Hemp Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

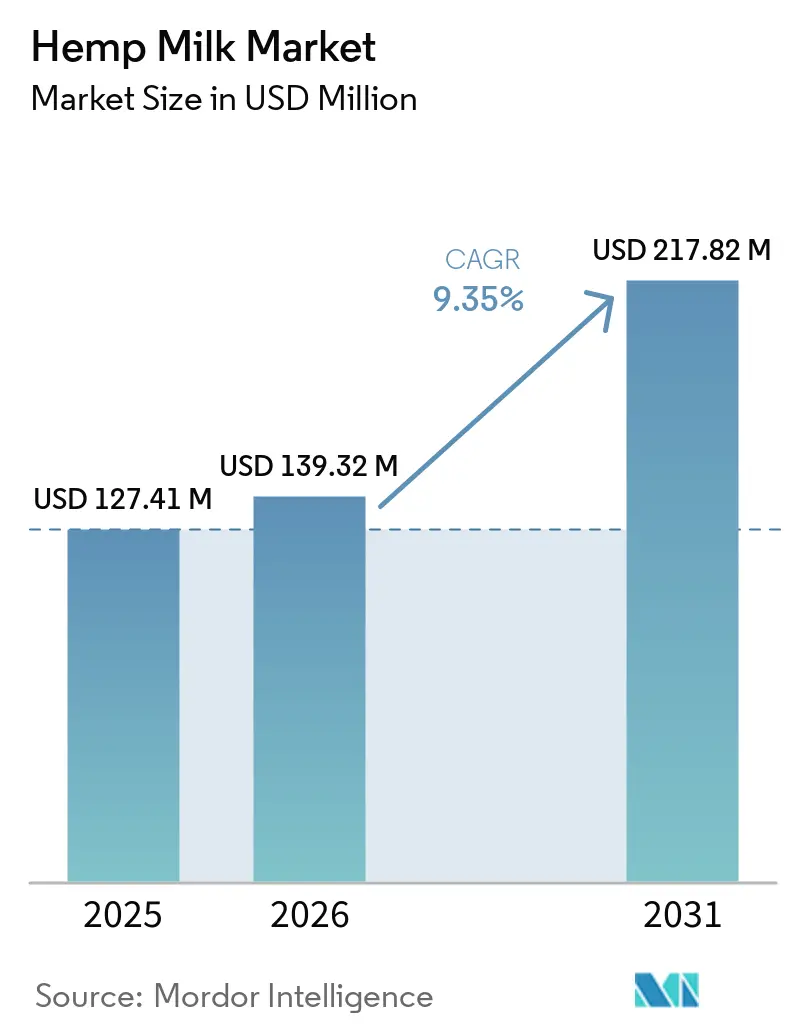

| Market Size (2026) | USD 139.32 Million |

| Market Size (2031) | USD 217.82 Million |

| Growth Rate (2026 - 2031) | 9.35% CAGR |

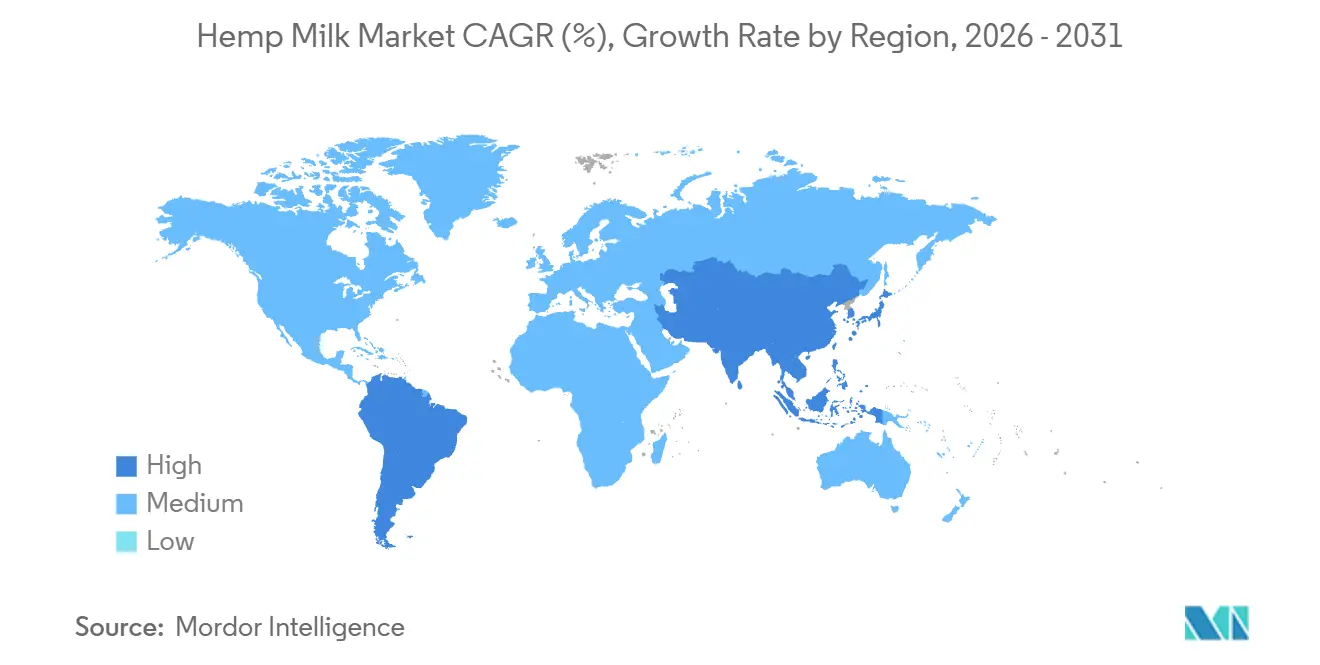

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

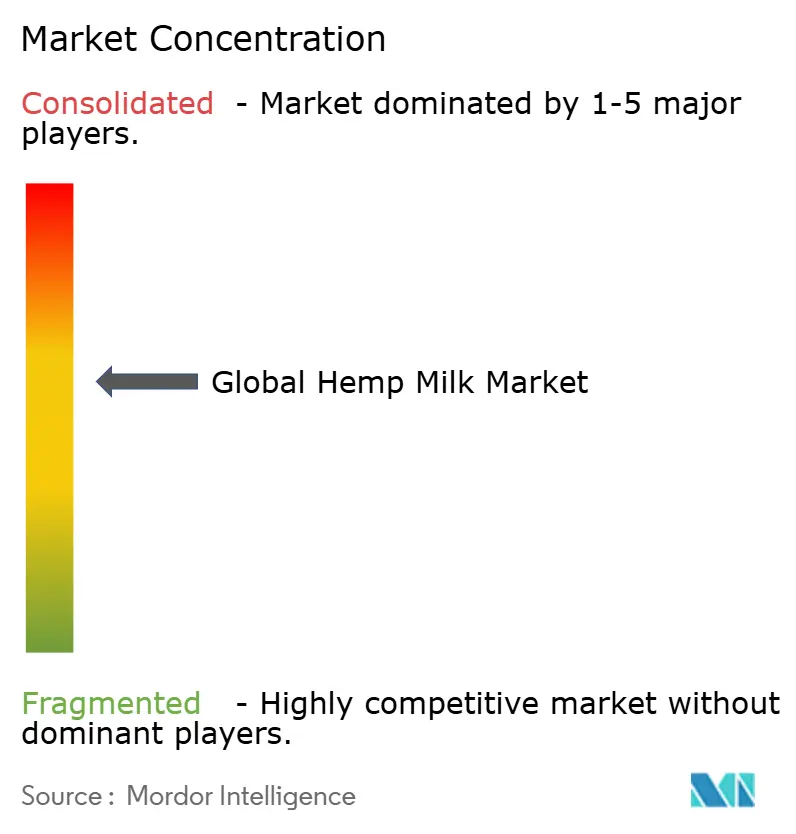

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hemp Milk Market Analysis by Mordor Intelligence

The Hemp Milk Market is expected to grow from USD 127.41 million in 2025 to USD 139.32 million in 2026 and reach USD 217.82 million by 2031, with a CAGR of 9.35% from 2026 to 2031. Growth is driven by improved regulations, rising health awareness, and environmental concerns. The FDA's 2025 draft guidance on plant-based milk labeling has clarified regulations, while increased hemp cultivation in the U.S. has strengthened the supply chain. Hemp milk's strong nutritional profile, including its amino acids and omega-6 to omega-3 ratio of 3:1-4:1, appeals to health-conscious consumers. The market is moderately consolidated, offering opportunities for new entrants in niche segments, while established players benefit from integrated operations. North America leads in value, while Asia-Pacific shows the fastest growth, reflecting a shift toward premium plant-based proteins.

Key Report Takeaways

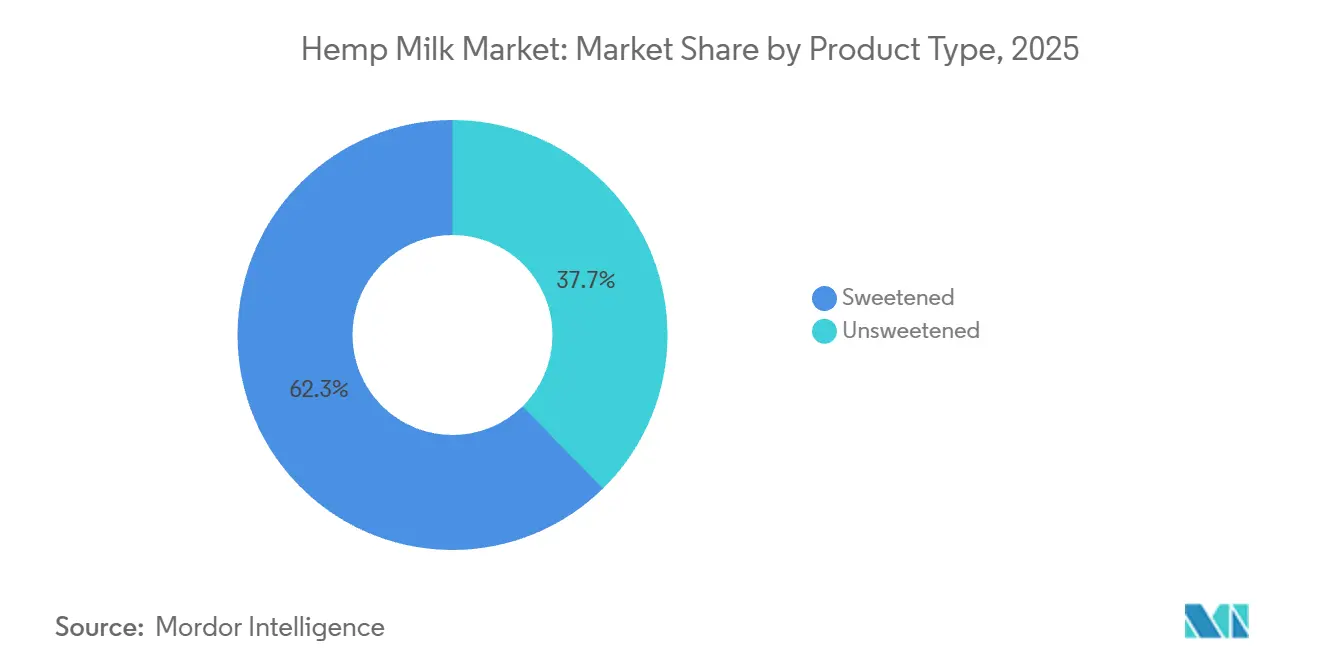

- By product type, sweetened variants held 62.34% of the hemp milk market share in 2024, whereas unsweetened products are forecast to expand at a 10.51% CAGR between 2026 and 2031.

- By flavor, flavoured hemp milk commanded a 58.91% share of the hemp milk market size in 2025, while unflavoured offerings are advancing at a 10.35% CAGR through 2031.

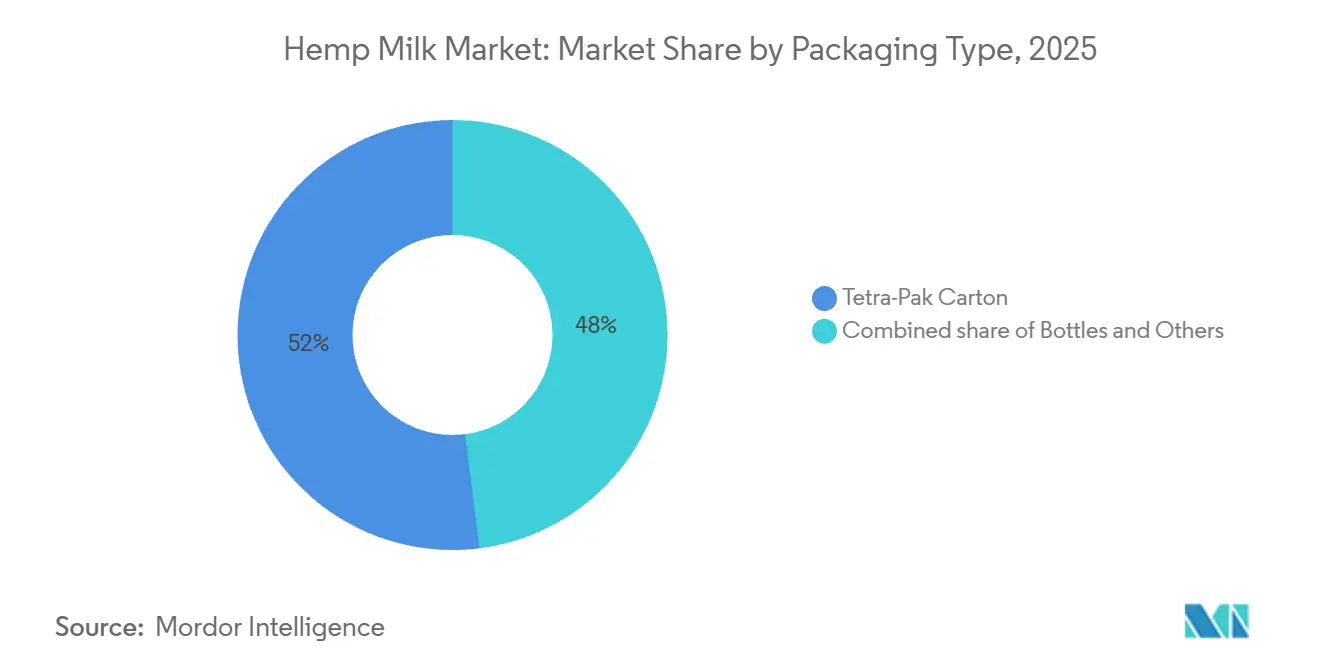

- By packaging, Tetra-Pak cartons accounted for 52.01% of the hemp milk market size in 2025; bottle formats are growing at a 11.21% CAGR to 2031.

- By distribution channel, retail captured 68.33% of 2025 sales, and food service is projected to maintain the fastest 9.81% CAGR over 2026-2031.

- By geography, North America controlled 38.96% of 2025 revenue, whereas Asia-Pacific is predicted to post the highest 11.65% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hemp Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising food allergies and intolerances | +1.8% | Global, with elevated incidence in North America and Europe | Medium term (2–4 years) |

| Shift toward plant-based diets boosts demand for dairy-free options like hemp milk | +2.1% | Global, led by North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Awareness of omega-3s, proteins, and low cholesterol content attracts wellness seekers | +1.5% | North America, Europe, and affluent Asia-Pacific metros | Medium term (2–4 years) |

| Demand for minimal-ingredient, natural products favors hemp milk formulations | +1.3% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Focus on environmentally sustainable food choices | +1.6% | Europe (regulatory-driven), North America (corporate procurement), Asia-Pacific (urban centers) | Long term (≥ 4 years) |

| Diversification of flavor options | +0.9% | North America and Europe retail; Asia-Pacific foodservice | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Plant-Based Diets Boosts Demand for Dairy-Free Options Like Hemp Milk

Health, ethical, and environmental motivations are reshaping dietary patterns, broadening the market from just lactose-intolerant individuals to include flexitarians and reducetarians. Hemp milk stands to gain from this expanding audience. While its protein content is lower than that of soy, it surpasses almond and rice variants. Moreover, its complete amino acid profile attracts consumers in search of diverse plant-based proteins. According to the USDA's 2024–2025 reports, hemp cultivation is on the rise in states with established organic certification. This not only enhances traceability but also allows for USDA Organic claims, which fetch higher retail prices. In a move reflecting a larger industry trend, Danone has pledged a multi-million-pound investment in the UK, committing to source 100% British oats for its Alpro plant-based drinks. This shift underscores a growing emphasis on localized, transparent supply chains that cut down carbon miles and resonate with provenance-aware consumers. Hemp's versatility as a dual-use crop—providing seeds for food and fiber for textiles—generates co-product revenue streams. This feature offers a buffer against price volatility, a distinct advantage over single-output botanicals like almonds.

Awareness of Omega-3s, Proteins, and Low Cholesterol Content Attracts Wellness Seekers

Hemp milk stands out in the market due to its omega-3 to omega-6 ratio of 1:3, which aligns better with dietary recommendations than most plant oils. Studies show that hemp seed protein contains bioactive peptides with ACE-inhibitory activity, offering potential cardiovascular benefits beyond being cholesterol-free. This supports its premium positioning and higher pricing in wellness-focused retail. However, fortification is essential. UK supermarket data revealed non-dairy milks provide only 53% of the vitamin B12 reference value per 200 mL serving compared to dairy's 120%, with no iodine fortification in surveyed products. Brands addressing these gaps with bioavailable forms like methylcobalamin for B12 and potassium iodide for iodine can stand out with stronger label claims and avoid regulatory issues as governments tighten standards for dairy alternatives.

Demand for Minimal-Ingredient, Natural Products Favors Hemp Milk Formulations

Clean-label trends are pushing manufacturers to replace gums, emulsifiers, and synthetic stabilizers as consumers increasingly reject these additives. Hemp milk naturally stabilizes emulsions due to its proteins and phospholipids, reducing the need for hydrocolloids like carrageenan and gellan gum. Physical methods, such as high-pressure homogenization and pH-shift processing, create shelf-stable emulsions without chemicals, supporting the "whole food" appeal that justifies premium pricing. JOI's organic hemp concentrate, made only from hemp seeds, uses steam pasteurization for an 18-month shelf life, avoiding preservatives. Packaged in glass jars, it eliminates water transport and allows portion control, appealing to zero-waste consumers. The main challenge is maintaining creaminess and mouthfeel without additives, but enzymatic processing and protein enrichment are addressing this issue.

Increased Awareness Around Health and Nutrition

Consumer education regarding functional nutrition continues to influence purchasing decisions as people seek products that deliver targeted health advantages beyond basic nutritional needs. Hemp milk contains naturally occurring gamma-linolenic acid (GLA) and optimal omega fatty acid ratios, providing anti-inflammatory properties that set it apart from competing plant-based alternatives. Research conducted on fermented hemp seeds reveals enhanced anti-inflammatory benefits through metabolite modulation, presenting opportunities for functional food development in premium market segments. The FDA's revised "healthy" food labeling definition creates regulatory pathways for hemp milk manufacturers to communicate nutritional benefits to consumers, which could increase market awareness and purchase consideration [1]Source: Federal Register, “Food Labeling: Nutrient Content Claims", federalregister.gov. This regulatory framework enables manufacturers to make evidence-based marketing claims, helping them establish a distinct position in the expanding plant-based beverage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory hurdles and ambiguous hemp classification in some regions | -1.2% | Asia-Pacific (China, India, Japan), Middle East, select European markets | Medium term (2–4 years) |

| Perceived association of hemp with psychoactive cannabis | -0.8% | North America, Europe, and emerging Asia-Pacific markets | Short term (≤ 2 years) |

| Limited consumer awareness in several large markets | -1.0% | Asia-Pacific (excluding Australia), South America, Middle East and Africa | Medium term (2–4 years) |

| Comparatively high retail prices than dairy and some plant-milks | -1.4% | Global, most acute in price-sensitive South America, MEA, and rural Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Hurdles and Ambiguous Hemp Classification in Some Regions

Hemp regulations differ across regions, creating compliance challenges that slow market growth and raise costs for manufacturers. Germany's Consumer Cannabis Act enforces strict THC limits and classifies hemp products as "novel foods," requiring pre-market approval. These rules make it harder for smaller manufacturers to enter the market. The EU's Novel Foods Regulation also demands detailed safety documentation, with hemp-derived foods facing extra scrutiny due to their link to cannabis. This process causes delays and disrupts operations. Research conducted by the German Federal Institute for Risk Assessment reveals that trace cannabinoids in hemp products can transfer to milk through animal feed consumption, raising significant food safety concerns that may restrict hemp's agricultural applications [2]Source: German Federal Institute for Risk Assessment, “Identify Risks – Protect Health", bfr.bund.de. These persistent regulatory complexities discourage potential investors from supporting hemp milk production initiatives and create obstacles for companies seeking to expand their presence in new geographic markets.

Perceived Association of Hemp with Psychoactive Cannabis

The persistent misconception between hemp and cannabis presents significant marketing hurdles that necessitate substantial investments in consumer education programs. Cultural resistance and misconceptions particularly impact market acceptance among older consumer segments and in traditionally conservative regions, which constrains hemp milk's potential market penetration compared to conventional plant-based alternatives. Scientific research has demonstrated conclusively that THC becomes completely undetectable in dairy products following a 15-day withdrawal period when dairy cows are fed hemp byproducts, offering concrete evidence to alleviate safety apprehensions [3]Source: Science X Network, “THC Is Undetectable After Withdrawal Period in Cows Fed Hemp By-product", phys.org. The FDA's 2025 regulatory guidance on plant-based milk labeling provides manufacturers with enhanced frameworks to effectively communicate hemp milk's non-psychoactive characteristics, although the financial burden of consumer education initiatives remains considerable. These perception-related challenges create strategic opportunities for businesses to gain first-mover advantages in markets where well-executed consumer education campaigns can successfully establish hemp milk as a mainstream beverage choice rather than a specialized product offering.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Unsweetened Gains on Wellness Pivot

Unsweetened hemp milk is growing at 10.51% annually through 2031, outpacing the category average as health-conscious consumers avoid added sugars and focus on glycemic control. This segment appeals to ketogenic, paleo, and diabetic consumers who prioritize low carbohydrates and natural ingredients. Hemp seed research highlights its low sugar and high fiber content, supporting satiety and metabolic health, making unsweetened hemp milk a functional beverage. Foodservice adoption is rising, with cafes and restaurants favoring neutral-tasting bases that complement coffee and culinary uses. Starbucks' October 2024 removal of plant-milk surcharges has further normalized non-dairy options. Brands are introducing barista-specific unsweetened variants designed for foam stability and heat resistance, mimicking dairy's performance in espresso drinks.

In 2025, sweetened hemp milk accounted for 62.34% of revenue, driven by mainstream retail demand where taste is key for repeat purchases. Flavors like vanilla, chocolate, and coffee help mask hemp's grassy notes, which can deter new consumers. However, sweetened products face challenges from clean-label demands and regulatory scrutiny. The FDA's draft guidance on plant-based milk labeling encourages nutrient-comparison statements, while added sugars increase calorie counts, undermining health-focused positioning. Nutiva's February 2026 previews highlight global flavors and reduced sodium, showing the need for taste innovation aligned with health trends. The challenge lies in balancing flavor and clean labels. Natural sweeteners like dates or monk fruit add costs, while artificial alternatives risk alienating health-conscious buyers.

By Flavor: Unflavored Bases Capture Foodservice and Culinary Demand

Unflavored hemp milk is growing at 10.35% annually, driven by its neutral taste, ideal for foodservice and home-cooking. Restaurants, cafes, and institutional kitchens use unflavored concentrates in coffee, smoothies, and recipes for consistent performance without flavor interference. JOI's organic hemp base, made from hemp seeds with an 18-month shelf life via steam pasteurization, targets culinary users valuing transparency and portion control. Barista-edition launches, like Elmhurst 1925's February 2026 expansion into Whole Foods, highlight how optimized features like foam stability and heat resistance can justify premium pricing. Processing innovations, such as high-pressure homogenization, improve emulsion stability without additives, enabling clean-label formulations that meet foodservice demands for functionality and simplicity.

Flavored variants accounted for 58.91% of the 2025 market, led by vanilla and chocolate, which attract taste-focused consumers. Good Hemp's 2020 oat-hemp blend at £1.85 per liter in Waitrose showed how combining oat's creamy sweetness with hemp's omega-3 benefits broadens appeal while maintaining uniqueness. However, added sugars and calories can conflict with wellness trends, and natural flavor use complicates batch consistency. A December 2024 UK Court of Appeal ruling on dairy-like marketing terms further restricts flavor naming, varying by jurisdiction. Seasonal flavors like pumpkin spice and matcha drive consumer trials but increase SKU management challenges, especially for smaller brands with limited co-packing capacity.

By Packaging Type: Bottles Gain on Sustainability and Premium Positioning

Bottle formats are growing at 11.21% annually, driven by the sustainability appeal of glass jars and their premium pricing. JOI's concentrate model, using reusable glass jars with metal lids, cuts water transport, reduces packaging waste, and offers an 18-month shelf life without preservatives, aligning with zero-waste values. Transparent glass packaging highlights product freshness and minimal processing. However, glass is heavy and fragile, raising logistics costs and breakage rates, which reduce profit margins. PET bottles are lighter but face criticism for plastic waste, pushing brands to use post-consumer recycled (PCR) content and deposit-return schemes, adding complexity. Regulations like Europe’s Single-Use Plastics Directive and extended producer responsibility rules favor reusable or recyclable formats, giving glass and aluminum bottles an edge in markets with strong reverse-logistics systems.

Tetra-Pak cartons held 52.01% of 2025 packaging volume due to cost-effective ambient distribution and long shelf life, reducing cold-chain needs. In February 2026, Tetra Pak launched paper-based barrier technology for its A3/Speed lines, achieving 87% renewable content and a 26% lower carbon footprint, verified by the Carbon Trust. Maeil Dairies’ use for soy milk at 24,000 packages per hour shows its viability for hemp milk co-packers. Cartons are easier to recycle with a shift from three-layer (paperboard, aluminum, polymer) to two-layer (paperboard and polymer with metallic coating) structures, improving fiber recovery and recycling efficiency. However, they lack the premium image of glass and face skepticism about recyclability in regions with weak recycling systems. Tethered caps, made from sugarcane-based polymers and designed to stay attached after opening, address litter concerns and comply with EU single-use plastic rules but increase costs and require filling-line changes.

By Distribution Channel: Foodservice Accelerates on Surcharge Elimination and Menu Simplification

Foodservice channels are growing at 9.81% annually, driven by Starbucks' October 2024 decision to remove plant-milk surcharges in North America. This change lowers barriers for non-dairy options and sets a trend for making them default in busy venues. Surcharges, typically USD 0.50 to USD 1.50 per drink, have limited adoption and complicated pricing. Cafes are streamlining operations by using versatile plant-based options for hot and cold drinks, focusing on barista-friendly formulations with foam stability and heat resistance. Elmhurst 1925's February 2026 barista line expansion shows that matching dairy's functionality allows premium pricing in foodservice, where consistency and labor efficiency outweigh ingredient costs. Institutions like schools, hospitals, and corporate cafeterias are adopting allergen-free plant milks to meet dietary needs and reduce contamination risks, creating growth opportunities for brands with strong distributor ties and food-safety certifications.

Retail made up 68.33% of 2025 sales, led by supermarkets and hypermarkets with refrigerated infrastructure and shelf visibility. Online retail is expanding quickly, especially for concentrate formats and subscription models that cut costs and automate restocking. JOI's "Subscribe & Save" program offers 5% discounts and free shipping at customizable intervals (every 2, 4, or 6 weeks), turning trials into repeat sales and boosting customer value. Convenience stores face challenges like limited cold-chain capacity and shelf space, but single-serve formats, Tetra Pak 200 mL Slim cartons, and biodegradable packets are emerging as solutions. Ripple Foods' Q1 2026 entry into Target, Whole Foods, and Walmart shows that mainstream retail success requires promotions, slotting fees, and sales guarantees, which smaller brands often cannot afford, giving larger players an edge.

Geography Analysis

North America stands at the forefront of the global hemp milk market, holding a commanding 38.95% market share in 2025. The region's success builds upon its forward-thinking regulatory environment and sophisticated hemp cultivation infrastructure that forms the backbone of efficient domestic supply chains. The implementation of Canada's Safe Food for Canadians Act has created a clear pathway for manufacturers, removing regulatory hurdles and streamlining market access. North American consumers demonstrate a deep understanding of plant-based alternatives, supported by an extensive retail network that effectively distributes premium specialty products. While the region maintains its market leadership, the mature market environment presents competitive challenges that may impact growth rates compared to emerging markets where alternative protein sectors are still developing.

Asia-Pacific emerges as the market's growth engine, recording a robust 11.65% CAGR through 2031. This dynamic growth reflects the region's evolving consumer landscape, characterized by an expanding middle class and increasing health awareness that drives demand for functional food products. Chinese consumers particularly demonstrate a strong inclination toward nutritional value in plant-based milk choices, placing health benefits above price considerations. The region's growth story is further enhanced by rising disposable incomes and ongoing urbanization trends that create natural demand for convenient, premium food products. However, the journey ahead requires significant investment in consumer education about hemp's nutritional benefits to achieve market penetration levels similar to established alternatives like soy and almond milk.

Europe continues to shape the market through its strong environmental ethos and well-established plant-based food ecosystem, creating natural opportunities for hemp milk adoption. The EU's Novel Foods Regulation provides a structured framework for product authorization, though manufacturers must navigate extended approval timelines that influence market entry strategies. Despite these regulatory considerations, Europe's commitment to sustainability and plant-based alternatives continues to drive market development and innovation in the hemp milk segment.

Competitive Landscape

The hemp milk market is moderately consolidated, maintains a balanced competitive structure, where established companies hold strong positions while providing space for specialized and regional players to thrive. Companies like Manitoba Harvest, under Tilray's ownership, have built comprehensive supply chains that span from hemp farms to manufacturing facilities. This end-to-end control gives them significant advantages in cost management and quality assurance, which smaller competitors find challenging to match, particularly when hemp seed prices change due to farming conditions and regulatory updates.

Innovation in processing technology has become a key success factor, as companies invest in advanced methods to enhance their products' nutritional value and improve taste characteristics. A notable example is Burcon NutraScience's breakthrough in developing the industry's first high-purity hemp protein isolate, demonstrating how technological advancement can create distinct market advantages in developing plant-based products.

The market's growth benefits from hemp's GRAS (Generally Recognized as Safe) classification across various regions, which simplifies market entry compared to other new protein sources that require extensive safety testing. The industry is experiencing a wave of consolidation as larger food companies purchase specialized hemp producers to gain their supply networks and established brands. This environment creates valuable opportunities for strategic alliances and potential business exits for smaller companies.

Hemp Milk Industry Leaders

-

Campbell Soup Company

-

Living Harvest Foods

-

Good Hemp

-

Manitoba Harvest Hemp Foods

-

Elmhurst 1925

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: A New Zealand (Kiwi) entrepreneur, Miah Faumuina, has recently entered the plant-based dairy space by launching a hemp milk business in Mexico, reflecting the growing global demand for alternative milk products. The move is largely driven by regulatory constraints in New Zealand, where strict rules around hemp production have limited large-scale commercialization, prompting the entrepreneur to expand operations overseas.

- November 2024: CV Sciences signed a definitive agreement to acquire Extract Labs, a hemp product manufacturer. The acquisition aims to expand the company's product portfolio through its +PlusCBD™ brand and improve supply chain efficiency.

- May 2024: Lithuanian hemp processing company established partnerships for organic hemp and pumpkin products across European markets, emphasizing pesticide-free production and innovative processing equipment.

- April 2023: JOI introduced Hemp Milk Concentrate, a product made from organic hemp hearts. The concentrate is available in 8 lb pails and can be used for cooking or mixed with water to create hemp milk.

Global Hemp Milk Market Report Scope

| Unsweetened |

| Sweetened |

| Unflavoured |

| Flavoured |

| Tetra-Pak Carton |

| Bottle |

| Others |

| Foodservice | |

| Retail | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Unsweetened | |

| Sweetened | ||

| By Flavor | Unflavoured | |

| Flavoured | ||

| By Packaging Type | Tetra-Pak Carton | |

| Bottle | ||

| Others | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is consumer demand for Hemp milk growing?

The category is projected to advance at a 9.35% CAGR between 2026-2031, outpacing many other plant-based beverages.

Which regions lead sales?

North America contributes the largest share at 38.96%, while Asia-Pacific will post the quickest growth at 11.65% CAGR to 2031.

Why do unsweetened variants outperform?

Low-sugar diets and barista demand for neutral bases are pushing unsweetened Hemp milk toward a 10.51% CAGR through 2031.

What packaging formats are gaining popularity?

Reusable glass bottles and paper-barrier aseptic cartons are expanding fastest because they help brands meet sustainability targets.

Page last updated on: