Railway Track Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 35.23 Billion |

| Market Size (2031) | USD 41.06 Billion |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

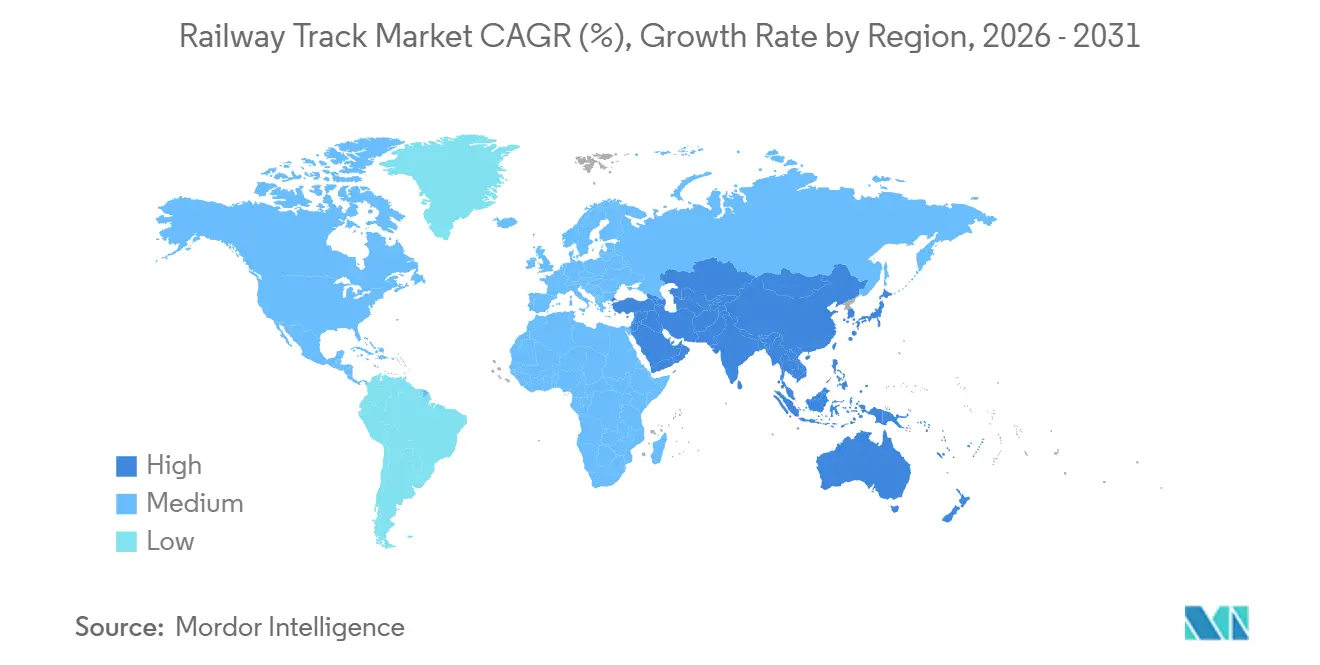

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Railway Track Market Analysis by Mordor Intelligence

The Railway Track Market size is projected to expand from USD 34.17 billion in 2025 and USD 35.23 billion in 2026 to USD 41.06 billion by 2031, registering a CAGR of 3.11% between 2026 and 2031. Asia-Pacific governments are front-loading capital into new high-speed passenger and heavy-haul freight corridors, while steel price volatility and lengthy environmental reviews are slowing replacement cycles in Europe and North America. Suppliers that bundle rail, fastening systems, and digital monitoring into turnkey packages are capturing wallet share as public-private partnerships (PPPs) expand procurement horizons. At the same time, component makers that patent clip geometry or embed sensors in fasteners are earning higher margins than commodity rail mills. Finally, climate-resilient track standards and welding labor shortages are accelerating demand for ballastless slab designs, modular pre-assembled panels, and AI-enabled predictive maintenance platforms.

Key Report Takeaways

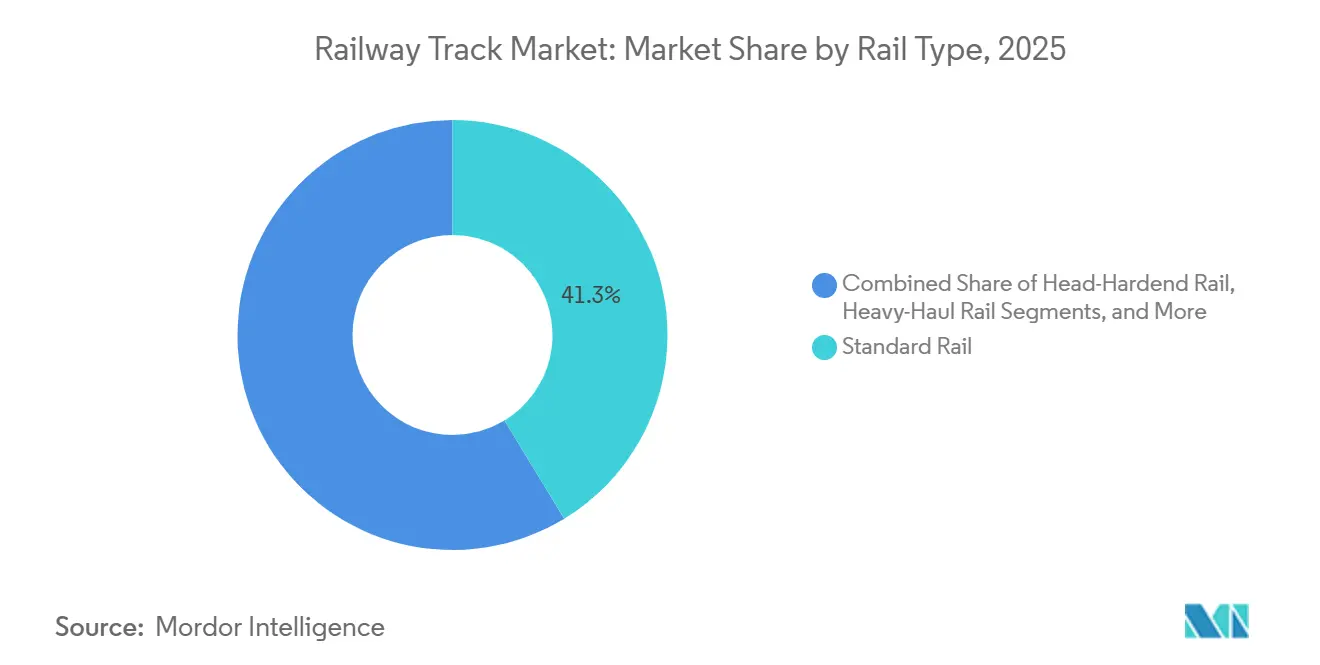

- By rail type, standard rail led with 41.27% revenue share of the railway track market in 2025; head-hardened rail is advancing at a 3.13% CAGR through 2031.

- By component, rails accounted for 55.27% of the railway track market size in 2025, while fastening systems are expanding at a 3.31% CAGR to 2031.

- By application, freight accounted for 38.71% in 2025, and high-speed corridors are forecast to post a 3.15% CAGR through 2031.

- By rail weight class, the 50-60 kg/m segment led with 36.17% of revenue in 2025; in the railway track market, the more-than-60 kg/m segment is projected to expand at a 3.17% CAGR through 2031.

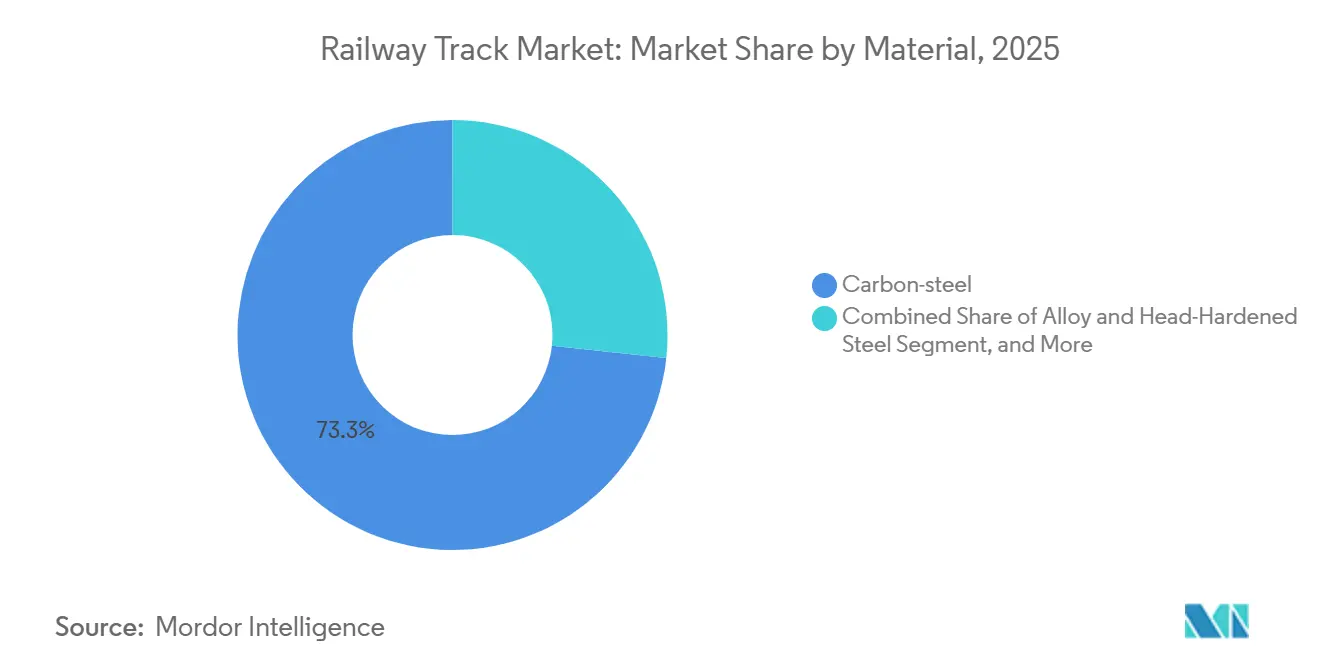

- By material, carbon steel retained a 73.27% share in 2025, and composite or hybrid polymer parts are growing at a 3.33% CAGR.

- By installation type, ballasted track held a 61.28% share in 2025; in the railway track market, ballastless slab solutions are projected to rise at a 3.23% CAGR.

- By track gauge, standard gauge (1,435 mm) captured 51.28% share in 2025, while broad gauge is forecast to post the fastest growth at a 3.26% CAGR over 2026-2031.

- By geography, Asia Pacific commanded 34.18% of the railway track market share in 2025 and remains the fastest-growing region with a 3.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Railway Track Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Dedicated High-Speed Rail Corridors | +0.8% | APAC core (China, India, Southeast Asia), Middle East (Saudi Arabia, UAE), spill-over to Southern Europe | Medium term (2-4 years) |

| Growing Demand for Heavy-Haul Tracks in Mineral-Rich Emerging Economies | +0.6% | Australia, Brazil, South Africa, Indonesia, Peru | Medium term (2-4 years) |

| Surge in Public-Private Partnership (PPP) Funding Models for Rail Infrastructure | +0.5% | Global, with concentration in India, Brazil, Turkey, and select African corridors | Long term (≥ 4 years) |

| Accelerated Replacement Cycles Driven by Climate-Resilient Track Standards | +0.5% | Global, with early gains in coastal and flood-prone regions (Bangladesh, Netherlands, US Gulf Coast) | Medium term (2-4 years) |

| Adoption of Predictive Track-Monitoring Analytics (AI-Enabled) | +0.4% | North America, EU, Japan, early pilots in India and China | Long term (≥ 4 years) |

| Localized Manufacturing Incentives in South and Southeast Asia | +0.3% | India, Vietnam, Indonesia, Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Dedicated High-Speed Rail Corridors

China cleared 3,000 km of fresh routes in 2025, including extensions around Chengdu and the Pearl River Delta, which require about 1.2 million t of 60E1 and 75N profiles. India’s 508 km Mumbai–Ahmedabad line moved into the slab-track construction phase, backed by Japanese Shinkansen technology. Saudi Arabia advanced the USD 7.5 billion Riyadh–Jeddah landbridge, specifying ballastless designs that tolerate 50 °C summer peaks [1]“Landbridge Project Factsheet,” Public Investment Fund, pif.gov.sa . Emerging studies on a Jakarta–Surabaya link indicate 350 km/h operations, which mandate a rail yield strength > 900 MPa. Suppliers able to deliver turnkey rail-plus-sensor packages are consequently gaining procurement preference in the railway track market.

Growing Demand for Heavy-Haul Tracks in Mineral-Rich Emerging Economies

Rio Tinto finalized a AUD 1.2 billion upgrade that added 400 km of head-hardened rail to its Pilbara network by mid-2025. Vale began swapping 220 km of standard rail for 68 kg/m alternatives on its Carajás line, targeting a 40% cut in grind cycles. South Africa’s 861 km coal corridor renewal contract for 180,000 t of 57E1 profiles went to EVRAZ late in 2024. Each project shows miners preferring incremental rail investments over complete track rebuilds when commodity prices are buoyant.

Surge in Public-Private Partnership Funding Models for Rail Infrastructure

Twelve PPP concessions covering 4,200 km of Indian freight corridors closed in 2025 with 30-year operate-maintain-transfer terms, encouraging private bidders to procure premium head-hardened rail for lifecycle savings [2]“Indian Railways Budget 2025-26 Highlights,” Press Information Bureau, pib.gov.in . Brazil approved three freight PPPs worth USD 6.8 billion the same year, all of which call for 57E1 or heavier profiles to cut grinding on tight curves. Similar models in Turkey and South Africa bundle track, signaling, and rolling stock, lengthening order visibility for rail makers while exposing them to schedule slippage if a single environmental permit stalls in the railway track market.

Accelerated Replacement Cycles Driven by Climate-Resilient Track Standards

The EU’s 2025 Technical Specifications for Interoperability require rail to be tolerant of 40 °C swings across 12,000 km of southern networks [3]“Revised TSI Infrastructure 2025,” European Union Agency for Railways, ERA. europa.eu . Bangladesh is replacing 450 km of lines in flood-prone areas with hot-dip galvanized systems under a USD 320 million program. New U.S. Federal Railroad Administration rules ask Gulf Coast Class 4+ routes to endure Category 3 hurricane winds, accelerating 2,800 km of renewals. Mandatory upgrades front-load demand into the 2026–2028 window.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel Prices Squeezing OEM Margins | -0.4% | Global, with acute impact in Europe and North America | Short term (≤ 2 years) |

| Procurement Delays Caused by Prolonged Environmental-Impact Clearances | -0.3% | EU, North America, Australia, select projects in India and Brazil | Medium term (2-4 years) |

| Short-Term Capex Diversion Toward Urban Metro Systems Vs. Inter-City Lines | -0.2% | APAC (India, Southeast Asia), Latin America, Middle East | Short term (≤ 2 years) |

| Skilled-Labor Shortages in Advanced Flash-Butt Welding and Track Installation | -0.2% | North America, EU, Japan, emerging in Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel Prices Squeezing OEM Margins

Hot-rolled coil rose 22% between January 2024 and March 2025, trimming rail-mill operating spreads by 300-400 basis points as steel input became the dominant cost driver. ArcelorMittal invoked force majeure clauses on fixed-price contracts once the coil price breached EUR 720/t, disrupting European national railway deliveries in 2Q 2025. Voestalpine’s rail division reported a 280-basis-point EBITDA margin drop in FY 2024-25 because coil purchases preceded rail invoicing by six months under framework deals with Deutsche Bahn and ÖBB. British Steel halted its Scunthorpe rail line for four weeks in mid-2025 to renegotiate Network Rail pricing, deferring 18,000 t of scheduled shipments. Steel Dynamics began inserting quarterly pass-through clauses in new North American rail contracts from 3Q 2025, shifting 70% of raw-material volatility to buyers and prompting more miniature regional railways to defer replacement cycles in the railway track market.

Procurement Delays Caused by Prolonged Environmental-Impact Clearances

Average clearance time for new European Union rail corridors has stretched to 38 months since the 2024 revision of the Environmental Impact Assessment Directive, forcing sponsors to reallocate near-term budgets to urban metro upgrades with lighter review requirements. The National Environmental Policy Act process kept the Brightline West high-speed project in California under review for 42 months, pushing track orders into early 2026 and compressing the construction window by 18 months. Australia’s Inland Rail Queensland segment faced 28 months of evaluation under the EPBC Act in 2024-25, delaying the purchase of 120 km of rail and redirecting USD 180 million to interim maintenance. India’s 2024 rule mandating an 18-month public consultation period for ecologically sensitive alignments put eight planned corridors totaling 1,400 km on hold. Brazil’s Amazon-basin Ferrogrão grain line remained stalled for 36 months as of early 2026 while IBAMA reviewed biodiversity impacts, freezing USD 3.2 billion in track and civil-works contracts in the railway track market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rail Type: Head-Hardened Rail Gains on Freight Intensity

Standard rail still held 41.27% of the railway track market in 2025, whereas head-hardened profiles captured 3.13% CAGR through 2031, benefiting from 40-ton axle-load upgrades on mining routes. Rio Tinto’s 400 km Pilbara retrofit and South Africa’s 180,000 t EVRAZ contract highlight the switch toward ≥ 380 Brinell hardness for curves and high-stress zones. The railway track market size for head-hardened product lines is projected to expand further, as only six mills globally can deliver ≥ 900 MPa yield strength economically. Nevertheless, passenger corridors with < 25-ton loads keep standard grades dominant because the premium is unjustified at moderate traffic density. Crane and tongue rail remain sub-10% niches focused on ports and switches that prize geometry precision over tonnage.

The economics lean toward incremental premium-rail swaps over total track rebuilds. Operators facing throughput constraints find that extending rail life by 40% on curves offsets the 18% to 22% unit-price premium. Suppliers that integrate thermite welding and post-grind services lock in after-sales annuities, while merchants lacking on-site support risk commoditization. Long term, AI-driven defect prediction may slow growth in absolute tonnage yet favor suppliers offering sensor-embedded rail that feeds maintenance algorithms.

By Component: Fastening Systems Outpace Rails on Maintenance Intensity

Rails still generated 55.27% of 2025 revenue, but fastening systems are pacing at a 3.31% CAGR through 2031. Elastic clips with polyurethane insulators, such as Vossloh’s W14, have been adopted for 1,200 km of Deutsche Bahn renewal projects, reducing ballast settlement and sleeper cracking. Pandrol’s e-Clip won 800 km of orders on India’s freight corridors in 2025, proof that vibration damping outweighs a 10% price bump. Because clips and insulators require renewal every 8–12 years, compared with 25–35 years for rail, the railway track market for fasteners generates a steadier aftermarket stream. Sleepers, switches, and ballast remain vital, but value migrates to intelligent systems that embed RFID or strain gauges for real-time load tracking.

Component makers thus secure higher gross margins than steel mills, especially when they bundle sensor analytics and warranty services. Integrated players that historically focused on tonnage are now partnering with clip specialists to avoid margin erosion. In parallel, composite sleepers made from recycled polyethylene and fiberglass weigh 40% less than concrete alternatives, lowering substructure costs on viaducts by up to 15%.

By Application: High-Speed Corridors Reshape Demand Mix

Freight still led with a 38.71% revenue share in 2025, yet the high-speed and bullet segments are expanding at a 3.15% CAGR through 2031 as governments seek to decongest short-haul aviation lanes. China’s 3,000 km approval wave alone demands 1.2 million t of premium 60E1 and 75N rail, a bulk that eclipses the combined annual needs of France and Germany. High-speed track costs 40%–50% more per km than freight lines due to tighter tolerances, continuous welded joints, and ballastless foundations. Consequently, the railway track market faces a rotating demand mix where heavy-haul tonnage drives volume while passenger corridors lift value per km. Light-rail and metro projects, although lower in tonnage, favor ballastless slab designs that pull through high-margin fastening and sensor packages.

Passenger conventional rail retains a quarter of revenue, growing more slowly but benefiting from electrification in India and Southeast Asia. Operators in mature Western markets prioritize digital signaling over wholesale track swaps, tempering growth there. Urban transit remains a policy favorite in megacities, shifting part of the order book to lighter 54E1 profiles manufactured by regional mills entering under local content rules.

By Rail Weight Class: Heavier Profiles for Axle-Load Escalation

The 50-60 kg/m band made up 36.17% of the 2025 volume, serving most commuter and mid-freight corridors. However, profiles above 60 kg/m are rising at a 3.17% CAGR through 2031 as mining and coal operators migrate to 32.5-ton axle loads.

Vale’s swap to 68 kg/m rail and Australian iron-ore renewals confirm the pivot. Heavier rail distributes stress, reducing ballast settlement by 20%–30%, but demands reinforced sleepers and deeper ballast, which can increase civil costs by up to 18%. The less-than-50 kg/m segment is retreating in developed networks yet persists on narrow-gauge and mountain lines where tight curvature keeps heavier profiles impractical.

By Material: Composite Polymers Target Niche Urban Applications

Carbon steel still commands a 73.27% share owing to cost and global availability, but composite or hybrid polymer products are the fastest-growing segment at a 3.33% CAGR through 2031. Jakarta MRT Phase 2 specified composite sleepers on 18 km of elevated guideway to cut dead load by 25%.

Hybrid polyurethane clips damp vibration by 30%–40%, extending the life of concrete sleepers. Alloy and head-hardened grades stay entrenched in heavy-haul and high-speed niches where wear resistance trumps price.

By Installation Type: Ballastless Track for Constrained Corridors

Ballasted designs covered 61.28% of the 2025 route length due to their low upfront cost and field adjustability. Yet ballastless slab systems are on track for a 3.23% CAGRthrough 2031 as tunnels, viaducts, and 250 km/h+ services seek maintenance windows amid tight urban curfews.

Japan’s Shinkansen network shows 60% lower geometry degradation, validating the lifecycle payoff. Operators, however, must nail subgrade precision; correcting slab misalignment costs three times as much as a ballasted lift.

By Track Gauge: Standard Gauge Dominates, Broad Gauge Holds Ground

The standard 1,435 mm gauge maintained a 51.28% share in 2025, benefiting from cross-border equipment fungibility. Broad gauge (> 1,520 mm) is still climbing at a 3.26% CAGR through 2031, fueled by India’s and Russia’s network expansions that value higher payload per train over interoperability.

Meter and narrower gauges sit near 18% and are slowly ceding ground except where mountainous terrain or legacy tourism justify retention.

Geography Analysis

Asia Pacific leads with a 34.18% share and a 3.22% CAGR, as China’s 3,000 km of high-speed rail approvals and India’s USD 28 billion rail allocation dominate order books. Metro builds in Jakarta, Manila, and Bangkok, adding lighter-profile volume, while upgrades to Australia’s iron-ore corridor keep demand for 68 kg/m head-hardened rail elevated.

Europe and North America together hold 38% share but face slower growth. The EU’s new thermal-stress rules extend the scope of replacement across Mediterranean lines, and Network Rail’s fiber-optic rollout underscores a pivot to condition-based maintenance. North America’s Class I railroads renewed 2,800 km in 2025, yet environmental reviews for greenfield high-speed projects, such as Brightline West, now exceed 40 months, pushing track orders into 2026 starts.

The Middle East and South America markets show the sharpest local spikes. Saudi Arabia’s USD 7.5 billion landbridge, Brazil’s USD 6.8 billion PPP wave, and Turkey’s Ankara–Izmir concession all specify ballastless or head-hardened systems. South Africa’s coal line, financed at USD 450 million, further underlines regional interest in 30-ton axle-load upgrades. African Development Bank financing could unlock 2,400 km of standard-gauge build-outs by 2030, but funding gaps and governance risks remain.

Competitive Landscape

The majority of global rail tonnage flows through the top five integrated mills—ArcelorMittal, Nippon Steel, Voestalpine, EVRAZ, and China Baowu—under 18- to 24-month framework agreements with national railways. Component specialists Vossloh, Pandrol, and Progress Rail earn superior margins on IP-rich fastening, switch, and modular-panel systems in the railway track market.

Chinese exporters such as Baowu, AGICO, and Ansteel undercut European offers by 12%–15% through Belt-and-Road EPC bundles. JSW Steel’s 400,000 t Karnataka mill and Hòa Phát’s planned 700,000 t Vietnamese line illustrate the regionalization push.

Digitally enabled offerings are the next battleground. Union Pacific and Network Rail pilots show predictive-maintenance platforms can slash emergency speed orders by one-third, but 80% of operators still lack such analytics. Players that integrate sensors into clips, welds, or rail webs will likely set de facto standards. Barriers remain high: ISO 17660 flash butt welding certification and EN 13674 profile compliance require multimillion-dollar QA labs, limiting disruptive entry.

Railway Track Industry Leaders

Voestalpine Schienen GmbH

Nippon Steel Corporation

Vossloh AG

ArcelorMittal SA

EVRAZ plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hòa Phát announced its intention to commence rail production by February 2027, targeting an annual capacity of 700,000 tons. This move aligns with the company's strategy to diversify its product portfolio and strengthen its position in the steel industry. The planned production facility is expected to serve both domestic and international markets, meeting the growing demand for high-quality rail products.

- March 2025: In Andhra Pradesh, AM/NS India, a subsidiary of Nippon Steel, acquired 890 hectares to establish a 7-million-ton steel mill. This facility aims to support domestic rail infrastructure projects, contributing to the development of the country's transportation network and meeting the growing demand for steel in the rail sector.

Global Railway Track Market Report Scope

The scope of the report includes Rail Type (Standard and More), Component (Rails, Sleepers, and More), Application (Freight and More), Rail Weight Class (Less Than 50 kg and More), Material (Carbon Steel and More), Installation Type (Ballasted and Ballast-less/Slab), Track Gauge (Standard 1 and More), and Geography.

| Standard Rail |

| Head-Hardened Rail |

| Heavy-Haul Rail |

| Crane Rail |

| Tongue Rail |

| Rails |

| Sleepers (Ties) |

| Fastening Systems (Clips, Spikes, Screws) |

| Switches and Crossings |

| Ballast & Sub-Ballast |

| Freight |

| Passenger - Conventional |

| High-Speed & Bullet |

| Urban and Light Rail |

| Less Than 50 kg |

| 50 - 60 kg |

| More Than 60 kg |

| Carbon Steel |

| Alloy and Head-Hardened Steel |

| Composite and Hybrid Polymer |

| Ballasted Track |

| Ballast-less / Slab Track |

| Standard (1,435 mm) |

| Broad (More than 1,520 mm) |

| Meter / Narrow (Less than 1,067 mm) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Rail Type | Standard Rail | |

| Head-Hardened Rail | ||

| Heavy-Haul Rail | ||

| Crane Rail | ||

| Tongue Rail | ||

| By Component | Rails | |

| Sleepers (Ties) | ||

| Fastening Systems (Clips, Spikes, Screws) | ||

| Switches and Crossings | ||

| Ballast & Sub-Ballast | ||

| By Application | Freight | |

| Passenger - Conventional | ||

| High-Speed & Bullet | ||

| Urban and Light Rail | ||

| By Rail Weight Class (kg/m) | Less Than 50 kg | |

| 50 - 60 kg | ||

| More Than 60 kg | ||

| By Material | Carbon Steel | |

| Alloy and Head-Hardened Steel | ||

| Composite and Hybrid Polymer | ||

| By Installation Type | Ballasted Track | |

| Ballast-less / Slab Track | ||

| By Track Gauge | Standard (1,435 mm) | |

| Broad (More than 1,520 mm) | ||

| Meter / Narrow (Less than 1,067 mm) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the railway track market today?

The railway track market size stands at USD 35.23 billion in 2026 and is projected to reach USD 41.06 billion by 2031.

Which region is expanding fastest?

Asia Pacific leads growth with a 3.22% CAGR as China, India, and Southeast Asia add high-speed and metro corridors.

What segment is gaining share the quickest?

Fastening systems are the fastest-growing component, advancing at a 3.31% CAGR due to shorter replacement cycles and demand for vibration-damping clips.

How are steel-price swings affecting suppliers?

A massive jump in hot-rolled coil prices between 2024 and 2025 compressed rail-mill margins, forcing contract repricing and temporary plant shutdowns in Europe and North America.

Why are ballastless tracks becoming popular?

Ballastless slab designs cut long-term maintenance by up to 80% on high-speed or tunnel sections, offsetting their 50%–60% higher upfront cost when access for tamping is limited.

Which companies hold the largest share?

ArcelorMittal, Nippon Steel, Voestalpine, EVRAZ, and China Baowu holds the largest share of global rail tonnage via multi-year framework deals with national railways.

Page last updated on: