Wireless Asset Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.99 Billion |

| Market Size (2031) | USD 42.88 Billion |

| Growth Rate (2026 - 2031) | 12.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wireless Asset Management Market Analysis by Mordor Intelligence

Wireless asset management market size in 2026 is estimated at USD 23.99 billion, growing from 2025 value of USD 21.36 billion with 2031 projections showing USD 42.88 billion, growing at 12.33% CAGR over 2026-2031. A shift from reactive tracking to predictive orchestration is underway as sub-USD 0.05 RFID tags, private 5G networks, and end-to-end compliance rules converge. Enterprises view real-time visibility as a working-capital lever that compresses safety stock, extends asset life, and cuts downtime. Hardware remains the installed-base backbone, yet shrinking device margins push suppliers toward software and services that monetize analytics and managed security. Cellular IoT modules paired with low-power firmware widen coverage beyond fixed chokepoints, while ESG commitments spur sensor deployment on consumables previously deemed too cheap to track. Competitive intensity is rising as industrial-automation majors, telecom carriers, and RFID specialists bundle connectivity and analytics into subscription offerings.

Key Report Takeaways

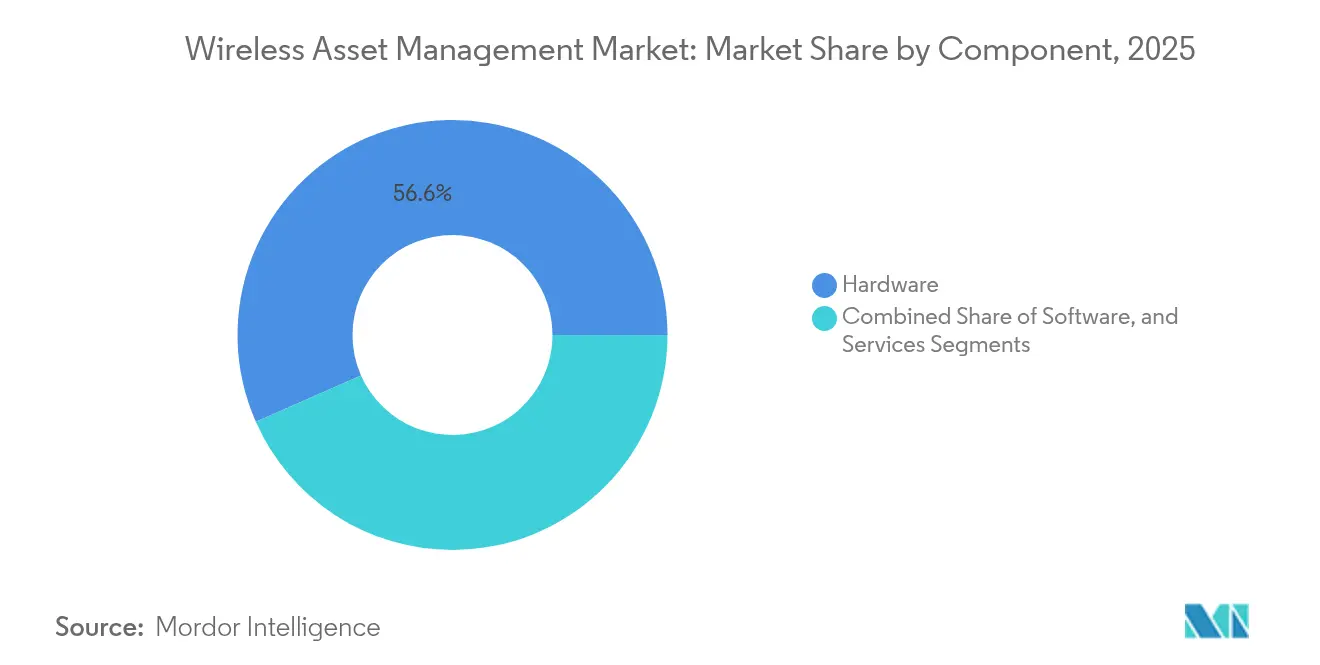

- By component, hardware commanded 56.62% revenue in 2025, while services are set to expand at a 13.78% CAGR through 2031.

- By connectivity, RFID captured 36.25% of the wireless asset management market share in 2025, whereas cellular IoT is poised to grow at a 15.05% CAGR to 2031.

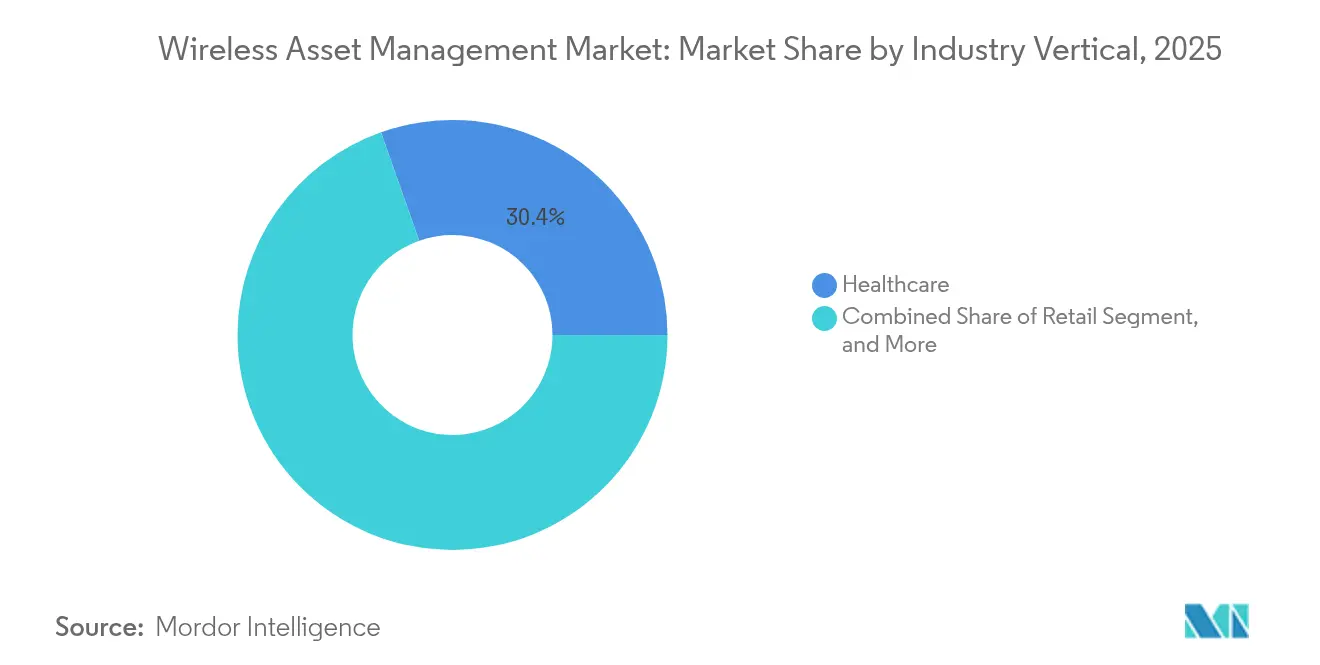

- By vertical, healthcare secured 30.40% revenue in 2025; retail is forecast to post the fastest 15.44% CAGR to 2031.

- By asset category, mobile equipment held 41.85% share of the wireless asset management market size in 2025, and consumables are projected to advance at 14.62% CAGR to 2031.

- By application, physical asset monitoring accounted for 36.74% revenue in 2025; predictive maintenance is expected to grow at a 14.97% CAGR through 2031.

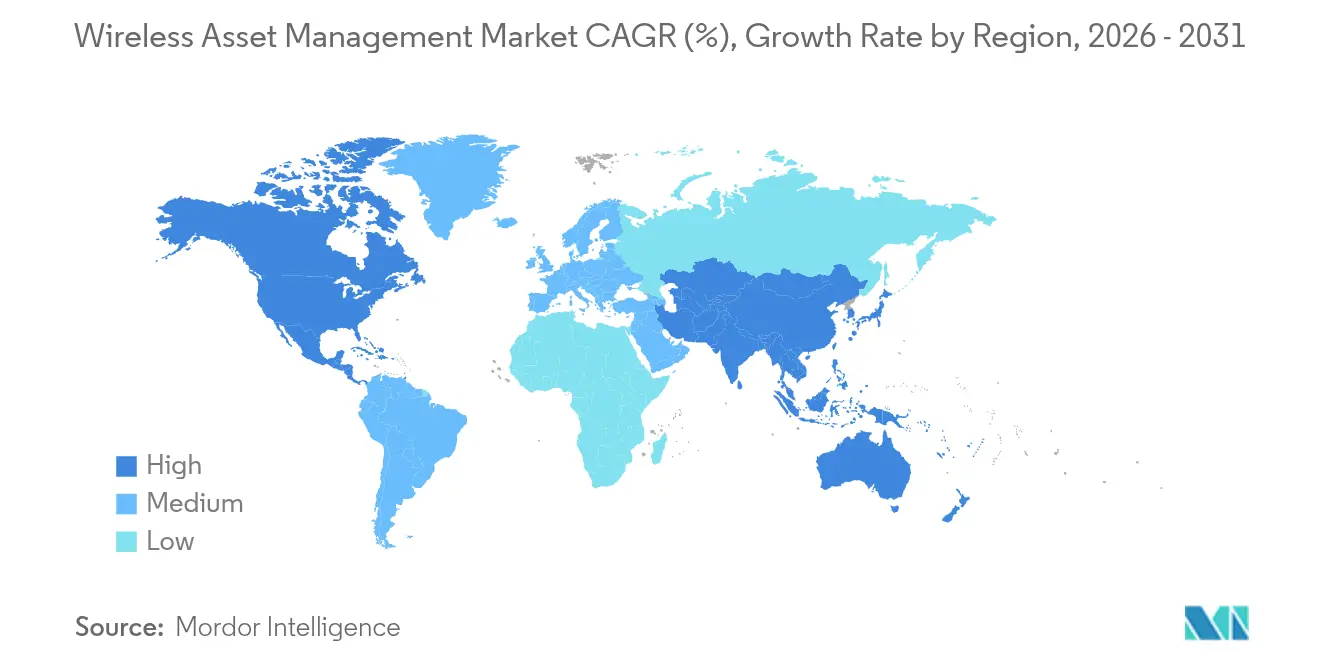

- By geography, North America led with 40.32% revenue in 2025, and Asia Pacific is the fastest climber at 14.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wireless Asset Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in IoT-enabled real-time locating solutions | +2.8% | North America, Western Europe | Medium term (2-4 years) |

| Declining cost of wireless sensors and tags | +2.1% | Global, fastest in Asia Pacific | Short term (≤ 2 years) |

| Strict regulatory mandates for healthcare traceability | +1.9% | North America, Europe, spillover to MEA and LATAM | Long term (≥ 4 years) |

| Expansion of Industry 4.0 predictive maintenance | +2.3% | China, Japan, South Korea, Central Europe | Medium term (2-4 years) |

| Integration of 5G private networks | +1.7% | North America, Europe, select APAC hubs | Long term (≥ 4 years) |

| Rising ESG pressure for utilization gains | +1.4% | Europe leading, global uptake | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in IoT-Enabled Real-Time Locating Solutions

Real-time locating systems (RTLS) now underpin warehouse orchestration, hospital workflows, and airport ground operations. Bluetooth Low Energy and ultra-wideband deliver sub-meter accuracy, allowing automated guided vehicles to operate safely among personnel. Hospitals report 40% cuts in equipment search time after tagging wheelchairs and infusion pumps, freeing staff for clinical tasks.[1]Zebra Technologies, “MotionWorks RTLS Benefits,” zebra.com Manufacturers integrate RTLS feeds into enterprise resource planning software, so work-in-progress data updates inventory ledgers without manual input. Airlines test RTLS on baggage carts to shave gate-turnaround minutes that cost USD 50-100 each. The resulting productivity gains cement RTLS as a default layer in the wireless asset management market.

Declining Cost of Wireless Sensors and Tags

Passive RFID tags slipped below USD 0.05 at volume as chip lithography and roll-to-roll printing matured. Battery-assisted tags for cold-chain drugs now sell for USD 2-3, down from USD 8-10 in 2020, broadening adoption among regional distributors. Bluetooth beacons priced at USD 10-15 spur construction firms to tag tools that roam across sites, trimming theft losses. Such price compression unlocks deployments in municipal services, agriculture, and small logistics operators traditionally priced out of sensor automation. Cost curves therefore accelerate volume, which in turn drives further cost declines, reinforcing the growth loop within the wireless asset management market.

Strict Regulatory Mandates for Healthcare Traceability

The FDA’s unique device identification (UDI) rule obliges manufacturers to encode implants and surgical tools with machine-readable IDs, creating a cradle-to-patient audit trail. Europe’s Medical Device Regulation 2017/745 extends similar obligations across Class II and III devices. Hospitals replace barcode scanners with RFID portals that read dozens of items simultaneously, slashing audit time from hours to minutes. Parallel drug-serialization laws such as the U.S. Drug Supply Chain Security Act push pharmacies to adopt unit-level wireless tracking. Japan implemented analogous serialization in 2024, accelerating RTLS uptake in Asia Pacific healthcare. Regulatory momentum therefore anchors the wireless asset management market in a needs-not-wants category for hospitals and suppliers.

Expansion of Industry 4.0 Predictive Maintenance

Manufacturers embed vibration, thermal, and acoustic sensors into machinery to detect anomalies before failure. Automotive plants achieved 25-35% downtime reduction after condition-monitoring rollouts, improving overall equipment effectiveness. Private 5G backbones deliver millisecond latency, pushing inference workloads to factory edges without cloud delay. Chemical and food processors extend wireless monitoring to pumps and conveyors, protecting batch integrity and customer commitments. As predictive algorithms mature, maintenance teams shift from calendar-based routines to data-driven scheduling, locking in service savings while lifting asset longevity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX for enterprise deployments | -1.6% | Small and mid-size enterprises worldwide | Short term (≤ 2 years) |

| Interoperability gaps across multi-vendor platforms | -1.2% | Firms with legacy IT in North America and Europe | Medium term (2-4 years) |

| Cybersecurity vulnerabilities | -0.9% | Regulated sectors globally | Long term (≥ 4 years) |

| Limited battery life in harsh environments | -0.7% | Oil and gas, mining, cold-chain operations in MEA and remote APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for Enterprise-Wide Deployments

Full-site rollouts require readers, gateways, middleware, and integration labor often exceeding USD 500,000 for a mid-size company. Hospitals face USD 100-200 per bed in RTLS infrastructure plus annual license fees, stretching capital budgets. Small logistics providers opt for partial coverage, protecting only high-value zones. Subscription pricing and leasing models lower entry barriers but raise concerns about long-term costs and vendor lock-in. Thin-margin sectors such as retail and agriculture therefore pace deployments cautiously, tempering near-term growth in the wireless asset management market.

Interoperability Gaps Across Multi-Vendor Platforms

Proprietary data schemas force IT teams to build custom middleware to reconcile RFID, Bluetooth, GPS, and LPWAN inputs. Lack of universal over-the-air update standards delays security patches across heterogeneous fleets. Industry groups like IEEE and GS1 push interoperability frameworks, yet vendor adoption is uneven. Enterprises thus weigh the convenience of bundled suites against the risk of future integration headaches, prolonging decision cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Scale as Integration Complexity Rises

Services revenue is forecast to grow 13.78% annually through 2031 as enterprises outsource deployment, cybersecurity, and performance tuning. Hardware delivered 56.62% of 2025 turnover, but commoditization drives device margins toward cost plus. Software platforms integrate data from readers, beacons, and cellular modules, feeding predictive analytics that unlock maintenance savings and asset-sharing models. The wireless asset management market rewards vendors that position services as glue across heterogeneous estates. Zebra extended its MotionWorks suite in 2024 to add maintenance-prediction modules, demonstrating the pivot toward recurring subscriptions. Systems integrators with vertical know-how clinical workflows, warehouse slotting logic, or food-safety compliance capture premium bill rates as clients seek domain-specific outcomes over generic dashboards. Cybersecurity burdens also tilt demand toward managed services that deliver continuous threat monitoring and firmware patching.

Software and services now shape buying criteria more than tag read range or antenna gain. Enterprises treat readers and gateways as interchangeable building blocks so long as uptime and API compatibility meet expectations. Consequently, market leaders emphasize open SDKs and cloud connectors that speed time-to-value. Over the forecast horizon, services will absorb incremental share even as device volumes soar, reshaping revenue mixes across the wireless asset management market.

By Connectivity Technology: Cellular IoT Rises with Private-5G Momentum

Cellular IoT, covering LTE-M, NB-IoT, and 5G, should post a 15.05% CAGR as operators bundle modules with private-network contracts. RFID retained 36.25% revenue in 2025, thanks to retail item-level tagging and healthcare device traceability. Yet RFID relies on physical portals, limiting reach to controlled chokepoints. Cellular modules, aided by power-saving modes and falling chip costs, push beyond four-wall boundaries into yards, railcars, and remote fields. Verizon and AT&T launched private-5G campuses that integrate asset trackers and edge gateways into one managed contract, reducing integration friction.

Bluetooth Low Energy and ultra-wideband excel in indoor positioning where sub-meter accuracy enables safe robot navigation. GPS remains staple for over-the-road fleets, though urban canyon effects persist. LPWAN protocols like LoRaWAN serve agriculture and utilities where low data throughput suffices. Hybrid tags dynamically select Bluetooth indoors, cellular on highways, and RFID at dock doors, optimizing battery life and coverage. As enterprises accept multi-radio design as standard, the wireless asset management market size for cellular IoT climbs in tandem with private-network rollouts.

By Asset Category: Consumables Accelerate as Circular Mandates Tighten

Mobile equipment, from forklifts to hospital beds, accounted for 41.85% revenue in 2025. Consumables, however, are projected to rise 14.62% annually as regulators and investors demand reuse tracking. Returnable packaging, surgical kits, and calibrated tools now carry durable RFID or BLE tags that survive sterilization and outdoor cycles. Europe’s revised Packaging and Packaging Waste Regulation mandates traceability for reusable transport items, forcing brand owners to retrofit crates and pallets. Fixed equipment such as HVAC units and generators adopt condition sensors, but retrofitting older assets slows penetration.

The wireless asset management market thus expands beyond high-value forklifts into once-disposable items, increasing tag volumes exponentially. Battery-assisted labels with multi-year life and temperature logging broaden coverage to cold-chain pharmaceuticals and fresh food. As reuse proof becomes a license to sell in ESG-sensitive sectors, consumable tracking will outpace mobile-equipment growth through 2031.

By Industry Vertical: Retail Sprints Ahead on Item-Level RFID

Healthcare held 30.40% of 2025 spending, propelled by UDI and sterilization compliance. Retail, however, is expected to grow 15.44% annually as chains extend RFID from apparel to grocery, pharmacy, and home-goods aisles. Walmart’s 2024 supplier mandate catalyzed upstream tagging at source, removing cost burdens from stores while standardizing data feed. Omnichannel fulfillment depends on 98-plus % inventory accuracy that item-level RFID delivers.

Manufacturing embraces work-in-progress tracking and predictive maintenance under Industry 4.0 roadmaps. Logistics operators fit GPS and cellular beacons on trailers and containers, monetizing shipment visibility. Oil and gas deploy rugged sensors on wellheads and offshore platforms to curb inspection costs. Collectively, these sectors diversify revenue streams, but retail’s volume surge cements its position as the fastest-growing segment in the wireless asset management market.

By Application: Predictive Maintenance Outpaces Location Tracking

Physical asset monitoring produced 36.74% revenue in 2025, covering basic location, environmental, and utilization metrics. Predictive maintenance, though smaller today, is forecast to expand 14.97% annually as downtime costs spike. Automotive lines lose USD 20,000–30,000 per minute of stoppage, making sensors and analytics cheap insurance.

Edge AI running on factory gateways detects bearing wear and lubrication shortfalls weeks early, scheduling repairs during planned breaks. Inventory-control automation leverages RFID to hit 95–99% accuracy, supporting same-day delivery promises. Loss prevention applications flag unauthorized movements of high-value pharmaceuticals and electronics. Over time, maintenance analytics will absorb more budget, differentiating suppliers that fuse condition data with enterprise asset-management workflows.

Geography Analysis

North America held 40.32% share in 2025, buoyed by mature logistics, early healthcare digitization, and a dense ecosystem of automation vendors. FDA device-traceability and the Drug Supply Chain Security Act create mandatory demand, while private-5G pilots in automotive, ports, and distribution centers set precedent for nationwide rollouts. Canada’s mining and energy sectors deploy rugged GPS and satellite trackers for remote-site assets, whereas Mexico’s export-oriented factories embed RFID in maquiladora supply chains. Interoperability challenges between new sensors and legacy ERP systems channel spend toward systems integrators versed in warehouse and healthcare IT.

Asia Pacific is projected to grow 14.55% annually, propelled by China’s subsidies for intelligent manufacturing and India’s smart-city vehicle-tracking mandates. China targets 70% predictive-maintenance adoption among large manufacturers by 2027, guaranteeing a captive sensor market. India’s Unified Logistics Interface Platform requires GPS on commercial vehicles, accelerating cellular IoT uptake. Japan’s labor shortages incentivize RTLS in hospitals and factories to offset staff gaps. South Korea’s semiconductor fabs monitor cleanroom equipment for contamination risk, while Australia’s mining hauls depend on satellite trackers. Diverse regulatory and infrastructure landscapes yield country-specific adoption curves, but aggregate growth positions Asia Pacific as the fastest-expanding region in the wireless asset management market.

Europe combines strict regulations with spectrum fragmentation. EU Medical Device and packaging-waste directives compel traceability, yet patchy LPWAN allocations complicate cross-border deployments. Germany’s automotive plants integrate Siemens asset-tracking suites with 5G shop-floors, whereas the U.K. National Health Service trials RTLS to slash equipment-search labor. France and Italy deploy RFID to authenticate luxury goods and combat counterfeits. Russia’s energy operators track pipelines despite sanctions limiting Western hardware access, turning to local suppliers. Middle East and Africa show nascency but rising potential as Saudi Vision 2030 and U.A.E. smart-city agendas earmark funds for logistics automation.

Competitive Landscape

The wireless asset management market remains moderately fragmented. Zebra Technologies, Honeywell, and Siemens leverage installed barcode, scanning, and control platforms to upsell wireless tracking. Impinj and SATO specialize in RFID chips and labels where unit-economics and intellectual-property depth create entry barriers. Cisco and Verizon push private-5G bundles, promising carrier-grade uptime and secure slicing.[3]Cisco Systems, “Ultra-Wideband RTLS Integration,” cisco.com Strategy themes hinge on vertical specialization, with vendors tailoring solutions for healthcare, retail, or heavy industry workflows.

Hardware commoditization compresses tag and reader margins, prompting players to differentiate through software analytics and managed services. Startups build cloud-native platforms that ingest data from any tag, eroding hardware lock-in. Patent races in ultra-wideband positioning, energy harvesting, and blockchain provenance hint at temporary moats, but rapid standardization diminishes lifespan of proprietary edges. Customers increasingly ask for ISO 27001 compliance and open APIs, rewarding suppliers that embrace ecosystem participation over walled gardens.

White-space opportunities persist in harsh environments. Honeywell’s 5-year cold-chain tag investment illustrates bets on battery-assisted labels for pharma distribution. Trimble’s satellite-cellular tracker targets equipment where cellular fades. Vendors that solve battery life, ingress protection, and temperature tolerances capture premium niches beyond warehouse walls. Overall, competitive intensity will sharpen as services and software overtake hardware in revenue contribution across the wireless asset management market.

Wireless Asset Management Industry Leaders

Cisco Systems Inc.

Siemens AG

Zebra Technologies Corporation

Honeywell International Inc.

Trimble Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Zebra Technologies unveiled a USD 150 million RFID factory in Malaysia to double tag capacity to 10 billion units yearly.

- September 2025: Impinj integrated its RAIN RFID platform with AWS IoT Core, enabling direct cloud streaming of tag events.

- August 2025: Honeywell bought a minority stake in a battery-assisted cold-chain tag startup to lengthen operational life to 5 years.

- July 2025: Siemens launched a bundled private-5G asset-tracking offer for automotive and machinery manufacturers.

Global Wireless Asset Management Market Report Scope

Wireless asset management provides a solution that is used to monitor and manage assets in the form of equipment, tools using wireless technology. Asset management is crucial for every organization, to improve its efficiency, wireless asset management alerts for examining equipment. This system helps in connecting various devices and monitors to customize the workflow, with the help of a real-time location system to track static assets, where wireless access can build a platform, benefiting various industries. Wireless asset management market refers to hardware + software solutions that track, monitor, and manage physical assets using wireless communication technologies, including:

The Wireless Asset Management Market Report is Segmented by Component (Hardware, Software, and Services), Connectivity Technology (RFID, Bluetooth Low Energy, Wi-Fi, Cellular IoT, GPS/GNSS, and LPWAN), Asset Category (Mobile Equipment, Fixed Equipment, Consumables, Returnable Transport Assets, Other Asset Category), Industry Vertical (Manufacturing, Healthcare, Logistics and Transportation, Oil and Gas, Retail, Other Industry Vertical), Application (Physical Asset Monitoring, Inventory Control Automation, Predictive Maintenance Management, Loss Prevention, Other Application), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| RFID |

| Bluetooth Low Energy |

| Wi-Fi |

| Cellular IoT (LTE-M, NB-IoT, 5G) |

| GPS / GNSS |

| LPWAN (LoRa, Sigfox etc.) |

| Mobile Equipment |

| Fixed Equipment |

| Consumables |

| Returnable Transport Assets |

| Other Asset Category |

| Manufacturing |

| Healthcare |

| Logistics and Transportation |

| Oil and Gas |

| Retail |

| Other Industry Vertical |

| Physical Asset Monitoring |

| Inventory Control Automation |

| Predictive Maintenance Management |

| Loss Prevention |

| Other Application |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Connectivity Technology | RFID | ||

| Bluetooth Low Energy | |||

| Wi-Fi | |||

| Cellular IoT (LTE-M, NB-IoT, 5G) | |||

| GPS / GNSS | |||

| LPWAN (LoRa, Sigfox etc.) | |||

| By Asset Category | Mobile Equipment | ||

| Fixed Equipment | |||

| Consumables | |||

| Returnable Transport Assets | |||

| Other Asset Category | |||

| By Industry Vertical | Manufacturing | ||

| Healthcare | |||

| Logistics and Transportation | |||

| Oil and Gas | |||

| Retail | |||

| Other Industry Vertical | |||

| By Application | Physical Asset Monitoring | ||

| Inventory Control Automation | |||

| Predictive Maintenance Management | |||

| Loss Prevention | |||

| Other Application | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 valuation of the wireless asset management market?

The market is valued at USD 23.99 billion in 2026.

How fast is the market expected to grow through 2031?

It is projected to register a 12.33% CAGR, reaching USD 42.88 billion by 2031.

Which industry vertical will expand the quickest?

Retail is forecast to post the fastest 15.44% CAGR as chains broaden item-level RFID.

Why are services revenue growing faster than hardware?

Integration complexity and continuous cybersecurity needs drive enterprises toward managed services projected to grow 13.78% annually.

Which region will add the most incremental revenue?

Asia Pacific, supported by intelligent manufacturing subsidies and smart-city mandates, is set for a 14.55% CAGR.

What technical challenge limits adoption in harsh environments?

Battery longevity remains a restraint, as extreme conditions shorten tag life and elevate maintenance costs.

Page last updated on: