Hydrogenated Nitrile Butadiene Rubber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

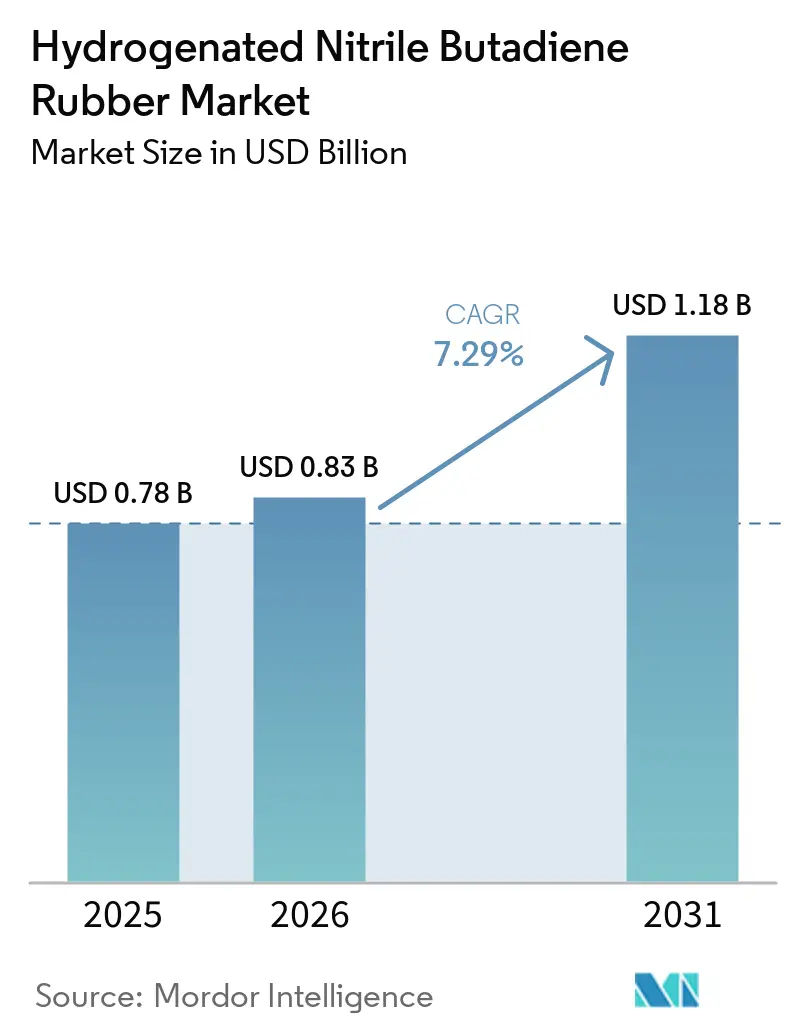

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.18 Billion |

| Growth Rate (2026 - 2031) | 7.29% CAGR |

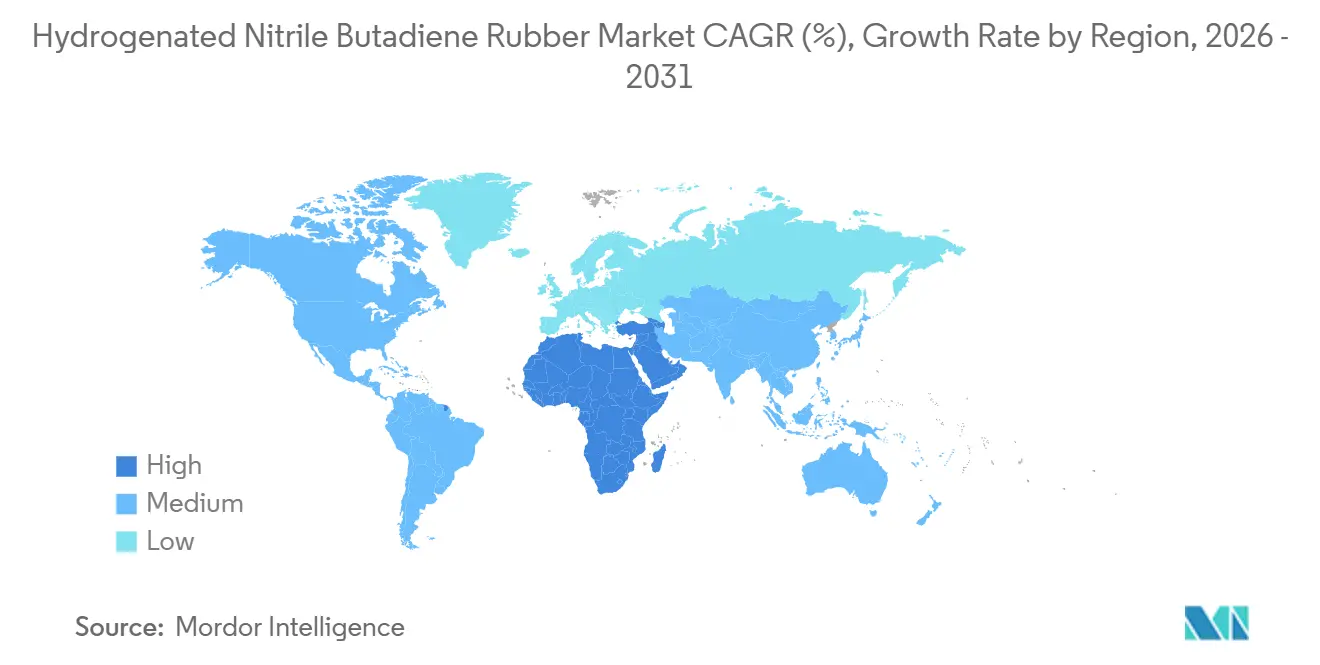

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrogenated Nitrile Butadiene Rubber Market Analysis by Mordor Intelligence

The Hydrogenated Nitrile Butadiene Rubber Market size is projected to grow from USD 0.78 billion in 2025 to USD 0.83 billion in 2026, and reach USD 1.18 billion by 2031, growing at a CAGR of 7.29% from 2026 to 2031. Intensifying demand for specialized seals in hybrid and battery-electric powertrains, together with higher-temperature drilling and carbon-capture activity, sustains a multi-year expansion cycle. Automakers are redesigning thermal-management circuits for next-generation refrigerants, narrowing the cost-performance gap between hydrogenated nitrile butadiene rubber and fluoroelastomers. Oil and gas operators are now targeting downhole zones exceeding 200 °C, where standard nitrile rubber rapidly degrades yet hydrogenated nitrile butadiene rubber maintains mechanical integrity, especially in sour-gas environments. On the supply side, new capacity in Changzhou and lower-cost Chinese units pressure Western incumbents, but advanced oxidation processes that cut emissions by 80% defend premium pricing in sustainability-sensitive tenders.

Key Report Takeaways

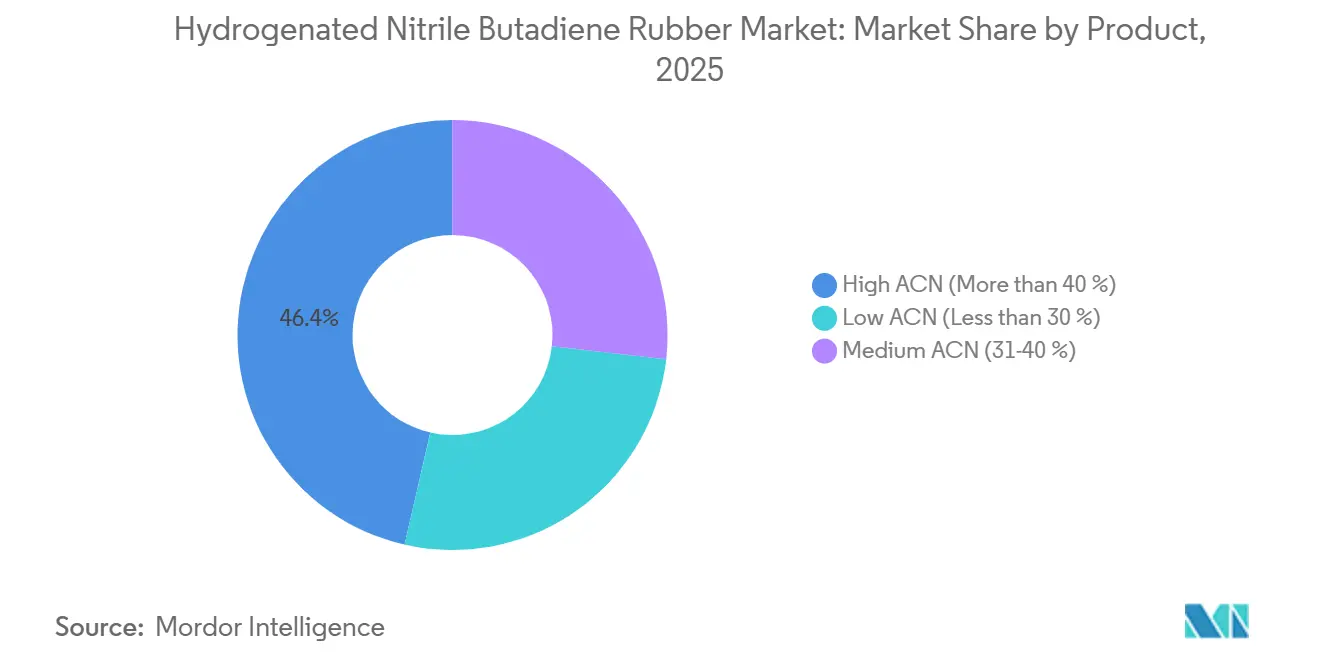

- By product category, high-acrylonitrile grades led with 46.42% revenue share in 2025, while low-ACN variants are projected to expand at an 8.56% CAGR through 2031.

- By application, seals and gaskets accounted for a 37.25% share of the hydrogenated nitrile butadiene rubber market size in 2025, whereas hoses and tubing are advancing at an 8.32% CAGR to 2031.

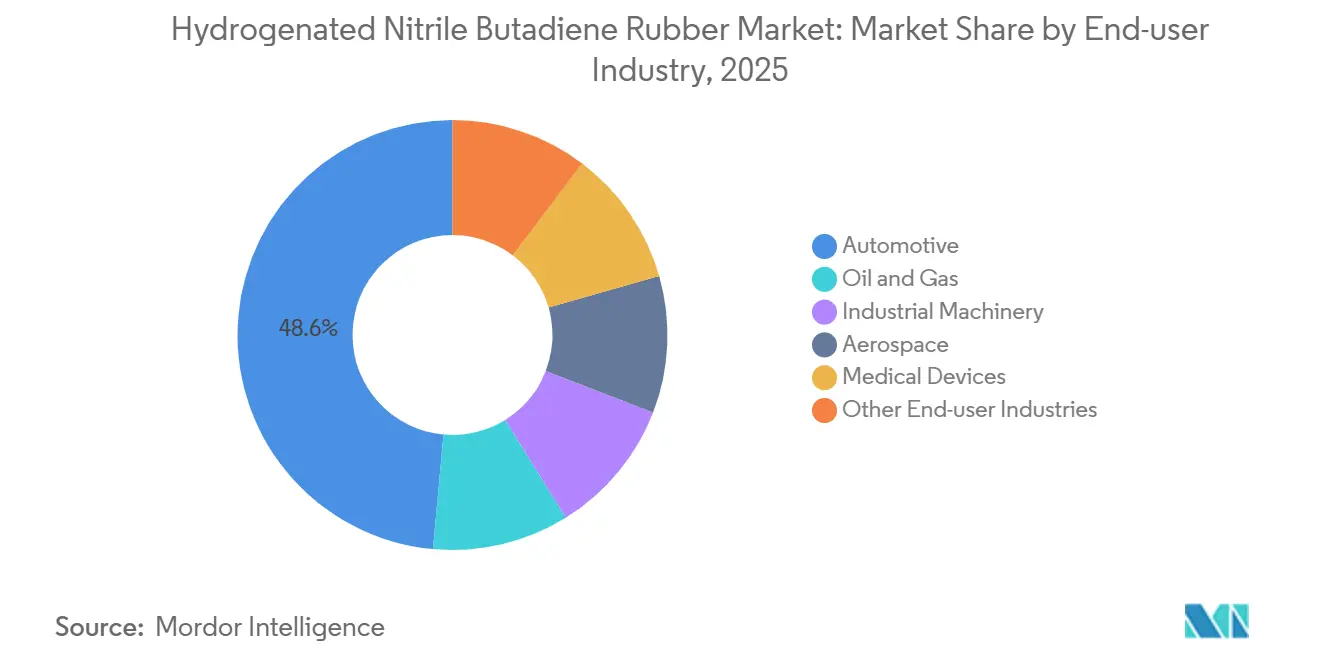

- By end-user industry, automotive held 48.55% of the hydrogenated nitrile butadiene rubber market share in 2025; medical devices recorded the highest projected CAGR at 8.74% through 2031.

- By geography, Asia-Pacific led with 42.18% share of the hydrogenated nitrile butadiene rubber market in 2025; the Middle East and Africa region is projected to register the highest CAGR of 8.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hydrogenated Nitrile Butadiene Rubber Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand from advanced ICE and hybrid seals | +1.8% | Global, APAC core, spillover to North America | Medium term (2-4 years) |

| Oil and gas deep-well elastomer needs >200 °C | +1.5% | Middle East and Africa, North America shale basins | Long term (≥4 years) |

| Breakthrough peroxide-cured low-temperature grades | +1.3% | Europe and North America cold-climate markets | Short term (≤2 years) |

| Replacement of FKM in cost-sensitive EV loops | +1.6% | APAC (China, South Korea), Europe | Medium term (2-4 years) |

| Ultra-deep geothermal drilling requirements | +1.1% | Global, early adoption in Iceland and East Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Demand From Advanced ICE and Hybrid Powertrain Seals

Hybrid platforms prolong internal-combustion relevance while imposing harsher duty cycles on timing belts, crankshaft seals, and turbocharger gaskets. Hydrogenated nitrile butadiene rubber resists ozone cracking and thermal oxidation better than conventional nitrile, thereby extending service intervals and lowering warranty costs. China shipped 723,000 new-energy vehicles in February 2026, including 246,000 plug-in hybrids that continue to rely on oil-resistant elastomers[1]China Passenger Car Association, “Wholesale New Energy Vehicle Sales February 2026,” cpcaauto.com.cn. Suppliers certified to IATF 16949 now export hydrogenated nitrile butadiene rubber timing belts worldwide, and demand for low-friction coatings builds a secondary market for specialty adhesion-optimized compounds. Processing gains—such as laser-etched tooth surfaces bonded with peroxide-cured compounds—further entrench the material in propulsion systems as hybrid volumes plateau.

Oil and Gas Deep-Well Elastomer Demands greater than 200 °C

Ultra-deep wells expose seals to 200 °C temperatures, 150 bar pressure, and hydrogen-sulfide levels above 10%. Trelleborg’s XploR H9T20 grade, certified under NORSOK M-710, withstands rapid gas decompression inside subsea blowout preventers. Field tests show high-ACN hydrogenated nitrile butadiene rubber maintains hardness after 30 days in 16% H₂S, outperforming standard nitrile. Occidental’s Brown Pelican CO₂-sequestration well in Texas specifies hydrogenated nitrile butadiene rubber packers, signaling that carbon-capture will mirror oil-field material standards. Tool string manufacturers now quote premium-priced peroxide-cured stators for positive-displacement motors, citing 20% longer run time before elastomer extrusion.

Breakthrough Peroxide-Cured Low-Temperature Grades

Traditional sulfur-cured hydrogenated nitrile butadiene rubber reaches its glass transition near –20 °C, limiting use in Arctic pipelines. Recent pendant-vinyl chemistry pushes Tg to −40 °C while preserving a tensile strength of 25.8 MPa. Eliminating sulfur bloom also improves compression set at 150 °C, opening transmission and e-axle seals that experience sub-zero parking and 120 °C operating swings. Versalis introduced BALANCE bio-attributed grades with up to 90% smaller carbon footprints, gaining rapid automotive validation under ISCC PLUS certification. The technical leap erodes fluoroelastomer incumbency in cold-start environments while satisfying OEM sustainability scorecards.

Rising Replacement of FKM in Cost-Sensitive EV Thermal Loops

Battery-cooling circuits circulate water-glycol mixtures from −40 °C to 100 °C under elevated pressure. Fluoroelastomers meet the duty but at two-to-three times the polymer cost. Freudenberg’s injection-moldable hydrogenated nitrile butadiene rubber delivers a tenfold improvement in helium leak rate, enabling IP67 battery housings without fluorinated materials. Formulations stable in R1234yf refrigerant allow cost reduction in mass-market EVs where bill-of-materials pressure is acute. Regulatory momentum around PFAS restrictions further accelerates the switch, with DuPont explicitly listing hydrogenated nitrile butadiene rubber as a non-fluorinated alternative in its 2024 dossier.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium versus conventional rubber | −0.8% | Global, strongest in price-sensitive APAC | Short term (≤2 years) |

| Processing complexity and filler limits | −0.6% | Global manufacturing hubs | Medium term (2-4 years) |

| Regulatory shift toward bio-based polymers | −0.5% | Europe and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Price Premium Versus Conventional Elastomers

Hydrogenated nitrile butadiene rubber sells for USD 4.00 per kg in North America, roughly 60% above standard nitrile rubber, driven by hydrogenation reactor capital cost and high-purity acrylonitrile feedstock volatility. Spot butadiene moved 0.8% month-on-month in March 2026, complicating annual contract negotiations. Integrated Chinese sites, such as Qilu Petrochemical, siphon low-cost feedstocks from adjacent crackers, exporting at prices that erode Western margins. Consequently, industrial machinery OEMs often default to cheaper polyurethane unless the failure risk justifies premium material spend.

Processing Complexity and Filler Compatibility Limits

A saturated backbone resists sulfur vulcanization, forcing peroxide cures that require tighter mold-temperature control and longer cycles. Dispersion of silica or carbon black demands surface-modified fillers; otherwise, agglomerates degrade low-temperature flexibility. Trials replacing 30% of virgin N330 carbon black with recycled material maintained tensile strength, yet higher substitution led to premature crosslink scission during aging. Smaller molders struggle with peroxide residue migration, which can corrode sensitive electronics in over-molded sensor housings, exposing them to warranty risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Performance Split Between High and Low ACN Grades

High-ACN grades captured 46.42% of 2025 revenue, cementing their role in fuel systems, hydraulic cylinders, and oil-field blowout preventers where aggressive hydrocarbon exposure necessitates maximum polarity. Medium-ACN formulations balance oil resistance and processability across general-purpose seals. Low-ACN variants, boosted by pendant-vinyl functionalization, are forecast to grow at an 8.56% CAGR through 2031 because peroxide-cured chemistries now unlock glass-transition points near −40 °C, a realm once reserved for fluoroelastomers.

High-ACN compounds comply with NORSOK M-710 for sour-gas wellheads, while medium-ACN gains share in EV coolant hoses where glycol compatibility is critical. Versalis BALANCE low-ACN hydrogenated nitrile butadiene rubber provides OEMs a route to meet recycled-content mandates without sacrificing performance. Recycled-carbon-black programs remain experimental; above 30% filler substitution, peroxide-cure density drops, constraining circular-economy claims until dispersion technology improves.

By Application: Seals Dominate, Hoses Accelerate on EV Cooling

Seals and gaskets delivered 37.25% of 2025 sales as crankshaft seals, hydraulic O-rings, and wellhead gaskets specify high-ACN hydrogenated nitrile butadiene rubber for chemical and thermal resilience. The segment benefits from FDA compliance in pharmaceutical processing seals, widening its industrial reach. Hoses and tubing are projected to outpace at an 8.32% CAGR during 2026-2031because EV batteries require glycol-compatible elastomers that tolerate temperature cycling from −40 °C to 100 °C.

Timing belts reinforce demand by bonding peroxide-cured compounds onto aramid cords for hybrid engines. Wire-and-cable insulation remains niche but strategic in subsea umbilicals and geothermal logging, where hydrogenated nitrile butadiene rubber shields conductors against hydrocarbon ingress. Although polyurethane outperforms in abrasion, hydrogenated nitrile butadiene rubber retains a share where oil resistance outweighs wear metrics.

By End-User Industry: Automotive Anchors, Medical Devices Surge

Automotive captured 48.55% of 2025 revenue as hybrid and plug-in models prioritize oil-resistant seals and R1234yf-ready hoses. China’s February 2026 wholesale deliveries show BYD at 187,782 units and Geely at 117,488 units, evidence that battery-electric and hybrid growth jointly underpin elastomer demand.

Medical devices are expected to post an 8.74% CAGR to 2031 as minimally invasive instruments and bioprocess gaskets adopt FDA-compliant hydrogenated nitrile butadiene rubber, which withstands repeated steam sterilization M-SEALS.DK. Oil and gas, industrial machinery, and aerospace remain critical secondary sectors, each valuing the material’s balance of heat, oil, and compression-set performance.

Geography Analysis

Asia-Pacific generated 42.18% of 2025 revenue, driven by China’s vehicle output and integrated petrochemical capacity. ARLANXEO launched a USD 210 million Changzhou line in February 2026, adding 5,000 tons/year via an oxidation process that cuts emissions by 80%. Chinese producers like Qilu Petrochemical achieve ≥99% hydrogenation conversion, offering lower pricing that pressures Western incumbents[2]Sinopec Chemical Federation, “Qilu Petrochemical HNBR Unit Commissioning,” cpif.org.cn. India’s machinery export growth is limited due to its limited domestic production.

North America and Europe split a significant share, supported by stringent emissions rules and mature drilling activity. ARLANXEO’s Orange, Texas, and Leverkusen, Germany sites form a resilient supply chain, while Zeon’s 4,400-tone U.S. plant feeds automotive demand despite postponed expansion amid permitting delays. Bio-attributed hydrogenated nitrile butadiene rubber gains traction in Europe as OEMs target higher recycled-content quotas. Shale and offshore operators in the Gulf of Mexico specify NORSOK-compliant seals for hydrogen-sulfide zones.

The Middle East and Africa are forecast to grow 8.21% annually to 2031. East African Rift geothermal drilling and Arabian Gulf offshore platforms require high-temperature elastomers, while emerging carbon-capture projects adopt oil-field sealing standards. Latin America remains smaller; Brazil’s automotive sector and Argentina’s shale play add incremental volumes yet rely on imports.

Competitive Landscape

Hydrogenated nitrile butadiene rubber market is moderately consolidated. ARLANXEO’s Changzhou plant validates Asia-centric expansion strategies while satisfying corporate sustainability metrics through wastewater-free operations. Zeon continues rationalizing commodity lines to prioritize specialty rubbers, yet U.S. permitting obstacles delay a 7,500-ton capacity boost.

Innovation focus now centers on bio-attributed products and process advances. Versalis BALANCE elastomers supply ISCC PLUS-certified renewable content, securing early automotive approvals. Freudenberg demonstrates that injection molding can deliver tenfold leakage improvements in battery enclosures, strengthening hydrogenated nitrile butadiene rubber’s position against lower-priced fluoroelastomer alternatives. Chinese entrants such as Qilu Petrochemical leverage co-located crackers to compress feedstock costs, enabling export offers that reshape global price floors.

Hydrogenated Nitrile Butadiene Rubber Industry Leaders

ARLANXEO

ZEON CORPORATION

Denka Company Limited

LG Chem

JSR Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: ARLANXEO inaugurated a new Changzhou unit with 5,000 t/y HNBR capacity, investing USD 210 million and deploying oxidation technology that cuts carbon emissions by 80%.

- March 2024: DuPont filed a PFAS-restriction dossier, naming hydrogenated nitrile butadiene rubber as a non-fluorinated substitute for selected sealing duties.

Global Hydrogenated Nitrile Butadiene Rubber Market Report Scope

Hydrogenated Nitrile Butadiene Rubber is a high-performance synthetic elastomer derived from hydrogenating NBR (Nitrile Butadiene Rubber) to saturate its polymer backbone. It delivers superior resistance to heat, chemicals, and oils, along with high tensile strength and durability, making it suitable for applications such as automotive belts, oilfield seals, and dynamic sealing components.

The Hydrogenated Nitrile Butadiene Rubber market is segmented by product, application, and end-user industry. By product, the market is segmented into low ACN (less than 30%), medium ACN (31-40%), and high ACN (more than 40%). By application, the market is segmented into seals and gaskets, O-rings, hoses and tubing, belts (timing, auxiliary), wire and cable insulation, and rollers and others. By end-user industry, the market is segmented into automotive, oil and gas, industrial machinery, aerospace, medical devices, and other end-user industries. The report also cover the market size and forecasts for the hydrogenated nitrile butadiene rubber market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Low ACN (Less than 30%) |

| Medium ACN (31-40%) |

| High ACN (More than 40%) |

| Seals and Gaskets |

| O-Rings |

| Hoses and Tubing |

| Belts (Timing, Auxiliary) |

| Wire and Cable Insulation |

| Rollers and Others |

| Automotive |

| Oil and Gas |

| Industrial Machinery |

| Aerospace |

| Medical Devices |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East |

| By Product | Low ACN (Less than 30%) | |

| Medium ACN (31-40%) | ||

| High ACN (More than 40%) | ||

| By Application | Seals and Gaskets | |

| O-Rings | ||

| Hoses and Tubing | ||

| Belts (Timing, Auxiliary) | ||

| Wire and Cable Insulation | ||

| Rollers and Others | ||

| By End-user Industry | Automotive | |

| Oil and Gas | ||

| Industrial Machinery | ||

| Aerospace | ||

| Medical Devices | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the 2026 value of the hydrogenated nitrile butadiene rubber market?

The hydrogenated nitrile butadiene rubber market size stands at USD 0.83 billion in 2026.

Which product grade dominates sales?

High-acrylonitrile grades hold 46.42% of 2025 revenue owing to superior hydrocarbon resistance.

Where is demand growing fastest geographically?

The Middle East and Africa are projected to expand at an 8.21% CAGR through 2031.

Why are EV makers shifting from fluoroelastomers?

Injection-moldable hydrogenated nitrile butadiene rubber cuts material cost while meeting IP67 battery housing leak standards.

How are suppliers reducing carbon footprints?

New oxidation processes and bio-attributed grades like Versalis BALANCE deliver up to 90% lower lifecycle emissions.

Page last updated on: