Patient Safety And Risk Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

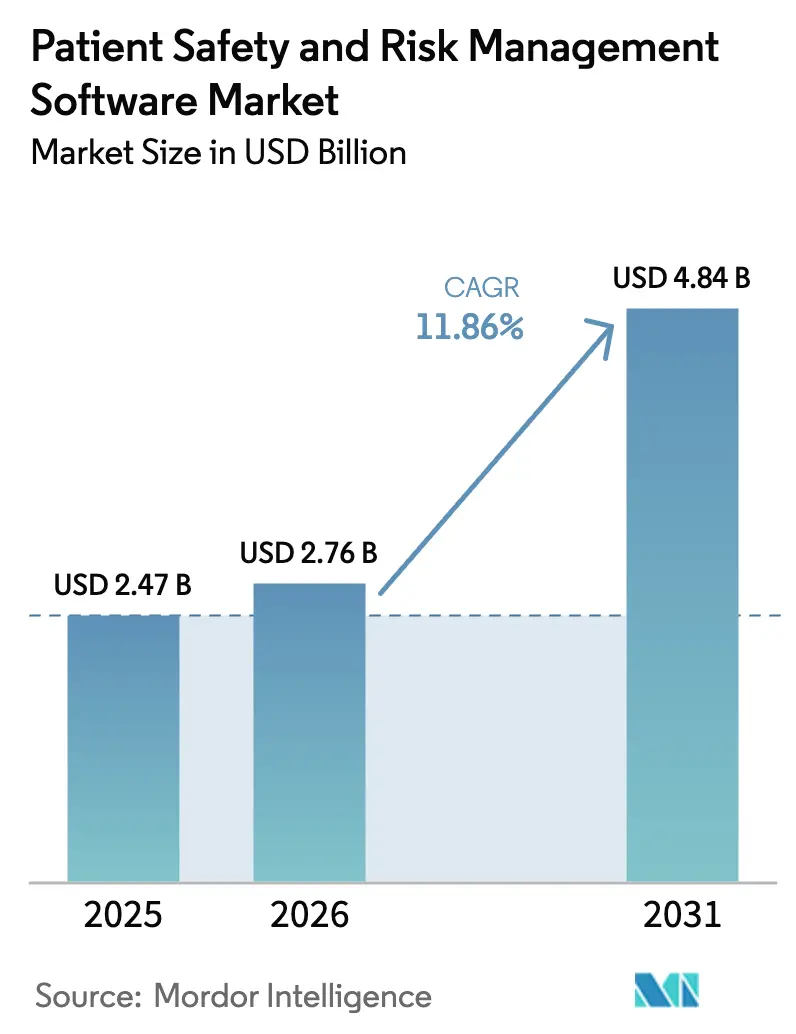

| Market Size (2026) | USD 2.76 Billion |

| Market Size (2031) | USD 4.84 Billion |

| Growth Rate (2026 - 2031) | 11.86% CAGR |

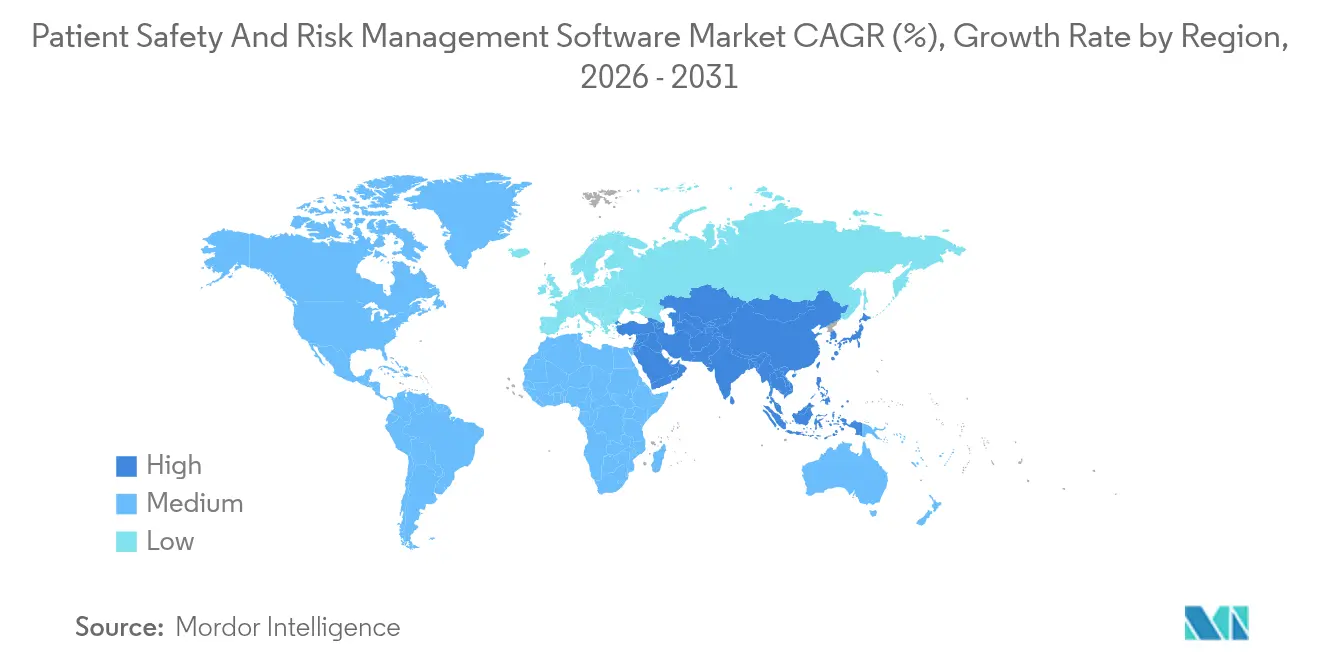

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Patient Safety And Risk Management Software Market Analysis by Mordor Intelligence

Patient Safety and Risk Management Software market size in 2026 is estimated at USD 2.76 billion, growing from 2025 value of USD 2.47 billion with 2031 projections showing USD 4.84 billion, growing at 11.86% CAGR over 2026-2031. The surge is closely tied to mandated incident-reporting rules, soaring malpractice liabilities, and the demand for transparent, AI-enabled decision support. Hospitals are modernizing workflows to satisfy the Centers for Medicare & Medicaid Services (CMS) Patient Safety Structural Measure and the Office of the National Coordinator’s algorithm-transparency requirements.[1]Centers for Medicare & Medicaid Services, “Calendar Year 2024 Program Requirements,” CMS, cms.govRisk analytics, hybrid cloud deployments, and EHR-integrated platforms underpin competitive advantage, while cybersecurity threats and legacy-system complexity remain core adoption hurdles. Small facilities view cloud subscriptions as a cost-effective path to compliance, whereas large health systems leverage scale to roll out enterprise-wide suites that combine patient-safety, claims, and cybersecurity monitoring.

Key Report Takeaways

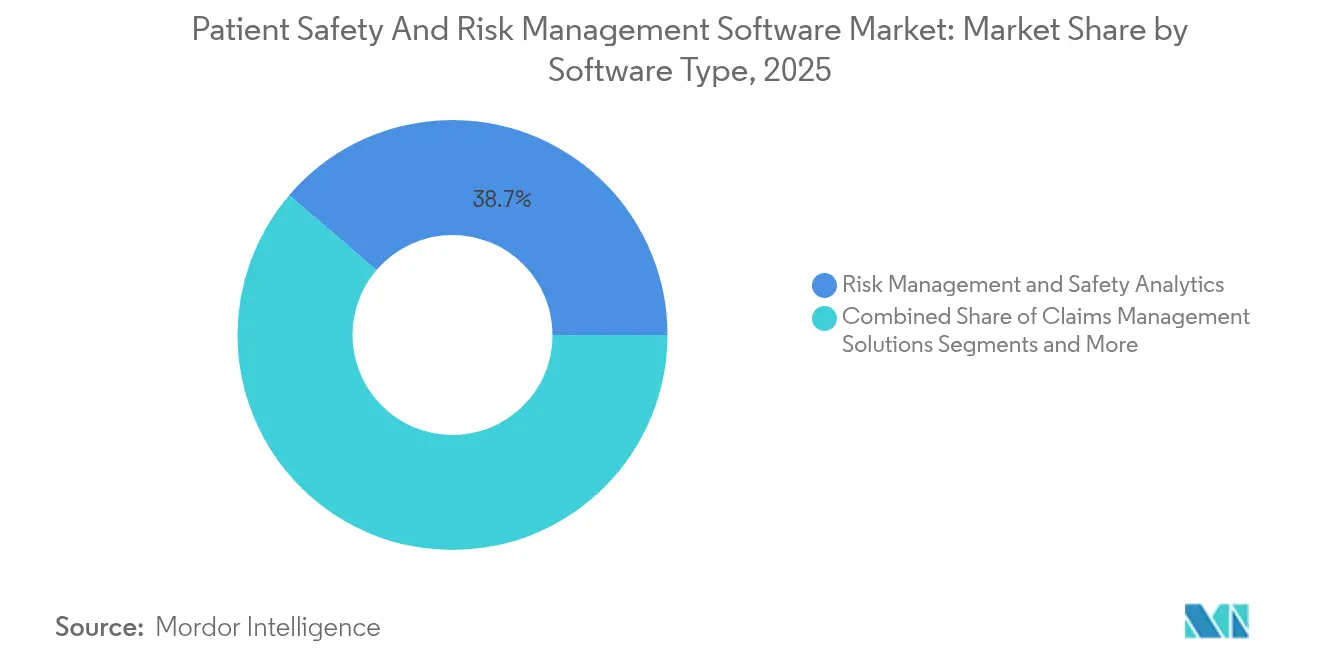

- By software type, Risk Management & Safety Analytics led with 38.74% of Patient Safety and Risk Management Software market share in 2025; Compliance & Audit Management is projected to post the fastest 16.21% CAGR through 2031.

- By deployment mode, cloud accounted for 70.92% share of the Patient Safety and Risk Management Software market size in 2025, while hybrid models are poised to grow at 14.99% CAGR to 2031.

- By organization size, large providers (≥500 beds) captured 49.32% Patient Safety and Risk Management Software market share in 2025; small facilities (<100 beds) are set to expand at a 14.31% CAGR over 2026-2031.

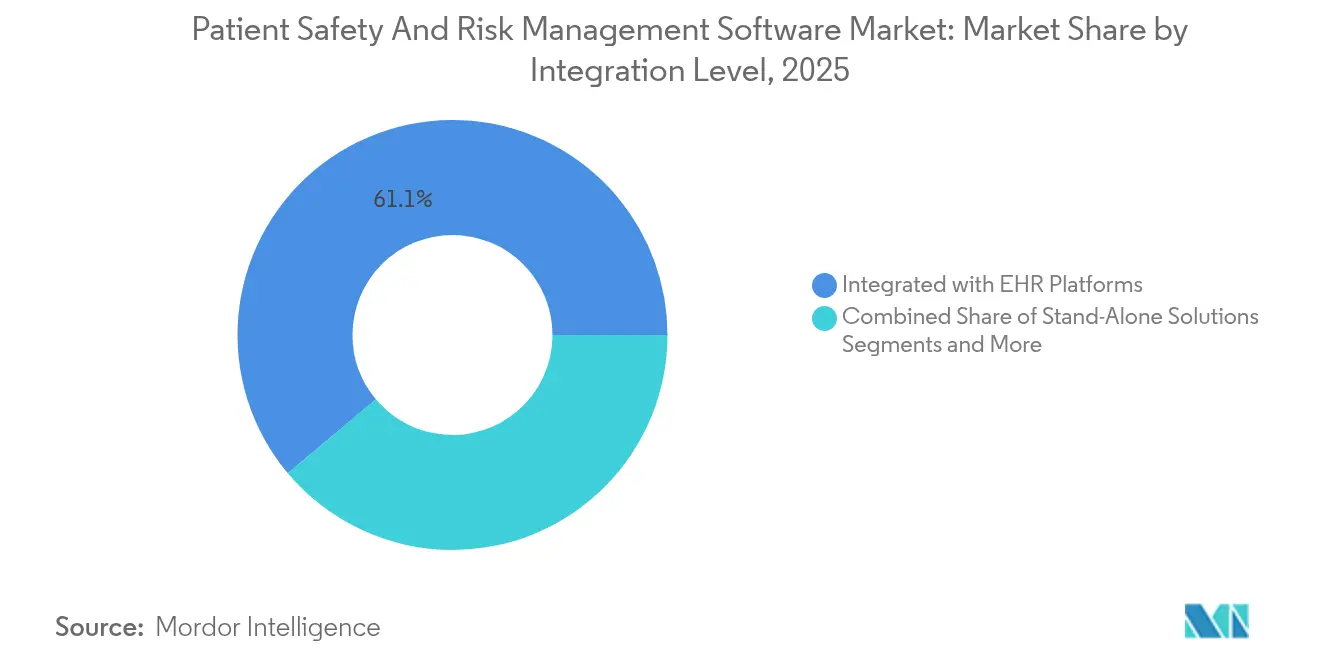

- By integration level, solutions embedded in EHR platforms claimed 61.11% share of the Patient Safety and Risk Management Software market size in 2025 and will accelerate at 15.41% CAGR through 2031.

- By end-user, hospitals took a 51.02% stake in the Patient Safety and Risk Management Software market in 2025, while home-healthcare providers are forecast to climb at a 15.62% CAGR to 2031.

- By geography, North America remained dominant with 45.83% share of the Patient Safety and Risk Management Software market in 2025; Asia-Pacific is projected to log the quickest 14.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Patient Safety And Risk Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Regulatory Mandates For Incident Reporting | + 2.8% | Global, strongest in North America & EU | Short term (≤ 2 years) |

| Rising Adoption Of EHR Integration & Interoperability | + 2.1% | Global, led by North America, expanding to APAC | Medium term (2-4 years) |

| Growth In Adverse-Event Litigation Costs Driving Risk Solutions | + 1.9% | North America & EU primarily | Medium term (2-4 years) |

| Shift To Value-Based Care Metrics Incentivising Safety Software | + 1.7% | North America, expanding to EU & APAC | Long term (≥ 4 years) |

| AI-Enabled Predictive Analytics Reduce Sentinel Events | + 2.3% | Global, early adoption in North America & EU | Medium term (2-4 years) |

| Real-Time Location Systems Data For Near-Miss Capture | + 1.5% | Global, strongest uptake in large healthcare systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates for Incident Reporting

CMS began enforcing the Patient Safety Structural Measure in 2024, compelling providers to complete SAFER Guides assessments and safety-culture surveys under threat of payment penalties. Europe followed with the European Health Data Space rule effective March 2025, obligating standardized, cross-border safety data exchange.[2]European Commission, “European Health Data Space Regulation (EHDS),” European Commission, ec.europa.euThe focus on real-time disclosure accelerates the Patient Safety and Risk Management Software market as providers replace manual logs with automated, analytics-ready platforms. Vendors that document measurable safety ROI gain preference because regulators now emphasize outcome dashboards during inspections.

EHR Integration and Interoperability Push

ONC’s United States Core Data for Interoperability v4 obliges vendors to offer transparent algorithm-logic and seamless data movement between safety suites and clinical records. Clinician frustration is acute—47% struggle to retrieve outside data inside their EHRs. Platform providers that furnish turnkey APIs and single-sign-on workflows see markedly quicker enterprise rollout, fuelling demand across the Patient Safety and Risk Management Software market.

Escalating Litigation Costs

Soaring malpractice verdicts motivate hospitals to adopt predictive-risk engines that log every decision point for defensibility.[3]X. Liu et al., “Artificial Intelligence for Patient Safety: A Systematic Review,” Frontiers in Medicine, frontiersin.orgThe Stanford HAI policy note warns that courts will scrutinize AI-powered tools under evolving liability frameworks, nudging providers toward enterprise systems that maintain auditable AI outputs. Consequently, integrated risk platforms that marry claims, peer review, and safety surveillance deliver dual value—proactive harm reduction and airtight legal evidence—which accelerates Patient Safety and Risk Management Software market adoption.

Shift to Value-Based Care Incentives

The PSI-90 composite now feeds directly into CMS’s Hospital-Acquired Conditions Reduction Program, tying reimbursement to safety metrics. Improved performance boosts star ratings and unlocks shared-savings bonuses, positioning safety software as a profit lever instead of a cost center. Providers are therefore acquiring AI-enabled dashboards that correlate interventions with avoided readmissions, cementing steady spend across the Patient Safety and Risk Management Software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity With Legacy HIS | -1.8% | Global, most severe in North America & EU | Medium term (2-4 years) |

| High Initial Investment & Training Costs | -1.2% | Global, particularly affecting smaller organizations | Short term (≤ 2 years) |

| Cyber-Security Concerns Around Aggregated Safety Data | -1.4% | Global, heightened in regions with strict data protection | Long term (≥ 4 years) |

| Vendor Lock-In Limiting Modular Upgrades | -0.9% | Global, most pronounced in mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy HIS

Fragmented IT stacks hamper rollout; the 2024 Compass Survey showed multi-vendor hospitals report quality lapses and clinician burnout because of disconnected systems. Interfaces must ensure data fidelity while respecting varied terminologies, delaying projects and tempering near-term growth in the Patient Safety and Risk Management Software market.

Cybersecurity Concerns over Aggregated Data

Ransomware incidents surged 300%, striking 108 million records in 2024. Consolidating sensitive safety logs in cloud stores raises breach stakes. Hesitant buyers often pilot hybrid deployments that keep patient identifiers on-premise, slowing full cloud migration but fostering demand for zero-trust-ready, encryption-first suites within the broader Patient Safety and Risk Management Software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software Type: Analytics Drive Risk Prevention

Risk Management & Safety Analytics contributed 38.74% to the Patient Safety and Risk Management Software market in 2025, converting raw event data into forward-looking alerts that avert sentinel events. Compliance & Audit Management is tracking the quickest 16.21% CAGR, powered by fresh audit-trail obligations in the European Health Data Space rule. Vendors now bundle claims, root-cause, and incident modules inside unified dashboards, positioning platform suites to eclipse siloed tools across the Patient Safety and Risk Management Software market.

A second wave of AI embeds natural-language processing into incident narratives, auto-classifying harm severity and mapping corrective actions. Health systems prioritize modules that demonstrate shorter investigation cycles and reduced malpractice reserves. As analytics establishes evidence of 92% medication-error reductions in long-term care settings, buyers push for enterprise licenses that amplify return on investment and swell the Patient Safety and Risk Management Software market size for cross-departmental deployments.

By Deployment Mode: Hybrid Models Gain Momentum

Cloud platforms owned 70.92% share of the Patient Safety and Risk Management Software market size in 2025, reflecting pay-as-you-grow economics. Hybrid architectures, however, are expanding fastest at 14.99% CAGR because they let providers retain PHI behind hospital firewalls while exploiting cloud-based AI pipelines. Systems integrators report shorter go-lives when hospitals adopt modular cloud kernels that synchronize nightly with on-premise databases.

Large multistate networks often host predictive-analytics sandboxes in hyperscale clouds, then replicate sanitized insights to on-prem repositories, striking a balance between innovation and security. Meanwhile, small hospitals gravitate toward single-tenant SaaS because vendor-managed upgrades shield limited IT teams from patching chores, unlocking new entry points for the Patient Safety and Risk Management Software market.

By Organization Size: Small Facilities Accelerate Adoption

Large health systems (≥500 beds) held 49.32% Patient Safety and Risk Management Software market share in 2025, but the small-facility cohort (<100 beds) is climbing at 14.31% CAGR as cash-conscious hospitals hunt subscription tiers starting below USD 50,000 annually. Small sites view the software as insurance against non-performance penalties under CMS’s PSI-90 scorecard. Vendors catering to this niche tout pre-built policy libraries and wizard-driven configuration that slashes training loads.

Medium-sized hospitals channel investments into advanced workflow engine add-ons that automate root-cause task assignments. The Patient Safety and Risk Management Software industry thus segments along resource depth: enterprise buyers want broad feature maps, whereas community facilities prioritize affordability and turnkey compliance.

By Integration Level: EHR Platforms Lead Connectivity

Solutions embedded directly in electronic health records controlled 61.11% of the Patient Safety and Risk Management Software market in 2025 and are projected to grow at 15.41% CAGR, propelled by ONC’s interoperability edicts. Embedded apps harvest structured clinical data without duplicative entry, boosting clinician adoption. Stand-alone tools persist in niche specialties but risk isolation as health-system CIOs consolidate toolsets.

Enterprise GRC suite integrations win favor among academic medical centers that manage reputational, financial, and operational risk inside a single repository. This convergence path enlarges total deal sizes and reinforces the Patient Safety and Risk Management Software market’s strategic value inside C-suite roadmaps.

By End-User: Home Healthcare Emerges as Growth Driver

Hospitals possessed 51.02% share of the Patient Safety and Risk Management Software market in 2025, yet home-healthcare agencies are slated to post the strongest 15.62% CAGR, spurred by complex home-use devices flagged in ECRI’s 2024 hazard list. Remote-first modules monitor vitals and device alarms, routing high-risk events back to supervising clinicians.

Ambulatory and long-term care centers integrate mobile incident apps, enabling caregivers to log near-misses in seconds instead of days. Evidence of 92% cutbacks in adverse-drug events at skilled-nursing facilities galvanizes peer adoption, spreading the Patient Safety and Risk Management Software market across every care continuum touchpoint.

Geography Analysis

North America led with a 45.83% stake in the Patient Safety and Risk Management Software market in 2025, buoyed by strict CMS metrics that tie payments to PSI-90 performance and high litigation payouts that exceed USD 200,000 per claim on average. The ONC rule improving algorithm transparency further compels providers to document AI decision logic, catalyzing platform upgrades. Canadian provinces integrate safety KPIs into bundled-payment pilots, while Mexico’s private hospital groups embed safety analytics to woo medical-tourism clientele. Together, the continent accounts for the largest Patient Safety and Risk Management Software market size.

Europe aligns digital-health policy around the EHDS, demanding cross-border safety-data sharing and rigorous GDPR safeguards—conditions that spark modernization budgets across Germany, France, and the United Kingdom. Providers favor platforms supporting role-based access and anonymization to satisfy data-minimization clauses. The region’s malpractice reforms cap non-economic damages, but heightened regulator scrutiny sustains software spending.

Asia-Pacific registers the fastest 14.61% CAGR through 2031 as India’s Ayushman Bharat Digital Mission constructs longitudinal health records for over half a billion citizens, creating fertile ground for plug-in safety modules. China’s virtual-hospital pilots rely on AI algorithms that require transparent audit trails, opening large contracts for risk-analytics vendors. Japan’s DX road map updates device-tracking mandates, pushing hospitals to procure integrated incident-reporting systems. Collectively, these initiatives expand the Patient Safety and Risk Management Software market across a region of diverse regulatory regimes.

The Middle East’s Gulf Cooperation Council invests heavily in EHR rollouts—over 75% of public facilities operate digital charts, paving the way for safety add-ons. Abu Dhabi’s 2025 partnership with RLDatix to construct a unified safety system signals strong governmental support. Africa and South America remain nascent yet promising: cloud-first offerings bypass capital-intensive data centers, allowing hospital groups in Brazil and Kenya to leapfrog into modern safety programs and enlarge the addressable Patient Safety and Risk Management Software market.

Competitive Landscape

The Patient Safety and Risk Management Software market is fragmented yet consolidating. Inovalon’s February 2024 acquisition of VigiLanz adds advanced clinical-surveillance capabilities to its payer-provider analytics stack. Health Catalyst followed in November 2024, paying USD 43 million for Intraprise Health to fuse cybersecurity intelligence with patient-safety analytics in a single pane of glass. These plays foreshadow more M&A as vendors seek breadth across compliance, cyber, and clinical domains.

Incumbent EHR suppliers embed native incident-reporting plugins, leveraging existing client bases. Best-of-breed challengers counter by offering interoperability toolkits, AI triage, and RTLS data fusion that detect near-misses in real time. Evidence of 92% adverse-event reductions in AI rollouts lends credibility, prompting health systems to pilot machine-learning modules that produce quantifiable savings and enlarge the Patient Safety and Risk Management Software market.

White-space remains in home-health and small-facility segments, where lightweight mobile apps and per-patient pricing resonate. Cybersecurity modules that encrypt safety logs and issue zero-day threat alerts differentiate offerings amid rising attacks. Vendors with validated security certifications (HITRUST, ISO 27001) and open FHIR APIs are gaining ground, shaping future competitive trajectories for the Patient Safety and Risk Management Software market.

Patient Safety And Risk Management Software Industry Leaders

-

RLDatix

-

Origami Risk

-

symplr

-

Cority

-

Clarity Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: PrimeVigilance integrated Oracle Argus to deliver AI-driven pharmacovigilance services and strengthen patient-safety compliance.

- May 2025: Abu Dhabi’s Department of Health partnered with RLDatix to build a unified, intelligent safety platform for the emirate’s providers.

- May 2025: Oracle Health, Cleveland Clinic, and G42 announced a joint AI platform aimed at nation-scale patient-care optimization.

- June 2024: KIMS Hospitals deployed Dozee’s contactless remote-patient monitoring system across smart wards, elevating real-time safety surveillance.

Global Patient Safety And Risk Management Software Market Report Scope

As per the report's scope, patient safety and risk management software refers to the software solutions designed to enhance patient safety, minimize risks, and improve the overall quality of care within healthcare settings.

The patient safety and risk management software market is segmented by software type, deployment mode, and end users. In terms of software, the market is segmented as risk management and safety solutions, claims management solutions, and others. By deployment mode, the market is bifurcated into cloud-based and on-premise. By end-user, the market is segmented into hospitals, ambulatory care centers, long-term care centers, and others. The market is segmented by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.

| Incident Reporting & Management Solutions |

| Risk Management & Safety Analytics |

| Claims Management Solutions |

| Compliance & Audit Management |

| Root-Cause Analysis & Action Tracking |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large (≥500 beds or multi-site systems) |

| Medium (100-499 beds) |

| Small (<100 beds) |

| Stand-Alone Solutions |

| Integrated with EHR Platforms |

| Integrated with Enterprise ERP/GRC Suites |

| Hospitals |

| Ambulatory Care Centres |

| Long-Term Care Centres |

| Specialty Clinics |

| Home Healthcare Providers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Software Type | Incident Reporting & Management Solutions | |

| Risk Management & Safety Analytics | ||

| Claims Management Solutions | ||

| Compliance & Audit Management | ||

| Root-Cause Analysis & Action Tracking | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Large (≥500 beds or multi-site systems) | |

| Medium (100-499 beds) | ||

| Small (<100 beds) | ||

| By Integration Level | Stand-Alone Solutions | |

| Integrated with EHR Platforms | ||

| Integrated with Enterprise ERP/GRC Suites | ||

| By End-User | Hospitals | |

| Ambulatory Care Centres | ||

| Long-Term Care Centres | ||

| Specialty Clinics | ||

| Home Healthcare Providers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Patient Safety and Risk Management Software market?

The market stands at USD 2.76 billion in 2026 and is projected to reach USD 4.84 billion by 2031.

Which software segment holds the largest Patient Safety and Risk Management Software market share?

Risk Management & Safety Analytics leads with 38.74% share in 2025.

Why are hybrid deployments gaining traction in the Patient Safety and Risk Management Software market?

Hybrid models balance cloud analytics with on-premise data control, addressing cybersecurity and compliance needs while enabling AI capabilities.

Which region is expanding fastest in the Patient Safety and Risk Management Software market?

Asia-Pacific, advancing at a 14.61% CAGR through 2031, spurred by large-scale digital-health programs.

How do value-based care models influence spending on patient-safety platforms?

CMS’s PSI-90 metric links reimbursement to safety performance, turning software investments into revenue-impacting decisions for providers.

What cybersecurity measures are buyers demanding from safety-software vendors?

Providers seek zero-trust architectures, end-to-end encryption, and HITRUST or ISO 27001 certifications to safeguard aggregated safety data.

Page last updated on: