Concentrated Milk Fat Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.65 Billion |

| Market Size (2031) | USD 7.65 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

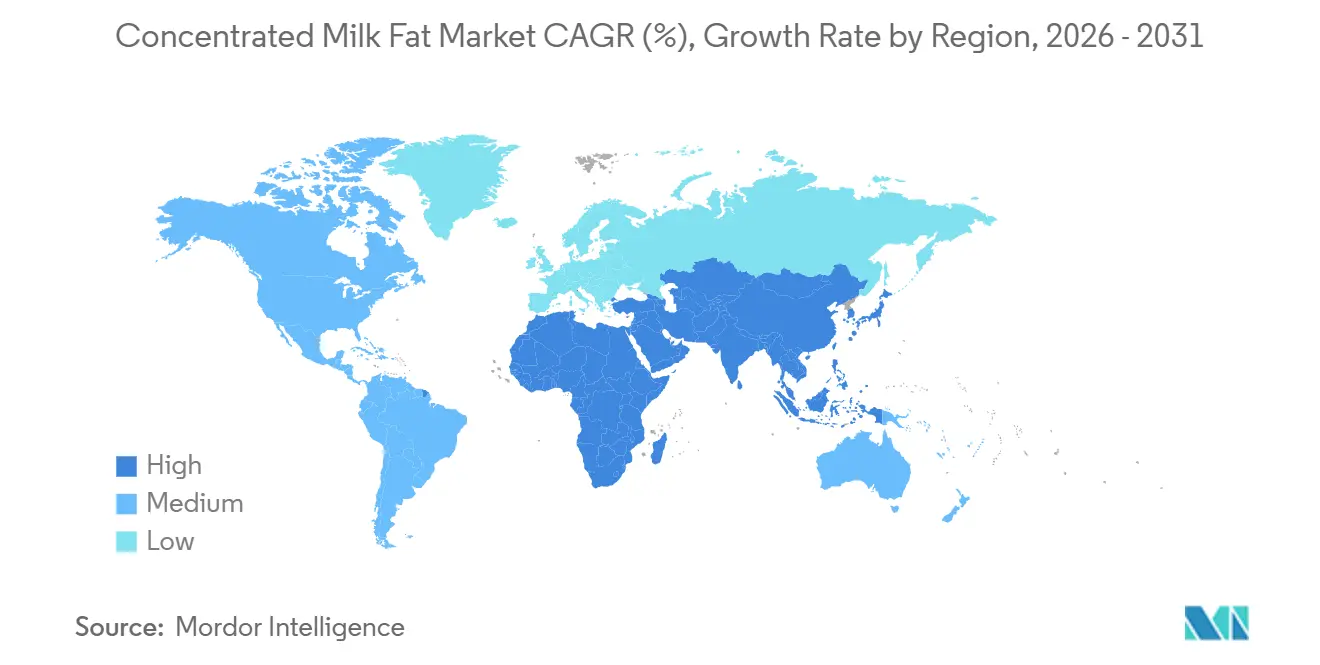

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

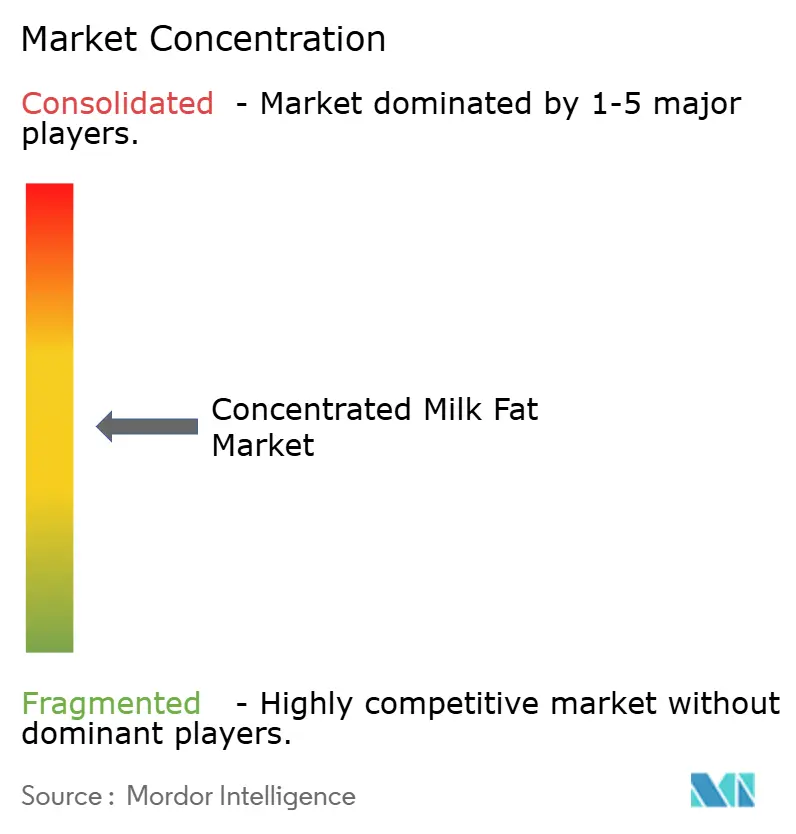

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Concentrated Milk Fat Market Analysis by Mordor Intelligence

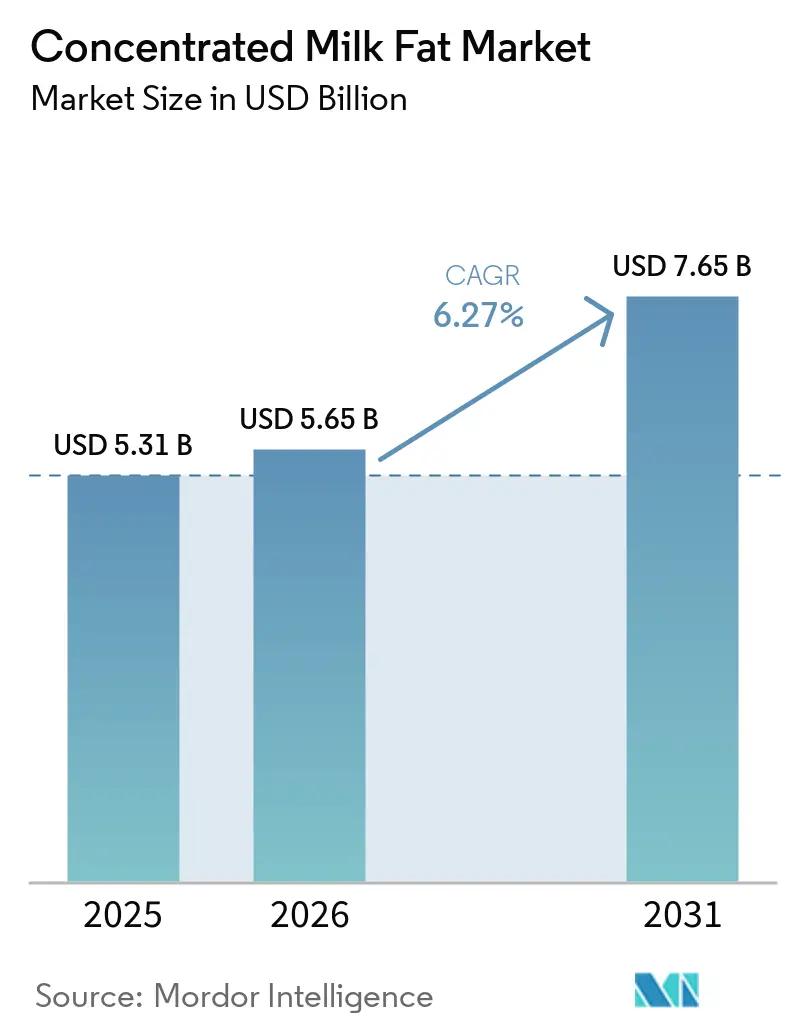

The concentrated milk fat market size was valued at USD 5.31 billion in 2025 and estimated to grow from USD 5.65 billion in 2026 to reach USD 7.65 billion by 2031, at a CAGR of 6.27% during the forecast period (2026-2031). Demand is shifting toward high-margin fat fractions as processors redirect cream away from powders, encouraged by 51.5% butter price inflation in 2024, which signaled a sustained supply squeeze. Conventional products dominated in 2025, yet organic variants are expanding as infant-formula and premium bakery buyers pursue clean-label claims. Anhydrous milk fat remains the workhorse for industrial baking, while butter oil is gaining ground in chocolate applications because it meets stricter cocoa butter-equivalent rules. Asia-Pacific leads consumption, followed by fast-growing Middle East and Africa, which is closing its dairy supply gap through imports.

Key Report Takeaways

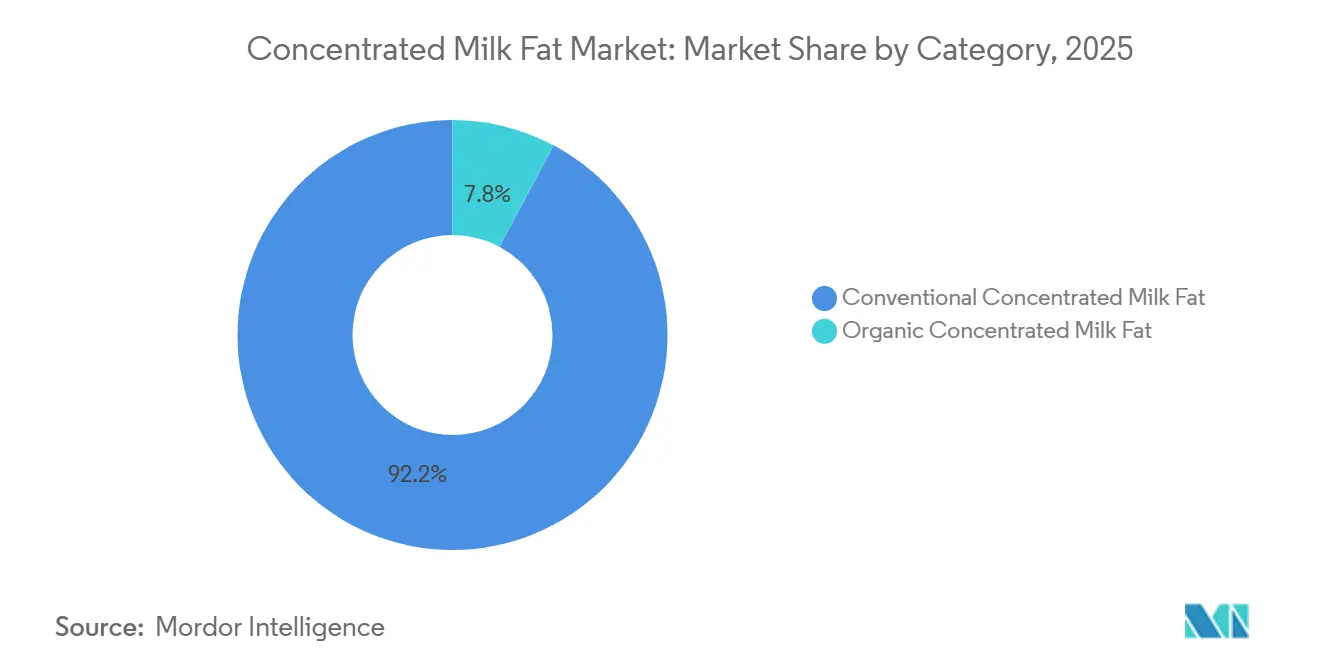

- By category, conventional products held 92.25% of the concentrated milk fat market share in 2025, while organic variants will expand at a CAGR of 9.46% through 2031.

- By product type, anhydrous milk fat captured 67.21% of 2025 revenue, whereas butteroil will post a CAGR of 7.94% between 2026 and 2031.

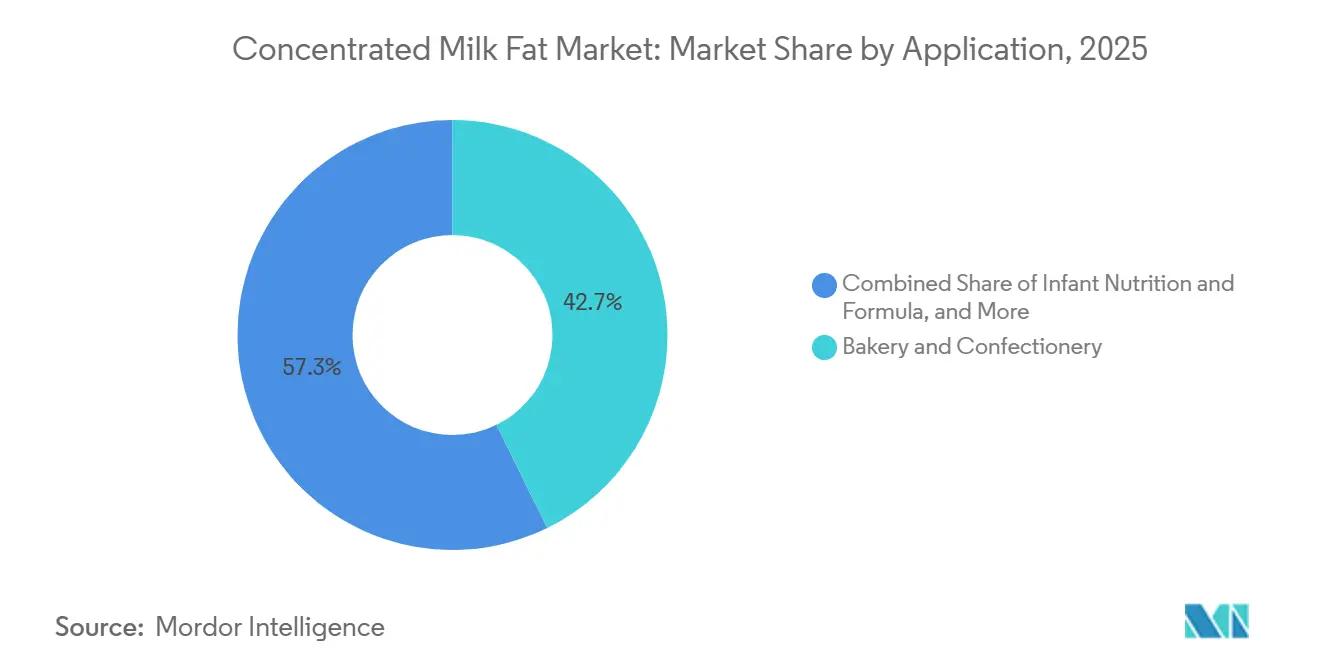

- By application, bakery and confectionery led with 42.74% of 2025 volume, yet infant nutrition will grow at a CAGR of 7.73% through 2031.

- By geography, Asia-Pacific accounted for 37.14% of demand in 2025, while the Middle East and Africa will advance at a CAGR of 8.37% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Concentrated Milk Fat Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Use of AMF in High-temperature Industrial Processing | +1.2% | Europe, North America, Asia-Pacific industrial hubs | Medium term (2-4 years) |

| Expansion of Recombined Dairy Products in Emerging Markets | +1.1% | Asia-Pacific, Middle East & Africa, South America | Long term (≥4 years) |

| Technological Advancements in Milk Fat Fractionation | +0.9% | Europe, Oceania, spill-over worldwide | Medium term (2-4 years) |

| Increased Utilization in Nutraceutical and Functional Dairy Blends | +0.8% | North America, Europe, Japan, Australia | Long term (≥4 years) |

| Demand for Flavor-carrier Fats in Premium Ready-to-eat Meals | +0.6% | North America, Western Europe, urban Asia-Pacific | Short term (≤2 years) |

| Increasing Adoption in Chocolate Fat Standardization | +0.7% | Europe, North America, premium Asia-Pacific confectionery | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising use of AMF in high-temperature industrial processing

Anhydrous milk fat's thermal stability above 180°C makes it indispensable in confectionery, biscuit baking, and spray-dried flavor systems where vegetable fats degrade or impart off-notes. Processors are substituting palm and coconut fractions with AMF to meet clean-label demands and avoid allergen cross-contact risks in shared production lines. The shift is particularly pronounced in Europe, where cocoa butter equivalent regulations under Directive 2000/36/EC permit only specified vegetable fats in chocolate, pushing premium manufacturers toward AMF blends that deliver mouthfeel without regulatory ambiguity. Industrial bakeries in North America increased AMF usage by an estimated 8-12% during 2024-2025 to reformulate laminated doughs and cream fillings as consumers reject hydrogenated oils. This application segment benefits from AMF's consistent, solid-fat-content profile across temperature ranges, which simplifies process control and reduces batch variability in high-throughput production environments.

Expansion of recombined dairy products in emerging markets

Recombined milk, cream, and yogurt formulations enable processors in milk-deficit regions to manufacture dairy products from imported skim milk powder, whey, and concentrated milk fat, bypassing the need for cold-chain fresh milk. Indonesia's Fortified Nutritious Meal program expanded the use of recombined dairy in school feeding, while the Philippines and Vietnam are scaling up recombined UHT milk to serve growing urban populations where farm-to-factory logistics remain fragmented, according to the United States Department of Agriculture, Foreign Agricultural Service. Saudi Arabia and the UAE imported approximately 162,000 metric tons of butter and milkfat products in 2026, much of which is recombined into cultured dairy and dessert applications to serve expatriate and local demand, as mentioned by the United States Department of Agriculture, Foreign Agricultural Service. This strategy decouples dairy manufacturing from domestic herd volatility and enables year-round production, though it exposes processors to global commodity price swings and freight cost fluctuations. The model is gaining traction in sub-Saharan Africa, where cold-chain infrastructure gaps make it uneconomical to collect fresh milk beyond peri-urban areas.

Technological advancements in milk fat fractionation

Supercritical carbon dioxide extraction and membrane filtration technologies enable processors to isolate short-chain and medium-chain fatty acid fractions from milkfat, creating tailored lipid profiles for infant formula, sports nutrition, and pharmaceutical excipients. Patents filed in 2024-2025 by European and Oceania ingredient firms describe ultrafiltration cascades that enrich milk fat globule membrane phospholipids and sphingomyelin to concentrations exceeding 15% by weight, targeting cognitive health and gut microbiome applications. These fractionation advances allow dairies to capture premiums 2-3 times higher than those for commodity anhydrous milk fat by positioning their outputs as functional ingredients rather than commodity fats. New Zealand processors are investing in selective crystallization units that separate high-melting triglycerides for chocolate and confectionery, while diverting low-melting fractions to spreadable butter and dairy blends. The technology reduces waste, as even minor fractions find outlets in personal care emulsions and pharmaceutical lipid matrices, improving overall milk utilization economics.

Increased utilization in nutraceutical and functional dairy blends

Milk fat globule membrane components, particularly phospholipids, gangliosides, and cholesterol, are being incorporated into infant formula, senior nutrition, and cognitive health supplements following clinical evidence of benefits in neural development and gut barrier function. FDA's Generally Recognized as Safe determinations for bovine milk fat globule membrane ingredients in 2024 accelerated their adoption in U.S. infant formula, while EFSA's positive opinion on phospholipid safety in 2025 opened European markets. Processors are blending concentrated milk fat with DHA, lutein, and prebiotic oligosaccharides to create turnkey functional dairy bases for ready-to-drink beverages and fortified yogurts. Japan's aging population is driving demand for milk fat-based cognitive health products, with domestic launches of MFGM-enriched dairy drinks rising sharply in 2025. This application commands margins 40-60% above commodity milkfat, incentivizing investment in fractionation and membrane separation capacity, yet it requires rigorous quality control and traceability to meet pharmaceutical-grade specifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Fluctuating Raw Milk Supply Chains | –0.8% | Oceania, Argentina, drought-prone regions | Short term (≤2 years) |

| Capital-intensive Processing Infrastructure Requirements | –0.6% | Emerging Asia-Pacific, Middle East & Africa, South America | Long term (≥4 years) |

| Regulatory Variability in Dairy Fat Standards Across Countries | –0.5% | Cross-border trade worldwide | Medium term (2-4 years) |

| Limited Cold-chain Infrastructure in Developing Markets | –0.4% | Sub-Saharan Africa, South Asia, Southeast Asia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Dependence on fluctuating raw milk supply chains

Raw milk availability and pricing exhibit pronounced seasonality and weather sensitivity, directly impacting concentrated milk fat output and margins. Argentina's milk production contracted 7% in 2024 due to heat, drought, and corn leafhopper damage in the Santa Fe and Córdoba basins, reducing whole milk powder and butter processing volumes by 10-15%[1]Source: Andrea Yankelevich, “Dairy and Products Annual: Argentina,” USDA Foreign Agricultural Service, USDA.GOV . New Zealand's milk output declined 0.5% in 2026, constraining butter and anhydrous milk fat exports despite strong demand from China and Southeast Asia, according to the USDA. Feed cost volatility compounds the risk, as milk-to-concentrate ratios in Argentina peaked in late 2024 but softened by mid-2025 when peso devaluations lagged grain price adjustments, squeezing dairy farmer margins and triggering herd liquidations. Processors with limited forward-contract coverage face abrupt input cost spikes that cannot be immediately passed through to customers, eroding profitability and discouraging long-term capacity commitments. La Niña weather patterns threaten 2026-2027 rainfall in the Pampas and southern Brazil, adding downside risk to South American milk supplies that underpin regional concentrated milk fat exports.

Capital-intensive processing infrastructure requirements

Establishing anhydrous milk fat and butteroil production lines demands investments of USD 50-150 million for mid-scale facilities, encompassing cream separation, pasteurization, vacuum evaporation, and packaging systems that meet food safety and traceability standards. Upstate Niagara Cooperative committed USD 150 million to a new processing plant in New York, while a Nebraska dairy consortium invested USD 165 million in expanded butter and powder capacity. Smaller cooperatives and regional processors in Asia-Pacific and Africa struggle to mobilize capital at this scale, perpetuating reliance on imports and limiting their ability to capture value from domestic milk production. Brazil's Lactalis subsidiary invested BRL 400 million (USD 75 million) across five facilities in Rio Grande do Sul to expand butter, whey protein, and dairy blend capacity, targeting 453,000 metric tons of annual dairy output by 2028. High capital intensity also deters entry by non-dairy food companies, sustaining moderate concentration among established dairy cooperatives and multinational ingredient suppliers. Financing constraints are acute in sub-Saharan Africa and South Asia, where credit costs and currency risks elevate the effective cost of imported processing equipment and delay capacity additions that could localize concentrated milk fat production.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Variants Gain Despite Conventional Dominance

Conventional concentrated milk fat held 92.25% of the market share in 2025, reflecting the cost sensitivity of industrial bakery, confectionery, and recombined dairy applications where organic premiums cannot be justified. Organic concentrated milk fat is forecast to expand at 9.46% CAGR through 2031, driven by infant formula brands seeking USDA Organic and EU Organic certifications to differentiate in competitive markets. Organic dairy herds in the United States grew modestly in 2025, yet supply remains constrained by the 3-year pasture transition requirement and limited organic grain availability, keeping organic milkfat prices 40-60% above conventional equivalents. European processors are channeling organic milk into butter and cream rather than powders, as retail demand for organic spreadable fats surged 12% year-over-year in 2025[2]Source: European Milk Volumes Continue to Pressurize Markets," Agriculture and Horticulture Development Board, ahdb.org.uk. The organic segment benefits from consumer willingness to pay premiums for clean-label, non-GMO, and animal-welfare-certified ingredients, yet scalability is limited by land availability and the slow pace of herd conversion.

Conventional volumes will continue to dominate through 2031, particularly in price-sensitive emerging markets where organic certification infrastructure is underdeveloped, and consumer awareness remains low. Processors are exploring hybrid models that blend organic and conventional milkfat in applications where partial organic content suffices for marketing claims, though regulatory ambiguity around such blends varies by jurisdiction. USDA's National Organic Program and EU Regulation 2018/848 prohibit labeling blended products as organic, constraining this strategy to non-certified premium tiers. Conventional concentrated milk fat also benefits from economies of scale in procurement, processing, and logistics that organic suppliers cannot yet replicate, sustaining a structural cost advantage that will persist through the forecast period.

By Product Type: AMF Leads but Butteroil Gains in Confectionery

Anhydrous milk fat accounted for 67.21% of product-type share in 2025, favored for its extended shelf life, low moisture content, and suitability for high-temperature industrial processes. Butteroil is projected to grow at 7.94% CAGR through 2031, capturing share in chocolate fat standardization and premium confectionery where its richer flavor profile and slightly higher moisture content enhance mouthfeel. Chocolate manufacturers in Europe and North America are reformulating to comply with cocoa butter equivalent regulations, substituting vegetable fats with butteroil to maintain clean-label positioning and avoid allergen cross-contact risks. Other concentrated milk fats, including cream concentrates and specialty fractions, serve niche applications in personal care, pharmaceuticals, and artisan food production, yet lack the scale and standardization to challenge AMF and butteroil dominance.

AMF's market leadership reflects its versatility across bakery lamination, spray-dried flavors, and recombined dairy formulations, where precise solid-fat-content profiles are critical for process consistency. New Zealand and EU processors export AMF in bulk tankers and intermediate bulk containers, optimizing freight economics for long-haul shipments to Asia-Pacific and Middle East markets. Butteroil's growth is concentrated in premium segments where flavor differentiation justifies higher costs, including artisan chocolate, high-end biscuits, and specialty ice cream. Fonterra's NZD 75 million (USD 45 million) Clandeboye butter expansion will increase both AMF and butteroil output, positioning the cooperative to serve divergent customer needs with a single capital investment, according to the Twinberrow, Annabel. The product-type split is also influenced by regional preferences, as Middle East markets favor butteroil for traditional sweets, while Asia-Pacific industrial users prioritize AMF for cost and shelf stability.

By Application: Infant Nutrition Outpaces Bakery Growth

Bakery and confectionery applications commanded 42.74% of end-use volume in 2025, driven by laminated dough production, cream fillings, and chocolate coatings, where concentrated milk fat delivers superior texture and flavor release. Infant nutrition and formula are forecast to grow at a 7.73% CAGR through 2031, the fastest growth rate, as formulators increase milkfat inclusion to mimic human milk lipid composition and comply with FDA, EFSA, and national nutrient specifications. FDA's updated infant formula guidance in 2024 and EFSA's 2025 opinion on the safety of milk fat globule membrane accelerated the adoption of concentrated milk fat in premium and specialty formulas with cognitive development and gut health claims[3]Source: EFSA Panel on Dietetic Products, Nutrition, and Allergies," European Food Safety Authority (EFSA), efsa.europa.eu. Dairy products applications, including recombined milk, yogurt, and cheese analogs, absorb significant volumes in emerging markets where fresh milk supply is unreliable, while nutraceuticals and functional foods represent a high-margin niche growing at double-digit rates as clinical evidence for MFGM benefits accumulates.

Personal care and cosmetics applications remain small but are expanding as clean-beauty brands incorporate milkfat-derived emollients and lipids into moisturizers, balms, and hair care products, leveraging consumer preference for recognizable, food-grade ingredients. Other applications, including pharmaceutical excipients and industrial lubricants, are stable but lack growth catalysts. The application mix is shifting toward higher-value, specification-driven segments where concentrated milk fat's functional properties command premiums over commodity vegetable fats. Bakery growth is moderating in mature markets as health-conscious consumers reduce pastry consumption, yet demand remains robust in Asia-Pacific and Middle East where Westernized bakery formats are gaining share. Infant formula's regulatory complexity creates barriers to entry that favor established ingredient suppliers with traceability systems and quality certifications, sustaining pricing power and margin stability in this application.

Geography Analysis

Asia-Pacific held 37.14% of global market share in 2025, propelled by China's 41.51 million metric tons of milk production and strategic pivot toward butter-plus-skim formulations in infant formula, which reduces whole milk powder imports while increasing demand for concentrated milk fat, according to the United States Department of Agriculture, Foreign Agricultural Service. India's butter production surged in 2025, supported by rising milk output and government initiatives to expand dairy processing infrastructure, yet cold-chain gaps in rural areas constrain the pace at which domestic concentrated milk fat can substitute imports from New Zealand and Europe. Indonesia's Fortified Nutritious Meal program scaled up recombined dairy use, driving imports of anhydrous milk fat and butter oil to blend with skim milk powder for school feeding and retail UHT milk. Japan and South Korea are importing premium organic and MFGM-enriched concentrated milk fat for cognitive health beverages and senior nutrition products, reflecting aging demographics and willingness to pay for functional ingredients. Southeast Asian markets, particularly Vietnam, Thailand, and the Philippines, are expanding recombinant dairy manufacturing to serve urban populations, yet reliance on imported ingredients exposes processors to volatility in freight costs and global commodity price swings.

Middle East and Africa is accelerating at 8.37% CAGR through 2031, the fastest regional pace, driven by population growth, rising per-capita incomes, and expanding infant formula consumption. Saudi Arabia and UAE collectively imported over 160,000 metric tons of butter and milkfat products in 2026, much of which is recombined into yogurt, desserts, and traditional sweets, according to the United States Department of Agriculture, Foreign Agricultural Service. Egypt's dairy sector is modernizing with investments in processing capacity, yet domestic milk production lags demand, sustaining import dependence on concentrated milk fat from Europe and Oceania. Sub-Saharan Africa faces acute cold-chain infrastructure gaps that limit fresh milk collection and processing, making recombined dairy formulations the most viable path to scale consumption, yet high import duties and freight costs elevate ingredient prices and constrain market penetration. South Africa's domestic dairy industry supplies regional markets with butter and cream, yet export volumes remain modest compared to Oceania and European suppliers. The region's growth trajectory depends on infrastructure investment, trade policy stability, and the pace at which domestic processing capacity can localize concentrated milk fat production.

Europe and North America together accounted for significant share of global demand in 2025, yet growth is moderating as mature consumption patterns and health trends shift preferences toward lower-fat dairy and plant-based alternatives. The EU reduced butter exports by 15% in 2026 to prioritize domestic cheese production, where margins remain more attractive than commodity fats, tightening concentrated milk fat availability for export markets, as analyzed by United States Department of Agriculture, Foreign Agricultural Service. U.S. milk production rose 1.2% in 2026, with processors channeling incremental volumes into cheese, dried whey, and lactose rather than butter, as new cheese plants in Wisconsin, Kansas, and Texas came online. North American industrial bakeries and confectioners are the largest regional consumers of anhydrous milk fat, yet demand growth is constrained by declining per-capita pastry consumption and reformulation toward lower-fat recipes. Europe's organic concentrated milk fat segment is expanding rapidly, driven by retail demand for certified butter and premium bakery fats, yet supply remains constrained by slow herd conversion rates and limited organic grain availability. South America's milk production rebounded in 2025 after drought-induced contractions in Argentina and Uruguay, with Argentina increased exports of whole milk powder, butter, and butteroil to Brazil, Algeria, and Middle East markets. Brazil's domestic concentrated milk fat production is rising, supported by Lactalis' BRL 400 million (USD 75 million) investment in butter and dairy blend capacity, yet imports of whole milk powder and nonfat dry milk remain substantial, reflecting persistent supply-demand imbalances. The EU-Mercosur trade agreement, signed in January 2026, introduces gradual duty-free quotas for European powdered milk and infant formula into Brazil, intensifying competitive pressure on domestic processors and potentially reshaping regional ingredient trade flows.

Competitive Landscape

The concentrated milk fat market exhibits moderate concentration, reflecting semi-consolidated leadership among Fonterra, FrieslandCampina, Lactalis, Dairy Farmers of America, and Arla Foods, yet regional fragmentation persists as local cooperatives in South America, Southeast Asia, and Eastern Europe capture flush-season milk volumes that multinational players cannot economically process. Fonterra's NZD 75 million (USD 45 million) Clandeboye butter expansion and USD 150 million UHT cream plant at Edendale position the cooperative to serve divergent customer needs, bulk anhydrous milk fat for industrial users and premium butteroil for confectionery, while its NZD 4.22 billion (USD 2.47 billion) asset sale to Lactalis in 2025 reshuffles Oceania market shares, according to the Agriculture and Horticulture Development Board. FrieslandCampina's acquisition of Milcobel and Wisconsin Whey Protein assets in 2024-2025 signals a strategic pivot toward higher-margin ingredients, including fractionated milk fats and functional dairy blends, as the cooperative exits commodity powder exposure.

Moreover, Arla Foods' USD 46.3 million Danish retrofit and EUR 300 million Swedish cheese-dairy investment through 2030 reflect a dual strategy of expanding concentrated milk-fat capacity while prioritizing cheese to capture superior margins. Saputo's CA 180 million (USD 133 million) Ripon facility upgrade and USD 59 million Caledonia investment underscore North American capacity rationalization, as the company consolidates production into fewer, higher-efficiency plants to improve cost competitiveness against European and Oceania exporters. White-space opportunities are emerging in nutraceutical blends, where milk fat globule membrane and polar lipids command premiums 2-3 times higher than commodity anhydrous milk fat, and in personal care formulations that leverage milkfat's clean-label appeal and emollient properties. Smaller regional processors, particularly in Argentina, Uruguay, and Eastern Europe, are capturing niche export opportunities by offering flexible contract terms and shorter lead times than multinational suppliers, yet they lack the traceability systems and quality certifications required for infant formula and pharmaceutical applications.

Technology adoption is uneven, with leading cooperatives investing in supercritical CO2 extraction and membrane filtration to isolate high-value fractions, while mid-tier processors rely on conventional cream separation and vacuum evaporation that yield commodity-grade outputs. Codex Alimentarius standards for milkfat composition and labeling provide a baseline for international trade, yet national variations, particularly in infant formula specifications and organic certification, create compliance complexity that favors incumbents with regulatory expertise and multi-market presence. Emerging disruptors include plant-based fat specialists exploring precision fermentation to replicate milkfat triglyceride profiles, though commercial-scale production remains years away and cost parity with dairy-derived fats is uncertain.

Concentrated Milk Fat Industry Leaders

-

Fonterra Co-operative Group

-

FrieslandCampina

-

Lactalis Ingredients

-

Dairy Farmers of America

-

Arla Foods Ingredients

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Arla Foods commenced a USD 46.3 million retrofit of its Danish dairy facility to expand anhydrous milk fat production capacity by 20%, with completion targeted for Q4 2027. The investment includes installing advanced cream-separation and vacuum-evaporation systems to improve consistency in solid-fat content and reduce energy consumption per kilogram of output.

- June 2025: Darigold commissioned its USD 1 billion Pasco, Washington, facility, adding 8 million lb/day processing capability and incorporating low-emission technologies aligned with the U.S. Dairy Net-Zero target.

- April 2025: Arla Foods and DMK Group merged to form Europe’s largest dairy cooperative with EUR 19 billion in revenue, aiming to combine research and development pipelines and expand premium ingredient portfolios.

- April 2025: Chobani unveiled plans for a USD 1.2 billion New York plant to support its growing protein-snack and yogurt lines, thereby boosting regional demand for concentrated milk fat.

Global Concentrated Milk Fat Market Report Scope

Concentrated milk fat refers to milk fat products with reduced moisture and non-fat solids, offering enhanced shelf life and rich dairy functionality. The concentrated milk fat market is segmented by category, product type, application, and geography. By category, the market includes conventional and organic concentrated milk fat. By product type, the market covers anhydrous milk fat (AMF), butteroil, and other concentrated milk fats. Based on application, the market is segmented into bakery and confectionery, dairy products, infant nutrition and formula, nutraceuticals and functional foods, personal care and cosmetics, and other applications. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD Billion) and volume (Tons).

| Conventional Concentrated Milk Fat |

| Organic Concentrated Milk Fat |

| Anhydrous Milk Fat (AMF) |

| Butteroil |

| Other Concentrated Milk Fats |

| Bakery and Confectionery |

| Dairy Products |

| Infant Nutrition and Formula |

| Nutraceuticals and Functional Foods |

| Personal Care and Cosmetics |

| Other Application |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Category | Conventional Concentrated Milk Fat | |

| Organic Concentrated Milk Fat | ||

| By Product Type | Anhydrous Milk Fat (AMF) | |

| Butteroil | ||

| Other Concentrated Milk Fats | ||

| By Application | Bakery and Confectionery | |

| Dairy Products | ||

| Infant Nutrition and Formula | ||

| Nutraceuticals and Functional Foods | ||

| Personal Care and Cosmetics | ||

| Other Application | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the concentrated milk fat market?

The concentrated milk fat market size is USD 5.65 billion in 2026.

How fast is global demand expected to grow?

Sales are projected to rise at a 6.27% CAGR between 2026 and 2031.

Which segment is expanding the quickest?

Infant nutrition shows the fastest growth, advancing at a 7.73% CAGR through 2031.

Who are the leading suppliers?

Fonterra, FrieslandCampina, Lactalis, Dairy Farmers of America, and Arla Foods head the field with just over half of global revenue.

Which region leads consumption?

Asia-Pacific accounts for 37.14% of worldwide demand, driven by China, India, and Southeast Asia.

Page last updated on: