Synchronous Generator Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.89 Billion |

| Market Size (2031) | USD 7.74 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

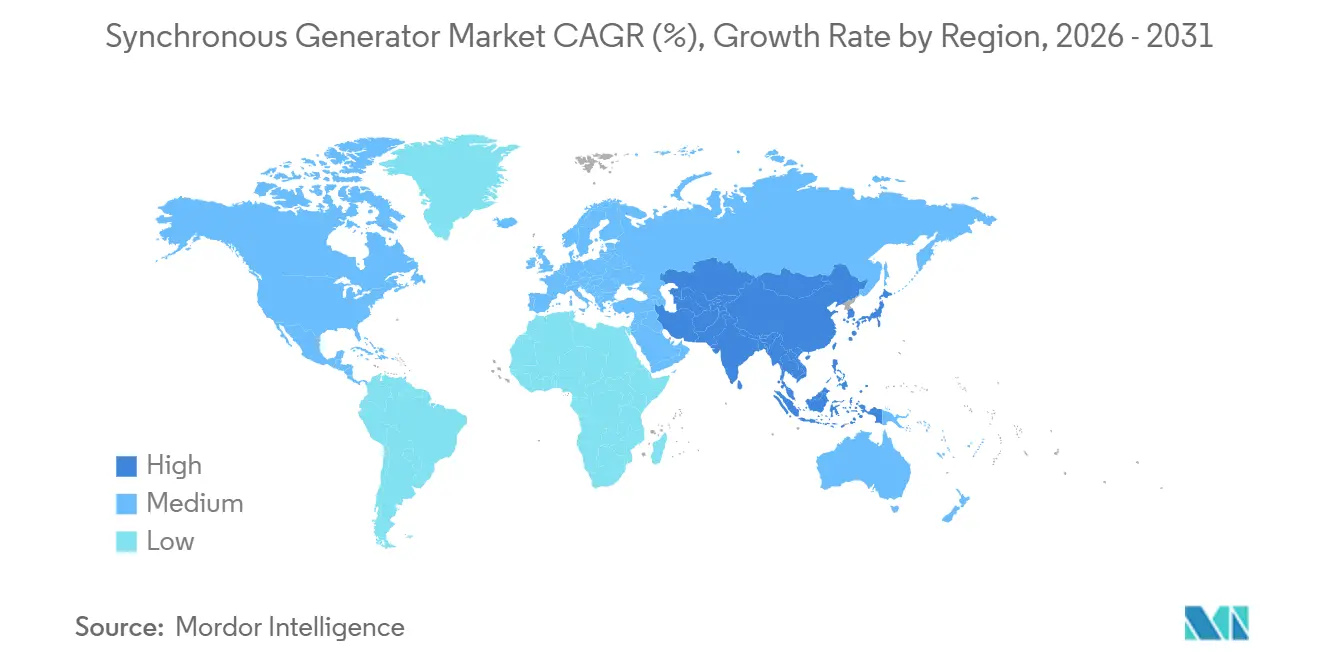

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

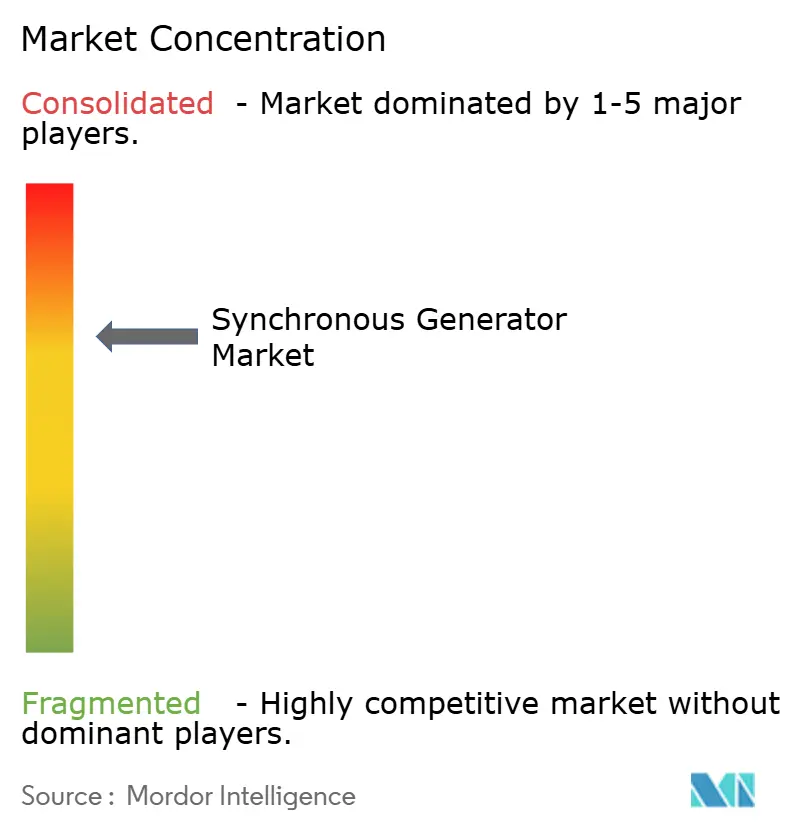

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Synchronous Generator Market Analysis by Mordor Intelligence

The Synchronous Generator Market size is expected to increase from USD 5.58 billion in 2025 to USD 5.89 billion in 2026 and reach USD 7.74 billion by 2031, growing at a CAGR of 5.25% over 2026-2031. Utilities and grid operators are increasingly adopting synchronous machines to provide physical inertia that inverter-dominated renewable grids cannot replicate. Retrofits at decommissioned coal plants, data center self-generation, and naval electric propulsion projects are expanding the technology's addressable market. Hydrogen-cooled designs, brushless excitation, and predictive maintenance digital twins are emerging as key differentiators, while rare-earth-free magnet research aims to reduce supply chain risks for permanent magnets. Cost-competitive inverter-based induction machines limit growth potential in some OECD jurisdictions, though synchronous condenser deployments and hyperscaler capacity additions continue to support market momentum.

Key Report Takeaways

- By type, cylindrical-rotor generators held 42.1% of the global synchronous generator market share in 2025, while permanent-magnet synchronous generators are forecast to grow at a 9.5% CAGR through 2031.

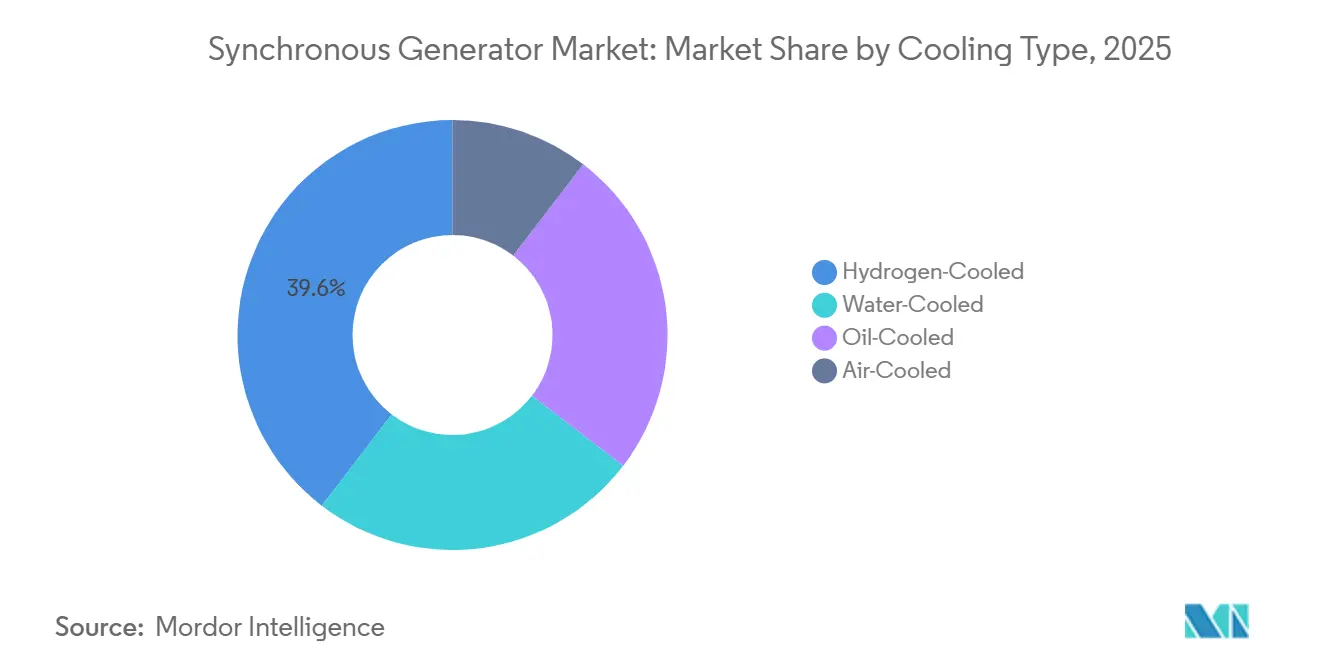

- By cooling type, hydrogen-cooled synchronous generators accounted for 39.6% of the global synchronous generator market share in 2025 and are projected to grow at a 5.8% CAGR through 2031.

- By phase, three-phase synchronous generators accounted for 91.2% of the global synchronous generator market share in 2025 and are projected to grow at a 5.6% CAGR through 2031.

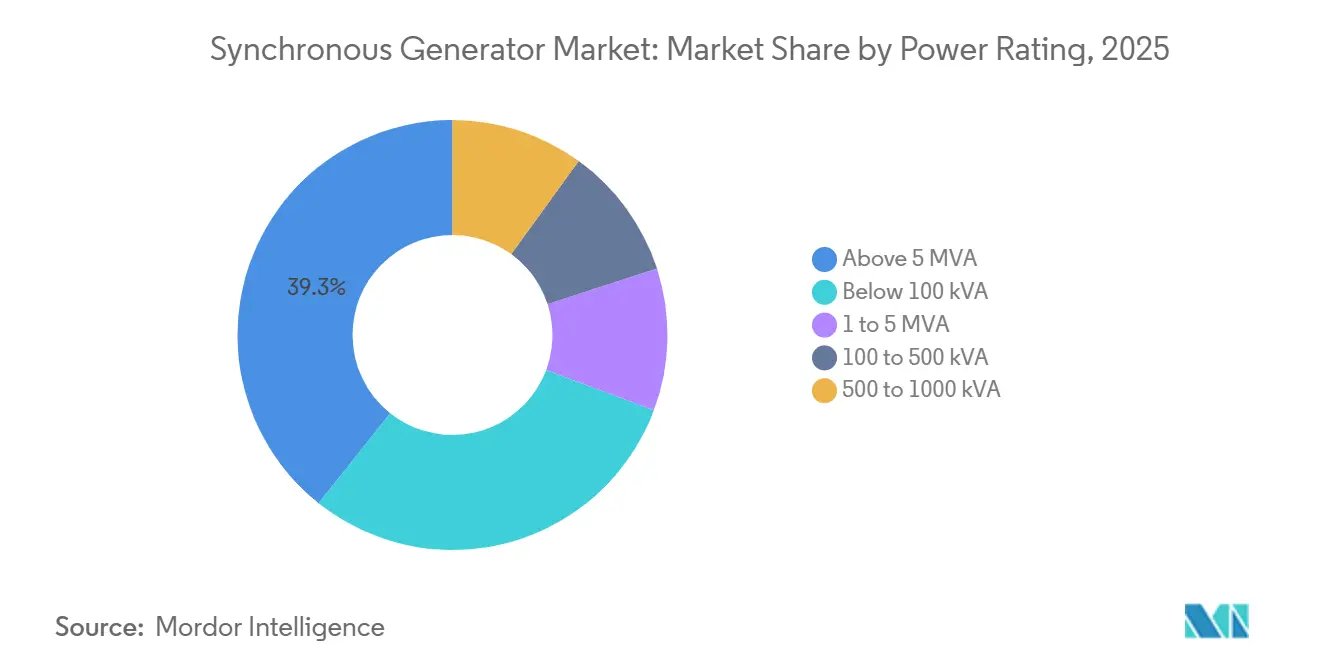

- By power rating, generators rated above 5 MVA accounted for 39.3% of the global synchronous generator market share in 2025, while the 1 to 5 MVA segment is anticipated to register a 6.9% CAGR through 2031.

- By application, power plants accounted for 64.7% of the global synchronous generator market share in 2025, while data centers are projected to grow at a 6.3% CAGR through 2031.

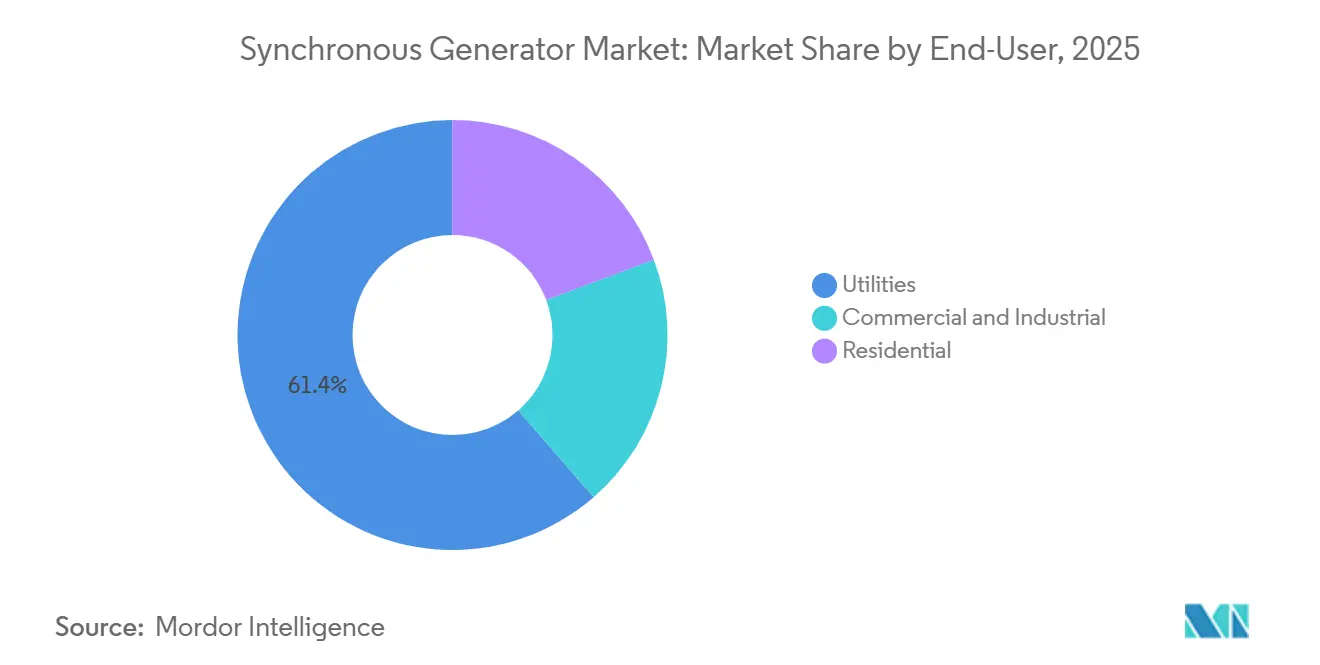

- By end-user, utilities accounted for 61.4% of the global synchronous generator market share in 2025 and are expected to grow at a 5.5% CAGR through 2031.

- By geography, North America accounted for 31.9% of the global synchronous generator market share in 2025, while Asia-Pacific is projected to grow at a 6.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Synchronous Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for grid-stabilizing generators in renewable-heavy power mixes | +1.2% | Global, with concentration in North America, Europe, Australia | Medium term (2-4 years) |

| Rapid expansion of hyperscale data centers worldwide | +0.9% | North America (60%), APAC (25%), Europe (15%) | Short term (≤ 2 years) |

| Industrial output growth in emerging economies | +0.8% | APAC core (India, Vietnam, Indonesia), spill-over to Middle East | Long term (≥ 4 years) |

| Modernization of ageing thermal & hydro plants in OECD | +0.7% | North America, Europe, Japan | Medium term (2-4 years) |

| Grid operators adopting synchronous condensers for inertia | +0.6% | North America, Australia, Ireland, United Kingdom | Short term (≤ 2 years) |

| Naval platforms shifting to integrated electric propulsion | +0.3% | United States, Poland, United Kingdom, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Grid-Stabilizing Generators in Renewable-Heavy Power Mixes

Transmission operators are turning to synchronous condensers because wind and solar penetration above 40% of the instantaneous load can trigger frequency deviations that violate NERC PRC-024-4 ride-through limits within milliseconds. Siemens Energy commissioned a 250 MVAr unit at Ireland’s Moneypoint site in 2024, providing 3,500 MW of inertia and reactive support for a dispatch that now tops 70% renewables.[1]Siemens Energy, “Synchronous Condenser Portfolio,” siemens-energy.com GE Vernova delivered a similar installation in Townsville, Australia, where cyclone-islanded operation raises stability risk. ENTSO-E’s 2024 roadmap obliges every European TSO to meet minimum inertia floors by 2027, effectively guaranteeing a multiyear order pipeline for synchronous machines.[2]ENTSO-E, “System Inertia Roadmap 2024,” entsoe.eu The physical-inertia attribute cannot be replicated economically by grid-forming inverters today, anchoring long-term value.

Rapid Expansion of Hyperscale Data Centers Worldwide

Hyperscalers are procuring on-site gas turbine generation to bypass interconnection bottlenecks and secure local baseload power for AI workloads that draw 50–100 MW per hall. Meta's Hyperion campus in Louisiana will deploy 7.5 GW of combined-cycle capacity with synchronous generators between 2026 and 2030. Microsoft signed a USD 16 billion power purchase agreement in 2024 to restart the 835 MW Three Mile Island Unit 1 reactor exclusively for its Pennsylvania cloud region. Amazon and Google have executed similar nuclear and SMR arrangements, reflecting a broader shift toward behind-the-meter generation that favors 1–5 MVA modules. Bloomberg estimates hyperscaler capital expenditure at USD 640 billion through 2027, of which USD 240 billion targets physical infrastructure such as generators and transformers.

Industrial Output Growth in Emerging Economies

India plans to double its installed capacity from 520.5 GW in 2025 to 1,121 GW by 2035-36, retaining 315 GW of coal-fired generation to support variable renewables. Vietnam adopted a USD 136 billion electrification plan targeting 183-236 GW by 2030, emphasizing combined-cycle gas turbines with synchronous generators for inertia and voltage control. Indonesia's PLN plans 69.5 GW of additions through 2034, anchored by coal and geothermal plants that require synchronous machines for grid-code compliance. OEMs such as Harbin Electric and BHEL are securing multi-gigawatt thermal orders by bundling long-term service agreements that reduce lifecycle cost risks.

Modernization of Aging Thermal & Hydro Plants in OECD

Utilities in North America and Europe are extending asset lives by replacing 30- to 50-year-old stators with high-efficiency windings, adding brushless excitation, and converting to hydrogen cooling. ANDRITZ upgraded a 122 MW unit at Norway's Vamma hydro plant and rewound a 215 MVA generator at the New York Power Authority's Niagara project under a USD 1.1 billion program. ABB is increasing Fortum's Loviisa nuclear output by 38 MW through generator modernization scheduled through 2027. Such retrofits cost one-quarter of greenfield builds yet deliver a 1-2% efficiency gain, supporting the continued relevance of synchronous generators in mature grids.

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost competitiveness of inverter-based induction generators | -0.8% | Global, with higher impact in cost-sensitive emerging markets | Medium term (2-4 years) |

| High CAPEX and maintenance intensity | -0.6% | Global | Long term (≥ 4 years) |

| Supply-chain tightness for rare-earth magnets | -0.5% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Tighter NOx/CO₂ norms accelerating shift to non-rotating solutions | -0.4% | Europe, California, select OECD jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Competitiveness of Inverter-Based Induction Generators

Grid-forming inverters deliver 20-30% lower upfront cost and simpler maintenance for applications where inertia is noncritical. NREL’s 2024 study confirmed they can emulate voltage-source behavior, but inadequate kinetic energy limits their ability to arrest large-signal frequency excursions. South Australia’s 100% renewable demonstration achieved two-hour stability using synthetic inertia, yet required over-specification of batteries, offsetting some capex benefit. Cost-sensitive markets in Southeast Asia and Africa favor induction-generator packages paired with static VAR compensators, which deliver roughly 85% of synchronous-machine performance at 60-70% of the cost.

High CAPEX and Maintenance Intensity

Utility-scale synchronous generators cost USD 500-800 per kW installed, and hydrogen-cooled units require quarterly seal inspections to maintain ≥ 98% purity. Large plants allocate USD 2-4 million annually for generator maintenance, including rotor rewind outages every 24-36 months. Permanent-magnet designs reduce O&M costs but increase upfront material costs; a 10 MW offshore wind turbine requires 6 metric tons of NdFeB magnets, valued at USD 1.8-2.4 million at 2025 prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Permanent-Magnet Machines Outpace Legacy Designs

Permanent-magnet synchronous generators are expanding at a 9.5% CAGR, nearly twice the synchronous generator market average. Their compact footprint attracts offshore wind and naval customers, while brushless excitation eliminates slip-ring maintenance. Cylindrical-rotor machines retained 42.1% of the synchronous generator market share in 2025, as 3,000–3,600 RPM steam- and gas-turbine drives continue to dominate baseload build-outs and their iron-core rotors are not affected by rare-earth supply shortages. Salient-pole units remain essential in hydro plants, where low-speed, high-pole designs provide large diameters without excessive centrifugal stress.

Rare-earth supply risk is limiting PMSG penetration. China's export controls pushed NdFeB magnet prices 18–22% higher in 2025, raising offshore wind capital expenditure forecasts. Research into high-entropy borides and manganese-based magnets could enable rare-earth-free rotors after 2028, easing supply constraints but not affecting the synchronous generator market size in the near term. Meanwhile, brushless wound-rotor machines are finding a practical application in marine and industrial settings by extending operation and maintenance intervals from 5,000 to 10,000 hours through static excitation.

By Cooling Type: Hydrogen Dominates Utility-Scale Installations

Hydrogen-cooled designs held 39.6% of the synchronous generator market in 2025 and are expected to grow at a CAGR of 5.8% through 2031. Superior thermal conductivity enables high power density; the payback period for retrofitting a 300 MVA air-cooled unit to hydrogen averages 3 years at an 80% capacity factor. Plants above 200 MVA predominantly select hydrogen cooling, while air-cooled machines continue to dominate below-100 kVA standby sets where simplicity takes priority over efficiency.

Hybrid water-hydrogen systems in ultra-high-power nuclear units reduce stator hot-spots by 12-15 °C, prolonging insulation life by up to 40%. Maintenance complexity remains a barrier: operators must maintain 98% hydrogen purity and monitor seals quarterly to avoid explosive mixtures. Air-cooled machines carry a 0.8-1.2% efficiency penalty and require 20-30% larger frames; however, their lower auxiliary-system cost keeps them attractive in distributed-generation and mobile applications.

By Phase: Three-Phase Machines Serve Universal Demand

Three-phase machines accounted for 91.2% of the synchronous generator market share in 2025 and are projected to grow at a CAGR of 5.6%. Constant torque output, lower conductor mass, and simpler transformer integration make them the standard choice for outputs above 10 kVA. Single-phase units remain in use for residential backup and rural irrigation applications where split-phase distribution is common. Defense and emergency-response agencies continue to procure sub-1 MVA single-phase sets; however, three-phase machines dominate in AI data centers, industrial campuses, and combined-cycle plants.

By Power Rating: Mid-Range Units Benefit from Data-Center Boom

Generators rated 1-5 MVA represent the fastest-growing power band, at a CAGR of 6.9%, driven by hyperscalers deploying modular blocks to bypass grid queues. Orders for 4.5 MVA gas gensets under Meta and Atlas Energy frameworks illustrate this trend. Generators above 5 MVA still account for 39.3% of the synchronous generator market, supported by utility-scale thermal, hydro, and nuclear projects where single-unit ratings can exceed 1 GVA. Long lead times and engineering complexity maintain high barriers to entry in this upper tier.

By Application: Data Centers Erode Power-Plant Dominance

Power plants account for 64.7% of demand. Data centers are growing at a 6.3% CAGR, driven by AI expansion and gigawatt-scale on-site generation requirements. Hyperscaler power purchase agreements for nuclear restarts and gas turbine blocks reflect strong demand, shifting market dynamics toward mid-size modules and 24/7 service contracts. Industrial cogeneration, marine propulsion, and mining make up the remainder of demand, each with specialized duty cycles that favor rugged synchronous designs.

By End-User: Utilities Retain Majority Share

Utilities accounted for 61.4% of the 2025 value and are projected to grow at a 5.5% CAGR, as emerging market build-outs offset retirements in OECD countries. Commercial and industrial buyers, led by data center operators, are gaining market share through captive power strategies that hedge against interconnection delays and price volatility. Residential uptake remains marginal, limited to micro-grids and premium backup applications.

Geography Analysis

North America accounted for 31.9% of 2025 revenue. FERC Order 842 and NERC PRC-024-4 upgrades, along with synchronous condenser retrofits at retired coal plants, support replacement demand. Hyperscalers in Virginia, Texas, and the Pacific Northwest are securing multi-gigawatt on-site capacity, while nuclear uprates in Canada and combined-cycle tenders in Mexico contribute additional volume.

Asia-Pacific is the fastest-growing region, with a CAGR of 6.1%. India, Vietnam, and Indonesia are ordering multi-gigawatt coal, gas, and hydro projects that require synchronous machines for inertia and voltage regulation. Japan's reactor restarts, China's ultra-supercritical builds, and gas conversions across ASEAN further broaden the market base.

Europe is balancing coal plant exits with inertia mandates. ENTSO-E's 2027 floor requirement is driving condenser installations even as Germany retires 42 GW of synchronous capacity. Nuclear uprates in Finland and hydro modernizations across Scandinavia sustain retrofit activity, while Russia's Volzhskaya overhaul adds 2.7 GW of refurbished units.

Competitive Landscape

The global synchronous generator market is consolidated. Siemens Energy, GE Vernova, ABB, and Mitsubishi Heavy Industries dominate utility-scale awards, while regional firms such as Harbin Electric, BHEL, Doosan Enerbility, and WEG compete on cost and local content. GE Vernova's electrification backlog reached USD 34.7 billion in 2024, following a 48% surge, supported by its USD 5.3 billion Prolec GE transformer acquisition that enables bundled grid-stabilization packages. Siemens Energy secured a USD 1.5 billion, 25-year maintenance contract in Saudi Arabia covering 4 GW of capacity, strengthening its recurring revenue base.

Innovation activity is concentrated in hydrogen cooling, brushless excitation, and digital twins. BRUSH Group reports 106 hydrogen-cooled units totaling 11,250 MW installed, while Materials Nexus and Georgetown University are developing rare-earth-free magnets that could alter permanent-magnet economics after 2028. Grid-forming inverters from Tesla, Fluence, and Wärtsilä compete in segments where grid inertia is less critical, pressuring synchronous generator manufacturers to strengthen their value propositions.

Synchronous Generator Industry Leaders

General Electric Company

Siemens AG

ABB Ltd.

Mitsubishi Heavy Industries, Ltd.

Andritz AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE Vernova committed over 2.7 GW of U.S.-manufactured turbines to the SunZia project and other wind farms, reinforcing domestic production

- March 2025: ANDRITZ won a generator contract from BC Hydro, deepening its North American hydro modernization presence

- February 2025: GE Vernova invested USD 10 million in its Pittsburgh plant to add FLEX INVERTER production for solar and storage

- December 2024: ABB moved to purchase Gamesa Electric’s power electronics business, adding a 40 GW installed base

Global Synchronous Generator Market Report Scope

An alternator, or synchronous generator, transforms mechanical energy from a prime mover into AC electric power. It operates at a constant "synchronous speed," aligned with the grid frequency. Utilizing electromagnetic induction, the device features a rotating DC-excited rotor that generates a magnetic field, subsequently inducing voltage in its stationary stator.

The synchronous generator market is segmented by type, cooling type, phase, power rating, application, end-user, and geography. By type, the market is segmented into cylindrical rotor synchronous generators, salient pole synchronous generators, brushless synchronous generators, and permanent-magnet synchronous generators (PMSG). By cooling type, the market is segmented into air-cooled, hydrogen-cooled, water-cooled, and oil-cooled. By phase, the market is segmented into single-phase and three-phase. By power rating, the market is segmented into below 100 KVA, 100 to 500 KVA, 500 to 1000 KVA, 1 to 5 MVA, and above 5 MVA. By application, the market is segmented into power plants, industrial, oil and Gas, marine, mining, data centres, and others (Aerospace, Military, Commercial Buildings). By end-user, the market is segmented into utilities, commercial and industrial, and residential. The report also covers the market size and forecasts for the synchronous generator market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Cylindrical Rotor Synchronous Generators |

| Salient Pole Synchronous Generators |

| Brushless Synchronous Generators |

| Permanent-Magnet Synchronous Generators (PMSG) |

| Air-Cooled |

| Hydrogen-Cooled |

| Water-Cooled |

| Oil-Cooled |

| Single-Phase |

| Three-Phase |

| Below 100 kVA |

| 100 to 500 kVA |

| 500 to 1000 kVA |

| 1 to 5 MVA |

| Above 5 MVA |

| Power Plants |

| Industrial |

| Oil and Gas |

| Marine |

| Mining |

| Data Centres |

| Others (Aerospace, Military, Commercial Buildings) |

| Utilities |

| Commercial and Industrial |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Cylindrical Rotor Synchronous Generators | |

| Salient Pole Synchronous Generators | ||

| Brushless Synchronous Generators | ||

| Permanent-Magnet Synchronous Generators (PMSG) | ||

| By Cooling Type | Air-Cooled | |

| Hydrogen-Cooled | ||

| Water-Cooled | ||

| Oil-Cooled | ||

| By Phase | Single-Phase | |

| Three-Phase | ||

| By Power Rating | Below 100 kVA | |

| 100 to 500 kVA | ||

| 500 to 1000 kVA | ||

| 1 to 5 MVA | ||

| Above 5 MVA | ||

| By Application | Power Plants | |

| Industrial | ||

| Oil and Gas | ||

| Marine | ||

| Mining | ||

| Data Centres | ||

| Others (Aerospace, Military, Commercial Buildings) | ||

| By End-user | Utilities | |

| Commercial and Industrial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the synchronous generator market in 2031?

The synchronous generator market is forecast to reach USD 7.74 billion by 2031.

Which region will grow fastest through 2031?

Asia-Pacific leads with a projected 6.1% CAGR, driven by large capacity additions in India, Vietnam, and Indonesia.

Why are data centers important for future demand?

Hyperscale campuses are installing gigawatt-scale on-site generation to secure reliable power for AI workloads, boosting mid-range synchronous generator orders.

How do hydrogen-cooled generators compare with air-cooled units?

Hydrogen cooling delivers 1-2% higher efficiency and shorter payback for plants above 200 MVA, though it requires stringent purity monitoring.

What is the main competitive threat to synchronous machines?

Grid-forming inverters and induction generators offer lower capex for applications where physical inertia is less critical, challenging market share in certain OECD markets.

Page last updated on: