Clinical Perinatal Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

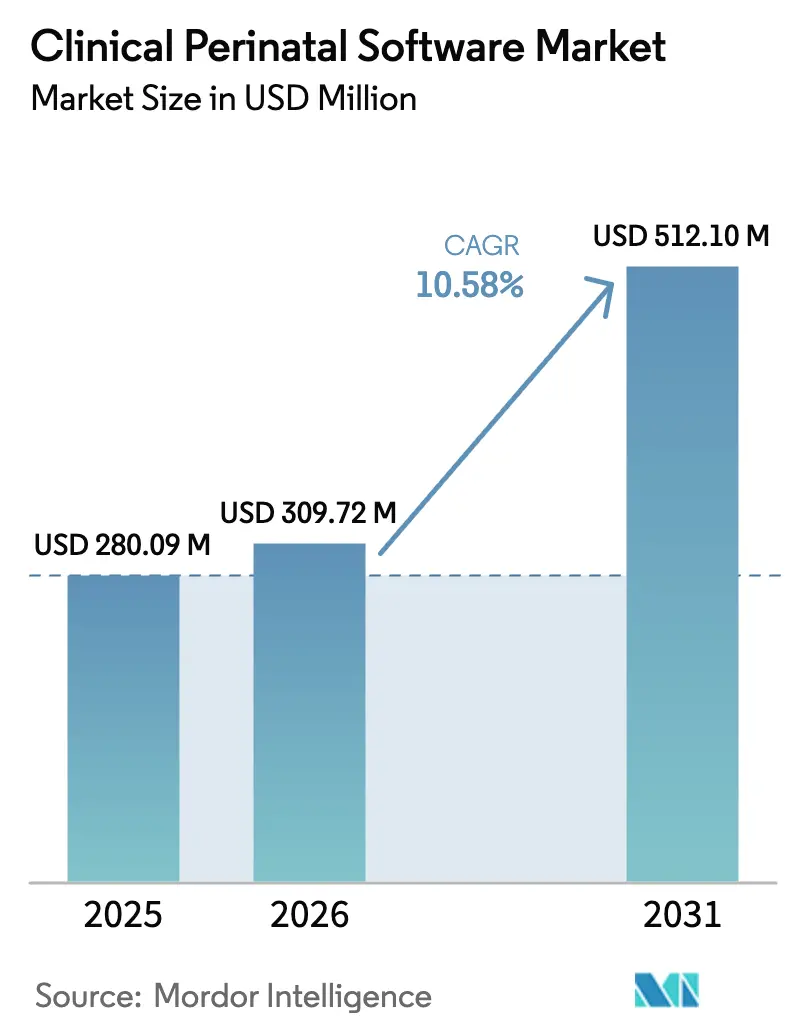

| Market Size (2026) | USD 309.72 Million |

| Market Size (2031) | USD 512.1 Million |

| Growth Rate (2026 - 2031) | 10.58% CAGR |

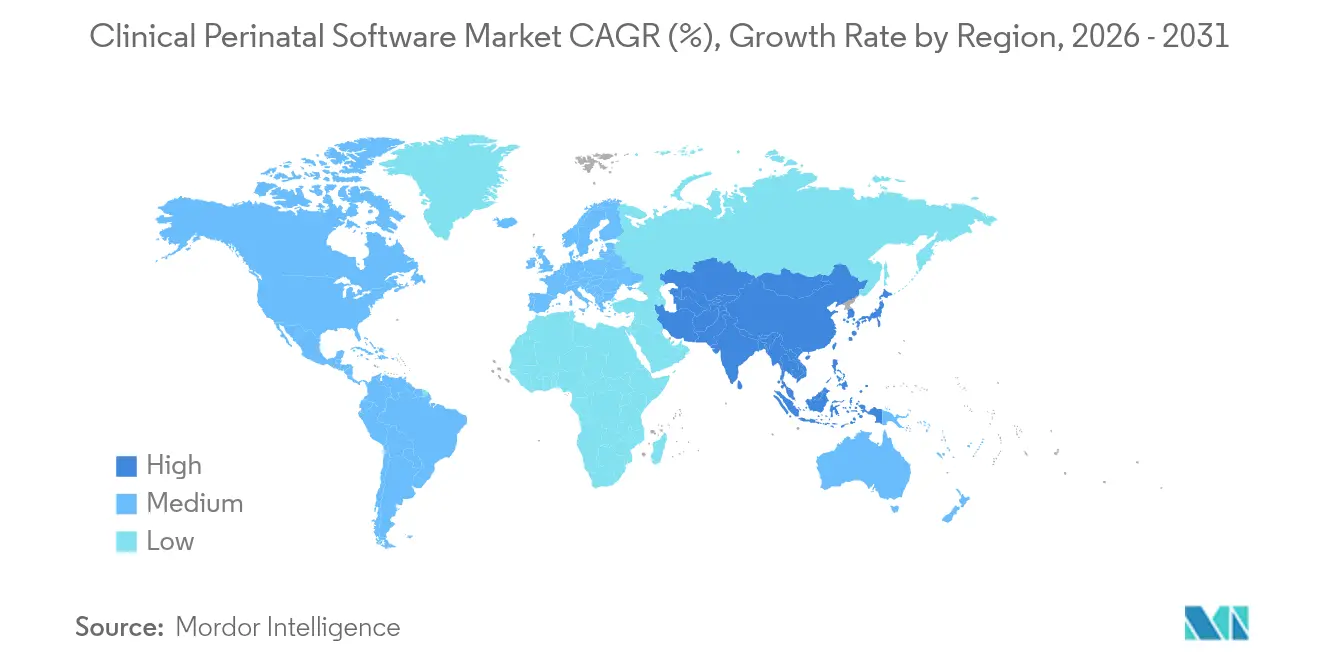

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Perinatal Software Market Analysis by Mordor Intelligence

The Clinical Perinatal Software Market size is expected to grow from USD 280.09 million in 2025 to USD 309.72 million in 2026 and is forecast to reach USD 512.1 million by 2031 at 10.58% CAGR over 2026-2031. This growth trajectory is underpinned by rapid uptake of AI-driven predictive analytics, expanding cloud-hosted interoperability, and policy mandates that elevate maternal-fetal monitoring standards.[1]Source: U.S. Department of Health and Human Services, “Healthy Women, Healthy Pregnancies, Healthy Futures: Action Plan to Improve Maternal Health in America,” aspe.hhs.gov North America remains the largest regional contributor, while Asia-Pacific delivers the quickest gains as digitization initiatives scale across middle-income populations. Integrated product suites dominate purchasing decisions because they unify data capture, decision support, and compliance reporting. Cloud deployment is now the default option for new installations, driven by lower up-front costs and easier multi-site roll-outs. Emerging reimbursement codes for remote cardiotocography (CTG) interpretation and the United States Core Data for Interoperability (USCDI) maternal-health dataset expansion further widen the addressable base.

Key Report Takeaways

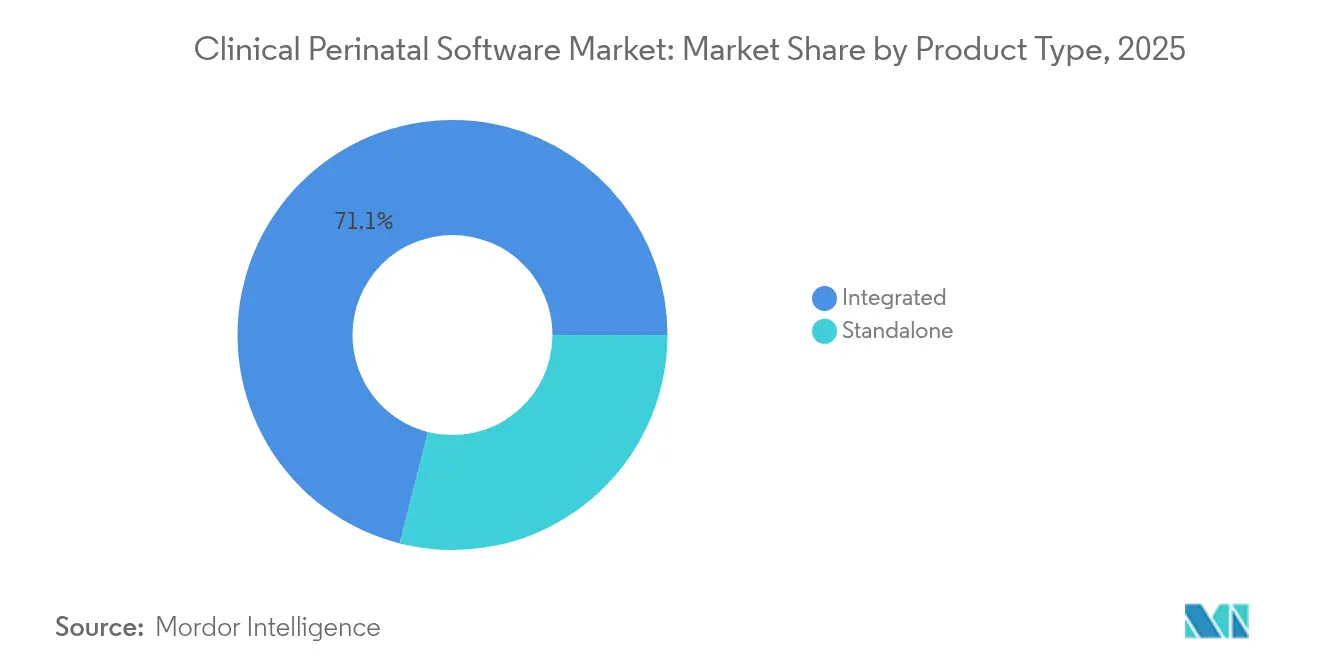

- By product type, integrated solutions commanded 71.05% of clinical perinatal software market share in 2025; standalone offerings are projected to grow at an 11.09% CAGR through 2031.

- By deployment mode, cloud-based platforms are advancing at a 12.21% CAGR to 2031, although on-premises systems still accounted for 68.35% of the clinical perinatal software market size in 2025.

- By end user, hospitals held a 65.42% revenue share of the clinical perinatal software market size in 2025, while maternity clinics are forecast to post an 11.32% CAGR through 2031.

- By application, fetal monitor data services captured 47.9% of the clinical perinatal software market size in 2025 and workflow management applications are set to expand at an 10.97% CAGR by 2031.

- By geography, North America controlled 43.65% of clinical perinatal software market share in 2025; Asia-Pacific is projected to record a 12.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Clinical Perinatal Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Antenatal and Neonatal Adverse-Event Reporting Mandates | +2.1% | North America & EU | Medium term (2-4 years) |

| AI-Driven Predictive Analytics Adoption Across OB-EHR Platforms | +1.8% | Global | Long term (≥ 4 years) |

| Cloud-Hosted Interoperability with Fetal Monitors and EMRs | +1.5% | Global | Short term (≤ 2 years) |

| Growing Government Initiatives and Awareness Regarding Fetal Care | +1.3% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Real-Time Decision-Support Demand in Value-Based Maternity Care | +1.2% | North America & EU | Long term (≥ 4 years) |

| Emerging Reimbursement Codes for Remote CTG Interpretation | +0.9% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Antenatal and Neonatal Adverse-Event Reporting Mandates

Hospitals in high-income economies must now file detailed maternal-morbidity data, including race and ethnicity stratification, under the revised Inpatient Severe Maternal Morbidity Measure.[2]Source: Agency for Healthcare Research and Quality, “Inpatient Severe Maternal Morbidity Measure Technical Specifications,” ahrq.gov The compliance burden compels procurement of platforms that automate real-time capture, analytics, and secure submissions. Software vendors differentiate by embedding templated reports that map directly to agency specifications, easing auditor reviews. Executives view adoption as a risk-mitigation strategy because non-compliance can trigger penalties and lower quality scores. The requirement also fosters cross-unit data sharing, a capability most easily delivered by integrated cloud offerings.

AI-Driven Predictive Analytics Adoption Across OB-EHR Platforms

Machine-learning models capable of 82% accuracy in preterm birth prediction are being embedded into mainstream EHRs. Epic Systems and Oracle Health have launched automated documentation and risk-scoring features that surface actionable alerts during routine charting. Early adopters report improved triage decisions and shorter average labor-ward stays. Yet the steep learning curve around interpreting algorithm outputs, plus lingering malpractice concerns, slows full reliance on AI recommendations. Vendors are therefore pairing algorithm releases with extensive clinician-education modules, anticipating a multi-year adoption curve.

Cloud-Hosted Interoperability with Fetal Monitors and EMRs

FHIR-enabled gateways such as Mirth Cloud Connect link bedside fetal monitors with enterprise EMRs in real time, dissolving longstanding data silos. Unified dashboards display maternal vitals alongside fetal heart-rate tracings, supporting faster interventions during emergent situations. Cloud services slash hardware outlays and speed multi-site rollouts, appealing to hospital chains consolidating maternity wards. Simultaneously, the USCDI maternal-health dataset standardizes message formats, minimizing interface re-work. Combined, these factors give cloud deployments an immediate uplift despite persistent cybersecurity questions.

Growing Government Initiatives and Awareness Regarding Fetal Care

National maternal-health programs funnel grants toward digital solutions that extend services into underserved communities. The White House Blueprint highlights telemonitoring and decision-support tools as levers to curb mortality disparities. Parallel efforts under Title V block grants finance state-level epidemiological surveillance upgrades, exemplified by Louisiana’s 2025 application that earmarks funds for perinatal analytics. These commitments signal durable, policy-anchored demand, though procurement cycles stretch timelines as agencies finalize budgets and vendor vetting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget Constraints in Low-Resource Maternity Units | -1.4% | Global, concentrated in rural areas | Short term (≤ 2 years) |

| Lengthy Clinician Training and Workflow Inertia | -1.1% | Global | Medium term (2-4 years) |

| Cyber-Security and Medico-Legal Liability Concerns | -0.8% | North America & EU | Long term (≥ 4 years) |

| Shortage of Skilled Professionals | -0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints in Low-Resource Maternity Units

Facilities serving low-income populations often rely on donor funds and national insurance schemes that rarely earmark sums for IT. A Ghanaian study shows that hospitals still levy unofficial fees despite nominally free maternity care, underscoring chronic under-funding.[3]Source: Nana Mensah Abrampah, “Why ‘Free Maternal Healthcare’ Is Not Entirely Free in Ghana,” BMC Health Research Policy and Systems, biomedcentral.com Up-front software licenses, annual maintenance, and broadband upgrades together exceed typical capital budgets, sidelining technology projects. Vendors answer with subscription models and hardware-agnostic designs, but reimbursement cycles and foreign-exchange volatility keep adoption uneven.

Lengthy Clinician Training and Workflow Inertia

Digital roll-outs disrupt entrenched paper-based processes, prompting resistance. South African midwives cite digital illiteracy and staffing gaps when assessing an electronic triage system, even though they acknowledge clinical benefits. In the United States, 2,718 maternal-fetal specialists surveyed by a leading professional society ranked usability frustrations among top practice burdens. Vendors that embed tutorials and align interface design with obstetric workflows shorten onboarding, yet multi-shift coverage and resident turnover stretch the learning curve to years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Integrated Solutions Drive Market Consolidation

Integrated platforms captured 71.05% of the clinical perinatal software market in 2025 and are forecast to grow at an 11.09% CAGR through 2031. Health systems prefer a single vendor that combines fetal monitoring, documentation, and analytics, reducing interface maintenance and eliminating manual data re-entry. Standalone applications remain relevant where niche capabilities, such as advanced ultrasound analytics, justify separate procurement. Thomson Medical Singapore’s deployment of MEDITECH Expanse, which links bedside monitors to clinical notes, illustrates integrated-suite momentum.

Integration reduces transcription errors and accelerates quality-measure reporting, supporting hospital accreditation renewals. Vendors package modules under tiered subscriptions, letting smaller clinics start with core CTG capture before adding analytics. As enterprise deals roll up individual departments into enterprise licenses, market consolidation favors suppliers with broad portfolios. Cross-selling of maintenance and consulting services further deepens account stickiness and raises switching costs, reinforcing integrated solutions’ dominance in the clinical perinatal software market.

By Deployment Mode: Cloud Migration Accelerates Despite Security Concerns

On-premises installations still accounted for 68.35% of the clinical perinatal software market in 2025, reflecting legacy estates in tertiary hospitals. Cloud solutions, however, are expanding at a 12.21% CAGR to 2031 as providers pursue elastic capacity and lower capital outlays. Early migrations focus on non-critical analytics sandboxes, but rising confidence in virtual private cloud architectures encourages full production moves. Interoperability advantages—automatic FHIR updates and continuous patching—aid cross-vendor data flows and strengthen disaster-recovery capabilities.

Security and sovereignty questions persist, especially with reproductive-health data newly designated as sensitive under updated HIPAA guidance. Providers negotiate enhanced encryption, in-country data centres, and contract clauses specifying breach remediation. Suppliers investing in SOC 2 audits and zero-trust frameworks will capture a growing slice of new tenders, cementing cloud’s position as the preferred deployment pathway within the clinical perinatal software market.

By End User: Maternity Clinics Emerge as Growth Catalysts

Hospitals commanded 65.42% of 2025 revenue due to comprehensive service offerings and mature IT teams. Yet maternity clinics are projected to deliver the fastest expansion, clocking an 11.32% CAGR to 2031. Clinics differentiate by offering personalised birthing environments and shorter admission cycles, necessitating software that automates intake, flags risk, and coordinates referrals. Subscription-based SaaS lowers entry barriers, allowing clinics to adopt advanced analytics without building large IT departments.

Health-insurer contracts increasingly recognise accredited clinics as cost-effective alternatives to hospital stays, creating reimbursement incentives. Vendors tailoring dashboards to clinic workflows—covering appointment scheduling, lactation support, and remote CTG—are well positioned. Hospitals, meanwhile, defend share by launching clinic-branded outpatient units, underscoring how end-user boundaries blur within the clinical perinatal software market.

By Application: Workflow Management Gains Momentum Amid Staffing Challenges

Fetal monitor data services dominated with 47.9% share in 2025, providing continuous tracings vital for obstetric assessment. Workflow management applications are forecast to outpace all others, advancing at an 10.97% CAGR to 2031. Automation of task assignments, alerts, and discharge planning eases staffing shortages, helping units handle higher patient loads without proportional head-count increases. K2 Athena exemplifies integrated workflow modules that overlay national guidelines and decision support.

Documentation tools remain foundational, feeding medico-legal records and quality metrics. However, growth concentrates where analytics harness documentation to optimize throughput. Vendors embedding process-mining insights that flag bottlenecks gain traction. Implementation success stories spur further adoption, positioning workflow management as a prime engine of value creation in the clinical perinatal software market.

Geography Analysis

North America retained leadership with a 43.65% revenue share in 2025. Mature EHR penetration, CMS value-based incentive models, and revised HIPAA privacy rules sustain demand for comprehensive perinatal platforms that simplify compliance and deliver audited outcomes. Yet rural hospitals facing budget cuts and staff shortages lag behind urban peers, prompting policy focus on remote monitoring to bridge care gaps. Vendors that offer tele-CTG modules aligned with new CPT codes gain footholds in critical-access sites.

Europe follows with a cohesive interoperability push under eHealth Network frameworks. Multi-language interfaces and GDPR-aligned encryption are prerequisite features, steering contracts to suppliers that can prove data protection credentials. Ireland’s nationwide maternity EHR roll-out confirms public-sector appetite for single-platform deployments that standardize care pathways. Adoption across Scandinavia and the DACH region emphasizes cross-border data-sharing for perinatal outcome benchmarking, enlarging addressable volume for vendors versed in EU nomenclature.

Asia-Pacific is the fastest-growing geography, tracking a 12.33% CAGR to 2031. China’s Healthy Mothers initiative subsidizes digital maternal-health pilots, while India’s Ayushman Bharat Digital Mission supports patient-record interoperability. Rising middle-class expectations and private-sector obstetric chains accelerate purchases of AI-enabled ultrasound analytics. Concurrently, Japan and Australia invest in cloud-first upgrades to extend coverage to remote islands. Suppliers able to localize interfaces and navigate diverse regulatory landscapes are poised to capture outsized gains as the clinical perinatal software market matures across the region.

Competitive Landscape

The clinical perinatal software industry is moderately fragmented. Philips and GE HealthCare exploit extensive fetal-monitor install bases to wrap software subscriptions around hardware, creating integrated ecosystems that bind customers. Philips collaborates with Georgia health plans to integrate remote monitoring into payer programs, highlighting a pivot toward outcome-linked solutions.

Specialists such as PeriGen and Sonio pioneer AI algorithms that score contraction patterns and automate ultrasound anomaly detection. Samsung’s 2024 acquisition of Sonio signals growing interest from consumer-device majors aiming to enter clinical verticals. Cloud-native newcomers like Delfina and Lucina focus on predictive analytics delivered via smartphone, targeting Medicaid populations with limited clinic access. Partnerships, rather than outright competition, characterize the landscape: Bloomlife’s alliance with PeriGen routes home-recorded CTG to hospital dashboards, a win-win that expands clinical oversight without straining beds.

Sustained differentiation rests on demonstrating outcome improvements and regulatory compliance. Vendors invest in FDA clearances for decision-support modules, as illustrated by BrightHeart’s 2024 510(k) for prenatal ultrasound software. Market entrants must also budget for SOC 2 audits and international certifications, raising barriers yet offering reputational dividends. Overall, competitive dynamics favor platforms that merge hardware telemetry, AI analytics, and reimbursement-ready workflows, positioning integrated ecosystems at the centre of future consolidation within the clinical perinatal software market.

Clinical Perinatal Software Industry Leaders

Koninklijke Philips N.V.

GE HealthCare

PeriGen, Inc.

Clinical Computer Systems, Inc.

Trium Analysis Online GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The Journey Pregnancy App integrated AI Vitals Scan technology, bringing clinical-grade monitoring to consumer smartphones.

- May 2025: GE HealthCare partnered with Raydiant Oximetry to co-develop advanced fetal monitoring solutions.

- August 2023: PeriGen Inc., the global leader in AI-powered perinatal care solutions, announced the general availability of LaborWatch following its first successful implementation across a major US health system. The LaborWatch platform employs artificial intelligence (AI)-driven maternal-fetal assessments and escalates persistent issues through automated SMS notifications.

Global Clinical Perinatal Software Market Report Scope

As per the scope of the report, clinical perinatal software provides proper management and monitoring solutions for maternal and fetal health during the perinatal period, which includes the time from pregnancy to the immediate postpartum period. The software is integrated with advanced technological features, improving decision-making and patient outcomes. By product type, the market is segmented into integrated and standalone. By deployment mode, the market is segmented into on-premises and cloud-based. By end user, the market is segmented into hospitals and maternity clinics. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the market size and forecasts for the clinical perinatal software market in 17 countries across major regions. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| Integrated |

| Standalone |

| On-premises |

| Cloud-based |

| Hospitals |

| Maternity Clinics |

| Other End Users |

| Fetal Monitor Data Services |

| Workflow Management |

| Patient Documentation |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Integrated | |

| Standalone | ||

| By Deployment Mode | On-premises | |

| Cloud-based | ||

| By End User | Hospitals | |

| Maternity Clinics | ||

| Other End Users | ||

| By Application | Fetal Monitor Data Services | |

| Workflow Management | ||

| Patient Documentation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the clinical perinatal software market in 2031?

The market is expected to reach USD 512.1 million by 2031, rising at a 10.58% CAGR from 2026.

Which region is growing fastest in the clinical perinatal software market?

Asia-Pacific is forecast to grow at a 12.33% CAGR through 2031 due to rapid healthcare digitization and expanding middle-class demand.

Why are integrated software suites preferred by healthcare providers?

Integrated suites combine monitoring, documentation, and analytics in one platform, reducing data silos and simplifying regulatory reporting.

How are reimbursement changes influencing adoption?

New CPT codes for remote CTG interpretation make off-site fetal-monitor reviews billable, accelerating software uptake among rural hospitals.

What deployment model is gaining momentum?

Cloud-based deployment is registering a 12.21% CAGR as providers seek scalability, lower capital costs, and easier interoperability.

Which application segment is expanding quickest?

Workflow management applications are advancing at an 10.97% CAGR because they streamline tasks amid staffing shortages.

Page last updated on: