Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.60 Billion |

| Market Size (2026) | USD 3.79 Billion |

| Market Size (2031) | USD 4.89 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Flavored Milk Market Analysis by Mordor Intelligence

The Europe flavored milk market size was valued at USD 3.60 billion in 2025 and estimated to grow from USD 3.79 billion in 2026 to reach USD 4.89 billion by 2031, at a CAGR of 5.23% during the forecast period (2026-2031). The market is growing due to the increasing demand for convenient, ready-to-drink beverages that save consumers time. Flavored milk is also gaining popularity as a source of protein, appealing to health-conscious individuals who seek a convenient and nutritious option. The introduction of hybrid products that combine dairy and plant-based ingredients is attracting a wider range of consumers, including those seeking alternative options. Sustainability regulations are encouraging manufacturers to use recyclable packaging, which aligns with the growing focus on environmental responsibility. To manage the volatility of raw milk prices, companies are adopting vertical integration, which enables them to control costs and maintain a stable supply. The market remains moderately fragmented, with competition among both global and regional players.

Key Report Takeaways

- By product type, dairy-based variants led the European flavored milk market with 85.02% of the market share in 2025; plant-based alternatives are forecasted to expand at a 5.31% CAGR through 2031.

- By flavor profile, chocolate held 51.40% revenue share in 2025, while strawberry is advancing at a 6.29% CAGR through 2031.

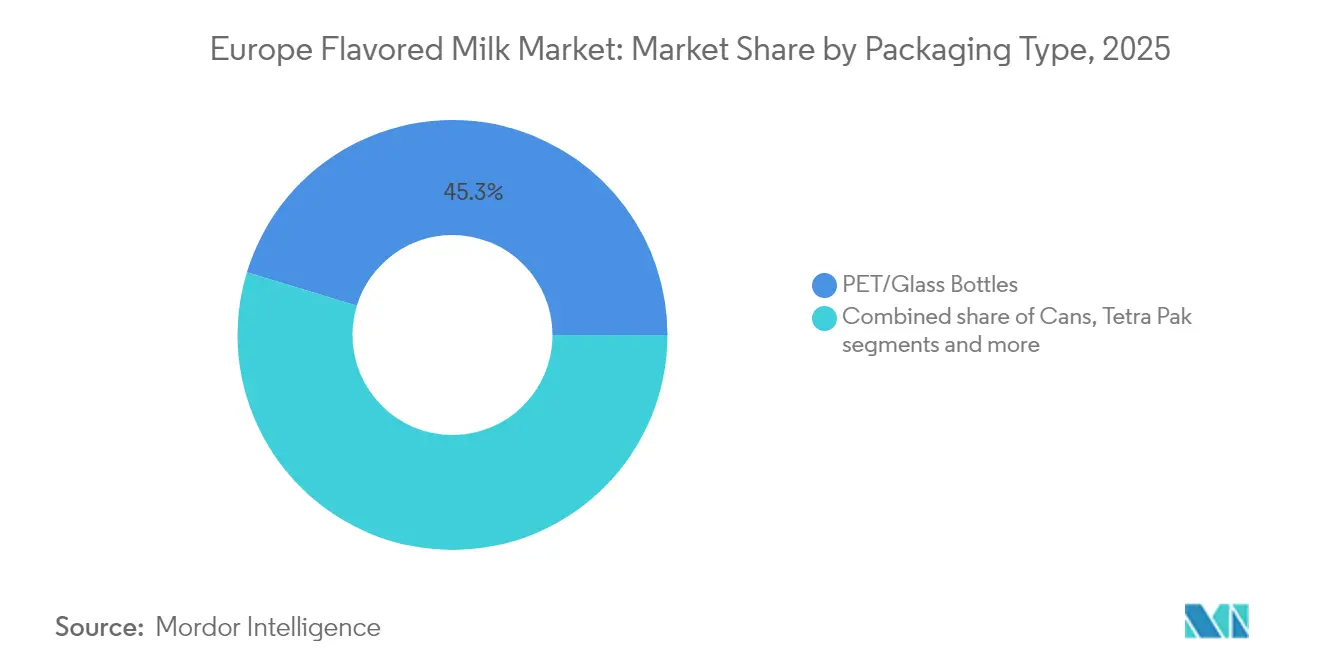

- By packaging type, PET/glass bottles dominated with a 45.29% contribution in 2025; aluminum cans are projected to grow at a 6.38% CAGR between 2026 and 2031.

- By distribution channel, the off-trade accounted for 45.55% of sales in 2025, whereas the on-trade is poised for a 7.05% CAGR over the forecast period.

- By country, the United Kingdom commanded a 24.05% share in 2025, and Spain is expected to post the fastest growth rate of 6.68% up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Flavored Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for convenient and ready-to-drink beverages | +0.9% | Strongest uptake in United Kingdom, Germany, Netherlands | Short term (≤ 2 years) |

| Preference for beverages that are protein-rich and packed with nutrients | +0.8% | United Kingdom, Germany, France, Nordics (Sweden, Denmark via Arla) | Medium term (2-4 years) |

| Growth in the availability of plant-based flavored milk options | +1.1% | United Kingdom, Germany, Netherlands, France; spill-over to Spain, Italy | Medium term (2-4 years) |

| Growing café culture and rising demand for coffee-flavored milk variants | +0.7% | United Kingdom, Germany, France, urban centers across Europe | Short term (≤ 2 years) |

| Rising demand for clean label flavored milk featuring natural ingredients and minimal additives | +0.6% | France, Germany, Netherlands, United Kingdom, Sweden | Long term (≥ 4 years) |

| Exclusive flavored milk launches through celebrity collaborations | +0.4% | United Kingdom, Germany, Poland (Arla-Mondelēz Milka) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Preference for beverages that are protein-rich and packed with nutrients

Consumers in Europe are increasingly focusing on meeting their daily protein requirements, which is driving the demand for fortified flavored milk. According to ScienceDirect in October 2025, the average protein intake across 20 European countries ranges between 0.8 g/kg/day and 1.25 g/kg/day[1]Source: ScienceDirect, "Protein Adequacy in Europe: Adjusting Crude Intakes Using the Protein Adequacy and Quality Score (PAQS)", sciencedirect.com. This growing awareness is encouraging people to choose convenient and nutrient-rich beverages that help fill their dietary protein gaps. To cater to this demand, major European dairy companies, such as Arla, Emmi, and Müller, are expanding their range of high-protein flavored milk products. These products are made using ultra-filtered milk and enriched with whey and casein proteins. Manufacturers are also utilizing advanced filtration and enrichment technologies to enhance the protein content and improve the texture of these beverages. As a result, fortified flavored milk is becoming a practical and accessible option for consumers seeking high-quality protein in their daily diets.

Growth in the availability of plant-based flavored milk options

The increasing availability of plant-based and hybrid dairy–plant milk options is driving growth in the European flavored milk market. This trend is supported by a growing number of plant-focused consumers, including the 964,800 vegans recorded in Italy in 2024, as reported by World Population Review[2]Source: World Population Review, "Veganism by Country 2025", worldpopulationreview.com. The demand for plant-based dairy alternatives is steadily rising, with retail sales of plant-based dairy products reaching EUR 3.6 billion in 2023 and continuing to grow at a faster rate than traditional dairy products. In May 2025, Farm Dairy in the Netherlands and PlanetDairy in Denmark introduced a new range of sustainable dairy–plant milk blends across Europe, reflecting the industry's shift toward environmentally friendly and flexitarian-friendly products. Leading brands like Alpro, Oatly are also expanding their production capacities to cater to the increasing demand for flavored milks made from oats, almonds, and soy.

Increasing demand for convenient and ready-to-drink beverages

The demand for convenient and ready-to-drink beverages is increasing across Europe, leading to a rise in the popularity of flavored milk. Consumers with busy lifestyles are opting for single-serve and portable options instead of traditional café beverages. Packaging innovations, such as lightweight bottles, cans, and ambient cartons, are making flavored milk more accessible in convenience stores and for on-the-go consumption. Additionally, the longer shelf life and availability of these products in ambient formats make them a practical choice for consumers who prioritize convenience. The success of similar portable packaging in other categories, like yogurt pouches, is also influencing consumer preferences and encouraging the adoption of flavored milk. These factors are collectively positioning flavored milk as a convenient and appealing everyday beverage for people with active and mobile lifestyles.

Growing café culture and rising demand for coffee-flavored milk variants

The growing café culture across Europe is driving demand for coffee-flavored milk products, as consumers increasingly seek the taste of café-style beverages in convenient, ready-to-drink options. Europe’s strong coffee consumption habits support this trend. For instance, in the United Kingdom, people consume approximately 98 million cups of coffee daily, according to the British Coffee Association[3]Source: British Coffee Association, "Coffee Consumption", britishcoffeeassociation.org. This widespread love for coffee, combined with the rapid growth of Europe’s ready-to-drink (RTD) coffee market, is encouraging consumers to explore affordable, dairy-based coffee alternatives. Countries like Germany are witnessing significant adoption of these products as more people develop a preference for premium coffee flavors. Partnerships between cafés and manufacturers, along with the increasing availability of these products in convenience stores, are making coffee-flavored milk more accessible.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising concerns regarding the high sugar content in flavored milk | -0.5% | United Kingdom, France, Germany, Netherlands, Sweden | Short term (≤ 2 years) |

| Increasing demand for clear and transparent ingredient labeling | -0.3% | France, Germany, Netherlands, United Kingdom | Medium term (2-4 years) |

| Fluctuating milk prices are driving up production costs | -0.7% | Europe-wide, with acute impact in Spain, Italy, Poland | Short term (≤ 2 years) |

| Concerns regarding the use of artificial flavors, colors, and stabilizers | -0.4% | France, Germany, Netherlands, United Kingdom, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising concerns regarding the high sugar content in flavored milk

Concerns about the high sugar content in flavored milk are increasingly limiting its market growth in Europe. Consumers are becoming more health-conscious, and policymakers are introducing stricter measures to reduce sugar consumption in beverages. For example, in Italy, the implementation of a sugar tax has proven highly effective. According to ScienceDirect, as of July 2024, this tax has resulted in an 18% reduction in purchases of sugar-sweetened beverages and a 24% decrease in sugar intake[4]Source: ScienceDirect, "The Distributional Implications of Health Taxes: A Case Study on the Italian Sugar Tax", sciencedirect.com. Such results are encouraging other European countries to consider similar policies, which are adding cost pressures for manufacturers of high-sugar flavored milk products. Labeling systems, such as Nutri-Score, are influencing consumer choices. Many popular flavored milk variants, such as chocolate and strawberry, receive low ratings (D or E), which impacts their visibility and shelf placement in retail stores.

Concerns regarding the use of artificial flavors, colors, and stabilizers

Concerns about artificial flavors, colors, and stabilizers are slowing the growth of the European flavored milk market. Consumers are becoming increasingly cautious about these ingredients, often linked to the “E-number stigma,” which refers to skepticism around additives labeled with E-numbers. Ingredients such as carrageenan, artificial vanilla, and certain stabilizers are facing increased scrutiny, even when they comply with EU safety standards. This has led consumers to pay closer attention to product labels and avoid heavily processed options. Stricter regulations on cocoa contaminants, such as limits on ochratoxin levels, are forcing manufacturers to improve supplier oversight and reformulate their products to meet these standards. In countries such as France and Germany, there is a growing demand for flavored milk made with natural ingredients or free from artificial additives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plant-Based Momentum Within Dairy Dominance

Dairy-based flavored milk held a significant 85.02% share of the European market in 2025, primarily due to its strong consumer preference and well-established cold-chain logistics. These products are naturally high in protein, offering 8–9 grams per serving, which makes them a popular choice for those seeking nutritious and satisfying beverages. Their widespread availability in supermarkets, cafés, and schools ensures they remain a convenient option for daily consumption. The introduction of new flavors and premium product lines continues to strengthen the position of dairy-based flavored milk in terms of both market volume and value across Europe.

Plant-based flavored milk is projected to grow at a CAGR of 5.31% through 2031, driven by the increasing demand for vegan, lactose-free, and flexitarian diets. Popular options, such as oat, soy, and almond milk, are gaining traction as consumers seek sustainable and ethical alternatives to traditional dairy products. Enhanced production capabilities and broader retail availability are making these products more accessible to a wider audience. Clean labels and allergen-free claims are appealing to health-conscious consumers. Although plant-based flavored milk currently holds a smaller market share, its growing variety of flavors and rising consumer interest are helping it establish a stronger presence as a complementary segment in the flavored milk market.

By Flavor Profile: Chocolate Reigns, Strawberry Rises

In 2025, chocolate made up 51.40% of the Europe flavored milk market, maintaining its position as the most preferred flavor. Its popularity stems from its universal appeal, making it a staple choice for both children and adults. Partnerships between dairy producers and well-known chocolate brands have helped chocolate-flavored milk gain prominent shelf space in stores, boosting its visibility. Seasonal limited-edition offerings and indulgent variations further drive consumer interest, ensuring steady demand. As a result, chocolate remains the leading flavor, contributing significantly to the market's overall growth in terms of both sales and value.

Strawberry-flavored milk is projected to grow at a CAGR of 6.29% through 2031, as more consumers opt for lighter, fruit-based flavors in their beverages. Its refreshing and versatile taste appeals to a wide range of age groups, and its adaptability to both dairy and plant-based formulations has led to its inclusion in various new product launches. Retailers are also increasing shelf space for strawberry-flavored milk to meet the rising demand for healthier and less sugary options. Additionally, advancements in natural coloring and cleaner, fruit-based ingredients are enhancing its appeal. These factors make strawberry the fastest-growing flavor segment in the European flavored milk market.

By Packaging Type: Aluminum Cans Accelerate Under Recycling Targets

PET/glass bottles made up 45.29% of the European flavored milk market in 2025. This dominance is due to their strong consumer acceptance and the transparency of the packaging, which allows customers to see the product inside, offering reassurance about its quality. These packaging types are commonly used in both retail stores and foodservice outlets because they are portable, durable, and easy to recycle within well-established collection systems. Additionally, their suitability for both single-serve and family-size options provides manufacturers with flexibility. The clear visibility of the product and branding through labels further attracts consumers, making PET and glass bottles the most preferred packaging options in the region.

Aluminum cans are projected to grow at a compound annual growth rate (CAGR) of 6.38% from 2026 to 2031. This growth is driven by increasing consumer demand for convenient and portable beverage packaging. Aluminum cans are lightweight, cool quickly, and are highly recyclable, which appeals to environmentally conscious buyers. They also help extend the shelf life of products and are ideal for placement in vending machines, convenience stores, and travel retail outlets. Furthermore, the growing popularity of ready-to-drink (RTD) coffee and energy drinks has encouraged the use of aluminum cans for flavored milk products. These combined benefits are driving the rapid adoption of aluminum cans, making them one of the fastest-growing packaging options in the European flavored milk market.

By Distribution Channel: On-Trade Gains Through Café Alliances

Off-trade channels, including supermarkets, hypermarkets, and discounters, accounted for 45.55% of the Europe flavored milk market in 2025. These channels dominate due to their affordable private-label options and prominent in-store promotions, which encourage impulse buying. Supermarkets and hypermarkets offer a wide variety of flavors and packaging sizes, making them a convenient choice for regular household shopping. Additionally, their well-established cold storage systems ensure the availability of fresh products, while frequent discounts and multi-pack deals attract cost-conscious consumers. Discounters, in particular, are gaining traction by offering budget-friendly flavored milk options, thereby further strengthening their market position.

On-trade channels, such as cafés, quick-service restaurants, and vending machines, are expected to grow at a 7.05% CAGR from 2026 to 2031. The increasing popularity of café culture and coffee-flavored milk products is driving demand in these settings. Consumers are also turning to on-the-go options, with vending machines in travel hubs, workplaces, and other high-traffic areas playing a significant role in expanding accessibility. Premium offerings in cafés, such as specialty flavored milk beverages, are encouraging consumers to try higher-priced products. These factors are collectively contributing to the rapid growth of on-trade channels, making them an important and expanding segment in the flavored milk market.

Geography Analysis

The United Kingdom was the largest flavored milk market in Europe in 2025, holding a 24.05% share. This strong position is supported by a well-developed grocery retail system and a popular café culture that encourages regular consumption of flavored milk and milk-based beverages. Major investments, such as Arla’s GBP 300 million upgrades, have increased the availability of high-protein and health-focused flavored milk options to meet the growing demand for wellness products. Additionally, the expected expansion of sugar levies is pushing manufacturers to create reduced-sugar alternatives. Frequent collaborations between brands and the introduction of trendy flavors further solidify the United Kingdom’s role as a leading market for testing new product ideas.

Spain is expected to be the fastest-growing flavored milk market in Europe, with a projected CAGR of 6.68% through 2031. Increasing imports drive this growth, a rising preference for premium and indulgent flavored milk options, and shifting consumer tastes, even as domestic production slows. The country’s strong tourism industry and diverse retail formats are exposing consumers to a wider variety of innovative products. These factors, combined with changing purchasing habits, are making Spain a key market for expansion in Europe. The focus on offering high-quality and indulgent products is helping brands attract a broader audience and gain a competitive edge.

Germany played a significant role in the growth of the European flavored milk market in 2024, supported by the expansion of discount retail chains and increasing interest in ready-to-drink coffee-inspired flavored milk products. Sustainability trends are also shaping the market, with a growing shift toward eco-friendly packaging solutions like aluminum-free cartons. Other countries, such as the Netherlands, the Nordics, Italy, Poland, and Switzerland, also contribute to the market with their unique consumer preferences, pricing strategies, and retail environments. While regulatory harmonization across Europe simplifies product launches, cultural and linguistic differences require brands to adopt localized strategies. This creates a wide range of opportunities for growth across the region.

Competitive Landscape

The European flavored milk market is moderately fragmented. FrieslandCampina’s merger with Milcobel in December 2024 has significantly enhanced its procurement capabilities and aseptic production capacity, enabling the company to execute more effective marketing and promotional strategies. Similarly, Arla’s acquisition of Volac in February 2025 has strengthened its position in the premium functional product segment by gaining access to advanced whey technology. Danone, through its Milk Academy initiative, is focusing on sustainable practices like regenerative sourcing and reducing methane emissions, which align with growing consumer and retailer demand for environmentally responsible products.

Plant-based brands such as Oatly and Alpro are expanding their presence by forming partnerships with cafés and offering direct-to-consumer bundles. These strategies cater to the increasing demand for sustainable and lactose-free options, which are gaining popularity among health-conscious consumers. Additionally, Refresco, a contract manufacturer, has acquired Frías Nutrición, allowing retailers to quickly enter the private-label market for oat and almond-based drinks. Smaller brands are leveraging social media campaigns and celebrity endorsements to gain visibility. However, stricter compliance regulations and new packaging requirements are expected to drive market consolidation, making it more challenging for new entrants to establish themselves in the European flavored milk market.

Technological advancements are playing a crucial role in helping companies differentiate themselves in the competitive market. Innovations such as enzyme-enabled hybrid proteins and mono-material packaging are enabling businesses to meet sustainability goals while maintaining profitability. The growing share of private-label products, which is projected to reach 40%, is pushing established brands to accelerate their innovation efforts. To stay competitive, these brands are focusing on creating compelling narratives around product origin, nutritional benefits, and sustainability, ensuring they retain their position on retail shelves in the European flavored milk market.

Europe Flavored Milk Industry Leaders

-

Nestlé S.A.

-

Danone S.A.

-

Royal FrieslandCampina N.V.

-

Müller Group

-

Arla Foods amba

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Arla, in collaboration with Mondelēz International, introduced a new range of Milka chocolate milk products. This launch marked a significant expansion for the Milka brand, as it ventures into a new product category.

- January 2024: Müller announced the launch of Cadbury milkshakes, marking a significant milestone as it introduced the Cadbury brand into the bottled milk drinks category for the first time in the United Kingdom and Ireland.

- September 2023: Empire Bespoke Foods introduced the Spanish chocolate milk brand, Cacaolat, to the market. Known for its rich and creamy texture, Cacaolat is a popular beverage in Spain and was made available to a broader audience through this launch.

Europe Flavored Milk Market Report Scope

The European flavored milk market is segmented by product type into dairy-based and plant-based. The flavor profile is segmented into chocolate, strawberry, vanilla, and other options. The packaging type is segmented as PET/glass bottles, Tetra Pak, cans, and others. The distribution channel is segmented into on-trade and off-trade. The market is also segmented by country, including the United Kingdom, Germany, France, Italy, Spain, the Netherlands, Sweden, Poland, Switzerland, and the Rest of Europe.

By Product Type

| Dairy-Based | Cow |

| Goat | |

| Others | |

| Plant-Based | Soy |

| Almond | |

| Oat | |

| Others |

By Flavor Profile

| Chocolate |

| Strawberry |

| Vanilla |

| Others |

By Packaging Type

| PET/Glass Bottles |

| Cans |

| Tetra Pak |

| Others |

By Distribution Channel

| On-trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Specialist Retailers | |

| Convenience Stores | |

| Online Retail | |

| Others |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Poland |

| Switzerland |

| Rest of Europe |

| By Product Type | Dairy-Based | Cow |

| Goat | ||

| Others | ||

| Plant-Based | Soy | |

| Almond | ||

| Oat | ||

| Others | ||

| By Flavor Profile | Chocolate | |

| Strawberry | ||

| Vanilla | ||

| Others | ||

| By Packaging Type | PET/Glass Bottles | |

| Cans | ||

| Tetra Pak | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Specialist Retailers | ||

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Switzerland | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe flavored milk market in 2026?

The Europe flavored milk market size is USD 3.79 billion in 2026 with a forecast 5.23% CAGR to 2031.

Which product type is growing the fastest?

Plant-based flavored milk is projected to post a 5.31% CAGR through 2031, outpacing dairy-based alternatives.

What flavor is most popular among European consumers?

Chocolate leads with 51.40% share, although strawberry is the fastest-growing at 6.29% CAGR.

Which country offers the highest growth opportunity?

Spain is expected to grow at 6.68% CAGR thanks to rising imports and premiumization trends amid stagnant local milk supply.

Page last updated on: