Zika Virus Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

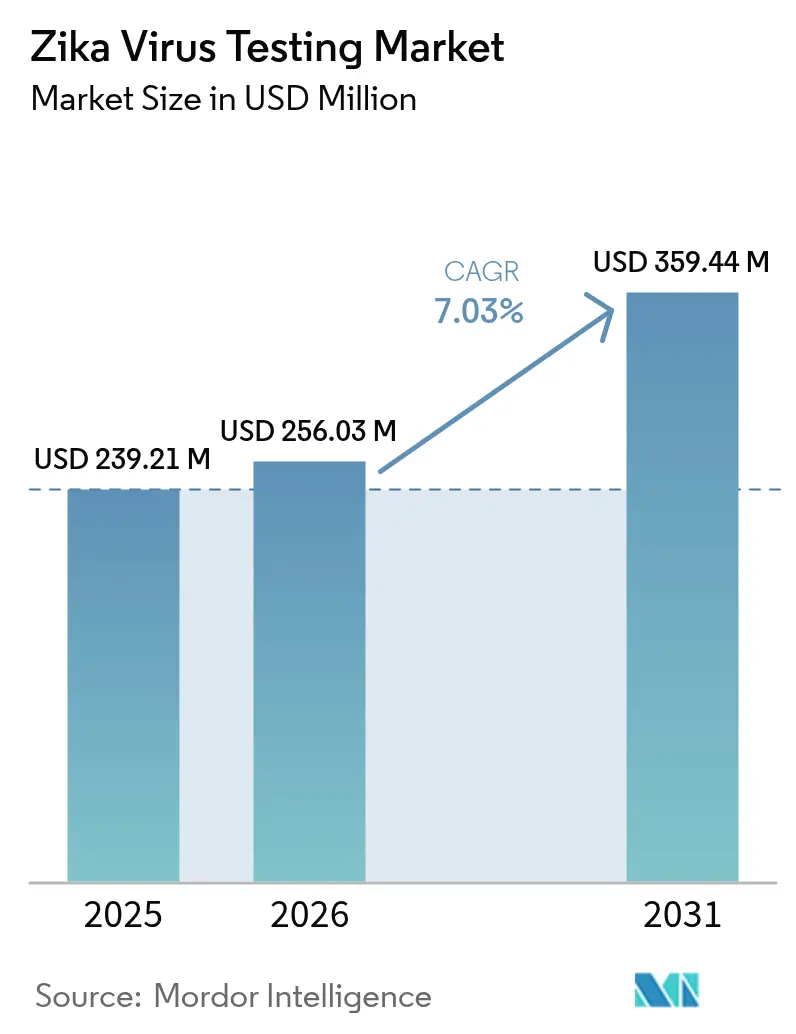

| Market Size (2026) | USD 256.03 Million |

| Market Size (2031) | USD 359.44 Million |

| Growth Rate (2026 - 2031) | 7.03% CAGR |

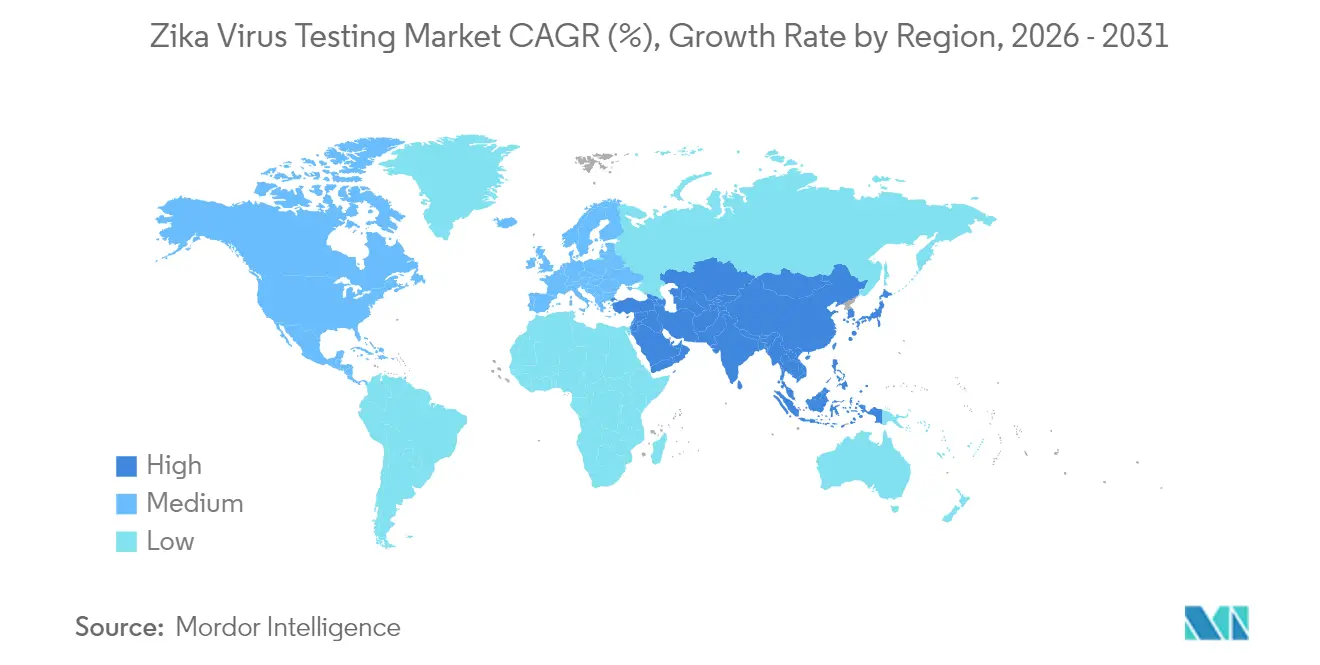

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

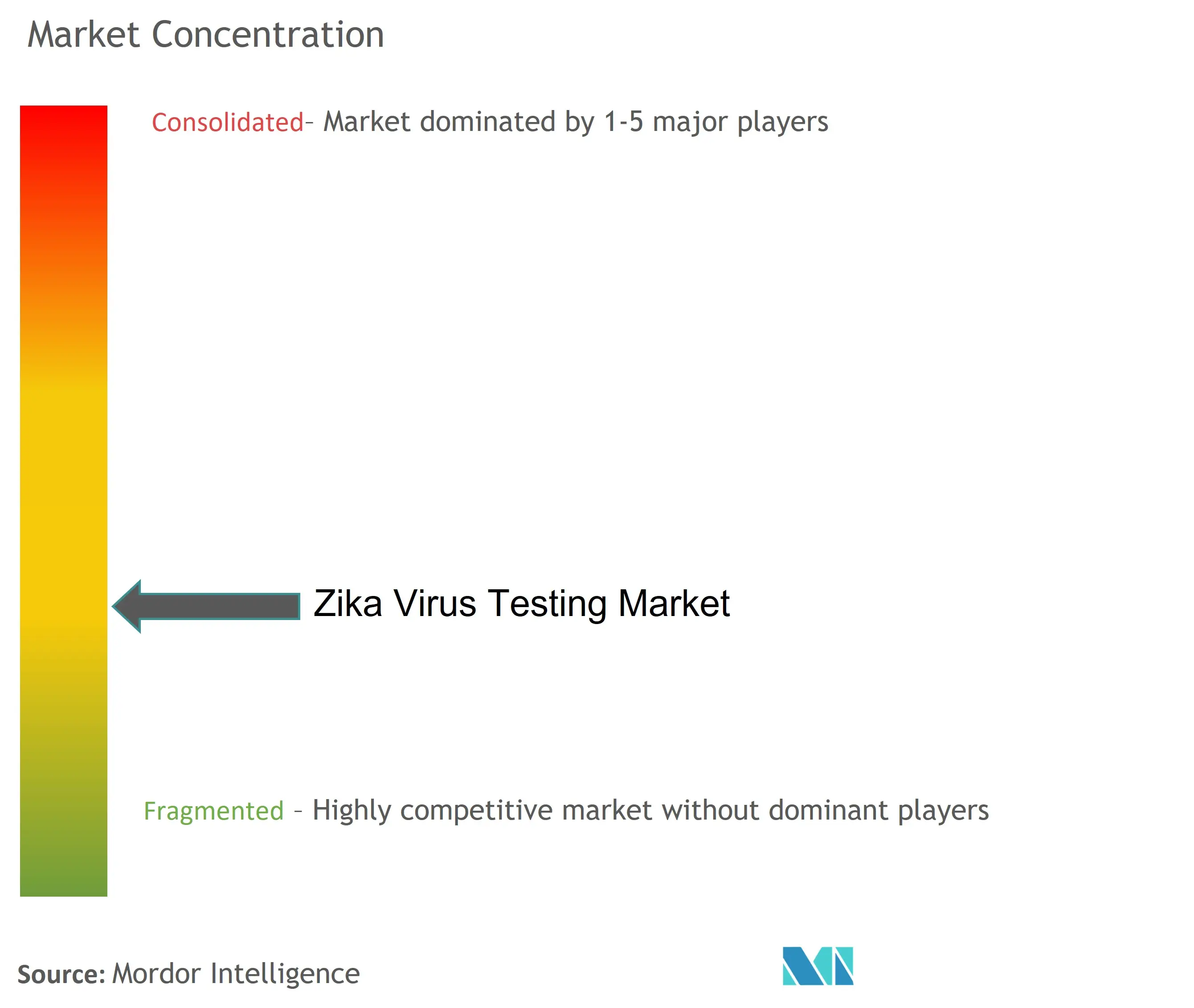

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zika Virus Testing Market Analysis by Mordor Intelligence

Zika virus testing market size in 2026 is estimated at USD 256.03 million, growing from 2025 value of USD 239.21 million with 2031 projections showing USD 359.44 million, growing at 7.03% CAGR over 2026-2031. Robust arboviral surveillance mandates, climate-driven vector expansion, and rising international travel sustain the growth momentum. Technology convergence is accelerating as laboratories adopt multiplex molecular platforms that detect Zika, dengue, and chikungunya in a single run, trimming diagnostic uncertainty in co-endemic regions. Artificial-intelligence-assisted assay design is mitigating historical cross-reactivity and shortening development cycles, while domestic manufacturing strategies are strengthening supply-chain resilience in response to pandemic-era disruptions[1]Source: World Health Organization, “Zika Epidemiology Update – May 2024,” who.int .

Key Report Takeaways

- North America retained 41.88% of Zika virus testing market share in 2025 as its surveillance infrastructure guarantees steady procurement during inter-epidemic phases.

- Asia-Pacific is projected to post the fastest regional expansion, climbing at a 7.08% CAGR through 2031 on the back of upgraded vector-borne disease laboratories and heightened outbreak vulnerability.

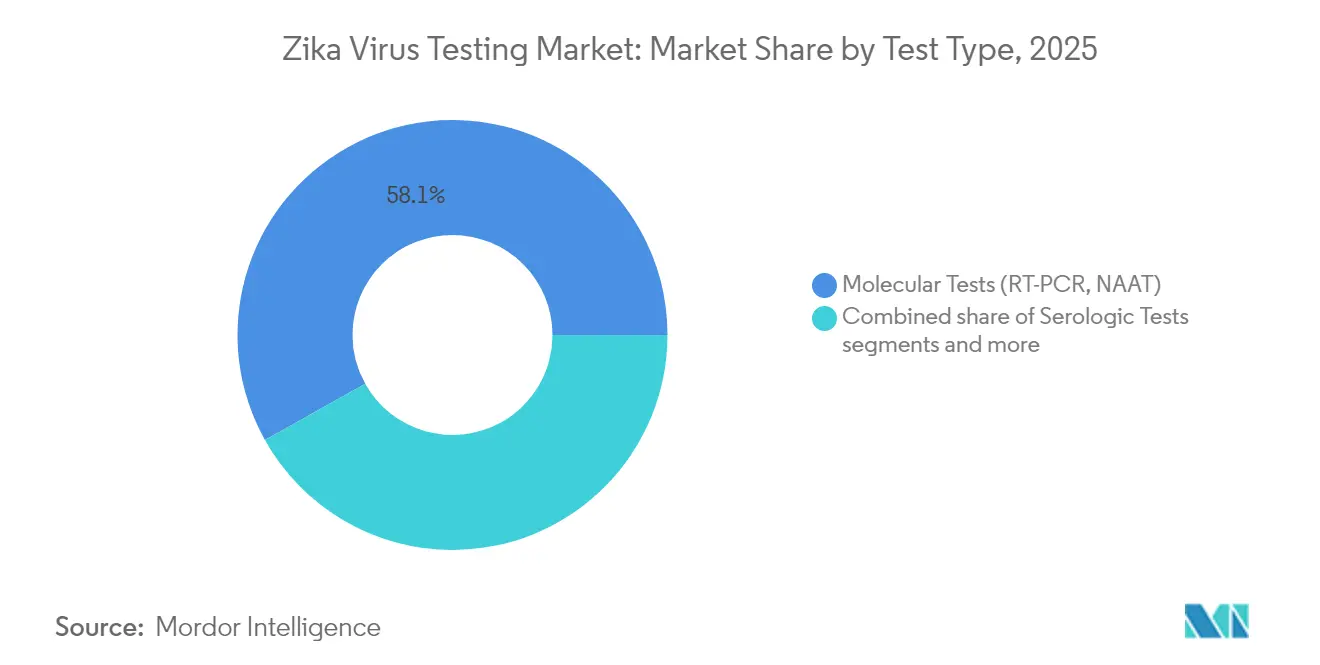

- Molecular tests accounted for 58.12% of 2025 revenue, while point-of-care molecular assays are poised for an 8.55% CAGR to 2031 as outbreak response demands shift toward decentralized testing.

- Blood/serum specimens commanded 70.84% share in 2025, yet saliva-based protocols are the fastest climbers at an 7.96% CAGR thanks to non-invasive self-collection convenience.

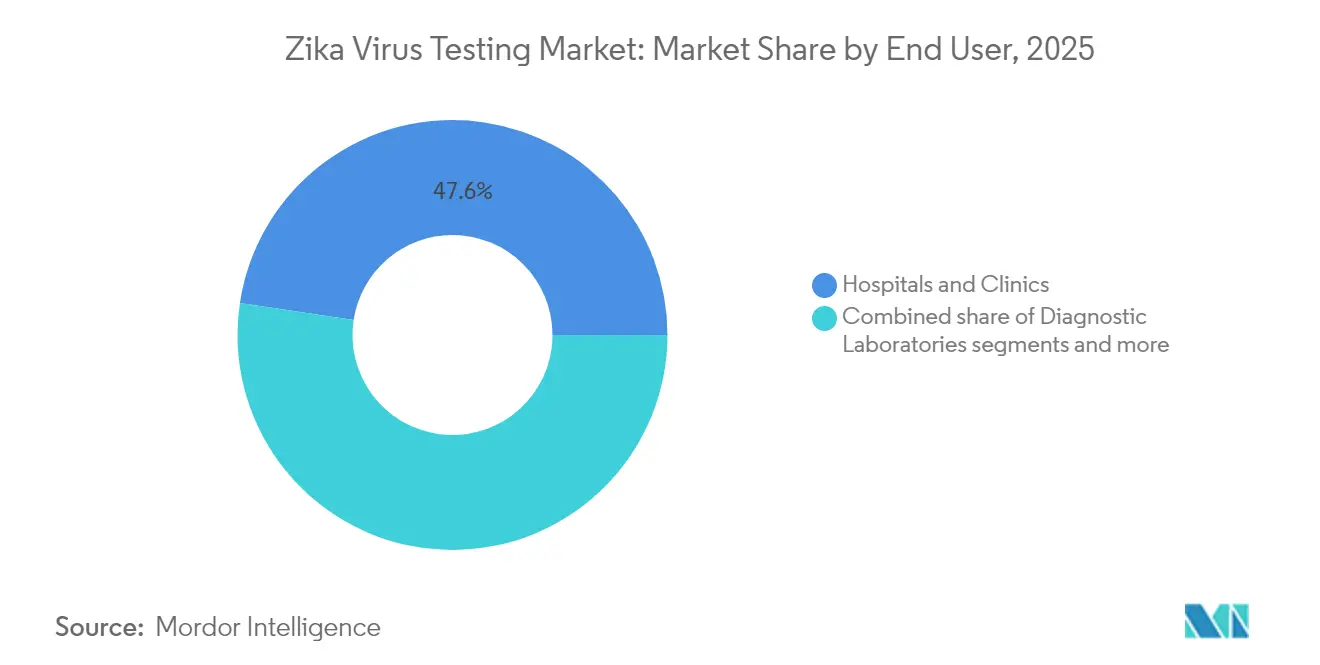

- Hospitals and clinics led with 47.62% revenue in 2025; point-of-care settings will expand at 7.44% CAGR as emergency departments embed rapid diagnostics into triage workflows.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Zika Virus Testing Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of Zika outbreaks | +1.8% | Americas, APAC | Medium term (2-4 years) |

| Government surveillance & funding | +1.5% | Global (endemic focus) | Long term (≥ 4 years) |

| Advances in RT-PCR & multiplex NAAT | +1.2% | North America, Europe | Short term (≤ 2 years) |

| POC test integration into ID panels | +1.0% | Global | Medium term (2-4 years) |

| Pre-conception screening demand | +0.8% | North America, Europe, urban APAC | Long term (≥ 4 years) |

| Vector/clinical-lab networks | +0.7% | Americas, APAC, Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Zika Outbreaks

Pan American Health Organization recorded 40,891 confirmed cases in 2024, a 14% jump from 2023, confirming the virus’s endemic status in tropical belts. Predictable seasonal surges spur hospitals to procure rapid molecular cartridges that distinguish Zika from dengue and chikungunya during triage. Brazil remains the epicenter at 84% of regional cases, while emergent clusters in Argentina and Colombia widen geographic test uptake. WHO guidance urges laboratories to maintain baseline capacity between epidemics, stabilizing annual reagent demand[2]Source: Pan American Health Organization, “Epidemiological Update: Zika Virus Infection – 2024,” paho.org .

Government Surveillance & Funding

Sustained public investment is anchoring the Zika virus testing market. The CDC’s Epidemiology and Laboratory Capacity program ring-fenced vector-borne allocations for FY 2025, guaranteeing reagent purchases for state labs. The World Bank’s Pandemic Fund channeled USD 16 million to Caribbean nations to bolster integrated arboviral surveillance networks. NIAID’s 2025 budget narrative earmarks diagnostics R&D, signalling multiyear funding visibility that reassures manufacturers of volume commitments.

Advances in RT-PCR & Multiplex NAAT

Loop-mediated isothermal amplification enables sub-30-minute detection without thermal cyclers, suiting field clinics. Roche’s cobas Mass Spec automation pipeline lifts daily throughput while AI-assisted primer design cuts cross-reactivity. Next-generation sequencing platforms integrated with BARDA-funded BugSeq analytics yield pathogen-agnostic readouts, future-proofing laboratories against variant emergence.

POC Test Integration into ID Panels

SpinChip Diagnostics’ microfluidic cartridge, now under bioMérieux, delivers whole-blood arboviral panels in 10 minutes, aligning with emergency-department turnaround targets. FDA Emergency Use frameworks that sped COVID-era authorizations provide a template for swift Zika panel clearances, encouraging firms to bundle flaviviruses on a single device. Cloud-linked readers transmit geotagged positives to epidemiological dashboards within minutes, tightening outbreak containment loops.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining epidemic momentum | -1.2% | Global (post-outbreak) | Short term (≤ 2 years) |

| Cross-reactivity with dengue antibodies | -0.8% | Americas, APAC | Medium term (2-4 years) |

| Short viraemic detection window | -0.6% | Global | Long term (≥ 4 years) |

| Antigen supply-chain bottlenecks | -0.4% | Manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Epidemic Momentum

Inter-epidemic lulls curb routine testing volumes as clinical suspicion wanes and budgets shift elsewhere. WHO’s May 2024 update flagged subdued case counts outside hotspots, prompting some laboratories to run down reagent stocks. Manufacturers bridge the demand trough with multiplex panels that preserve cartridge turnover even when Zika incidence dips, yet revenue variability remains a headwind.

Cross-reactivity with Dengue Antibodies

Shared flaviviral epitopes yield false-positive ELISAs, pushing clinicians toward costlier neutralization assays. Nanobody-based blocking ELISAs under peer review promise higher specificity, but widespread adoption awaits regulatory clearance. In the interim, laboratories rely on molecular confirmation, narrowing serology’s revenue pool in high-dengue-burden regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Tests Propel Market Leadership

Molecular assays delivered 58.12% revenue in 2025, underscoring their primacy in acute-phase diagnosis. The Zika virus testing market size for point-of-care molecular platforms is forecast to expand at 8.55% CAGR through 2031, supported by CLIA-waived systems that slot into emergency rooms and obstetric clinics. The Zika virus testing market share for serology trails due to dengue cross-reactivity, though population-level IgM surveys sustain baseline demand. Isothermal amplification and AI-curated primers are shrinking run times and manual steps, enhancing scalability in resource-constrained laboratories.

Second-generation LAMP cartridges leverage lyophilized reagents for ambient shipping, lowering cold-chain costs. Digital PCR is emerging for low-prevalence surveillance, offering femtogram-level sensitivity suited to blood-bank screening. PRNT remains reference-grade yet limited to a handful of BSL-3 centers, constraining its commercial footprint. Serology firms are pivoting toward epitope-engineered antigens to claw back specificity, but molecular dominance is unlikely to be challenged within the forecast window.

By Sample Type: Blood Prevails, Saliva Climbs

Blood and serum retained 70.84% revenue in 2025 due to entrenched clinical protocols and established throughput. The Zika virus testing market size for saliva and other non-invasive matrices is projected to grow 7.96% CAGR, propelled by self-collection kits that decouple sampling from clinical sites. Whole-saliva ATR-FTIR spectroscopy paired with machine learning achieved 100% sensitivity and 87.5% specificity in pilot studies, previewing mass-screening potential in antenatal clinics.

Urine extends RNA detectability beyond the seven-day serum window, underpinning repeat-testing algorithms for travelers who present late. Paper-microfluidic serum cards validated at 98.5% accuracy facilitate postal transport from rural communities. Cerebrospinal fluid testing remains niche, limited to neuro-complication work-ups, yet underlines assay versatility across specimen types. Regulatory approvals for home sampling boxes are broadening direct-to-consumer channels, further diversifying specimen logistics.

By End-User: Point-of-Care Settings Accelerate

Hospitals and clinics generated 47.62% revenue in 2025, benefitting from in-house laboratories and insurance reimbursements. Point-of-care environments are the fastest climbers at 7.44% CAGR, as disaster response teams and maternity wards embed cartridge-based devices on site. The Zika virus testing market share uplift in public-health labs stems from federal surveillance contracts that guarantee steady volume, although batch testing favors high-throughput platforms.

Research institutes act as crucibles for next-generation diagnostics, yet commercial revenues remain modest. Telemedicine portals now bundle at-home collection with virtual consultations, eroding traditional outpatient volumes. Mobile container labs equipped with solar-powered PCR units are extending diagnostic reach into rainforest settlements, illustrating use-case diversity that vendors must serve.

Geography Analysis

North America’s 41.88% revenue in 2025 reflects CDC grant flows and rapid Emergency Use Authorizations that de-risk vendor investment. The Zika virus testing market size in the region will advance steadily as travel-linked importations sustain screening in blood banks and fertility clinics. Federal stockpiles guarantee reagent turnover even during low-incidence years.

Asia-Pacific leads in growth at 7.08% CAGR as governments mainstream arboviral surveillance within universal healthcare expansions. Climate-driven Aedes range shifts toward temperate latitudes spur Japan, South Korea, and northern China to adopt early-warning molecular platforms. Urban megacities in India and Indonesia are piloting saliva kiosks that transmit real-time positives to municipal dashboards.

South America, anchored by Brazil, remains the epidemiological hotspot that drives bulk cartridge demand. PAHO-coordinated reagent tenders create price stability for regional labs while cross-training programs standardize assay performance. Europe focuses on traveler testing and antenatal screening in Mediterranean mosquito zones. Harmonization under IVDR is accelerating adoption of multiplex CE-marked panels.

The Middle East and Africa exhibit nascent but fast-rising demand as vector surveillance gains donor support. Nigeria’s National Arbovirus Laboratory Network installed its first high-throughput NAAT line in 2024, signaling emerging opportunities. Gulf nations procure diagnostics to screen migrant labor inflows, adding a travel-linked revenue stream.

Competitive Landscape

Market structure is moderately fragmented. Roche, Abbott, and Thermo Fisher collectively control a sizable multiplex PCR footprint, leveraging global logistics to secure formulary positioning. bioMérieux’s EUR 111 million SpinChip purchase underscores rising valuations for microfluidic POC assets.

AI differentiation is sharpening: BugSeq’s BARDA-backed analytics convert raw sequencing reads into variant-level reports in minutes, reducing bioinformatics barriers for clinical labs. Thermo Fisher’s USD 1.5 billion U.S. capacity build revamps cartridge supply resilience, courting federal procurement.

White-space lies in low-resource geographies demanding solar-powered, tablet-operated devices. Start-ups exploiting DNA-nanotechnology biosensors promise lower per-test costs and field ruggedness. Vendors able to refresh assay software rapidly to chase emerging flaviviruses will outpace hardware-locked rivals.

Zika Virus Testing Industry Leaders

Abbott

DiaSorin (Luminex Corporation)

F. Hoffmann-La Roche Ltd

Quest Diagnostics

Siemens Healthcare GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: FDA issued draft guidance on rapid validation of IVDs for emerging pathogens, streamlining future Zika panel authorizations

- May 2024: FDA ruled Zika virus no longer a relevant communicable disease agent for tissue establishments, easing donor-screening burdens while maintaining surveillance

Global Zika Virus Testing Market Report Scope

As per the scope of the report, the Zika virus test is usually a blood test or a urine test, where the physician or other healthcare provider will take a blood sample from a vein in the patient's arm using a small needle.

The Zika Virus Testing Market is segmented by Test Type (Molecular Test and Serologic Test), End-User (Hospital/Clinic, Diagnostics Laboratory and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (USD million) for the above segments.

| Molecular Tests (RT-PCR, NAAT) |

| Serologic Tests (IgM/IgG ELISA) |

| Plaque-Reduction Neutralisation Test (PRNT) |

| Blood / Serum |

| Urine |

| Saliva & Others |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Home care Settings |

| Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Test Type (Value) | Molecular Tests (RT-PCR, NAAT) | |

| Serologic Tests (IgM/IgG ELISA) | ||

| Plaque-Reduction Neutralisation Test (PRNT) | ||

| By Sample Type (Value) | Blood / Serum | |

| Urine | ||

| Saliva & Others | ||

| By End-User (Value) | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Home care Settings | ||

| Research Institutes | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Zika Virus Testing Market?

The Zika Virus Testing Market size is expected to reach USD 256.03 million in 2026 and grow at a CAGR of 7.03% to reach USD 359.44 million by 2031.

What is the current Zika Virus Testing Market size?

In 2026, the Zika Virus Testing Market size is expected to reach USD 256.03 million.

Who are the key players in Zika Virus Testing Market?

Abbott, DiaSorin (Luminex Corporation), F. Hoffmann-La Roche Ltd, Quest Diagnostics and Siemens Healthcare GmbH are the major companies operating in the Zika Virus Testing Market.

Which is the fastest growing region in Zika Virus Testing Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Zika Virus Testing Market?

In 2026, North America accounts for the largest market share in Zika Virus Testing Market.

What years does this Zika Virus Testing Market cover, and what was the market size in 2025?

In 2025, the Zika Virus Testing Market size was estimated at USD 256.03 million. The report covers the Zika Virus Testing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Zika Virus Testing Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: