Railway Cybersecurity Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

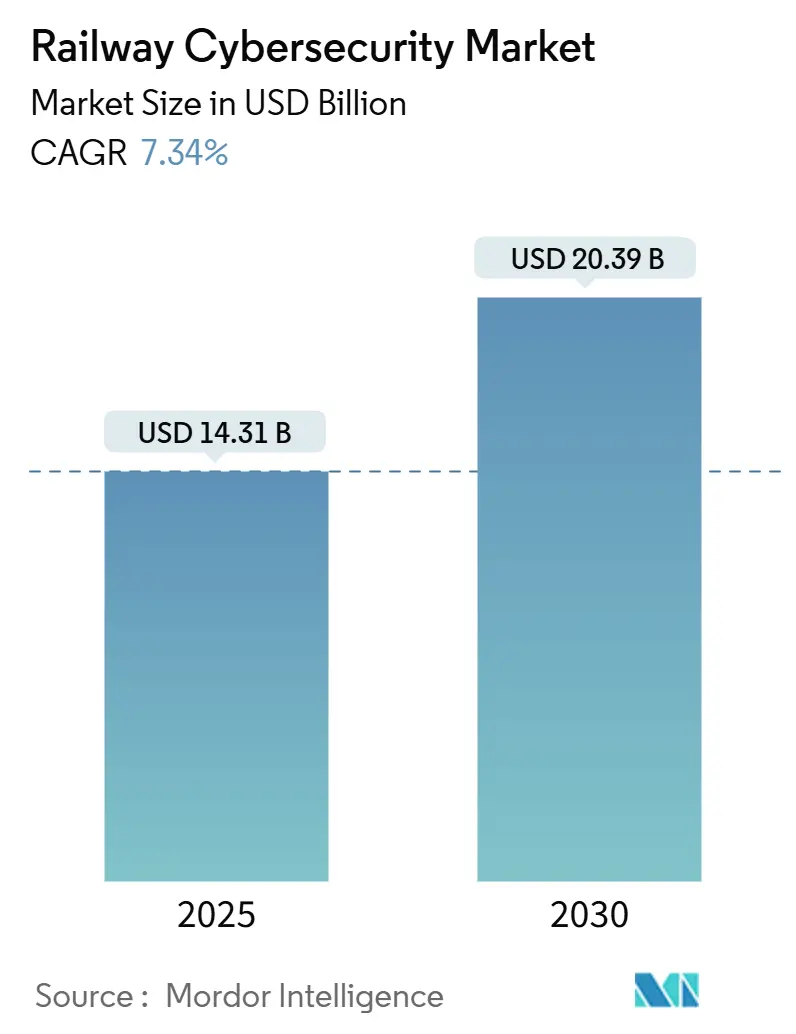

| Market Size (2025) | USD 14.31 Billion |

| Market Size (2030) | USD 20.39 Billion |

| Growth Rate (2025 - 2030) | 7.34% CAGR |

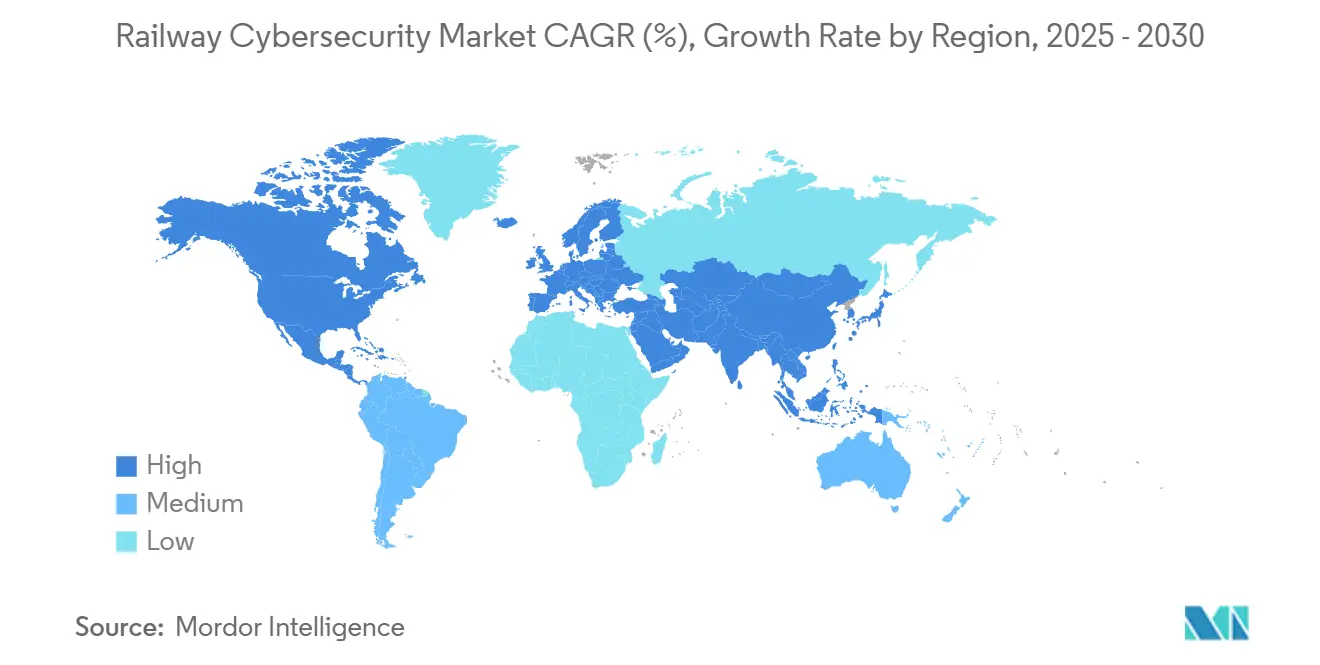

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Railway Cybersecurity Market Analysis by Mordor Intelligence

The railway cybersecurity market size stands at USD 14.31 billion in 2025 and is projected to reach USD 20.39 billion by 2030, advancing at a 7.34% CAGR. Rising digitalization of signaling, ticketing, and rolling-stock management systems, coupled with a 220% surge in reported railway cyberattacks during the past five years, is forcing operators to prioritize security-by-design practices. Mandatory regulations—including the EU Cyber Resilience Act and the Transportation Security Administration’s performance-based rulemaking—are synchronizing global procurement requirements and accelerating adoption of compliance-ready solutions. Convergence of operational technology and information technology budgets is expanding coverage from network perimeters to endpoints, while AI-driven predictive maintenance platforms reshape data-protection needs. Rapid deployment of 5G rail-to-ground connectivity and CBTC systems adds new wireless attack surfaces that demand layered defense architectures.

Key Report Takeaways

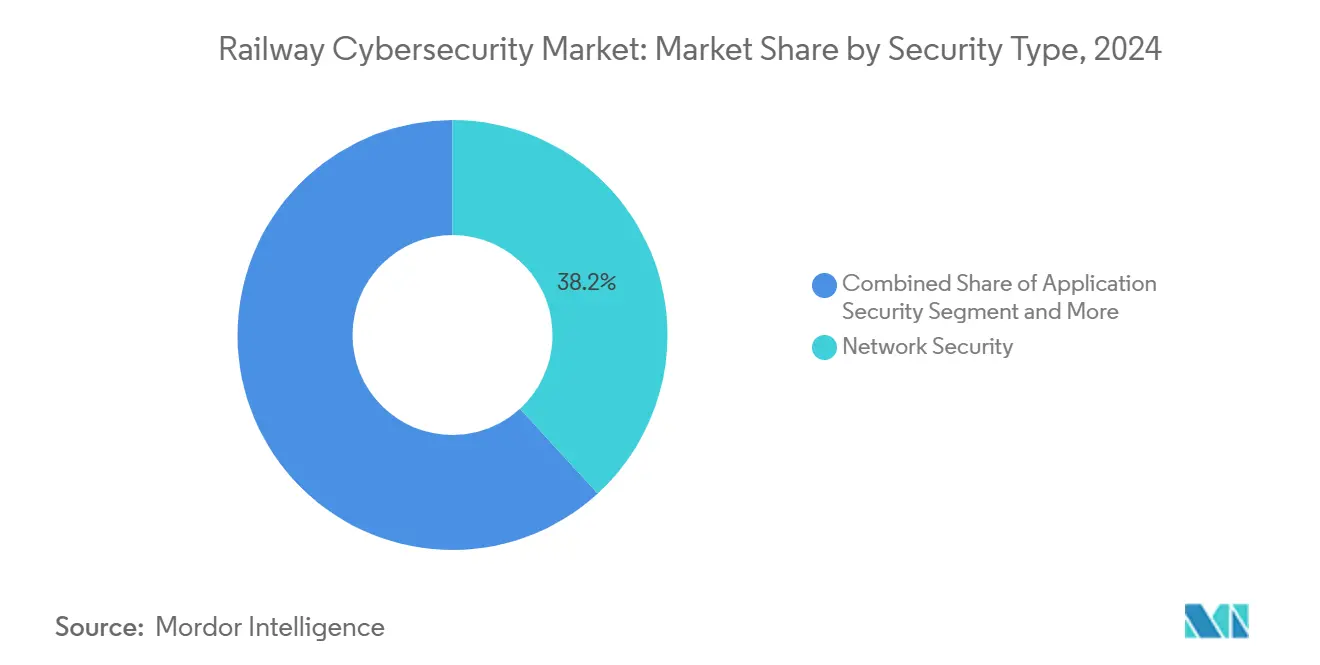

- By security type, Network Security led with 38.23% revenue share in 2024; Endpoint Security is forecast to expand at a 14.53% CAGR through 2030.

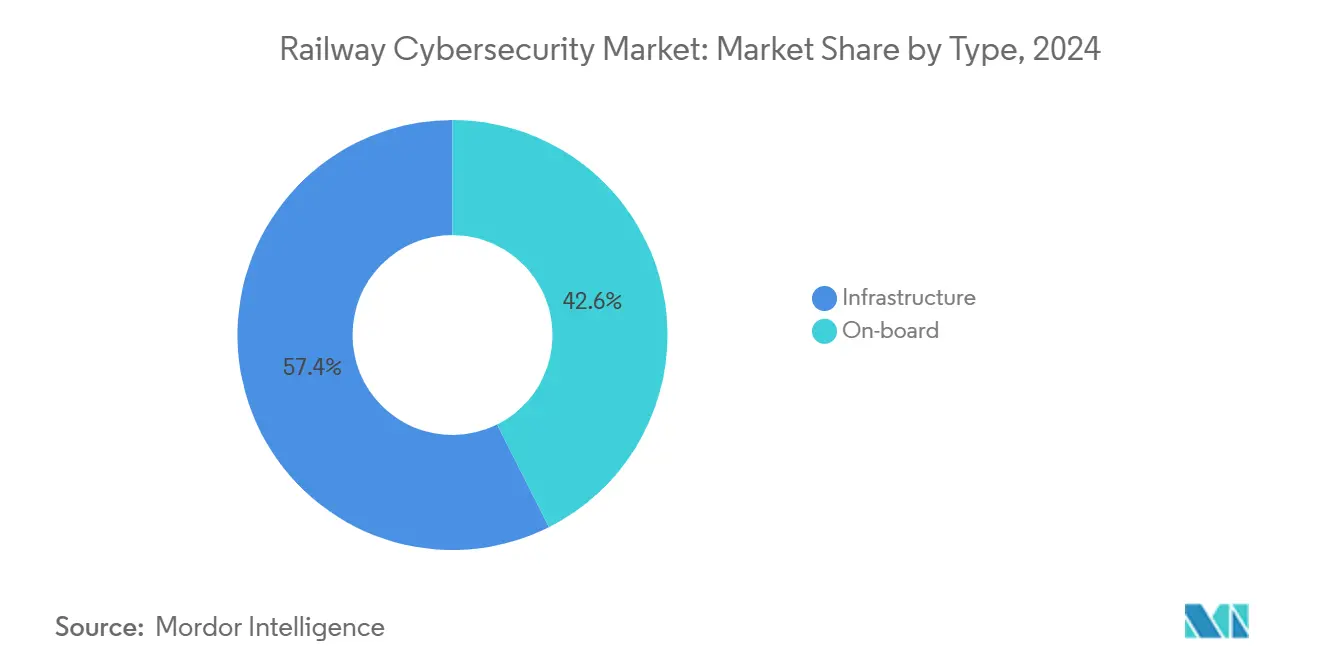

- By type, Infrastructure systems captured 57.41% of the railway cybersecurity market share in 2024, while On-board systems are projected to grow at an 11.24% CAGR to 2030.

- By application, Passenger Trains accounted for a 52.18% share of the railway cybersecurity market in 2024; urban rail is advancing at a 12.83% CAGR through 2030.

- By rail type, Metro Rail dominated with 41.07% revenue share in 2024, whereas High-Speed Rail is set to register the fastest 12.04% CAGR between 2025 and 2030.

- By end use, railway operators held 63.32% of 2024 demand; private rail companies exhibited the highest 13.47% CAGR over the forecast period.

- By geography, Europe retained 34.28% market share in 2024 and Asia-Pacific is positioned for a 12.62% CAGR, driven by large-scale CBTC roll-outs.

Global Railway Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Cyber-Resilience Projects | +1.8% | Europe, with spillover to global suppliers | Medium term (2-4 years) |

| U.S. Rail Cyber Directives | +1.2% | North America, influencing global standards | Short term (≤ 2 years) |

| CBTC and Interlocking Expansion | +2.1% | Asia-Pacific core, extending to MEA | Long term (≥ 4 years) |

| AI Predictive Maintenance | +1.5% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| 5G Rail Connectivity | +0.9% | Global, led by Asia-Pacific and Europe | Long term (≥ 4 years) |

| OT-IT Security Convergence | +0.7% | Global, accelerated in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Uptake of EU Cyber Resilience Act Compliance Projects

The December 2024 enforcement of the Cyber Resilience Act requires railway products with digital elements sold in Europe to adopt secure-by-design development, vulnerability management, and 10-year update support. Mandatory third-party conformity assessments for Important and Critical components increase demand for specialized testing laboratories and certification consultancies. Manufacturers face fines up to EUR 15 million or 2.5% of global revenue, prompting proactive security investment throughout the supply chain. Global suppliers must upgrade entire portfolios to retain European market access, effectively exporting CRA standards worldwide. The regulation harmonizes product-level requirements with the NIS2 Directive’s operator obligations, encouraging integrated compliance frameworks and fueling adoption of holistic security platforms.

TSA Rail-Sector Cybersecurity Directives in the U.S.

The Transportation Security Administration’s November 2024 notice of proposed rulemaking compels designated freight and passenger railroads to establish risk-based cybersecurity programs aligned with NIST outcomes. Operators must submit Cybersecurity Operational Implementation Plans that detail segmentation, access control, continuous monitoring, and patch-management measures[1]"TSA Releases Proposed Rule to Enhance Pipeline and Railroad Cyber Risk Management," Jones Day, jonesday.com.. A performance-based model lets railroads tailor controls, spurring demand for advisory services that convert broad objectives into operator-specific roadmaps. Continuous monitoring requirements benefit vendors offering OT-aware threat-detection platforms capable of real-time analyzing signaling traffic. The directive reinforces CISA reporting obligations, accelerating investment in incident-response automation across North American networks.

Expansion of CBTC and Digital Interlockings in Asia

Asia-Pacific cities are commissioning CBTC projects that centralize train-control functions over wireless links, thereby exposing safety-critical signaling to cyber risk. China’s metro build-out, India’s interlocking upgrades, and Japan’s autonomous train trials create sustained demand for purpose-built security architectures that safeguard radio communications and IP-networked trackside devices[2]"ASIA PACIFIC 5G Industry & IoT UPDATES Oct 2024," GSMA, gsma.com.. Vendors are opening regional R&D centers to co-develop encryption, key-management, and anomaly-detection solutions optimized for high-density urban settings. 5G integration magnifies attack surfaces but also provides deterministic bandwidth that supports security telemetry and over-the-air patch delivery. Lessons learned in Asia are shaping global best practices for resilient moving-block operations.

Surge in AI-Powered Predictive Maintenance Platforms

Operators now deploy sensor suites that stream up to 8,000 real-time variables per train into cloud-based analytics engines. SNCF’s initiative across 1,100 trainsets improved fault-prediction accuracy to 95% and reduced unscheduled breakdowns by over 50%[3]"A global leader in predictive maintenance," groupe-sncf.com.. The resulting data deluge raises confidentiality and integrity risks that require tokenization, granular access control, and tamper-proof audit trails. Security teams must harden machine-learning pipelines against data-poisoning and model-theft attacks. Vendor-managed algorithms create third-party dependencies, driving adoption of zero-trust architectures and contractual clauses for continuous vulnerability disclosure. Predictive-maintenance platforms act as both productivity accelerators and catalysts for end-to-end cybersecurity overhauls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy SCADA Protocols | -1.4% | Global, particularly acute in mature markets | Long term (≥ 4 years) |

| Cybersecurity Talent Gap | -0.9% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Costly Rolling Stock Retrofits | -1.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Fragmented Rail Governance | -0.6% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy SCADA Systems with Proprietary Protocols

Many railroads still depend on supervisory control and data acquisition platforms installed two decades ago, running unencrypted, vendor-specific protocols and default credentials that cannot be patched without complete hardware replacement. Retrofitting modern defenses requires deployment of data-diode gateways, passive network-monitoring probes, and protocol-translation appliances that maintain deterministic latency. Safety certification constraints limit code changes, extending exposure windows and pushing operators toward compensating controls rather than software upgrades. Hybrid environments that blend relay-based equipment with IP-connected devices complicate asset inventories and vulnerability assessments. Funding cycles favor incremental improvements, resulting in patchwork security postures that skilled adversaries can exploit.

Shortage of Rail-Focused Cybersecurity Talent

Global cybersecurity vacancies outnumber qualified professionals, and the rail domain suffers more acutely because candidates must understand both signaling and security principles. A 2024 U.K. survey found that 44% of organizations lacked confidence in basic cybersecurity tasks, illustrating systemic skills gaps. Railways therefore depend heavily on external consultants, driving costs and limiting internal knowledge transfer. Managed security service providers offer remote monitoring, but incident-response effectiveness suffers when local engineers lack forensic expertise. Talent shortages prolong project timelines, delaying deployment of critical countermeasures and leaving networks exposed for longer periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Infrastructure Systems Lead While On-board Digitalization Accelerates

Infrastructure systems dominate with 57.41% market share in 2024, encompassing Railway IT Systems and Control Centers that form the backbone of modern railway operations and require comprehensive cybersecurity protection against threats targeting critical operational functions. The Infrastructure segment's leadership reflects the centralized nature of railway cybersecurity investments, where operators prioritize protecting control centers, signaling systems, and trackside equipment that can affect entire network operations if compromised. On-board systems represent the fastest-growing segment at 11.24% CAGR through 2030, driven by accelerating digitalization of rolling stock through advanced train management systems, passenger interfaces, and IoT-enabled predictive maintenance platforms that require specialized cybersecurity solutions.

The growth differential between Infrastructure and On-board segments illustrates the phased approach to railway cybersecurity implementation, where operators initially focus on protecting centralized systems before extending security controls to distributed rolling stock assets. Infrastructure cybersecurity investments are driven by regulatory mandates and the high operational impact of control center compromises, while On-board security growth reflects the increasing connectivity of trains through 5G networks and the deployment of passenger services that create new attack vectors. BlackBerry QNX's rebranding and focus on mission-critical embedded systems for rail applications demonstrates the growing importance of secure operating systems for On-board applications that must meet both safety and cybersecurity requirements. The convergence of Infrastructure and On-board security requirements is creating demand for integrated solutions that can provide consistent security policies across both domains while accommodating the unique operational constraints of each environment.

By Application: Urban Rail Modernization Outpaces Traditional Segments

Passenger Trains hold the largest application share at 52.18% in 2024, driven by high-frequency operations, extensive passenger-facing systems, and stringent safety requirements that demand comprehensive cybersecurity protection across ticketing, information systems, and operational controls. Urban Rail emerges as the fastest-growing application segment with 12.83% CAGR through 2030, reflecting massive metro modernization programs across Asia-Pacific and the deployment of advanced CBTC systems that require sophisticated cybersecurity architectures to protect wireless train control communications. Freight Trains represent a substantial but slower-growing segment, where cybersecurity investments focus on protecting cargo management systems and ensuring supply chain security rather than passenger-facing applications.

Urban Rail's growth acceleration stems from the unique cybersecurity challenges of high-density, automated metro operations that rely heavily on wireless communications and centralized control systems vulnerable to cyber attacks. The segment benefits from concentrated investment in new metro lines and system upgrades that incorporate cybersecurity requirements from the design phase, contrasting with legacy passenger rail systems that require costly retrofits. RailTel's strategic partnership with Cylus to deploy rail-specific cybersecurity solutions across Indian Railway infrastructure exemplifies the targeted approach needed for different application segments. The application segmentation reflects varying threat profiles, with Urban Rail systems facing risks from both operational disruption and passenger safety impacts, while Freight operations must address supply chain security and cargo protection concerns that require different cybersecurity approaches and technologies.

By Rail Type: High-Speed Innovation Drives Security Evolution

Metro Rail systems command 41.07% market share in 2024, reflecting the concentration of cybersecurity investments in urban transit networks that serve millions of daily passengers and operate sophisticated automated systems requiring comprehensive protection against cyber threats. High-Speed Rail emerges as the fastest-growing segment at 12.04% CAGR through 2030, driven by next-generation projects incorporating advanced cybersecurity features from the design phase and the unique security challenges of high-velocity operations that demand ultra-reliable communications and control systems. Light Rail and Freight Rail segments show moderate growth as operators balance cybersecurity investments against operational priorities and cost constraints in these typically lower-margin operations.

The segmentation reflects the varying cybersecurity maturity levels across different rail types, with Metro Rail systems leading adoption due to their high automation levels and passenger safety criticality. High-Speed Rail's rapid growth stems from greenfield projects that can incorporate state-of-the-art cybersecurity architectures without the constraints of legacy system integration, creating opportunities for vendors offering integrated security solutions. Japan's development of driverless bullet trains by 2029 exemplifies the cybersecurity innovation occurring in High-Speed Rail, where autonomous operations require unprecedented levels of system security and reliability. The rail type segmentation also reflects different regulatory environments, with High-Speed Rail projects often subject to more stringent cybersecurity requirements due to their strategic importance and cross-border operations that must meet multiple national security standards.

By Security Type: Network Security Dominance Drives Infrastructure Protection

Network Security commands 38.23% market share in 2024, reflecting railway operators' prioritization of protecting critical communications infrastructure that underpins modern signaling, train control, and passenger information systems. This segment's leadership stems from the fundamental shift toward IP-based railway networks that require sophisticated perimeter defenses, intrusion detection, and secure communications protocols to protect against increasingly sophisticated cyber threats Cisco. Endpoint Security emerges as the fastest-growing segment with 14.53% CAGR through 2030, driven by the proliferation of connected devices across rolling stock and trackside infrastructure that create new attack vectors requiring specialized protection. Application Security and Data Protection segments are experiencing steady growth as operators recognize the importance of securing software applications and protecting sensitive operational data from breaches that could compromise safety or operational continuity.

The segment dynamics reflect the evolution from traditional perimeter-based security toward comprehensive defense-in-depth strategies that address the unique challenges of railway OT environments. Network Security solutions must accommodate the stringent latency requirements of safety-critical signaling systems while providing robust protection against DDoS attacks and network intrusions that could disrupt operations. Endpoint Security growth is accelerated by regulatory requirements such as the EU Cyber Resilience Act, which mandates security-by-design principles for connected railway devices and creates demand for solutions that can secure diverse endpoint populations without compromising operational performance. The convergence of IT and OT security budgets among railway operators is driving integrated security platforms that can address multiple security types through unified management interfaces, creating opportunities for vendors offering comprehensive railway cybersecurity suites.

By End Use: Private Sector Growth Reshapes Market Dynamics

Railway Operators maintain the dominant end-use position with 63.32% market share in 2024, reflecting their direct responsibility for operational cybersecurity and the concentration of cybersecurity investments within organizations that must protect critical infrastructure assets from increasingly sophisticated threats. Private Rail Companies emerge as the fastest-growing end-use segment at 13.47% CAGR through 2030, driven by public-private partnerships, rail privatization initiatives, and the entry of technology-focused companies that bring different approaches to cybersecurity investment and implementation. Government Agencies represent a significant but slower-growing segment, where cybersecurity investments are often constrained by procurement processes and budget cycles that can delay implementation of critical security measures.

The end-use dynamics reflect the changing structure of the railway industry, where traditional state-owned operators are increasingly partnering with private companies that bring cybersecurity expertise and investment capacity. Private Rail Companies' growth advantage stems from their ability to make rapid cybersecurity investments without the bureaucratic constraints that often limit government agencies and traditional railway operators. The Association of American Railroads' Rail Information Security Committee demonstrates how industry collaboration is evolving to address cybersecurity challenges, with major freight and passenger operators sharing threat intelligence and best practices through structured information-sharing mechanisms. This collaborative approach is creating new opportunities for cybersecurity vendors that can provide platforms supporting multi-operator threat intelligence sharing and coordinated incident response capabilities across different end-use segments.

Geography Analysis

Europe generated USD 4.9 billion in 2024, representing 34.28% of the global total. The region benefits from the railway cybersecurity market share leadership driven by the NIS2 Directive’s operator obligations and the Cyber Resilience Act’s product mandates, forming the world’s strictest compliance landscape. National regulators in Germany, France, and the United Kingdom require harmonized reporting, accelerating the adoption of IEC 62443-aligned controls across high-speed and metro networks. Funding from the EU Connecting Europe Facility earmarks cybersecurity as a prerequisite for digital-rail grants, ensuring sustained investment beyond 2030.

Asia-Pacific is on track for a 12.62% CAGR, moving from USD 3.1 billion in 2025 to more than USD 5.7 billion by 2030. Massive CBTC tenders in China, 5G-backed interlockings in Japan, and the the Indian Railway’s nationwide CylusOne deployment exemplify how the region leapfrogs legacy limitations with security-by-design architectures. Regional governments incorporate cybersecurity scoring into supplier pre-qualification, favoring vendors with local labs and skill-building programs.

North America, valued at USD 3.3 billion in 2024, advances at a moderate 6.8% CAGR as freight giants align with TSA guidance and the Association of American Railroads’ information-sharing protocols. South America and the Middle East and Africa collectively represent under 10% of current spending but register above-average growth due to new metro lines in Riyadh, Cairo, and São Paulo that integrate modern security frameworks from project inception. Local operators often partner with European system integrators, transferring best practices into emerging markets.

Competitive Landscape

Traditional rail suppliers have expanded portfolios through alliances that blend deep operational expertise with cybersecurity credentials. Siemens introduced SINEC Security Guard to automate OT vulnerability management across interlocking and SCADA assets. Alstom and Airbus Protect co-develop IEC 62443 risk-assessment playbooks for rolling-stock platforms, reducing certification timelines by up to 30%. Hitachi’s EUR 1.66 billion acquisition of Thales Ground Transportation Systems added a 2,400-engineer cybersecurity team, strengthening integrated digital-rail offerings.

Specialist firms continue to disrupt with rail-specific detection engines. Cylus leverages deep-packet inspection tuned for GSM-R and ETCS traffic, while RazorSecure embeds machine-learning agents directly into train control units for anomaly detection during movement. BlackBerry QNX targets safety-certified embedded OS niches, boasting 255 million vehicles powered and expanding into train-control environments. Cisco adapts industrial IoT firewalls with deterministic-latency extensions that protect signaling frames in less than 50 microseconds.

Market rivalry now centers on outcome-based service contracts. Managed Detection and Response packages guarantee maximum time-to-detect metrics, while platform providers bundle training that mitigates talent shortages. Suppliers integrating threat-intelligence sharing APIs aligned to the EU Rail ISAC gain preference as collaborative defense becomes an operator imperative. Intellectual property barriers erode as IEC 63452 advances toward finalization, setting common functional-security benchmarks that lower switching costs and intensify competition.

Railway Cybersecurity Industry Leaders

-

Siemens Mobility

-

Thales Group

-

Alstom

-

Nokia

-

Hitachi Rail STS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The International Electrotechnical Commission published IEC 62351:2025 SER, a consolidated cybersecurity standard for power systems management that provides technical frameworks applicable to railway electrification and traction power systems requiring secure communications protocols.

- January 2025: BlackBerry announced the strategic relaunch of its IoT division as QNX, emphasizing mission-critical software for railway applications and safety-certified embedded systems. The rebrand reinforces QNX's position in powering over 255 million vehicles and expanding into railway control systems requiring ISO 26262 ASIL D certification for safety-critical applications.

Global Railway Cybersecurity Market Report Scope

| Network Security |

| Application Security |

| Endpoint Security |

| Data Protection |

| Infrastructure | Railway IT Systems |

| Control Centers | |

| On-board | Train Systems |

| Passenger Interfaces |

| Passenger Trains |

| Freight Trains |

| Urban Rail |

| High-Speed Rail |

| Light Rail |

| Metro Rail |

| Freight Rail |

| Railway Operators |

| Government Agencies |

| Private Rail Companies |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Security Type | Network Security | |

| Application Security | ||

| Endpoint Security | ||

| Data Protection | ||

| By Type | Infrastructure | Railway IT Systems |

| Control Centers | ||

| On-board | Train Systems | |

| Passenger Interfaces | ||

| By Application | Passenger Trains | |

| Freight Trains | ||

| Urban Rail | ||

| By Rail Type | High-Speed Rail | |

| Light Rail | ||

| Metro Rail | ||

| Freight Rail | ||

| By End Use | Railway Operators | |

| Government Agencies | ||

| Private Rail Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the railway cybersecurity market in 2030?

The sector is forecast to reach USD 20.39 billion by 2030, reflecting a 7.34% CAGR from 2025.

Which geographic region is expected to grow fastest?

Asia-Pacific is projected to register a 12.62% CAGR between 2025 and 2030 due to large-scale CBTC and digital-interlocking deployments.

Which security segment leads current spending?

Network Security holds the top position with a 38.23% share of 2024 revenue, driven by perimeter and communications-infrastructure protection.

Why is the EU Cyber Resilience Act important for rail suppliers?

It mandates secure-by-design requirements and 10-year update obligations, with fines up to EUR 15 million, forcing global suppliers to upgrade product portfolios for European market access.

How does talent scarcity affect railway cybersecurity programs?

Only 85% of open cybersecurity roles can be filled, delaying implementation of controls and increasing reliance on external managed-security providers.

Which application segment is set for the fastest growth?

Urban Rail systems are forecast to expand at a 12.83% CAGR as metro modernization drives demand for wireless-centric security architectures.

Page last updated on: