Train Control And Management System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

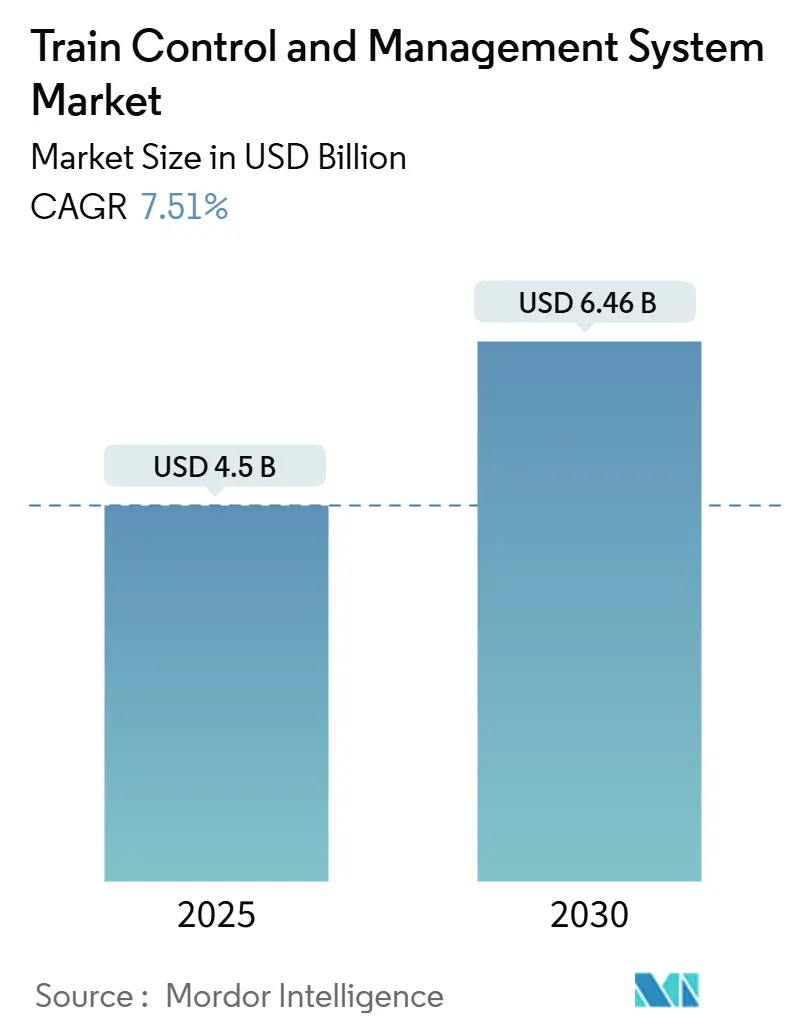

| Market Size (2025) | USD 4.5 Billion |

| Market Size (2030) | USD 6.46 Billion |

| Growth Rate (2025 - 2030) | 7.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Train Control And Management System Market Analysis by Mordor Intelligence

The train control and management system market size reached USD 4.50 billion in 2025 and is projected to expand to USD 6.46 billion by 2030, registering a 7.51% CAGR over 2025-2030. Rising urbanization, regulatory emphasis on safety, and the shift toward autonomous rail operations are accelerating demand for digital platforms that merge Communication-Based Train Control (CBTC) with artificial intelligence. Operators in densely populated corridors deploy moving-block automation to unlock latent capacity, while stringent interoperability rules in Europe and PTC compliance in North America sustain upgrade cycles. Suppliers with full-stack digital portfolios from hardware to data analytics are gaining competitive traction as rail agencies streamline vendor ecosystems.

Key Report Takeaways

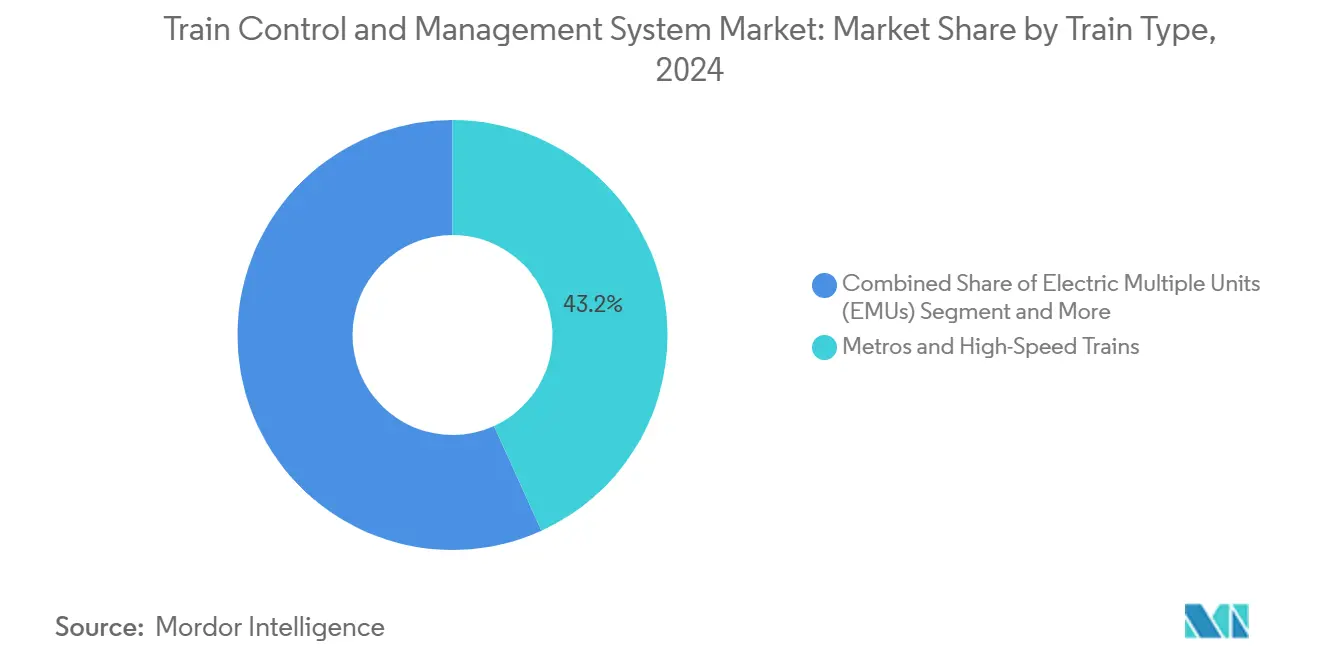

- By train type, Metros and High-Speed Trains led with 43.15% of the train control and management system market share in 2024; Electric Multiple Units are forecast to expand at an 8.56% CAGR through 2030.

- By component, Vehicle Control Units accounted for 39.04% of the train control and management system market share in 2024, while Mobile Communication Gateways are advancing at a 9.08% CAGR to 2030.

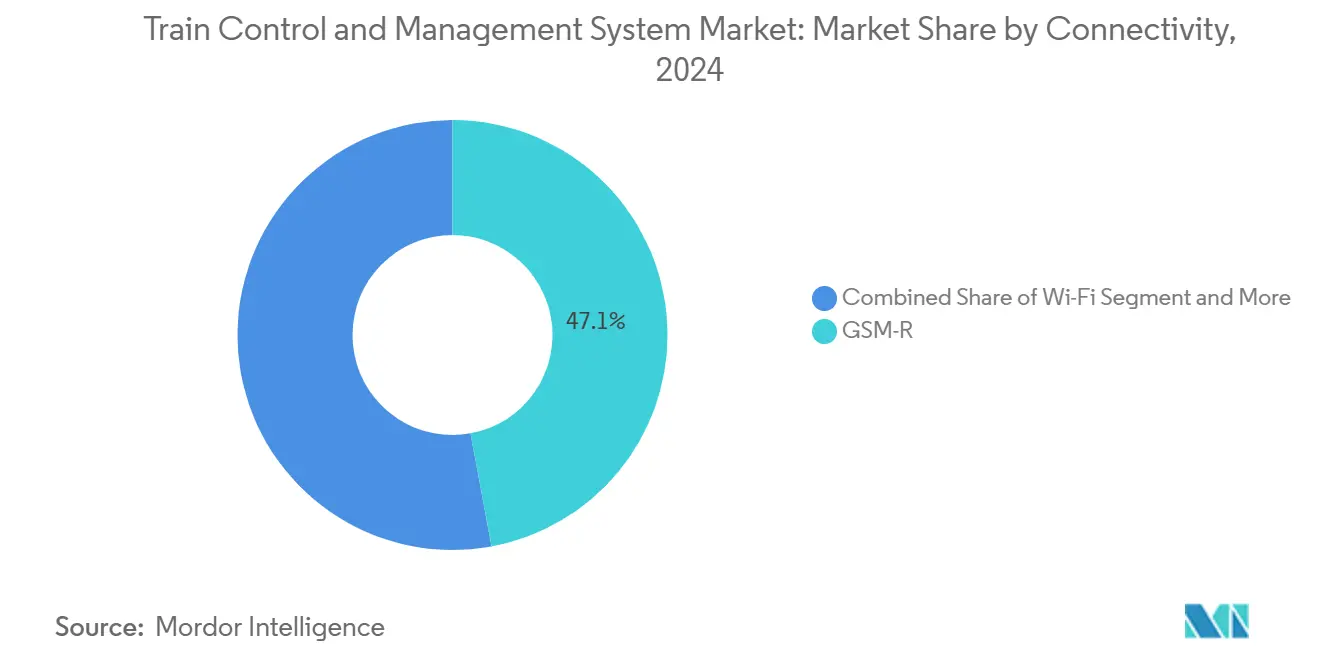

- By connectivity, GSM-R held 47.12% of the train control and management system market share in 2024; Wi-Fi solutions are projected to rise at a 9.45% CAGR during 2025-2030.

- By control solution, Communication-Based Train Control (CBTC) captured 53.41% of the train control and management system market share in 2024, whereas Integrated Train Control platforms are set to grow at a 10.04% CAGR through 2030.

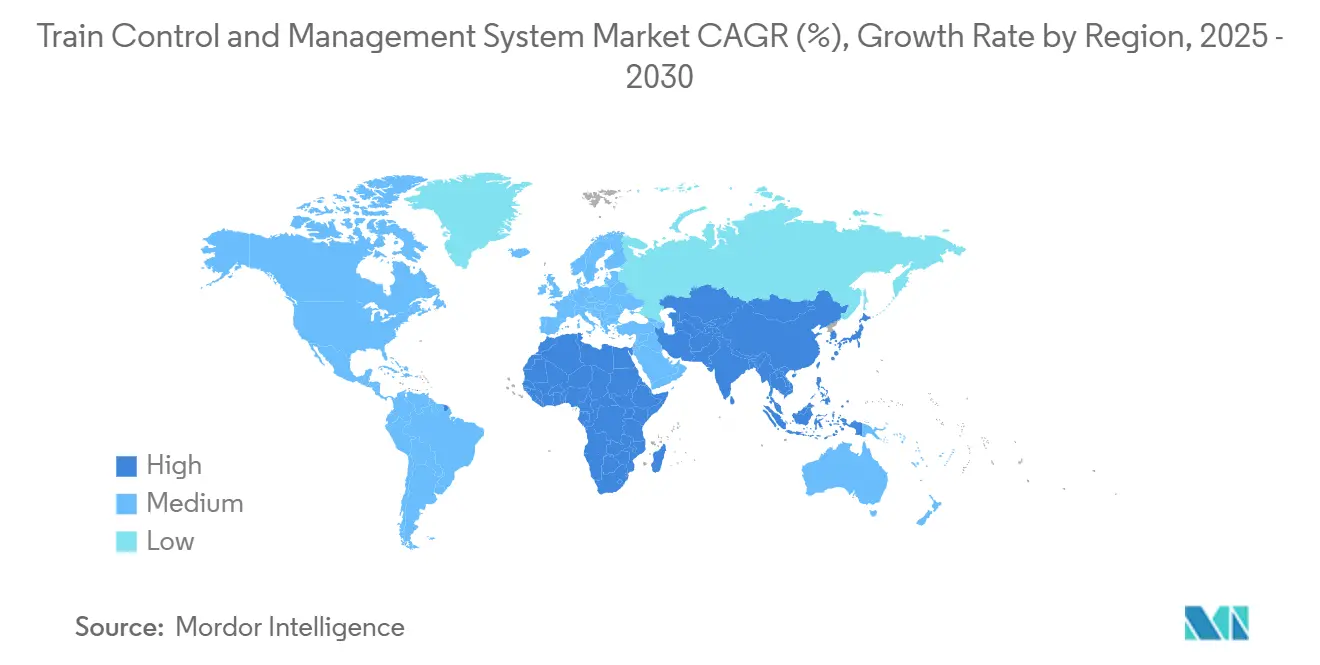

- By geography, Asia-Pacific dominated with a 39.66% of the train control and management system market share in 2024 and is poised for an 8.13% CAGR to 2030.

Global Train Control And Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urban Rail Expansion | +1.8% | APAC core; spill-over to MEA | Medium term (2-4 years) |

| Upgrade Cycles to Digital Signaling | +1.5% | Global; early gains in Europe and APAC | Medium term (2-4 years) |

| Mandatory Safety Regulations (EU TSI) | +1.2% | Europe; adoption elsewhere | Long term (≥ 4 years) |

| Moving-Block ETCS Level 3 Adoption | +1.1% | Europe core; expanding to APAC | Long term (≥ 4 years) |

| Rising Demand for Energy-Efficient Rail | +0.9% | Global | Long term (≥ 4 years) |

| Digital-Twin-Based Predictive Maintenance | +0.8% | North America and EU; global rollout | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban Rail Expansion in Emerging Economies

Megacities in China, India, and Southeast Asia are commissioning unprecedented lengths of metro track, often exceeding 1,000 kilometers of new lines annually in China alone. These greenfield projects specify CBTC and autonomous operation from day one, eliminating costly retrofits typical in mature networks. Governments view rail as a lever for job creation, with every USD 1 billion invested supporting roughly 30,000 positions while cutting bus-related emissions. Standardized system architectures across city clusters let suppliers scale reference designs, accelerating deployment schedules and lowering unit costs. Operators also gain integrated energy management and predictive maintenance modules that reduce lifecycle expenses. Consequently, advanced control platforms become embedded in regional infrastructure blueprints rather than discretionary add-ons.

Upgrade Cycles From Analog to Digital Signaling (ETCS, CBTC)

Digital signaling can raise corridor capacity by 20-40% without track widening, making it the default strategy for saturated European routes. Deutsche Bahn targets nationwide ETCS rollout by 2030, and SNCF’s command-center modernization covers both TGV and conventional lines [1]“Command-center modernization program,” SNCF Group, sncf.com. Parallel CBTC deployments in metros cut headways to under 90 seconds, translating into higher farebox revenue and better fleet utilization. During migration, operators must dual-run analog and digital systems, creating a lucrative replacement market for interface hardware and integration services. The shift also unlocks data monetization opportunities, from dynamic timetable optimization to real-time seat-occupancy analytics.

Mandatory Safety Regulations (e.g., EU Technical Specifications for Interoperability)

Europe’s TSI framework obliges passenger and freight operators to implement ETCS Levels 2 and 3, prompting a ripple effect across non-EU corridors that link to European routes [2]“Digital rail solutions fact sheet,” Siemens AG, siemens.com. Compliance windows accelerate procurement, while the cybersecurity clauses aligned with the NIS2 Directive elevate demand for secure protocols and intrusion detection. Suppliers with established CE-marking workflows and in-house certification labs realize shorter approval cycles, allowing them to price more competitively. Beyond Europe, South American and Middle-Eastern projects adopt TSI-compliant subsystems to secure multilateral funding tied to interoperability benchmarks. The regulations thus act as an export catalyst for European technologies.

Adoption of Moving-Block ETCS Level 3 to Boost Line Capacity

Moving-block logic removes fixed block constraints, spacing trains dynamically according to real-time speed and braking curves. Early pilots in Switzerland and Denmark record significant throughput gains on congested trunk lines. As ERTMS specifications mature, suppliers bundle Level 3 modules in standard product roadmaps, trimming incremental costs. Freight carriers in Europe and Asia eye the technology to increase axle-load productivity without expensive siding extensions, expanding the demand pool beyond metros and high-speed services.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX, Long ROI for Rail | -1.3% | Global | Short term (≤ 2 years) |

| Complex Multi-Vendor Interoperability Challenges | -0.9% | Global; acute in Europe | Medium term (2-4 years) |

| Escalating Cybersecurity Compliance Costs | -0.7% | North America and EU; global spread | Medium term (2-4 years) |

| 5G Spectrum Uncertainty for GSM-R Sunset | -0.6% | Europe core; global implications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Long ROI Periods for Rail Operators

Complete CBTC installations can incur significant cost per route kilometer on freight lines, stretching payback horizons to a decade for operators that monetize capacity gradually [3]“Infrastructure investment financing trends 2025,” Economic Commission for Latin America and the Caribbean, cepal.org. Urban agencies face political pressure to favor visible civil works over back-office electronics, delaying control-system refresh cycles. Leasing and performance-based contracts shift some risk to vendors but often increase total lifecycle expense. Finance ministries and multilateral lenders increasingly condition low-interest loans on energy-efficiency or safety-improvement metrics, nudging agencies toward phased procurement that matches annual budget envelopes.

Complex Multi-Vendor Interoperability Challenges

A fragmented supply chain can double implementation timelines and inflate costs versus single-vendor projects. European corridors that serve multiple operators expose the issue acutely: infrastructure managers, rolling-stock owners, and tech providers must harmonize interfaces covering data models, fail-safe logic, and cybersecurity policies. Legacy equipment adds complexity as bespoke gateways bridge analog and IP networks. Service disruptions tied to compatibility failures trigger penalties that dwarf initial savings from multi-source bidding, motivating agencies to pre-qualify integrators with proven orchestration credentials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Train Type: EMUs Anchor Electrification Momentum

Metros and High-Speed Trains still command 43.15% of the train control and management system market share in 2024, but their share is expected to decline marginally as EMUs penetrate intercity routes. The train control and management system market size for Electric Multiple Units (EMUs) is expanding rapidly, with the segment projected to post an 8.56% CAGR through 2030. EMUs benefit from lower operating costs and cleaner propulsion, making them the default option for suburban and regional services in newly electrified corridors. Emerging economies that deploy rail for climate-mitigation goals skip diesel phases and go straight to electric rolling stock.

Advanced control modules integrated into EMUs unlock regenerative braking coordination and load balancing that trim traction energy by 15-25% compared with legacy setups. Driverless metro configurations further boost demand for sensor fusion and fail-safe logic within Vehicle Control Units, carving opportunities for suppliers with software-centric portfolios.

By Component: Mobile Gateways Accelerate Connectivity Evolution

Vehicle Control Units captured the largest 39.04% of the train control and management system market share in 2024, reflecting their centrality to safety-critical tasks. Nevertheless, Mobile Communication Gateways are forecast for a 9.08% CAGR through 2030, riding the wave of 5G-ready FRMCS deployments. Operators view gateways as pivotal enablers for predictive maintenance, passenger Wi-Fi, and real-time diagnostics, turning connectivity into a value generator rather than overhead.

Modular gateway architectures permit hot-swappable radio cards, allowing fleets to transition from GSM-R to 5G without total hardware replacement. Parallel advances in Human-Machine Interfaces introduce touchscreens and augmented-reality overlays that streamline driver workflows and maintenance checks. Suppliers capable of providing secure, over-the-air software updates differentiate themselves as cyber mandates tighten.

By Connectivity: Wi-Fi Bridges the 5G Gap

Although GSM-R retained a 47.12% of the train control and management system market share in 2024, the technology’s sunset sparks a dual-track investment pattern. Agencies migrate non-mission-critical services, ticketing, CCTV backhaul, passenger internet to Wi-Fi, which is growing at a 9.45% CAGR toward 2030. This incremental path avoids disturbing safety-critical applications until 5G spectrum becomes definitive.

TETRA persists in industrial and mining railways where ruggedized voice and narrowband data suffice. Europe’s FRMCS trials set benchmarks that North America and Asia monitor, yet differing spectrum policies may yield regional implementation variants. Integration layers that abstract radio technologies shield application software from underlying changes, easing future migrations.

By Train Control Solution: Integrated Platforms Gain Ground

Communication-Based Train Control (CBTC) maintained a dominant 53.41% of the train control and management system market share in 2024, cemented by widespread metro rollouts in Asia-Pacific megacities. However, operator appetite for platform consolidation propels Integrated Train Control systems toward a 10.04% CAGR through 2030. Unified platforms blend CBTC, ETCS, energy analytics, and diagnostics under one software suite, slashing vendor interfaces and simplifying certification audits.

Positive Train Control in North America transitions into an enhancement phase, focusing on energy optimization and fleet-wide data integration. Vendors incorporating cybersecurity by design win bids as agencies evaluate lifecycle vulnerabilities introduced by cloud links and remote maintenance.

Geography Analysis

Asia-Pacific accounted for 39.66% of the train control and management system market share in 2024 and is forecast to have an 8.13% CAGR to 2030, underpinned by China’s multi-billion-dollar metro pipeline and India’s plan to extend metro systems across several cities. Regional authorities link rail expansion to economic development and emissions targets, guaranteeing predictable procurement schedules that help vendors scale local manufacturing hubs. Suppliers with Mandarin and Hindi localization, plus strong after-sales networks, hold a competitive edge.

Europe advances through mandatory ETCS adoption, generating a steady replacement stream as legacy signaling phases out. National track owners coordinate funding with EU infrastructure envelopes, supporting joint procurement that spreads risk across borders. High labor costs incentivize automation, benefitting vendors of driverless technologies and centralized traffic management.

North America enters a post-mandate landscape where the installed PTC backbone becomes a springboard for data-driven freight optimization. Agencies channel budgets toward energy savings and resilience against severe weather events. Latin America shows sporadic growth, highlighted by São Paulo’s ETCS Level 2 deployment, though macroeconomic volatility tempers immediate prospects. Middle East megaprojects, Etihad Rail in the UAE and Saudi Arabia’s planned high-speed links offer long-term opportunities, provided bidders navigate local-content clauses and security requirements.

Competitive Landscape

The train control and management system market features moderate concentration, with Siemens, Alstom, and Hitachi Rail leveraging global footprints and full-line portfolios to clinch turnkey contracts. Their integrated offerings encompass hardware, software, and lifecycle services, meeting operator preference for single-throat accountability.

Mid-tier companies specialize in cybersecurity, digital twins, or edge analytics, forming alliances with OEMs to plug niche gaps. Recent tie-ups pair rolling-stock builders with cloud providers, marrying operational technology to IT expertise. Start-ups focus on SaaS-based energy-management modules that bolt onto legacy systems, generating recurring revenue beyond initial capex.

Strategic moves include Alstom’s purchase of a cybersecurity boutique to harden its portfolio and Siemens’ partnership with a 5G chipset vendor to accelerate FRMCS readiness. Hitachi Rail invests in digital-twin labs that shorten validation cycles and cut physical prototyping costs. Buyers increasingly weigh measurable outcomes, energy-cut percentages, punctuality gains over mere technical compliance, reshaping RFP scoring criteria.

Train Control And Management System Industry Leaders

Siemens Mobility GmbH

Alstom SA

Hitachi Rail STS

Thales Group

Wabtec Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Alstom agreed with ViaMobilidade and São Paulo’s government to install Latin America’s first ETCS Level 2 on Metro Lines 8 and 9.

- February 2025: San Francisco MTA advanced its Train Control Upgrade Project, selecting Hitachi Rail’s CBTC solution for the 71-mile Muni Metro network.

- December 2024: Stadler secured a USD 500 million contract with MARTA to deploy NOVA Pro CBTC across Atlanta’s heavy-rail system.

- April 2024: BEML and Bharat Electronics inked an MOU to co-develop an indigenous i-TCMS platform for Indian railways.

Global Train Control And Management System Market Report Scope

| Metros and High-Speed Trains |

| Electric Multiple Units (EMUs) |

| Diesel Multiple Units (DMUs) |

| Vehicle Control Units (VCU) |

| Mobile Communication Gateway |

| Human-Machine Interface (HMI) |

| Others |

| GSM-R |

| Wi-Fi |

| TETRA |

| Others |

| Communication-Based Train Control (CBTC) |

| Integrated Train Control |

| Positive Train Control (PTC) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Train Type | Metros and High-Speed Trains | |

| Electric Multiple Units (EMUs) | ||

| Diesel Multiple Units (DMUs) | ||

| By Component | Vehicle Control Units (VCU) | |

| Mobile Communication Gateway | ||

| Human-Machine Interface (HMI) | ||

| Others | ||

| By Connectivity | GSM-R | |

| Wi-Fi | ||

| TETRA | ||

| Others | ||

| By Train Control Solution | Communication-Based Train Control (CBTC) | |

| Integrated Train Control | ||

| Positive Train Control (PTC) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the train control and management system market in 2025?

The train control and management system market size is valued near USD 4.50 billion in 2025, tracking toward USD 6.46 billion by 2030.

Which train type shows the fastest growth through 2030?

Electric Multiple Units are projected to register the highest 8.56% CAGR due to global electrification drives.

What region leads demand for advanced train control solutions?

Asia-Pacific commands the largest 39.66% share and posts an 8.13% CAGR thanks to massive metro expansions.

Which components attract the quickest investment?

Mobile Communication Gateways grow at 9.08% CAGR as connectivity becomes pivotal for predictive maintenance and passenger services.

Page last updated on: