Reconstituted Milk Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

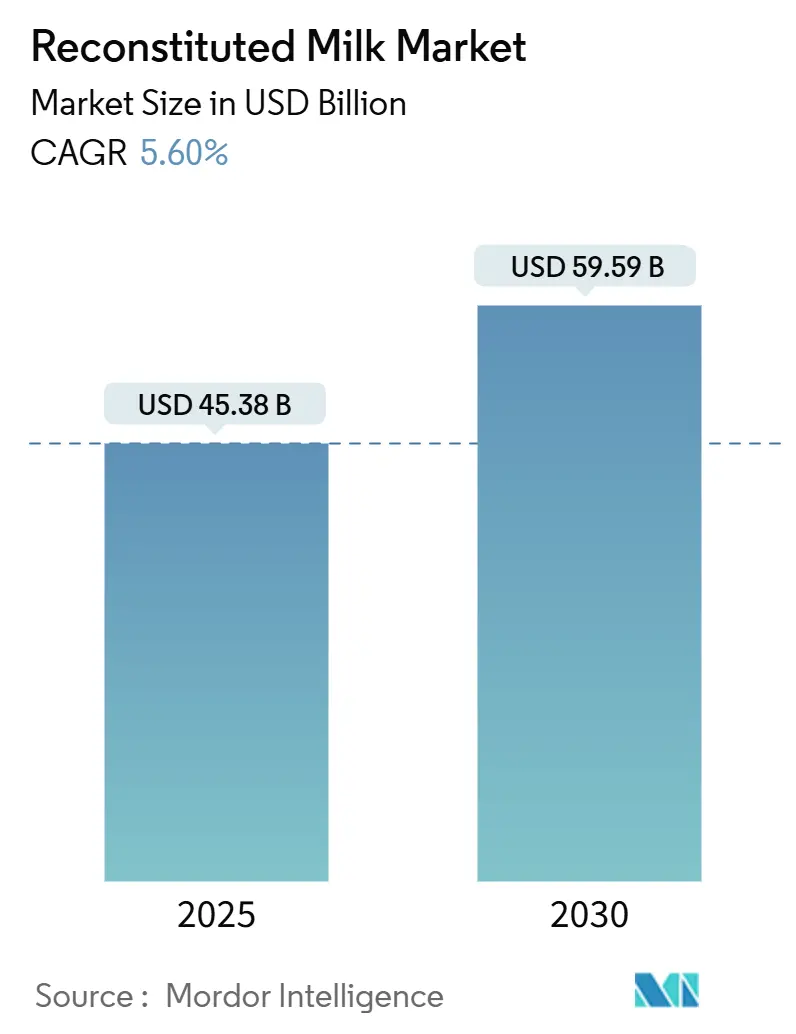

| Market Size (2025) | USD 45.38 Billion |

| Market Size (2030) | USD 59.59 Billion |

| Growth Rate (2025 - 2030) | 5.60% CAGR |

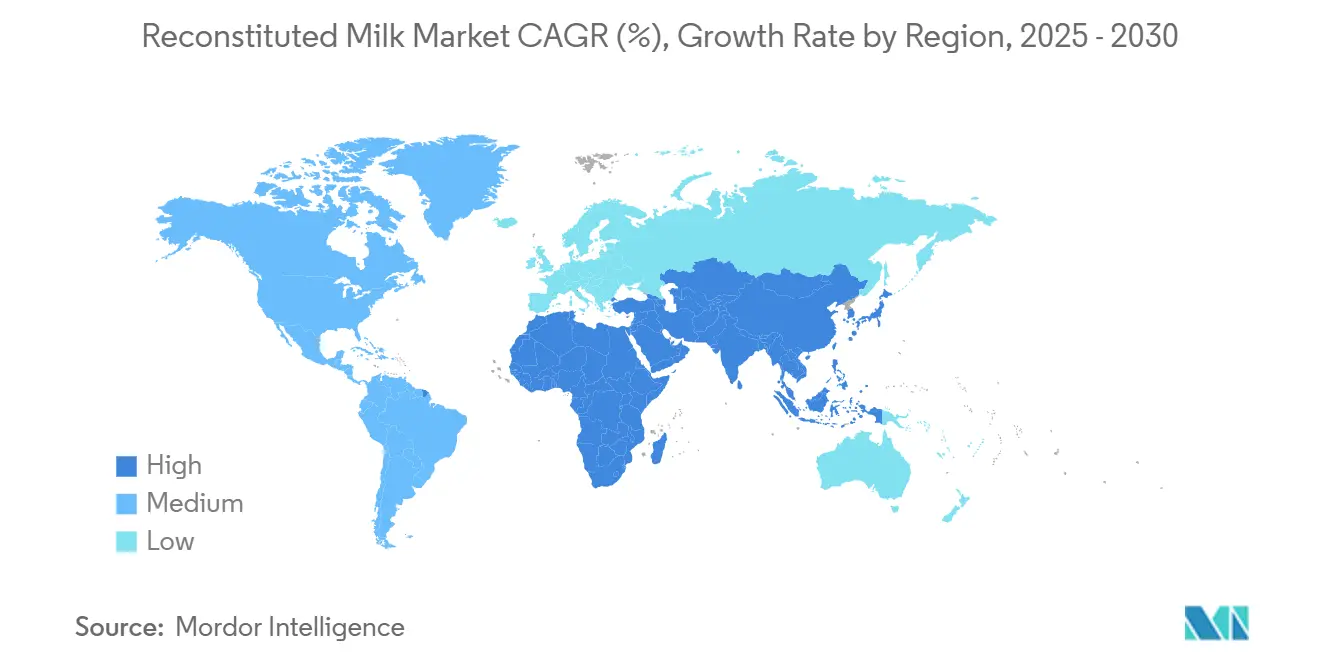

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

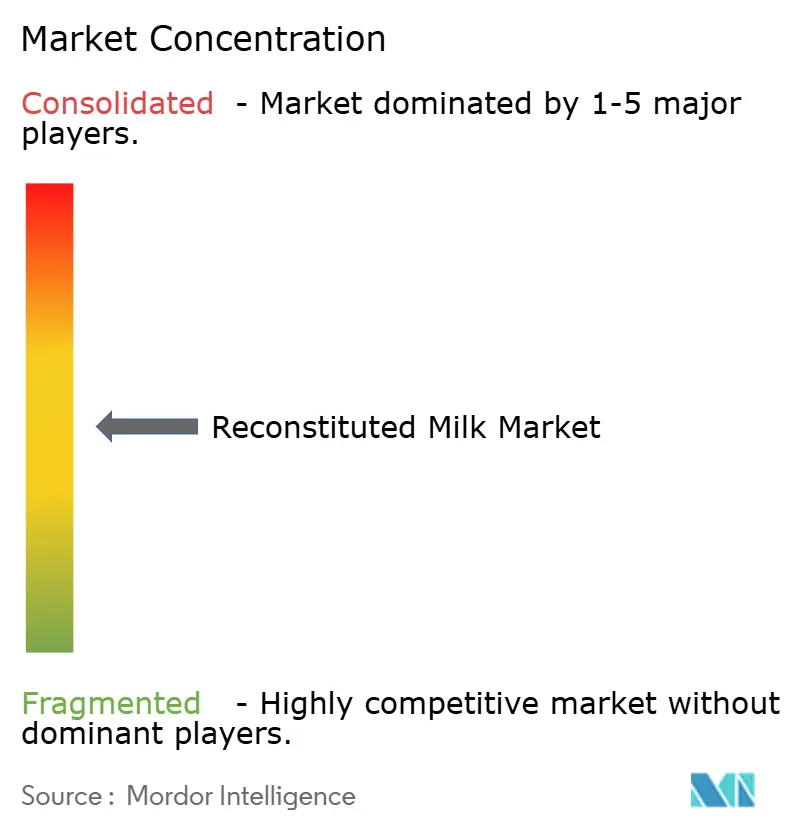

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Reconstituted Milk Market Analysis by Mordor Intelligence

The reconstituted milk market size reached USD 45.38 billion in 2025 and is projected to advance to USD 59.59 billion by 2030, expanding at a 5.60% CAGR over the forecast period. Growth is supported by rising preference for shelf-stable dairy formats, heightened penetration in regions with limited cold-chain infrastructure, and policy support for school milk schemes. Technology upgrades in low-temperature recombination are closing the sensory gap with fresh milk, enabling premium pricing. Conversely, exposure to skim-milk-powder price swings and the ascent of plant-based drinks temper near-term margins, making supply-chain agility a competitive differentiator within the reconstituted milk market.

Key Report Takeaways

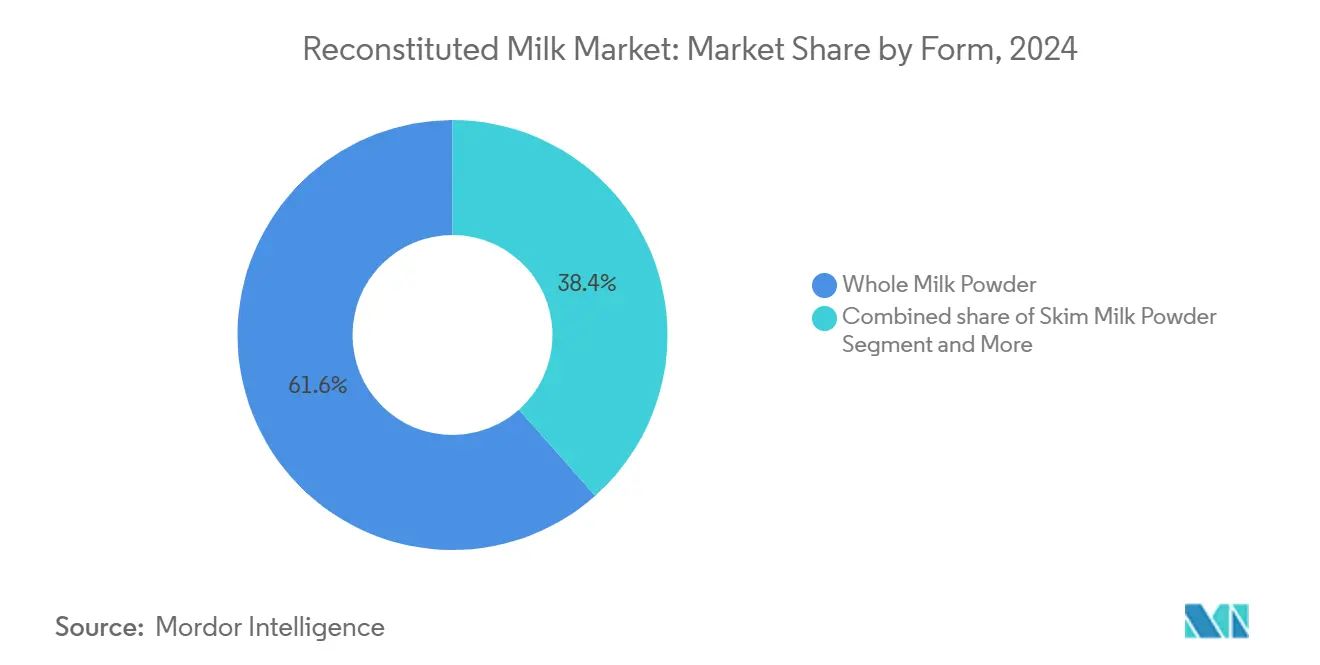

- By form, whole milk powder reconstitution held 62.18% of the reconstituted milk market share in 2024, while fortified formulations are tracking 7.42% CAGR growth through 2030.

- By application, direct milk consumption represented 44.25% of the reconstituted milk market size in 2024, whereas yogurt applications are forecast to expand at an 8.15% CAGR.

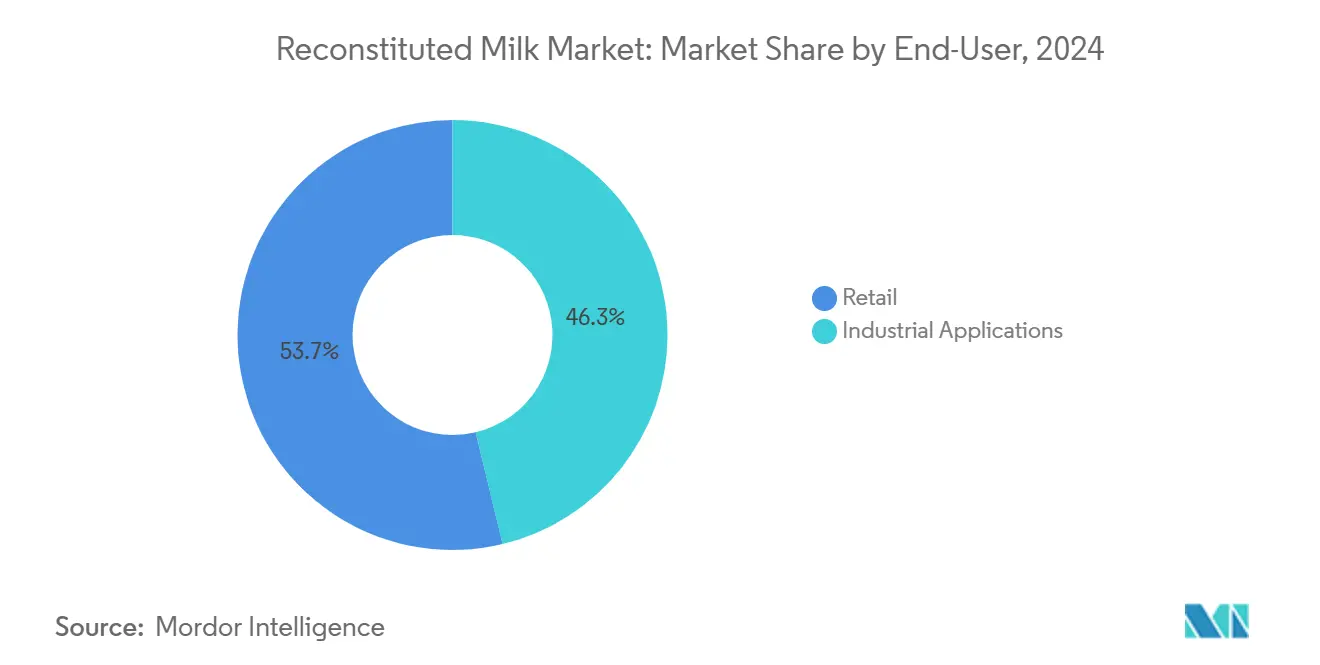

- By distribution channel, retail accounted for 54.28% of revenue in 2024; industrial end-users are rising at a 6.95% CAGR as foodservice and packaged-food manufacturers prioritize shelf-stable inputs.

- By geography, Asia-Pacific contributed 47.16% of global sales in 2024 and is poised to register a 7.92% CAGR through 2030, reinforcing its role as the growth nucleus for the reconstituted milk market.

Global Reconstituted Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust demand for shelf-stable dairy in emerging markets | +1.2% | Asia-Pacific, Africa, Latin America | Medium term (2-4 years) |

| Rising infant-formula consumption in Asia-Pacific | +0.8% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Expansion of e-commerce grocery platforms | +0.6% | Global, with early gains in North America, Europe | Short term (≤ 2 years) |

| Government-backed school milk programs | +0.9% | Asia-Pacific, Africa, select Latin America | Medium term (2-4 years) |

| Surge in high-protein ready-to-mix beverage launches | +0.7% | North America, Europe, urban Asia | Short term (≤ 2 years) |

| Low-temperature recombination tech cutting flavor loss | +0.4% | Global, led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Demand for Shelf-Stable Dairy in Emerging Markets

In Sub-Saharan Africa, UHT milk consumption is set to hit a high, marking a robust 13% growth from the previous year. This uptick is largely attributed to urbanization trends that favor the convenience of shelf-stable products, especially in areas where refrigeration hasn't kept pace with population surges. Such dynamics offer a distinct edge to reconstituted milk producers, allowing them to tap into markets that were once the domain of fresh dairy suppliers. Meanwhile, with oil prices on the decline, packaging innovations have flourished, enhancing shelf life and streamlining distribution. This evolution empowers brands to connect with rural consumers via standard retail channels, sidestepping the need for costly cold-chain setups.

Rising Infant-Formula Consumption in Asia-Pacific

Asia-Pacific infant formula demand is reshaping reconstituted milk supply chains, with China's new national food safety standards for infant formula taking effect in March 2026, requiring enhanced nutritional profiles and stricter manufacturing protocols[1]U.S. Department of Agriculture. "China: National Food Safety Standard for Cream Butter and Anhydrous Milk Fat Finalized." fas.usda.gov/data. The regulatory upgrade coincides with H&H Group's 44.3% revenue growth in Q1 2025 from infant formula sales, demonstrating how premium positioning can offset declining birth rates through higher per-unit value capture. This dynamic creates sustained demand for high-quality milk powder inputs that meet increasingly stringent nutritional and safety requirements. The shift toward premium infant nutrition products generates higher margins for reconstituted milk suppliers who can demonstrate compliance with evolving regulatory frameworks.

Expansion of E-commerce Grocery Platforms

E-commerce grocery expansion is fundamentally altering dairy distribution patterns, with online food and beverage retail sales positioning for continued growth as the primary driver of food sector expansion[2]Putch, Kristen. "Dairy industry examines e-commerce trends, shipping, food safety." Supermarket Perimeter, supermarketperimeter.com. The direct-to-consumer model enables dairy manufacturers to bypass traditional retail intermediaries while maintaining better control over product positioning and customer relationships. Reconstituted milk products benefit disproportionately from this channel shift due to their extended shelf life and reduced shipping complexity compared to fresh alternatives. The FDA and USDA have established best practices for online dairy orders that emphasize proper packaging and temperature control, creating standardized protocols that favor shelf-stable products over perishable alternatives.

Government-Backed School Milk Programs

Government nutrition initiatives are creating institutional demand anchors that provide predictable revenue streams for reconstituted milk suppliers, with the US Whole Milk for Healthy Kids Act advancing through Congress to allow whole and reduced-fat milk in school cafeterias[3]Teodora Lyubomirova, “Whole Milk for Healthy Kids Act Expected to Move to Senate,” dairyreporter.com. The legislation addresses declining milk consumption among school-aged children, where 75% fail to meet daily dairy intake recommendations, creating a policy-driven demand floor for milk products in educational settings. Indonesia's parallel initiative targeting 83 million students represents the largest institutional feeding program globally, with initial costs exceeding USD 11 billion annually and creating sustained demand for shelf-stable dairy formats that can withstand tropical distribution challenges. These programs establish long-term contracts that provide revenue visibility while reducing market volatility for participating suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile global skim-milk-powder pricing | -0.8% | Global, acute in export-dependent regions | Short term (≤ 2 years) |

| Growing consumer shift to plant-based dairy alternatives | -1.1% | North America, Europe, urban Asia | Medium term (2-4 years) |

| Tighter regulations on palm-oil-based fat-filled powders | -0.3% | Europe, select Asian markets | Long term (≥ 4 years) |

| Carbon-footprint labeling curbing demand in Europe | -0.4% | Europe core, expanding to developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Global Skim-Milk-Powder Pricing

Skim milk powder price volatility is constraining reconstituted milk profitability, with EU production declining 3% in 2024 to just under 1.5 million tons due to reduced Asian import demand and processors favoring cheese production over powder manufacturing. This supply contraction coincides with China's dairy market uncertainty, where suppliers face 24 months of declining farmgate prices and historically high powder inventories that depress global pricing benchmarks. The pricing instability forces reconstituted milk manufacturers to implement more sophisticated hedging strategies while potentially passing cost volatility to end consumers. Raw material cost fluctuations of 15-20% within quarterly periods create margin compression that particularly impacts smaller regional players lacking financial resources to weather extended price cycles

Growing Consumer Shift to Plant-Based Dairy Alternatives

Plant-based dairy alternatives are capturing market share through improved taste profiles and aggressive pricing strategies. The growth trajectory for plant-based milk exceeds traditional dairy expansion rates and reflects consumer preferences for perceived health and environmental benefits over conventional dairy products. Oatly's market challenges, including supply chain disruptions and declining stock prices, demonstrate that plant-based success requires sustained operational excellence rather than just consumer interest. The competitive pressure forces reconstituted milk producers to emphasize nutritional advantages and cost competitiveness while potentially exploring hybrid products that blend dairy and plant-based ingredients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominance Faces Fortification Challenge

In 2024, whole milk powder reconstitution commands a dominant 62.18% market share, underscoring a strong consumer preference for full-fat dairy products known for their traditional taste and nutritional richness. Yet, there's a notable surge of 7.42% CAGR in fortified formulations, driven by health-conscious consumers who seek benefits that transcend basic nutrition. This disparity in growth rates hints at a market evolution: premium positioning through vitamin and mineral enhancements is carving out differentiation opportunities, justifying elevated price points. While skim milk powder reconstitution enjoys consistent demand in budget-sensitive applications, fortified variants are making inroads, especially in the burgeoning sports nutrition and elder care markets.

The contrast between leading market shares and growth trajectories underscores a shift in consumer focus, prioritizing functional benefits over conventional dairy attributes. In a testament to this shift, Arla Foods has teamed up with Valley Queen to roll out Nutrilac ProteinBoost ingredients. This move highlights how industry stalwarts are pivoting towards protein-enriched formulations, eyeing the burgeoning high-protein beverage sector. Central to this collaboration is the installation of new machinery at Valley Queen's South Dakota plant, which has the capacity to process 3 billion pounds of milk annually. Such a scale underscores the competitive edge in protein ingredient production. This trend of infrastructure investment points to a future where specialized manufacturing for fortified formulations could lead to a consolidation of production, favoring larger industry players.

By Application: Milk Consumption Leads While Yogurt Accelerates

In 2024, direct milk consumption commands a 44.25% share of the market, solidifying its status as the leading end-use for reconstituted milk products in both developed and emerging markets. This stronghold is rooted in milk's universal appeal as a dietary staple, offering vital nutrition to a growing global populace. Meanwhile, yogurt applications are on the rise, expanding at 8.15% CAGR through 2030, mirroring a consumer shift towards probiotic-rich foods and health-conscious snacking. This divergence in growth rates between traditional milk and the burgeoning yogurt segment underscores a maturation in established markets and a surge in value-added categories.

Applications like cheese, ice cream, and baked goods, while maintaining consistent demand, bolster overall market stability and drive volume growth through industrial food channels. The success of ambient yogurt products, especially in China, highlights the potential of shelf-stable formats to revolutionize conventional dairy categories. Such innovations not only facilitate yogurt consumption in areas without refrigeration but also open new distribution avenues for reconstituted milk suppliers. This trend of ambient yogurt is making inroads into Africa and Brazil, with forecasts suggesting a production surge to 10 million liters by 2025, underscoring the vast potential for shelf-stable dairy applications.

By End-User: Retail Strength Meets Industrial Growth

In 2024, retail distribution channels seize a commanding 54.28% market share, riding the wave of consumer preference for branded products and the ease of purchasing reconstituted milk from established grocery networks. This dominance underscores the pivotal role of consumer marketing and brand recognition in shaping dairy product purchase decisions. Meanwhile, industrial applications are on an upward trajectory, expanding at a 6.95% CAGR through 2030. This growth is fueled by food service operators and manufacturers who are gravitating towards reconstituted milk as a cost-effective alternative to fresh dairy, offering both supply chain predictability and extended storage capabilities.

The industrial sector's momentum is bolstered by the operational advantages of reconstituted milk over its fresh counterparts. These advantages include slashed transportation costs, streamlined inventory management, and the elimination of cold-chain requirements. Convenience stores and online retail are steadily increasing their market share, thanks to enhanced product availability and efforts to educate consumers on the benefits of reconstituted milk. Additionally, the foodservice and institutional segment reaps rewards from government nutrition programs and commercial food operations, which prioritize cost efficiency and operational simplicity over the premium positioning of fresh dairy.

Geography Analysis

Asia-Pacific holds 47.16% market share in 2024 while expanding at 7.92% CAGR through 2030, creating a dual advantage of scale and momentum that positions the region as the primary growth engine for global reconstituted milk demand. This leadership stems from large population bases with rising disposable incomes, government nutrition initiatives, and infrastructure constraints that favor shelf-stable dairy products over fresh alternatives. The region's growth trajectory reflects urbanization patterns that increase dairy consumption while creating distribution challenges that reconstituted milk products are uniquely positioned to address.

North America and Europe maintain significant market positions through established consumption patterns and premium product positioning, though growth rates lag behind Asia-Pacific due to market maturity and competition from plant-based alternatives. The Middle East and Africa represent emerging opportunities where population growth and economic development are driving increased dairy consumption, particularly in urban centers where convenience and shelf stability provide competitive advantages.

South America is witnessing steady expansion, primarily driven by Brazil’s expanding middle class and the rising preference for packaged dairy products that ensure consistent quality, safety, and extended shelf life. Growing urbanization and evolving retail infrastructure are further supporting the shift from traditional fresh dairy to reconstituted milk, as consumers increasingly seek convenient, reliable, and affordable nutrition options. This structural transformation in consumption behavior underscores the region’s gradual but stable contribution to global market growth.

Competitive Landscape

The reconstituted milk market exhibits moderate concentration with a 5 out of 10 rating, indicating sufficient fragmentation to support both global leaders and regional specialists while maintaining competitive pricing dynamics. Major players, including Nestlé, Fonterra, Danone, FrieslandCampina, and Arla Foods, leverage scale advantages in procurement and distribution while competing through product innovation and geographic expansion strategies. The market structure enables niche players to capture value through specialized applications or regional expertise, particularly in emerging markets where local knowledge and distribution networks provide sustainable competitive advantages.

Strategic patterns emphasize vertical integration and technology adoption to improve operational efficiency and product quality. The FDA approved Tamarack Biotics' TruActive UV milk treatment technology in June 2025, an advancement in non-thermal processing that preserves nutritional and immune-active components. This innovation addresses growing consumer demand for minimally processed foods while maintaining the safety standards required for shelf-stable products.

Technology adoption trends indicate that companies prioritizing advanced processing solutions and automation are poised to strengthen their market position through enhanced product consistency, nutritional retention, and cost efficiency. Investments in innovations such as non-thermal treatment, membrane filtration, and digitalized quality monitoring enable manufacturers to deliver superior shelf-stable milk with minimal nutrient loss, aligning with evolving consumer expectations for clean-label and high-quality dairy products. Conversely, traditional players with limited technological adaptation may encounter margin compression and competitive disadvantages as efficiency-driven, innovation-led firms redefine industry benchmarks.

Reconstituted Milk Industry Leaders

-

Nestlé S.A.

-

Fonterra Co-operative Group

-

Danone S.A.

-

FrieslandCampina N.V.

-

Arla Foods amba

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nova Dairy has launched a skimmed milk powder, targeting those who seek the benefits of milk without the added fat. This product is tailored for health-conscious individuals and families in search of a convenient and dependable milk alternative.

- February 2025: Dairy Farmers of America launched Milk50, a low-calorie fluid milk containing 50 calories per serving and 75% less sugar than fat-free skim milk, utilizing advanced ultra-filtration technology Food Business News. The product targets health-conscious consumers seeking real dairy alternatives to plant-based beverages.

- January 2024: Hatsun Agro Product announced acquisition of Milk Mantra Dairy to expand market presence in India's growing dairy sector. The deal strengthens Hatsun's position in the reconstituted milk market through increased production capacity and distribution reach.

Global Reconstituted Milk Market Report Scope

| Whole Milk Powder (WMP) Reconstitution |

| Skim Milk Powder (SMP) Reconstitution |

| Other Fortified Formulations |

| Milk (Direct Consumption) |

| Cheese |

| Yogurt |

| Ice Cream |

| Bakery and Confectionery |

| Others |

| Industrial applications (B2B) | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Foodservice/Institutional |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa |

| By Form | Whole Milk Powder (WMP) Reconstitution | |

| Skim Milk Powder (SMP) Reconstitution | ||

| Other Fortified Formulations | ||

| By Application | Milk (Direct Consumption) | |

| Cheese | ||

| Yogurt | ||

| Ice Cream | ||

| Bakery and Confectionery | ||

| Others | ||

| End-User | Industrial applications (B2B) | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Foodservice/Institutional | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the reconstituted milk market in 2030

The reconstituted milk market is projected to reach USD 59.59 billion by 2030, expanding at a 5.60% CAGR.

Which region leads both size and growth in global demand?

Asia-Pacific holds 47.16% of sales and is forecast to advance at a 7.92% CAGR, sustaining dual leadership.

Why are fortified formulations growing faster than whole milk powder?

Health-conscious consumers pay premiums for vitamin and protein enrichment, driving a 7.42% CAGR for fortified products through 2030.

How are e-commerce channels influencing distribution?

Shelf-stable properties reduce shipping complexity, making reconstituted powders well-suited for rapid growth in online grocery sales.

What technology recently received FDA approval for non-thermal milk processing?

TruActive UV, approved in June 2025, permits pathogen control without high-heat treatment, preserving nutritional integrity.

Page last updated on: