Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

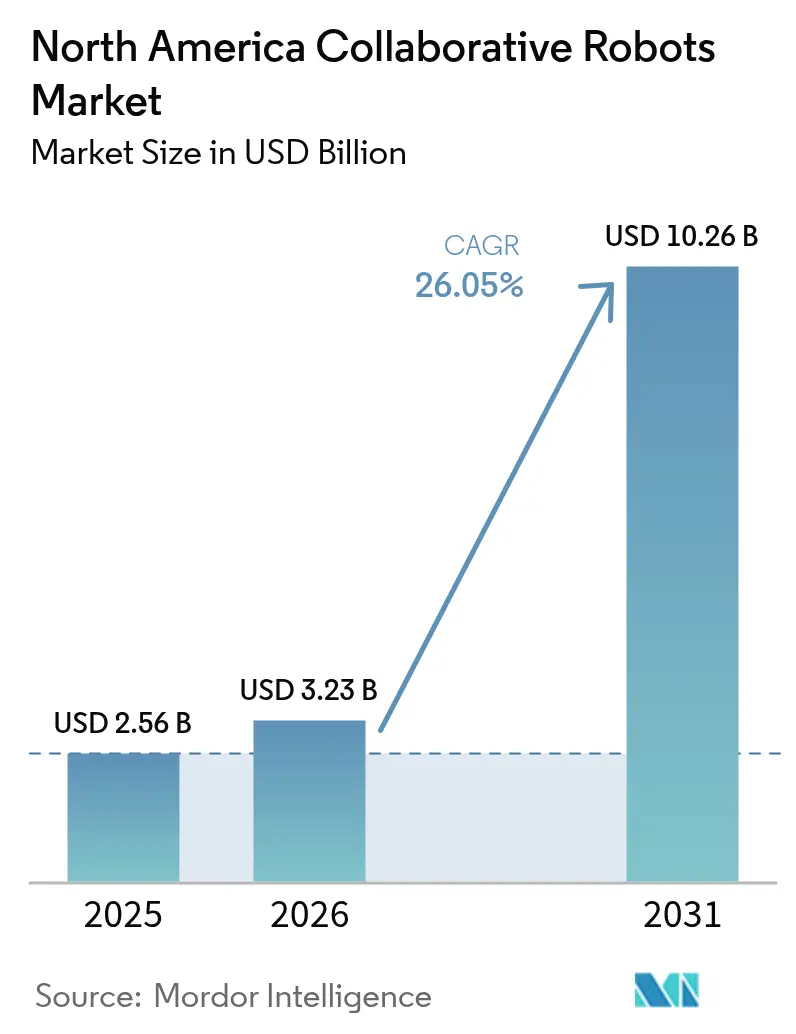

| Base Year Market Size (2025) | USD 2.56 Billion |

| Market Size (2026) | USD 3.23 Billion |

| Market Size (2031) | USD 10.26 Billion |

| Growth Rate (2026 - 2031) | 26.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Collaborative Robots Market Analysis by Mordor Intelligence

The North America collaborative robots market size is expected to grow from USD 2.56 billion in 2025 to USD 3.23 billion in 2026 and is forecast to reach USD 10.26 billion by 2031 at 26.05% CAGR over 2026-2031. Reshoring incentives, ongoing labor shortages, and simplified human–robot interaction are converging to position the North America collaborative robots market as a structural pillar of regional manufacturing modernization. Federal grants covering up to 40% of qualified automation expenditures compress pay-back periods below 18 months, even for small and midsized enterprises. Tier-one automakers and semiconductor fabs are broadening orders beyond pilot cells, signaling that cobots have moved from experimentation to core capital-equipment budgets. Vendors, meanwhile, are embedding edge-AI controllers that learn tasks in hours rather than weeks, creating a recurring software revenue stream that may exceed hardware sales before decade-end.

Key Report Takeaways

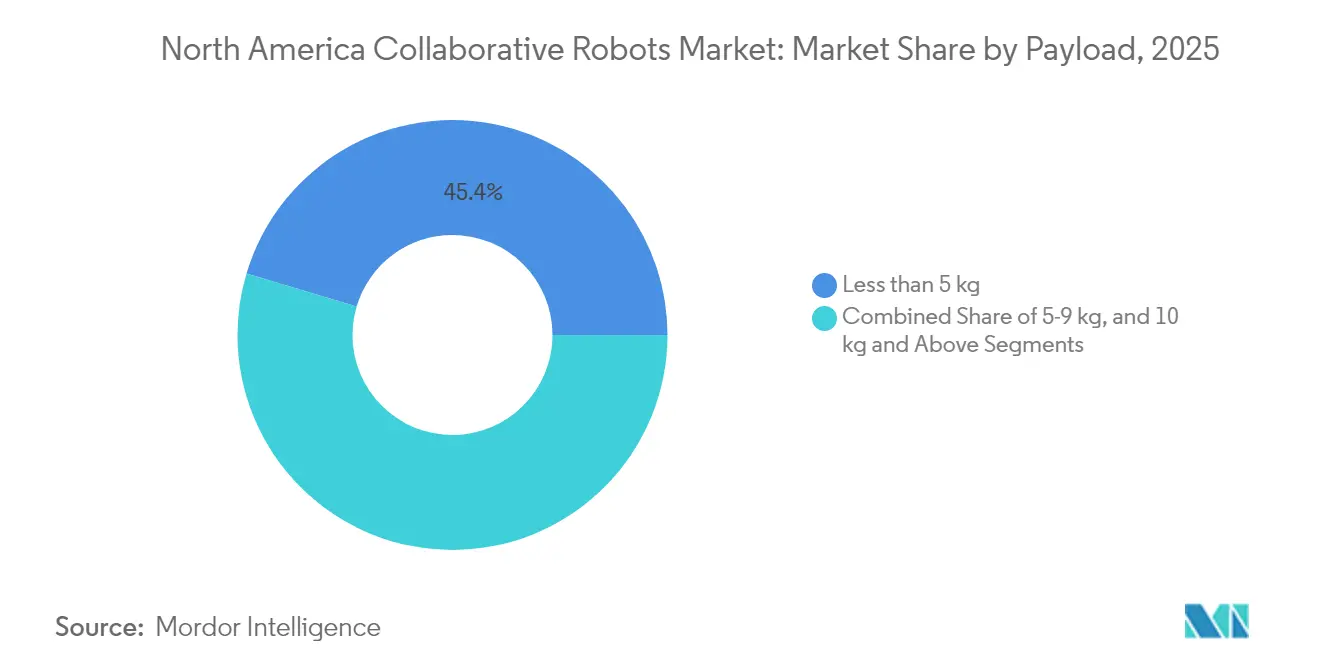

- By payload, units rated below 5 kg captured 45.38% of the North America collaborative robots market share in 2025, while payloads of 10 kg and above are forecast to expand at an 17.65% CAGR through 2031.

- By end-user industry, electronics and semiconductors commanded 36.95% revenue in 2025; food and beverage is set to grow at a 14.88% CAGR to 2031.

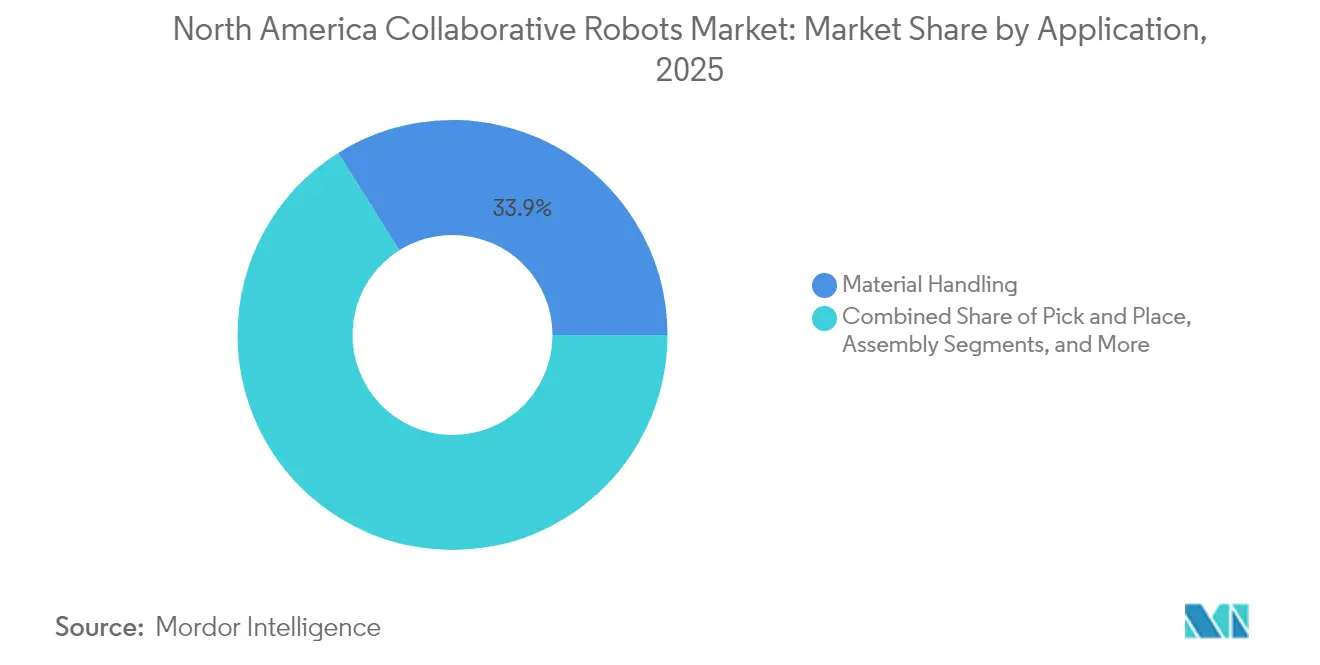

- By application, material handling held 33.92% of the North America collaborative robots market size in 2025, whereas assembly tasks are advancing at a 16.90% CAGR.

- By component, hardware delivered 51.64% of 2025 revenue, yet software is rising at a 18.82% CAGR through 2031.

- By Country, the United States accounted for 78.55% of 2025 revenue, while Mexico is the fastest-growing country at an 17.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Collaborative Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Automation in Manufacturing Processes | +6.2% | United States, Mexico, Canada | Medium term (2-4 years) |

| High Return on Investment Enabled by Easy Deployment | +4.8% | United States, Canada | Short term (≤ 2 years) |

| Rapid Advances in Edge Computing and AI Integration | +5.1% | United States, with spillover to Mexico | Medium term (2-4 years) |

| Rising Labor Costs and Labor Shortages Across Industries | +5.4% | United States, Canada | Short term (≤ 2 years) |

| Adoption of Collaborative Robots in Precision Agriculture Operations | +2.3% | United States, Canada | Long term (≥ 4 years) |

| Incentive Grants for Reshoring Electronics Assembly Lines | +3.7% | United States, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Automation in Manufacturing Processes

Manufacturers that repatriate lines from Asia must balance throughput and flexibility. Cobots allow quick re-tooling without cages, satisfying this dual mandate. The 2024 House AI Task Force urged USD 500 million per year for human–robot collaboration pilots, accelerating early-stage deployments.[1]House AI Task Force, “Artificial Intelligence in Manufacturing Report,” congress.gov Yaskawa’s 185,000 square-foot U.S. expansion underscores vendor confidence in sustained orders. As a result, the North America collaborative robots market is expanding beyond tier-one plants toward rural contract manufacturers that previously lacked access to robotics expertise.

High Return on Investment Enabled by Easy Deployment

Drag-and-drop design suites and pre-engineered grippers now let job shops integrate a cobot cell in under 48 hours, down from 6-12 weeks. ABB’s GoFa-Vention bundle cut installation labor costs by 60-70% for first-wave adopters. Lower integration overhead unlocks use cases with batch sizes below 100 units, allowing the North America collaborative robots market to penetrate segments once deemed too small for automation.

Rapid Advances in Edge Computing and AI Integration

On-device inference transforms cobots into adaptive co-workers that optimize trajectories in real time. Universal Robots’ MotionPlus software reduced cycle-time variability by 18% during multi-arm assembly trials. National Science Foundation hubs are funding AI-enabled manufacturing test beds, anchoring the North America collaborative robots market in federally backed innovation clusters.

Rising Labor Costs and Labor Shortages Across Industries

Median manufacturing wages rose 4.8% in 2024, intensifying pressure to automate tasks with high injury rates. Toyota’s Kentucky battery-plant layout shows how cobots handle repetitive material moves while technicians manage diagnostics. The North America collaborative robots market therefore functions as a workforce multiplier rather than a direct labor substitute, mitigating union resistance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Payload and Speed Capabilities Versus Traditional Robots | -2.1% | United States, Canada, Mexico | Medium term (2-4 years) |

| High Initial Integration and Training Costs for SMEs | -1.8% | United States, Canada | Short term (≤ 2 years) |

| OSHA Standard Ambiguity Creating Certification Bottlenecks | -1.4% | United States | Short term (≤ 2 years) |

| Cybersecurity Vulnerabilities in Open-Source Robot Operating Systems | -0.9% | United States, with spillover to Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Payload and Speed Capabilities Versus Traditional Robots

ISO/TS 15066 force limits cap most cobots at 35 kg payload and 1.5 m/s speed, excluding applications such as body-in-white welding or press tending. Traditional arms still handle 88.4% of automotive installations.[2]International Federation of Robotics, “World Robotics 2024,” ifr.org Hybrid cells that pair fenced heavy-duty robots with cobots increase floor-space needs, diluting some flexibility benefits and slowing penetration of the North America collaborative robots market into legacy press shops.

High Initial Integration and Training Costs for SMEs

End-of-arm tooling, vision systems, and process redesign can top USD 50,000 per cell. A 2024 NIST survey found 62% of small manufacturers still view integration services as the primary barrier. Government extension programs train fewer than 5,000 operators annually, creating a temporary adoption bottleneck that curbs near-term growth of the North America collaborative robots market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payload: Miniaturization Sustains Sub-5 kg Dominance

Less-than-5 kg cobots captured 45.38% of the North America collaborative robots market share in 2025, propelled by cleanroom electronics assembly that values compact footprints and gentle force limits. Standard Bots’ 30 kg model, released in 2025, signals supplier intent to penetrate heavier-duty palletizing, pointing to segment blurring. Over time, vendors will package modular arms allowing end users to swap joints and extend reach, reinforcing the scalability narrative that fuels the North America collaborative robots market.

Demand for 10 kg-plus units, forecast to grow at an 17.65% CAGR, stems from food palletizing and machine tending where ergonomic risk drives automation budgets. KUKA’s mosaixx remote-monitoring stack lowers service visits, cutting total cost of ownership and attracting multi-site processors. As high-payload designs mature, the North America collaborative robots market size for heavy-duty units could exceed USD 1.12 billion by 2031.

By End-User Industry: Food and Beverage Takes the Growth Lead

Electronics retained 36.95% revenue in 2025 owing to wafer handling and die bonding tasks that demand particle-free operation. Nonetheless, food and beverage posts a 14.88% CAGR to 2031, reshaping the North America collaborative robots market as processors confront hygiene mandates and 50% annual turnover on packaging lines.

Logistics, pharmaceuticals, and aerospace form an emerging cohort, collectively advancing as fulfillment centers deploy cobots for order picking. Compliance with ISO 22000 food-safety rules and FSMA preventive controls accelerates uptake, ensuring the North America collaborative robots market diversifies across verticals.

By Application: Assembly Narrows the Gap With Material Handling

Material handling held 33.92% of 2025 revenue, reflecting early wins in palletizing and machine tending. Assembly is set to grow at 16.90% CAGR, buoyed by inverse-kinematics optimizers that cut cycle time 12%, making cobots viable for fast takt operations. Sensor-rich end effectors let cobots seat press-fits or apply torque within ±3%, once exclusive to precision gantries.

As vendors ship task-specific software bundles, buyers increasingly pay for guaranteed takt-time outcomes, shifting value capture from hardware to recurring licenses and enlarging the North America collaborative robots market size allocated to digital add-ons.

By Component: Software Monetization Redraws Revenue Mix

Hardware made up 51.64% of 2025 sales, but software is rising at 18.82% CAGR on the back of cloud dashboards and predictive-maintenance algorithms. ABB’s subscription tier for welding cobots spreads costs over the asset life, a model now echoed by KUKA’s mosaixx and Yaskawa’s forthcoming AI-optimizer module.

Services revenue, traditionally one-off, is migrating to multi-year support contracts. As margins on metal sell-offs thin, vendors rely on analytics to retain differentiation, reinforcing software’s share of the North America collaborative robots market.

Geography Analysis

The United States controlled 78.55% of the North America collaborative robots market in 2025, underpinned by semiconductor fabs in Arizona and automotive clusters in the Midwest. Senate appropriations for 2025-26 allocate USD 1.5 billion to cobot integration grants, sustaining demand during macro softness. Yaskawa’s USD 180 million Wisconsin expansion doubles domestic capacity and reduces lead times, bolstering supply resilience.

Mexico, expanding at an 17.95% CAGR through 2031, benefits from nearshoring of electronics and vehicle parts. Government incentives target high-value assembly lines, and cobots bridge labor gaps without proportional headcount. Vendors are responding by setting up parts depots in Monterrey and Queretaro, signaling long-term commitment to the North America collaborative robots market south of the border.

Canada remains smaller but steady, led by Ontario and Quebec food processors that leverage provincial automation grants. Clear adoption of ISO/TS 15066 by workplace-safety regulators shortens certification cycles, making Canada a test bed for hygienic stainless-steel cobot designs. Although its manufacturing base is modest, Canada’s focus on aerospace subassembly and cold-chain food packaging provides high-margin niches within the broader North America collaborative robots market.

Competitive Landscape

Market concentration is moderate. ABB, Universal Robots, and FANUC together held roughly 45% of 2024 unit shipments, with remaining share divided among KUKA, Yaskawa, Doosan, and emerging domestic players. Competition pivots on payload envelopes, AI-driven path planning, and ecosystem reach. Universal Robots’ NVIDIA-powered accelerator slashed integration time by 30%, while FANUC’s IEC 62443-certified controller addresses cybersecurity mandates in pharma and defense.

Standard Bots targets Buy-America opportunities with its 30 kg model manufactured in New York. KUKA’s dedicated digital division reflects the strategic pivot toward recurring revenue as hardware commoditizes. Intellectual-property portfolios in force-torque sensing raise entry barriers, yet ROS2 middleware lowers development cost for start-ups, fostering healthy churn and sustaining innovation across the North America collaborative robots industry.

Strategic plays increasingly revolve around platform monetization. ABB’s partnership with Vention enables plug-and-play cells for job shops, while KUKA’s mosaixx allows over-the-air updates, mirroring cloud trends in industrial IoT. With vendors racing to lock in developer communities, ecosystem orchestration rather than arm kinematics is emerging as the decisive battleground in the North America collaborative robots market.

North America Collaborative Robots Industry Leaders

ABB Ltd.

Universal Robots A/S

FANUC Corporation

Techman Robot Inc.

AUBO (Beijing) Robotics Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Yaskawa committed USD 180 million to expand its Franklin, Wisconsin, campus, adding 300 jobs and doubling cobot assembly capacity.

- May 2025: Standard Bots released a 30 kg collaborative robot built in Glen Cove, New York, aimed at heavy-duty palletizing and automotive subassembly.

- February 2025: Universal Robots launched its AI Accelerator with NVIDIA, embedding edge inference for real-time path optimization.

- November 2024: KUKA rolled out its mosaixx cloud platform for fleet monitoring and predictive maintenance.

North America Collaborative Robots Market Report Scope

The North America collaborative robots (cobots) market refers to the industry focused on robots designed to work safely alongside humans in shared workspaces, enhancing productivity, flexibility, and automation. These robots are deployed across various sectors, including electronics, automotive, and food and beverage, for applications such as material handling, pick-and-place, and assembly.

The North America Collaborative Robots Market Report is Segmented by Payload (Less than 5 kg, 5-9 kg, 10 kg and Above), End-user Industry (Electronics/Semiconductor and FPD, Automotive, Food and Beverage, Other End-user Industries), Application (Material Handling, Pick and Place, Assembly, Other Applications), Component (Hardware, Software, Services), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Payload

| Less than 5 kg |

| 5-9 kg |

| 10 kg and Above |

By End-user Industry

| Electronics/Semiconductor and FPD |

| Automotive |

| Food and Beverage |

| Other End-user Industries |

By Application

| Material Handling |

| Pick and Place |

| Assembly |

| Other Applications (Palletizing/De-palletizing, Welding, Painting, Sorting, Positioning, etc.) |

By Component

| Hardware |

| Software |

| Services |

By Country

| United States |

| Canada |

| Mexico |

| By Payload | Less than 5 kg |

| 5-9 kg | |

| 10 kg and Above | |

| By End-user Industry | Electronics/Semiconductor and FPD |

| Automotive | |

| Food and Beverage | |

| Other End-user Industries | |

| By Application | Material Handling |

| Pick and Place | |

| Assembly | |

| Other Applications (Palletizing/De-palletizing, Welding, Painting, Sorting, Positioning, etc.) | |

| By Component | Hardware |

| Software | |

| Services | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How fast is collaborative-robot adoption growing in North America?

The North America collaborative robots market is expanding at a 26.05% CAGR between 2026 and 2031, supported by reshoring incentives and labor shortages.

Which payload class leads current cobot demand?

Arms rated below 5 kg hold 45.38% market share, favored in electronics and light assembly lines.

What segment will be the biggest revenue driver by 2031?

Software subscriptions, growing at a 18.82% CAGR, are expected to overtake hardware as the primary revenue source.

Why are food processors investing heavily in cobots?

High labor turnover and strict hygiene rules push food-and-beverage producers to automate packaging and palletizing tasks at a 14.88% CAGR.

Which country is the fastest-growing market in the region?

Mexico leads with an 17.95% CAGR, fueled by nearshored electronics and automotive production.

How are vendors differentiating their products?

Suppliers embed edge-AI controllers, cloud dashboards, and cybersecurity certifications to cut integration time and meet compliance demands.

Page last updated on: