Generator Paralleling Switchgear Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 2.13 Billion |

| Market Size (2030) | USD 2.98 Billion |

| Growth Rate (2025 - 2030) | 7.33% CAGR |

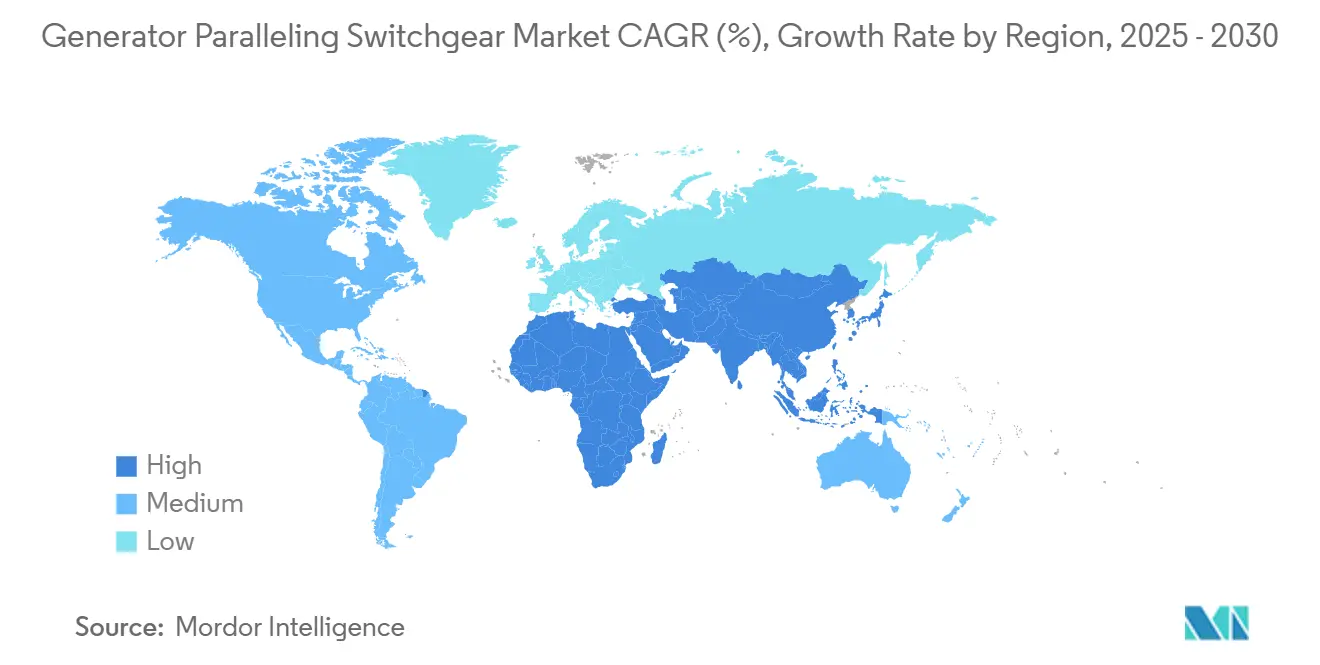

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

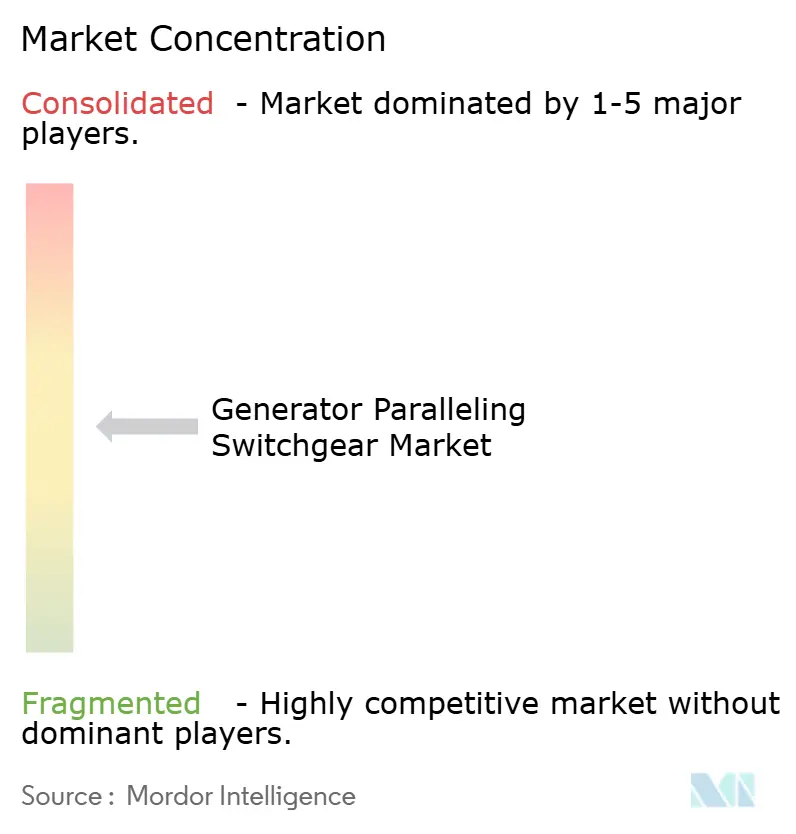

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Generator Paralleling Switchgear Market Analysis by Mordor Intelligence

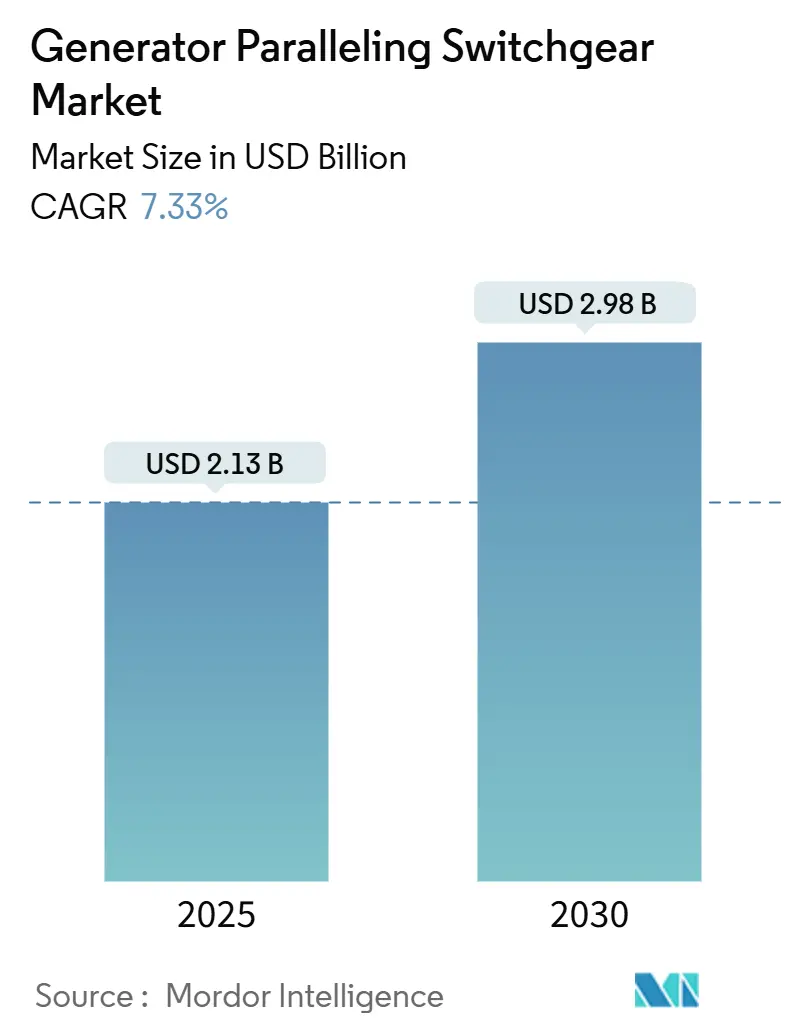

The Generator Paralleling Switchgear Market size is estimated at USD 2.13 billion in 2025, and is expected to reach USD 2.98 billion by 2030, at a CAGR of 7.33% during the forecast period (2025-2030).

Demand strengthens as critical facilities expand distributed-generation assets, adopt digital controls, and pursue grid-code compliance. Standby systems remain the volume driver, but prime-power and hybrid micro-grid projects fuel the next leg of growth. Medium-voltage platforms gain traction in data centers where rack densities exceed 30 kW, while utilities accelerate procurement to integrate distributed resources. Competitive rivalry centers on digital-native control packages, cybersecurity hardening, and turnkey service models.

Key Report Takeaways

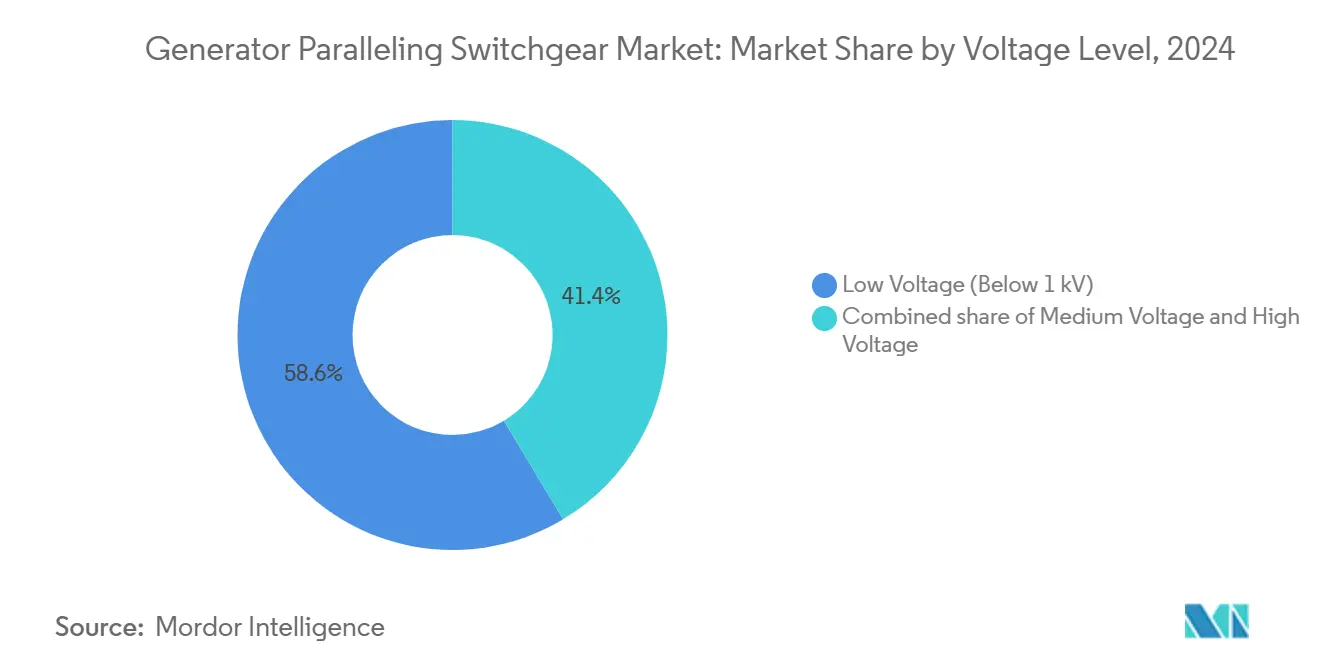

- By voltage level, low-voltage platforms dominated with 58.6% revenue share in 2024; medium-voltage is forecast to expand at an 8.9% CAGR through 2030.

- By application, standby power captured 60.2% of the generator paralleling switchgear market share in 2024, whereas prime-power posts the fastest 9.2% CAGR to 2030.

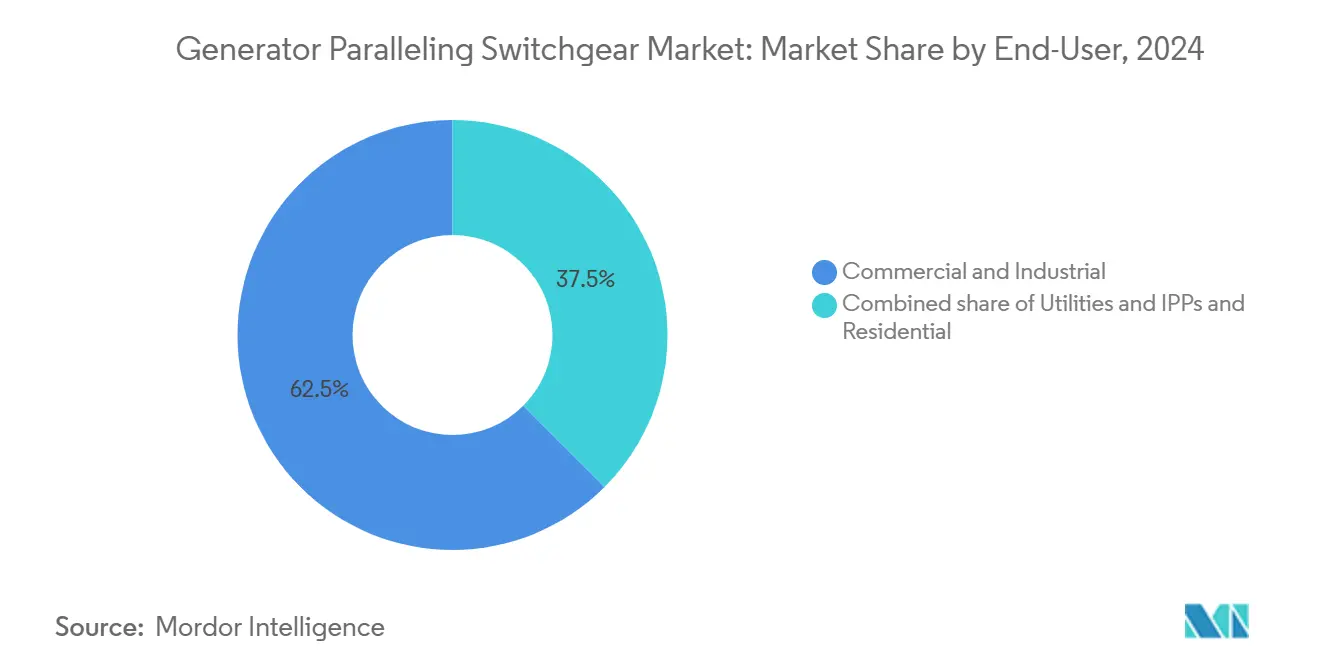

- By end user, commercial & industrial sites held a 62.5% share of the generator paralleling switchgear market size in 2024, and utilities grow at a 9.5% CAGR through 2030.

- ABB, Siemens, Caterpillar, and Schneider Electric jointly controlled 41% revenue in 2024, underscoring a moderately concentrated landscape.

Global Generator Paralleling Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Micro-grid build-outs in hospitals & data-center campuses | 1.80% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Rising grid‐instability penalties for large commercial users | 1.20% | North America & EU primarily, expanding to APAC | Short term (≤ 2 years) |

| Digitally-native paralleling-control upgrades (edge analytics) | 1.50% | Global, led by developed markets | Long term (≥ 4 years) |

| CAPEX subsidies for on-site backup in critical infrastructure | 0.90% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| Demand for hybrid-fuel gen-sets in remote mining clusters | 0.60% | Global, concentrated in resource-rich regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Micro-grid build-outs in hospitals & data-center campuses

Hospitals must transition loads within 10 seconds to protect Level 1 life-support equipment, pushing demand for sophisticated generator paralleling architectures that maintain voltage and frequency stability.[1]PowerSecure, “Healthcare Micro-grids,” powersecure.com Data-center workloads—especially AI inference—raise facility power above 50 MW, making multi-generator micro-grids with bidirectional battery integration the norm. Caterpillar’s ECS 200 controller delivers adaptive load-sharing that synchronizes sets even if communications fail.[2]Caterpillar, “ECS 200 Control,” cat.com Hourly downtime costs averaging USD 740,000 compel operators to treat paralleling switchgear as business-critical infrastructure rather than discretionary spend.

Rising grid-instability penalties for large commercial users

Peak-demand charges account for up to 70% of an industrial facility’s electricity bill in North America, prompting peak-shaving deployments that depend on switchgear capable of seamless utility synchronization. FERC Order 2023 shortens interconnection queues yet imposes stricter performance criteria, so facilities install IEEE 1547-2018-compliant controls that can island, grid-support, and ride through disturbances. Revenue streams of USD 50-200 per kW annually from demand-response programs strengthen the return profile.

Digitally-native paralleling-control upgrades

Replacing discrete relays with edge analytics platforms cuts O&M costs 15-25% and boosts uptime through predictive maintenance. ABB’s SACE Emax 3 breaker integrates IEC 62443-certified cybersecurity plus onboard analytics, enabling local optimization without cloud dependence. Schneider Electric’s EcoStruxure Power suite overlays continuous thermal monitoring to reduce arc-flash risk.[3]Schneider Electric, “EcoStruxure Power,” se.com AI-driven algorithms learn load patterns and auto-tune generator dispatch, a feature insurers and regulators increasingly require for critical sites.

CAPEX subsidies for on-site backup in critical infrastructure

FEMA’s Hazard Mitigation Grants finance generator projects with benefit-cost ratios above 2.0 for hospitals and police stations. The Grid Resilience State & Tribal Formula Grants earmark USD 2.3 billion for backup-power enhancements through 2027. California’s USD 200 million Microgrid Incentive Program adds state-level leverage, accelerating procurement in wildfire-prone zones.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile copper & steel input costs | -1.10% | Global, particularly impacting manufacturing hubs | Short term (≤ 2 years) |

| Lengthy utility‐interconnect approvals | -0.80% | North America & EU primarily | Medium term (2-4 years) |

| Cyber-hardening compliance gaps in legacy switchgear | -0.50% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile copper & steel input costs

Copper and steel constitute up to 60% of material input for medium-voltage assemblies, so 2024 commodity spikes compressed OEM margins and stretched lead times. Power-transformer delivery now exceeds five years, forcing manufacturers to carry high-value inventories that tie up working capital. Schneider Electric is investing USD 700 million across six U.S. sites to regionalize supply, but near-term pricing pressure remains.

Lengthy utility-interconnect approvals

Interconnection queues hold 1,570 GW across 12,000 projects, with only 19% reaching commercial operation.[4]Lawrence Berkeley National Laboratory, “Queued Up: Interconnection Trends 2024,” lbl.gov FERC’s cluster studies accelerate reviews, but regional transmission operators struggle with staffing and tariff harmonization, prolonging prime-power and peak-shave deployments. California ISO’s new zonal scoring reduces some bottlenecks yet introduces additional data-submission layers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage Level: Medium voltage drives technical innovation

Low-voltage units under 1 kV captured 58.6% of 2024 revenue. Nonetheless, the medium-voltage class posts the strongest 8.9% CAGR as AI-centric data halls request 5-50 MW blocks and utilities adopt 13.8 kV campus loops. The generator paralleling switchgear market size for medium-voltage applications is projected to expand from USD 0.81 billion in 2025 to USD 1.24 billion by 2030. Advanced gas-insulated and solid-insulated designs help OEMs meet SF6-phase-out mandates.

Rising rack densities push operators toward 33 kV backbone distribution, slashing cable cross-section requirements by 70% and freeing white-space. Eaton’s USD 1.4 billion Fibrebond deal underscores the shift to prefabricated, medium-voltage e-houses tailored for hyperscale campuses.

By Application: Prime power emerges as strategic priority

Standby duty retained a 60.2% share of the generator paralleling switchgear market size in 2024, valued at USD 1.2 billion, supported by healthcare and colocation assets. Prime-power grows fastest at 9.2% through 2030 as mining, remote oil & gas, and islanded communities seek grid independence. The segment benefits from hybrid configurations that blend diesel, renewables, and storage to lower LCOE below USD 0.12 per kWh.

IEEE 1547-2018 compliance plus black-start capability differentiates prime-power panels. Caterpillar rates set for continuous duty at 70% average load, demanding enhanced cooling and filtration. Peak-shaving remains niche but expands with utility tariffs that penalize 15-minute demand spikes. Participation in demand-response markets monetizes fast-ramp assets, improving IRR by 200-300 basis points.

By End User: Utilities embrace distributed generation

Commercial & industrial entities led with 62.5% revenue in 2024, yet utility and independent power producer uptake accelerates at 9.5% CAGR. Policy such as the United States Virtual Power Plant roadmap targets 80-160 GW of aggregated DER by 2030, each node requiring certified paralleling interfaces. State Grid Corporation of China’s CNY 600 billion (USD 84.5 billion) modernization push prioritizes smart substations that embed medium-voltage generator paralleling switchgear.

Residential penetration remains low outside premium estates, but California’s community micro-grid pilots indicate latent demand as inverter prices fall. Revenue stacking across backup, solar self-consumption, and market exports could open a long-tail opportunity after 2028.

Geography Analysis

North America contributed 37.9% revenue in 2024, growing steadily as FERC Order 2023 streamlines interconnections and FEMA resilience grants underwrite backup power for critical assets. Data-center clustering in Northern Virginia, Phoenix, and Columbus sustains bulk orders for 15–25 kV paralleling line-ups. Utilities increasingly procure campus micro-grid kits to serve wildfire evacuation centers.

Asia-Pacific posts the fastest 9.8% CAGR. India plans 850 MW of incremental data-center capacity by 2026, translating to more than 1,100 generator sets that must synchronize with battery storage. China’s USD 84.5 billion grid upgrade reshapes sub-transmission networks and drives demand for IEC 62271-tested switchgear that can parallel distributed assets while withstanding high fault currents. Australia’s resource sector pilots hybrid-fuel gen-sets at mines, further boosting regional sales.

Europe shows steady replacement demand as legacy SF6 panels face retirement. Industrial decarbonization pushes factories to balance renewable generation with gas engines through digital switchgear. Siemens’ Trayer Engineering acquisition expands its sealed pad-mount offering U.S. side, then back-imports technology to flood-prone EU markets. Brexit supply-chain friction and geopolitical tensions elevate inventory buffers but do not materially slow project timelines.

Competitive Landscape

Four multinational groups—ABB, Siemens, Caterpillar, and Schneider Electric—shared 41% of 2024 revenue, indicating moderate concentration. Each leverages proprietary controller firmware, global service crews, and retrofit kits to defend installed bases. ABB’s December 2024 buyout of Gamesa Electric secures 40 GW of renewable converter footprint, opening cross-sell potential for paralleling gear. Siemens absorbs Trayer Engineering to address pad-mount segments where undergrounding rises.

Eaton’s Fibrebond purchase positions it for modular e-houses that ship factory-tested, compressing construction schedules by 25%. GE Vernova invests USD 10 million to expand FLEX INVERTER production, signaling convergence between inverter and switchgear portfolios. Disruptors like Exro Technologies promote solid-state battery systems that can substitute diesel gensets in certain edge cases.

Generator Paralleling Switchgear Industry Leaders

Siemens AG

ABB Ltd.

Caterpillar Inc.

Schneider Electric SE

Cummins Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Schneider Electric to invest USD 700 million in six U.S. plants, adding 1,000 jobs and boosting switchgear capacity.

- February 2025: Eaton announces a USD 340 million transformer plant in South Carolina, opening in 2027.

- December 2024: ABB to acquire Gamesa's Electric power electronics unit, adding 40 GW installed base.

- September 2024: Siemens agrees to purchase Trayer Engineering, expanding its sealed pad-mount switchgear range.

Global Generator Paralleling Switchgear Market Report Scope

| Low Voltage (Below 1 kV) |

| Medium Voltage (1 to 36 kV) |

| High Voltage (Above 36 kV) |

| Prime Power |

| Standby Power |

| Peak-Shaving/Demand-Response |

| Commercial and Industrial |

| Utilities and IPPs |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Voltage Level | Low Voltage (Below 1 kV) | |

| Medium Voltage (1 to 36 kV) | ||

| High Voltage (Above 36 kV) | ||

| By Application | Prime Power | |

| Standby Power | ||

| Peak-Shaving/Demand-Response | ||

| By End-User | Commercial and Industrial | |

| Utilities and IPPs | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What growth rate is forecast for generator paralleling switchgear through 2030?

The market is projected to expand at a 7.33% CAGR, taking revenue from USD 2.13 billion in 2025 to USD 2.98 billion by 2030.

Which voltage class shows the fastest adoption?

Medium-voltage systems (1–36 kV) lead with an 8.9% CAGR as hyperscale data centers and industrial campuses upgrade to higher power densities.

Why are prime-power applications gaining momentum?

Rising utility tariffs and grid unreliability push remote mines and energy-intensive industries to run generators continuously, giving prime-power a 9.2% CAGR.

How do subsidies influence procurement?

FEMA and DOE resilience grants offset up-front costs for critical facilities, accelerating adoption especially in hospitals and public-safety sites.

Who are the principal suppliers?

ABB, Siemens, Caterpillar, Schneider Electric, and Eaton dominate, collectively holding about 60% of global revenue.

What is the key technical shift shaping future products?

Digital-native, edge-analytics controllers with built-in cybersecurity and IEEE 1547-2018 compliance are becoming standard for new installations.

Page last updated on: