Rabies Diagnostics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.11 Billion |

| Market Size (2030) | USD 2.68 Billion |

| Growth Rate (2025 - 2030) | 4.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rabies Diagnostics Market Analysis by Mordor Intelligence

The rabies diagnostics market size reached USD 2.11 billion in 2025 and is projected to advance to USD 2.68 billion by 2030 at a 4.92% CAGR, reflecting the combined effect of WHO’s “Zero by 2030” target, rising investment in surveillance, and rapid penetration of molecular and point-of-care technologies.[1]World Health Organization, “Rabies,” WHO.INT Demand is concentrated in Asia and Africa, where 95% of rabies deaths occur, yet North America still holds a dominant share thanks to its long-standing wildlife surveillance systems and supportive regulations. Diagnostic preferences are shifting from the Fluorescent Antibody Test (FAT) toward PCR-based assays as laboratories seek higher sensitivity, while portable lateral-flow devices and smartphone-linked platforms bring accurate testing to rural clinics. Funding from Gavi and national One-Health programs is expanding sample-collection networks and reference-lab capacity, further supporting the rabies diagnostics market. Competitive intensity remains moderate, with multinational suppliers leveraging global distribution while start-ups focus on low-cost isothermal or CRISPR-based detection kits that work without cold chains.

Key Report Takeaways

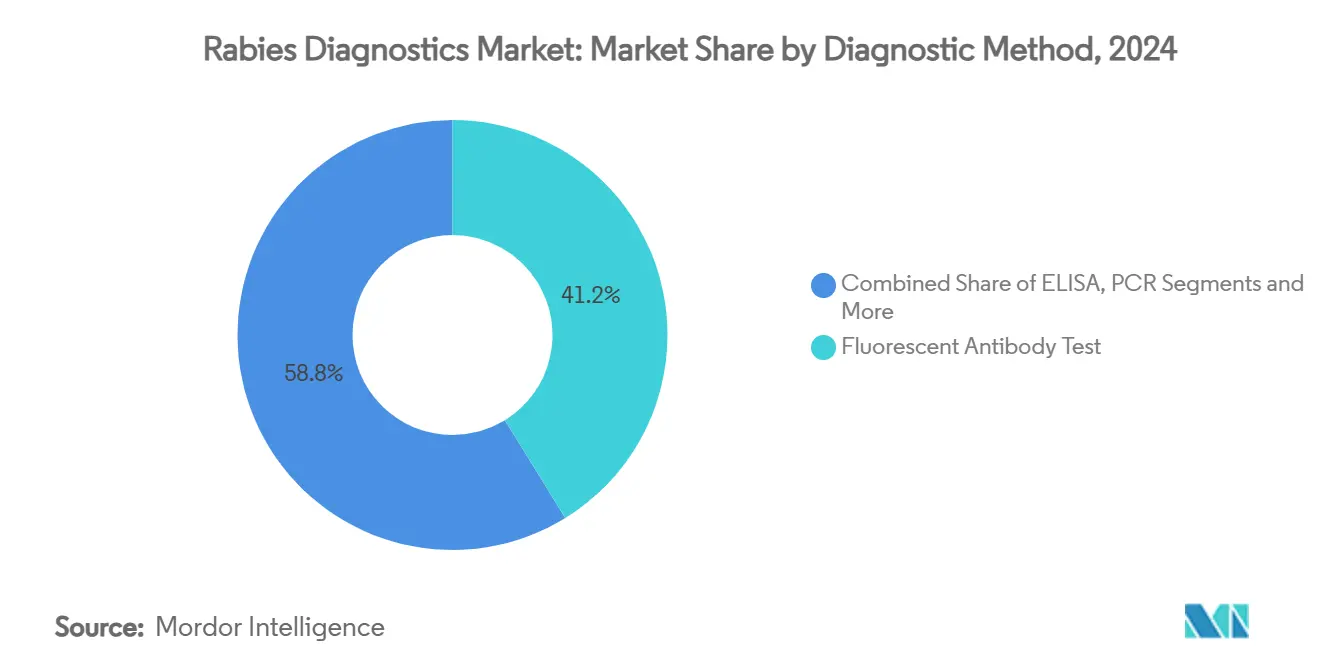

- By diagnostic method, the Fluorescent Antibody Test led with 41.21% rabies diagnostics market share in 2024, while PCR/RT-PCR is poised to grow at an 8.23% CAGR through 2030.

- By technology, immunodiagnostics accounted for 53.43% of the rabies diagnostics market size in 2024, whereas molecular diagnostics will expand at an 8.68% CAGR to 2030.

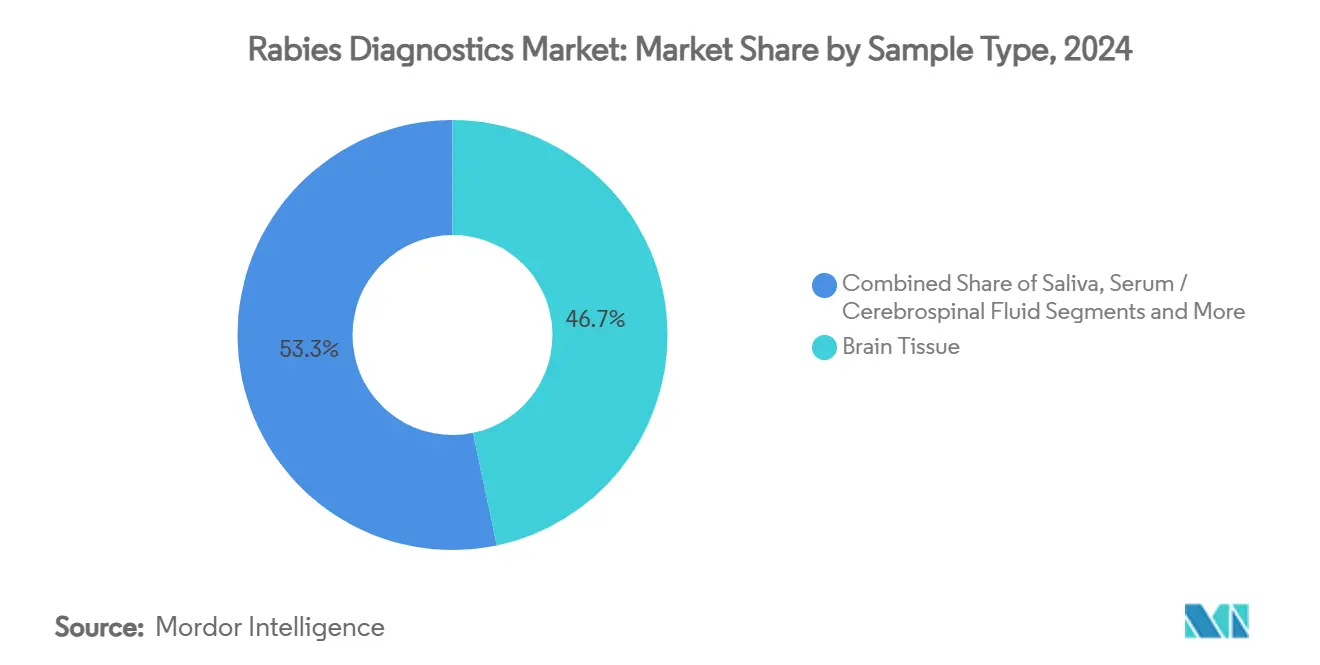

- By sample type, brain tissue captured 46.71% of the rabies diagnostics market in 2024; saliva testing is forecast to advance at a 6.37% CAGR during the same horizon.

- By end user, reference laboratories held 44.32% share of the rabies diagnostics market in 2024, but point-of-care and veterinary clinics record the highest projected CAGR at 7.25% through 2030.

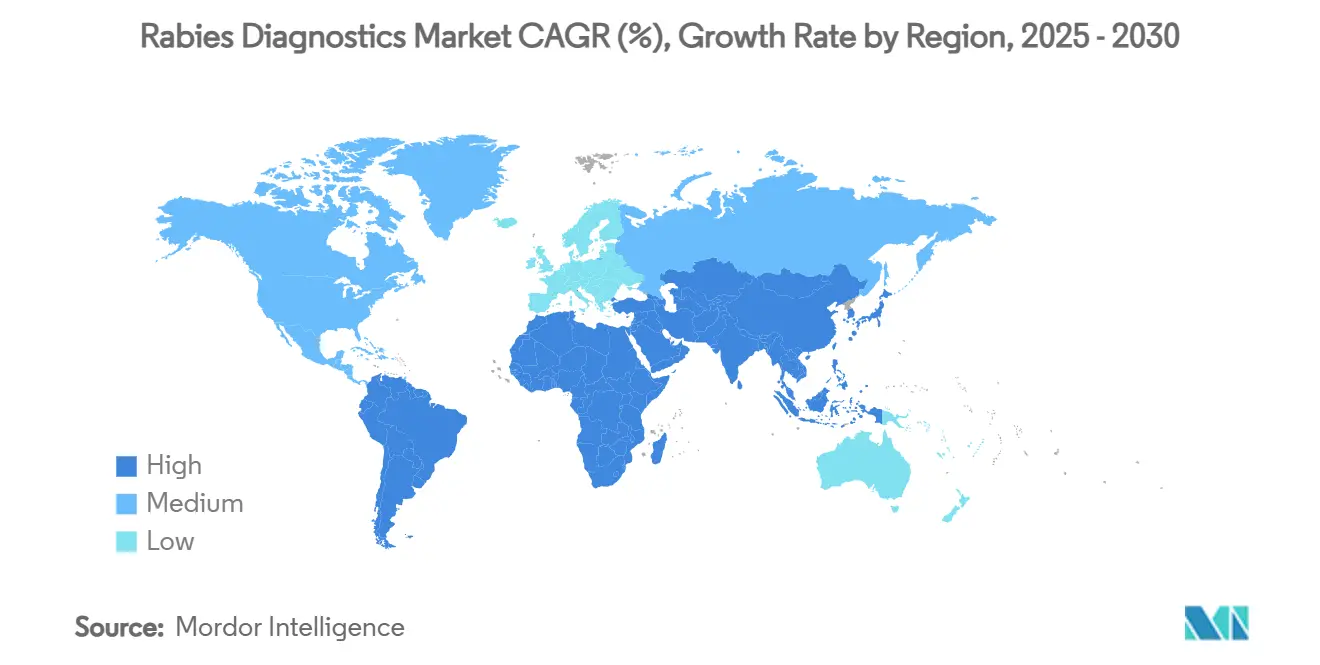

- By geography, North America commanded 33.38% of revenue in 2024, whereas Asia-Pacific is expected to post the fastest 6.18% CAGR by 2030.

Global Rabies Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of point-of-care rapid rabies tests in endemic areas | +1.2% | Asia-Pacific, Africa, spill-over Latin America | Medium term (2-4 years) |

| “Zero by 2030” elimination initiatives boosting surveillance funding | +0.9% | Global, focus Asia & Africa | Long term (≥ 4 years) |

| Rising incidence of animal bites in Asia & Africa | +0.8% | Asia-Pacific core, Africa | Short term (≤ 2 years) |

| Technological advances in molecular assays (RT-PCR, qPCR) | +0.7% | Global, early in North America & Europe | Medium term (2-4 years) |

| Smartphone-based fluorescence readers enabling community testing | +0.5% | Asia-Pacific, Africa, rural worldwide | Long term (≥ 4 years) |

| One-Health data-integration platforms linking human & veterinary labs | +0.4% | Global, pilot in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Point-of-Care Rapid Rabies Tests in Endemic Areas

Portable tests are narrowing the diagnostic gap in communities lacking laboratory infrastructure. The CDC-validated LN34 assay delivers PCR-grade results on existing field platforms, cutting reporting times from days to hours. Coupled with lateral-flow devices that hit 97% sensitivity and 100% specificity, health workers can confirm infection without complex equipment.[2]Ewen Callaway, “Simpler Test for Rabies in Dogs Could Be Step Toward Eradication,” NATURE.COM Smartphone fluorescence readers transmit results instantly, creating real-time dashboards that guide post-exposure prophylaxis decisions. As regional programs roll out subsidized kits, uptake is accelerating across India, the Philippines, and Kenya. This surge directly enlarges the rabies diagnostics market, driving revenues for both established IVD vendors and start-ups specializing in isothermal detection.

“Zero by 2030” Elimination Initiatives Boosting Surveillance Funding

WHO, FAO, and Gavi are channeling multi-year grants into diagnostics so countries can monitor progress toward dog-mediated rabies elimination. National action plans reserve dedicated budgets for laboratory upgrades, procurement of PCR reagents, and deployment of integrated data platforms such as the GARC system. The FAO’s One-Health toolkit links vaccination records with diagnostic outcomes, giving policymakers evidence to optimize dog-vaccination drives.[3]Food and Agriculture Organization, “Towards Zero Human Deaths from Dog-Mediated Rabies by 2030,” FAO, fao.org Continuous funding reduces reagent stock-outs and encourages manufacturers to localize kit assembly, thereby expanding the rabies diagnostics market in low- and middle-income economies.

Rising Incidence of Animal Bites in Asia & Africa

Changes in urbanization and pet ownership are pushing bite-case numbers upward, particularly among children aged 5-14 in the Philippines and Vietnam.[4]Maria Lourdes Hernandez, “Puppies as the Primary Causal Animal for Human Rabies Cases,” Frontiers in Microbiology, frontiersin.orgUganda’s communities adjacent to wildlife reserves experience incidence rates up to 157 cases per 1,000 people or dogs, spurring urgent demand for rapid diagnostic triage. Domestic-wildlife interfaces and bat lyssavirus spill-over events underscore the need for assays that can differentiate genetic variants. As bite surveillance improves, testing volumes rise, further expanding the rabies diagnostics market.

Technological Advances in Molecular Assays (RT-PCR, qPCR)

PCR platforms now integrate isothermal amplification, CRISPR-Cas readouts, and AI-driven analytics to identify viral RNA at concentrations below 15 copies/mL. Loop-mediated isothermal amplification (LAMP) sidesteps the need for thermal cyclers, slashing capital costs for district laboratories. Paper-based extraction strips and open-source fluorimeters such as qByte cut consumable costs to under USD 2 per test. These innovations reduce barriers for small clinics and veterinary stations, intensifying competition across the rabies diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & limited supply of confirmatory reagents in LMICs | -0.8% | Asia-Pacific, Africa, Latin America | Short term (≤ 2 years) |

| Shortage of trained personnel for FAT outside reference labs | -0.6% | Global, acute Sub-Saharan Africa & rural Asia | Medium term (2-4 years) |

| Cold-chain dependence of gold-standard assays | -0.4% | Tropical regions, remote areas worldwide | Medium term (2-4 years) |

| Genetic drift in emerging bat-borne lyssaviruses causing false-negatives | -0.3% | Europe, North America, emerging Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost & Limited Supply of Confirmatory Reagents in LMICs

Median post-exposure prophylaxis still costs INR 1,400 (USD 22) in Indian public hospitals, rising to INR 3,685 (USD 58) in private settings, squeezing household budgets. Imported monoclonal antibodies and fluorescent tags for FAT remain priced beyond many provincial labs, while the COVID-19 pandemic exposed fragile reagent supply chains. New FDA rules on laboratory-developed tests add documentation burdens that can deter low-volume kit importers. Although local manufacturing initiatives are gaining ground, the short-term effect is a drag on rabies diagnostics market growth.

Shortage of Trained Personnel for FAT Outside Reference Labs

FAT demands skilled microscopy and antigen recognition, yet commune-level veterinary services in Vietnam report significant competency gaps. Rural Philippine provinces needed a USD 47,000 investment in training and infrastructure just to meet a 2-day diagnostic turnaround. Cold-chain logistics compound the problem, and evolving lyssavirus strains can bypass conventional probes, producing false-negatives in Europe and North America. Automated slide readers and simplified PCR protocols are mitigating these constraints but cannot close the personnel gap overnight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Diagnostic Method: Molecular Platforms Gain Traction

The rabies diagnostics market size for diagnostic methods is undergoing a pivot as FAT retained 41.21% revenue share in 2024, yet PCR/RT-PCR platforms are expanding at an 8.23% CAGR through 2030. FAT’s established accuracy secures its role in reference laboratories, but its fluorescent microscopes, cold-chain reagents, and skilled-staff requirements limit reach in rural Africa. Direct Rapid Immunohistochemical Tests (DRIT) provide a bridge by delivering FAT-level accuracy on standard light microscopes. Rapid antigen lateral-flow tests supply near-instant answers for bite-victim triage, and the CDC’s LN34 protocol demonstrates how simplified PCR can slash skill barriers.

Moving forward, CRISPR-enabled assays and smartphone-integrated PCR promise field detection at a fraction of traditional equipment cost, opening fresh revenue pools for small device makers. As local funding cycles favor reagents with shelf lives beyond 12 months, molecular kits that tolerate ambient temperatures will erode FAT’s dominance, accelerating the rabies diagnostics market.

By Technology: Molecular Diagnostics Redefine Competitive Rules

Immunodiagnostics maintained 53.43% rabies diagnostics market share in 2024, anchored by well-established ELISA kits used for sero-monitoring of vaccination campaigns. Yet molecular diagnostics will grow at an 8.68% CAGR, driven by low-power LAMP devices and AI-assisted CRISPR-Cas detection that can recognize emerging bat-borne variants. Hybrid platforms blend antigen capture with amplification readouts, offering confirmatory power in minutes.

Cloud-connected apps feed results into One-Health dashboards, tightening response times to suspected cases. As ministries of health earmark budgets for technology that can prove elimination status, molecular vendors gain a strategic edge in the rabies diagnostics market.

By Sample Type: Saliva Testing Accelerates Adoption

Brain tissue commanded 46.71% of revenue in 2024, but cultural resistance to post-mortem sampling spurs interest in ante-mortem saliva assays, which are projected to rise at a 6.37% CAGR. Trans-nasal brain probes that avoid skull opening improve acceptance in Muslim-majority regions, yet saliva sampling offers even greater scalability for community surveillance. Improved RNA extraction buffers and portable fluorimeters amplify sensitivity, reducing false-negatives.

Wildlife programs rely on fecal and oral swabs to monitor bat colonies, broadening the rabies diagnostics market size across ecological niches. As mobile clinics pair saliva tests with smartphone readers, diagnostic reach extends to herders and school health officers alike.

By End User: Point-of-Care Networks Expand Reach

Reference laboratories still hold 44.32% share thanks to their accreditation status and capacity for FAT confirmatory testing. However, point-of-care and veterinary clinics will post a 7.25% CAGR through 2030 as open-source qByte fluorimeters and low-cost LAMP cartridges reach prices below USD 60. Tele-consultation portals allow field technicians to upload fluorescence images for expert review, bridging skills gaps.

Hospitals and public-health labs integrate results with electronic medical records, streamlining PEP decisions. Research institutes validate CRISPR prototypes and move them toward WHO prequalification, sustaining a virtuous cycle of innovation in the rabies diagnostics market.

Geography Analysis

North America led revenue in 2024 with a 33.38% share, supported by comprehensive wildlife surveillance and FDA-regulated reference labs. Though human cases are rare, testing persists for raccoon-variant spill-overs, such as the 2023 Nebraska kitten incident. The market is mature, yet innovation thrives as suppliers develop smartphone-enabled test readers that comply with new LDT guidelines.

Asia-Pacific will record the fastest 6.18% CAGR, propelled by high rabies burden and increasing government budgets. China is scaling rapid-test procurement in provincial Centers for Disease Control, while the Philippines reported 426 human cases in 2024 despite progress, sparking expanded diagnostic coverage in 2025. India’s make-in-India initiatives promote local kit manufacturing, trimming import costs. Field validation of LAMP devices in Vietnam and smartphone readers in Indonesia demonstrates regional appetite for low-cost solutions.

Europe displays steady demand driven by wildlife surveillance and the need to detect evolving bat lyssaviruses. Germany’s raccoon-dog monitoring studies exemplify integrated surveillance models that combine PCR and sequencing. The Middle East & Africa segment grows from a lower base, benefiting from Gavi-funded diagnostic rollouts and One-Health workshops in Mozambique. South America witnesses incremental growth as Brazil, Peru, and Colombia enhance canine-vaccination audits with ELISA serology, widening the rabies diagnostics market.

Competitive Landscape

The rabies diagnostics market is moderately concentrated. Bio-Rad Laboratories supplies ELISA kits such as Platelia Rabies II and leverages a global distributor network. IDEXX and Zoetis cross-sell rabies diagnostics alongside broader veterinary panels; Zoetis added a 32,000 sq ft Louisville reference lab in 2025 to cut turnaround times for U.S. clinics. Start-ups such as SpinChip, now majority-owned by bioMérieux, commercialize microfluidic cartridges capable of multiplex rabies detection.

Strategy hinges on technology portfolios that meet WHO prequalification and FDA class-II requirements. Ceva’s 2025 acquisition of Artemis Technologies expands oral vaccine offerings, creating potential bundling with diagnostic kits for dog-population campaigns. Partnerships between AI analytics firms and PCR-kit makers accelerate variant-detection software that can be updated over-the-air. Competitive differentiation also emerges in reagent shelf life, smartphone-app usability, and local tech-support footprints—key purchase criteria for ministries in Africa and Southeast Asia.

Looking ahead, emerging players targeting reagent-free LAMP chemistries and open-source hardware stand to disrupt incumbent positions, especially if they secure WHO prequalification. Nevertheless, established multinationals maintain entry barriers through regulatory know-how, validated manufacturing, and long-term procurement contracts, sustaining a balanced yet dynamic rabies diagnostics market.

Rabies Diagnostics Industry Leaders

Bio-Rad Laboratories, Inc.

Merck KGaA

Creative Diagnostics

Bioneer Corporation

BioNote Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: A dog tested positive for rabies in Grant County, marking the county’s eleventh animal case since 2020, confirmed by the New Mexico Department of Health Scientific Laboratory Division.

- March 2025: Aim Vaccine Co. Ltd. filed for regulatory approval of the first serum-free human rabies vaccine after phase III trials showed superior safety and immunogenicity.

- September 2024: The City of Trenton Department of Health and Human Services held its annual free rabies clinic to improve vaccination coverage.

Global Rabies Diagnostics Market Report Scope

| Fluorescent Antibody Test (FAT) |

| Direct Rapid Immunohistochemical Test (DRIT) |

| Rapid Antigen Test (Lateral Flow Immunoassay) |

| Enzyme-Linked Immunosorbent Assay (ELISA) |

| Polymerase Chain Reaction (PCR / RT-PCR) |

| Others |

| Immunodiagnostics |

| Molecular Diagnostics |

| Other / Hybrid Platforms |

| Brain Tissue |

| Saliva |

| Serum / Cerebrospinal Fluid |

| Others |

| Reference Laboratories |

| Point-of-Care / Veterinary Clinics |

| Hospitals & Public Health Laboratories |

| Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Diagnostic Method | Fluorescent Antibody Test (FAT) | |

| Direct Rapid Immunohistochemical Test (DRIT) | ||

| Rapid Antigen Test (Lateral Flow Immunoassay) | ||

| Enzyme-Linked Immunosorbent Assay (ELISA) | ||

| Polymerase Chain Reaction (PCR / RT-PCR) | ||

| Others | ||

| By Technology | Immunodiagnostics | |

| Molecular Diagnostics | ||

| Other / Hybrid Platforms | ||

| By Sample Type | Brain Tissue | |

| Saliva | ||

| Serum / Cerebrospinal Fluid | ||

| Others | ||

| By End User | Reference Laboratories | |

| Point-of-Care / Veterinary Clinics | ||

| Hospitals & Public Health Laboratories | ||

| Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current rabies diagnostics market size?

The rabies diagnostics market size reached USD 2.11 billion in 2025 and is forecast to climb to USD 2.68 billion by 2030.

2. Which diagnostic method dominates the rabies diagnostics market?

The Fluorescent Antibody Test led with 41.21% market share in 2024, although PCR/RT-PCR is the fastest-growing method.

3. Why is Asia-Pacific the fastest-growing region?

High rabies incidence, expanded surveillance funding, and rapid adoption of point-of-care tests push Asia-Pacific to a 6.18% CAGR through 2030.

4. How are molecular technologies reshaping the rabies diagnostics industry?

Isothermal LAMP and CRISPR-Cas assays deliver PCR-level sensitivity without bulky equipment, reducing costs and enabling field deployment.

5. What are the main restraints on market growth?

High reagent costs, limited skilled personnel for FAT, cold-chain dependence, and genetic drift in bat lyssaviruses all curb near-term expansion.

Page last updated on: