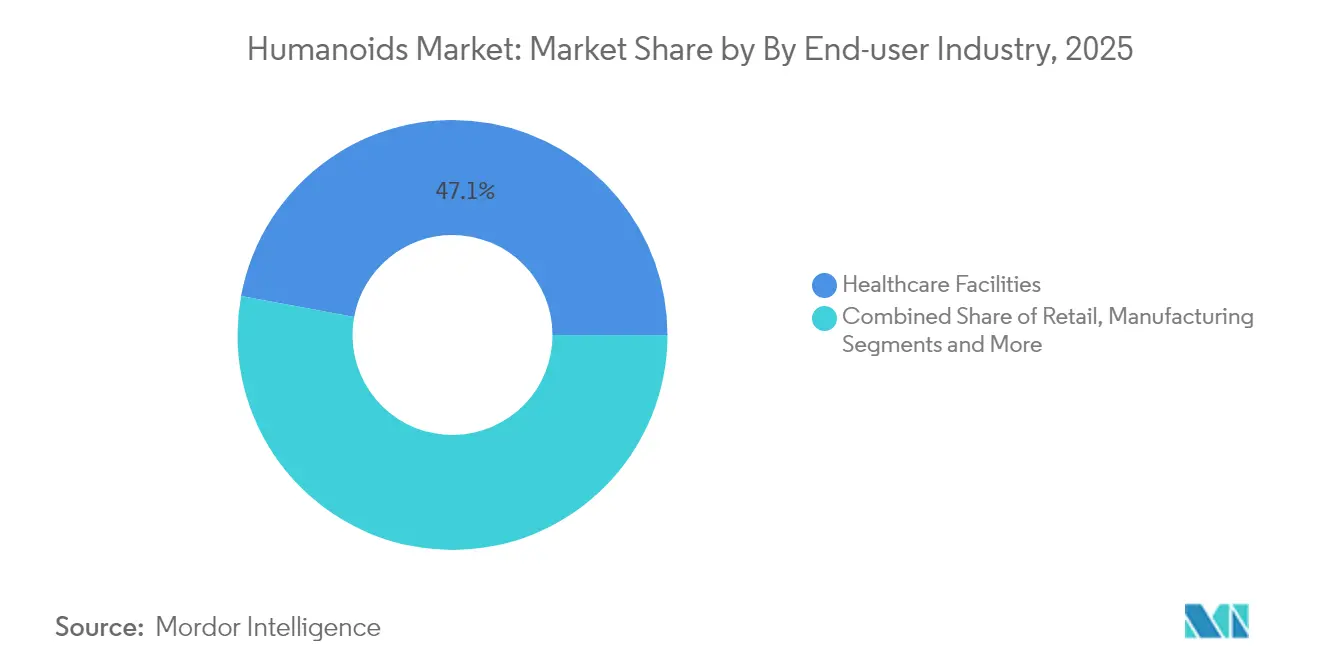

- By end-user industry, healthcare facilities led with a 47.10% revenue share in 2025; manufacturing & warehousing is forecast to expand at a 58.6% CAGR to 2031.

- By form factor, full-size (>140 cm) models captured 32.60% of the humanoids market share in 2025; mid-size platforms are expected to post the fastest growth as costs fall.

- By geography, North America commanded 37.40% of 2025 global revenues, while Asia-Pacific is projected to register the highest 53.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Humanoids Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging-population care gap intensifies demand | +7.2% | Japan, Germany, South Korea; global spillover | Long term (≥ 4 years) |

| AI cost curve falling below USD 25 k per unit | +5.7% | North America, China; global scaling | Medium term (2–4 years) |

| Factory labour shortages in G7 & China | +4.8% | G7, China, emerging-market exporters | Short term (≤ 2 years) |

| National “Humanoid 2025” investment programmes | +3.8% | China, South Korea; allied technology corridors | Medium term (2–4 years) |

| Emerging elderly-care robot safety standards | +2.9% | EU, North America; global adoption | Long term (≥ 4 years) |

| EV battery-motor supply-chain spill-overs | +2.4% | China, Europe, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging-Population Care Gap Intensifies Demand

Japan’s population aged 65 years and older reached 29.1% in 2024, and healthcare worker deficits may exceed 2.4 million by 2030. Hospitals are turning to humanoids for continuous patient monitoring, medication rounds, and social interaction, trimming operating costs by 30–40% while keeping quality consistent. Honda’s Haru units now assist nurses in Spanish geriatric wards, demonstrating cross-border relevance. Retail and hospitality operators facing similar labour gaps are introducing reception and service robots to protect customer experience despite shrinking staff levels. South Korea already operates 1,102 robots per 10,000 employees, the highest robot density worldwide.[1]Anthony Cuthbertson, “South Korea Becomes First Country to Fill 10% of Workforce With Robots,” The Independent, independent.co.uk

AI Cost Curve Falling Below USD 25 k Per Unit

Economies of scale, standardised actuators, and low-cost GPUs are pushing manufactured costs down from USD 35,000 in 2025 to a targeted USD 13,000–17,000 by 2030. Tesla expects to build 10,000 Optimus units priced at USD 20,000–30,000 each, reflecting automotive-style throughput. Apptronik’s partnership with Google DeepMind ties large-language-model reasoning to Apollo’s manipulation skills, compressing what once required USD 100,000 servers onto edge processors. Battery pack prices, already 85% lower than 2010 levels thanks to the electric-vehicle industry, further erode total cost of ownership.[2]Mackenzie Ferguson, “Apptronik and Google DeepMind Join Forces: A Game-Changer for Humanoid Robots,” OpenTools, opentools.ai

Factory Labour Shortages in G7 & China

Germany recorded 2 million unfilled industrial jobs in 2024, and China’s working-age cohort is shrinking by 5 million annually. Agility Robotics’ Digit units, deployed with Amazon and GXO, handle order picking and tote movement around-the-clock. West Japan Railway’s 12 m-reach maintenance humanoids replace high-risk manual work while raising safety compliance. For manufacturers, a single adaptable humanoid offers multi-task coverage via software updates, strengthening ROI even where hourly costs still exceed cobots.

National “Humanoid 2025” Programmes (China, South Korea)

China has earmarked more than USD 10 billion for domestic humanoid lines, with six companies targeting 1,000-plus units each by 2025. South Korea’s policy bank is directing KRW 3.5 trillion (USD 2.53 billion) into AI-driven robotics, bundling finance with procurement guarantees. Such scale aligns suppliers, regulators, and buyers, and is elevating the Asia-Pacific share of the humanoids market from fast follower to innovation leader.

Restraints Impact Analysis of Humanoids Market*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High cap-ex & TCO above USD 0.50/hr vs cobots | −3.8% | Global; acute in emerging, price-sensitive economies | Short term (≤ 2 years) |

| Safety / liability regulation uncertainty | −2.4% | EU, North America | Medium term (2–4 years) |

| Rare-earth magnet supply bottlenecks | −1.9% | Non-Chinese OEMs | Short term (≤ 2 years) |

| Societal acceptance & labour-union pushback | −1.4% | Europe, North America; cultural divergences | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cap-ex & TCO Above USD 0.50/hr Compared with Cobots

Operating a humanoid costs USD 0.75–1.25 per hour today, versus USD 0.35–0.50 for six-axis cobots. Precision gearboxes, 25-plus degrees of freedom, and richer sensor arrays inflate both acquisition and maintenance outlays. Nevertheless, in tasks demanding human reach and navigation, cobots require costly re-engineering of facilities, offsetting their per-hour advantage. In developed economies where average factory wages top USD 45,000, a humanoid’s USD 25,000–35,000 annual running cost is increasingly competitive.

Safety / Liability Regulation Uncertainty

Enterprises must currently interpret ISO 10218 for industrial arms, ISO 13482 for service robots, and emerging IEC 80601-2-77 drafts for medical platforms. Insurers lack actuarial data on humanoid risk, leaving companies to self-insure or pay premiums that erode ROI. Forthcoming EU AI liability rules could impose strict product-use reporting, but they may also reward first movers that validate compliance early, raising the bar for later entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Humanoids Market Segment Analysis

By Motion Type:

Biped Systems Drive Future EvolutionThe wheel-drive class held 62.40% of 2025 revenues, underscoring current user preference for energy-efficient, low-maintenance mobility in flat-floored plants and fulfilment centres. This dominance meant the wheel cohort accounted for the largest slice of the humanoids market share that year. However, the biped category is expanding at a 57.1% CAGR, signalling that the humanoids market will pivot toward full human-environment compatibility as costs fall.

Improved model-predictive controllers, compliant ankle joints, and whole-body coordination algorithms are delivering steady-state walking above 1.5 m/s while cutting energy draw by 30%. Hybrid and multi-leg robots remain niche solutions for disaster response where debris or uneven terrain precludes wheels. As AI motion planners mature, buyers anticipate re-deploying the same biped unit across multiple sites, raising lifetime value and tightening the link between software updates and operational output.

By Component:

Software Intelligence Transforms Value CreationHardware captured 67.20% of the humanoids market size in 2025, reflecting large capital bills for actuators, composite frames, and high-resolution sensor stacks. Yet software revenue is tracking a 55.9% CAGR, outpacing any mechanical upgrade cycle.

Cloud-enhanced vision, natural-language models, and reinforcement-learning stacks enable the same chassis to perform kitting in the morning and concierge duties after hours. As recurring licence fees overtake one-off hardware margins, vendors are shifting to service-level agreements that guarantee uptime, security patches, and feature drops. This echo of the smartphone ecosystem positions code as the foremost differentiator even inside a physical-goods category, and heightens buyer focus on cybersecurity and data-ownership clauses.

By End-user Industry:

Manufacturing Automation Accelerates AdoptionHealthcare settings led with 47.10% of 2025 spend as nurses and orderlies used robots for repetitive rounds, freeing qualified staff for high-value care. Increasing adoption of humanoid platforms in the educational robot is also supporting demand for socially interactive robots across academic and research institutions. Nonetheless, manufacturing & warehousing is set to register a 58.6% CAGR, the fastest among tracked verticals, ensuring the humanoids market will see its centre of gravity shift toward shop-floor and logistics corridors.

Amazon pilots with Agility Robotics proved that a single biped can substitute for disparate pallet jacks, vertical lifts, and picking carts. Meanwhile, assembly plants value humanoids’ ability to swap end-effectors and software workflows instead of installing new fixed conveyors. As more factories benchmark labour productivity to robots per worker, humanoid deployment pipelines are becoming a board-room KPI.

By Form Factor:

Full-Size Dominance Reflects Enterprise PreferencesFull-size models exceeding 140 cm accounted for 32.60% of 2025 shipments, anchoring their lead in the humanoids market. User studies show employees accept machines that mirror average adult stature more readily than child-sized units. Tesla’s 5’ 8″, 57 kg specification is rapidly emerging as the quasi-standard around which tool handles, drawer heights, and control-panel reach zones are tuned.

Mid-size and small robots serve hospital bedside tasks or retail greeting roles where cramped aisles or seated interactions prevail. Upper-torso-only designs capture assembly-cell use cases centred on dexterity rather than locomotion. Even so, full-size variants draw the highest order volumes because buyers can redeploy them across departments without re-engineering existing assets, protecting capital budgets.

Geography Analysis

North America Humanoids Market

North America retained 37.40% of global 2025 revenue, catalysed by USD 2 billion in venture rounds and early regulatory sandboxes that cut deployment risk. United States OEMs such as Tesla, Boston Dynamics, and Agility Robotics collectively secured USD 1.2 billion during 2024–2025, bankrolling commercial tooling and pilot roll-outs. Canada’s universities specialise in compliant-actuator research, and Mexico supplies precision gear casings, threading NAFTA supply-chain integration into humanoid economics.

APAC Humanoids Market

Asia-Pacific is the fastest-growing theatre, advancing at a 53.2% CAGR to 2031. China’s USD 10 billion National Humanoid programme aligns provincial grants, military adoption, and purchasing quotas, while six local firms target ≥ 1,000 units each for 2025 volume. South Korea’s KRW 3.5 trillion stimulus channels funds through its policy bank to private labs, fostering R&D and domestic content rules. Japan’s automotive heritage yields high-precision strut and joint modules, and India supplies cloud-control middleware at lower cost. Collectively, these forces scale output and compress unit costs, bolstering the humanoids market across emerging Asian economies.

Europe Humanoids Market

Europe posts steady, policy-led growth. Germany’s Industrie 4.0 facilities adopt humanoids to keep high-mix assembly at home rather than offshoring. The EU’s draft AI liability directive compels rigorous fail-safe designs, adding qualification overhead but reducing long-run reputational risk. France and the United Kingdom emphasise advanced haptic-sensor R&D, while Nordic eldercare pilots validate robots in long-term-care settings. Although certification timelines push some buyers to slower roll-outs, established automotive suppliers in Germany and Italy are lining up to build sub-assemblies, reinforcing trans-Atlantic competition.

Competitive Landscape

The humanoids market shows moderate fragmentation: roughly 20 funded OEMs vie for marquee contracts, yet none holds a double-digit global revenue share. Automotive entrants such as Tesla, Honda, and Toyota leverage mature stamping lines and battery know-how, chasing cost leadership. Pure-play robotics firms—Boston Dynamics, Agility Robotics, Figure AI—differentiate through locomotion agility and AI orchestration strength. Patent filings covering humanoid gait, balance, and manipulation jumped 340% between 2022 and 2024.

Strategic options fall into three camps. Vertically integrated builders own hardware, firmware, and cloud telemetry to lock-in customers and secure data moats. Platform players license AI stacks or high-precision actuators across multiple OEMs, aiming for volume royalty streams. Niche specialists target hazardous-environment work—nuclear inspection, offshore rig maintenance—where price is secondary to safety. M&A activity is rising as cash-rich firms purchase control of component suppliers to mitigate rare-earth and servo-gear bottlenecks.

Regulatory permissioning is emerging as a competitive barrier: Certification test benches, digital twins validated by notified bodies, and workforce-coexistence trials require budgets that favour incumbents. Still, white-space remains in compliant soft-robotics skins, context-aware voice interaction, and lithium-sulphur battery packs built for 24-hour duty cycles. Start-ups that solve any one of these pain points can attract strategic investment or acquisition offers.

Humanoids Industry Leaders

SoftBank Robotics Group Corp.

UBTECH Robotics Inc.

Boston Dynamics Inc.

Tesla, Inc.

Agility Robotics LLC

- *Disclaimer: Major Players sorted in no particular order

Humanoids Market Companies Covered in this Report

- Honda Motor Co., Ltd.

- Toyota Motor Corporation

- SoftBank Robotics Group Corp.

- UBTECH Robotics Inc.

- PAL Robotics SL

- Hanson Robotics Ltd.

- Kawada Robotics Corporation

- Promobot LLC

- Invento Robotics Pvt. Ltd.

- ROBOTIS Co., Ltd.

- Boston Dynamics Inc.

- Tesla, Inc. (Optimus)

- Agility Robotics LLC

- Figure AI, Inc.

- Engineered Arts Ltd.

- Unitree Robotics Co., Ltd.

- Fourier Intelligence Co., Ltd.

- Xiaomi Corp. - Robotics Lab

- Samsung Electronics Co., Ltd.

- Apptronik Inc.

Recent Industry Developments in Humanoids Market

- February 2025: Apptronik secured USD 350 million in Series A funding to accelerate Apollo humanoid robot production and commercial deployment, with partnerships planned across manufacturing, logistics, and eldercare sectors to demonstrate commercial viability through pilot programs.

- January 2025: OpenAI-backed 1X Technologies acquired Kind Humanoid to strengthen its position in home robotics applications, combining 1X's Neo Beta humanoid capabilities with Kind Humanoid's bipedal robot technology for enhanced domestic applications.

- January 2025: Apptronik and Jabil announced collaboration to scale Apollo humanoid robot production through integration into Jabil's manufacturing operations, enabling robots to perform inspection, sorting, and assembly tasks while optimizing production costs.

- December 2024: Apptronik partnered with Google DeepMind to integrate advanced AI capabilities into Apollo humanoid robots, focusing on enhanced dexterity and real-world navigation for manufacturing and logistics applications.

Global Humanoids Market Report Scope

A humanoid is a robot with a body shape built to resemble the human body. The design may be for functional purposes, such as interacting with human tools and environments, experimental, or other goals.

The studied market is segmented by different applications such as education, research and space exploration, personal assistance, entertainment, and hospitality among various geographies (North America, Europe, Asia-Pacific, and the Rest of the World). The impact of COVID-19 on the market and impacted segments is also covered under the scope of the study. Further, the disruption of the factors affecting the market's expansion in the near future has been covered in the study regarding drivers and restraints.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Segmentation Overview

| Wheel-drive |

| Biped |

| Hybrid / Multi-leg |

| Hardware |

| Software |

| Services |

| Healthcare Facilities |

| Retail and Shopping Centres |

| Manufacturing and Warehousing |

| Hospitality (Hotels, Theme Parks) |

| Academic and Research Institutes |

| Full-size (Greater than 140 cm) |

| Mid-size (100-140 cm) |

| Small (Less than 100 cm) |

| Upper-torso only |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Motion Type | Wheel-drive | |

| Biped | ||

| Hybrid / Multi-leg | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By End-user Industry | Healthcare Facilities | |

| Retail and Shopping Centres | ||

| Manufacturing and Warehousing | ||

| Hospitality (Hotels, Theme Parks) | ||

| Academic and Research Institutes | ||

| By Form Factor | Full-size (Greater than 140 cm) | |

| Mid-size (100-140 cm) | ||

| Small (Less than 100 cm) | ||

| Upper-torso only | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size of the humanoids market by 2031?

The humanoids market is forecast to reach USD 17.80 billion by 2031.

Which region is expected to grow fastest in humanoid adoption?

Asia-Pacific is set to expand at a 53.2% CAGR through 2031, driven by China’s and South Korea’s national programmes.

Why are biped humanoid robots gaining traction?

Biped designs navigate stairs and uneven floors that wheel-driven units cannot handle, and the segment is growing at a 57.1% CAGR.

Which end-user industry will add the most new deployments?

Manufacturing and warehousing is on track for the highest 58.6% CAGR as firms tackle labour shortages and flexible automation needs.

What is the biggest cost barrier to humanoid robot adoption?

Current total cost of ownership ranges between USD 0.75 and USD 1.25 per hour, higher than cobots, though declining component prices are narrowing the gap.

How are governments influencing the humanoids industry?

Direct funding, procurement incentives, and localisation policies, such as China’s USD 10 billion budget and South Korea’s KRW 3.5 trillion AI fund, are accelerating R&D and scaling.

Page last updated on: