Connected Rail Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

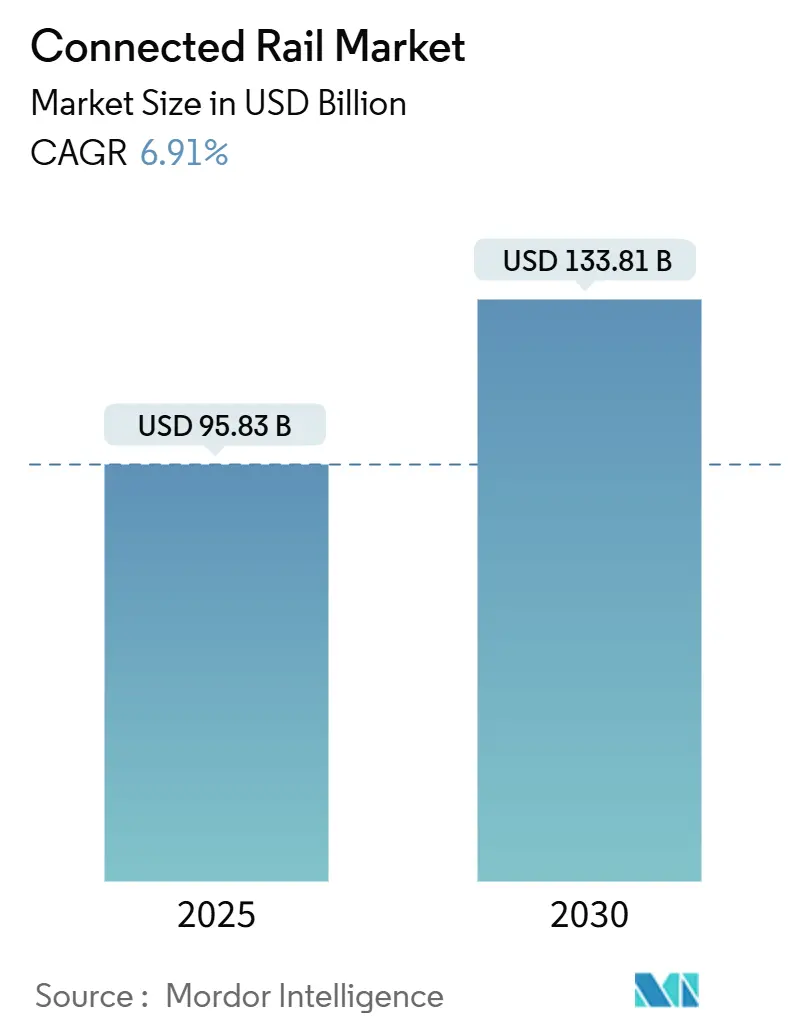

| Market Size (2025) | USD 95.83 Billion |

| Market Size (2030) | USD 133.81 Billion |

| Growth Rate (2025 - 2030) | 6.91% CAGR |

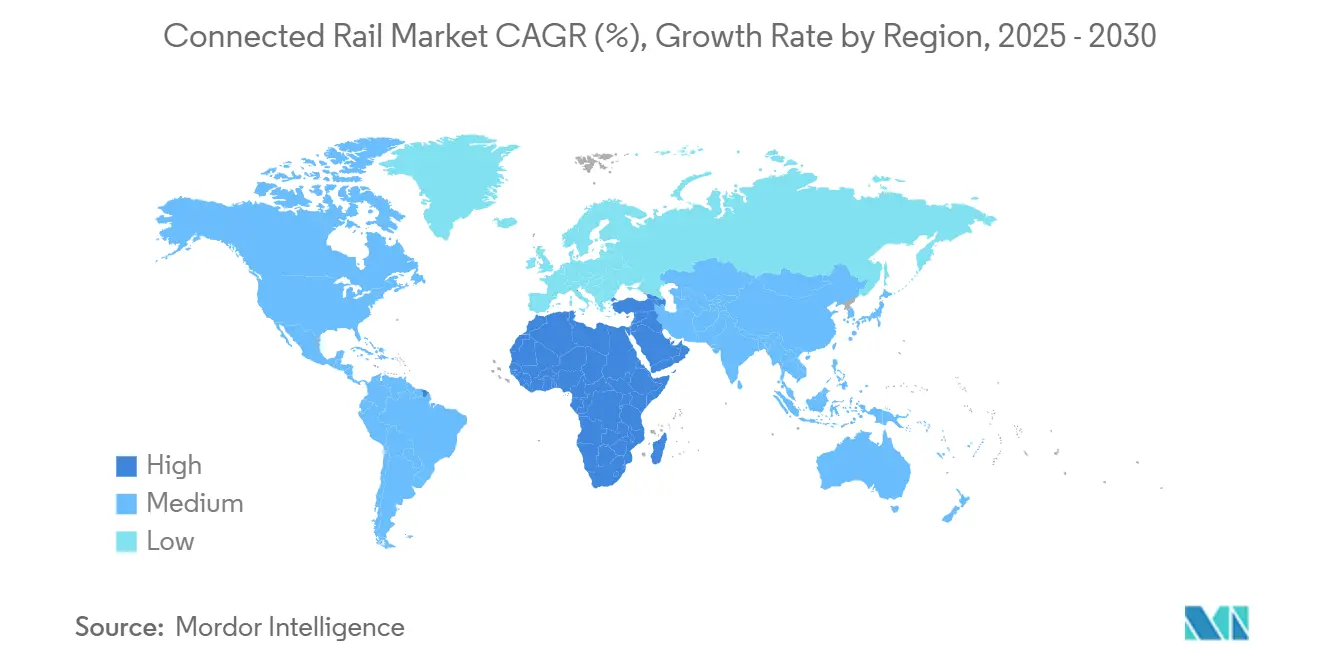

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Connected Rail Market Analysis by Mordor Intelligence

The Connected Rail Market size is estimated at USD 95.83 billion in 2025, and is expected to reach USD 133.81 billion by 2030, at a CAGR of 6.91% during the forecast period (2025-2030). Robust government funding, mounting labor shortages, and rising passenger expectations for real-time information amplify demand for digital rail infrastructure. Large-scale federal and regional programs in Europe, North America, and the Middle East compress traditional replacement cycles and accelerate technology refresh rates. Vendors that combine hardware, software, and analytics capabilities gain early-mover advantages as operators prioritize integrated platforms that reduce the total cost of ownership. Meanwhile, spectrum reallocation for private 5G and FRMCS-ready networks positions rail corridors as critical testbeds for mission-critical cellular deployments, reshaping competitive dynamics across connectivity suppliers.

Key Report Takeaways

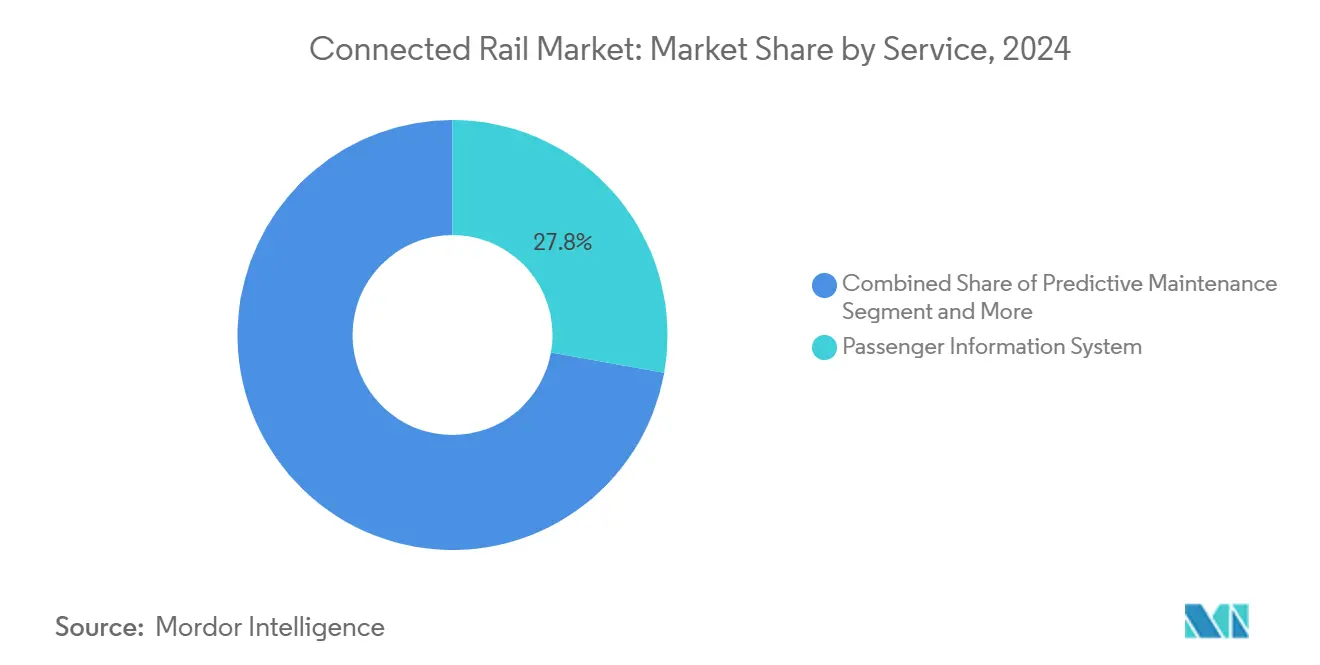

- By service, Passenger Information Systems led with 27.83% of the connected rail market share in 2024, while Predictive Maintenance advanced at a 6.93% CAGR through 2030.

- By rail signaling system, Positive Train Control held 35.46% of the connected rail market share in 2024; Communication-Based Train Control is projected to record a 7.06% CAGR to 2030.

- By rolling stock type, Electric Multiple Units accounted for 21.37% of the connected rail market share in 2024; Light Rail/Tram Cars are forecast to expand at a 7.11% CAGR through 2030.

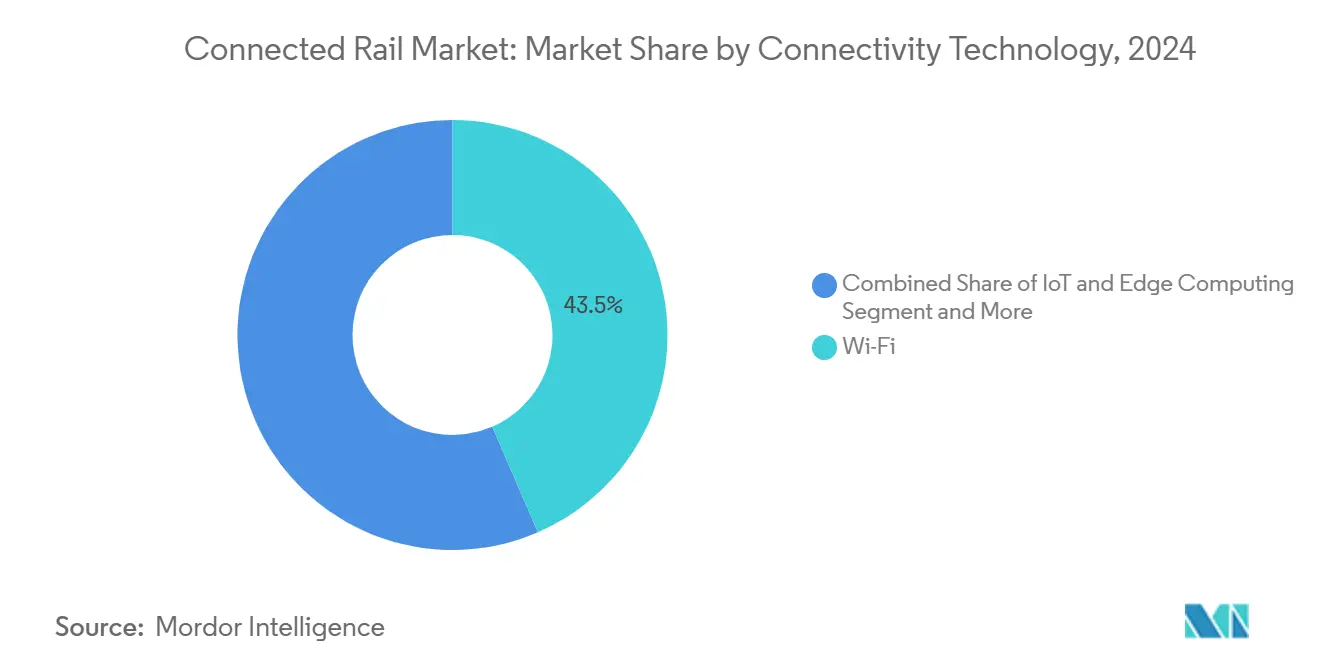

- By connectivity technology, Wi-Fi systems commanded 43.48% of the connected rail market share in 2024, while Private 5G/FRMCS-ready cellular solutions are growing at a 6.95% CAGR to 2030.

- By application, Safety and security maintained a 27.78% of the connected rail market share in 2024. Operational Efficiency is anticipated to register the fastest expansion, advancing at a 6.99% CAGR through 2030.

- By geography, Europe controlled 28.21% of the connected rail market share in 2024; the Middle East & Africa region is on track for a 7.03% CAGR through 2030.

Global Connected Rail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Funding | +1.8% | Global, with the EU and North America leading | Medium term (2-4 years) |

| Predictive-Maintenance ROI | +1.5% | Global, early adoption in Europe and Asia Pacific | Medium term (2-4 years) |

| Passenger Demand For Real-Time Connectivity | +1.2% | Global, concentrated in urban metros | Short term (≤ 2 years) |

| Private 5G / FRMCS Corridor Roll-Outs | +1.0% | Europe primary, expanding to Asia Pacific and MEA | Long term (≥ 4 years) |

| MaaS-Ready Open API Ecosystems | +0.8% | Europe and North America focus | Medium term (2-4 years) |

| Freight Crew Shortages Driving Automation | +0.7% | North America and Australia are primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Funding & Digital-Rail Mandates

Federal and supranational programs shave years off typical payback periods by underwriting large segments of rail digitization. The U.S. Bipartisan Infrastructure Law allocates a huge investment for network modernization, while the Federal Railroad Administration is moving toward mandatory continuous track-geometry monitoring that will push operators beyond periodic visual inspections[1]“Rail Safety Advisory Committee—Track Geometry Measurement System,” Federal Railroad Administration, fra.dot.gov . Japan’s private 5G framework enables a dedicated spectrum for autonomous Shinkansen trials planned for 2029[2]“Private 5G Spectrum Allocation for Rail,” Ministry of Internal Affairs and Communications Japan, mic.go.jp. In Europe, the EU-Rail Joint Undertaking coordinates 34-month FRMCS validation projects, accelerating standard-setting ahead of the 2027 CCS-TSI update. Together, these mandates front-load demand, allowing suppliers to achieve volume efficiencies years earlier than market-only adoption would permit.

Predictive-Maintenance ROI & Uptime Gains

Operators leveraging IoT sensors and machine learning cut failures and extend asset life. SNCF reduced train breakdowns by half and trimmed maintenance outlays by one-third after deploying predictive diagnostics across rolling stock[3]“Predictive Maintenance Performance Report,” SNCF, sncf.com . IBM’s analytics partnership with Downer Rail improved reliability by more than half for an Australian fleet. As sensor costs fall and cloud resources scale, smaller carriers can now access enterprise-grade predictive tools without heavy on-premise investment, further fueling connected rail market adoption.

Passenger Demand For Real-Time Connectivity

Smartphone-native riders expect live status updates, digital ticketing, and in-journey infotainment. East Midlands Railway monetizes passenger information systems through targeted advertising and premium Wi-Fi tiers. Transport for London reported that contactless transactions rose to four-fifths of all taps in 2024, validating the revenue case for open-loop fare collection. Yet operators must balance passenger bandwidth with safety-critical communications on limited spectrum, prompting many to segregate consumer and operational traffic via private cellular networks.

Private 5G / FRMCS Corridor Roll-Outs

A dedicated railway spectrum eliminates contention issues that are seen on public LTE. Deutsche Bahn and Nokia operate a live private 5G pilot that streams real-time position and video feeds to traffic control[4]“5G Rail Pilot,” Deutsche Bahn, db.de . The EU harmonized 874.4–880 MHz and 919.4–925 MHz for FRMCS, providing certainty that equipment vendors need to mass-produce radios. Infrastructure sharing agreements are emerging to reduce the capital burden, particularly for secondary lines with lower passenger volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and Long Payback Cycles | -1.2% | Global, particularly affecting smaller operators | Long term (≥ 4 years) |

| Escalating Cybersecurity | -0.8% | Global, with stricter requirements in North America and EU | Medium term (2-4 years) |

| Unclear National Spectrum Roadmaps | -0.6% | Europe primary, with spillover to Asia Pacific and MEA | Medium term (2-4 years) |

| Legacy-System Interoperability Hurdles | -0.5% | Global, concentrated in mature rail networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX & Long Payback Cycles

Capital budgets struggle to accommodate large-scale digital overhauls. Network Rail’s Train Control Systems Framework illustrates the investment required for nationwide signaling upgrades. Smaller freight and regional passenger lines often defer projects unless subsidies offset initial outlays, exacerbating a two-tier deployment landscape that may hinder network interoperability.

Escalating Cybersecurity & Compliance Costs

Expanded connectivity widens attack surfaces. The Transportation Security Administration now mandates annual drills and vulnerability scans for rail operators. Alstom helped craft IEC 63452, the first rail-specific global cybersecurity standard, adding new audit layers to every major project. Compliance drains operating budgets, particularly for carriers needing specialized consultants, tempering connected rail market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Predictive Maintenance Gains Momentum

Passenger Information Systems held a 27.83% stake in the connected rail market in 2024, underscoring their role in boosting customer satisfaction across metro and intercity services. Although predictive Maintenance accounts for a smaller revenue base, it is projected to lead growth at a 6.93% CAGR through 2030 as falling sensor prices and proven ROI attract budget-constrained operators. Train Tracking and monitoring continue steady uptake due to regulatory visibility mandates, and Automated Fare Collection benefits from contactless payment saturation in developed corridors.

Predictive analytics platforms deliver measurable value by converting real-time condition data into actionable maintenance schedules, cutting service disruptions and spare-parts wastage. Passenger Mobility and entertainment services face prioritization challenges when operators weigh them against mission-critical upgrades, yet premium onboard Wi-Fi tiers produce ancillary revenue that justifies selective rollout. Integrated platforms, such as SWARCO’s Astana deployment, bundle multiple service layers, trimming per-capability costs and increasing reliability.

By Rail Signaling System: CBTC Accelerates Despite PTC Dominance

Positive Train Control commanded 35.46% of the connected rail market in 2024 due to North American mandates. Growth moderates going forward as rollouts enter the maintenance phase. Communication-Based Train Control is set for a 7.06% CAGR, driven by metro operators seeking 30% capacity gains without constructing new track. Automatic Train Control systems remain essential for high-speed lines requiring granular speed enforcement.

Ongoing ETCS Level 2 conversions across European corridors exemplify the sustained investment horizon: ÖBB plans more than three thousand kilometers of coverage by 2038. Suppliers like Hitachi Rail invest heavily in CBTC labs to future-proof their portfolios for driverless operation. Standardization through EU-Rail reduces integration friction and supports cross-border services, a critical factor for multinational train operating companies.

By Rolling Stock Type: Light Rail Leads Growth Trajectory

Electric Multiple Units represented 21.37% of the connected rail market in 2024 as suburban and intercity operators valued their self-propelled flexibility. However, light Rail/Tram Cars are forecast to expand at a 7.11% CAGR, benefiting from city-center emissions regulations and urban densification. Diesel Locomotives maintain relevance in freight, but new orders concentrate on dual-fuel or hydrogen-ready variants.

Battery-electric and hydrogen fuel cell powertrains gain momentum thanks to falling battery prices and policy incentives. Subway vehicles continue incremental additions linked to population growth, while conventional passenger coaches lose share as operators shift to multiple-unit formations. Freight wagons integrate telematics to track cargo conditions and mileage, creating new data streams that feed maintenance and logistics platforms.

By Connectivity Technology: Private 5G Challenges Wi-Fi Dominance

Given its low entry cost and backward compatibility with passenger devices, Wi-Fi retained 43.48% of the connected rail market in 2024. Private 5G/FRMCS-ready networks, projected to register a 6.95% CAGR, offer deterministic latency and stronger security, essential for autonomous operation and advanced diagnostics. Edge computing nodes amplify value by processing sensor feeds locally, cutting backhaul requirements.

Vehicle-to-everything (V2X) links emerge in grade-crossing safety and yard automation use cases. EU standardization unlocks equipment scale economies, whereas North American carriers explore unlicensed millimeter-wave backhaul to sidestep spectrum auctions. Early pilots indicate that hybrid architectures, Wi-Fi for passengers and 5G for operations, deliver optimal cost-benefit balance.

By Application: Operational Efficiency Drives Future Growth

Safety & Security dominated with 27.78% of the connected rail market in 2024 as compliance objectives guided spending. Operational Efficiency, forecast at a 6.99% CAGR, captures management focus as energy costs rise and crew availability tightens. Real-time passenger services keep gaining share but at a slower rate in mature markets; Smart Ticketing shows the highest upside in emerging economies transitioning from cash to digital payments.

Integrated analytics suites consolidate safety assurances with efficiency dashboards, helping dispatchers predict congestion and proactively reroute traffic. Cross-border projects such as the Network Rail–ProRail corridor prove the benefits of data sharing for punctuality and energy optimization. Unified platforms that support both applications lower integration costs while elevating situational awareness.

Geography Analysis

Europe led global revenue with 28.21% of the connected rail market in 2024, propelled by the EU-Rail innovation program and a harmonized FRMCS spectrum plan that minimizes equipment fragmentation. Germany’s Digitale Schiene Deutschland allocates to FRMCS pilots and automatic train operations, reinforcing the region’s technology leadership. The Control Command and Signalling Technical Specification for Interoperability guarantees backward compatibility, ensuring long asset lifecycles even during migrations.

The Middle East & Africa region exhibits the fastest trajectory, targeting a 7.03% CAGR through 2030. Saudi Arabia’s Landbridge, the Riyadh Metro, and the Haramain High-Speed Railway illustrate how oil-rich states deploy connected systems to diversify economies and enhance tourism. The UAE integrates rail into broader smart-city frameworks, spurring demand for IoT sensors, fare collection, and passenger-information APIs.

North America accelerates adoption through the Bipartisan Infrastructure Law’s rail stimulus and upcoming FRA track-geometry mandates. Canada’s Enhanced Train Control framework raises the performance baseline for advanced train protection. Asia–Pacific shows heterogeneous patterns: Japan’s Shinkansen automation program aims for driverless runs by the mid-2030s. China continues high-speed expansion, and India focuses on safety upgrades across its extensive conventional grid.

Competitive Landscape

The connected rail market shows moderate consolidation as leading infrastructure suppliers purchase niche technology firms to fill capability gaps. Hitachi Rail’s acquisition of Thales Ground Transportation Systems adds cybersecurity depth and FRMCS expertise. Wabtec’s purchase of Dellner Couplers aligns mechanical and digital portfolios, enabling end-to-end offerings.

Competitive differentiation is shifting toward software and analytics rather than hardware inputs. Vendors able to layer predictive maintenance, traffic optimization, and cybersecurity onto signaling systems win multiyear service contracts that lock in recurring revenue. Private 5G competence and FRMCS certification are new buying criteria for operators charting GSM-R sunset plans. Smaller, freight-focused technology entrants exploit white spaces in yard automation and crew-shortage solutions, presenting acquisition targets for diversified groups.

Cybersecurity capabilities now sit at the core of supplier selection. The TSA and EU impose rigorous standards, prompting partnerships between rail specialists and IT security firms. Standardization efforts under the EU Agency for Railways narrow hardware differentiation, making software ecosystems and lifetime service support the primary battlefronts for market leaders.

Connected Rail Industry Leaders

Siemens Mobility

Alstom

Hitachi Rail

Thales Group

Wabtec Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Deutsche Bahn awarded Siemens Mobility a EUR 2.8 billion contract to digitize 3,000 km of German track with ETCS Level 2, FRMCS-ready radios, and integrated control centers.

- January 2025: UIC launched the EUR 13.5 million FP2-MORANE-2 project to validate FRMCS across European corridors, involving Deutsche Bahn, Network Rail, SBB, Alstom, Ericsson, Hitachi Rail, Nokia, and Siemens.

- May 2024: Hitachi Rail finalized the EUR 1.66 billion acquisition of Thales Ground Transportation Systems, expanding its signaling and communications portfolio.

Global Connected Rail Market Report Scope

| Passenger Information System |

| Predictive Maintenance |

| Train Tracking & Monitoring |

| Automated Fare Collection |

| Passenger Mobility & Entertainment |

| Positive Train Control (PTC) |

| Communication-Based Train Control (CBTC) |

| Automatic Train Control (ATC) |

| Diesel Locomotive |

| Electric Locomotive |

| Electric Multiple Unit (EMU) |

| Diesel Multiple Unit (DMU) |

| Light Rail / Tram Car |

| Subway / Metro Vehicle |

| Passenger Coach |

| Freight Wagon |

| Wi-Fi |

| Cellular (4G/5G) |

| IoT & Edge Computing |

| V2X Communication |

| Real-Time Passenger Services |

| Safety & Security |

| Operational Efficiency |

| Smart Ticketing |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Service | Passenger Information System | |

| Predictive Maintenance | ||

| Train Tracking & Monitoring | ||

| Automated Fare Collection | ||

| Passenger Mobility & Entertainment | ||

| By Rail Signaling System | Positive Train Control (PTC) | |

| Communication-Based Train Control (CBTC) | ||

| Automatic Train Control (ATC) | ||

| By Rolling Stock Type | Diesel Locomotive | |

| Electric Locomotive | ||

| Electric Multiple Unit (EMU) | ||

| Diesel Multiple Unit (DMU) | ||

| Light Rail / Tram Car | ||

| Subway / Metro Vehicle | ||

| Passenger Coach | ||

| Freight Wagon | ||

| By Connectivity Technology | Wi-Fi | |

| Cellular (4G/5G) | ||

| IoT & Edge Computing | ||

| V2X Communication | ||

| By Application | Real-Time Passenger Services | |

| Safety & Security | ||

| Operational Efficiency | ||

| Smart Ticketing | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the 2025 valuation of the connected rail market?

The connected rail market size reached USD 95.83 billion in 2025.

How fast is the connected rail market expected to grow?

Revenue is projected to rise to USD 133.81 billion by 2030, reflecting a 6.91% CAGR.

Which service category is expanding the quickest?

Predictive maintenance is forecast at a 6.93% CAGR through 2030 based on the strength of proven ROI.

Which region shows the highest growth rate?

The Middle East & Africa region leads with a 7.03% CAGR, fueled by large-scale rail investments.

Why are private 5G networks gaining traction in rail?

They provide dedicated, low-latency connectivity essential for autonomous operation and advanced analytics.

What are the main barriers to adoption?

High capital expenditure, extended payback periods, and escalating cybersecurity compliance costs remain the chief restraints.

Page last updated on: