Rail Infrastructure Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

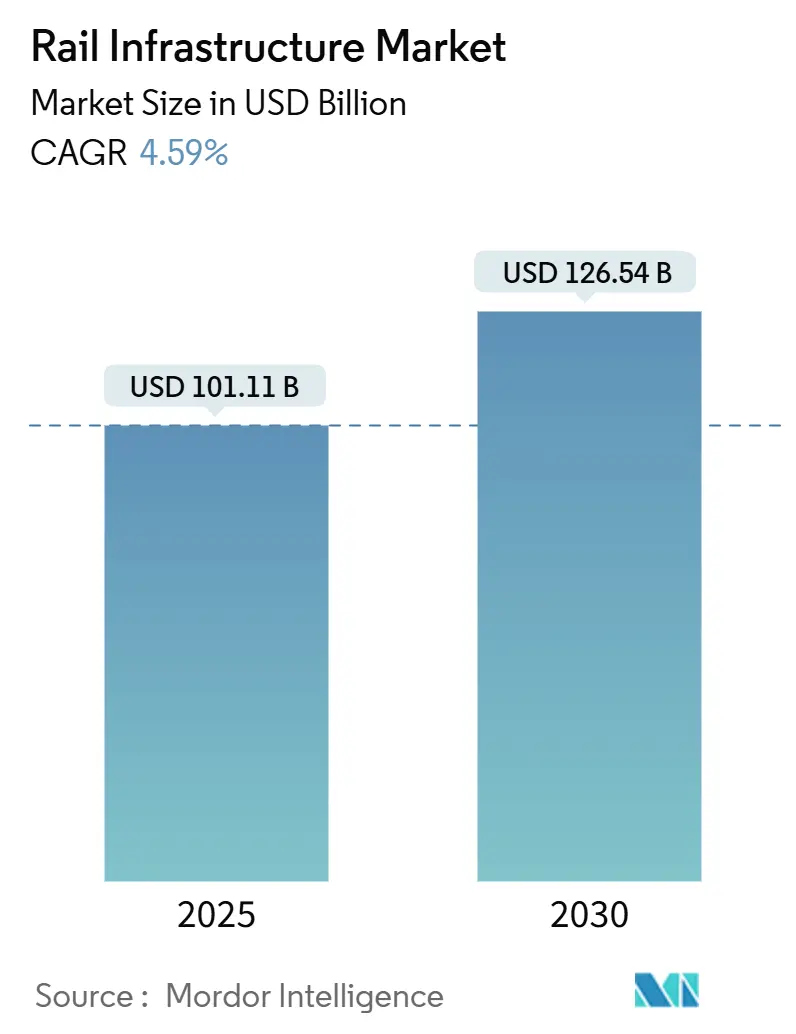

| Market Size (2025) | USD 101.11 Billion |

| Market Size (2030) | USD 126.54 Billion |

| Growth Rate (2025 - 2030) | 4.59% CAGR |

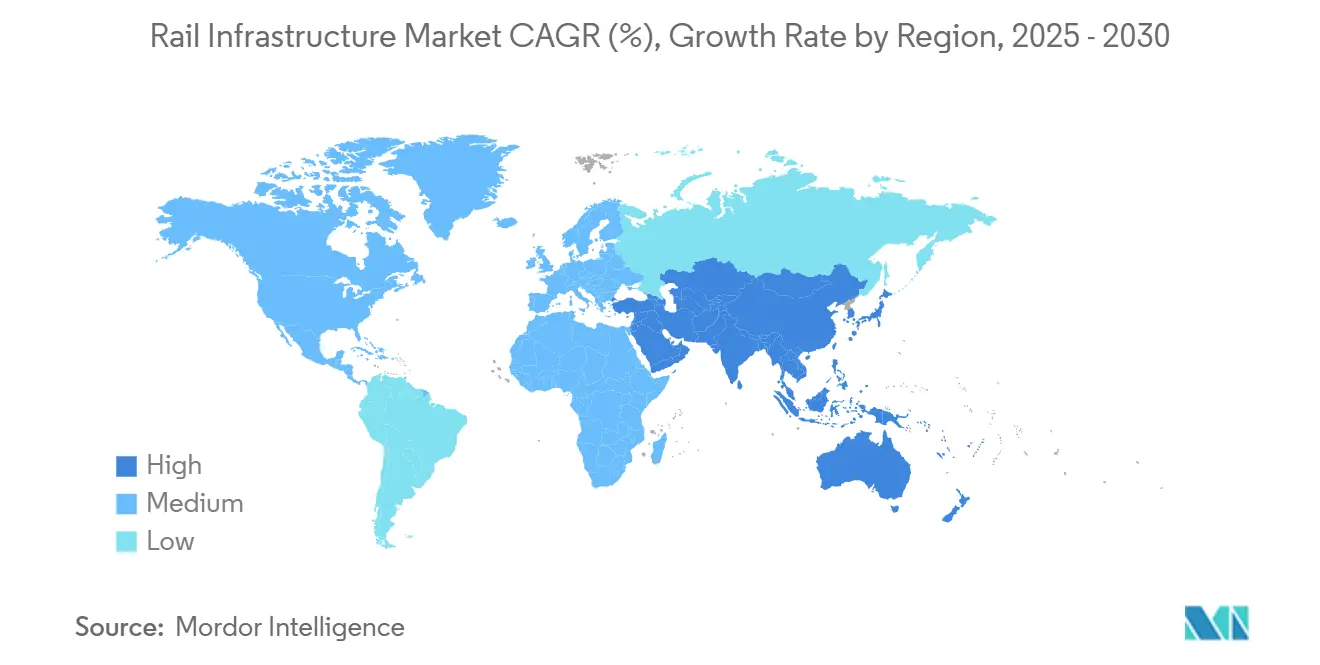

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rail Infrastructure Market Analysis by Mordor Intelligence

The rail infrastructure market size reached USD 101.11 billion in 2025 and is forecast to climb to USD 126.54 billion by 2030, expanding at a 4.59% CAGR during the forecast period (2025-2030). Continuous public-sector commitments to low-carbon transport, large-scale fiscal stimuli, and climate-policy alignment keep the rail infrastructure market resilient even when other capital projects stall. Growing high-speed corridors, heightened urban transit demand, and fast digitalization of assets encourage suppliers to scale production capacity and embed analytics software into physical equipment. Procurement frameworks increasingly reward lifecycle cost reductions, which shifts investment toward signaling upgrades, predictive maintenance, and green construction materials. Competitive rivalry intensifies in technology-rich niches such as control systems, even as civil works work packages remain dominated by cost leadership[1]“Rail Infrastructure Investment Program 2024 Funding Allocation,” U.S. Department of Transportation, DOT.gov.

Key Report Takeaways

- By construction type, new construction held a 53.27% share of the rail infrastructure market in 2024, whereas expansion projects are set to grow at a 7.56% CAGR during the forecast period (2025-2030).

- By equipment, track infrastructure led with a 31.75% share of the rail infrastructure market in 2024; signaling equipment is projected to advance at an 8.92% CAGR during the forecast period (2025-2030).

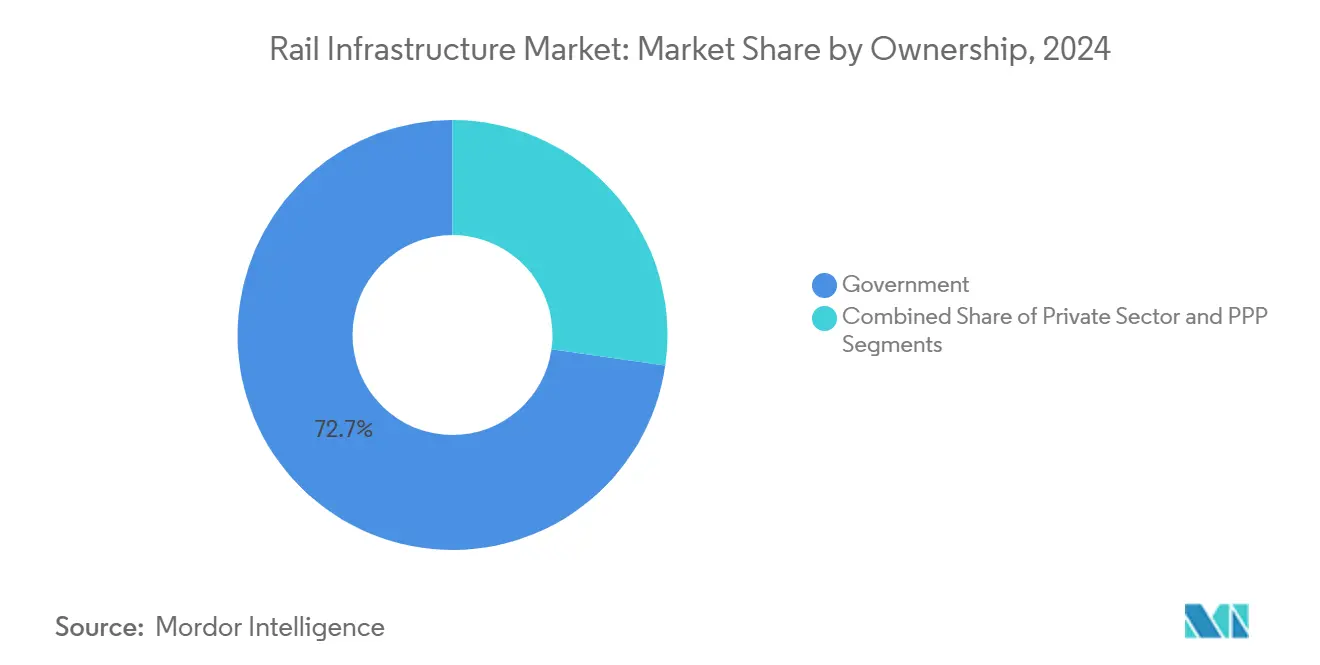

- By ownership, government entities commanded a 72.73% share of the rail infrastructure market in 2024; public-private partnerships are projected to record the quickest 7.98% CAGR during the forecast period (2025-2030).

- By rail type, conventional lines accounted for a 45.07% share of the rail infrastructure market in 2024, while high-speed systems are projected to post a 9.15% CAGR during the forecast period (2025-2030).

- By geography, Asia-Pacific captured 38.93% share of the rail infrastructure market in 2024 and is progressing at a 6.63% CAGR during the forecast period (2025-2030), the fastest among all regions.

Global Rail Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stimulus for Green Transport | +1.2% | Global, with concentration in EU, North America, and China | Medium term (2-4 years) |

| Rising Passenger-Kilometre Demand | +0.9% | Asia-Pacific core, spill-over to South America and Africa | Long term (≥ 4 years) |

| Cross-Border Rail Initiatives | +0.7% | Europe, Southeast Asia, and emerging African corridors | Long term (≥ 4 years) |

| Asset-Life Extension Programs | +0.6% | North America and EU, with adoption spreading to Asia-Pacific | Short term (≤ 2 years) |

| Low-Carbon Steel and Recycled Ballast | +0.4% | Global, led by European regulatory frameworks | Medium term (2-4 years) |

| Rail-As-A-Service Concession Models | +0.3% | Emerging markets, particularly Southeast Asia and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Public-Sector Stimulus for Green Transport

Governments keep raising rail allocations within climate-oriented stimulus packages, exemplified by the United States earmarking USD 2.4 billion for corridor upgrades in 2024. Germany’s infrastructure funds mirror this scale by targeting complete network electrification. Poland channels EUR 43 billion (USD 46.15 billion) toward track modernization, signaling how European Union members use recovery funds to deliver on the Green Deal[2]“Trans-European Transport Network Investment Priorities 2024-2030,” European Commission, Europa.eu. Such predictable pipelines reduce demand risk for suppliers and foster long-lead investments in regional manufacturing. At the same time, visibility into multi-year funding unlocks blended-finance structures that lower the cost of capital for private investors while preserving public service mandates.

Rising Passenger-Kilometer Demand in Megacities

Daily ridership across Asian megacities surges as urban dwellers return to public transport. On August 8, 2025, Delhi Metro achieved a milestone, recording 8.19 million rides, eclipsing its peak of 7.87 million in November 2024. China's major cities are steadily expanding their metro systems, and newer urban centers are bolstering their transit networks to accommodate their burgeoning populations. The resulting crowding pressures push operators to opt for headway-reduction solutions, platform extensions, and rolling-stock augmentation rather than new corridor footprints. Technology providers benefit from orders for CBTC upgrades, platform screen doors, and greater rolling-stock fleet-wide adoption of regenerative braking. These shifts elevate aftermarket service revenue and lengthen supplier backlogs.

Increasing Cross-Border High-Speed Rail Initiatives

Projects such as the Rail Baltic Estonia inked infrastructure construction contracts worth nearly EUR 1 billion (USD 1.07 billion). By 2030, project teams spearheaded by Finnish and French firms will finalize the Estonian segment of the Rail Baltica railway. Similar momentum appears in Southeast Asia, where the Thailand-China route acts as a regional blueprint. Cross-jurisdictional projects demand harmonized safety rules, customs integration, and joint procurement, which favor suppliers with pan-regional certification portfolios. The political symbolism of post-pandemic recovery and decarbonization elevates high-speed rail to top infrastructure diplomacy, channeling grants and export-credit agency support that underwrite long-tenor risk. Supply chains localize as multiple host countries push for domestic manufacturing quotas to capture employment benefits.

Digital-Twin-Enabled Asset-Life Extension Programs

Operators deploy IoT sensors and AI analytics to detect track-geometry deviations before they mature into faults. Software-as-a-service models shift spending from capex peaks toward opex subscriptions, smoothing cash flows for both railways and vendors. Predicted failure windows shrink maintenance delays, boosting on-time performance metrics crucial to winning passenger confidence post-pandemic. In Europe, common data-model standards emerge to aid interoperability of digital twins, which eases multi-vendor integration. Early adopters of the solution see marked decreases in unforeseen operational disruptions, underscoring the benefits of broadening its application throughout the network.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital Intensity | -0.8% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

| Volatile Steel and Cement Costs | -0.6% | Global, with regional variations based on supply chains | Short term (≤ 2 years) |

| Land-Acquisition Litigation Delays | -0.4% | India, California, and densely populated European corridors | Medium term (2-4 years) |

| Cyber-Security Upgrade Gaps | -0.3% | North America & EU legacy networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity and Long ROI Horizon

Building rail infrastructure comes with a hefty price tag. Conventional lines need a significant investment, while high-speed lines push the financial envelope further. These steep initial costs frequently lead to extended payback periods, occasionally stretching across multiple decades. Cost escalations, as seen in the United States West Coast corridor, illustrate how scope creep and design revisions strain fiscal capacity. Private financiers demand sovereign guarantees or minimum-revenue covenants, and their absence curtails appetite for greenfield risk. To compress financial close timelines, authorities now prepare de-risking mechanisms such as availability-based payments, yet budget headroom remains limited. Persistent cost overruns, therefore, threaten to dampen project pipelines and restrain rail infrastructure market growth.

Volatile Steel and Cement Input Costs

Global steel prices have fluctuated due to supply chain disruptions. These fluctuations have compelled contractors to bolster their cost buffers to mitigate financial risks. Additionally, governments are postponing project tenders to avoid budget overruns. Given the significant steel demand in rail construction, even slight price changes can lead to considerable unforeseen costs, impacting project timelines and overall feasibility. Cement follows similar volatility when energy prices spike, leading to periodic procurement pauses. Inflation adjustment clauses in contracts partly shield suppliers, yet backlog profitability narrows, lowering reinvestment capacity. Sustained volatility thus discourages rapid project scale-up and erodes contractor margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Construction Type: Expansion Projects Drive Infrastructure Optimization

New construction maintained a 53.27% share in the rail infrastructure market in 2024. Yet, expansion initiatives generated a 46.73% share in the rail infrastructure market in 2024 and are advancing at a 7.56% CAGR during the forecast period (2025-2030), outpacing greenfield jobs. Operators prefer capacity boosts, double-tracking, grade separations, and platform lengthening because returns materialize quickly once service frequency rises. Regulatory reviews for brownfield work are shorter, trimming holding costs and lifting the rail infrastructure market size linked to upgrades. Environmental impact is lower, which accelerates permit issuance and aligns with climate commitments.

Growth concentrates in Europe’s TEN-T corridors and North American freight pinch points where land scarcity pushes agencies to wring extra throughput from existing rights-of-way. Engineering firms specializing in live-traffic upgrades capture premium fees due to staging complexity. Renovation work, including electrification retrofits, grows, supported by aging-asset replacement cycles and stimulus packages for carbon reduction. Combined, these trends broaden the revenue mix and spread risk across diverse project categories, reinforcing the rail infrastructure market’s robustness.

By Equipment: Signaling Technology Transformation Accelerates Growth

Track-related components retained the largest 31.75% share in the rail infrastructure market in 2024, owing to their ubiquity. Yet, signaling equipment will post the strongest 8.92% CAGR during the forecast period (2025-2030) as European Train Control System and CBTC mandates proliferate. Each kilometer of ETCS Level 2 upgrade adds material and software value that surpasses traditional relay-based spending, lifting average revenue per kilometer and enlarging the rail infrastructure market share of digital equipment. Rolling stock replacements contribute to track renewal cycles because heavier axle-load capacities necessitate rail-grade enhancements.

Investment also pivots toward power supply resiliency and 5G communication backbones that enable fully automated train operations, adding a further impetus to the “other equipment” basket. Bridges and tunnels, while lower-growth, gain from seismic retrofits in Japan and California. Suppliers benefit from multi-year framework contracts, locking in visibility and encouraging R&D into modular track panels and fiber-optic sensing, which extend maintenance intervals.

By Ownership: PPP Models Gain Momentum Despite Government Dominance

Government entities held a 72.73% share in the rail infrastructure market in 2024, underlining rail’s position as a strategic public good. Nonetheless, PPP concessions will expand at a 7.98% CAGR during the forecast period (2025-2030), as authorities blend private capital with public-interest mandates to accelerate project delivery. Availability-based payment schemes allow investors to recoup costs through performance metrics instead of ridership risk, improving bankability and boosting the rail infrastructure market size attached to privately financed projects.

Freight corridors and suburban transit lines dominate the private-sector share because freight yields remain commercially attractive. PPP units in India and Southeast Asia now issue standardized contracts that minimize renegotiation, creating scale economies for concessionaires across multiple geographies. As these structures mature, procurement pipelines diversify beyond mega projects, tapping regional and brownfield segments that were historically state-funded, broadening market liquidity.

By Rail Type: High-Speed Systems Lead Innovation Despite Conventional Dominance

Conventional rail accounted for a 45.07% share in the rail infrastructure market in 2024. Still, high-speed lines will enjoy the quickest 9.15% CAGR during the forecast period (2025-2030), as countries pursue intercity mobility and carbon targets. Each kilometer of high-speed alignment demands specialized slab track, continuous welded rail, and advanced signaling, tripling the cost relative to conventional equivalents. Consequently, the rail infrastructure market size for high-speed projects expands quickly once a nation commits to a multi-line program.

Urban transit continues to secure municipal funding because metros alleviate congestion and support dense land-use planning. Earnings from automated metro builds are resilient, given guaranteed patronage subsidies and real-estate tax capture. Supplier roadmaps now converge: hybrid rolling stock platforms share components between high-speed and metro categories, lowering unit costs and elevating fleet renewal cadence, which underpins recurring aftermarket income.

Geography Analysis

Asia-Pacific retained a 38.93% share in the rail infrastructure market in 2024 and progresses at a 6.63% CAGR during the forecast period (2025-2030), underpinned by China’s Belt and Road extensions and India’s National Rail Plan implementation. As urban populations swell, smaller cities in China swiftly roll out metro systems, paralleling the rapid expansion of high-speed rail networks across various provinces. Japan exports Shinkansen know-how through public-finance packages, opening doors for home suppliers to capture overseas orders. Southeast Asian corridors, epitomized by Laos–Thailand connectivity, adopt harmonized standards to spur freight and tourism, enriching supplier addressable markets.

North America is on a 5.21% CAGR during the forecast period (2025-2030) due to investment in federal rail allocations that cover passenger service upgrades and freight bottleneck removal. Canada’s corridor improvement around Toronto-Montreal-Ottawa deepens demand for signaling retrofits and bilevel rolling stock. Mexico aligns Pacific port cargo lines toward the United States gateways, leveraging USMCA provisions. Strict Federal Railroad Administration compliance barriers keep new entrants low, favoring incumbents with certified safety systems, thereby stabilizing competitive margins.

Europe grows at 4.66% CAGR during the forecast period (2025-2030), steered by the Trans-European Transport Network budget and Rail Baltica funding. Germany allocates multi-billion through 2030 to boost freight capacity and finalize electrification. France accelerates regional network upgrades while Eastern European members modernize Soviet-legacy tracks. Interoperability regulations drive mass ETCS procurement, standardizing demand and simplifying supplier qualification. Climate taxation on aviation also nudges modal shift toward rail, indirectly enlarging revenue pools.

Competitive Landscape

Chinese state-owned enterprises dominate large civil-works packages through scale economies and state-credit backing, led by China Railway Group’s and China Railway Construction Corp.’s shares. European firms Alstom and Siemens Mobility hold technology moats in signaling, rolling stock, and digital services, extending lifecycle contracts that elevate recurring revenues. North American contractors specialize in freight and heavy-haul earthworks, yet their global footprint remains limited compared to Asian peers.

Competitive strategy converges on vertical integration: CREC fabricates steel girders in-house, while Alstom extends into predictive-maintenance software, bundling hardware and analytics. M&A activity continues, typified by Hitachi Rail’s acquisition of a major signaling unit, sharpening end-to-end offerings. Regional capacity investments, such as Stadler’s Eastern European factory, mitigate currency volatility and cut logistics costs, preserving bid competitiveness. Cyber-resilience and low-carbon credentials emerge as new tender differentiators, spurring R&D alliances across the value chain.

Supplier margins vary by segment: signaling and digital twins command double-digit EBIT thanks to IP barriers and certification complexity, whereas conventional civil works trend toward mid-single-digit profitability due to commoditization. Nonetheless, long project cycles stabilize revenue, and strong order books shield incumbents from short-term macro shocks. Sustainable-finance taxonomies begin influencing capital access, rewarding firms with science-based emission targets and circular-economy material sourcing.

Rail Infrastructure Industry Leaders

China Railway Group (CREC)

China Railway Construction Corp. (CRCC)

Alstom SA

Siemens Mobility

Hitachi Rail

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Portalp Group, renowned for its expertise in automatic doors and entrance systems, has launched Portalp Railway. This new venture focuses on the railway sector, offering solutions like platform screen doors, guided transport systems, railway access control, and specialized metalwork.

- August 2025: Texmaco Rail & Engineering Ltd has partnered with Rail Vikas Nigam Ltd (RVNL) in a joint venture to advance India's railway modernization and export competitiveness. The venture will produce rolling stock, undertake EPC projects, manage depot operations, and pursue global tenders. Texmaco will hold a 49% stake, while RVNL will remain the majority shareholder.

- August 2025: Amtrak has started preconstruction activities and awarded design-build contracts for three rail yard modernization projects along the Northeast Corridor (NEC). These upgrades aim to bolster service reliability and facilitate top-tier train maintenance.

- June 2025: PORR, an Austrian construction firm, secured a €428m (USD 487.7m) contract from Romania's National Railway Company to renovate and modernize the Craiova–Drobeta Turnu Severin–Caransebeș railway line. The project, part of efforts to upgrade Romania's railway infrastructure to European standards, includes transforming 32.6km of track to a double-track system, constructing 18 bridges and 54 culverts, building a 1,279m twin-track Poarta I tunnel, and renovating the 496m Rachitoberg Tunnel.

Global Rail Infrastructure Market Report Scope

| New Construction |

| Expansion |

| Renovation |

| Track |

| Bridges |

| Tunnels |

| Signals |

| Rolling Stock |

| Others |

| Government / Public Sector |

| Private Sector |

| Public–Private Partnerships (PPP) |

| Conventional Rail Systems |

| High-Speed Rail Systems |

| Urban Transit Systems (Metro, Light Rail) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Construction Type | New Construction | |

| Expansion | ||

| Renovation | ||

| By Equipment | Track | |

| Bridges | ||

| Tunnels | ||

| Signals | ||

| Rolling Stock | ||

| Others | ||

| By Ownership | Government / Public Sector | |

| Private Sector | ||

| Public–Private Partnerships (PPP) | ||

| By Rail Type | Conventional Rail Systems | |

| High-Speed Rail Systems | ||

| Urban Transit Systems (Metro, Light Rail) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the rail infrastructure market in 2025 and how fast will it grow?

Revenue reached USD 101.11 billion in 2025 and is forecast to expand at a 4.59% CAGR to USD 126.54 billion by 2030.

Which region contributes the most revenue to global rail projects?

Asia-Pacific held 38.93% of 2024 revenue and continues to lead due to large-scale builds in China and India.

Which construction type is expanding quickest?

Expansion projects outpace new builds at a 7.56% CAGR as operators maximize existing network capacity.

Why are signaling systems attracting more investment than other equipment?

Mandatory ETCS and CBTC upgrades push signaling spend to an 8.92% CAGR, outstripping track and civil segments.

What share do government entities still control?

Public bodies account for 72.73% of global revenue, but PPP concessions are the fastest-growing ownership model.

Page last updated on: