Wet Pet Food Processing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.52 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

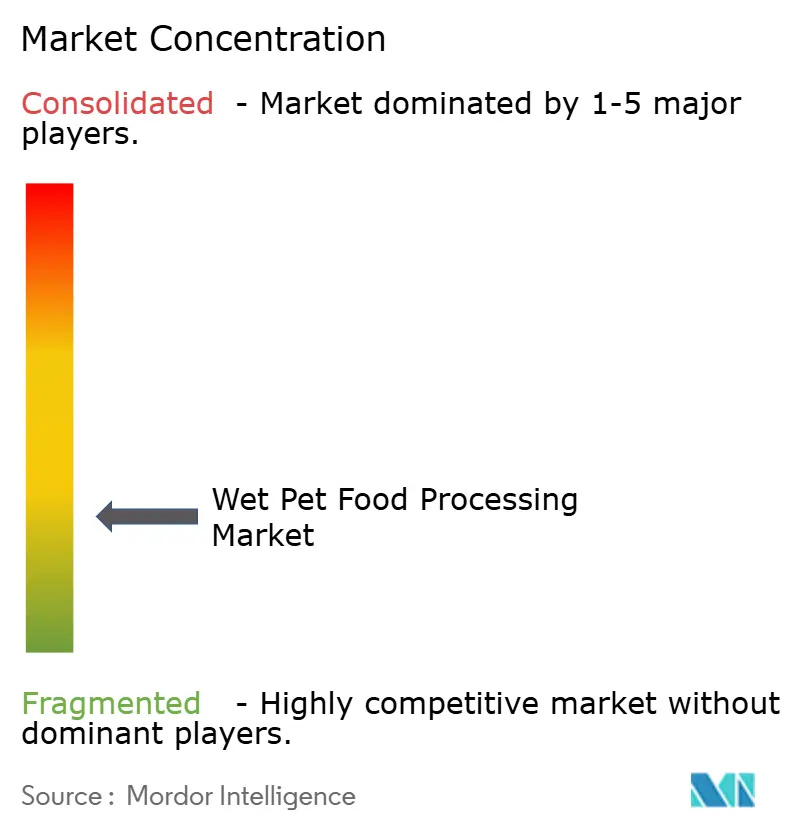

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wet Pet Food Processing Market Analysis by Mordor Intelligence

The wet pet food processing market was valued at USD 1.76 billion in 2025 and is projected to grow from USD 1.87 billion in 2026 to USD 2.52 billion by 2031, registering a CAGR of 6.10% during the forecast period from 2026 to 2031. Growth in this market is driven by a shift among producers from dry kibble to high-moisture diets, which require specialized equipment for mixing, pumping, cooking, sterilization, and filling. This transition increases production line complexity, as wet pet food formats demand a more capital-intensive process architecture compared to dry extrusion. Additionally, these formats impose stricter requirements for texture control, hygiene, and thermal validation. The market is further supported by the growth of premium pet food brands and stricter food safety regulations, which are encouraging manufacturers to adopt validated kill-step systems, enhanced traceability, and integrated digital controls. Competitive dynamics are shifting toward broader product portfolios and tighter line integration, as large buyers increasingly favor suppliers capable of managing the entire production process, from raw protein intake to final packaging. However, high capital costs, significant utility requirements, and a shortage of skilled professionals in thermal validation continue to pose challenges for smaller producers. Despite these barriers, the wet pet food processing market is projected to maintain steady growth, driven by rising per-capita spending on pet nutrition and ongoing modernization of production facilities.

Key Report Takeaways

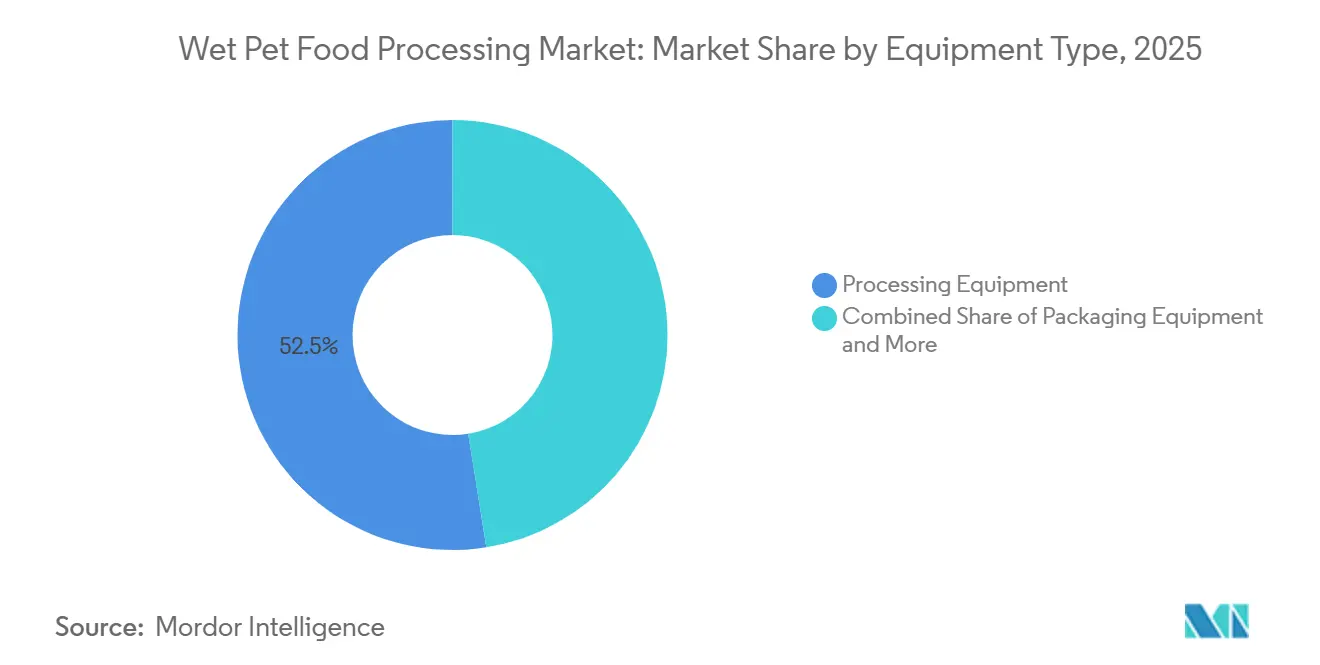

- By equipment type, the wet pet food processing market share for the processing equipment segment held the largest 52.5% in 2025, while the wet pet food processing market size for the packaging equipment segment is projected to grow at the fastest CAGR of 6.1% from 2026 to 2031.

- By pet food type, cat food held the largest share of 62.2% in 2025 and is also forecast to grow at the fastest CAGR of 6.2% from 2026 to 2031.

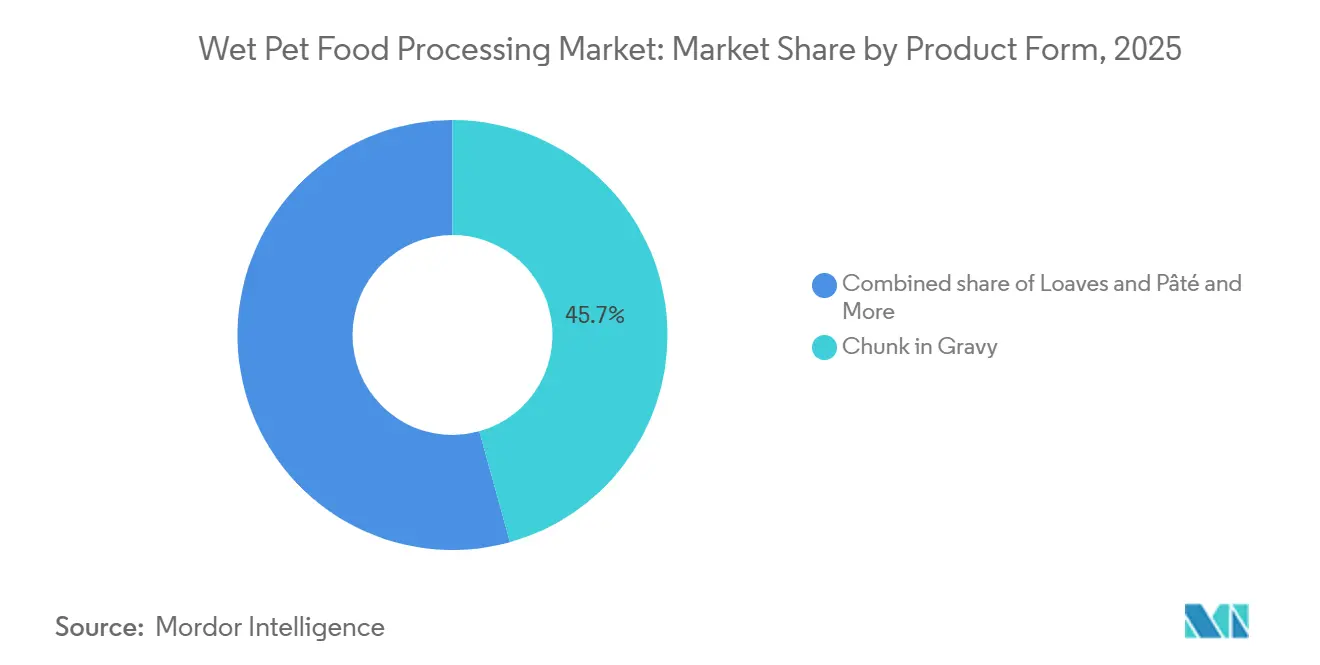

- By product form, chunk in gravy accounted for the largest share of 45.7% in 2025 and is projected to grow at the fastest CAGR of 6.3% from 2026 to 2031.

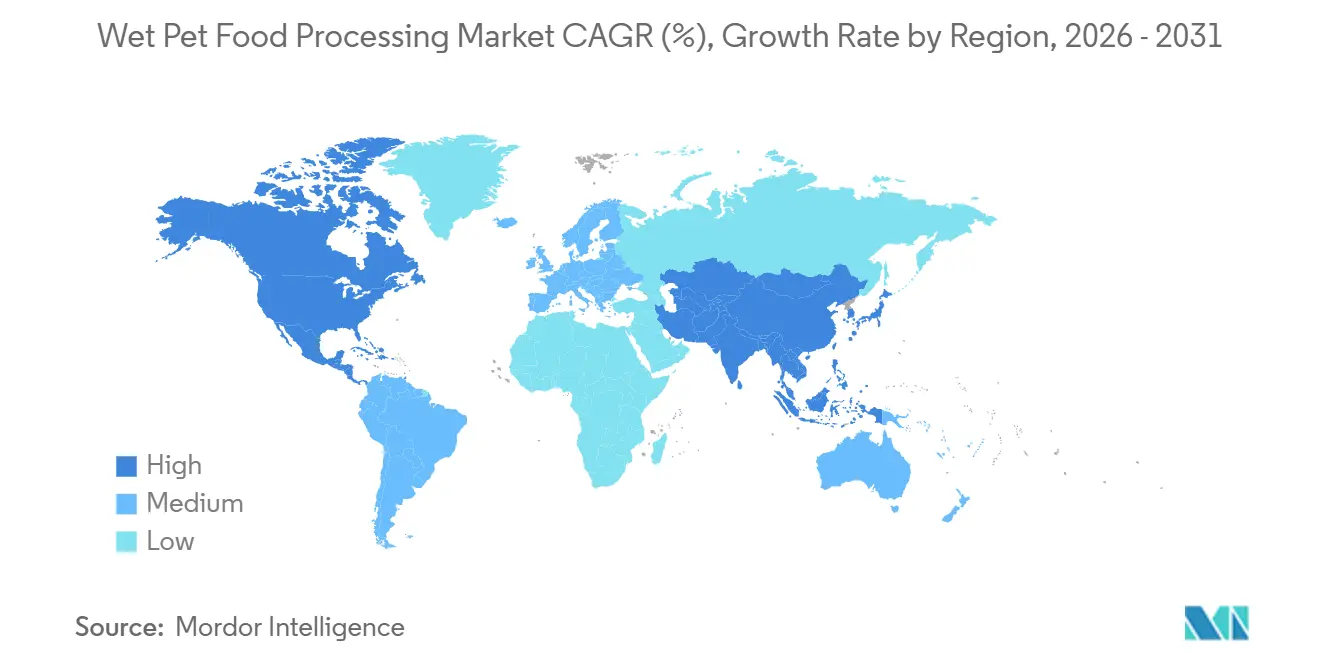

- By geography, North America led with the largest share of 31.6% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 6.3% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wet Pet Food Processing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium wet pet food premiumization | +1.5% | Global, with highest intensity in North America and Europe | Medium term (2-4 years) |

| Food safety and traceability upgrades | +0.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Automation and digital line control adoption | +1.1% | Global, with fastest deployment in Europe and North America | Medium term (2-4 years) |

| Rising wet cat food intensity | +1.0% | Global, with outsized pull from Asia-Pacific and Europe | Long term (≥ 4 years) |

| Shift to pouches and trays | +0.7% | North America, Europe, and rapidly expanding Asia-Pacific | Medium term (2-4 years) |

| Demand for chunk integrity and nutrient retention | +0.5% | Global, especially premium-tier markets in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Wet Pet Food Premiumization

Premiumization trends are driving increased demand for equipment in the wet pet food processing market. Manufacturers require advanced processing systems to handle high-meat and human-grade formulations while ensuring product texture, appearance, and hygiene standards are maintained. According to the 2026 Processing State of the Industry report by the Association for Packaging and Processing Technologies (PMMI) and the Food Processing Suppliers Association, some pet food facilities in the United States have shifted over half of their production to human-grade standards in recent years. This shift is fostering the adoption of technologies such as vacuum blending, high-pressure processing, steam-tunnel cooking, and precision thermal-control systems tailored for premium wet pet food manufacturing environments.

Food Safety and Traceability Upgrades

Increasing food safety and traceability requirements are driving the demand for equipment modernization in the wet pet food processing market. Manufacturers face growing pressure to validate thermal processing and enhance hazard monitoring systems. In January 2025, the United States Food and Drug Administration Center for Veterinary Medicine directed pet food manufacturers using raw or unpasteurized poultry or cattle materials to reassess their food safety plans and account for Highly Pathogenic Avian Influenza H5N1 as a foreseeable hazard[1]Source: United States Food and Drug Administration Center for Veterinary Medicine, “Cat and Dog Food Manufacturers Required to Consider H5N1 in Food Safety Plans,” fda.gov. This regulatory emphasis is accelerating the adoption of retorts, pasteurization systems, and digital critical control point monitoring technologies, which enhance traceability, sanitation control, and audit readiness in wet pet food production facilities.

Automation and Digital Line Control Adoption

Automation adoption is driving demand in the wet pet food processing market as manufacturers aim to reduce labor dependency and enhance production consistency in temperature-sensitive processing environments. According to a 2026 industry update by The Association for Packaging and Processing Technologies (PMMI) and the Food Processing Suppliers Association, persistent labor shortages are prompting increased investment in automated processing systems that require fewer operators, particularly for inspection, monitoring, and production control tasks. This has led to the growing implementation of automated retort systems, clean-in-place sanitation technologies, and intelligent recipe management platforms in wet pet food production facilities, improving operational consistency and minimizing manual processing errors.

Rising Wet Cat Food Intensity

Wet cat food continues to drive significant demand in the wet pet food processing market, as feline diets typically favor moisture-rich formats more than many dog diets. The equipment requirements for cat food production differ from those for dog food, with a focus on finer emulsification, smaller fill weights, and stricter control of chunk sizes for formats like pâté. Veterinary endorsement of moisture-rich cat diets further supports this demand, as cats naturally have a low thirst drive, and wet diets are often recommended for managing urinary tract and renal health issues. In March 2026, Nestlé Purina invested CHF 370 million (USD 473.6 million) in a new wet pet food facility in Vargeão, Brazil, to cater to domestic demand and South American exports[2]Source: Nestlé S.A., “Nestlé to Invest CHF 370 Million in New Pet Food Factory in Brazil,” nestle.com. This investment highlights the scale of capital being directed toward feline-oriented wet food production. Such capacity expansions sustain a consistent demand for vacuum mixing, emulsification, and small-format pouch-filling systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital intensity of integrated lines | -1.2% | Global, with the sharpest effect in emerging markets across Asia-Pacific, South America, and Africa | Long term (≥ 4 years) |

| High steam, water, and sanitation load | -0.7% | Global, with stronger pressure in water-stressed regions | Medium term (2-4 years) |

| Plant utility and wastewater bottlenecks | -0.6% | Asia-Pacific, South America, Africa, and secondary markets in Eastern Europe | Medium term (2-4 years) |

| Thermal-process validation skill shortages | -0.5% | Global, and most severe among new entrants and new-market geographies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity of Integrated Lines

High capital intensity continues to be a significant restraint in the wet pet food processing market. Manufacturers are required to make substantial investments in integrated processing lines, sterilization systems, filling equipment, packaging machinery, and quality control infrastructure to achieve commercial-scale production. Additionally, these facilities must adhere to strict food safety and traceability standards, further increasing upfront costs and operational complexity. As regulatory requirements and production demands grow, larger companies are typically better equipped to manage these investments compared to smaller processors. These financial and operational challenges can delay capacity expansion and deter new entrants, thereby constraining the overall growth potential of the wet pet food processing market.

High Steam, Water, and Sanitation Load

High steam, water, and sanitation requirements continue to pose a significant challenge for the wet pet food processing market. Wet processing systems depend heavily on retort sterilization, continuous cleaning cycles, and wastewater management to ensure compliance with food safety standards. These processes contribute to increased operational complexity and reliance on utilities within production facilities. Additionally, manufacturers face mounting pressure to enhance energy efficiency and reduce water usage while adhering to stringent hygiene standards, particularly for premium and human-grade pet food products. Consequently, processors often encounter elevated operating costs, additional infrastructure demands, and extended investment payback periods when expanding or upgrading wet pet food processing lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Processing Equipment Anchors Lines, Packaging Drives Future Growth

The wet pet food processing market share for the processing equipment segment accounted for the largest 52.5% in 2025. This segment maintained its leading position due to the critical role of systems such as mixing, emulsification, grinding, cooking, pumping, and chilling in ensuring texture consistency, ingredient integration, and food safety in wet pet food production. These systems are essential for production efficiency, as premium wet formulations require precise thermal treatment and controlled material handling throughout the processing cycle. Manufacturers continue to focus on upgrading hygienic equipment designs, automated process controls, and modular cleaning systems to enhance operational flexibility. Additionally, demand remains diversified as processors require multiple integrated machine categories rather than relying on a single processing function.

The wet pet food processing market size for the packaging equipment segment is forecast to grow at the fastest CAGR of 6.1% from 2026 to 2031. The rising demand for packaging equipment is driven by the need for flexible pouches, trays, and premium portion-controlled formats, which require precise filling, sealing, sterilization compatibility, and labeling capabilities, surpassing those of traditional canning systems. Wet pet food manufacturers are increasingly investing in automated packaging lines to enhance operational speed, hygiene compliance, and traceability across production facilities. The growing adoption of premium retail packaging formats is also driving the use of intelligent inspection systems and advanced sealing technologies, which are designed to support shelf-stable wet food applications in both premium and private-label manufacturing operations.

By Pet Food Type: Feline Nutrition Commands Both Volume and Growth Leadership

The cat food segment accounted for the largest 62.2% share in 2025, and it is projected to grow at the fastest CAGR of 6.2% from 2026 to 2031. This dominance in wet pet food production is attributed to the reliance of feline diets on moisture-rich formulations and premium texture-focused recipes. Manufacturers are increasingly investing in smaller-fill processing systems, precision emulsification equipment, and gentle ingredient handling technologies specifically designed for feline wet food products. Premium cat food brands demand higher consistency in appearance, palatability, and ingredient integration, driving the need for advanced processing and packaging infrastructure. These requirements continue to support investments in high-specification wet cat food manufacturing facilities worldwide.

The dog food segment remains a significant production category, with manufacturers expanding premium stew, gravy, and chunk-based formulations aligned with human-grade and functional nutrition trends. Processing systems for dog food often require larger-capacity handling equipment and stronger conveying capabilities to accommodate heavier inclusions and denser formulations. Equipment suppliers are increasingly focusing on species-specific production configurations rather than standardized processing layouts for both canine and feline products. Additionally, consolidation among premium pet food brands is influencing equipment investment patterns, as larger manufacturers with greater financial resources are better positioned to support high-value processing upgrades, automation initiatives, and integrated wet food production expansions across multiple manufacturing sites globally.

By Product Form: Chunk in Gravy Leads as Texture Complexity Redefines Equipment Specs

The chunk in gravy held the largest 45.7% share in 2025 and it is forecast to grow at the fastest CAGR of 6.3% from 2026 to 2031. This product form leads because visible meat inclusions and gravy-based formulations require highly controlled processing conditions to preserve texture integrity during mixing, filling, sterilization, and cooling stages. Manufacturers increasingly prioritize low-shear conveying systems, precision thermal processing, and controlled portioning technologies to maintain premium product appearance and consistency. The technical complexity associated with chunk-based wet pet food production continues to support demand for advanced equipment systems designed specifically for high-value and texture-sensitive premium formulations across feline and canine applications.

The loaves and pâté products remain important because they can be produced using more established emulsification and vacuum-mixing technologies with lower processing complexity than chunk-based formulations. Stew formats are also gaining popularity among premium dog food brands seeking differentiated recipes with visible vegetable and protein inclusions. Shreds and flakes in broth or jelly continue supporting demand for precision slicing, gentle pumping, and specialized conveying technologies designed to protect delicate textures during production. This broad range of wet food forms benefits equipment suppliers because manufacturers require specialized solutions across emulsification, chunk formation, filling, dosing, sterilization, and packaging operations instead of relying on one standard processing configuration.

Geography Analysis

North America accounted for the largest share, 31.6%, in 2025. The region maintains its leadership due to a mature wet pet food manufacturing base, supported by premiumization trends, advanced food safety standards, and significant investment in automated production infrastructure. Manufacturers in the United States and Canada are modernizing existing production lines to accommodate premium wet formulations, enhance sanitation standards, and improve operational efficiency. Regulatory oversight related to food safety and traceability also influences equipment purchasing decisions across the region. Mexico is strengthening its role as a regional manufacturing hub through increased investment in processing and packaging activities serving North and Central America.

Asia-Pacific is forecast to grow at the fastest CAGR of 6.3% from 2026 to 2031. This growth is driven by increasing pet ownership, expanding middle-class spending, and rising demand for premium wet pet food products across China, India, Southeast Asia, Japan, and South Korea. Manufacturers are investing in domestic wet food production capacity as premium and human-grade formulations gain greater consumer acceptance. Thailand and Australia are also enhancing export-oriented processing capabilities to serve international pet food markets. The region's relatively smaller installed production base compared to North America and Europe presents opportunities for new processing infrastructure and advanced packaging system deployment.

Europe remains the second-largest region due to strong wet pet food consumption in Germany, the United Kingdom, France, and Italy, coupled with the presence of major food processing and packaging equipment manufacturers. Regional demand is supported by the adoption of premium products, stringent hygiene requirements, and the modernization of food production infrastructure. MULTIVAC Sepp Haggenmüller SE & Co. KG expanded its production plant in Wolfertschwenden in 2025, highlighting increased investment in advanced packaging and processing capabilities for premium food applications including wet pet food[3]Source: MULTIVAC Sepp Haggenmüller SE & Co. KG, “Bringing Automation, Sustainability and Efficiency Together in Harmony – Press Conference at IFFA 2025,” multivac.com. South America continues to grow, driven by multinational investments in Brazil and Argentina, while the Middle East and Africa remain emerging markets.

Competitive Landscape

The wet pet food processing market is fragmented, with key players including GEA Group Aktiengesellschaft, JBT Marel Corporation, Bühler AG, Andritz AG, and Cabinplant A/S. These companies maintain their market positions through integrated processing systems, hygienic equipment design, automation technologies, and extensive packaging capabilities. Competitive differentiation is increasingly driven by operational efficiency, expertise in thermal processing, digital monitoring integration, and the ability to meet premium wet pet food production requirements in large-scale manufacturing facilities worldwide.

Competition is intensifying in areas such as automated processing, intelligent packaging systems, and advanced sanitation technologies tailored for premium wet pet food applications. Equipment suppliers are focusing on modular production systems, automated clean-in-place technologies, and digital production monitoring tools to enhance process consistency and minimize operational downtime. Companies specializing in filling, sterilization, portioning, and sealing technologies remain competitive in segments where format-specific expertise outweighs the need for full-line integration. Strategic partnerships, production expansion, and application-focused engineering capabilities are shaping competitive dynamics as manufacturers increasingly prioritize operational flexibility, traceability, and hygienic production standards in wet pet food processing facilities.

Specialist suppliers such as VEMAG Maschinenbau GmbH, Handtmann Maschinenfabrik GmbH & Co. KG, and MULTIVAC Sepp Haggenmüller SE & Co. KG continue to compete through their expertise in portioning, tray sealing, alternative packaging, and filling systems. JBT Marel Corporation enhanced its wet pet food processing capabilities in April 2026 by integrating Wenger and Extru-Tech under a unified pet food solutions platform, which was showcased at Petfood Forum 2026. This development highlights the growing focus on integrated processing, application-specific engineering, and full-line production support for premium wet pet food manufacturing. Competitive positioning is increasingly influenced by technical service capabilities and digital production support rather than solely by standalone equipment supply.

Wet Pet Food Processing Industry Leaders

GEA Group Aktiengesellschaft

JBT Marel Corporation

Bühler AG

Andritz AG

Cabinplant A/S (CTB, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: JBT Marel Corporation collaborated with Aurum Process Technology to incorporate aseptic processing and aseptic filling for flexible packaging into its global portfolio. This partnership focuses on premium wet pet food and ready-meal categories and was highlighted at Interzoo 2026 in Nuremberg. The initiative enhances the company's end-to-end capabilities for shelf-stable, flexible-format wet pet food production lines.

- April 2026: JBT Marel Corporation consolidated Wenger and Extru-Tech into a single pet food solutions brand during the Petfood Forum 2026 in Kansas City. This unified offering includes extrusion, steam-tunnel gentle cooking, and high-pressure processing for minimally processed wet pet food, reflecting a strategic shift toward a comprehensive positioning in the pet food equipment market.

- September 2025: Andritz AG unveiled the ExMax S1021 single-screw extruder at VICTAM LATAM in São Paulo. This extruder incorporates the DensiFlex automated cooking and expansion control system, designed to improve processing efficiency, ensure product consistency, and enhance operational reliability. The technology supports manufacturers in producing high-quality pet food and strengthens capabilities within the wet pet food processing market.

Global Wet Pet Food Processing Market Report Scope

Wet pet food processing involves the industrial production of moisture-rich pet food products, including pâté, chunks in gravy, stews, and shredded formulations for cats and dogs. The process includes ingredient mixing, grinding, cooking, sterilization, filling, sealing, and packaging to ensure safety, consistent texture, shelf stability, and nutritional quality. The wet pet food processing market report is segmented by equipment type (processing equipment, packaging equipment, and cleaning and sanitization equipment), by pet food type (dog food and cat food), by product form (loaves and pâté, chunk in gravy, stew, and shreds and flakes in broth and jelly), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Processing Equipment | Mixing and Blending Equipment |

| Grinding Equipment | |

| Pre-Cooking Equipment | |

| Cooling and Chilling Equipment | |

| Emulsification and Texturizing Equipment | |

| Pumping and Conveying Equipment | |

| Packaging Equipment | Cans |

| Trays | |

| Pouches | |

| Tubes | |

| Cleaning and Sanitization Equipment |

| Dog Food |

| Cat Food |

| Loaves and Pâté |

| Chunk in Gravy |

| Stew |

| Shreds and Flakes in Broth and Jelly |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Thailand | |

| Australia | |

| New Zeland | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Equipment Type | Processing Equipment | Mixing and Blending Equipment |

| Grinding Equipment | ||

| Pre-Cooking Equipment | ||

| Cooling and Chilling Equipment | ||

| Emulsification and Texturizing Equipment | ||

| Pumping and Conveying Equipment | ||

| Packaging Equipment | Cans | |

| Trays | ||

| Pouches | ||

| Tubes | ||

| Cleaning and Sanitization Equipment | ||

| By Pet Food Type | Dog Food | |

| Cat Food | ||

| By Product Form | Loaves and Pâté | |

| Chunk in Gravy | ||

| Stew | ||

| Shreds and Flakes in Broth and Jelly | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Thailand | ||

| Australia | ||

| New Zeland | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of wet pet food processing by 2031?

The wet pet food processing market is projected to grow from USD 1.87 billion in 2026 to USD 2.52 billion by 2031, registering a CAGR of 6.1% during the period 2026-2031.

Which equipment category leads spending on wet pet food lines?

Processing Equipment led with the largest 52.5% share in 2025 because upstream steps such as mixing, grinding, pre-cooking, emulsification, and pumping carry most of the capital weight.

Why is packaging equipment growing faster than other equipment types?

Packaging Equipment is forecast to grow at the fastest 6.1% CAGR from 2026 to 2031 because pouches and trays require more precise sealing, flexible film handling, and higher-accuracy filling than legacy can lines.

Why does cat food matter so much for equipment demand?

Cat Food held the largest 62.2% share in 2025 and also shows the fastest 6.2% CAGR from 2026 to 2031, which keeps demand strong for finer emulsification, smaller fill sizes, and tighter texture control.

Page last updated on: