Risk-Based Monitoring Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

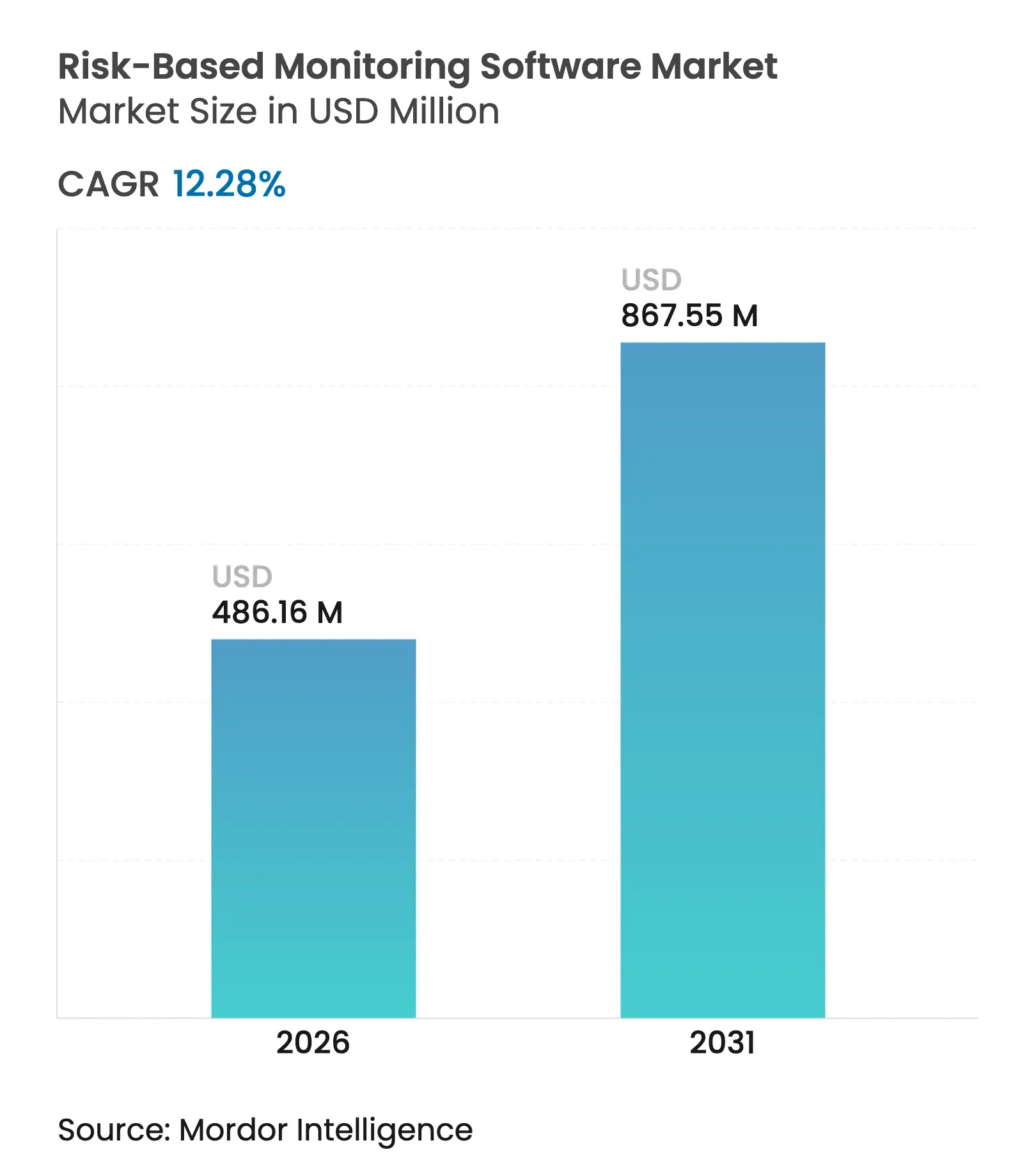

| Market Size (2026) | USD 486.16 Million |

| Market Size (2031) | USD 867.55 Million |

| Growth Rate (2026 - 2031) | 12.28 % CAGR |

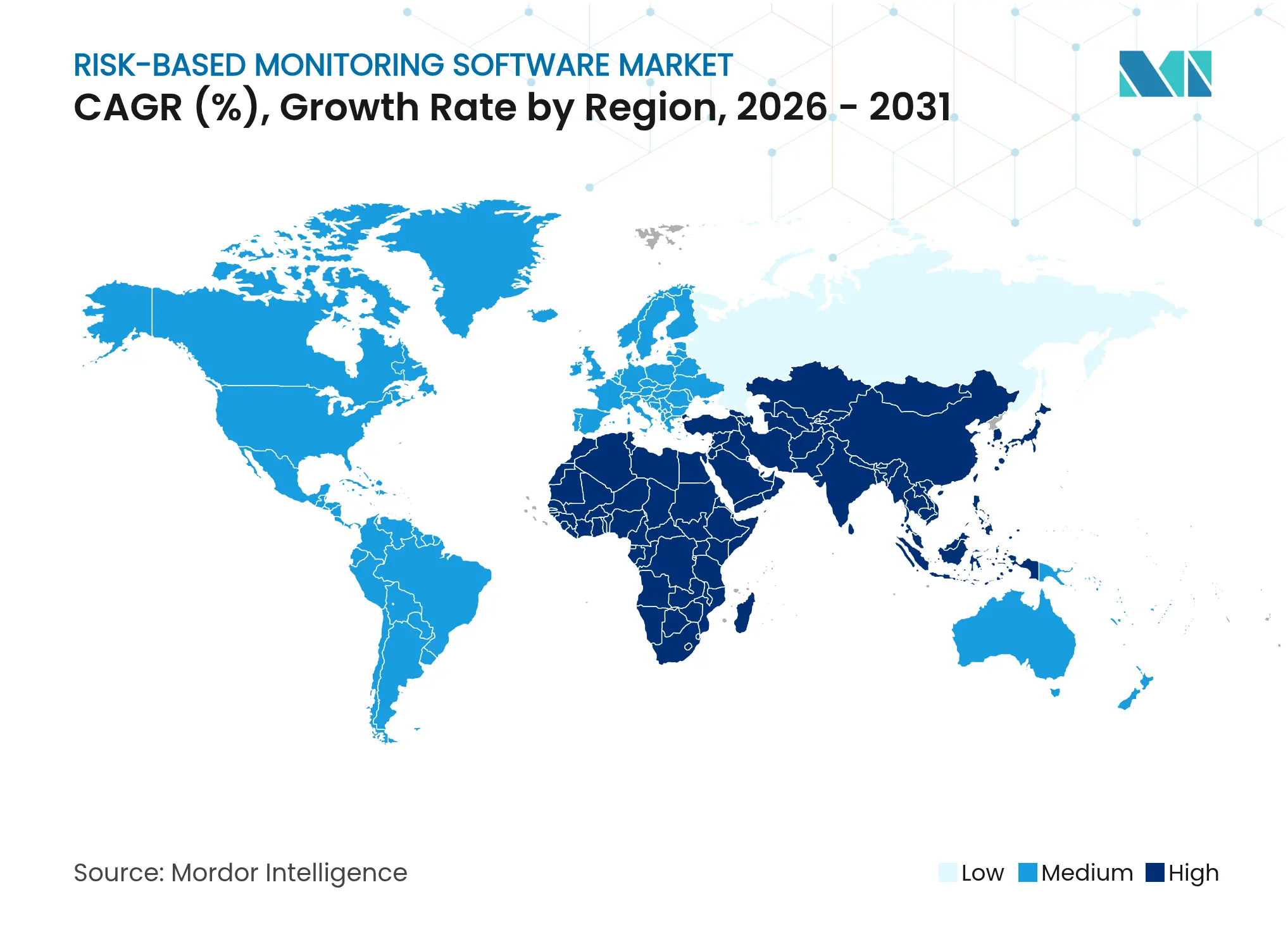

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Risk-Based Monitoring Software Market Analysis by Mordor Intelligence

The risk-based monitoring software market size is expected to grow from USD 432.99 million in 2025 to USD 486.16 million in 2026 and is forecast to reach USD 867.55 million by 2031 at 12.28% CAGR over 2026-2031. The acceleration stems from the pharmaceutical sector’s shift toward data-driven quality oversight as regulators adopt proportionate risk-assessment rules such as ICH E6(R3). Uptake intensifies as decentralized and hybrid trials multiply, data volumes soar, and sponsors seek to curb rising study costs while safeguarding data integrity. Cloud-first deployment models, AI-powered analytics, and unified eClinical ecosystems further boost adoption by cutting IT barriers and enabling real-time collaboration. Competitive pressure is mounting as major platform vendors expand their suites and specialized providers introduce predictive risk engines, reinforcing the value proposition of the risk-based monitoring software market across all trial phases and geographies.

Key Report Takeaways

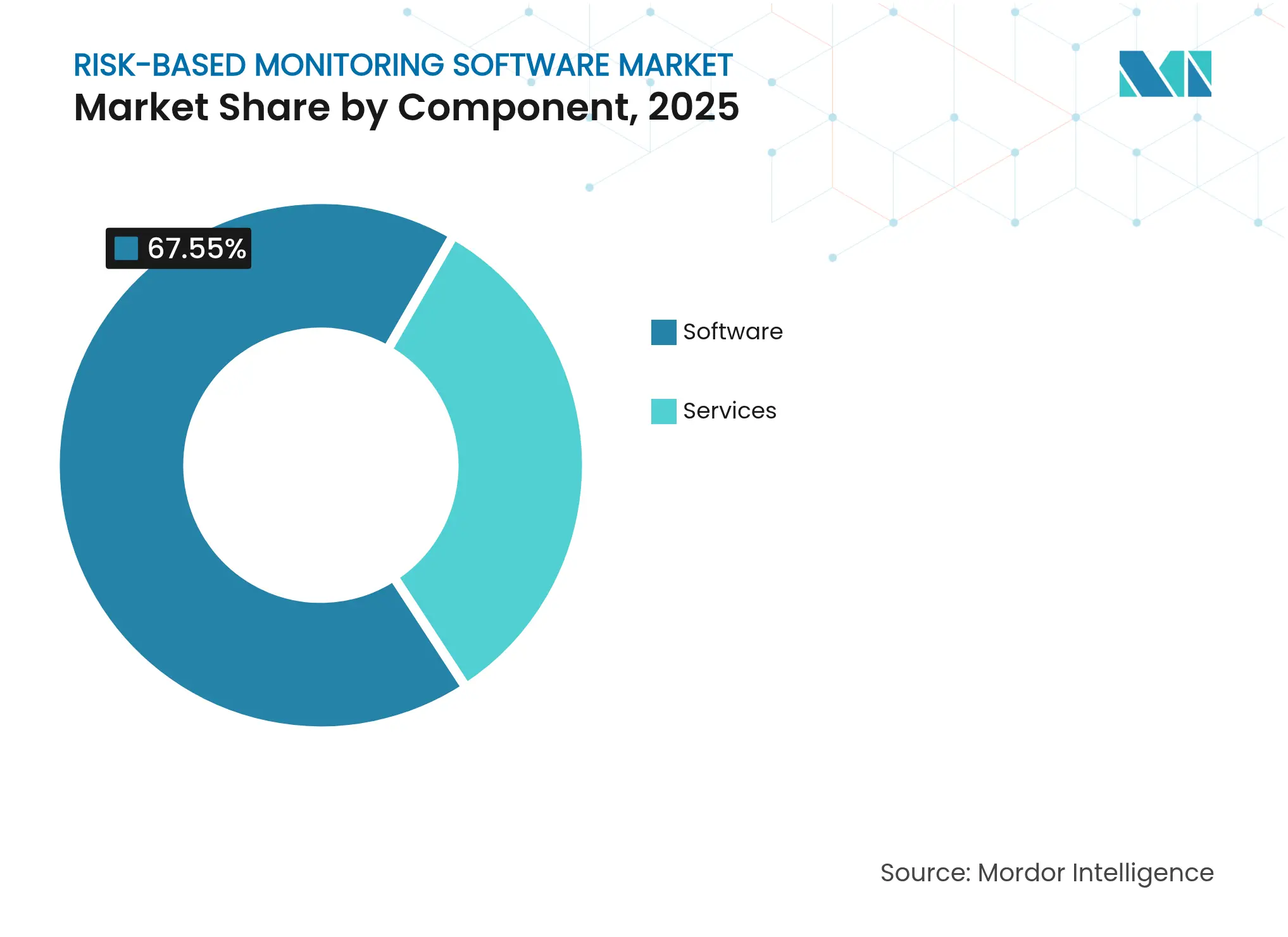

- By component, software captured 67.55% of the risk-based monitoring software market share in 2025; services are forecast to post the fastest 14.65% CAGR through 2031.

- By delivery mode, web-hosted platforms led with 69.10% revenue share in 2025, while cloud-based solutions are projected to expand at a 15.52% CAGR to 2031.

- By end user, pharmaceutical and biopharmaceutical companies held 58.10% share of the risk-based monitoring software market size in 2025, whereas contract research organizations are set to grow at a 13.05% CAGR.

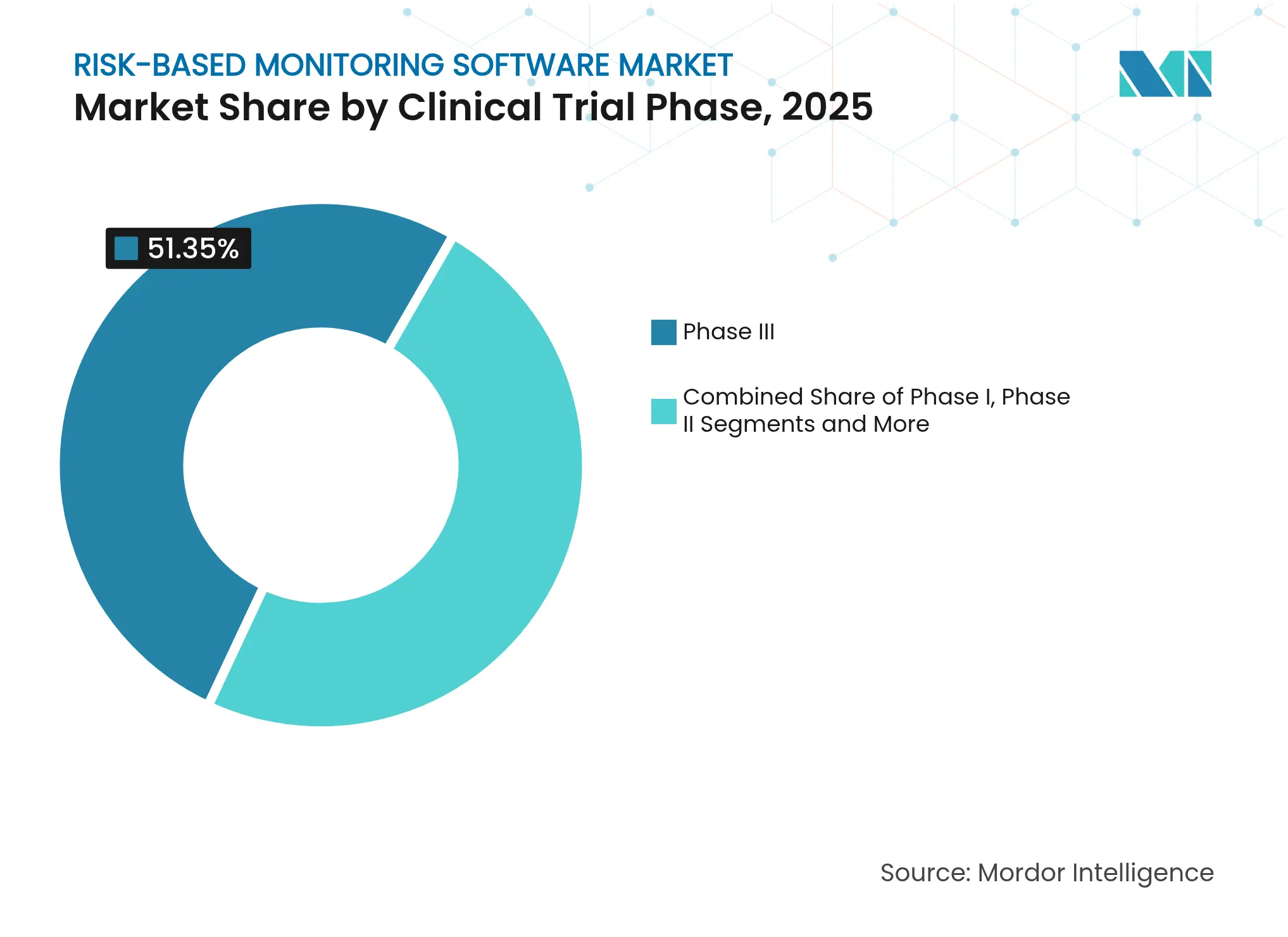

- By clinical phase, Phase III studies commanded 51.35% of implementations in 2025; Phase I is advancing at a 15.68% CAGR.

- By decentralization level, conventional site-centric trials accounted for 68.05% share in 2025, yet fully decentralized models represent the fastest-rising segment at a 14.25% CAGR.

- By geography, North America dominated with 36.85% market share in 2025, while Asia-Pacific leads growth at a 14.79% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Risk-Based Monitoring Software Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High efficiency & cost-saving

versus 100% SDV

High efficiency & cost-saving

versus 100% SDV

| +3.2% | Global; early uptake in North America and EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+3.2%

|

Geographic Relevance

:

Global; early uptake in North

America and EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Regulatory mandates in ICH E6(R3)

& FDA guidance

Regulatory mandates in ICH E6(R3)

& FDA guidance

| +2.8% | Global; strongest in regulated markets | Short term (≤ 2 years) | |||

Rapid rise of complex, decentralized

& hybrid trials

Rapid rise of complex, decentralized

& hybrid trials

| +2.1% | North America & EU core; expanding to APAC | Medium term (2-4 years) | |||

Cloud-first eClinical ecosystems

Cloud-first eClinical ecosystems

| +1.9% | Global; faster in emerging markets | Long term (≥ 4 years) | |||

AI-driven predictive risk scoring

AI-driven predictive risk scoring

| +1.7% | North America & EU; selective APAC adoption | Long term (≥ 4 years) | |||

Synthetic clinical data for

continuous surveillance

Synthetic clinical data for

continuous surveillance

| +1.4% | Developed markets first; global rollout | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Efficiency & Cost-Saving Versus 100% SDV

Monitoring expenses escalate as trial complexity drives a 30% jump in overall study costs, with a Phase III program averaging USD 36.58 million in 2024. Risk-based strategies trim monitoring spend by up to 30% while improving data quality through focused oversight of critical data points. Centralized statistical review exposes anomalies across entire datasets, enabling corrective action sooner than traditional sampling-based visits. Studies show 83% of sites using statistical monitoring achieve lower inconsistency scores versus 56% under conventional methods.[1]Gary Cramer, “Does Risk-Based Quality Management (RBQM) Actually Improve Quality?,” Clinical Researcher, acrpnet.org The approach also supports faster enrollment recovery as 80% of trials struggle to meet recruitment timelines, and every month saved in an 89.8-month development cycle protects revenue opportunities.

Regulatory Mandates in ICH E6(R3) & FDA Guidance

ICH E6(R3), effective January 2025, formalizes risk-proportionate quality management, replacing rigid source verification with adaptive oversight.[2]FDA/CDER, “Good Clinical Practice: ICH E6(R3),” fda.gov The FDA’s Annex 2 guidance issued December 2024 clarifies how decentralized components and real-world data fit within Good Clinical Practice requirements.[3]Food and Drug Administration, “E6(R3) Good Clinical Practice: Annex 2,” federalregister.gov The new framework allows “acceptable ranges” in place of fixed tolerance limits, giving sponsors latitude to tailor monitoring intensity. Emphasis on data governance, cybersecurity, and traceability elevates demand for validated platforms over manual processes. Harmonization across ICH regions eliminates earlier regulatory fragmentation and accelerates global deployment of the risk-based monitoring software market.

Rapid Rise of Complex, Decentralized & Hybrid Trials

Hybrid and decentralized designs funnel streaming data from wearables, telemedicine, and home nursing services, raising data volumes in Phase III studies by 283.2%. FDA guidance finalized in November 2024 removes ambiguity around remote oversight and paves the way for broader adoption. New risk domains emerge—identity verification, IP accountability, and continuous data attribution—that legacy site visits cannot address. Sponsors therefore rely on dashboards delivering real-time KPIs and predictive analytics to keep dispersed teams aligned and ensure protocol adherence.

Cloud-First eClinical Ecosystems

Life-science cloud migration accelerated in 2024 as firms recognized subscription models that ease upfront capex while enhancing scalability. Leading providers deliver stronger cybersecurity than many in-house teams, reassuring sponsors of compliance with FDA 21 CFR Part 11. Cloud-native risk-based monitoring software market platforms integrate AI engines without hardware constraints, support global collaboration, and simplify upgrades. Hybrid deployment lets firms keep sensitive data on-premise while tapping off-prem resources for analytics, offering a prudent migration path.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High implementation & validation

costs

High implementation & validation

costs

| -2.1% | Global; tougher for small sponsors | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-2.1%

|

Geographic Relevance

:

Global; tougher for small sponsors

|

Impact Timeline

:

Short term (≤ 2 years)

|

Persistent data-privacy /

cybersecurity gaps

Persistent data-privacy /

cybersecurity gaps

| -1.8% | Global; heightened in EU under GDPR | Medium term (2-4 years) | |||

CRO–sponsor change-management

resistance

CRO–sponsor change-management

resistance

| -1.4% | North America & EU focus | Medium term (2-4 years) | |||

Algorithmic bias in AI-based RBM

engines

Algorithmic bias in AI-based RBM

engines

| -1.1% | Developed markets using advanced AI | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Implementation & Validation Costs

Computer system validation can absorb 80% more effort if workflows remain manual. Transitioning to the FDA-endorsed “computer software assurance” model demands fresh training and process redesign that many mid-sized companies find hard to fund. End-to-end platform rollouts often span 12–18 months, during which parallel legacy monitoring keeps overall costs high. Smaller biotech firms lacking dedicated IT staff encounter the steepest hurdles when entering the risk-based monitoring software industry.

Persistent Data-Privacy / Cybersecurity Gaps

The 2024 Oracle Health breach underscored risks tied to centralized data environments. GDPR, HIPAA, and local privacy laws add layers of compliance complexity, especially as AI tools require broad data access. Security incidents can jeopardize patient confidentiality and proprietary assets, prompting sponsors to invest in encryption and role-based access controls, which inflate total cost of ownership.

Segment Analysis

By Component: Software Dominance Drives Platform Consolidation

Software accounted for a commanding 67.55% of the risk-based monitoring software market in 2025. Sponsors prioritize platforms that unify data capture, analytics, and audit trails under one interface, satisfying ICH E6(R3) documentation requirements. Vendors such as Medidata introduced streamlined electronic data capture modules like Rave Lite to curb fragmentation and promote end-to-end quality oversight. Services, while smaller, are expanding at a 14.65% CAGR as firms seek specialist guidance to configure key risk indicators and retrain monitoring teams.

Growth in services mirrors the organizational shift toward process transformation. Consultants design RBQM frameworks, manage change adoption, and validate AI algorithms, positioning the services segment as a catalyst for more sophisticated software use. Market leaders offering bundled software-plus-services packages gain an edge by shortening implementation timelines and easing validation burdens.

Note: Segment shares of all individual segments available upon report purchase

By Delivery Mode: Cloud Migration Accelerates Despite Legacy Constraints

Web-hosted platforms still represented 69.10% of spending in 2025, anchored by long-standing deployments. Yet cloud-based options are advancing at a 15.52% CAGR, reflecting demand for elastic computing and global access. Cloud delivery unlocks AI-enabled risk scoring and continuous data feeds that legacy hosting struggles to support.

Resistance lingers among sponsors citing data-sovereignty rules; hybrid models consequently gain traction. Under hybrid deployment, raw subject data can stay on-premise, whereas de-identified analytics run in the cloud, maintaining compliance while exploiting advanced tooling. This bridge strategy smooths the pathway for the risk-based monitoring software market as regulatory comfort with cloud environments grows.

By End User: CRO Expansion Reshapes Market Dynamics

Pharmaceutical and biopharmaceutical firms retained 58.10% share in 2025, leveraging deep capital resources. CROs, however, are the fastest movers at a 13.05% CAGR as outsourcing accelerates. Consolidating CROs now roll out standardized monitoring templates across multi-sponsor portfolios, driving economies of scale.

Academic institutes and site networks adopt risk-based models more selectively due to budget limits, but patient-centric funding initiatives are sparking pilot programs. The surge in CRO demand stimulates competitive differentiation, with providers embedding AI chat assistants and remote-monitoring dashboards to remain attractive to sponsors seeking holistic trial orchestration.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Clinical Trial Phase: Early-Stage Adoption Accelerates Innovation

Phase III trials comprised 51.35% of current deployments in 2025, reflecting the complexity and financial stakes of late-stage programs. Phase I shows the steepest adoption curve at 15.68% CAGR as safety-intensive dose escalation relies on real-time analytics for rapid decision-making.

Adaptive designs in Phase II amplify the need for predictive oversight. Real-world evidence requirements extend RBM principles into Phase IV surveillance, where integrated pharmacovigilance modules blend with monitoring dashboards to track long-term signals. This lifecycle view underscores the versatility of the risk-based monitoring software market.

Note: Segment shares of all individual segments available upon report purchase

By Trial Decentralization Level: Virtual Models Drive Technology Innovation

Conventional site-centric designs held 68.05% revenue in 2025, yet virtual and hybrid models are scaling quickly. Fully decentralized trials post a 14.25% CAGR, fueled by patient convenience and geographic reach. Remote data capture from wearables and tele-visits demands platforms that verify source authenticity and monitor protocol adherence in real time.

Hybrid configurations balance onsite assessments with remote activities, easing the learning curve for sites and regulators. Vendors now integrate identity verification, drug-dispensing oversight, and telehealth video logs within a single platform, solidifying their position in the risk-based monitoring software market.

Geography Analysis

North America retained 36.85% of spending in 2025, underpinned by FDA leadership, strong venture investment, and mature IT infrastructures. Sponsors here increasingly link RBM initiatives to enterprise R&D modernization drives aiming to trim timelines by up to 30%. Heightened cybersecurity scrutiny after the Oracle breach pushed buyers toward platforms with robust compliance pedigrees.

Asia-Pacific exhibits the fastest 14.79% CAGR as China, Japan, and India expand research capacity and harmonize rules with ICH standards. Sponsors leverage the region’s diverse patient pools and cost advantages, while local regulators streamline approval cycles. Australia and South Korea serve as regional coordination hubs, offering advanced digital health frameworks for decentralized monitoring.

Europe maintains steady uptake. EMA endorsement of ICH E6(R3) aligns quality expectations, and GDPR continues to shape data-handling requirements. Western European nations drive platform adoption through established pharma clusters, whereas Eastern Europe attracts cost-sensitive studies needing treatment-naive populations. Sustainability goals also influence buying behavior as virtual monitoring cuts travel-related emissions within the risk-based monitoring software market.

Competitive Landscape

Market Concentration

The market shows moderate concentration, with Oracle, Veeva Systems, and IQVIA holding notable positions through comprehensive suites and global support footprints. Oracle extended its platform with feasibility and recruitment modules in 2024. Veeva upgraded Site Connect to streamline sponsor-site document exchange. IQVIA deepened its alliance with Salesforce to co-develop Life Sciences Cloud, reinforcing end-to-end capabilities.

Specialists such as Signant Health target mid-sized biotech firms via tailored offerings launched under Signant Biotech in July 2024. AI-native entrants focus on anomaly detection and predictive scheduling, differentiating themselves from legacy architectures. Strategic investments, such as Dassault Systèmes acquiring stakes in digital therapeutics providers, extend monitoring tools into real-world evidence and patient-engagement domains.

Competitive intensity encourages platform interoperability and open-API strategies to embed risk-based monitoring software market functions within broader eClinical ecosystems. Vendors combining technology with consulting and site-enablement programs enhance stickiness and cross-sell opportunities.

Risk-Based Monitoring Software Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Dassault Systèmes invested in Click Therapeutics to augment patient-centric digital therapeutics within its Medidata portfolio.

- March 2025: Medidata introduced the Site Insights Program to amplify site feedback and improve engagement.

- January 2025: Suvoda and Greenphire merged to unify randomization, supply management, and patient payments into one clinical-technology platform.

Table of Contents for Risk-Based Monitoring Software Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1High Efficiency & Cost-Saving Versus 100% SDV

- 4.2.2Regulatory Mandates For RBQM In ICH-E6(R3) & FDA Draft Guidance

- 4.2.3Rapid Rise Of Complex, Decentralized & Hybrid Trials

- 4.2.4Cloud-First eClinical Ecosystems Lowering IT Barriers

- 4.2.5AI-Driven Predictive Risk Scoring Improves Interim ROI

- 4.2.6Synthetic Clinical Data Enabling Continuous Risk Surveillance

- 4.3Market Restraints

- 4.3.1High Implementation & Validation Costs

- 4.3.2Persistent Data-Privacy / Cybersecurity Gaps

- 4.3.3CRO–Sponsor Change-Management Resistance

- 4.3.4Algorithmic Bias Risks In AI-Based RBM Engines

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Component

- 5.1.1Software

- 5.1.2Services

- 5.2By Delivery Mode

- 5.2.1Web-Hosted

- 5.2.2Cloud-Based (SaaS)

- 5.2.3On-Premise

- 5.2.4Hybrid

- 5.3By End User

- 5.3.1Pharmaceutical & Biopharmaceutical Companies

- 5.3.2Medical Device Companies

- 5.3.3Contract Research Organizations (CROs)

- 5.3.4Academic Research Institutes

- 5.3.5Other End Users

- 5.4By Clinical Trial Phase

- 5.4.1Phase I

- 5.4.2Phase II

- 5.4.3Phase III

- 5.4.4Phase IV / Post-Marketing

- 5.5By Trial Decentralization Level

- 5.5.1Conventional Site-Centric

- 5.5.2Hybrid

- 5.5.3Fully Decentralized / Virtual

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Oracle

- 6.3.2Dassault Systèmes

- 6.3.3Veeva Systems

- 6.3.4Signant Health

- 6.3.5Parexel

- 6.3.6IQVIA

- 6.3.7IBM

- 6.3.8Clario

- 6.3.9MedNet Solutions

- 6.3.10DSG Inc.

- 6.3.11Cyntegrity

- 6.3.12Medable

- 6.3.13ArisGlobal

- 6.3.14Cloudbyz

- 6.3.15OpenClinica

- 6.3.16Anju Software

- 6.3.17BioClinica

- 6.3.18eClinical Solutions

- 6.3.19MasterControl

- 6.3.20DATATRAK

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Global Risk-Based Monitoring Software Market Report Scope

As per the scope of the report, the risk-based monitoring (RBM) software market centers on software solutions tailored to streamline clinical trial monitoring. These solutions prioritize resources based on identified risks, boost efficiency, and ensure regulatory compliance. They leverage advanced analytics and real-time data monitoring to enhance trial outcomes, reduce costs, and ease resource burdens. The risk-based monitoring software market is segmented by component, delivery mode, end-user, and geography. By component, the market is segmented into software and services. The market is segmented by delivery mode into web-based (on-demand), on-premise, and cloud-based (SAAS). The market is segmented by end users into pharma and biopharmaceutical companies, medical device companies, contract research organizations (CROs), and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market sizing and forecasts are done based on value (in USD).