Wi-Fi Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

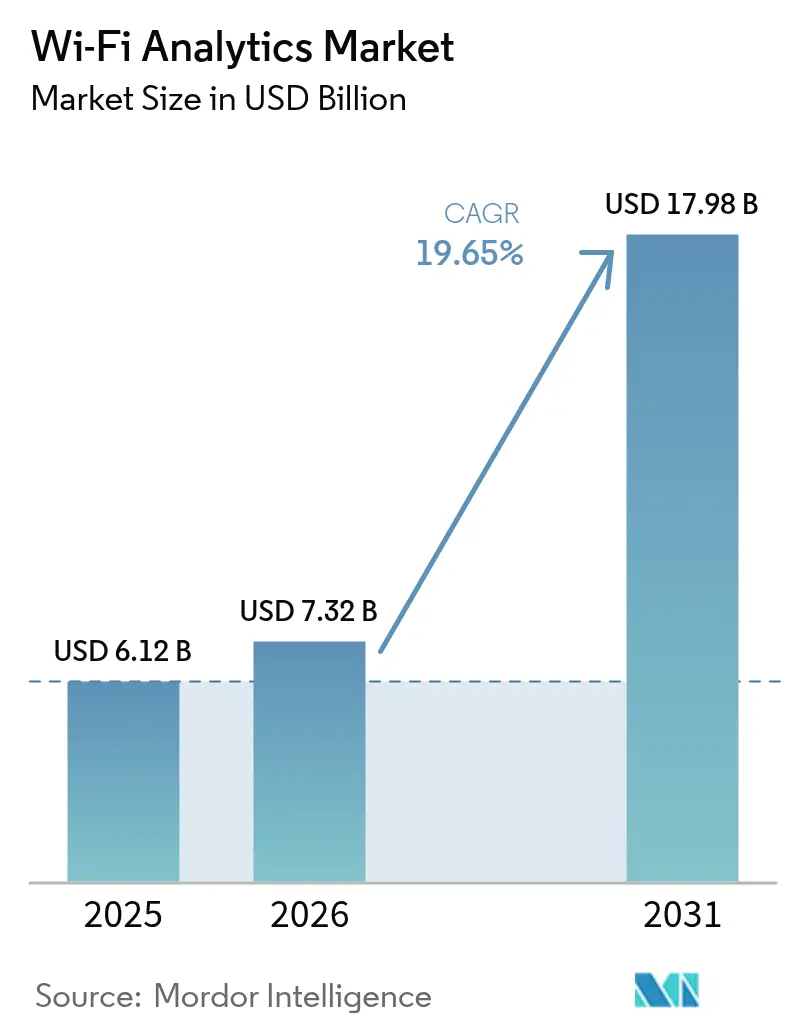

| Market Size (2026) | USD 7.32 Billion |

| Market Size (2031) | USD 17.98 Billion |

| Growth Rate (2026 - 2031) | 19.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wi-Fi Analytics Market Analysis by Mordor Intelligence

The Wi-Fi analytics market size was valued at USD 6.12 billion in 2025 and estimated to grow from USD 7.32 billion in 2026 to reach USD 17.98 billion by 2031, at a CAGR of 19.65% during the forecast period (2026-2031). Enterprises now treat access points as data-collection assets that fuel real-time decision making, rather than as basic connectivity tools. Commercial roll-outs of Wi-Fi 7, wider 6 GHz spectrum access, and the spread of edge AI in access points amplify demand. Hospitality remains the largest user group, while retail’s fast climb shows how brick-and-mortar operators are turning location data into a competitive advantage. Cloud deployment rules the landscape as companies favor subscription models that scale without heavy capital expense.

Key Report Takeaways

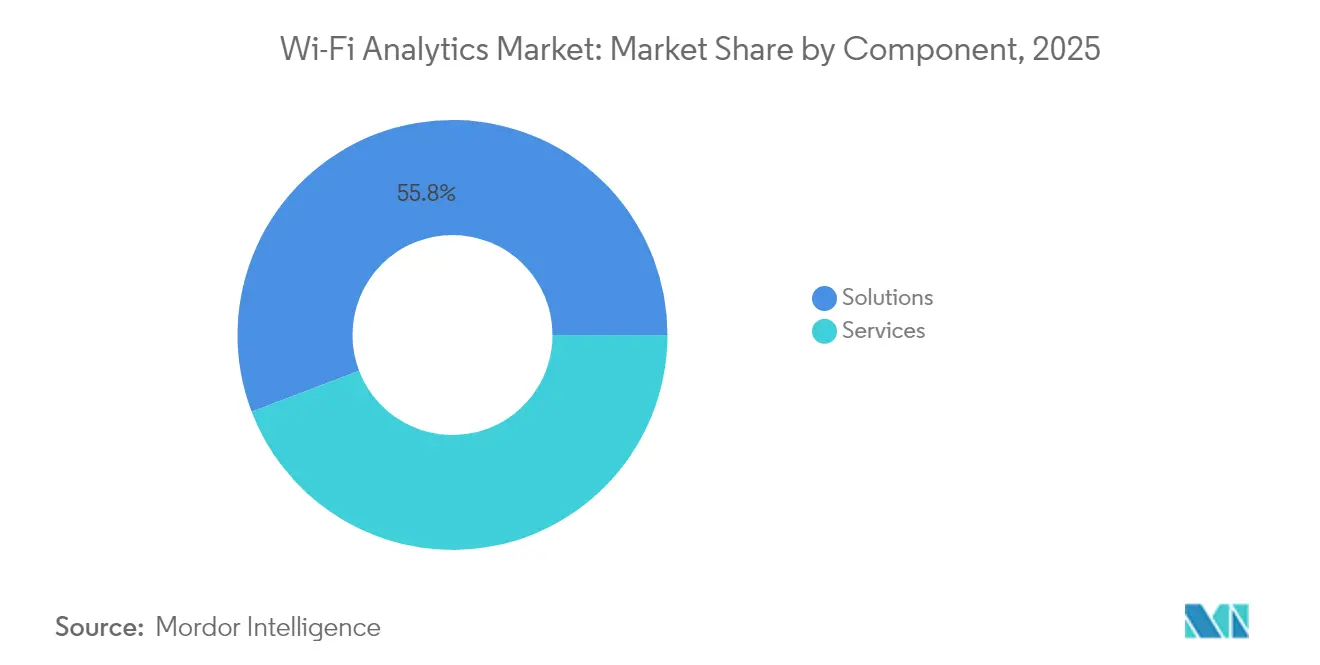

- By component, solutions held 55.80% of the Wi-Fi analytics market share in 2025; services are forecast to expand at a 20.95% CAGR to 2031.

- By deployment, the cloud segment commanded 62.10% share of the Wi-Fi analytics market size in 2025 and is projected to grow at 21.35% CAGR through 2031.

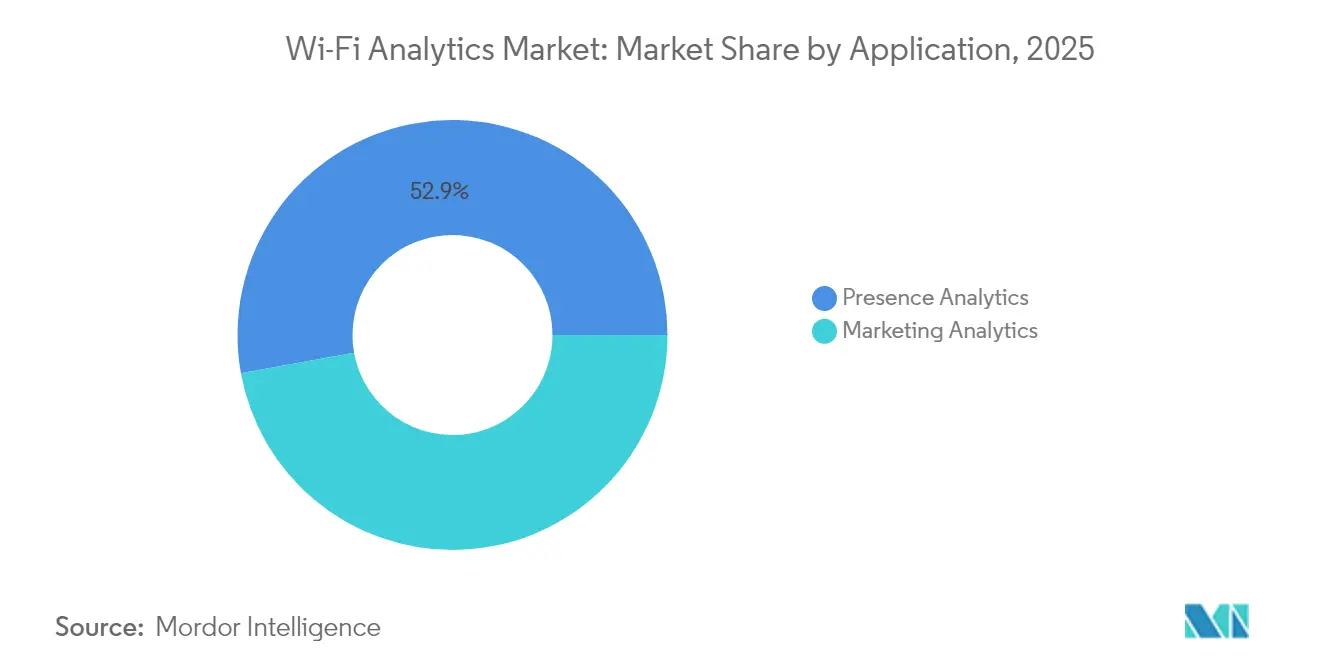

- By application, presence analytics captured 52.85% revenue share in 2025; marketing analytics is advancing at a 20.05% CAGR to 2031.

- By end-user vertical, hospitality led with 31.60% share in 2025, while retail is set to expand at 20.35% CAGR through 2031.

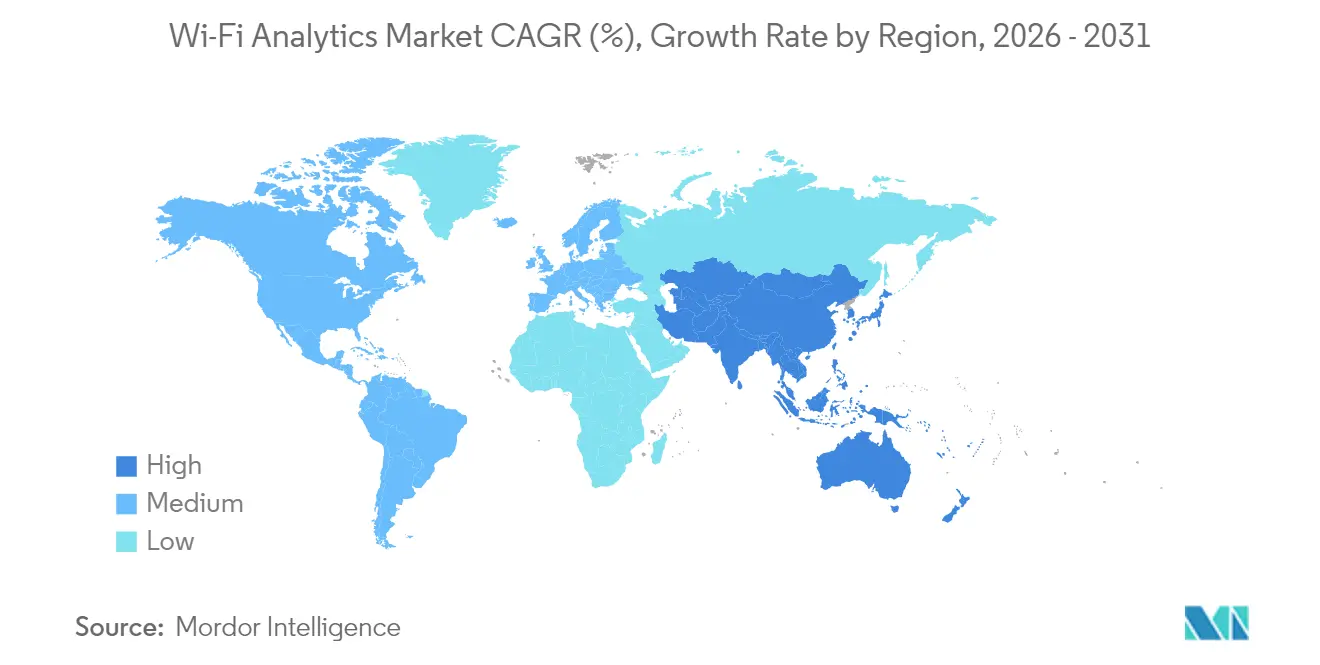

- By geography, North America retained 30.85% share in 2025; Asia-Pacific records the highest regional CAGR at 20.12% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wi-Fi Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging smartphone and smart-device penetration | +4.2% | Global, with highest impact in APAC emerging markets | Medium term (2-4 years) |

| Rapid rollout of public Wi-Fi in physical venues | +3.8% | Global, concentrated in urban centers and transport hubs | Short term (≤ 2 years) |

| Demand for real-time CX personalisation in retail and hospitality | +3.5% | North America and EU leading, expanding to Asia-Pacific | Medium term (2-4 years) |

| Integration of AI/ML engines with Wi-Fi analytics platforms | +4.1% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Adoption of Wi-Fi RTT for sub-meter indoor positioning | +2.9% | Enterprise-focused, primarily North America and EU | Long term (≥ 4 years) |

| Edge-based analytics on access points lowering TCO | +3.7% | Global, particularly relevant for cost-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Smartphone and Smart-Device Penetration

More than 21.1 billion Wi-Fi devices were active in 2024, with 576.2 million Wi-Fi 6E and 231.4 million Wi-Fi 7 units shipped during the year.[1]Kevin Robinson, “Wi-Fi Alliance: 2024 Market Update,” Wi-Fi Alliance, wi-fi.org Each connected user now carries multiple devices, enabling richer cross-session behavioral profiles. Enterprises that harness this density translate anonymous foot-traffic counts into layered customer-journey maps, improving conversion and dwell time. Retail chains that correlate device classes with in-store heatmaps allocate associates and promotions more precisely, raising basket size and reducing stock-outs. The trend strengthens predictive modeling accuracy as sample sizes grow, feeding AI that anticipates queue build-ups or product interest shifts minutes ahead of time.

Rapid Rollout of Public Wi-Fi in Physical Venues

Stadiums, airports, and malls moved Wi-Fi from cost center to revenue engine. Extreme Networks now supports analytics at 25 NFL stadiums, turning fan movement into real-time engagement cues.[2]Extreme Networks, “Delivering the NFL’s Wi-Fi,” Extreme Networks, extremenetworks.com TD Garden’s guest platform shows how seamless log-in increases opted-in first-party data capture. Transport hubs use dwell metrics to reshape concession placement, while quick-service restaurants upgrade access points to push queue-length alerts to managers. The emerging norm links splash-page consent with loyalty IDs, building persistent profiles that extend beyond venue walls into omnichannel marketing.

Demand for Real-Time Customer Experience Personalisation

Retailers merging Wi-Fi signals, cameras, and PoS data create dynamic store layouts. Fashion brand SAMSØE SAMSØE posted a 5.5% lift in men’s sales after deploying Cisco Meraki’s integrated analytics suite. Algorithms now adjust shelf assignments every few hours based on live heatmaps and historical purchase probabilities. Hospitality chains push room-upgrade offers when corridor sensors show idle housekeeping staff, boosting ancillary revenue. Such real-time orchestration shifts physical commerce from reactive service to proactive experience curation.

Integration of AI/ML Engines with Wi-Fi Analytics Platforms

Edge AI enables access points to label footpaths, flag anomalies, or predict equipment failures locally. Relay2’s Service Point embeds compute in Wi-Fi 7 hardware to deliver sub-second analytics without back-haul latency.[3]“Relay2 Introduces Service Point,” Wevolver, wevolver.comOrganizations gain GDPR-friendly insights since raw identifiers stay on-site. Machine-learning models retrain nightly on actual venue patterns, increasing accuracy over time and reducing manual calibration. The outcome is autonomous networks that self-heal and feed operations dashboards with predictive KPIs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent privacy regulations (GDPR, CCPA, etc.) | -2.8% | EU and California leading, expanding globally | Short term (≤ 2 years) |

| Persistent network-level security vulnerabilities | -1.9% | Global, with higher impact in enterprise environments | Medium term (2-4 years) |

| MAC-address randomisation impacting data accuracy | -2.1% | Global, with varying implementation rates by OS | Medium term (2-4 years) |

| Spectrum congestion in high-density locations | -1.7% | Urban centers and high-traffic venues globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Privacy Regulations (GDPR, CCPA, etc.)

Hefty fines push operators to overhaul consent flows, add data-protection officers, and run routine audits that can add 15-20% to deployment budgets. Firms such as Purple pivoted to explicit user accounts and granular consent logs that meet GDPR demands. Some venues now anonymize probe-request data at the chip level, trading individual paths for aggregated density maps. Vendors that bake privacy first in their design win bids as enterprises seek compliance assurance.

MAC-Address Randomization Impacting Data Accuracy

From iOS 14 and Android 10 onward, roughly one-third of devices rotate MAC addresses, weakening visitor-return metrics. Retailers respond by integrating guest Wi-Fi authentication with loyalty programs or by merging probabilistic matching with camera analytics. The shift accelerates the adoption of AI that clusters movement patterns independent of unique identifiers, guiding staffing and merchandising through crowd behavior rather than individual tracking.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum Through Managed Expertise

Solutions continued to dominate, holding 55.80% of the Wi-Fi analytics market share in 2025. However, services are outpacing at 20.95% CAGR, driven by demand for turnkey insight rather than do-it-yourself dashboards. Enterprises outsource analytics interpretation, privacy governance, and cross-system integration to specialists, lowering internal workloads while compressing time-to-value.

The Wi-Fi analytics market size for services is anticipated to more than double between 2026 and 2031 as vendors bundle consulting, managed operations, and outcome-based pricing. RetailNext’s fresh funding from Battery Ventures underscores investor belief that analytics-as-a-service will underpin future growth. Cloud4Wi’s Fogsense micro-device shows how service firms shrink hardware footprints and shift value upstream to business context.

By Deployment: Cloud Flexibility Underpins Scalable Roll-outs

Cloud platforms controlled 62.10% of the Wi-Fi analytics market share in 2025, and the segment is forecast to advance at a 21.35% CAGR. Subscription models eliminate capex and provide elastic storage plus AI updates on release day. Small and midsize retailers that once lacked internal IT staff now deploy within hours, unlocking network data that previously sat idle.

Edge compute addresses latency and data-sovereignty concerns; Cisco’s AI-native Wi-Fi 7 access points process telemetry locally while syncing summaries to the cloud.On-premise remains relevant in defense, healthcare, and financial institutions where sovereign hosting or legacy architectures persist.

By Application: Marketing Analytics Rises on Personalisation Demand

Presence analytics retained 52.85% revenue share in 2025 as venue operators depend on occupancy maps for staffing and safety. Marketing analytics, however, is the growth engine, expanding at 20.05% CAGR as brands connect in-store behavior to loyalty data and push personalised offers within seconds.

The Wi-Fi analytics market size attributed to marketing applications grow significnatly, reflecting retailers’ need to emulate e-commerce precision in physical aisles. Kaufland’s holiday traffic study used guest Wi-Fi logs to reorder staffing and promotions, lifting conversion post-event.

By End-User Vertical: Retail Overtakes on Data-Driven Transformation

Hospitality led with 31.60% share in 2025, using analytics to optimise guest journeys from check-in to conference room usage. Retail, climbing at 20.35% CAGR, is poised to overtake as chains integrate Wi-Fi insights with PoS and e-commerce data.

Gap Inc. implemented Juniper’s AI-native platform to fuel location-based campaigns, reporting higher footfall-to-purchase ratios. In healthcare, Belgium’s UZ Leuven applied analytics to asset tracking, freeing staff time for patient care. Sports arenas leverage dwell metrics to reroute concessions, boosting per-capita spend.

Geography Analysis

North America accounted for 30.85% of global revenue in 2025, driven by early enterprise adoption and mature regulatory balance between privacy and analytics. Flagship examples include Extreme Networks’ deployments across 25 NFL stadiums that demonstrate best practices in high-density Wi-Fi. High smartphone penetration and robust cloud infrastructure sustain continuous platform upgrades.

Asia-Pacific is the fastest expanding region, growing at a 20.12% CAGR through 2031. China hosts about 4,000 private wireless factories that lay groundwork for granular analytics, while India’s prospective 6 GHz allocation could unlock USD 4,030 billion in economic value by 2034. Rapid urbanisation and government digital-in-public policies spur deployments across transport hubs, malls, and smart campuses.

Europe presents a privacy-led model where GDPR dictates platform design. Operators that secure user consent and anonymise data gain first-mover advantage. Germany leads with large retail chains linking guest Wi-Fi to loyalty programs under strict compliance, and the United Kingdom’s public Wi-Fi initiatives in rail stations illustrate high-traffic analytics at national scale. Edge-enabled deployments lower cloud egress costs and align with the region’s sustainability targets.

Regulatory Landscape

Wi-Fi analytics deployments operate under tightening privacy and location-data controls because identifiers derived from Wi-Fi signals (for example, MAC addresses and inferred geolocation) are treated as personal data under GDPR and, in the United States, can fall under FCC customer privacy constructs such as CPNI principles. In Europe, regulators and data-protection bodies have reinforced consent-first collection, data-minimization, and DPIA-style risk assessment practices for tracking technologies in physical venues, pushing vendors toward explicit opt-in flows via captive portals and stronger anonymization of probe and association data.

In 2026, compliance pressure increased on two fronts relevant to Wi-Fi analytics. In the United States, the Supreme Court upheld the FCCs authority to issue fines for mishandling customer location data under Section 222, elevating enforcement risk for location-derived datasets. In the EU, the AI Act timeline adds another governance layer for analytics stacks that incorporate AI models for behavior inference, and related 2026 regulatory opinions signaled heightened scrutiny of data use in digital networks. That has accelerated privacy-by-design implementations such as edge processing and rotating hashed identifiers to limit exposure of raw identifiers.

Competitive Landscape

Competition is moderately fragmented but trending toward converged platform providers that merge hardware, software, and analytics services. Legacy networking giants such as Cisco and HPE/Aruba fortify portfolios with AI and edge compute, while specialist firms like Purple and Cloud4Wi carve niches in retail and hospitality. Emerging vendors embed analytics directly into Wi-Fi 7 radios, shortening data-to-insight cycles.

Service-centric revenue models dominate recent bids. Cloud4Wi became a 2025 Cisco Meraki Strategic Technology Partner, indicating tighter coupling between infrastructure and value-added analytics. Boldyn Networks’ acquisition of Apogee expands managed Wi-Fi for higher education, recognising that many universities prefer OPEX engagements over on-premise builds. White-space opportunities include privacy-first analytics engines, AI-optimised spectrum management, and vertical-specific dashboards.

Vendors differentiate on three axes: accuracy of indoor positioning, depth of AI insight, and simplicity of multi-site roll-out. Integrations with CRM and marketing platforms become decisive as physical-digital convergence accelerates. As consolidation continues, leaders with large device ecosystems and channel presence are positioned to absorb niche analytics startups.

Wi-Fi Analytics Industry Leaders

Cisco Systems Inc.

Cloud4Wi Inc.

Purple WiFi Ltd

RetailNext Inc.

Yelp WiFi Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most immediate whitespace sits at the intersection of accuracy, privacy compliance, and ease of authentication in high-traffic venues where MAC randomization reduces repeat-visitor fidelity. Vendors are moving beyond passive tracking toward consented engagement and identity-based access, using captive portals, loyalty linkage, and network access control to replace shared passwords and improve auditability of user consent. Cloud-led deployments (62.10% share in 2025) combined with edge anonymization also open opportunities with data-sovereignty and GDPR-driven buyers that want aggregated insights without exporting raw identifiers, consistent with deployments that keep sensitive processing on-site.

Standards progression expands the addressable use cases beyond classical footfall and dwell dashboards. IEEE 802.11bf (finalized in March 2025) supports WLAN sensing for presence and motion recognition, creating new commercial pathways in facilities operations and safety-oriented analytics that do not rely solely on persistent device identifiers. On the connectivity side, wider 6 GHz availability in the United States supports denser Wi-Fi 6E and 7 deployments that can capture richer telemetry and enable higher-resolution analytics in stadiums, airports, and retail, where operators already treat access points as data-collection assets rather than basic connectivity tools.

Recent Industry Developments

- July 2026: Cloud4Wi announced general availability of its AI-Powered Cloud NAC, positioning network access control as an extension of guest Wi-Fi and analytics rather than a separate security layer. By shifting from shared passwords to identity-based access, the launch supports cleaner consent capture and more reliable session continuity for analytics in multi-site enterprises.

- January 2025: RetailNext launched Traffic 3.0 to expand its in-store behavior analytics capabilities for physical retailers. The update strengthens RetailNexts platform posture as retailers combine presence analytics with marketing and operations workflows to improve conversions and staffing decisions.

- May 2024: RetailNext partnered with pass_by to integrate internal store data with external geospatial insights for performance forecasting. The integration broadens the data inputs available to Wi-Fi and location analytics users, supporting more contextual decisioning beyond venue-only signals.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the wi-fi analytics market covers software and related services that turn wi-fi network signals into usable insights, such as visitor presence, dwell time, repeat visits, and engagement reporting for enterprises and venues.

Scope exclusions: Excludes core wi-fi access hardware sales, general network installation, and telecom connectivity services when they are not sold as part of analytics delivery.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment

- On-premise

- Cloud

- By Application

- Presence Analytics

- Marketing Analytics

- By End-user Vertical

- Retail

- Hospitality

- Sports and Leisure

- Transportation

- Healthcare

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the boundaries of what counts as wi-fi analytics and to collect anchor data points that can be checked across regions. We referred to public sources such as FCC releases and spectrum updates, US Census retail and services activity, Eurostat digital economy indicators, ITU connectivity statistics, and OECD ICT data to understand adoption direction and venue density.

To translate those signals into market math, we also reviewed company annual reports, earnings call decks, product documentation on public websites, and reputable press coverage of guest wi-fi, location analytics, and privacy rules. In a few places, paid subscriptions were used for company financials and intelligence, patent databases, and news and financials so we could verify product positioning and revenue mix assumptions. This desk list is illustrative only, and many other sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating how buyers actually purchase wi-fi analytics (subscription versus license), how deployments scale by venue type, and where pricing tends to move when features such as real-time dashboards and privacy controls are included. We spoke with a mix of solution providers, channel partners, and enterprise users across the Americas, EMEA, and APAC so regional differences in venue density and compliance practice could be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 43% |

| Mid tier: 55% | Functional/Unit leaders: 37% | EMEA: 35% |

| Smaller Players: 17% | Managers: 48% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where venue and enterprise demand pools are reconstructed using counts of active sites, guest wi-fi penetration in target verticals, and typical attach rates of analytics modules to managed wi-fi deployments. Once the demand pool is formed, it is converted to value using a mix of subscription pricing, service attach, and renewal assumptions that are adjusted by region and buyer size.

To keep the totals realistic, we corroborate the result with selective bottom-up approximations, such as sampled price points across use cases (presence and marketing), partner channel checks on deal sizes, and roll-ups from a limited set of suppliers where revenue splits are disclosed. Inputs that matter most include the pace of cloud migration for network management, the number of high footfall venues adding guest wi-fi, average contract duration, analytics feature bundling rates, and regulatory pressure on consent and data retention, which can slow rollout timelines.

Forecasting is done using scenario analysis supported by trend lines on connected device growth, enterprise networking spend direction, and expected ASP movement as more functionality is bundled into platform subscriptions. When a bottom-up check cannot be completed for a smaller geography or niche venue type, we apply proxy ratios from similar markets and then re-test the output with interview feedback before finalizing.

Data Validation & Update Cycle

Outputs are checked in several steps so we can spot break points early, such as unrealistically high spend per venue or sudden jumps that do not match deployment cycles. Analysts compare results against independent signals like cloud managed wi-fi adoption, venue footprint trends in retail and hospitality, and reported software and services growth patterns, and then review variances before sign-off.

The model and assumptions go through peer review, and follow-up calls are triggered when a key input moves sharply, such as pricing resets, major privacy enforcement changes, or demand shocks in travel and retail. Reports are refreshed annually, and interim updates are made when material events occur. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Wi Fi Analytics Market Sizing Compared With Other Published Estimates

Published market values for wi-fi analytics can differ a lot because studies do not always count the same revenue lines, and the timing of base year updates can vary across publishers. We also see differences when one estimate leans more on broad IT spend proxies, while another builds the market from venue level adoption and subscription pricing.

By tracking venue footprint by vertical and refreshing cloud subscription ASP assumptions each cycle, Mordor Intelligence keeps the total tied to solutions and services that are directly sold as wi-fi analytics, rather than folding in general WLAN management or access hardware revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.12 B (2025) | |

| Global Consultancy A | USD 8.06 B (2024) | Uses an earlier value year and its scope discussion emphasizes analytics-as-a-service and broader end-use buckets, which can pull in adjacent location and engagement software that is not always tied to wi-fi network data. |

| Industry Research Group B | USD 8.13 B (2024) | Starts from a 2024 base and includes an expanded application list, which may count advertising analytics and smart infrastructure programs more widely even when wi-fi is not the primary data collection layer. |

Taken together, the spread is mainly explained by base year choice and how strictly analytics revenue is separated from adjacent networking and location software. Our approach stays repeatable because each step can be traced back to venue adoption, deployment mix, and pricing logic, and then checked again through interviews before the totals are finalized.

Key Questions Answered in the Report

What is the current size of the Wi-Fi analytics market?

The Wi-Fi analytics market generated USD 7.32 billion in 2026 and is projected to reach USD 17.98 billion by 2031.

Which deployment model leads the Wi-Fi analytics market in 2026?

Cloud deployment holds 62.10% of global revenue and is forecast to grow at a 21.35% CAGR through 2031.

Why is retail the fastest-growing vertical for Wi-Fi analytics?

Retailers use location data to personalise in-store experiences and compete with e-commerce, driving a 20.35% CAGR from 2026 to 2031.

How do privacy regulations affect Wi-Fi analytics adoption?

GDPR and CCPA add compliance costs, but platforms that embed consent management gain a competitive edge.

Page last updated on: