Railway NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

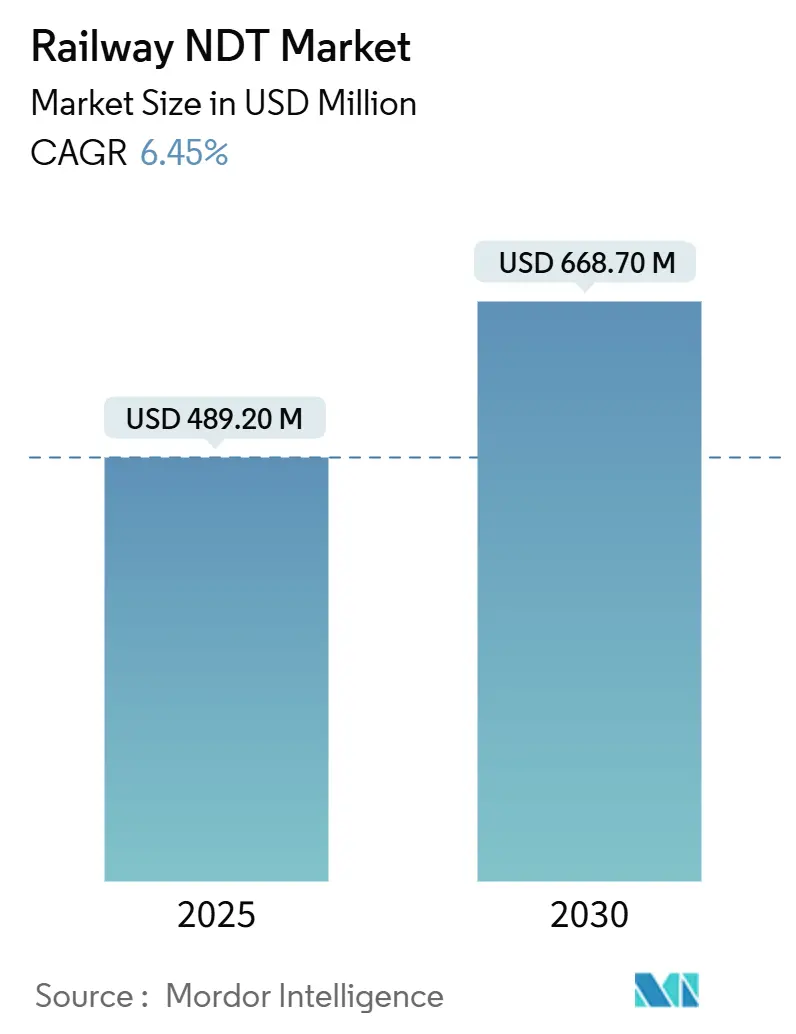

| Market Size (2025) | USD 489.20 Million |

| Market Size (2030) | USD 668.70 Million |

| Growth Rate (2025 - 2030) | 6.45% CAGR |

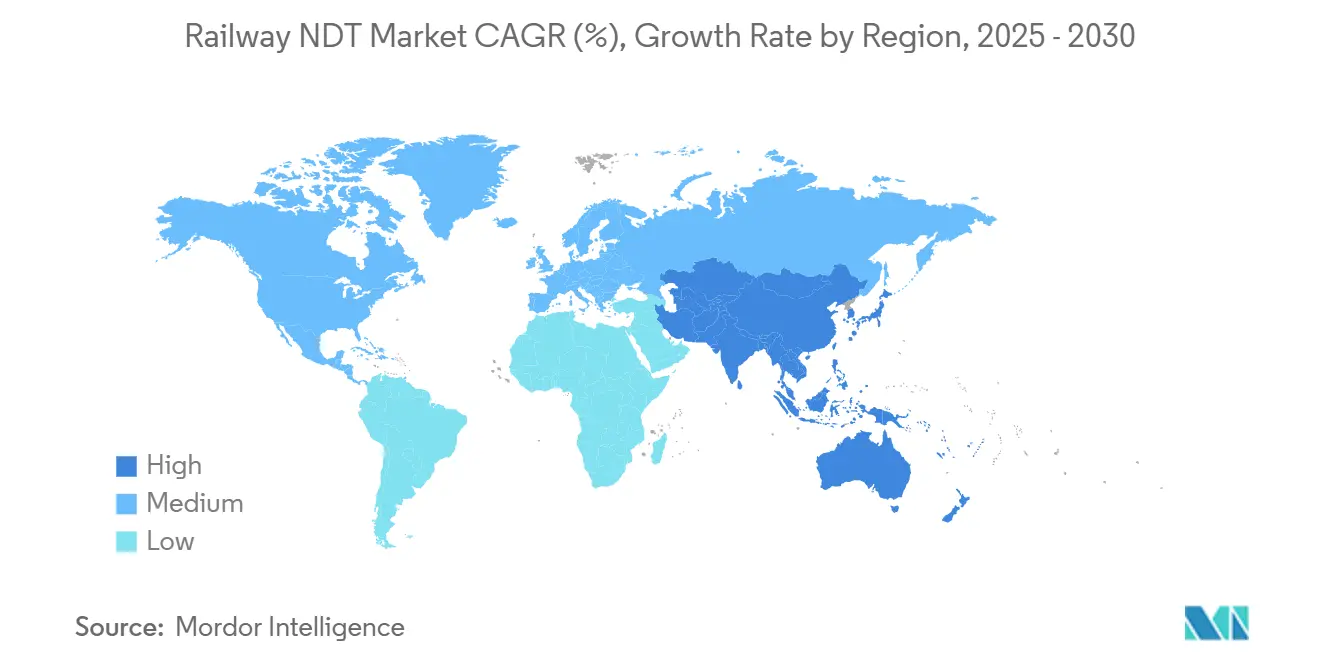

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

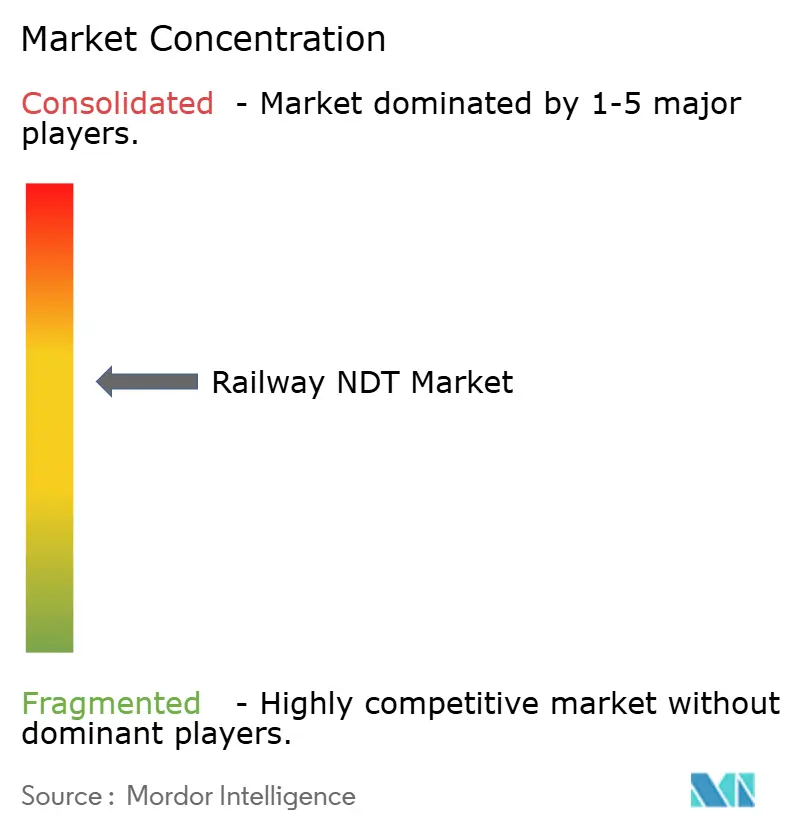

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Railway NDT Market Analysis by Mordor Intelligence

The railway NDT market size is estimated at USD 0.49 billion in 2025 and is projected to reach USD 0.67 billion by 2030, growing at a 6.45% CAGR over the forecast period. The Asia-Pacific region remains the pivotal growth engine as governments accelerate network expansion, while digitalization, stricter safety regulations, and condition-based maintenance contracts collectively reinforce demand for non-destructive testing across global rail assets. Service outsourcing continues to dominate procurement decisions because operators prefer turnkey inspection agreements that bundle equipment, personnel, and analytics. At the same time, rapid adoption of AI-driven software, eddy-current sensors, and wayside monitoring hardware signals the sector’s transition toward always-on asset health visibility. Competitive intensity is shifting from hardware differentiation to integrated data platforms, which promise lower life-cycle costs and higher network availability. The net result is a steady, broad-based expansion of the railway NDT market that is resilient to cyclical capex swings, given its regulatory and safety underpinnings.

Key Report Takeaways

- By component, services led with 78.8% revenue share in 2024, while software is projected to expand at an 11.4% CAGR through 2030.

- By testing method, ultrasonic testing accounted for 27.5% of the railway NDT market share in 2024, and eddy-current testing is set to register the fastest CAGR of 8.4% from 2024 to 2030.

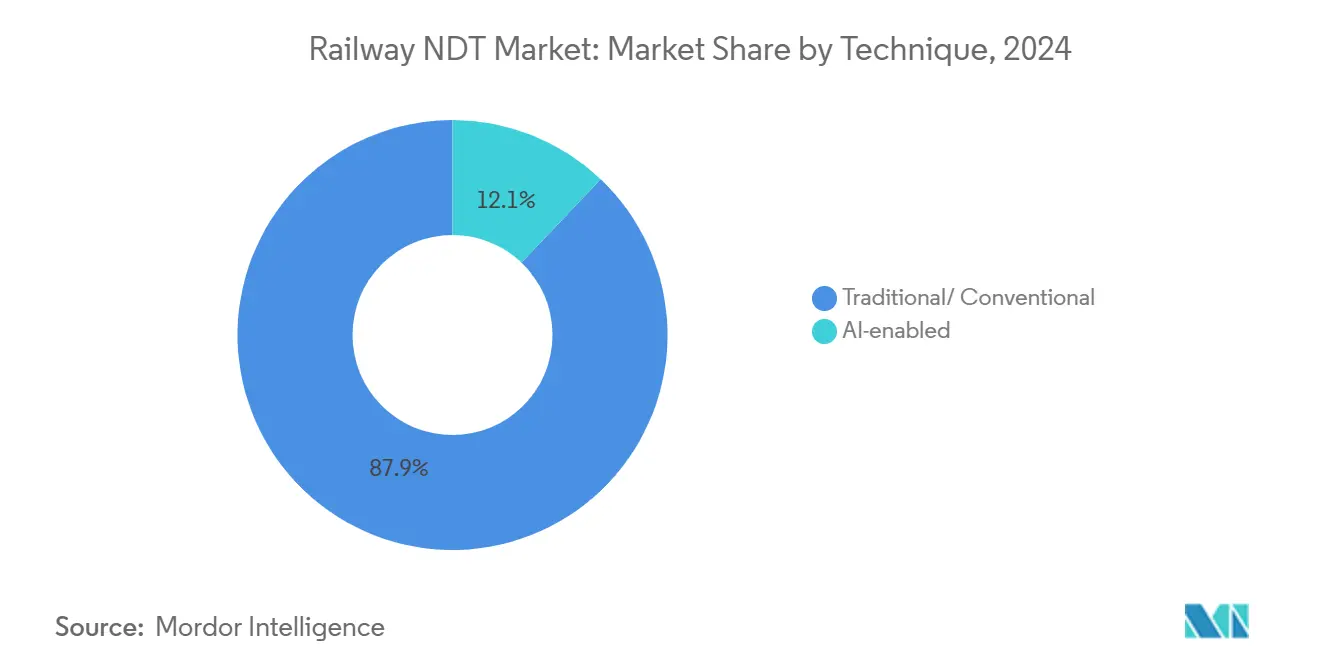

- By technique, traditional approaches commanded an 87.9% share of the railway NDT market size in 2024; AI-enabled techniques are projected to post the highest 14.5% CAGR through 2030.

- By geography, the Asia-Pacific region captured 36.3% of the railway NDT market in 2024 and is expected to advance at a 7.1% CAGR over the forecast horizon.

Global Railway NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising high-speed rail investments | +1.8% | Asia-Pacific core, spillover to Europe and North America | Medium term (2-4 years) |

| Digitalization of rail asset maintenance | +1.2% | Global, led by developed markets | Short term (≤ 2 years) |

| Stricter rail-safety regulations worldwide | +0.9% | Global, with varying enforcement timelines | Long term (≥ 4 years) |

| Shift toward condition-based maintenance | +0.8% | North America and Europe leading, Asia-Pacific following | Medium term (2-4 years) |

| Hydrogen-powered trains | +0.4% | Europe and Asia-Pacific early adopters | Long term (≥ 4 years) |

| Deployment of 5G-enabled wayside systems | +0.6% | Initially developed markets, global expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising High-Speed Rail Investments

Record infrastructure outlays are intensifying inspection requirements. China committed USD 50 billion to new high-speed corridors in 2024, while the European Union earmarked EUR 12 billion (USD 13.6 billion) for network upgrades.[1]European Union, “Trans-European Transport Network Investment Program,” ec.europa.euHigh-speed tracks require inspection cycles at least three times more frequently than conventional lines, resulting in approximately USD 15,000 in annual service demand per kilometer, compared to USD 4,000 on legacy routes. Japan’s USD 8 billion Shinkansen extensions affirm that even mature markets fuel incremental growth. Ultrasonic and eddy-current modalities benefit most, as they detect micro-fractures and fatigue patterns induced by sustained operations at 300 km/h.

Digitalization of Rail Asset Maintenance Programs

Operators integrate IoT sensors, 5G links, and AI analytics to migrate from calendar-based to data-driven upkeep. Deutsche Bahn’s 2024 rollout across 33,000 km of track reduced unplanned interventions by 23% and lowered inspection spend by 15%. Such platforms propel the software component and raise demand for portable devices that stream readings to central dashboards. Condition-based contracts reward uptime rather than task execution, nudging suppliers toward predictive algorithms that flag anomalies weeks in advance of manual checks.

Stricter Rail-Safety Regulations Worldwide

The United States Federal Railroad Administration enforced enhanced ultrasonic schedules for services exceeding 125 mph beginning in 2024.[2]Federal Railroad Administration, “Revised Track Safety Standards,” fra.dot.gov Europe’s Technical Specifications for Interoperability now require thermography of electrics and acoustic emission monitoring on load-bearing members. Harmonization by the International Union of Railways establishes a new baseline, ensuring stable demand even when capital budgets are tightened. Certified, full-suite vendors gain negotiating leverage because operators favor single-source compliance assurance.

Shift Toward Condition-Based Maintenance Contracts

Network Rail achieved 18% cost savings and 99.2% track availability in 2024 by transitioning 20,000 miles of infrastructure to outcome-based agreements. The model encourages suppliers to install embedded sensors, automate data capture, and assume performance risk throughout the asset's life cycle. Smaller firms find the investment hurdle steep, spurring consolidation as larger groups acquire analytics specialists to close capability gaps. The trend reinforces software growth, creating a feedback loop where reliable predictions unlock further contract wins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive inspection rolling stock | –1.1% | Global, higher impact in developing markets | Short term (≤ 2 years) |

| Shortage of certified NDT technicians | –0.8% | North America and Europe primarily | Medium term (2-4 years) |

| Fragmented rail-standards landscape | –0.6% | Global, with regional variations | Long term (≥ 4 years) |

| Self-diagnostic track materials | –0.4% | Developed markets initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Inspection Rolling Stock

Acquiring a multifunction inspection vehicle can cost USD 15-20 million, a sum that strains budgets in emerging economies.[3]Railway Gazette International, “Cost Analysis of Inspection Rolling Stock,” railwaygazette.com Operators must choose between extending track length and modernizing diagnostic fleets, which limits the near-term uptake of computed tomography or thermography systems. Leasing mitigates upfront costs but increases operating expenses over the contract life. The divide is creating a two-speed railway NDT market where advanced techniques cluster in developed regions while basic ultrasonic sets prevail elsewhere.

Shortage of Certified NDT Technicians

Retirements, aging demographics, and slow training cycles have widened the talent gap, with unfilled positions increasing by 35% in 2024 across North America and Europe. A newly certified railway technician typically requires up to 24 months of mentored practice before qualifying for Level II roles. The scarcity caps throughput even when equipment is available, prompting suppliers to adopt automated scanners, remote evaluation centers, and AI classification to alleviate the manual burden. Larger firms invest in academies, yet the supply lag is likely to persist through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Dominance Amid Software Surge

Services represented 78.8% of the railway NDT market in 2024 as operators relied on turnkey inspection partnerships for regulatory compliance and risk transfer. Equipment upgrades nevertheless sustain a secondary replacement cycle, notably as fleets retire aging single-frequency ultrasonic rigs in favor of digital multi-sensor carts. The software slice, although only a fraction of the total spend, is scaling at the fastest rate, with an 11.4% CAGR, mirroring the industry’s pivot from data collection to data interpretation. Railway NDT market size gains increasingly depend on these AI dashboards, which process terabytes of readings into actionable alerts that cut downtime.

Continuous contract revenue gives service majors predictable cash flows and the balance sheet strength to invest in cloud platforms and technician academies. Conversely, equipment vendors tend to gravitate toward outcome-based financing, bundling hardware, software, and maintenance into subscription models. Consumables, though small, track underlying test volumes because magnetic particle powders, penetrants, and couplants must be replenished regularly. Together, these dynamics ensure that the railway NDT market remains service-centric yet progressively software-enabled, blurring historical boundaries among value chain players.

By Testing Method: Ultrasonic Leadership With Eddy-Current Acceleration

Ultrasonic testing captured 27.5% of the railway NDT market share in 2024, favored for rail head, weld, and wheel inspections that need volumetric flaw sizing. Portable phased-array sets and automated ride-on systems extend reach to switches and crossings, sustaining healthy replacement demand. Eddy-current testing, which accounts for a smaller slice, is the rising star with an 8.4% CAGR, as it excels at detecting surface and near-surface cracks formed under high-speed loads. Its rapid scan rates and minimal couplant needs make it ideal for wayside installations along 300 km/h corridors.

Radiography retains a niche in weld quality assurance, while magnetic particle and liquid penetrant methods are used to inspect axles and fastening components. Acoustic emission testing is gaining momentum for bridge monitoring, offering real-time alerts for crack growth. Thermography, bolstered by widespread railway electrification, finds application in catenary and power electronics diagnostics. Computed tomography remains limited to depots and R&D labs given its cost and throughput constraints, yet it offers unmatched insight for failure analysis of complex castings.

By Technique: Traditional Methods Dominate While AI Surges

Conventional procedures, such as manual ultrasonic, visual, and magnetic particle evaluation, still hold 87.9% share because regulators mandate proven processes for safety-critical networks. Documentation, technician familiarity, and existing capital stock reinforce this leadership. However, AI-enabled solutions are expanding at a 14.5% CAGR, integrating machine learning with robotics to automate image analysis, classify defect severity, and predict growth rates. Adoption accelerates where operators embrace remote-first strategies that minimize track possession time.

Hybrid workflows are emerging. An automated trolley performs the scan, uploads data to a cloud engine, and dispatches exception reports to a central control room. Field personnel then validate only flagged hotspots, cutting inspection hours and exposure risks. As algorithms gain certification and trust, AI is expected to shoulder a greater share of approval decisions, carving out an irreversible growth trajectory within the railway NDT market.

Geography Analysis

The Asia-Pacific region remains the gravitational center of the railway NDT market. The region accounted for 36.3% of global revenue in 2024 and is advancing at a 7.1% CAGR as China, India, Thailand, and Indonesia pour billions into new high-speed corridors, double-tracking, and electrification. China’s 2024 budget alone allocated USD 50 billion for fresh mileage, generating large recurrent inspection volumes. India’s National Rail Plan prioritizes modern signaling, track upgrading, and dedicated freight routes that require ultrasonic, eddy-current, and thermography coverage. Local suppliers offer competitive pricing, yet multinational NDT specialists often win contracts that require global certifications and multi-technology fleets.

Europe ranks second, buoyed by the European Union’s Trans-European Transport Network funding that mandates rigorous cross-border safety harmonization. Ultrasonic testing remains the backbone, but deployments of eddy-current and acoustic emission testing are rising along newly upgraded 200 km/h corridors in Spain and Italy. The region’s mature operators also lead the adoption of AI analytics, leveraging standardized data formats to compare performance across national boundaries.

North America exhibits steady expansion, anchored by robust freight networks and selective passenger upgrades on the Northeast Corridor. Tight Federal Railroad Administration standards drive non-discretionary demand. Canadian National Railway’s five-year condition-based contract exemplifies long-cycle outsourcing, which combines rolling stock, software, and technicians into a single service envelope. Middle East and Africa, although smaller in value, present double-digit growth pockets as Saudi Arabia and the United Arab Emirates embed comprehensive NDT programs into new intercity and freight lines. Africa’s standard-gauge railway builds in Kenya and Tanzania are increasingly specifying ultrasonic and visual tools during the construction phase, setting the stage for sustained aftermarket revenues.

Competitive Landscape

The railway NDT market presents moderate concentration. Baker Hughes, MISTRAS Group, Olympus (Evident), SGS, and Eddyfi Technologies anchor the top tier, boasting diversified portfolios that span from handheld devices to cloud analytics. Deals such as Eddyfi’s 2025 acquisition of Rail Technology International illustrate consolidation aimed at blending hardware depth with software agility. Baker Hughes invested USD 45 million in a dedicated research hub and AI-ready ultrasonic line to secure its position on high-speed projects.[4]Baker Hughes, “Waygate Technologies Investment Announcement,” bakerhughes.com

Outcome-based agreements alter the competitive landscape: providers now guarantee asset availability rather than delivering tests, thereby raising capital requirements and increasing risk exposure. Smaller regional firms pivot to subcontract niches in consumables or technician leasing. Technology disruptors focus on computer vision, drones, and edge AI that unlock remote monitoring. Barriers persist, however, as operators prefer partners with global certifications and proven incident-free records. Market leaders leverage scale to absorb R&D costs and roll out training academies that alleviate technician scarcity, reinforcing their grip on premium contracts.

Regional fragmentation still offers entry points. In Southeast Asia, new-build railways often package NDT scope with civil works, creating temporary openings for specialized firms. Conversely, in Europe and North America, established frameworks and insurance stipulations favor incumbents. Over the next five years, strategic alliances between sensor manufacturers and software houses are likely to accelerate, positioning combined entities to capture the expanding AI-enabled slice of the railway NDT market.

Railway NDT Industry Leaders

MISTRAS Group Inc.

Eddyfi Technologies Inc.

Olympus Corporation (Evident)

SGS SA

Bureau Veritas SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Baker Hughes Company committed USD 45 million to broaden Waygate Technologies’ railway portfolio, establishing an NDT research center in Germany and partnering with European operators for high-speed ultrasonic field trials.

- August 2025: MISTRAS Group won a USD 78 million five-year contract with Canadian National Railway covering 32,000 km of track, featuring automated inspection vehicles and real-time dashboards that aim to cut service disruptions by 35%.

- July 2025: Eddyfi Technologies acquired Rail Technology International for USD 23 million, bolstering eddy-current offerings and deepening its European and North American customer base.

- June 2025: Olympus Corporation (Evident) rolled out OmniScan X4, an AI-assisted ultrasonic platform tailored to railway needs that reduces scan time by 40% through automated defect recognition.

Global Railway NDT Market Report Scope

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional / Conventional |

| AI-enabled |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Equipment | ||

| Software | |||

| Services | |||

| Consumables | |||

| By Testing Method | Ultrasonic Testing | ||

| Radiographic Testing | |||

| Magnetic Particle Testing | |||

| Liquid Penetrant Testing | |||

| Visual Inspection Testing | |||

| Eddy-Current Testing | |||

| Acoustic Emission Testing | |||

| Thermography / Infrared Testing | |||

| Computed Tomography Testing | |||

| By Technique | Traditional / Conventional | ||

| AI-enabled | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the railway NDT market in 2025, and at what rate is it growing?

The railway NDT market size is USD 489.2 million in 2025 and is projected to reach USD 668.7 million by 2030 at a 6.45% CAGR.

Which region contributes the largest share to railway nondestructive testing?

The Asia-Pacific region is expected to lead with a 36.3% share in 2024, driven by high-speed line construction in China, India, and Southeast Asia.

What component segment is expanding the fastest?

Software is the fastest-growing component, advancing at an 11.4% CAGR as operators adopt AI analytics for predictive maintenance.

Which testing method is gaining momentum besides ultrasonic inspection?

Eddy-current testing is emerging rapidly, with an 8.4% CAGR, because it excels at detecting surface cracks on high-speed rail tracks.

Why are AI-enabled techniques important for future inspection strategies?

AI systems automate defect recognition and predict failure timelines, reducing manual workloads and preventing unplanned service outages.

What is the main challenge limiting short-term growth?

A shortage of certified technicians and the high capital cost of modern inspection rolling stock restrain near-term expansion, especially in developing markets.

Page last updated on: