Teleradiology Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

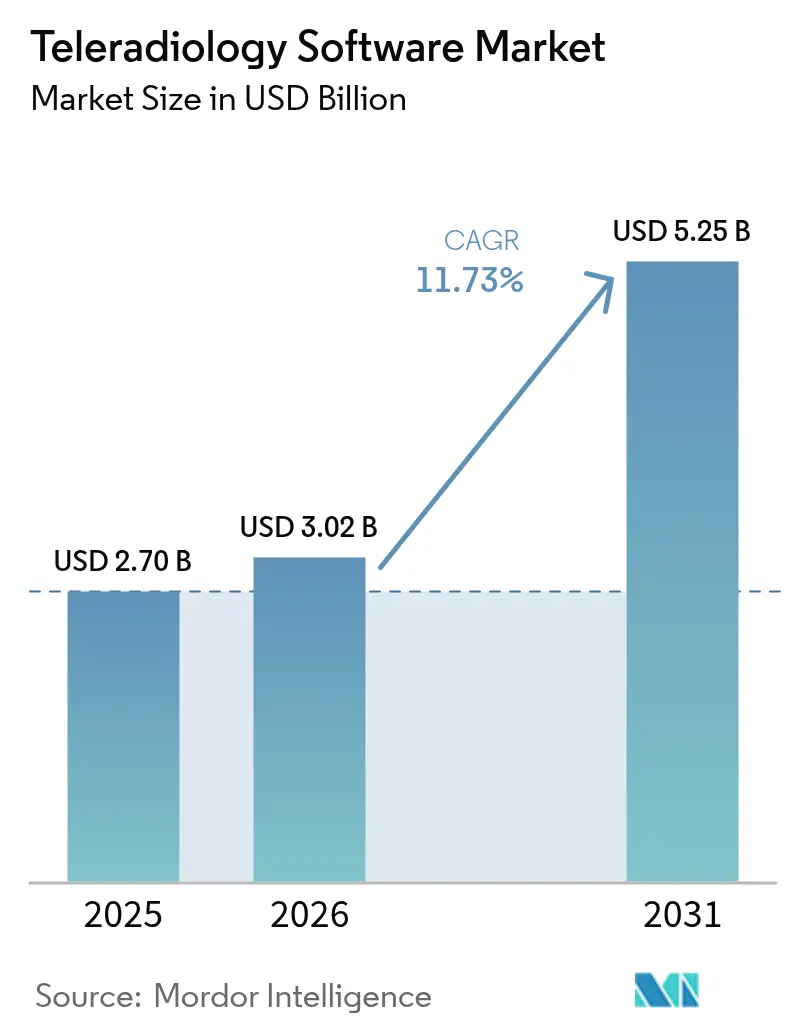

| Market Size (2026) | USD 3.02 Billion |

| Market Size (2031) | USD 5.25 Billion |

| Growth Rate (2026 - 2031) | 11.73% CAGR |

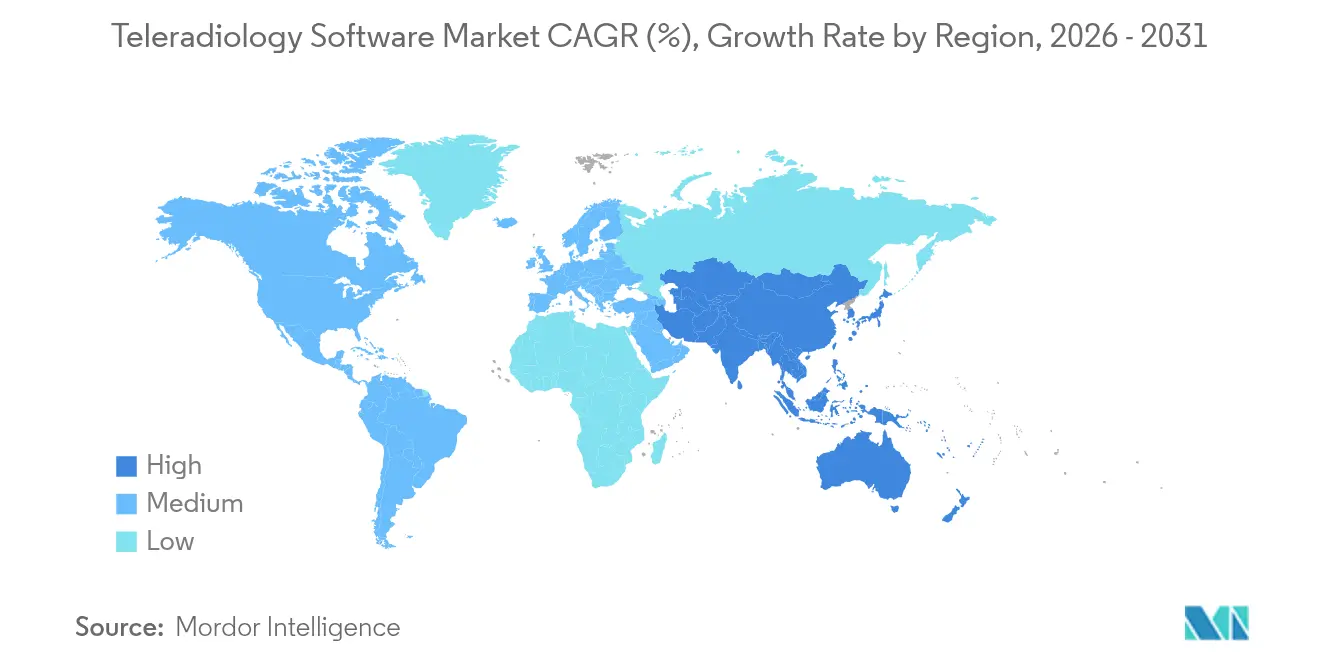

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

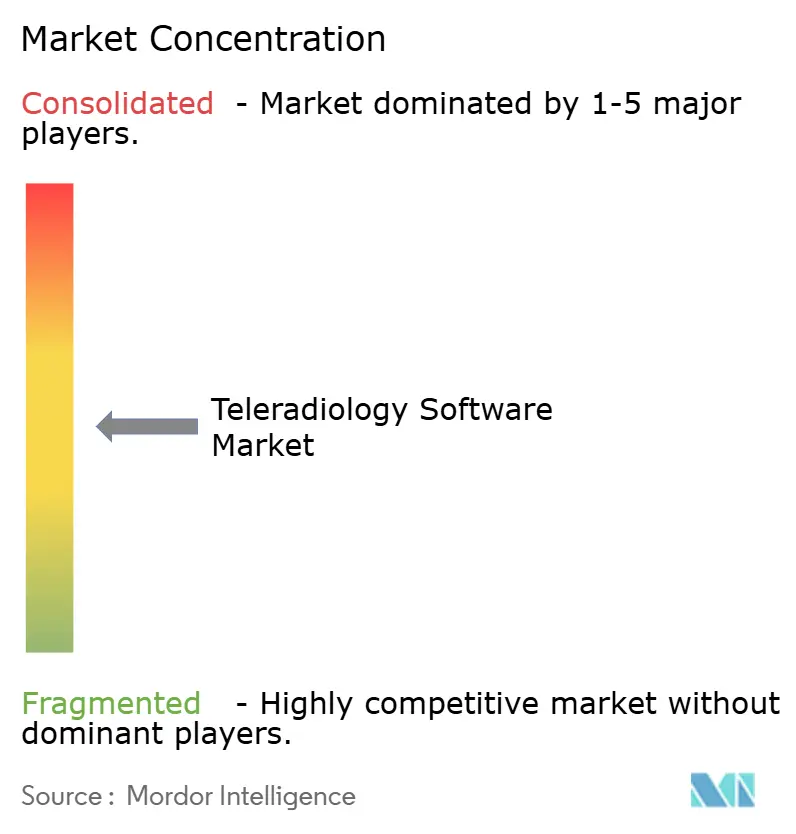

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Teleradiology Software Market Analysis by Mordor Intelligence

The Teleradiology Software market size is expected to grow from USD 2.70 billion in 2025 to USD 3.02 billion in 2026 and is forecast to reach USD 5.25 billion by 2031 at 11.73% CAGR over 2026-2031. The teleradiology software market size trajectory rests on three mutually reinforcing forces: a widening global radiologist shortfall, imaging volumes that climb 3-4% a year, and cloud architectures that allow instant scale. Hospitals deploy the platforms to secure 24/7 subspecialist coverage, while diagnostic centers harness them to extend hours without hiring on-site radiologists. Technology vendors are embedding AI triage and structured-report modules, which boost reading productivity by up to 30% and help mitigate burnout. Regulations now formally recognize remote preliminary reads, and growing reimbursement parity is steering budgets toward digital infrastructure. Together, these dynamics sustain double-digit growth while intensifying competition around cloud-native, AI-ready ecosystems.

Key Report Takeaways

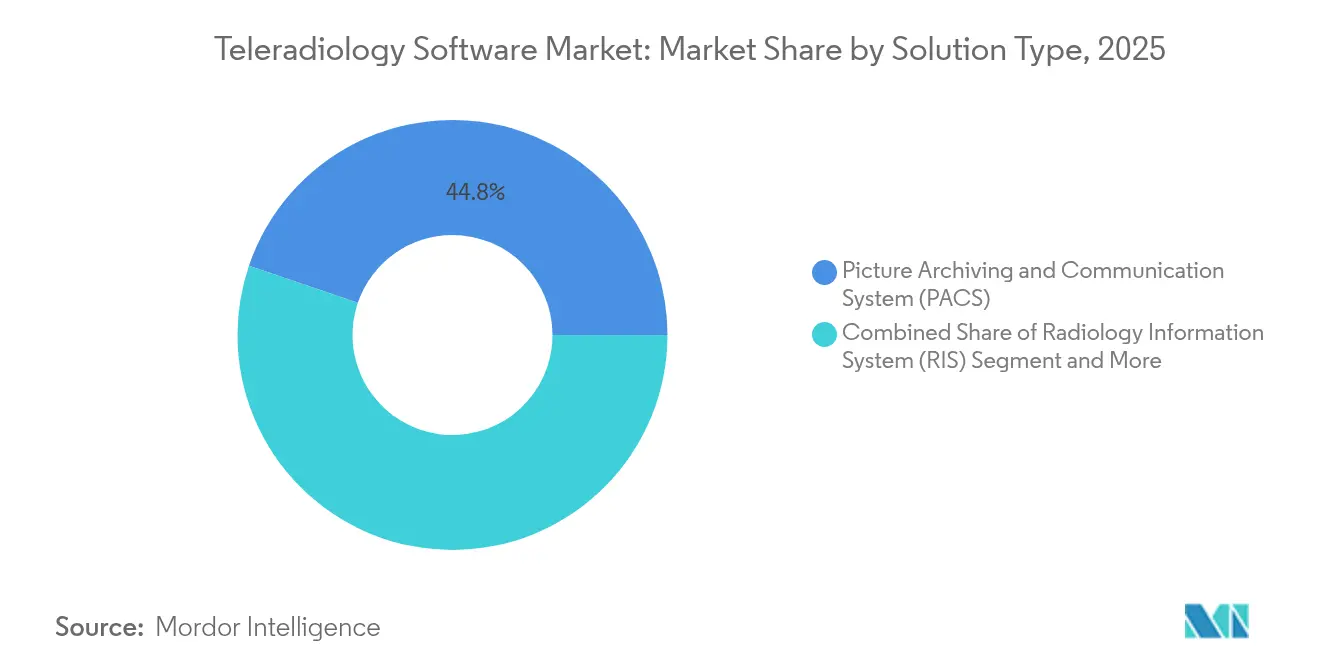

- By solution type, Picture Archiving and Communication Systems (PACS) led with 44.78% revenue share in 2025, whereas Vendor-Neutral Archive (VNA) is projected to advance at a 12.83% CAGR through 2031.

- By deployment mode, cloud-based platforms accounted for 61.83% of the teleradiology software market share in 2025 and are slated to grow at 12.55% CAGR to 2031.

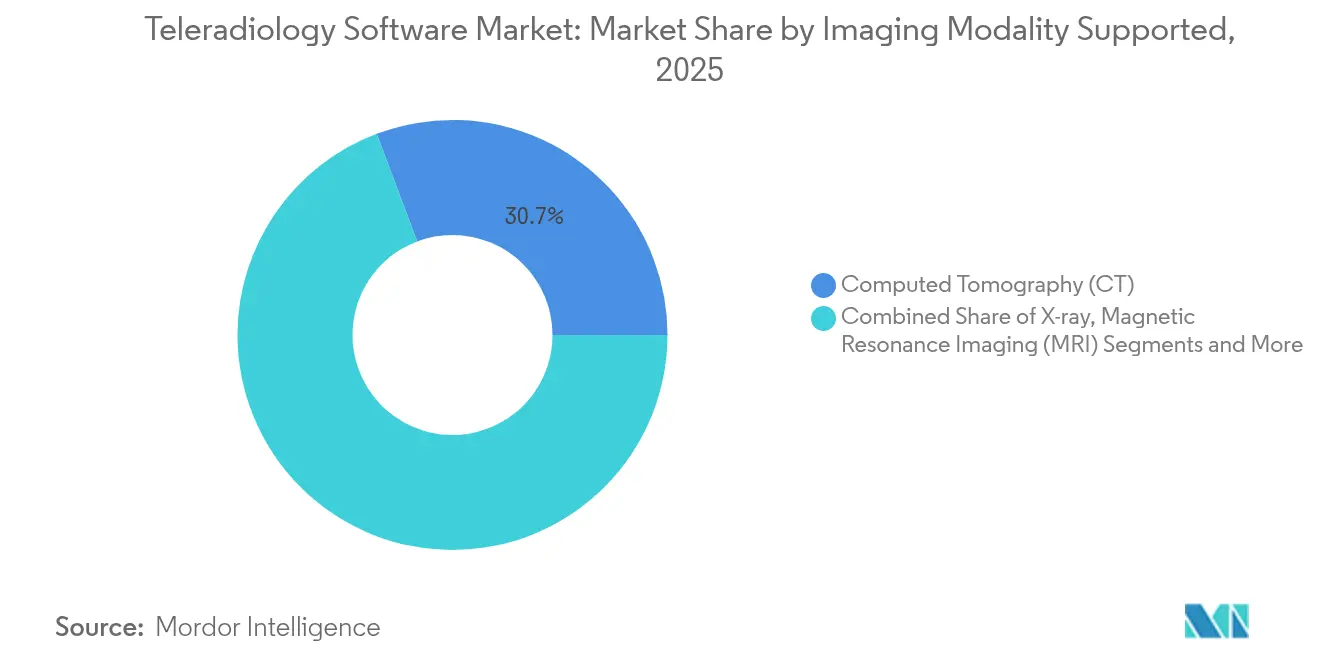

- By imaging modality, Computed Tomography (CT) captured 30.74% of the teleradiology software market size in 2025; Magnetic Resonance Imaging (MRI) shows the fastest 12.71% CAGR to 2031.

- By end user, hospitals retained 60.52% share in 2025, while diagnostic imaging centers exhibit the quickest 12.42% CAGR up to 2031.

- By geography, North America commanded 39.27% share in 2025, yet Asia-Pacific is on course for a 13.18% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Teleradiology Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Chronic Disease Burden and Imaging Volume | +2.8% | Global, with concentration in aging populations of North America, Europe, and Japan | Long term (≥ 4 years) |

| Global Radiologist Shortage and Outsourcing Surge | +3.2% | Global, most acute in rural areas of US, UK, and emerging markets | Medium term (2-4 years) |

| Rapid Adoption of Cloud PACS / VNA Architectures | +2.1% | North America & EU leading, APAC following rapidly | Medium term (2-4 years) |

| Rise of Telehealth and Remote Care Trends | +1.9% | Global, accelerated in post-COVID healthcare systems | Short term (≤ 2 years) |

| Stronger Regulatory and Infrastructure Support | +1.6% | North America & EU primarily, expanding to APAC | Medium term (2-4 years) |

| Hardware and Edge AI Integration at Point-of-Care | +1.4% | North America & EU leading, selective adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Chronic Disease Burden and Imaging Volume

Medical imaging demand is set to climb another 27% by 2055, amplifying pressure on limited radiology resources.[1]Source: Eric W. Christensen, “Projected US Imaging Utilization, 2025 to 2055,” PubMed, pubmed.ncbi.nlm.nih.gov CT studies alone could rise 25.1%, while nuclear medicine and X-ray work keep pace. With 4.2 billion examinations already performed each year, health systems depend on teleradiology to flex reading capacity, distribute subspecialist expertise, and keep turnaround times within quality benchmarks. The ability to route overflow studies across national or even continental networks preserves continuity of care and mitigates appointment backlogs.

Global Radiologist Shortage and Outsourcing Surge

The United States may face a deficit of up to 124,000 physicians by 2034, and radiology posts are among the hardest to fill. The United Kingdom reports a 30% radiologist gap, while attrition sits near 13% annually. Productivity metrics show teleradiology groups processing as many as one-third more studies per reader than conventional onsite teams. As rural and community hospitals struggle to staff night and weekend shifts, outsourcing becomes a structural solution, solidifying demand for software that coordinates multi-site workflows and credentialing.

Rapid Adoption of Cloud PACS / VNA Architectures

Hospitals migrating imaging archives to the cloud cut operational expenses by up to 30% and sidestep recurrent hardware-refresh cycles. VNA rollouts further ease vendor lock-in and enable seamless AI integration, evidenced by the Children’s Hospital of Philadelphia saving USD 3 million across five years after its VNA move. These economics underpin the sustained cloud preference throughout the teleradiology software market.

Rise of Telehealth and Remote-Care Trends

Virtual consultations have jumped from 1% to 17% of all visits post-2020, normalizing remote service delivery. National funding schemes, such as the EU Recovery and Resilience Facility that allocates 20% of health budgets for digital initiatives, embed imaging interoperability into wider telehealth ecosystems, reinforcing cross-border reading workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Data-Privacy Compliance (HIPAA/GDPR) Costs | -1.8% | North America & EU primarily, expanding globally | Long term (≥ 4 years) |

| High Integration and Change-Management Costs for Small Sites | -1.5% | Global, particularly affecting smaller healthcare providers | Medium term (2-4 years) |

| Cloud-Vendor Lock-In Via High Egress Fees | -1.2% | Global, most significant in multi-cloud environments | Medium term (2-4 years) |

| Cross-Border Medico-Legal Liability for AI Preliminary Reads | -1.0% | Global, particularly affecting international teleradiology providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Data-Privacy Compliance (HIPAA/GDPR) Costs

Meeting HIPAA encryption rules in the United States and GDPR restrictions in Europe raises deployment expenses, particularly for smaller clinics that lack dedicated security staff. Organizations managing cross-border reads must navigate overlapping consent regulations and incident-reporting duties, often commissioning third-party audits that inflate total cost of ownership. Cybersecurity investments become mandatory as healthcare organizations address increasing cyber threats, with legal implications for clinicians requiring robust incident response plans and encryption protocols.[2]Source: Chukwuka Elendu et al., “Legal Implications for Clinicians in Cybersecurity,” Medicine, journals.lww.com

Cross-Border Medico-Legal Liability for AI Preliminary Reads

When AI flags urgent findings across jurisdictions, questions arise over which clinician, algorithm vendor, or facility holds ultimate responsibility. Analysis of 299 teleradiology malpractice cases shows 35.6% related to patient death and higher median indemnities compared with onsite radiology. The proposed EU AI Liability Directive heightens exposure by treating diagnostic algorithms as high-risk medical devices. Insurers respond by raising premiums, making some providers wary of aggressive AI rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: VNA Disrupts Traditional PACS Dominance

PACS remained the anchor technology with 44.78% share in 2025. At the same time, VNA logged a 12.83% CAGR outlook, signaling a pivot toward vendor neutrality and enterprise imaging consolidation. The teleradiology software market size attached to VNA is set to rise sharply as organizations migrate away from siloed archives. Children’s Hospital of Philadelphia reported USD 3 million savings in five years after its VNA transition.

RIS and nascent enterprise platforms now integrate over 110 certified AI apps through single interfaces, as shown by CARPL.ai’s FDA-cleared hub. Such interoperability compresses report-turnaround times and reduces costly data migrations, giving VNAs tangible economic and clinical advantages.

By Deployment Mode: Cloud Infrastructure Accelerates Market Transformation

Cloud installations represented 61.83% of the teleradiology software market in 2025 and are on track for a 12.55% CAGR. Amazon Web Services underpins GE HealthCare’s Genesis portfolio, which promises one-click elasticity and AI scalability.

On-premise systems persist in defense and academic centers with bespoke latency or sovereignty mandates. Yet hybrid setups emerge, allowing sensitive studies to remain local while leveraging cloud analytics for population health. This balanced approach reconciles compliance with innovation and keeps demand for multi-tier deployment orchestration strong within the teleradiology software market.

By Imaging Modality Supported: MRI Growth Outpaces Traditional Dominance

CT retained 30.74% revenue share in 2025, but MRI posts the fastest 12.71% CAGR through 2031. Increased neurological and musculoskeletal referrals, combined with AI-assisted sequence optimization, elevate MRI throughput and the associated slice count per exam. The teleradiology software market size for MRI workflows grows parallel to these trends.

Ultrasound gains ground via point-of-care probes and autonomous capture pilots co-developed by GE HealthCare and NVIDIA. Mammography incorporates SmartMammo AI to cut recall rates, while PET/SPECT leverages quantitative analytics for oncology staging. Platform vendors therefore configure multimodality viewers and structured reporting templates, cementing ecosystem lock-in.

By End User: Diagnostic Centers Drive Market Expansion

Hospitals controlled 60.52% share in 2025, yet diagnostic imaging centers are sprinting ahead at 12.42% CAGR on the back of outpatient procedure shifts. The teleradiology software market share attached to these centers benefits from evening and weekend coverage strategies that favor outsourced reading.

Consolidation is reshaping the professional landscape: the number of groups with 100+ radiologists has risen 350% over the last decade. Larger entities negotiate enterprise contracts that bundle AI triage, analytics dashboards, and native speech recognition into long-term software-as-a-service deals.

Geography Analysis

North America led with 39.27% share in 2025, buoyed by reimbursable telehealth policies and FDA clearance of more than 1,000 clinical AI tools, 758 of which target radiology. Rural access initiatives channel grants to small hospitals, further propelling the teleradiology software market. Ongoing mergers, such as ONRAD absorbing Direct Radiology, extend independent coverage networks and promote standardized workflow software.

Asia-Pacific registers the quickest 13.18% CAGR, underpinned by India’s Ayushman Bharat Digital Mission that issues unique health IDs ready for image exchange. Indonesia’s launch of PT. Teleradiologi Center Indonesia widens subspecialist access, while Australia’s National Digital Health Strategy funds secure image-sharing grids. Combined, these initiatives lower entry barriers for cloud PACS vendors and local startups.

Europe shows steady adoption, aided by the EUR 4 billion Hospital Future Act that scored German hospitals at just 33.3 on a 100-point digitization index, spotlighting investment gaps. The EU Recovery and Resilience Facility stipulates that a fifth of spending targets digital infrastructure, catalyzing cross-border image-sharing pilots and harmonized medico-legal frameworks. Middle East, Africa, and South America remain nascent, yet public cloud rollouts and urban cancer-center build-outs are laying foundational demand for the teleradiology software market.

Competitive Landscape

Consolidation is accelerating, though the top five vendors still control a substantial combined revenue, pointing to moderate fragmentation. Private-equity activity funds roll-ups such as Radiology Partners’ multistate acquisitions that create scale to negotiate AI licences.

Competitive moats now revolve around cloud readiness and end-to-end orchestration. GE HealthCare links its Centricity viewer to NVIDIA Clara for de-noising and triage, Siemens Healthineers embeds DeepHealth mammography AI, and Sectra integrates zero-footprint viewers. Pure-play providers like Intelerad differentiate through vendor-neutral ingestion and outcome analytics, partnering with RADPAIR to speed structured reports.

Strategic moves center on AI portfolios, multi-tenant cloud hosting, and reimbursement consultancy. Konica Minolta pairs its Exa platform with NewVue’s curation engine, while ZettaHealth debuts the first ERP tuned to radiology group billing. These offerings bundle revenue-cycle modules and credentialing management, locking customers into broader ecosystems and augmenting the teleradiology software market growth curve.

Teleradiology Software Industry Leaders

Carestream Health

Telerad Tech

GE HealthCare

Koninklijke Philips N.V.

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Konica Minolta Healthcare Americas partnered with NewVue to launch Exa Teleradiology, Powered by NewVue.

- February 2025: ZettaHealth Solutions released Z-Suite, an ERP/BIS built for radiology reading groups and teleradiology providers.

- September 2024: Experity enhanced its teleradiology over-read service by integrating FDA-approved AI for fracture detection.

Global Teleradiology Software Market Report Scope

As per the scope of the report, teleradiology is the transmission of radiological patient images, such as X-rays, CTs, and MRIs, from one site to another for the reason of sharing studies with other radiologists and physicians.

Teleradiology enhances patient care by allowing radiologists to provide services without having to be at the location of the patient. The teleradiology software market is segmented by type (radiology information system, picture archive, communication system, vendor-neutral archive), modality (cloud-based, on-premise), and geography North America, Europe, Asia-Pacific, Middle East and Africa, South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Radiology Information System (RIS) |

| Picture Archiving & Communication System (PACS) |

| Vendor-Neutral Archive (VNA) |

| Other Solution Types |

| Cloud-Based |

| On-Premise |

| X-ray |

| Computed Tomography (CT) |

| Magnetic Resonance Imaging (MRI) |

| Ultrasound |

| Nuclear Imaging (PET/SPECT) |

| Mammography |

| Hospitals |

| Diagnostic Imaging Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Radiology Information System (RIS) | |

| Picture Archiving & Communication System (PACS) | ||

| Vendor-Neutral Archive (VNA) | ||

| Other Solution Types | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| By Imaging Modality Supported | X-ray | |

| Computed Tomography (CT) | ||

| Magnetic Resonance Imaging (MRI) | ||

| Ultrasound | ||

| Nuclear Imaging (PET/SPECT) | ||

| Mammography | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the teleradiology software market?

The market is valued at USD 3.02 billion in 2026 and is forecast to hit USD 5.25 billion by 2031.

Which deployment model is growing fastest?

Cloud-based platforms, already holding 61.83% share in 2025, are expanding at 12.55% CAGR thanks to scalability and lower maintenance costs.

Why are diagnostic imaging centers adopting teleradiology faster than hospitals?

Outpatient migration and the need for subspecialist coverage without on-site hires drive a 12.42% CAGR among diagnostic centers.

Which imaging modality will contribute most to future growth?

MRI is projected to grow at 12.71% CAGR, outpacing CT even though CT remains the largest revenue contributor.

What regions present the strongest expansion opportunities?

Asia-Pacific is on track for a 13.18% CAGR due to national digitization programs and investments in imaging infrastructure.

How is AI influencing competitive dynamics?

FDA clearance of 1,000+ clinical AI applications, most in radiology, favors vendors that can embed triage and structured-report tools within cloud-native workflows, creating new competitive advantages.

Page last updated on: