Tire Reinforcement Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 17.76 Billion |

| Market Size (2031) | USD 21.49 Billion |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

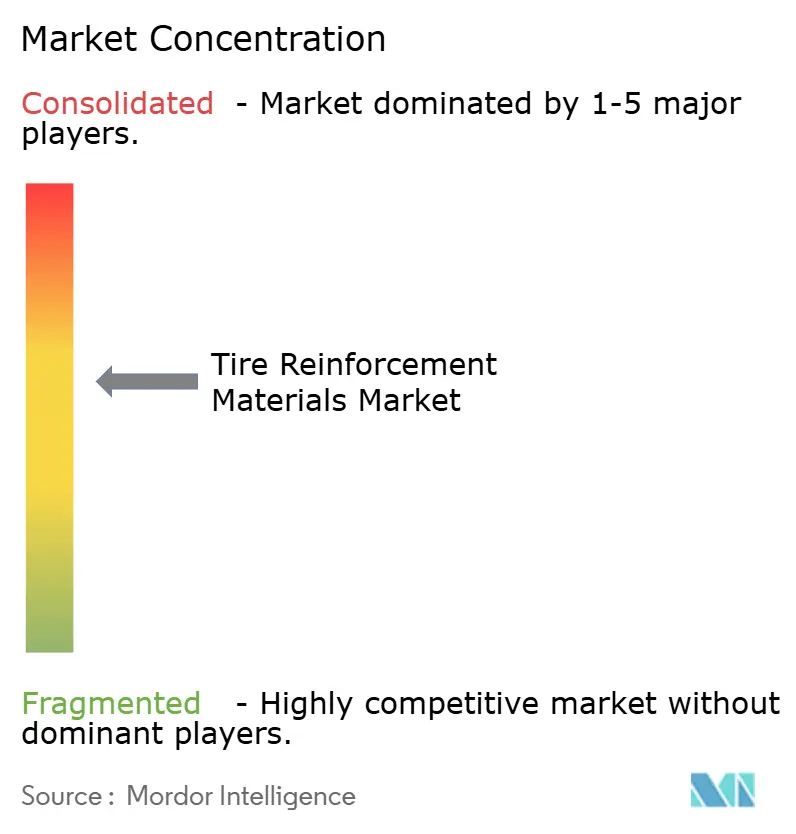

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tire Reinforcement Materials Market Analysis by Mordor Intelligence

The Tire Reinforcement Materials Market size was valued at USD 17.22 billion in 2025 and is estimated to grow from USD 17.76 billion in 2026 to reach USD 21.49 billion by 2031, at a CAGR of 3.89% during the forecast period (2026-2031). The e-commerce logistics sector in Asia-Pacific is expanding, while new safety regulations in Europe and North America, along with increasing demand for electric-vehicle (EV) tires, are driving changes in supply chains. Steel cord is experiencing renewed demand as EVs require bead wire with tensile strengths exceeding 2,800 MPa to handle higher torque loads. Concurrently, polyester and hybrid cords are strengthening their presence in two-wheeler and light-truck radial tires across India and Southeast Asia, as original equipment manufacturers (OEMs) prioritize weight reduction. Capacity expansions are being strategically located near just-in-time distribution hubs, reducing lead times from eight weeks to three. This shift is pressuring mid-tier wire-rod mills that are unable to comply with ISO 9001:2015 traceability standards. Additionally, regulatory costs are rising, with the EU Carbon Border Adjustment Mechanism increasing the landed prices of imported steel cord by up to 12%, further driving near-shoring efforts to Eastern Europe.

Key Report Takeaways

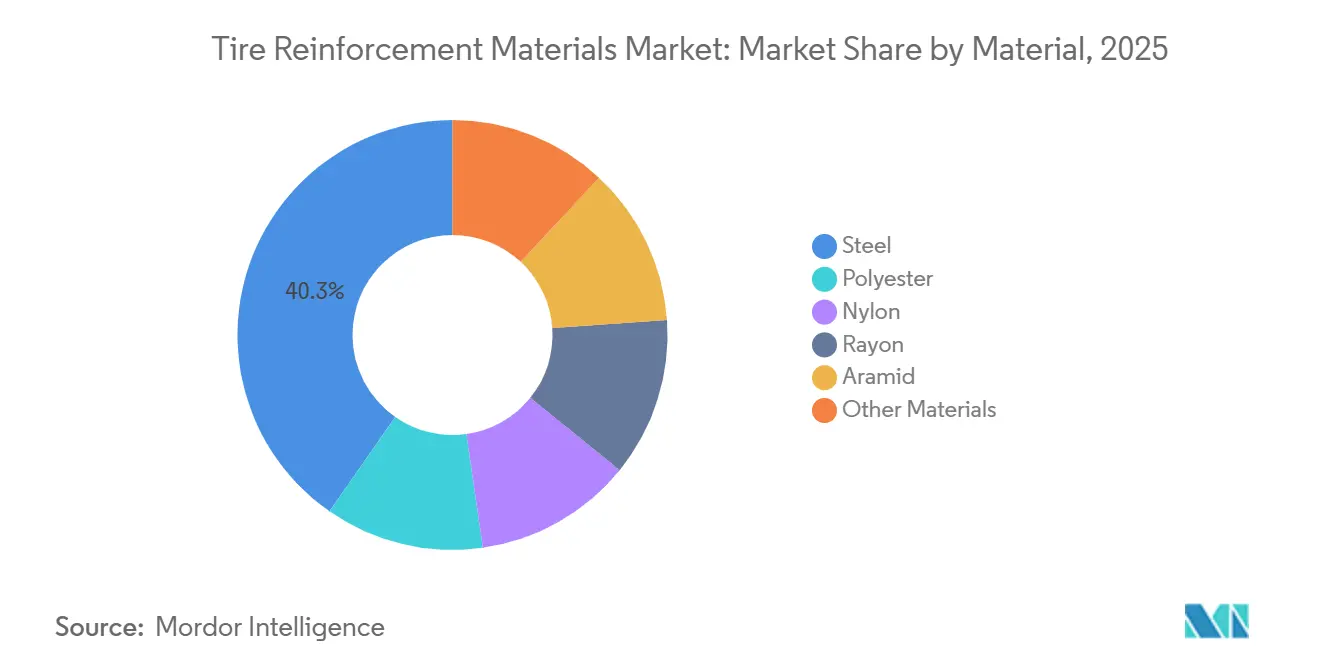

- By material, steel commanded 40.30% of the tire reinforcement materials market share in 2025 and is expected to grow at a 4.19% CAGR through 2031.

- By technology, melt spinning led with a 56.66% of the tire reinforcement materials market share in 2025 and is expected to grow at a 4.22% CAGR through 2031.

- By reinforcement type, tire bead wire held 61.11% of the tire reinforcement materials market share in 2025; tire cord fabric is projected to grow fastest at a 4.14% CAGR through 2031.

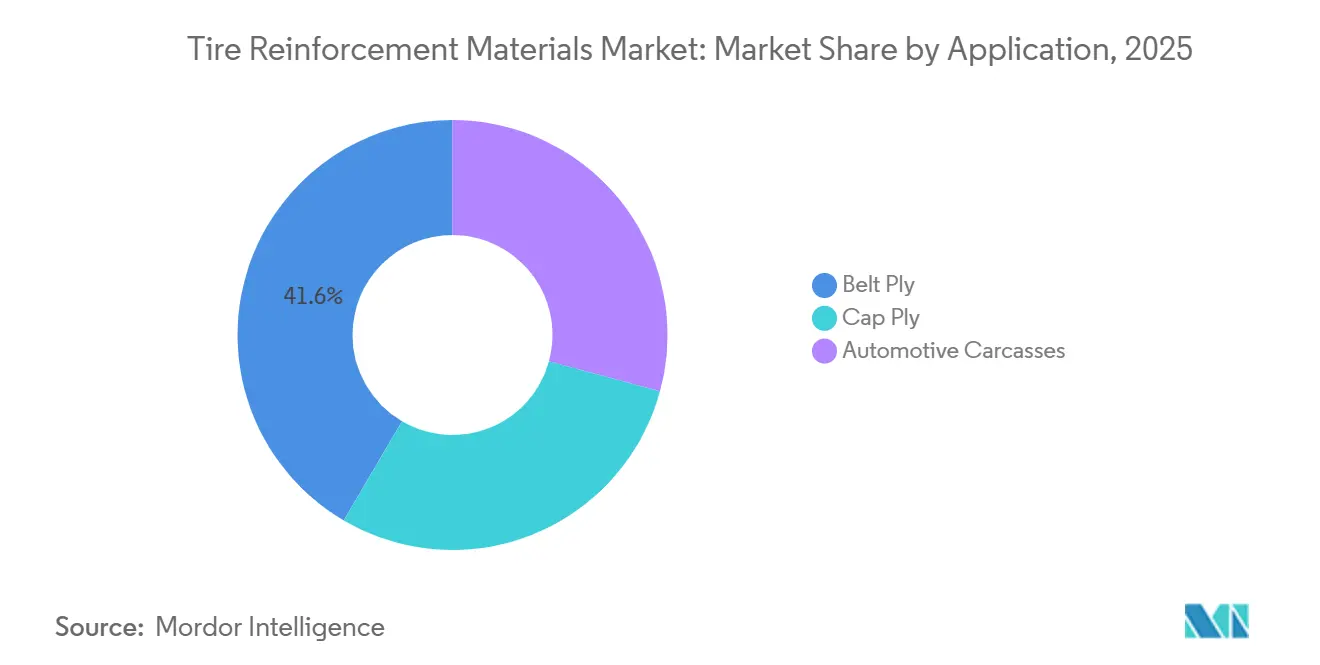

- By application, belt ply accounted for 41.57% of the tire reinforcement materials market share in 2025 and is poised to expand at a 4.36% CAGR through 2031.

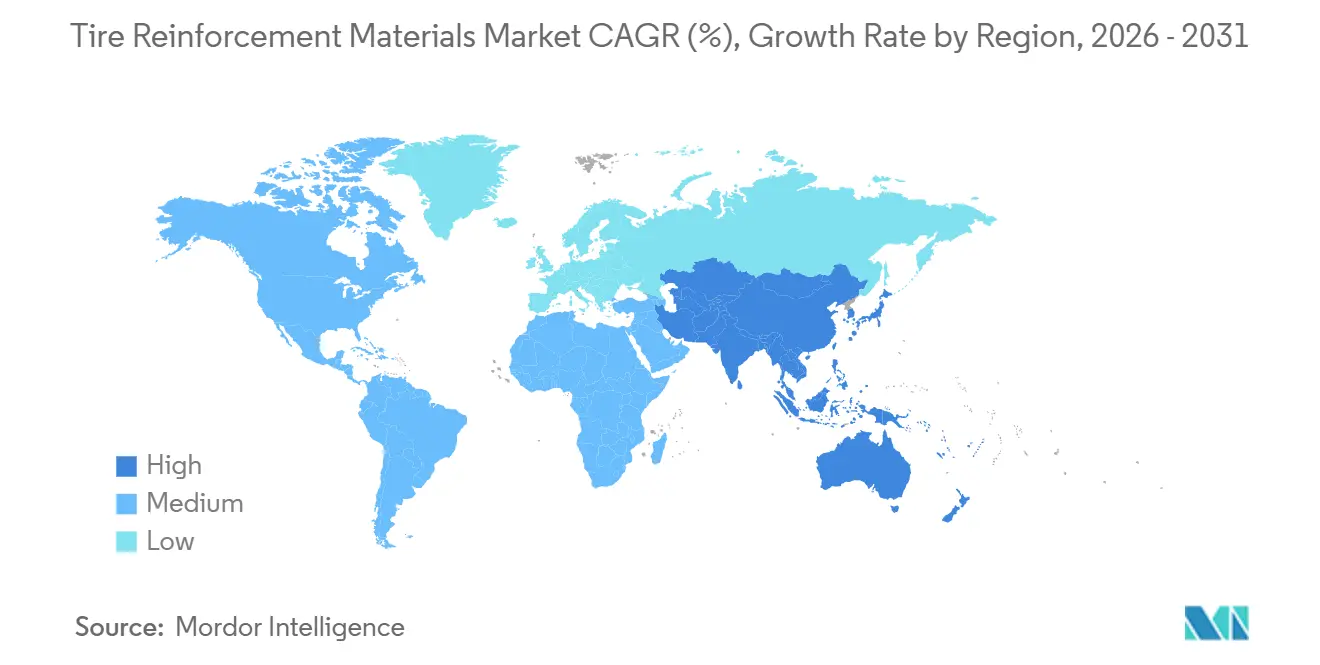

- By geography, Asia-Pacific captured 51.15% of the tire reinforcement materials market share in 2025 and is on track for the fastest regional CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tire Reinforcement Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global vehicle parc and replacement-tire demand | +1.2% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Rapid APAC e-commerce logistics boom boosting radial output | +1.5% | APAC core, spill-over to-Middle-East | Medium term (2-4 years) |

| Lightweight high-strength hybrid cords for fuel-efficiency compliance | +0.9% | Global, led by EU and China regulatory zones | Medium term (2-4 years) |

| Tire OEM shift to graphene-enhanced cords | +0.6% | North America, Europe, APAC pilot markets | Long term (≥ 4 years) |

| Safety-critical ADAS mandates elevating premium reinforcement uptake | +0.8% | Europe, North America, Japan, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Vehicle Parc and Replacement-Tire Demand

The global light-vehicle fleet exceeded 1.4 billion units in 2025, with the average vehicle age in the United States reaching 12.6 years. While older vehicles extend replacement intervals, the overall increase in vehicle numbers continues to drive demand for end-of-life tires. In China, commercial fleets added 3.2 million heavy trucks between 2023 and 2025, all equipped with radial tires featuring multi-ply steel belts. Truck tire replacement cycles, averaging 18–24 months, create consistent demand, insulating cord manufacturers from fluctuations in new-vehicle production. To enhance customer proximity, suppliers are positioning inventory in Hebei and Shandong, reducing delivery times to three weeks and gaining market share from smaller competitors with limited working capital.

Rapid APAC E-Commerce Logistics Boom Boosting Radial Output

Parcel volumes in the Asia-Pacific region reached over 150 billion units in 2025, reflecting a 22% increase from 2023. Fleet operators are transitioning from bias-ply to radial tires, which require 30%-40% more steel cord. Kolon Industries has allocated USD 20.5 million for a new polyester cord production line in Vietnam to capitalize on this trend. In India, the production-linked incentive program offers a 15% rebate on incremental cord sales, prompting companies like Century Enka and SRF Limited to expand melt-spinning capacities. Additionally, e-commerce fleets demand tighter uniformity tolerances, driving cord manufacturers to invest in USD 2 million automated tension-control winders, which raise entry barriers for smaller competitors.

Lightweight High-Strength Hybrid Cords for Fuel-Efficiency Compliance

Stricter fuel efficiency regulations, such as the EU passenger car CO₂ limit of 93.6 g/km in 2025 and China’s fleet average of 4.0 L/100 km, are pushing automakers to reduce tire rolling resistance[1]European Commission, “CO₂ Emission Performance Standards,” europa.eu. In 2024, Hyosung introduced a PET-aramid hybrid cord that reduces carcass weight by 10% and improves rolling resistance by 5%. Despite a 25%-35% price premium, automakers are adopting these cords to avoid penalties of EUR 95 per excess gram of CO₂. Advanced melt-spinning lines with co-extrusion technology have reduced scrap rates to 3%. These hybrid cords are also well-suited for electric vehicle platforms, where weight reduction is critical.

Tire OEM Shift to Graphene-Enhanced Cords

Michelin and Levidian have developed a nylon 66 cord infused with 0.3% graphene oxide, achieving a 15% reduction in rolling resistance and an 8% improvement in wet grip. Graphene’s lattice structure enhances the bond between the cord and rubber, enabling thinner belt-ply designs. However, cost remains a challenge, with graphene oxide priced at USD 200 per kg compared to USD 3 for nylon 66. Levidian aims to reduce graphene oxide costs by 50% by 2027. Meanwhile, Toray filed 12 patents between 2024 and 2025 for graphene-doped polyester cords, signaling Japanese firms’ strategic focus on nanomaterial reinforcement. If costs drop to around USD 6 per kg, graphene cords could replace aramid in ultra-high-performance tires.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (steel, nylon) | -0.9% | Global, acute in import-dependent markets | Short term (≤ 2 years) |

| Carbon-black and steel-cord plant emission caps | -0.5% | Europe, China, North America | Medium term (2-4 years) |

| Global aramid-fiber supply tightness due to defense demand | -0.4% | Global, concentrated in high-performance tire segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Steel, Nylon)

Steel wire-rod prices fluctuated between USD 650 and USD 850 per ton from 2024 to 2025, driven by reduced steel output in China and lower iron-ore shipments. Cord fabricators, operating under 3- to 6-month contracts, experienced a decline in gross margins from 18% in 2023 to 15% in 2025. Nylon 66 resin prices rose by 12% in 2025 due to reduced adipic acid production in Europe, driven by nitrous oxide emission caps, and a U.S. plant shutdown that constrained hexamethylenediamine supply. These cost pressures led to the exit of three mid-tier cord producers in India and Thailand within two years. Dual-sourcing strategies and quarterly price-adjustment clauses provide some relief but lag behind spot price movements by up to 90 days, leaving smaller firms vulnerable.

Carbon-Black and Steel-Cord Plant Emission Caps

The EU Industrial Emissions Directive of 2024 reduced particulate limits for wire-drawing plants to 10 mg/m³, necessitating investments of USD 5-8 million in electrostatic precipitators. In China, the Ministry of Ecology and Environment (MEE) mandated a 30% reduction in sulfur dioxide emissions by 2027, prompting some Hebei mills to relocate to industrial parks with shared scrubbers. Two Chinese cord plants suspended operations in 2025 pending upgrades. In the United States, the Environmental Protection Agency (EPA) imposed benzene caps on carbon-black production in 2024, increasing raw material costs for tire manufacturers by up to 9%[2]U.S. EPA, “National Emission Standards 2024,” epa.gov. These environmental compliance costs are accelerating industry consolidation, as only larger players can afford the necessary retrofits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Steel Dominates, Polyester Gains in Radial Transition

Steel contributed 40.30% of the 2025 revenue and is projected to grow at a 4.19% CAGR through 2031, surpassing the overall tire reinforcement materials market growth. This growth is attributed to the torque loads of electric vehicles, which requirebead wire capable of withstanding high tensile forces without elongation. Polyester is gaining traction in Asia's two-wheeler radial tires, where lighter cords help reduce unsprung weight. Nylon remains a niche material in aircraft and high-speed passenger tires due to its heat resistance, though its growth is constrained by adipic acid supply challenges.

Rayon is primarily used in specialty racing tires that demand low hysteresis. Aramid retains its premium position, with prices ranging between USD 12-18 per kg compared to USD 2-3 for polyester. However, the development of graphene-doped nylon cords could significantly narrow the cost gap with aramid, potentially challenging its dominance in cap-ply applications if Levidian achieves cost-reduction targets by 2027.

By Technology: Melt Spinning Leads, Solution Spinning Holds Niche

Melt spinning accounted for 56.66% of the 2025 revenue and is expected to grow at a 4.22% CAGR through 2031, as polyester and nylon manufacturers prefer its continuous extrusion process, which achieves line speeds of up to 4,000 m/min. This method consumes 20%-25% less energy than solution spinning, reducing operational costs. Multi-stage stretching, with ratios up to 8:1, remains critical for enhancing modulus.

Solution spinning, primarily used for aramid and rayon, ensures filament uniformity essential for high-modulus cords. However, its capital costs, ranging from USD 40-50 million, are more than double those of melt-spinning lines. Japanese manufacturers like Toray operate eight melt-spinning lines, producing polyester cords with tenacity exceeding 8.5 g/denier. In-line heat setting has become standard, reducing shrinkage during curing to below 1% and meeting ISO 23671 uniformity standards.

By Reinforcement Type: Bead Wire Anchors, Cord Fabric Accelerates

Tire bead wire accounted for 61.11% of the 2025 revenue, driven by its role in securing tires to rims against radial forces exceeding 20 tons. Its growth aligns with the increasing adoption of wider rim diameters in electric vehicles. Tire cord fabric is projected to grow at a 4.14% CAGR through 2031, supported by the rising use of multi-ply belts for stress distribution.

Bead-wire production requires 12-15 drawing passes to achieve 0.9 mm diameters, creating a capital-intensive barrier that benefits large players like Bekaert. The expansion of cord fabric is fueled by the relocation of tire assembly plants to ASEAN countries. For instance, Indorama Ventures' new facility in Thailand increased regional output by 15,000 tons annually. Automated looms with real-time defect detection have reduced scrap rates from 5% to 2%, prompting smaller weaving companies to consider consolidation.

By Application: Belt Ply Leads Growth, Carcass Demand Steady

Belt ply accounted for 41.57% of the 2025 revenue and is expected to grow at a 4.36% CAGR through 2031, the highest among applications. This growth is attributed to the braking demands of advanced driver-assistance systems (ADAS), which require stable tread blocks during high deceleration. Two- or four-layer steel or hybrid belts, oriented at approximately 20°, reduce irregular wear and extend tread life by 10,000 km.

Cap ply, primarily composed of nylon and aramid layers, prevents belt-edge separation at speeds exceeding 200 km/h. Electric vehicle platforms favor high-modulus belts, with innovations like Michelin's single-ply hybrid design reducing belt weight by 18% without compromising strength. Truck fleets increasingly specify cap plies to mitigate zipper ruptures, contributing to Kordsa's 25% share of the European premium truck tire market.

Geography Analysis

Asia-Pacific contributed 51.15% of the 2025 revenue and is projected to grow at a 4.62% CAGR through 2031, the fastest among all regions. China's Stage VI emission regulations for trucks in 2027 are driving demand for low-rolling-resistance tires with hybrid cords, reducing fuel consumption by 5%. India's USD 85 million SRF melt-spinning plant, commissioned in 2025, has reduced reliance on imports from Thailand and China. Kolon's USD 20.5 million investment in Vietnam highlights the region's growth potential.

In North America, the USMCA's 75% content rule has incentivized bead-wire production in Mexico and the southern United States. However, rising carbon-black prices, up 9% due to EPA benzene caps, have pressured margins. In Europe, CO₂ fines are pushing OEMs toward lightweight cords, with Germany, the UK, Italy, and France leading in aramid cap-ply adoption. Russia has turned to Turkish and Indian wire-rod suppliers due to sanctions. CBAM levies have increased Asian cord costs by up to 12%, prompting capacity shifts to Poland and Romania. In South America, Brazil dominates, while the Middle-East and Africa see demand driven by mining and agriculture in Saudi Arabia and South Africa.

Competitive Landscape

The tire reinforcement materials market is moderately concentrated, with the top five players, including Bekaert, Hyosung Advanced Materials, Kordsa, Michelin, and Jiangsu Xingda Steel Cord Co., Ltd, accounting for approximately 56% of the 2025 capacity. Vertical integration provides a competitive edge, as seen with Bekaert, which owns eight wire-rod mills, insulating it from steel price volatility. In January 2026, Bekaert invested EUR 60 million to acquire Bridgestone's cord plants in China and Thailand, adding 120,000 tons of annual capacity.

Hyosung is considering a USD 1 billion sale of its steel-cord unit to focus on aramid and carbon fiber. Kordsa increased European shipments by 28% following ADAS-driven aramid demand. Indorama Ventures expanded its Thai polyester cord fabric capacity by 15,000 tons per year in 2025 to support logistics fleets. Kolon's investment in Vietnam positions it for growth in Southeast Asia.

Technological advancements are reshaping the competitive landscape. Michelin and Levidian's graphene-doped nylon proof-of-concept could redefine performance benchmarks if costs drop below USD 6 per kg by 2027. Automated tension-control winders and inline camera systems have raised the minimum efficient scale to 20,000 tons per year, pressuring smaller plants to consolidate or exit. A European consortium's 2024 patent for end-of-life tire pyrolysis offers recycled steel and polyester feedstock at 60% of virgin costs but requires USD 50-80 million for commercialization.

Tire Reinforcement Materials Industry Leaders

Bekaert

HS HYOSUNG ADVANCED MATERIALS

Michelin

Jiangsu Xingda Steel Cord Co., Ltd

Kordsa Teknik Tekstil A.Ş.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bekaert acquired the tire reinforcement business from Bridgestone in China and Thailand, strengthening its market position. The agreement included a long-term supply arrangement and the transfer of two captive tire cord manufacturing facilities from Bridgestone.

- October 2025: Continental AG expanded its use of recycled steel and polyester derived from PET, aiming to incorporate over 40% renewable or recycled materials in tire production by 2030. The company’s strategy involved utilizing sustainable materials such as silica sourced from rice husk ash and synthetic rubber produced from bio-based feedstocks, with a long-term objective of achieving 100% sustainable materials by 2050.

Global Tire Reinforcement Materials Market Report Scope

Tire reinforcement materials, such as steel, polyester, nylon, rayon, and aramid, are essential components embedded in rubber to ensure structural integrity, durability, and shape retention.

The tire reinforcement materials market is segmented by material, technology, reinforcement type, application, and geography. By material, the market is segmented into steel, polyester, nylon, rayon, aramid, and other materials. By technology, the market is segmented into melt spinning, drawing, and solution spinning. By reinforcement type, the market is segmented into tire bead wire and tire cord fabric. By application, the market is segmented into belt ply, cap ply, and automotive carcasses. The report also covers the market size and forecasts for tire reinforcement materials in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Steel |

| Polyester |

| Nylon |

| Rayon |

| Aramid |

| Other Materials |

| Melt Spinning |

| Drawing |

| Solution Spinning |

| Tire Bead Wire |

| Tire Cord Fabric |

| Belt Ply |

| Cap Ply |

| Automotive Carcasses |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material | Steel | |

| Polyester | ||

| Nylon | ||

| Rayon | ||

| Aramid | ||

| Other Materials | ||

| By Technology | Melt Spinning | |

| Drawing | ||

| Solution Spinning | ||

| By Reinforcement Type | Tire Bead Wire | |

| Tire Cord Fabric | ||

| By Application | Belt Ply | |

| Cap Ply | ||

| Automotive Carcasses | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the tire reinforcement materials market?

The tire reinforcement materials market size stands at USD 17.76 billion in 2026 and is projected to reach USD 21.49 billion by 2031.

How fast is the market expected to grow through 2031?

Between 2026 and 2031, the market is projected to post a 3.89% CAGR.

Which region leads in demand for tire reinforcement materials in 2025?

Asia-Pacific held 51.15% of 2025 revenue and shows the fastest regional CAGR at 4.62% through 2031.

Which material segment has the highest market share in 2025?

Steel dominated with 40.30% share in 2025 because of its critical role in radial truck and passenger-car tires.

Page last updated on: