United States Non-Dairy Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

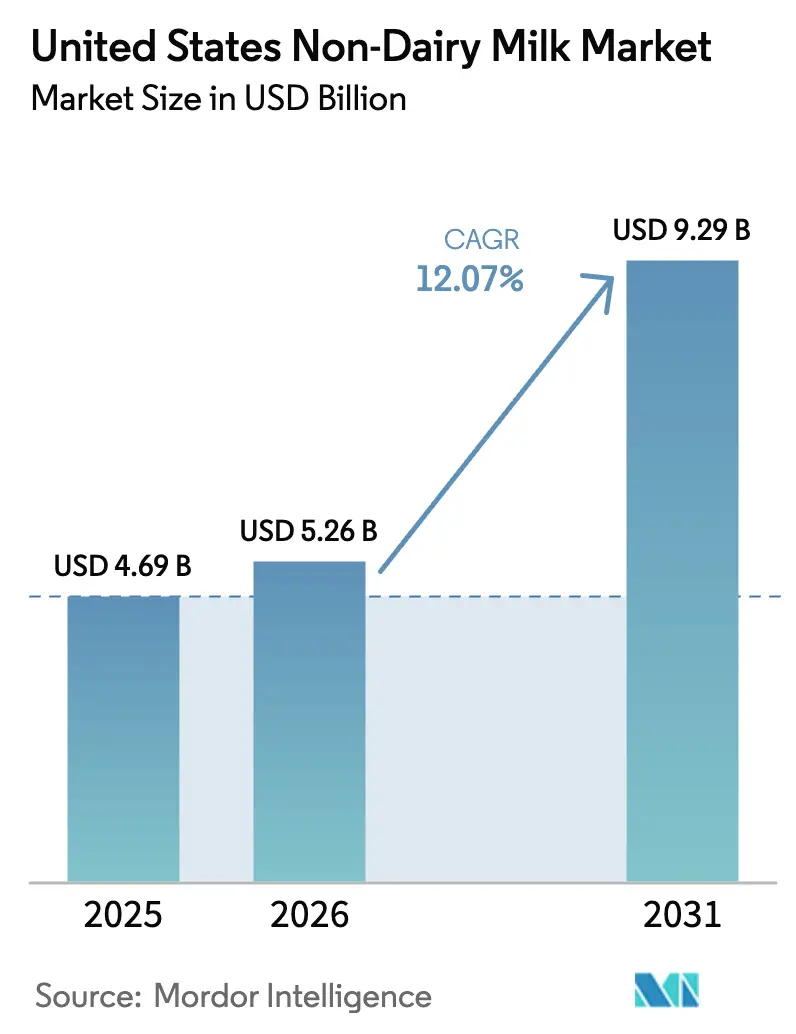

| Base Year Market Size (2025) | USD 4.69 Billion |

| Market Size (2026) | USD 5.26 Billion |

| Market Size (2031) | USD 9.29 Billion |

| Growth Rate (2026 - 2031) | 12.07% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Non-Dairy Milk Market Analysis by Mordor Intelligence

The United States non-dairy milk market size was valued at USD 4.69 billion in 2025 and estimated to grow from USD 5.26 billion in 2026 to reach USD 9.29 billion by 2031, at a CAGR of 12.07% during the forecast period (2026-2031). This growth is supported by regulatory clarity that allows plant-based beverages to be labeled as "milk," addressing consumer familiarity and trust. Additionally, the high prevalence of lactose intolerance, affecting 36% of the national population, and a growing focus on health and wellness among younger demographics are key drivers of demand. The market's expansion is further fueled by advancements in barista-grade formulations, which ensure seamless integration into foodservice coffee applications, meeting the expectations of both consumers and businesses. Innovations in protein fortification continue to enhance the nutritional profile of non-dairy milk, while the introduction of diverse flavors caters to the preferences of various ethnic groups, broadening the appeal of these products. On the supply side, improvements in aseptic processing technology have extended product shelf life, while environmentally friendly packaging solutions have reduced the ecological footprint of non-dairy milk products. These developments have strengthened retailer confidence, encouraging them to stock a wider range of offerings. Moreover, the market's oligopolistic structure minimizes aggressive pricing competition, allowing leading brands to allocate resources toward sustainability initiatives and targeted marketing campaigns. This strategic focus has enabled greater penetration of non-dairy milk products across mainstream grocery stores and on-trade channels, further solidifying their position in the market.

Key Report Takeaways

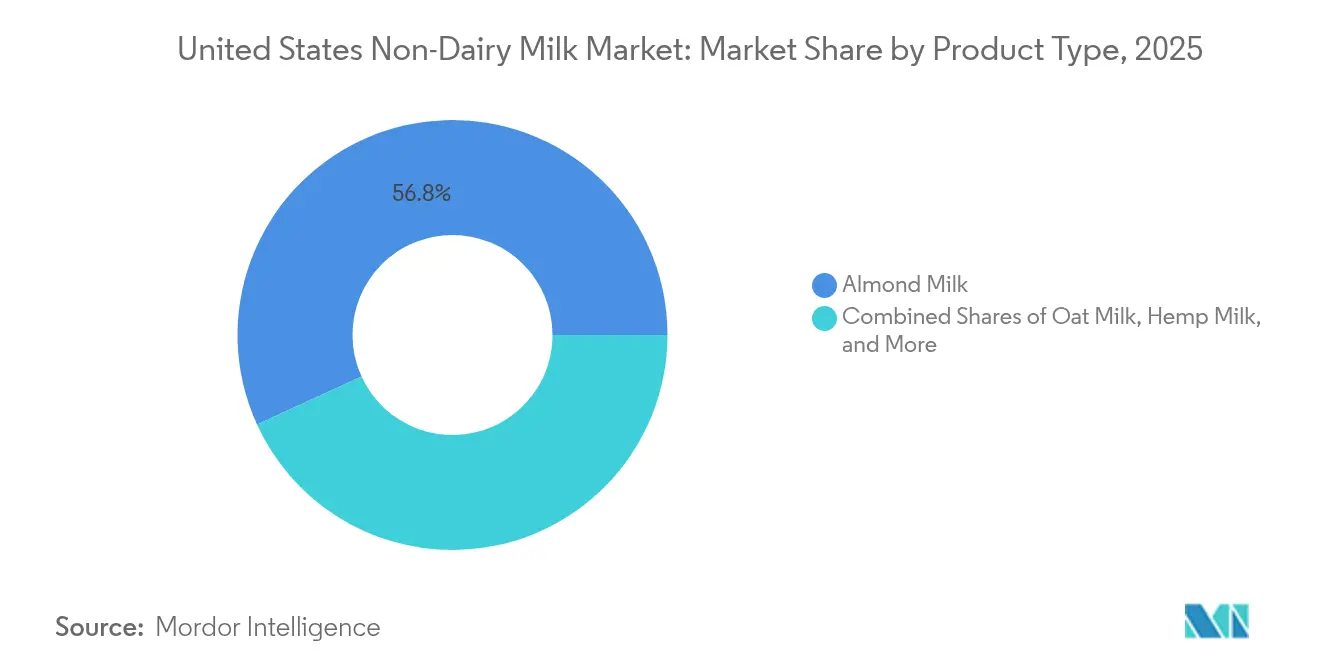

- By product type, almond milk led with 56.83% of the non-dairy milk market share in 2025, while hemp milk posted the fastest 13.33% CAGR through 2031.

- By flavor, un-flavored formulations accounted for 73.12% of the non-dairy milk market size in 2025; flavored variants are expanding at a 12.74% CAGR to 2031.

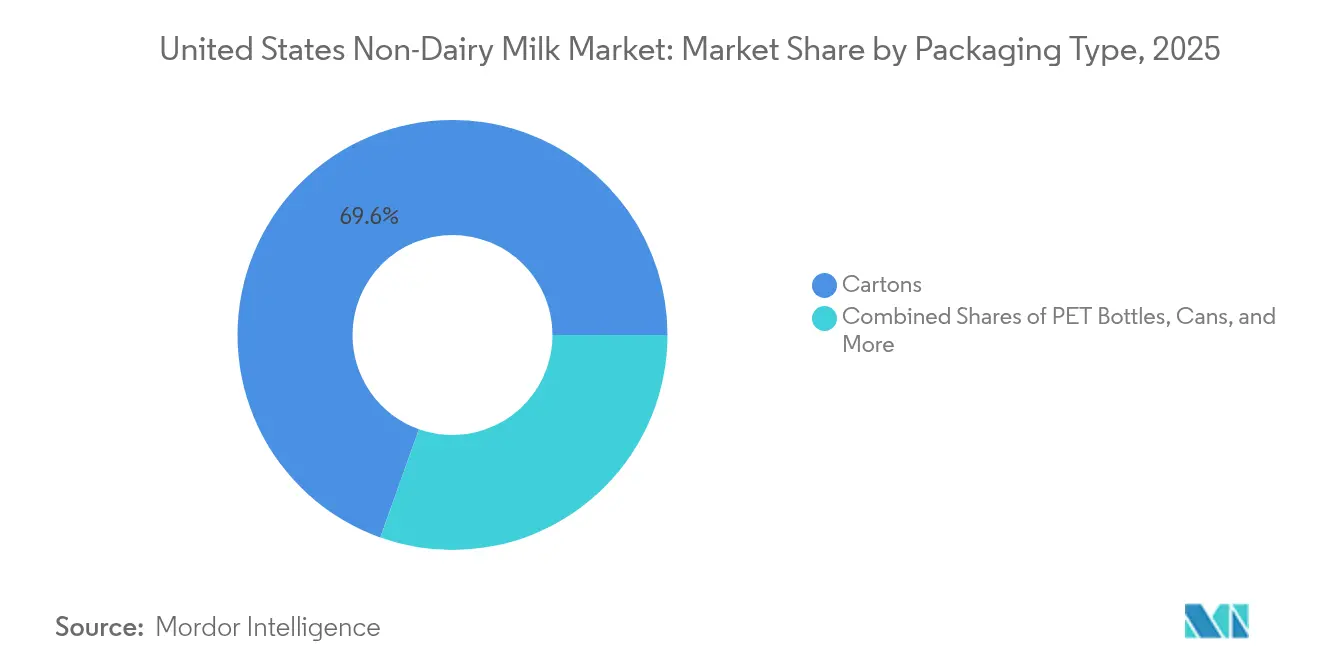

- By packaging type, cartons captured 69.55% revenue share in 2025, whereas cans exhibit the highest 12.55% CAGR for 2026-2031.

- By distribution channel, off-trade outlets held 67.54% share in 2025, and on-trade venues are advancing at a 12.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Non-Dairy Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising lactose intolerance among U.S. consumers increases demand for non-da | +2.8% | National, with higher concentrations in Northeast and West Coast | Medium term (2-4 years) |

| Greater awareness of milk allergies and dietary restrictions drives plant-b | +2.1% | National, with early gains in California, New York, Texas | Short term (≤ 2 years) |

| Growth in veganism and plant-based lifestyles influences consumer preferenc | +1.9% | Urban centers, particularly West Coast and Northeast metropolitan areas | Long term (≥ 4 years) |

| Concerns about animal welfare encourage shifts toward non-dairy alternative | +1.4% | National, with stronger influence in college towns and urban areas | Long term (≥ 4 years) |

| Expanding variety of flavors and formats | +1.7% | National, with premium segments in affluent suburban markets | Medium term (2-4 years) |

| Product launches catering to niche and ethnic dietary preferences | +1.3% | Diverse metropolitan areas, Hispanic and Asian American communities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Lactose Intolerance Drives Market Expansion

Lactose intolerance is a widespread condition among American adults, influenced significantly by genetic predisposition across various ethnic groups. This has led to a rising demand for plant-based alternatives, as consumers look for products that meet their dietary needs. For many, non-dairy milk transitions from being a lifestyle choice to a necessity as they age. Research highlights that symptoms of lactose malabsorption can develop or worsen over time, broadening the consumer base to include individuals without a formal diagnosis. This biological factor ensures a steady demand for non-dairy products, offering stability to the market even during economic challenges. Additionally, the FDA's acknowledgment of lactose intolerance as a genuine health concern has helped companies position their products more effectively while increasing consumer awareness and understanding. The prevalence of lactose intolerance is closely linked to family history and ethnic background. In the United States, around 15% of adult Caucasians and 85% of adult African Americans are affected. The condition is also highly common among individuals of Asian, Hispanic, Native American, and Jewish descent [1]Source: American College of Gastroenterology, "Lactose Intolerance Overview," gi.org.

Health Consciousness and Protein Fortification Trends

Consumer interest in protein consumption continues to grow, with 71% of Americans actively seeking to increase their protein intake, as highlighted by the International Food Information Council's 2024 Food & Health Survey [2]Source: International Food Information Council, “2024 Food & Health Survey,” ific.org. This rising demand is fueling advancements in plant-based milk formulations, particularly in hemp and pea protein variants, which are valued for their ability to provide complete amino acid profiles. In response, manufacturers are enhancing their offerings by fortifying these products with additional nutrients, aiming to create functional beverages that closely mirror the nutritional benefits of dairy milk. The emphasis on protein is no longer limited to fitness enthusiasts; it now resonates with a broader audience, including aging individuals focused on maintaining muscle health and parents prioritizing nutritious choices for their children. Regulatory frameworks under the oversight of the FDA play a critical role in ensuring that fortification claims are accurate and adhere to established nutritional standards.

Vegan Lifestyle Adoption Accelerates Category Growth

The adoption of plant-based lifestyles is gaining momentum among younger demographics, with Generation Z emerging as a key driver of consumption trends focused on environmental sustainability and ethical values. This generational shift is expected to support sustained market growth, as these consumers are likely to maintain their preferences as they enter higher-income earning stages. Social media platforms are playing a significant role in promoting plant-based messaging, enabling rapid and widespread adoption that traditional marketing methods cannot easily replicate. This trend extends beyond individual consumption, influencing household purchasing behaviors as younger family members increasingly advocate for non-dairy and plant-based alternatives. Additionally, corporate sustainability initiatives within the foodservice and retail industries are contributing to this growth by enhancing product accessibility and fostering normalized consumption habits. According to the Good Food Institute, 59% of U.S. households purchased plant-based foods in 2024, a figure consistent with the previous year [3]Source: Good Food Institute, "U.S. retail market insights for the plant-based industry," gfi.org.

Flavor Innovation Targets Ethnic and Niche Preferences

Product development is increasingly being tailored to meet the unique dietary preferences of specific cultural groups. For instance, coconut milk has seen growing acceptance among Hispanic communities, while rice milk resonates strongly with Asian American consumers. By focusing on these distinct preferences, brands are able to implement premium pricing strategies and cultivate strong customer loyalty within these demographic segments. Furthermore, innovation in the form of seasonal and limited-edition flavors not only creates a sense of urgency for purchases but also encourages consumers to try new products. This strategy reflects a deep understanding of market dynamics, moving beyond generic, one-size-fits-all formulations to deliver solutions that are more aligned with consumer needs. However, navigating regulatory compliance remains critical, as requirements vary depending on the ingredients and flavor profiles. Companies must carefully adhere to FDA guidelines for additive approvals and labeling to ensure compliance and maintain consumer trust.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher price point than dairy milk | -2.4% | National, with stronger impact in price-sensitive rural and suburban markets | Short term (≤ 2 years) |

| Taste and mouthfeel barriers | -1.8% | National, with higher resistance in traditional dairy-consuming regions | Medium term (2-4 years) |

| Limited shelf life for certain non-dairy milk formats | -1.2% | National, with greater impact in regions with limited cold chain infrastructure | Short term (≤ 2 years) |

| Consumer skepticism of food additives, stabilizers, gums, and emulsifiers | -1.5% | National, with stronger influence in health-conscious and organic-focused markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Premium Challenges Market Penetration

Non-dairy milk alternatives are often priced significantly higher than conventional dairy milk, creating affordability challenges for consumers who are sensitive to price and limiting the market's reach among lower-income groups. This higher pricing is primarily due to smaller production scales, specialized processing requirements, and ingredient costs that surpass those of traditional dairy products. Economic pressures, such as inflation and rising food costs, further amplify these affordability concerns, particularly for families with multiple children who consume substantial amounts of milk. Retailers frequently position plant-based alternatives in premium sections, which reinforces their image as luxury items rather than everyday staples. However, in certain segments like oat milk, the price difference has become less pronounced due to economies of scale, highlighting opportunities for cost reductions through increased production volumes and improved manufacturing processes.

Taste and Texture Acceptance Remains Inconsistent

Consumer acceptance varies significantly across product categories, with taste and mouthfeel continuing to be major challenges for widespread adoption. This is particularly evident in coffee applications, where the steaming properties of dairy milk remain unmatched, offering a creamier and more consistent experience. While ongoing formulation efforts aim to replicate the creamy texture and neutral flavor profile of dairy, many consumers still perceive aftertastes or a thinner consistency in alternatives, which can diminish their overall satisfaction. These challenges become even more pronounced in cooking and baking applications, where the functional properties of dairy alternatives often fall short, limiting their versatility and reducing the likelihood of repeat purchases. Generational preferences also play a role, as older consumers tend to be more resistant to variations in taste, whereas younger demographics are generally more open and adaptable to alternative flavor profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hemp Innovation Challenges Almond Dominance

Almond milk continues to lead the market with a commanding 56.83% share in 2025, reflecting its widespread acceptance and popularity among consumers. Meanwhile, hemp milk is emerging as the fastest-growing segment, with a projected CAGR of 13.33% through 2031. This growth highlights a notable shift in consumer preferences toward nutrient-dense alternatives. Hemp milk's appeal lies in its superior protein content and omega-3 fatty acid profile, which resonate with health-conscious individuals seeking functional benefits that go beyond simply replacing dairy products. This trend underscores the evolving priorities of consumers who are increasingly focused on health and wellness in their dietary choices.

Oat milk is also gaining significant traction, driven by strategic partnerships with coffee shops and the development of barista-grade formulations that cater to the growing demand for plant-based options in beverages. On the other hand, soy milk, despite its long-standing presence in the market, is witnessing a decline in interest. Coconut milk continues to serve niche applications, particularly in ethnic cuisines and baking, maintaining steady yet modest growth. Additionally, cashew and hazelnut milk variants occupy a premium position in the market, appealing to a smaller but loyal consumer base that values their unique taste and quality.

By Flavour: Premiumization Drives Flavoured Segment Acceleration

Unflavored varieties are anticipated to account for a significant 73.12% market share in 2025, underscoring their appeal as versatile options suitable for a wide range of applications. This preference highlights the practicality and adaptability of unflavored products, which cater to diverse consumer needs. At the same time, the flavored segment is gaining momentum, projected to grow at a robust CAGR of 12.74% through 2031. This growth is fueled by the rising demand for premium products, as consumers increasingly seek unique and enhanced taste experiences. Vanilla and chocolate continue to dominate as the most preferred flavored options, while seasonal and limited-edition varieties create a sense of urgency and encourage trial purchases.

The expansion of the flavored segment also reflects a shift in consumer behavior, particularly among younger demographics who view plant-based milk as more than just a dairy alternative, it is seen as a lifestyle choice. These consumers are willing to pay a premium for products that align with their taste preferences and lifestyle aspirations. Additionally, unsweetened flavored options are emerging as a popular choice among health-conscious individuals. These products offer a balance between flavor variety and health considerations, catering to those who want to avoid added sugars while still enjoying diverse taste profiles.

By Packaging Type: Sustainability Concerns Propel Can Innovation

Cartons are anticipated to dominate the packaging market in 2025, holding a significant 69.55% share. This dominance is attributed to their well-established supply chains and the familiarity they offer to consumers. Cartons have long been a preferred choice due to their practicality and widespread availability, making them a staple in the packaging industry. On the other hand, cans are emerging as the fastest-growing packaging format, with a projected CAGR of 12.55% through 2031. This growth is largely driven by increasing sustainability efforts and the rising popularity of on-the-go consumption. The recyclability of cans and their reduced environmental footprint compared to multi-layer cartons make them an attractive option for environmentally conscious consumers who are willing to invest in sustainable alternatives.

While PET bottles continue to play a role in convenience channels, their growth potential is constrained by mounting environmental concerns. These bottles face criticism for their contribution to plastic waste, which has led to a shift in consumer preferences toward more eco-friendly packaging solutions. The evolving landscape of packaging reflects a broader awareness among consumers about the environmental impact of packaging materials, extending beyond the product itself. This shift underscores the growing importance of sustainability in influencing purchasing decisions and shaping the future of the packaging industry.

By Distribution Channel: Foodservice Integration Accelerates On-Trade Growth

Off-trade channels are anticipated to maintain a dominant 67.54% market share in 2025. This is largely attributed to their well-established retail networks and the ingrained shopping habits of consumers. These channels continue to serve as a reliable avenue for distributing plant-based products, ensuring accessibility and convenience for customers. Meanwhile, the on-trade segment is emerging as a significant growth area, with a projected CAGR of 12.96% through 2031. This growth is being fueled by the increasing adoption of plant-based alternatives in coffee shops and their integration into foodservice operations.

The expansion of SunOpta's Dream Oatmilk Barista to 6,700 locations underscores the strategic importance of the on-trade channel for brand visibility and consumer engagement. Coffee shops, in particular, provide an opportunity for consumers to trial plant-based products in familiar settings, such as lattes or other beverages, which often encourages subsequent retail purchases for home use. In the foodservice sector, the adoption of plant-based alternatives requires tailored formulations that can consistently perform under the demands of commercial equipment and high-volume operations, ensuring quality and reliability for end-users.

Geography Analysis

The non-dairy milk market in the United States shows clear regional differences shaped by demographics, cultural preferences, and economic factors. California leads the way, driven by a health-conscious population, environmental awareness, and diverse ethnic communities with a history of consuming plant-based alternatives. The Northeast follows closely, supported by urban populations and higher disposable incomes that make premium-priced products more accessible. Meanwhile, Texas is experiencing rapid growth, thanks to its expanding Hispanic population, which favors coconut and rice-based options, creating opportunities for culturally tailored products. In contrast, the Southeast is adopting non-dairy milk at a slower pace but holds significant growth potential as awareness grows and distribution extends beyond urban areas.

Supply chain dynamics also play a key role in shaping the market. California’s almond production provides cost advantages for almond milk but raises concerns about water usage, especially during droughts. The Midwest benefits from its strong agricultural base, which supports oat production and offers potential cost efficiencies for oat milk manufacturing and distribution. While regulatory compliance is consistent nationwide under FDA guidelines, local health departments may impose additional requirements for foodservice applications. Climate factors also influence ingredient sourcing and transportation costs, with regional production facilities emerging to better serve local markets and improve efficiency.

Urban and rural consumption patterns highlight further differences. Urban areas consume 2-3 times more non-dairy milk than rural regions, where dairy farming traditions and price sensitivity remain barriers to adoption. College towns stand out as high-demand areas, driven by younger demographics with a preference for plant-based options. These geographic insights emphasize the need for targeted strategies that address regional preferences, economic conditions, and cultural factors, rather than relying on a one-size-fits-all national approach to market expansion.

Competitive Landscape

The United States non-dairy milk market is dominated by a few key players, showcasing an oligopolistic structure where established companies use their scale, distribution networks, and brand strength to maintain a competitive edge. Leading brands adopt unique strategies to stand out—Oatly highlights sustainability and barista-grade products, while Danone's Silk brand focuses on nutritional benefits and widespread availability through strong retail partnerships. Blue Diamond Growers leverages its vertically integrated almond processing operations to achieve cost efficiencies and maintain quality standards that smaller competitors struggle to match. The market is also seeing a shift toward clean-label products, sustainable packaging, and functional nutrition, which help brands command premium pricing and build consumer trust.

There are significant growth opportunities in areas like ethnic-specific formulations, protein-enriched options, and niche applications such as infant nutrition. While regulatory barriers in these segments can be challenging, they also offer substantial rewards for companies that successfully navigate them. Innovation in processing technologies is another area of focus, with companies working to improve taste, extend shelf life, and lower production costs. Investments in proprietary formulations and advanced manufacturing techniques are helping businesses create strong competitive advantages in this evolving market.

The FDA's changing regulatory landscape is shaping the market dynamics, presenting both opportunities and challenges. Clearer labeling guidelines are expected to support market growth by improving transparency for consumers. At the same time, stricter nutritional standards require companies to invest in reformulating products and ensuring compliance. These demands tend to favor larger players with the resources to manage regulatory complexities, giving them an edge in maintaining market leadership.

United States Non-Dairy Milk Industry Leaders

-

Blue Diamond Growers

-

Danone SA

-

Califia Farms LLC

-

Oatly Group AB

-

Ripple Foods PBC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Califia Farms acquired Uproot Inc., a sustainable packaging technology company, for an undisclosed amount to advance environmental initiatives and reduce packaging waste across its product portfolio. This acquisition demonstrates the industry's commitment to sustainability beyond product ingredients and positions Califia for competitive advantage in environmentally conscious market segments.

- June 2024: SunOpta announced a USD 26 million expansion of its Modesto, California facility and secured distribution agreements covering 6,700 retail locations for Dream Oatmilk Barista products. The expansion increases production capacity by 40% and strengthens SunOpta's position in the rapidly growing foodservice segment.

- March 2024: MALK Organics expanded distribution from natural specialty channels to conventional grocery stores, securing shelf space in over 2,000 locations including Kroger and Whole Foods Market. The expansion represents a strategic shift toward mainstream market penetration for the premium organic brand.

United States Non-Dairy Milk Market Report Scope

Almond Milk, Cashew Milk, Coconut Milk, Hemp Milk, Oat Milk, Soy Milk are covered as segments by Product Type. Off-Trade, On-Trade are covered as segments by Distribution Channel.| Oat Milk |

| Hemp Milk |

| Hazelnut Milk |

| Soy Milk |

| Almond Milk |

| Coconut Milk |

| Cashew Milk |

| Flavoured |

| Un-flavoured |

| PET Bottles |

| Cans |

| Cartons |

| Others |

| On-Trade | |

| Off-Trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others |

| By Product Type | Oat Milk | |

| Hemp Milk | ||

| Hazelnut Milk | ||

| Soy Milk | ||

| Almond Milk | ||

| Coconut Milk | ||

| Cashew Milk | ||

| By Flavour | Flavoured | |

| Un-flavoured | ||

| By Packaging Type | PET Bottles | |

| Cans | ||

| Cartons | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Convenience Stores | |

| Specialist Retailers | ||

| Supermarkets and Hypermarkets | ||

| On-line Retail | ||

| Others | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms