Gastrointestinal (GI) Stool Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

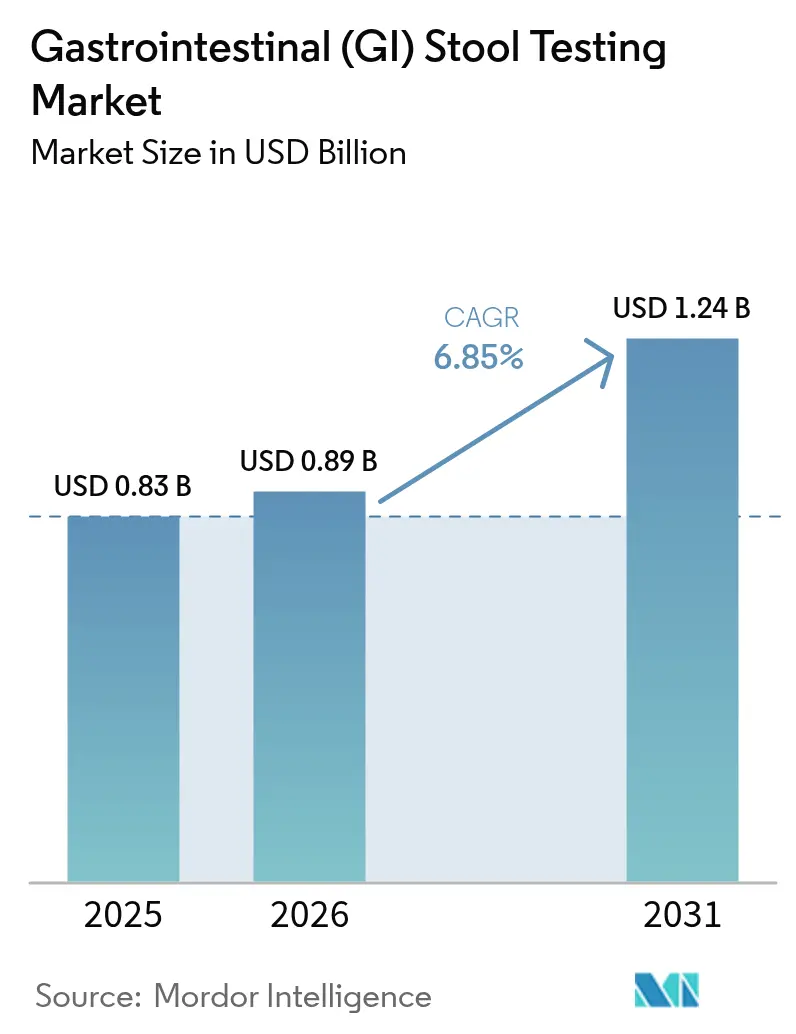

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.24 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gastrointestinal (GI) Stool Testing Market Analysis by Mordor Intelligence

The gastrointestinal (GI) stool testing market size in 2026 is estimated at USD 0.89 billion, growing from 2025 value of USD 0.83 billion with 2031 projections showing USD 1.24 billion, growing at 6.85% CAGR over 2026-2031. Expanding reimbursement for multi-target stool DNA tests, rapid uptake of point-of-care immunochemical assays and broader adoption of multiplex PCR panels are enlarging the overall test pool while sustaining double-digit volume growth across both developed and emerging regions. Suppliers of consumables gain recurring revenue as laboratories automate preprocessing and as home-collection kits proliferate under telehealth programs. Meanwhile, viral pathogen detection and metagenomic sequencing broaden test menus, allowing providers to bundle screening for cancer, infection and microbiome status in a single sample run. Competitive intensity escalates as large diagnostics groups use acquisitions and financing rounds to secure molecular capabilities, regulatory expertise and direct-to-consumer channels that expand brand loyalty within the fast-evolving gastrointestinal (GI) stool testing market.

Key Report Takeaways

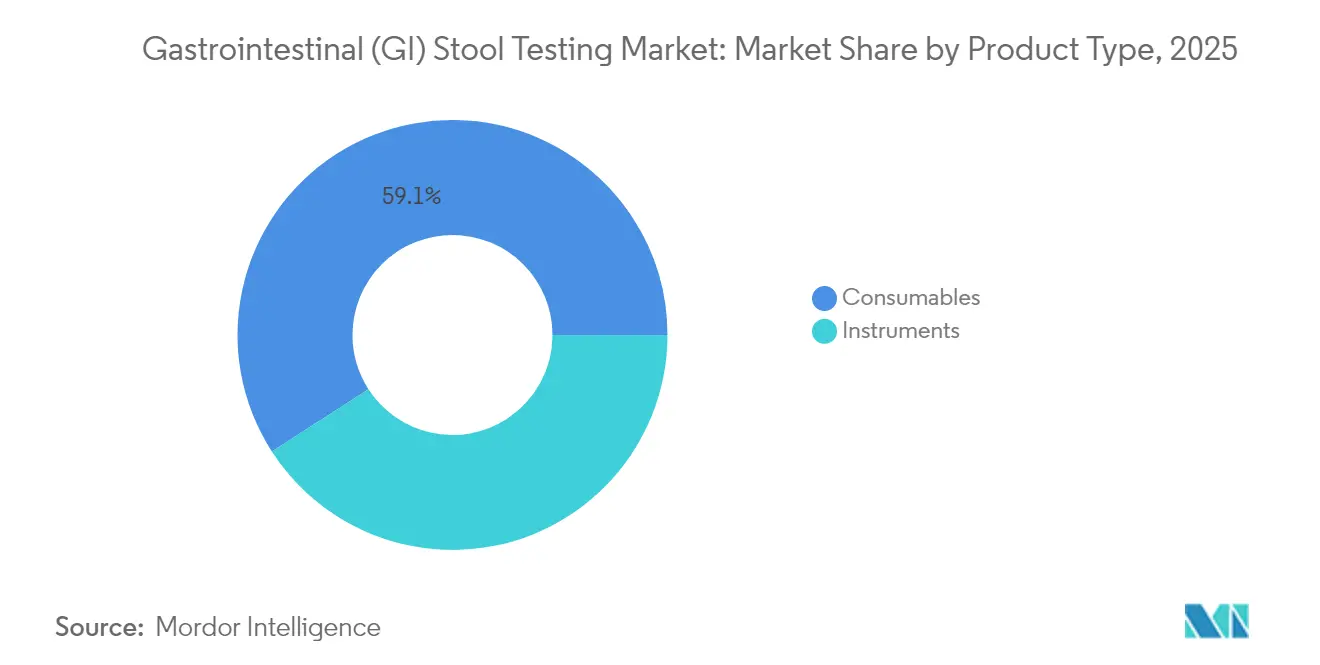

- By product type, consumables captured 59.12% of the gastrointestinal (GI) stool testing market share in 2025; the segment is projected to rise at a 7.32% CAGR through 2031.

- By test type, occult blood tests held 40.75% of revenue in 2025, while viral pathogen panels are set to grow the fastest at 7.26% CAGR.

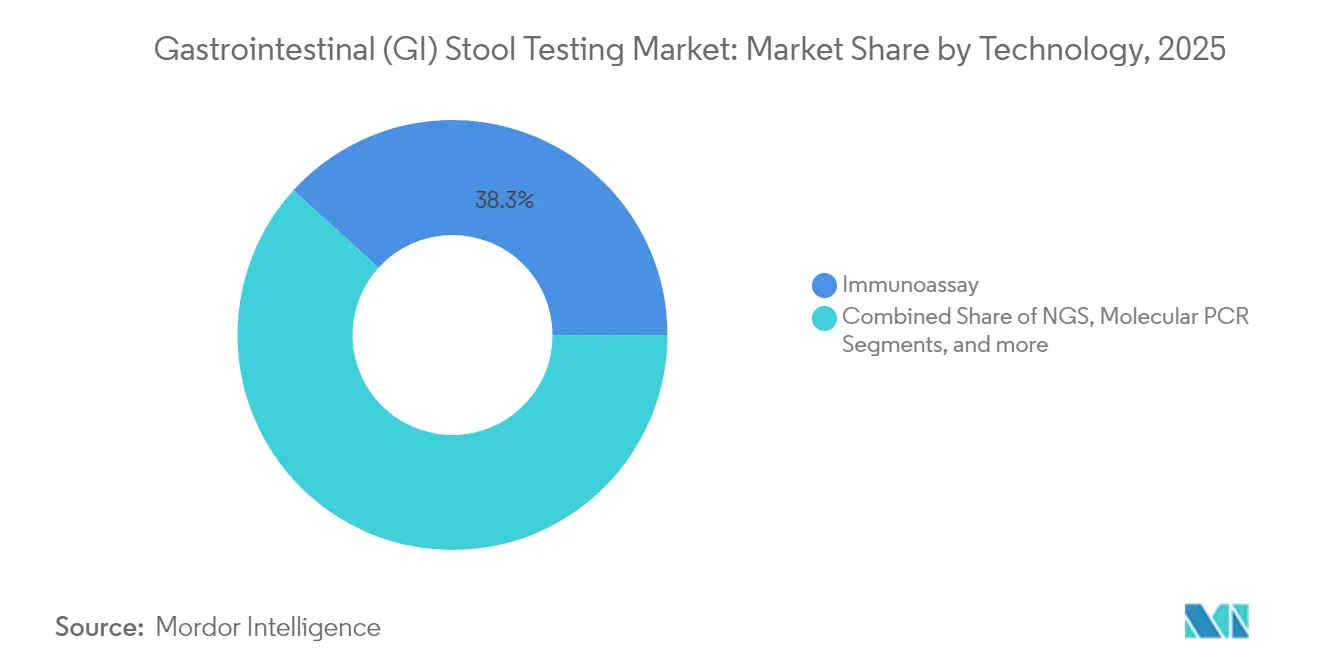

- By technology, immunoassays led with 38.25% revenue in 2025, whereas next-generation sequencing is forecast to accelerate at a 7.41% CAGR.

- By end user, diagnostic laboratories retained 35.02% revenue in 2025, yet physician offices and point-of-care sites will expand the quickest at 7.29% CAGR.

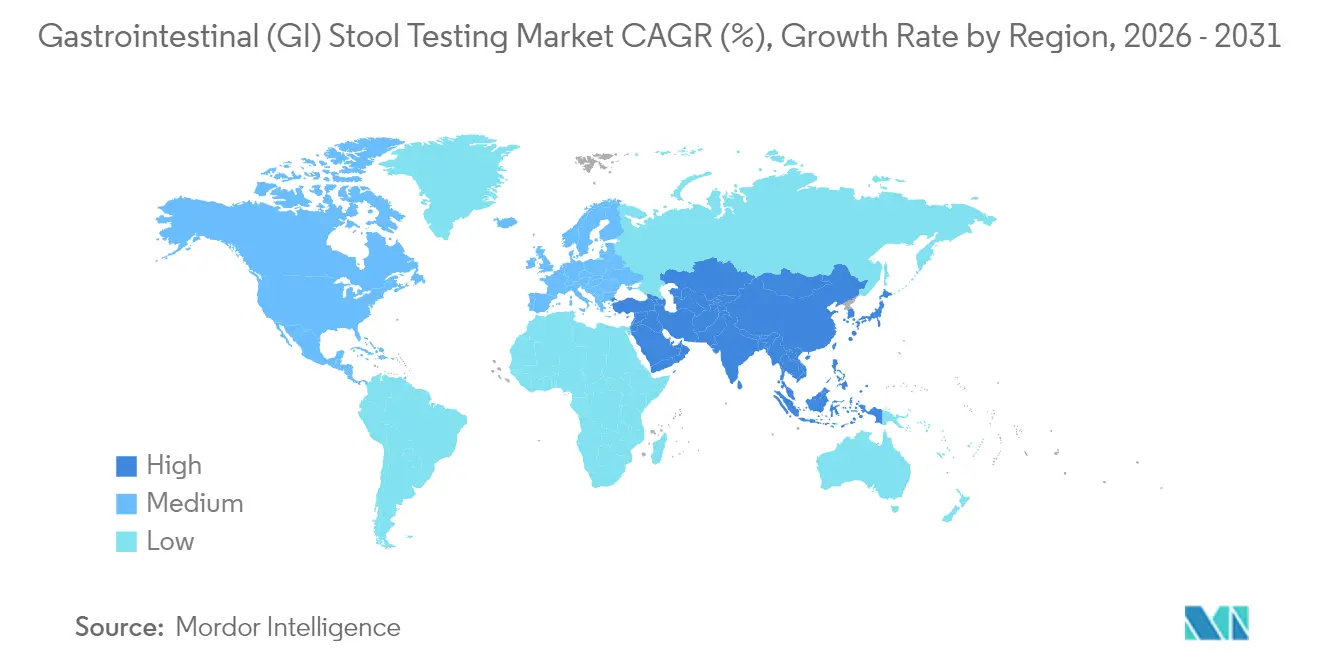

- By region, North America generated 39.08% of revenue in 2025, but the Asia-Pacific region is poised for the fastest 7.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gastrointestinal (GI) Stool Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of GI disorders & CRC screening mandates | +1.8% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Point-of-care FIT/iFOBT adoption surge | +1.2% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Expansion of molecular enteric-pathogen panels | +1.5% | Global, led by developed markets | Medium term (2-4 years) |

| Growth of at-home collection & telehealth integration | +1.1% | North America core, expanding to APAC | Short term (≤ 2 years) |

| Payer coverage for microbiome-based diagnostics | +0.9% | National, with early gains in US, Germany, Japan | Long term (≥ 4 years) |

| AI-enabled stool-image analytics for triage | +0.6% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of GI disorders & CRC screening mandates

Lowering the US colorectal-cancer screening age to 45 instantly added 19 million eligible adults, swelling the overall screening cohort to 117.1 million. Medicare now reimburses multi-target stool DNA tests every three years for average-risk beneficiaries, eliminating out-of-pocket cost barriers when providers accept assignment[2]Centers for Medicare & Medicaid Services, “Local Coverage Determination L39226,” cms.gov. Community clinics saw a 22.9% jump in completed screenings after the guideline change, yet uptake among newly eligible 45–49-year-olds lags at 9.6%. Persistently low participation among Hispanic adults with limited English proficiency underscores the need for culturally adapted outreach tools. Exact Sciences reports its flagship Cologuard test has already detected 623,000 cancers and precancers, 80% at early stage, preventing an estimated USD 22 billion in downstream treatment costs.

Point-of-care FIT/iFOBT adoption surge

Immunochemical rapid tests remove dietary restrictions tied to traditional guaiac cards and deliver results within 10 minutes, enabling same-visit clinical decisions. FDA clearance of multiple CLIA-waived lateral-flow platforms, plus Medicare Local Coverage Determination L39226 supporting multiplex pathogen panels, has quickened placement in primary-care settings. The EU’s Regulation 2017/746 harmonizes device rules, though separate UKCA marking now applies post-Brexit. Health-economic studies show PCR-based point-of-care testing cuts unnecessary antibiotic days from 4 to 1, offsetting higher per-test costs through reduced drug use. Smartphone-connected devices such as Preventis QuantOn Cal transmit calprotectin results directly to clinicians and bolster chronic-disease monitoring.

Expansion of molecular enteric-pathogen panels

Multiplex PCR detects up to 20 pathogens in one hour and uncovers bacterial agents in 49.2% of symptomatic samples versus 5.2% for culture, with Campylobacter ranking highest. FDA-cleared panels—BD MAX, Luminex xTAG GPP and BioFire GI—deliver sensitivities beyond 95% while trimming time-to-result to less than two hours. Reimbursement guidance A58761 mandates use of FDA-cleared panels billed under specific CPT codes, streamlining claims for bacterial, viral and parasitic identification. Targeted therapy based on panel results reduces unnecessary imaging and accelerates isolation protocols, especially valuable for immunocompromised or pediatric patients. Payers are beginning to cover fecal calprotectin add-ons that surpass 90% sensitivity for differentiating inflammatory bowel disease.

Growth of at-home collection & telehealth integration

Mail-in kits remove clinic visits while maintaining diagnostic accuracy, with Cologuard fueling a 77% rise in completed screenings between 2018 and 2021. BIOHIT’s FAEX Sample System combines a leak-proof tube and precision-engineered stick, simplifying specimen handling under new EU IVDR rules. bioMérieux’s preprocessing module cuts stool-handling time to 5 minutes and enhances adenovirus detection limits, reducing laboratory bottlenecks. Consumer surveys show 78% willingness to undertake blood-based CRC screening if insurers cover the assay, signalling that stool tests must compete on convenience and price. Geneoscopy and Labcorp combine RNA isolation with digital PCR to commercialize ColoSense via a laboratory-telehealth model that supports nationwide logistics.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High instrument & cartridge costs | -1.4% | Global, particularly emerging markets | Medium term (2-4 years) |

| Limited awareness and access in emerging markets | -1.1% | MEA, Latin America, rural APAC | Long term (≥ 4 years) |

| Stringent & varied regulatory approval timelines | -0.8% | Global, with variations by region | Medium term (2-4 years) |

| Sample-stability issues for microbiome sequencing | -0.5% | Global, affecting NGS applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High instrument & cartridge costs

Multiplex PCR analyzers cost USD 150,000–300,000 and entail consumables running USD 40–60 per assay, deterring uptake in budget-constrained systems. Cost modelling indicates stool DNA screening must fall from USD 350 to roughly USD 50 to equal annual fecal occult blood testing on cost-effectiveness metrics. Emerging-market laboratories report mean diagnostic prices of USD 2.62, underscoring extreme price sensitivity. Limited manufacturer competition and opaque procurement processes further elevate local pricing, while some private insurers classify broad fecal analysis panels as investigational and deny payment.

Stringent & varied regulatory approval timelines

Geneoscopy’s ColoSense cleared the FDA 510(k) pathway but must still enroll 12,500 subjects in post-approval studies, extending commercialization milestones. Europe’s IVDR, effective May 2022, demands more clinical evidence and notified-body oversight, stretching approval to 18–24 months for high-risk assays. Divergent rules force companies to run separate studies for US and EU submissions, and proposed FDA oversight of laboratory-developed tests could further burden small innovators. Complying with ISO 15189 quality requirements adds documentation demands that lengthen product cycles and favor firms with dedicated regulatory teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Drive Market Expansion

Consumables generated 59.12% of sales in 2025 and are forecast to post a 7.32% CAGR, the quickest pace within the gastrointestinal (GI) stool testing market. Instruments accounted for the remaining revenue and will track a slower 6.68% advance as the installed base matures yet still requires routine updates. Recurring reagent purchases, high-tolerance collection tubes and single-use cartridges position consumables as the backbone of day-to-day testing workflows. Innovation such as BIOHIT’s FAEX Sample System tightens leak control and doubles as a dropper tube, reducing laboratory preprocessing steps and supporting premium price points despite budgetary scrutiny.

Ongoing guideline updates that expand eligible populations lift specimen volumes, ensuring strong pull-through for reagents, stabilizers and molecular cartridges. As labs automate extraction and amplification, high-margin consumables increasingly outpace capital equipment in total contribution to the gastrointestinal (GI) stool testing market size.

By Test Type: Viral Detection Accelerates Beyond Traditional Screening

Occult blood tests held 40.75% of global revenue in 2025, anchored by widespread FIT reimbursement and physician familiarity. Viral pathogen panels, though smaller, are projected to grow at 7.26% CAGR, outstripping all other categories within the gastrointestinal (GI) stool testing market. Demand is fueled by norovirus- and rotavirus-driven outbreaks that require real-time containment, especially in long-term-care and food-service environments. Multiplex PCR assays identify co-infections rapidly and support precise isolation policies, giving hospitals a compelling ROI even at higher list prices.

Bacterial panels and ova-and-parasite assays continue to serve endemic regions and immunocompromised cohorts, but viral panels’ superior growth trajectory reflects heightened post-pandemic vigilance and willingness to pay for speed and comprehensiveness. These dynamics are expected to tilt incremental spending toward syndromic testing menus and to enlarge the overall gastrointestinal (GI) stool testing market size for infectious disease management.

By Technology: NGS Innovation Challenges Immunoassay Dominance

Immunoassays commanded 38.25% of 2025 revenue due to low cost per test and streamlined workflows in primary care. Next-generation sequencing, while still a niche, is poised for a 7.41% CAGR through 2031 as reagent costs decline and cloud-based bioinformatics shorten analysis times, bringing culture-independent diagnostics into routine practice. PCR/NAAT systems, bolstered by FDA-cleared multiplex panels, retain a solid share and address mid-complexity needs at regional laboratories.

NGS can reveal pathogens in culture-negative diarrhea and decode antimicrobial-resistance genes within hours, broadening its utility beyond rare-case research. Early adopters report 91.2% sensitivity and 96.2% specificity on enteric bacteria, nearing cost parity with multiplex PCR and further diversifying the GI stool testing industry.

By End User: POC Sites Challenge Laboratory Centralization

Diagnostic laboratories delivered 35.02% of 2025 revenue, leveraging established logistics, quality control and payer contracts. Physician offices and other point-of-care venues, however, are projected for a leading 7.29% CAGR thanks to CLIA-waived cartridges that generate actionable results in under 10 minutes. Hospitals maintain roughly 30% share as onsite labs remain vital for inpatient gastroenteritis triage and outbreak management.

Convenience, immediate counseling and reduced follow-up visits make rapid testing attractive for busy clinics, and payer recognition of FIT and molecular panels performed onsite further closes the gap with centralized services. This trend accelerates equipment placement at non-traditional settings and feeds fresh demand for single-use cartridges within the gastrointestinal (GI) stool testing market.

Geography Analysis

North America retained 39.08% of global revenue in 2025 on the back of expansive Medicare coverage, clear FDA pathways and high provider awareness. The region’s CRC screening mandates, strong payer mix and concentration of sophisticated laboratories keep test volumes high, contributing materially to the gastrointestinal (GI) stool testing market size. Yet Asia-Pacific is forecast for the swiftest 7.52% CAGR as Japan’s aging population, China’s broadened reimbursement basket and India’s infectious-disease burden converge with regulatory harmonization efforts to boost adoption of molecular panels. Local manufacturing incentives and value-priced platforms cater to cost-conscious purchasers, further accelerating uptake.

Europe, home to roughly 27.86% of revenue, benefits from consistent IVDR standards and robust public insurance coverage, though reimbursement differences among member states temper uniform roll-out. South America’s combined 20.62% share reflects steady public-health investment in screening and pathogen surveillance, while local currency volatility constrains premium platform imports. The Middle East and Africa hold about 12.44% share, with select Gulf Cooperation Council states tapping oil-backed budgets to fund molecular diagnostics, contrasted with low-income countries relying on donor support for FIT distribution. Rising GI disease awareness and decentralization of testing within emerging markets steadily close the adoption gap. Portable platforms and caravan-style screening campaigns demonstrate value where lab infrastructure is sparse, supporting incremental expansion of the gastrointestinal (GI) stool testing market.

Regulatory Landscape

In the United States, GI stool testing products span traditional immunochemical fecal occult blood tests and molecular enteric pathogen panels that fall under FDA medical device oversight, including Class II categorization for gastrointestinal microorganism multiplex nucleic acid-based assays under 21 CFR 866.3990. A key compliance inflection point is FDA's May 2024 final rule that phases out enforcement discretion for laboratory developed tests (LDTs) over a four-year period, increasing regulatory and quality-system obligations for labs and test developers that historically relied on LDT pathways.

In Europe, the In Vitro Diagnostic Regulation (IVDR, Regulation (EU) 2017/746), effective since May 2022, continues to shape clinical evidence and notified-body requirements for both assays and specimen receptacles used for stool collection, with MDCG 2024-11 clarifying classification principles for specimen receptacles (commonly Class A when intended for collection for later examination). The EU also moved to standardize conformity-assessment expectations through Commission Implementing Regulation (EU) 2026/977 (published May 4, 2026), which sets uniform quality management and procedural requirements for notified bodies, with application from February 25, 2027.

Value Chain Analysis

The GI stool testing value chain starts with specialized inputs such as antibodies for immunoassays and enzymes/primers for molecular PCR and sequencing workflows, alongside plastics and engineered collection devices that support home collection and clinic distribution. A recurring constraint is the availability of high-titre, native biological materials used in calibration and quality control, which can delay lot release and compel manufacturers to evaluate alternative materials that require revalidation.

Manufacturing commonly combines in-house assay development with scaled kit assembly through ISO 13485-compliant contract manufacturing partners, while distribution flows through hospital and reference laboratory procurement channels as well as direct-to-consumer and mail-in logistics for at-home programs. Cold-chain and controlled logistics remain important to preserve sample integrity and reagent performance across transit and storage, especially as multiplex PCR and sequencing menu expansion raises sensitivity to stability and contamination controls. Cost and supply risk management also includes supplier diversification and longer-term procurement agreements, given landed-cost volatility for imported reagents and plastic components.

Competitive Landscape

Market leadership rests with diversified diagnostics groups that blend acquisition, R&D and payer-policy expertise to secure durable positions. Quest Diagnostics’ USD 1.35 billion Lif eLabs takeover extends North-American reach and generates CAN 970 million in new revenue, reaffirming the group’s hub-and-spoke courier model[3]Quest Diagnostics Incorporated, “Acquisition of LifeLabs Investor Presentation,” questdiagnostics.com. Exact Sciences pushes the innovation frontier with Cologuard Plus, Oncodetect residual-disease monitoring and Oncoguard esophageal screening, aiming to capture adjacent workflows and foster life-cycle loyalty at a premium. Geneoscopy’s USD 105 million Series C, led by Bio-Rad, funds RNA-based ColoSense and pipeline IBD assays, underlining investor confidence in RNA signatures as a next wave of stool diagnostics.

White-space innovation occurs in AI-enabled stool imaging, highlighted by Cylinder’s acquisition of Dieta Health’s software that triages images for clinician review, promising workload relief and earlier flagging of red-flag symptoms. As the FDA weighs stricter oversight of laboratory-developed tests, scale advantages may accrue to multinationals with regulatory compliance infrastructures, potentially nudging smaller niche players toward partnership or exit.

Gastrointestinal (GI) Stool Testing Industry Leaders

Abbott Laboratories

Genova Diagnostics

bioMérieux SA

Cardinal Health

Danaher Corporation (Beckman Coulter, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace is the expansion of syndromic gastrointestinal pathogen testing into more routine settings through fully automated and flexible panel designs that reduce hands-on time and allow target selection by clinical need. Multiple 2026 US clearances for GI panels underscore active product refresh cycles and create room for labs to upgrade from legacy methods toward sample-to-answer workflows, supported by pay-per-target customization approaches such as DiaSorin's LIAISON PLEX Gastrointestinal Flex Assay.

Another opportunity area is noninvasive colorectal cancer screening pathways that increasingly formalize stool testing as an at-home and primary-care accessible option, with guideline and payer frameworks putting more emphasis on validated performance. The American Cancer Society's May 2026 guideline update explicitly incorporated next-generation multi-target stool DNA and multi-target stool RNA at-home tests (including ColoSense), while CMS in June 2026 adopted a national performance-based framework for coverage of non-invasive biomarker screening tests, raising the bar for sensitivity and specificity evidence. In parallel, system-level workflow integration efforts, such as Health New Zealand's July 2026 initiative using FIT as a first-line investigation for symptomatic patients, highlight operational demand for scalable kit supply, reliable logistics, and streamlined reporting that can be replicated across other constrained endoscopy-capacity settings.

Recent Industry Developments

- June 2026: bioMérieux submitted the BIOFIRE FILMARRAY Gastrointestinal 1.1 (GI1.1) Panel and GI1.1 Panel Mid to the US FDA for 510(k) review to update performance for gastrointestinal pathogen detection. The filing supports a refresh cycle for installed molecular platforms and can help laboratories standardize on newer panel versions as testing menus broaden.

- January 2025: Geneoscopy closed a USD 105 million Series C financing led by Bio-Rad Laboratories to accelerate the commercial launch of ColoSense and expand inflammatory bowel disease assay development. The funding strengthened the company's ability to scale laboratory operations and compete for payer and provider adoption in stool-based molecular screening.

- October 2024: The US FDA approved Exact Sciences Cologuard Plus for colorectal cancer screening, with reported performance metrics including 95% CRC sensitivity and 94% specificity. The approval broadened premium stool DNA screening options and intensified competition among noninvasive screening modalities offered through at-home collection pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the GI stool testing market covers in-vitro tests that use human stool samples to detect gastrointestinal disease signals, such as occult blood, infectious pathogens, and inflammation-related biomarkers. The market value includes test kits, related consumables, and lab instrumentation tied to routine stool testing workflows.

Scope exclusions: We exclude endoscopy-led diagnosis, blood-based tests, and breath tests, even when they are ordered for similar symptoms.

Segmentation Overview

- By Product Type

- Instruments

- Consumables

- By Test Type

- Occult Blood

- Ova & Parasites

- Bacterial Pathogens

- Viral Pathogens

- Others

- By Technology

- Immunoassay

- Molecular PCR

- Next-Generation Sequencing

- Lateral Flow / Rapid Tests

- By End User

- Hospitals

- Diagnostic Labs

- Physician Offices & POC Sites

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of stool-based GI diagnostics and to create a starting dataset before assumptions were tested. We reviewed non-paywalled sources such as the US CDC and the World Health Organization, along with public guidance and method updates from groups such as USPSTF and similar national screening bodies. To ground disease and testing demand, we also used peer-reviewed gastroenterology journals and public health surveillance releases that discuss enteric infections and colorectal screening participation.

On the supply side, we used company filings and investor decks to see where stool testing revenues sit within broader diagnostic portfolios, and we checked reputable press and association websites for product launches, regulatory clearances, and reimbursement changes. Where helpful, paid subscriptions for company financials and a patent database were referenced to confirm product focus and timing of innovation, especially around molecular and multiplex panels. The sources listed here are illustrative, and many other public references were consulted to collect data, cross-check assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on talking with clinical laboratory leaders, gastroenterology-focused clinicians, distributors, and diagnostic product managers who see ordering patterns and price movements firsthand. We used these discussions to confirm how often key stool tests are used, how home collection is handled in practice, and how pricing differs by setting (hospital labs versus reference labs). Because this is a global market, we checked inputs across major regions so the final totals are not driven by one country's reimbursement or screening cadence.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 15% | APAC: 43% |

| Mid tier: 54% | Functional/Unit leaders: 34% | EMEA: 34% |

| Smaller Players: 17% | Managers: 51% | Americas: 23% |

Market-Sizing & Forecasting

The core model uses a top-down build that reconstructs demand from stool-testing volumes and testing intensity, then translates those into value using an average selling price range that reflects kit, reagent, and processing economics. To keep the numbers practical, we start by mapping the addressable testing pool created by colorectal screening participation, symptomatic GI workups, and infectious gastroenteritis investigations, and then apply realistic ordering rates for common stool tests.

To check the output, selective bottom-up approximations were added, including sampled ASP times estimated test volumes from labs and channel checks, followed by a sanity check against publicly visible diagnostics revenue footprints. Key inputs that typically move the market include FIT and FOBT utilization in screening programs, adoption of multiplex molecular GI panels, use of inflammatory markers such as fecal calprotectin in IBD pathways, the split between hospital and reference lab processing, and the share of home collection within routine testing. Forecasts were built using scenario analysis, where variables like screening guideline changes, reimbursement tightening or expansion, and molecular panel penetration are adjusted with consensus from interview feedback.

Data Validation & Update Cycle

Validation starts by triangulating the modeled market totals against independent signals, such as screening participation trends, lab throughput commentary, and the pace of molecular panel adoption. When results fall outside expected ranges, we revisit the assumptions that usually drive the variance, such as test frequency per patient, pricing bands, and the mix between routine immunoassays and molecular panels, and then we re-check them with additional callbacks.

Before sign-off, the model goes through a multi-step analyst review that includes logic checks, year-over-year variance checks, and consistency checks across regions. Reports are refreshed annually, and interim updates are triggered when a material event occurs, such as a major guideline change, reimbursement shift, or a notable technology adoption jump. Right before delivery, a final pass is performed so clients receive the most current view available.

Mordor Intelligence's Gi Stool Testing Market Size Compared With Other Published Estimates

It is common to see different market sizes for GI stool testing because publishers draw the boundary in different places and use different ways to turn test activity into revenue. Differences also show up when one study uses a future base year, another uses a current year, or when currency timing and inflation assumptions are applied differently.

By tracking unit-level testing signals and refreshing price bands with lab-side checks, Mordor Intelligence places molecular stool panels and routine immunoassays inside the same stool-testing scope while keeping endoscopy and blood-based diagnostics out, which can shift totals versus studies that bundle broader GI diagnostics or include microbiome wellness services.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.89 B (2026) | |

| Industry Publisher A | USD 1.03 B (2024) | Uses a 2024 base year and a broader segment lens that can pull in adjacent GI diagnostic services, which lifts the current value versus a model anchored to stool-test-only product revenues. |

| Healthcare Publisher B | USD 2.93 B (2024) | Appears to include wider stool-related offerings, such as expanded microbiome profiling and wellness-led testing, and it may apply higher average prices without separating routine screening tests from premium panels. |

The spread across estimates mainly comes from year choice and what is counted as stool testing revenue, not from disagreement that demand is rising. Our approach keeps the math traceable to testing volumes, pricing bands, and adoption indicators, which makes it easier for readers to repeat the logic and stress-test assumptions.

Key Questions Answered in the Report

What is the current size of the gastrointestinal (GI) stool testing market?

The market reached USD 0.89 billion in 2026 and is forecast to climb to USD 1.24 billion by 2031.

Which product segment is growing the fastest?

Consumables are advancing at a 7.32% CAGR, outpacing instruments due to recurring demand for reagents and collection kits.

How quickly is Asia-Pacific expanding?

Asia-Pacific is projected for a 7.52% CAGR, the highest regional growth rate through 2031.

What technology is challenging immunoassays?

Next-generation sequencing is gaining ground with a projected 7.41% CAGR and near-parity costs compared with multiplex PCR.

Why are point-of-care sites important?

Physician offices and other POC venues are expected to grow 7.29% annually, driven by CLIA-waived devices that deliver results in minutes.

How concentrated is the competitive landscape?

The top five companies control about 55% of global revenue, indicating moderate consolidation.

Page last updated on: