Railway Maintenance Machinery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.77 Billion |

| Market Size (2031) | USD 6.21 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Railway Maintenance Machinery Market Analysis by Mordor Intelligence

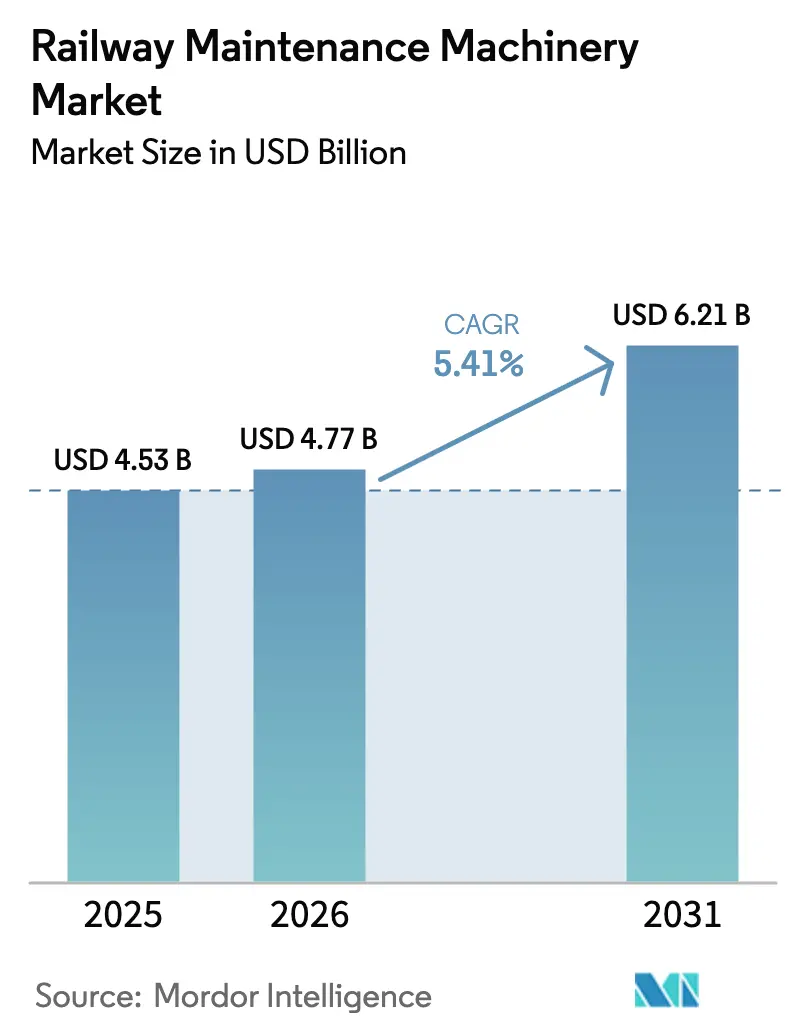

The Railway Maintenance Machinery Market size was valued at USD 4.53 billion in 2025 and estimated to grow from USD 4.77 billion in 2026 to reach USD 6.21 billion by 2031, at a CAGR of 5.41% during the forecast period (2026-2031). This healthy trajectory underpins sustained public-sector rail capital expenditure, rapid high-speed network build-outs, and rising freight-corridor investments. Operators focus on life-extension programs for aging assets, accelerating demand for rail grinding, tamping, and ballast cleaning systems. OEMs are bundling equipment with lifecycle-service contracts to secure recurring revenue, while hybrid and battery-electric powertrains gain ground as environmental regulations tighten.

Key Report Takeaways

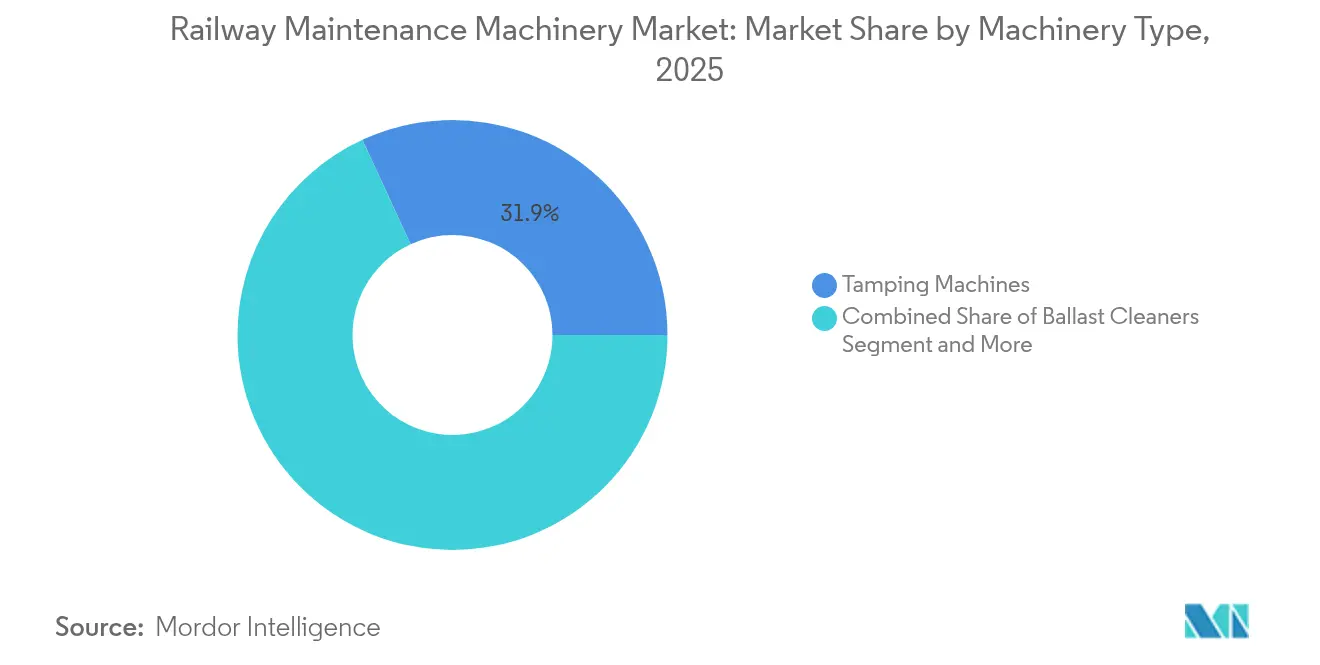

- By machinery type, tamping machines led with 31.88% revenue share in 2025; rail grinding and milling systems are forecast to expand at a 6.29% CAGR through 2031.

- By application, ballast track accounted for 51.25% of the railway maintenance machinery market size in 2025, while slab track is advancing at a 5.48% CAGR to 2031.

- By sales channel, OEM direct sales held 72.95% of the railway maintenance machinery market share in 2025, whereas distributor channels recorded the highest projected CAGR at 6.04% through 2031.

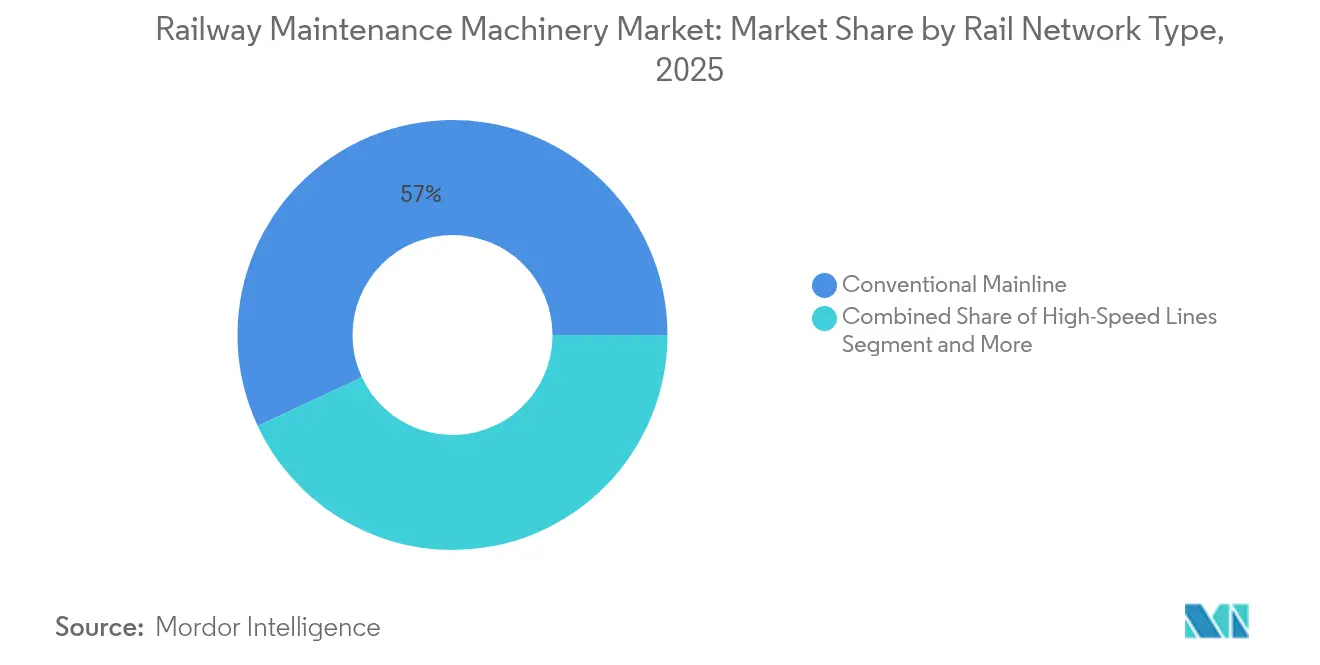

- By rail network type, conventional mainlines represented 56.95% share in 2025; high-speed lines are the fastest-growing segment at a 6.47% CAGR to 2031.

- By power source, diesel-hydraulic platforms retained a 65.60% share in 2025; hybrid/battery-electric units are set to grow at a 5.87% CAGR over the forecast period.

- By geography, Asia Pacific dominated with 38.20% revenue share in 2025, leading growth prospects at a 7.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Railway Maintenance Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Public-Sector Rail CAPEX | +1.8% | Asia Pacific, Europe | Medium term (2-4 years) |

| Electrification-Driven Track Renewals | +1.2% | Global, concentrated in Asia Pacific & Europe | Long term (≥ 4 years) |

| Ageing Legacy Infrastructure in North America | +0.9% | North America | Short term (≤ 2 years) |

| Expansion of Dedicated Freight Corridors | +0.7% | Global, spill-over to emerging markets | Medium term (2-4 years) |

| OEM-Guaranteed Lifecycle-Service Contracts | +0.6% | Global | Short term (≤ 2 years) |

| Automation-Ready MOW Fleets | +0.5% | North America & EU, early adoption in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Public-Sector Rail CAPEX in Asia & Europe

Record government outlays are reshaping the railway maintenance machinery market. The European Union has approved over EUR 7 billion in grants for 134 transport projects, with 80% earmarked for rail infrastructure.[1]“CEF Transport: EUR 7 Billion Investment Package,” European Commission, europa.eu Germany’s EUR 500 billion rail modernization plan and China’s push toward a 50,000 km high-speed network drive persistent demand for tamping machines, ballast cleaners, and integrated service packages. OEMs now embed predictive-maintenance analytics and fleet leasing options to win multi-year contracts. Vietnam’s USD 67 billion North–South high-speed line signals new regional demand pockets, while comprehensive workforce plans targeting 338,000 rail employees by 2030 create parallel requirements for training simulators and support services.

Electrification-Driven Track Renewals Across High-Speed Corridors

Global decarbonization efforts accelerate electrification programs such as the UK Government’s GBP 1 billion Network North initiative and the USD 66 billion allocation in the US Bipartisan Infrastructure Law. Electrified routes need machinery configured for catenary clearance and insulated tooling, prompting a product shift toward height-restricted tampers and rail grinders with onboard measurement sensors. High-speed corridors impose stricter tolerance and inspection intervals; CRTS I slab track sections in China have posted 22.4% compressive-strength declines after 10 years, amplifying the need for non-intrusive monitoring platforms. Predictive maintenance software tied to on-track equipment is gaining traction as operators aim to achieve near-zero unplanned outages.

Ageing Legacy Infrastructure in North America Requiring Life-Extension Overhauls

Class I railroads boosted maintenance-of-way (MOW) budgets to USD 5.1 billion in 2024, up from USD 4.9 billion in 2023.[2]“2024 Capital Investment Plan,” BNSF Railway, bnsf.com BNSF replaces 365 miles of rail and 2.8 million ties, while Union Pacific allocates USD 3.4 billion for infrastructure and locomotive upgrades. Rail grinding now costs USD 22,500–45,000 daily, underscoring the complexity of re-profiling worn railhead geometries. AI-enabled machine-vision systems capture 35 million wheel interface readings daily, feeding analytics platforms that schedule tamping and surfacing tasks more accurately. These digital overlays augment demand for equipment capable of streaming real-time condition data.

Expansion of Dedicated Freight Corridors Boosts Upkeep Demand

Heavy-haul freight corridors induce higher wear rates, spurring specialty ballast cleaning and rail-milling demand. Canadian National Railway’s CAD 3.4 billion 2025 budget plans over 225 miles of rail installation and multiple western-Canada capacity projects.[3]“2025 Capital Expenditure Outlook,” Canadian National Railway, cn.ca The EU intends to double rail freight traffic by 2050, funding port-rail links such as the Marseille intermodal hub. Drone-based automated yard checks adopted by BNSF raise inspection accuracy by 20%, encouraging procurement of compatible autonomous MOW fleets. Chinese-backed freight lines in Thailand and Vietnam extend these opportunities into Southeast Asia, further enlarging the addressable fleet for the railway maintenance machinery market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost | -0.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Skills Shortage for Machinery Operation | -0.6% | North America & EU, spreading to Asia Pacific | Medium term (2-4 years) |

| Volatile Steel Prices | -0.4% | Global | Short term (≤ 2 years) |

| Fragmented Rail-Standards | -0.3% | Global, acute in Europe & Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Tampers & Ballast Cleaners

Premium tamping or ballast-cleaning units with GPS stabilization, automated leveling, and hybrid drives cost several million dollars and require dedicated depots, software licenses, and operator training. Emerging-market railways often face currency volatility and limited access to long-term finance, delaying fleet renewal. Hybrid and battery-electric upgrades add 15–20% to list prices, creating a dilemma between sustainability goals and budget realism. Leasing models are gaining traction; GATX reported 99.3% fleet utilization and renewal rates above 80%, signaling acceptance of pay-per-use schemes that lower capital barriers.

Skills Shortage for Advanced On-Track Machinery Operation

Digital-ready fleets need personnel versed in GPS alignment, automated controls, and data analytics. City & Guilds’ bootcamps show 90% placement rates into skilled rail maintenance roles, but still undersupply labor versus demand. Retirements of veteran tamping crews compress institutional knowledge, while high-speed networks require stricter safety certification. As equipment becomes more automated, operators must interpret system diagnostics rather than perform purely mechanical tasks, raising the baseline competence level and widening the talent gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Tamping Machines Lead, Grinding Systems Accelerate

Tamping machines captured 31.88% revenue share in 2025, underscoring their indispensable role in post-installation stabilization and cyclical ballast maintenance. This railway maintenance machinery market slice is anchored by universal track-geometry requirements across freight, passenger, and metro networks. Rail grinding and milling systems top the growth chart at a 6.29% CAGR, buoyed by life-extension strategies that defer costly rail replacements.

Growing adoption of continuous-action tampers and high-output combination machines is shortening track-possession windows. Meanwhile, automated grinding trains equipped with multi-sensor inspection pods illustrate convergence between material-removal and condition-assessment functions. OEMs add subscription-based software that converts on-board telemetry into maintenance recommendations, increasing the stickiness of after-sales revenue streams and expanding the overall railway maintenance machinery market.

By Application: Ballast Track Dominance Faces Slab Track Challenge

Ballast track accounted for 51.25% of total revenue in 2025, benefiting from a vast installed base of conventional lines. Slab track, however, is pacing at a 5.48% CAGR through 2031 as high-speed and urban transit projects seek lower lifecycle costs and reduced vibration. Slab-track growth alters equipment demand: tamping loses relevance while precision rail-grinding, automated ultrasonic inspection, and slab-lifting devices gain importance.

China’s CRTS I lines highlight advantages and maintenance complexities, with compressive-strength declines necessitating intensive monitoring. Lifecycle-cost modeling increasingly guides procurement, pushing operators toward machinery with lower total-cost-of-ownership credentials, thereby reshaping the railway maintenance machinery market.

By Sales Channel: OEM Direct Sales Dominate amid Distributor Growth

In 2025, OEM direct sales controlled 72.95% of market revenue, reflecting the need for deep technical support and tailored financing for multi-million-dollar assets. Distributor networks, however, register a faster 6.04% CAGR as regional players offer refurbished stock, localized service, and flexible rental plans.

Progress Rail’s six-year maintenance deal with PT Kereta Indonesia illustrates the blending of equipment supply and long-term service scope. As tenders increasingly mandate lifecycle performance guarantees, local dealer footprints become critical for rapid parts delivery and remote-diagnostic support, reinforcing the shift toward hybrid direct-plus-dealer models in the railway maintenance machinery market.

By Rail Network Type: Conventional Mainlines Lead as High-Speed Segments Surge

Conventional mainlines delivered 56.95% revenue in 2025, reflecting widespread freight and mixed-traffic infrastructure. High-speed corridors, however, post a 6.47% CAGR, driven by China’s network expansion, Europe’s TEN-T build-outs, and emerging markets’ flagship projects. High-speed lines require tighter alignment tolerances, automated slab inspection, and ETCS-compatible equipment.

Urban metros pursue compact, low-noise machinery, whereas heavy-haul freight lines demand ruggedized ballast and grinding assets capable of absorbing higher axle loads. This diversity broadens addressable demand and pushes suppliers to develop configurable platforms covering multiple duty cycles within the broader railway maintenance machinery market.

By Power Source: Diesel-Hydraulic Dominance Challenged by Hybrid Innovation

Diesel-hydraulic units retain 65.60% share, prized for range, refueling speed, and entrenched maintenance know-how. Yet hybrid and battery-electric variants grow at a 5.87% CAGR as operators target emission-reduction targets. Canadian National Railway’s hybrid locomotive pilot seeks 50% fuel cuts, while Wabtec’s R255 hybrid work locomotives now serve New York City subway maintenance after eight-hour zero-emission approvals.

Operators weigh upfront cost premiums against future carbon-pricing risks and noise restrictions in urban tunnels. Diesel-electric hybrids offer an interim step, preserving familiarity while enabling regenerative braking, gradually tilting the railway maintenance machinery market toward lower-carbon alternatives.

Geography Analysis

Asia Pacific commanded 38.20% of the railway maintenance machinery market in 2025 and is expanding at 7.24% CAGR to 2031, fueled by record infrastructure spending in China and India. China plans to add 3,800 km of new high-speed lines in 2025 on its path to a 50,000 km network target. India’s USD 30 billion railway budget backs nationwide electrification and the roll-out of 4,000 Vande Bharat trainsets. Urban rail mileage across 59 Chinese cities reached 11,123.65 km in 2024, creating a sizable installed base that needs metro-specific tampers and rail-grinding equipment.

Europe remains a mature yet investment-heavy arena, underpinned by the European Union’s EUR 7 billion grant package that directs 80% of funds to rail modernization. Germany’s EUR 500 billion rail program emphasizes digital signaling and high-output tamping fleets able to meet tight possession windows. The United Kingdom is channeling GBP 1 billion through Network North to accelerate electrification and associated track-renewal works. Technical Specifications for Interoperability standardize equipment interfaces, allowing OEMs to market modular machines across borders without extensive re-engineering.

North America is a replacement-driven market as mid-20th-century infrastructure reaches end-of-life. BNSF’s USD 3.92 billion plan covers 365 miles of rail replacement and 2.8 million ties, while Union Pacific allocates USD 3.4 billion to geometry corrections and locomotive overhauls. Mexico and Canada add capacity along port-energy corridors, boosting orders for heavy-haul ballast cleaners and automated inspection drones. In South America, Brazil’s Ferrogrão and Argentina’s Belgrano upgrades spark niche demand, whereas GCC railways specify desert-resistant hydraulics and sand-filtration kits for extreme climates.

Competitive Landscape

The railway maintenance machinery market is moderately fragmented, with European incumbents and fast-scaling Asian firms competing on technology depth and service reach. Plasser & Theurer leverages over 70 years of know-how and over 10,000 patents to defend its share in tamping and high-output track-renewal trains. CRCC High-Tech Equipment capitalizes on China’s vast domestic needs to expand export sales across Asia, Africa, and South America. Loram Maintenance of Way bundles rail-grinding hardware with proprietary analytics, positioning itself as an end-to-end rail-health partner for Class I operators.

Strategic consolidation is gathering pace as suppliers seek scale and complementary technologies. Wabtec paid USD 960 million for Dellner Couplers, adding 100,000 installed coupler units and USD 250 million in projected 2025 revenue to its passenger-rail portfolio. EQT Infrastructure VI agreed to acquire Eagle Railcar Services, gaining 13 US repair sites and about 1,500 employees to bolster rolling-stock maintenance capabilities. These deals mirror earlier moves by Progress Rail and Alstom to lock in service contracts that provide predictable cash flows and deepen customer engagement across equipment lifecycles.

Technology integration now separates leaders from followers. OEMs embed AI-driven condition monitoring, autonomous tamping controls, and hybrid powertrains to deliver measurable fuel and labor savings. Alstom reports a 95% renewal rate on operations-and-maintenance agreements, underscoring the stickiness of service-centric models alstom.com. High certification barriers, complex mechanical-hydraulic integration, and the need for 24/7 parts logistics keep new entrants at bay, while niche innovators often partner with major brands for distribution reach. With the top five suppliers holding nearly 55% combined share, competitive intensity remains high but balanced by ongoing specialization and digital-service expansion within the railway maintenance machinery market.

Railway Maintenance Machinery Industry Leaders

Plasser & Theurer Export von Bahnbaumaschinen Gesellschaft m. b. H.

China Railway Construction Corporation Limited

MATISA MATÉRIEL INDUSTRIEL S.A.

Loram Maintenance of Way

Enviri (Harsco Rail/Progress Rail)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: EQT Infrastructure VI agreed to acquire Eagle Railcar Services, adding 13 US repair sites and 1,500 employees to its rail-services portfolio.

- March 2025: Wabtec Corporation completed the USD 960 million purchase of Dellner Couplers, expanding its installed base of 100,000 couplers worldwide and targeting USD 250 million revenue in 2025.

- January 2025: Canadian National Railway launched a medium-horsepower hybrid locomotive pilot with Knoxville Locomotive Works, featuring a 2.4 MWh battery-diesel stack targeting 50% fuel savings.

- January 2025: Wabtec’s R255 hybrid battery-diesel work locomotives gained New York MTA approval for subway maintenance, offering up to eight hours of zero-emission operation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study measures revenue from brand-new on-track machines, tampers, ballast cleaners, rail grinders, track-laying systems, and diagnostic vehicles that keep conventional, high-speed, and urban rail lines serviceable. Figures appear in USD for 2019-2030.

Scope exclusion: Refurbished units, software-only solutions, service contracts, and spare parts lie outside this scope.

Segmentation Overview

- By Machinery Type

- Tamping Machines

- Ballast Cleaners

- Rail Grinding & Milling Systems

- Stabilising & Lining Equipment

- Rail Handling & Renewal Trains

- Surface & Vegetation Control Machinery

- By Application

- Ballast Track

- Non-Ballast (Slab) Track

- By Sales Channel

- Original-Equipment Manufacturer (OEM)

- Distributor / Dealer

- By Rail Network Type

- Conventional Mainline

- High-Speed Lines

- Urban Transit / Metro

- Heavy-Haul Freight

- By Power Source

- Diesel-Hydraulic

- Diesel-Electric

- Hybrid / Battery-Electric

- Electric

- Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- Egypt

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed maintenance planners at state railroads, buyers at Asia-Pacific and European metros, and product managers at leading OEMs. The conversations clarified live CAPEX pipelines, hybrid-drive uptake, and typical machine lifespans, fine-tuning assumptions carried into our sizing.

Desk Research

We drew baseline data from the International Union of Railways, World Bank rail infrastructure tables, the European Union Agency for Railways, and the US Federal Railroad Administration. Tender logs on Volza, patent counts via Questel, and OEM filings revealed shipment volumes and price corridors, while Dow Jones Factiva news confirmed recent fleet orders. These sources illustrate the broader desk review that underpins our model.

Market-Sizing & Forecasting

A top-down build starts with installed track kilometers and standard upkeep spend per kilometer, then adjusts for electrification share, axle-load intensity, and renewal backlog. Bottom-up spot checks, OEM dispatch records and sample ASP × volume estimates, calibrate totals. Key variables include annual track additions, machine life cycles, national rail budgets, hybrid penetration, and tamping-cycle frequency. Multivariate regression, stress-tested under policy and cost scenarios, projects values through 2030; any data gaps are filled with conservative ranges agreed during expert calls.

Data Validation & Update Cycle

Outputs pass variance checks against tender awards and import statistics before senior review. Reports refresh each year, with interim tweaks for material events, and a final analyst sweep ensures clients receive the latest view.

Why Mordor's Railway Maintenance Machinery Baseline Commands Reliability

Published estimates often differ because some firms blend service revenue with new-equipment sales, reuse stale currency rates, or assume very short replacement cycles.

Mordor Intelligence confines scope to factory-fresh machinery, applies consensus lifespans validated in 2025 expert calls, and updates exchange rates at every refresh, delivering a balanced, transparent baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.53 Bn (2025) | Mordor Intelligence | - |

| USD 5.30 Bn (2023) | Global Consultancy A | Includes refurbished units and retrofit services, older base year |

| USD 4.31 Bn (2023) | Industry Journal B | Uses uniform ASP worldwide, limited primary validation |

The comparison highlights how Mordor Intelligence grounds its figures in clear scope choices, fresh variables, and repeatable steps, giving decision-makers a number they can trust.

Key Questions Answered in the Report

What is the current size of the railway maintenance machinery market?

The market is valued at USD 4.77 billion in 2026 and is forecast to grow to USD 6.21 billion by 2031 at a 5.41% CAGR.

Which region shows the fastest growth?

Asia Pacific leads with a 7.24% CAGR to 2031, driven by China’s high-speed build-out and India’s USD 30 billion modernization budget.

Which machinery segment is expanding the quickest?

Rail grinding and milling systems post the highest CAGR at 6.29%, reflecting a strategic pivot toward rail-life-extension practices.

How are sustainability goals influencing equipment choices?

Hybrid and battery-electric powertrains are gaining traction, growing at a 5.87% CAGR as operators seek to reduce emissions and lower operating costs.

Why are lifecycle-service contracts becoming common in tenders?

Operators seek guaranteed performance, predictable costs, and embedded analytics; OEMs bundle services to secure long-term revenue and customer lock-in.

What is the biggest restraint for new buyers?

High upfront costs for advanced tampers and ballast cleaners remain a barrier, although leasing and rental models are helping to mitigate capital hurdles.

Page last updated on: