Railway System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

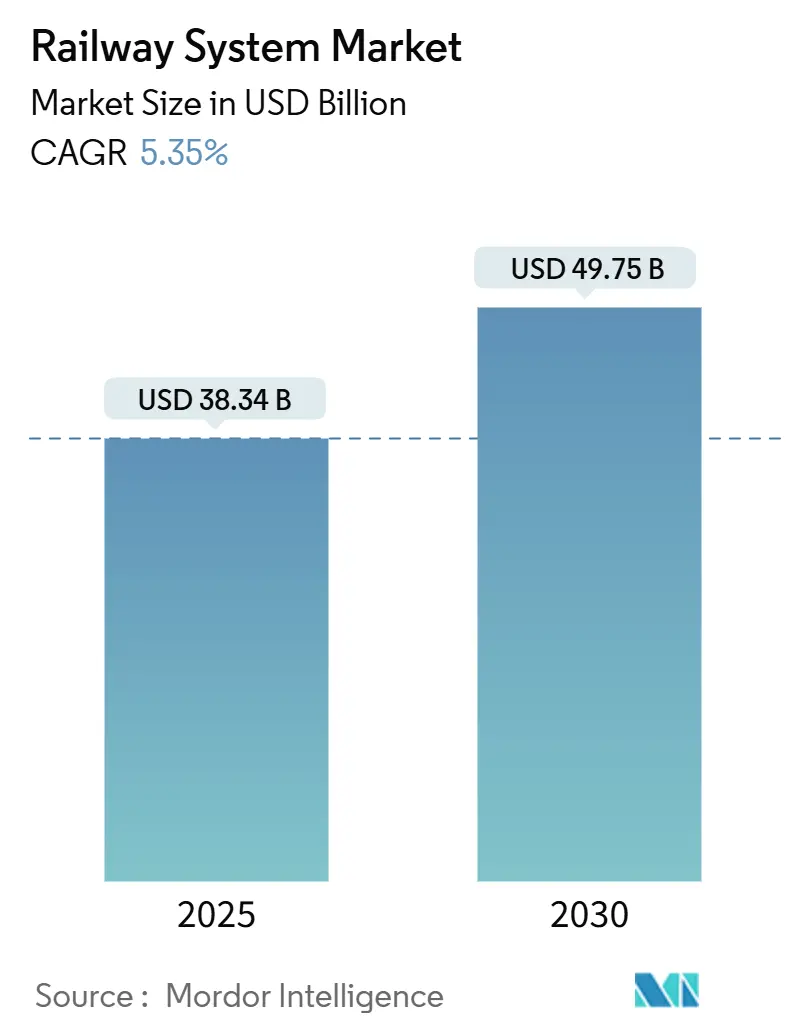

| Market Size (2025) | USD 38.34 Billion |

| Market Size (2030) | USD 49.75 Billion |

| Growth Rate (2025 - 2030) | 5.35% CAGR |

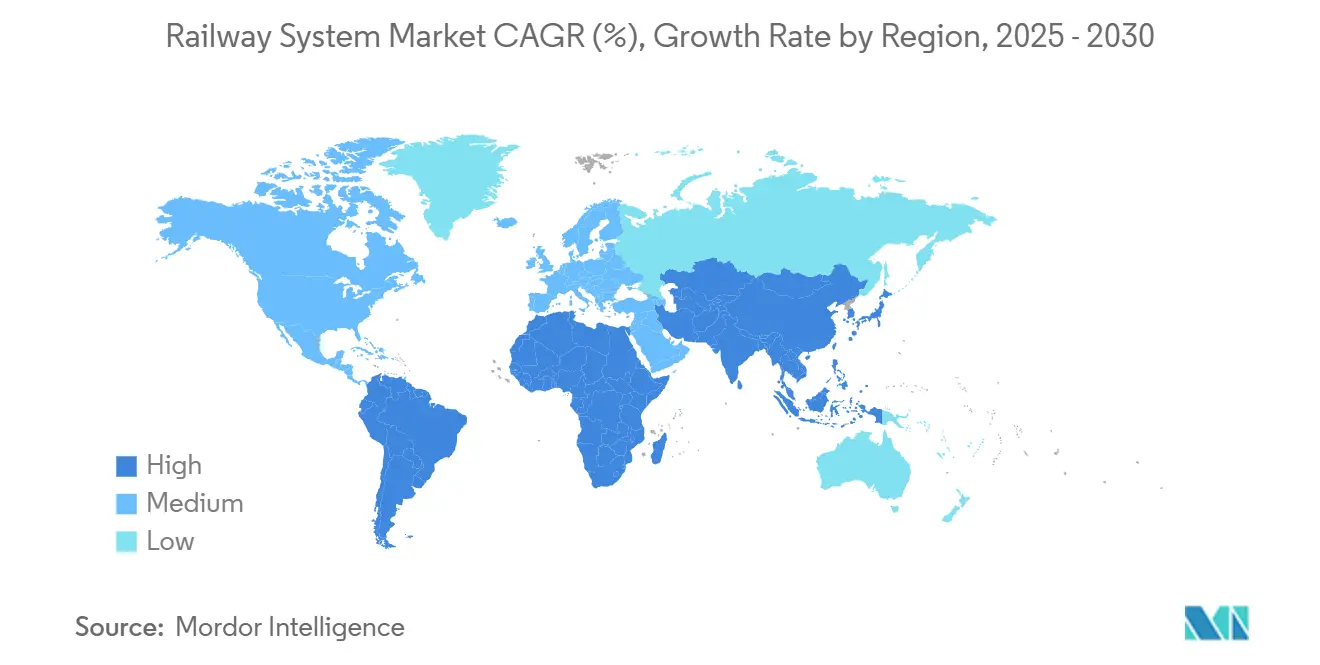

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

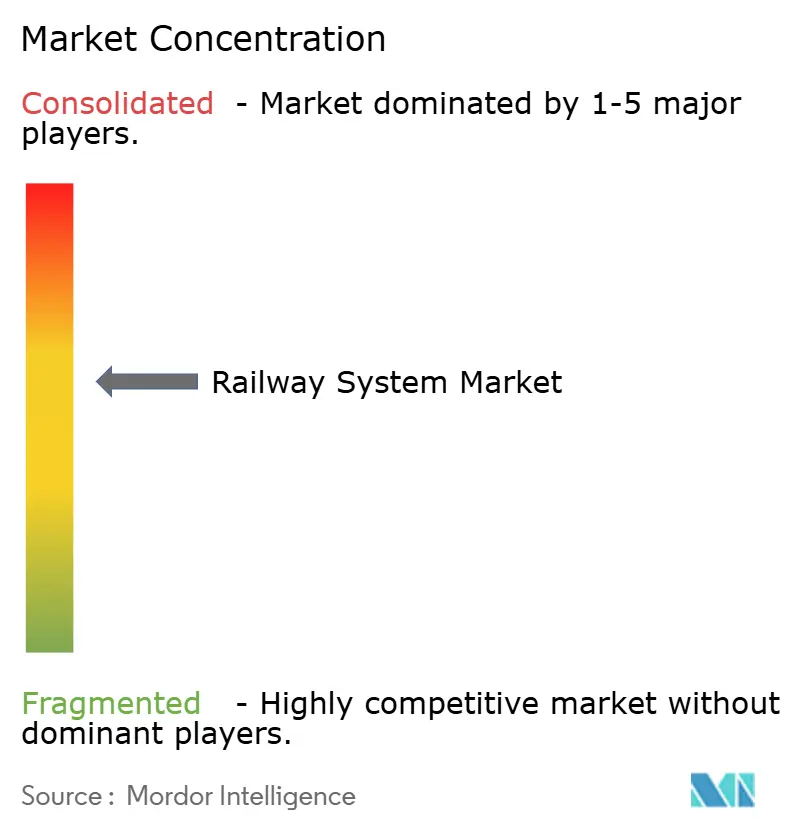

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Railway System Market Analysis by Mordor Intelligence

The railway system market size is valued at USD 38.34 billion in 2025 and is projected to reach USD 49.75 billion by 2030, representing a 5.35% CAGR during the forecast period. Rising public funding for rail electrification, stringent decarbonization mandates, and rapid adoption of digital signaling platforms anchor this growth trajectory. Operators prioritize smart, energy-efficient rolling stock and software-defined control systems that lower whole-life operating costs and help cities meet net-zero carbon targets. Sovereign infrastructure funds across Asia-Pacific, alongside policy incentives in Europe and North America, continue to redirect transportation budgets from highways to rail corridors. Suppliers that bundle rolling stock, predictive maintenance, and mobility-as-a-service solutions into subscription models are gaining pricing power and stickier customer relationships. At the same time, semiconductor supply chain reshoring and volatile steel and copper prices shape procurement strategies and margin resilience.

Key Report Takeaways

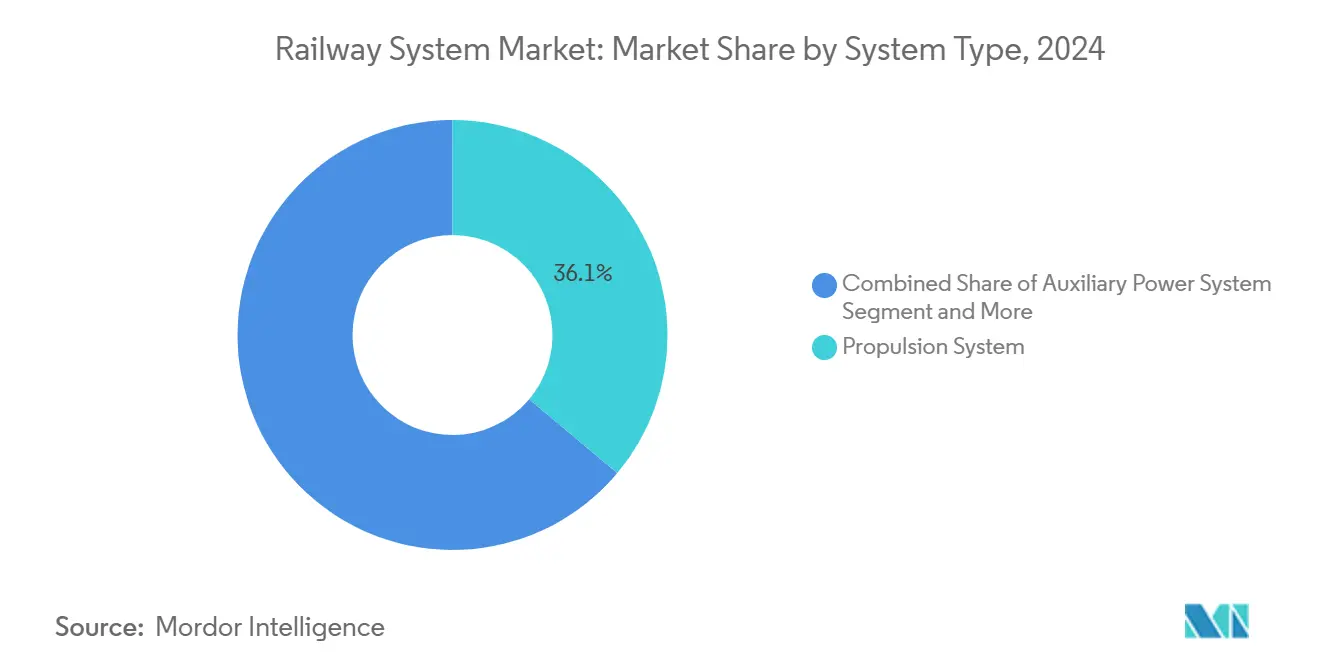

- By system type, propulsion systems led with 36.12% of the railway system market share in 2024 while expanding at a 5.88% CAGR through 2030.

- By transit type, conventional rail accounts for 62.15% of the railway system market share in 2024, whereas rapid transit recorded the fastest growth at 6.41% CAGR.

- By application, passenger transportation commanded 69.33% of the railway system market share in 2024 and is forecast to rise at a 6.03% CAGR to 2030.

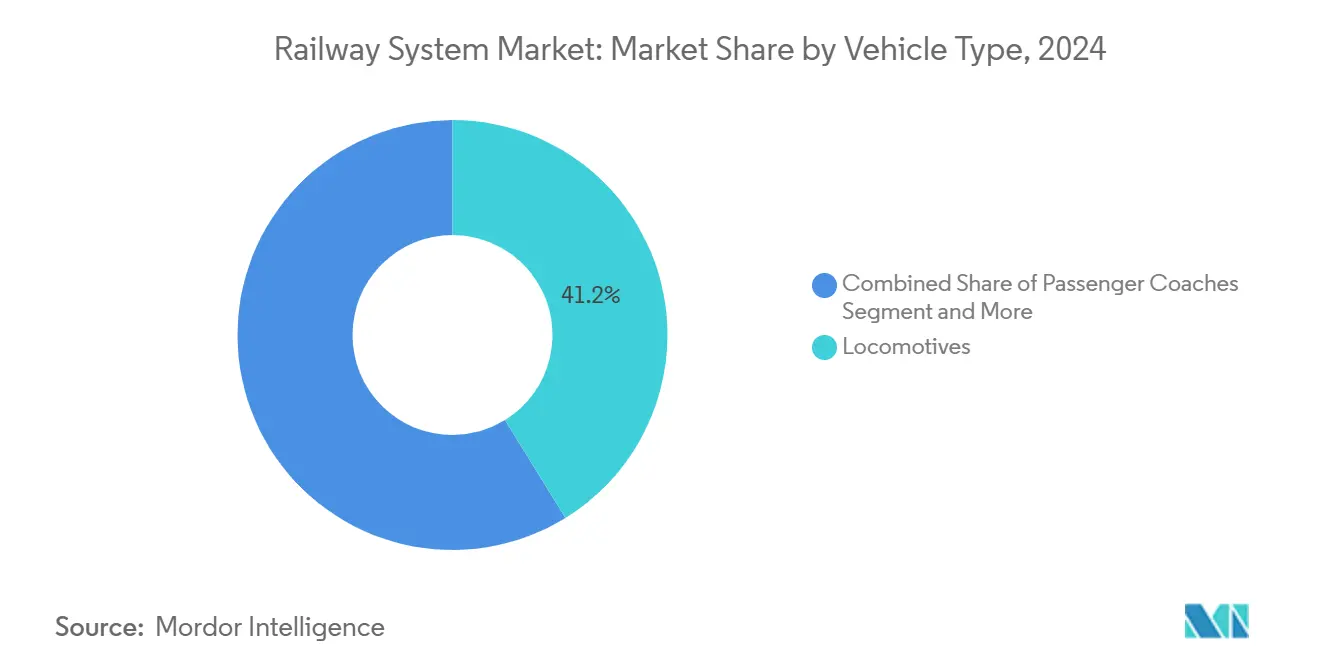

- By vehicle type, locomotives retained 41.24% of the railway system market share in 2024, while light rail achieved the highest 7.12% CAGR.

- By end use, public operators controlled 73.66% of the railway system market share in 2024, but private operators are projected to post a 7.53% CAGR through 2030.

- By geography, Asia-Pacific captured 49.13% of the railway system market share in 2024 and is expected to grow at a 6.25% CAGR.

Global Railway System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rail Decarbonization Gets Government Stimulus | +1.2% | EU, North America, China | Medium term (2-4 years) |

| Digital Control Lowers Rail OPEX | +0.9% | Europe leading, expanding to North America and APAC | Medium term (2-4 years) |

| Congestion Drives Shift to Rail | +0.8% | Asia-Pacific core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Hydrogen and Battery-Electric Trains | +0.7% | Germany, UK, India, Japan | Long term (≥ 4 years) |

| Asset-as-a-Service Business Models | +0.6% | North America and the EU, emerging in APAC | Short term (≤ 2 years) |

| Reshoring Semiconductors Boosts Local Suppliers | +0.5% | North America, EU, allied nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Stimulus for Rail Decarbonization

Major economies use green stimulus packages to accelerate electrification, signaling upgrades, and next-generation propulsion projects. Germany earmarked EUR 86 billion (~USD 101 billion) to 2030, with 60% set aside for catenary expansion and digital interlocking upgrades, creating long-tail demand for inverter drives, pantographs, and ETCS components [1]“Strengthening Rail for Climate Policy,” Federal Ministry for Digital and Transport, bmdv.de. Canada’s transit plan funds zero-emission rolling stock procurement, while India has ring-fenced 100% network electrification. These predictable pipelines enable suppliers to raise R&D spending on hydrogen stacks, battery modules, and software-defined train control without balance-sheet stress. Vendors able to certify components under evolving cybersecurity and safety norms secure preferred-bidder status, reinforcing entry barriers for late movers. As diesel bans accelerate, long-term contracts linked to availability guarantees protect operator cash flows and elevate recurring revenue participation in the railway system market.

Digital-Train Control (ETCS/ATO) Lowering OPEX

Operators adopt ETCS Levels 2 and 3 paired with ATO to unlock capacity without laying new track. Hamburg’s S-Bahn achieved 15% energy savings and 20% throughput gains post-deployment, validating the payback model for midsize commuter lines [2]Deutsche Bahn Netz, “Digital S-Bahn Hamburg Achieves Performance Milestones,” dbnetze.com . Stuttgart shortened headways from 120s to 90s, raising trains per hour. Eliminating 300 legacy signal boxes on the UK East Coast Main Line will cut annual maintenance and improve punctuality benchmarks significantly. Operators therefore prioritize software resilience, fail-safe communications, and cybersecurity certification. Vendors that package control hardware, cloud-based analytics, and sleep-cycle optimization algorithms reduce the total cost of ownership and secure long-term maintenance revenue streams in the railway system market.

Urban Congestion Pushing Modal Shift to Rail

Congestion costs reaching double-digit percentages of city GDP spur planners to prioritize track-based transit over road widening. Malaysia quantified annual congestion losses at MYR 20 billion (~USD 5 billion) and fast-tracked MRT 3, along with LRT extensions to cut commuter travel times [3]“Congestion Impact Assessment,” Ministry of Transport Malaysia, mot.gov.my. Berlin–Munich’s high-speed corridor reduced the four-hour drive to 3.5 hours by rail and drew a notable share away from aviation within 18 months, underscoring rail’s competitiveness on a 300–800 km corridor. Rapid transit segments such as metro and light rail benefit because grade-separated alignments bypass gridlock, offer higher passenger throughput per corridor, and justify land-value-capture financing. Cities now embed transit-oriented development rules that integrate affordable housing and last-mile micro-mobility hubs, entrenching rail as the backbone of sustainable urban mobility strategies.

Hydrogen and Battery-Electric Multiple Units

Alternative propulsion systems move from demonstration to scaled purchase orders despite infrastructure constraints. Germany’s hydrogen multiple units now deliver a significant fleet availability, compared to early trials, after durability upgrades to fuel-cell stacks. India unveiled a 180 km/h hydrogen train for 5,000 km of non-electrified routes by 2030. Stadler’s RS Zero battery unit provides a 200 km range that covers 80% of Central European regional services. Hydrogen suits long-regional corridors where catenary is uneconomic, while battery-electric addresses commuter lines able to recharge at terminals. Weight penalties still constrain seat capacity, and hydrogen refueling corridors remain sparse, but long-term carbon-pricing trajectories make these platforms economically viable.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiscal Pressure Delays Projects | –0.6% | Global, higher impact in developing markets | Short term (≤ 2 years) |

| Volatile Prices Inflate CAPEX | –0.4% | Global, sensitive in price-competitive contracts | Medium term (2-4 years) |

| Right-Of-Way Hurdles In Cities | –0.3% | APAC urban centers, European cities, North American metros | Long term (≥ 4 years) |

| Skilled Labor Shortages Persist | –0.2% | North America, Europe, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fiscal Pressure Post-COVID Delaying Projects

Budget reallocations toward health and economic relief in 2024 caused funding gaps for several marquee rail programs. The UK reported a shortfall for Network Rail’s Control Period 7, putting catenary extensions and digital resignaling on slower timelines. Victoria, Australia, cut transport spending, delaying the Suburban Rail Loop by 18 months. Singapore deferred a significant amount of MRT work to reorient cash toward public-health safeguards. Such deferrals compress order books for signaling and rolling-stock suppliers and elongate revenue recognition cycles. Although multi-year frameworks remain intact, suppliers hedge with shorter lead-time service contracts to bridge near-term volume volatility.

Volatile Steel and Copper Prices Inflating CAPEX

Steel prices have experienced a significant increase, reflecting substantial growth compared to previous levels, while copper crossed USD 9,200 per ton, inflating budgets for catenary and transformers. These materials account for up to 30% of track and power-supply project costs, pressuring developers to seek fixed-price bids that transfer risk to contractors. Smaller fabricators lacking hedging instruments face insolvency threats, accelerating industry consolidation. Operators are exploring modular track-form solutions with reduced steel content and are recycling scrap rails more aggressively. Cost-plus contracts now integrate escalation clauses tied to commodity indices, stabilizing cash flows yet capping margin upside.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Propulsion Dominance Drives Electrification

Propulsion platforms accounted for 36.12% of the railway system market size in 2024 and are forecast to post a 5.88% CAGR to 2030 on the back of diesel phase-out mandates and falling battery and hydrogen fuel-cell costs. Electric traction reduces energy expense up to 30% compared with diesel, producing compelling paybacks that accelerate fleet renewal cycles. Next-generation traction inverters support multiple power inputs, allowing operators to migrate from catenary to onboard energy storage without swapping traction motors. Train information and passenger-infotainment systems see growing uptake as ridership gains raise expectations for Wi-Fi and journey-time information. At the same time, HVAC retrofits integrate HEPA filtration to meet post-pandemic ventilation norms.

Auxiliary power modules and safety systems present mature replacement demand yet experience incremental upgrades through software integration and remote condition monitoring. Integrated propulsion-control software that supports over-the-air updates enables continuous efficiency tuning, cutting unscheduled downtime. Siemens Mobility’s modular Vectron locomotives illustrate the trend, allowing operators to retrofit hydrogen or battery packs onto a single chassis, a flexibility that deepens lifecycle engagement with clients. As a result, the railway system market rewards suppliers capable of bundling hardware, firmware, and analytics into end-to-end offers.

By Transit Type: Rapid Transit Acceleration

Conventional rail still contributes 62.15% of the railway system market size in 2024, underpinned by established freight and intercity passenger services. Yet the momentum behind urban rapid-transit buildout channels supplier R&D toward higher acceleration rates, regenerative-braking systems, and communications-based train control that lifts throughput without adding track. Bangkok’s Orange Line monorail achieved a notable on-time performance within six months, showcasing the operational gains of grade-separated corridors. Consequently, the railway system market prioritizes modular vehicle platforms adaptable across metro, monorail, and automated line deployments.

Rapid transit posted a 6.41% CAGR, the highest among transit formats, driven by urbanization and congestion relief imperatives. Metro systems dominate orders in China and India, where city pairs like Shenzhen–Dongguan integrate cross-boundary services that lift corridor ridership. Monorail and automated people movers gain share in Southeast Asian cities that value narrow footprints and reduced expropriation costs. High-speed rail remains a premium niche but delivers strategic capacity on 300 km-plus corridors, positioning rail as a competitive alternative to aviation while cutting per-passenger emissions.

By Application: Passenger Transportation Strength

Passenger services commanded 69.33% of the railway system market size in 2024, and are anticipated to expand at a 6.03% CAGR, as governments frame rail as a climate-friendly alternative to private cars and short-haul flights. Return-to-office mandates and integrated ticketing that blends rail with micro-mobility feed ridership gains on suburban and regional lines. High-speed corridors provide premium services with average load factors above 75%, underpinning strong farebox recovery and policy support.

Freight rail experiences steady expansion through intermodal hubs integrating port and e-commerce supply chains. Trucks retain dominance for sub-500 km routes, yet driver shortages and carbon pricing reshape the modal balance for longer distances. Rail access charges that reflect dynamic energy pricing shift operators toward energy-saving locomotive software, boosting adoption of real-time driver advisory systems. Overall, passenger-centric investments continue to direct technology roadmaps within the railway system market.

By Vehicle Type: Light Rail Momentum

Locomotives represent the single largest slice of 41.24% of the railway system market size in 2024, but grow modestly as operators maximize existing fleets via mid-life refurbishments and digital upgrades. Battery-electric and hydrogen stand enter locomotive platforms for shunting and short-haul freight. Tram systems gain traction in European car-free inner cities, where curbside running lanes leverage existing streetscapes while offering permanent right-of-way advantages over buses. These dynamics ensure diverse vehicle demand patterns across the railway system market.

Light rail posted a leading 7.12% CAGR owing to municipalities seeking cost-effective, flexible alignments that can be built at USD 60–80 million per kilometer compared with USD 150 million or more for heavy metro. Vehicle standardization and shorter construction schedules expedite project approvals and lower disruption to surface traffic. Portland’s MAX network attains a significant farebox recovery, validating financial viability with dense land-use zoning.

By End Use: Private Sector Acceleration

Public agencies held 73.66% of the railway system market size in 2024, reflecting historic ownership of core infrastructure and rolling stock. Nevertheless, private operators registered a 7.53% CAGR, fueled by European liberalization and public-private partnerships in Asia and the Americas. Open access frameworks allow independent passenger services to run alongside incumbents, fostering competitive timetables and ancillary revenue streams.

Private freight rail consolidates through cross-border mergers such as the Canadian Pacific–Kansas City Southern deal, creating a continental reach that attracts volume from long-haul trucking. Private concessionaires invest in customer-facing digital platforms that offer door-to-door booking, raising service differentiation. Safety certification under ISO 45001 becomes a tender prerequisite, giving well-capitalized players an edge. As asset-as-a-service models mature, private lessors expand leased fleet portfolios, increasing their influence over procurement specifications in the railway system market.

Geography Analysis

Asia-Pacific controlled 49.13% of the railway system market size in 2024 and continues to lead with a 6.25% CAGR through 2030. China is working on expanding high-speed track to 45,000 km with a plan to hit 70,000 km by 2035. Urban metros added 1,200 km of new lines in the same year, while dedicated freight corridors increased coal and container throughput. India accelerates modernization via Vande Bharat Express and USD 30 billion in electrification funding, complemented by Eastern and Western Dedicated Freight Corridors. Southeast Asian projects such as Indonesia’s Jakarta–Bandung high-speed line and Malaysia’s East Coast Rail Link highlight Belt and Road financing. In contrast, Japan and South Korea focus on exporting technology and operations expertise.

Europe ranks second, characterized by mature infrastructure needing digital upgrading and decarbonization. The Trans-European Transport Network mandates ETCS across 35,000 km by 2030, solidifying long-run demand for signaling installations. Germany’s EUR 86 billion (~USD 101 billion) program leads the region, and France’s Grand Paris Express adds 200 km of driverless metro. Despite budget overruns, the United Kingdom persists with HS2, while Poland and the Czech Republic use EU cohesion funds to electrify and raise line speeds. Attention to station accessibility and last-mile connectivity supports ancillary system spending on elevators, ticketing, and bike-share integration.

North America emphasizes freight performance and corridor-focused passenger enhancements. The Infrastructure Investment and Jobs Act allocates USD 66 billion toward Amtrak expansion and safety upgrades, prioritizing the Northeast Corridor and new intercity links such as Cleveland-Chicago. The Canadian Pacific–Kansas City Southern merger creates the first network linking Canada, the United States, and Mexico, highlighting cross-border supply-chain optimization. Freight carriers invested in positive train control, bridge replacements, and intermodal terminals. Middle East and Africa see early-stage growth, driven by Saudi Arabia’s NEOM linear city rail blueprint and Egypt’s high-speed line connecting Cairo to the New Administrative Capital. South Africa targets commuter rail restoration after pandemic disruptions, while Morocco extends its Al Boraq high-speed service toward Agadir.

Competitive Landscape

Competition in the railway system market is moderately concentrated, with top players blending product depth and digital service portfolios. Alstom, Siemens Mobility, and CRRC command global footprints spanning rolling stock, signaling, and turnkey project delivery. They pivot from one-off equipment sales toward subscription-based condition monitoring, onboard data analytics, and integrated mobility-as-a-service platforms that ensure revenue visibility. Hitachi Rail’s EUR 1.66 billion (USD 1.94 billion) acquisition of Thales Ground Transportation Systems amplifies its command of signaling and cybersecurity competencies. At the same time, Wabtec’s USD 960 million purchase of Dellner Hitachi enhances coupler and suspension product breadth.

Strategic focus centers on cross-domain systems integration rather than standalone component performance. Operators award contracts to vendors that guarantee reliability, punctuality, and energy-saving KPIs under multi-decade service contracts. Consequently, suppliers invest heavily in cloud-native software stacks, edge computing gateways, and cybersecurity certifications such as ISO 27001 to secure tender compliance. Disruptive entrants include AI-powered predictive maintenance firms that reduce unplanned downtime and hydrogen-refueling-infrastructure startups that partner with energy majors to roll out green hydrogen corridors.

Supply chain resilience remains a competitive differentiator. Firms sign long-term semiconductor sourcing agreements with onshore fabs and build regional assembly hubs to shorten delivery schedules. Inflationary pressure on steel and copper prompts advanced procurement hedges and materials-light design innovations. Skilled-labor scarcity in advanced signaling drives collaborations with universities and coding-boot-camp operators to enlarge the talent pool. Collectively, these actions strengthen market positioning while reinforcing barriers to entry for new challengers in the railway system market.

Railway System Industry Leaders

CRRC Corporation Limited

Alstom SA

Siemens Mobility

Hitachi Rail

Stadler Rail AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Concord Control Systems unveiled India’s first fully indigenous zero-emission propulsion package, aligning with the nation’s 2030 net-zero rail target.

- July 2025: Tata AutoComp Systems and Skoda Group launched a joint venture in India to manufacture propulsion components under a multi-million-euro investment.

- July 2025: DB Cargo retrofitted a locomotive with Automatic Train Operation and Remote Train Operation features, enabling autonomous long-distance freight runs.

- December 2024: Indian Railways deployed Kavach, a Safety Integrity Level 4 automatic train-protection suite that raises collision-avoidance reliability.

Global Railway System Market Report Scope

| Propulsion System |

| Auxiliary Power System |

| HVAC System |

| Onboard Vehicle Control |

| Train Information System |

| Train Safety System |

| Conventional Rail | |

| Rapid Transit | Metro |

| Monorail | |

| High-Speed Rail |

| Passenger Transportation |

| Freight Transportation |

| Locomotives |

| Passenger Coaches |

| Freight Wagons |

| Light Rails |

| Trams |

| Public Sector (Government Railways) |

| Private Operators |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By System Type | Propulsion System | |

| Auxiliary Power System | ||

| HVAC System | ||

| Onboard Vehicle Control | ||

| Train Information System | ||

| Train Safety System | ||

| By Transit Type | Conventional Rail | |

| Rapid Transit | Metro | |

| Monorail | ||

| High-Speed Rail | ||

| By Application | Passenger Transportation | |

| Freight Transportation | ||

| By Vehicle Type | Locomotives | |

| Passenger Coaches | ||

| Freight Wagons | ||

| Light Rails | ||

| Trams | ||

| By End Use | Public Sector (Government Railways) | |

| Private Operators | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue for global railway systems by 2030?

Revenue is expected to reach USD 49.75 billion by 2030, reflecting consistent 5.35% CAGR growth.

Which region leads current and future railway investment?

Asia-Pacific holds 49.13% of 2024 revenue and will advance at a 6.25% CAGR, driven by high-speed expansion in China and metro build-outs across Southeast Asia.

Which system segment delivers the strongest growth?

Propulsion platforms record a 5.88% CAGR because operators replace diesel fleets with hydrogen and battery-electric units.

How are asset-as-a-service models changing procurement?

Leasing bundles shift large upfront costs into predictable OPEX, expanding private-operator participation and generating annuity-style revenue for suppliers.

Page last updated on: