Lyme Disease Diagnostic Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

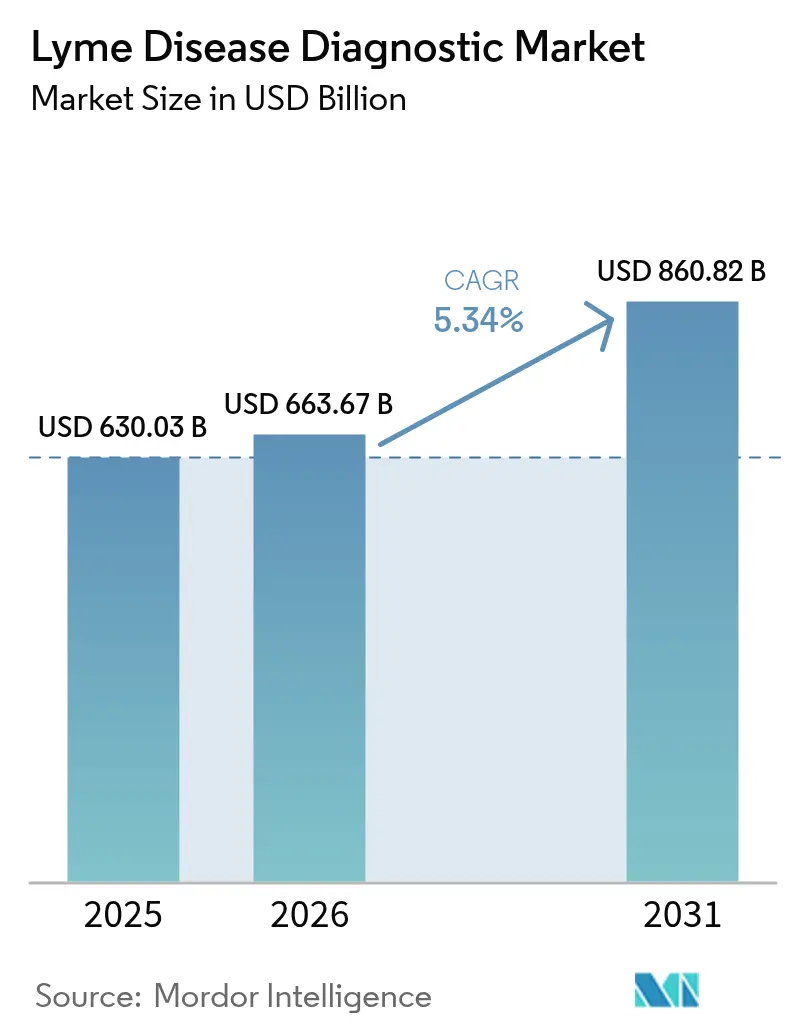

| Market Size (2026) | USD 663.67 Billion |

| Market Size (2031) | USD 860.82 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

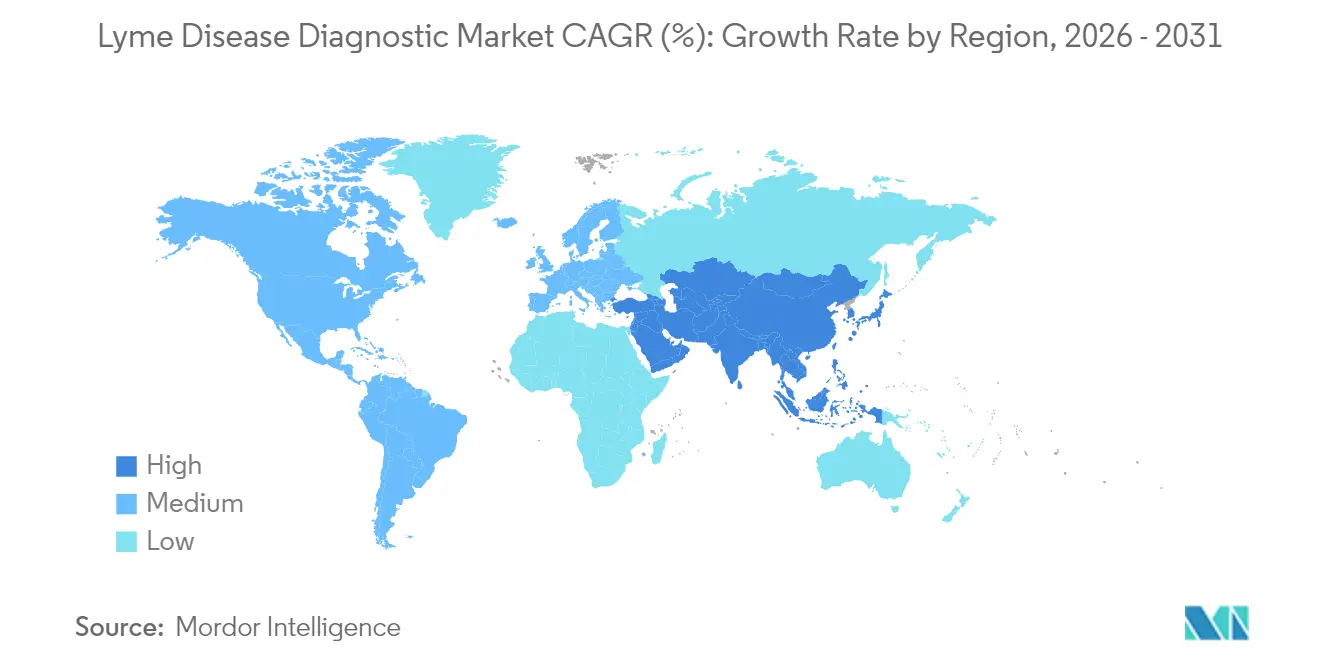

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lyme Disease Diagnostic Market Analysis by Mordor Intelligence

Lyme disease diagnostics market size in 2026 is estimated at USD 663.67 million, growing from 2025 value of USD 630.03 million with 2031 projections showing USD 860.82 million, growing at 5.34% CAGR over 2026-2031. Growth reflects the steady rise in Lyme disease incidence as ticks expand into warmer latitudes, while laboratories pivot toward more sensitive modified two-tier algorithms and AI-guided readers that cut false-negative rates[1]Source: Food and Drug Administration, “Medical Devices: Laboratory-Developed Tests,” federalregister.gov. Point-of-care investments, home-collection kits, and FDA approvals of rapid ImmunoBlot and xVFA assays broaden patient access and shorten result turnaround times. Global reimbursement policies are gradually recognizing multiplex assays, yet coverage gaps persist, especially for urine-based and multianalyte panels[2]Source: U.S. National Institutes of Health, “Diagnostics Reimbursement Knowledge Guide,” seed.nih.gov. Competitive intensity is moderate: legacy firms rely on regulatory expertise and distribution scale, whereas smaller innovators focus on direct pathogen detection and smartphone-enabled platforms. Climate-linked tick habitat expansion continues to be the single biggest volume catalyst, sustaining test demand in new endemic zones across North America, Europe, and Asia-Pacific.

Key Report Takeaways

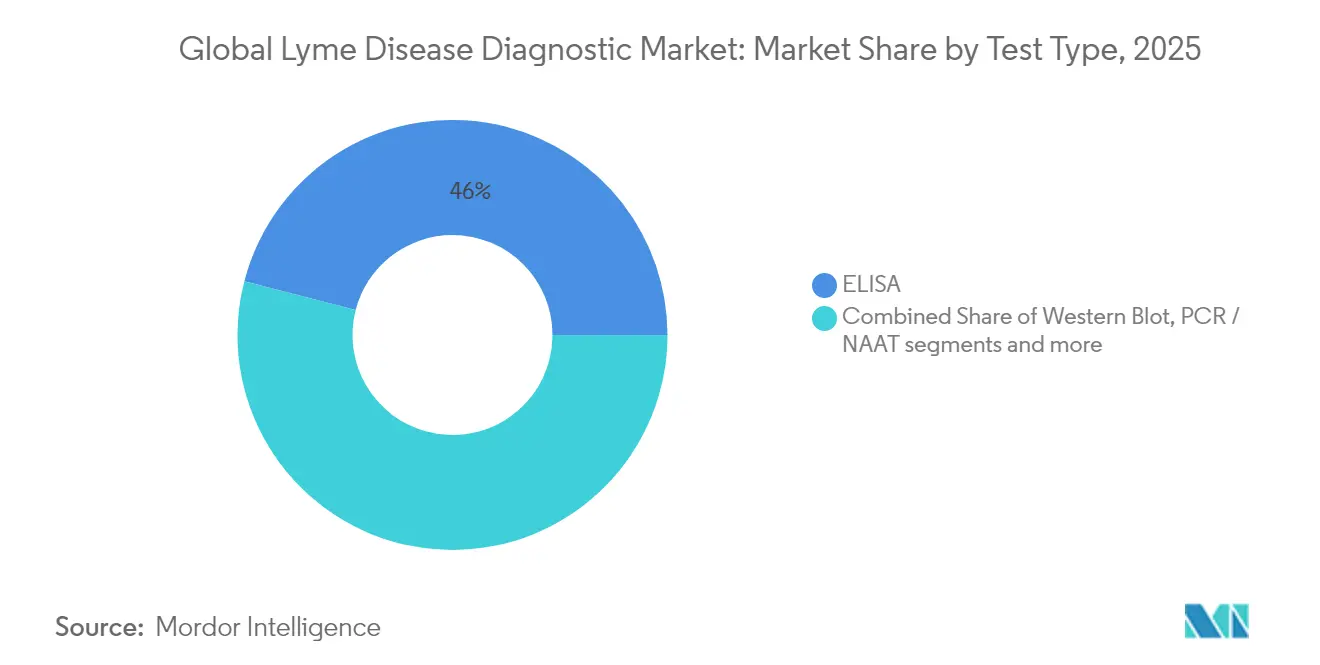

- By test type, ELISA retained 45.98% of the Lyme disease diagnostics market share in 2025, while multiplex microarray is projected to grow at 6.07% CAGR through 2031.

- By technology, serology generated 57.12% revenue in 2025; digital and AI-augmented platforms are expected to post the fastest 6.62% CAGR to 2031.

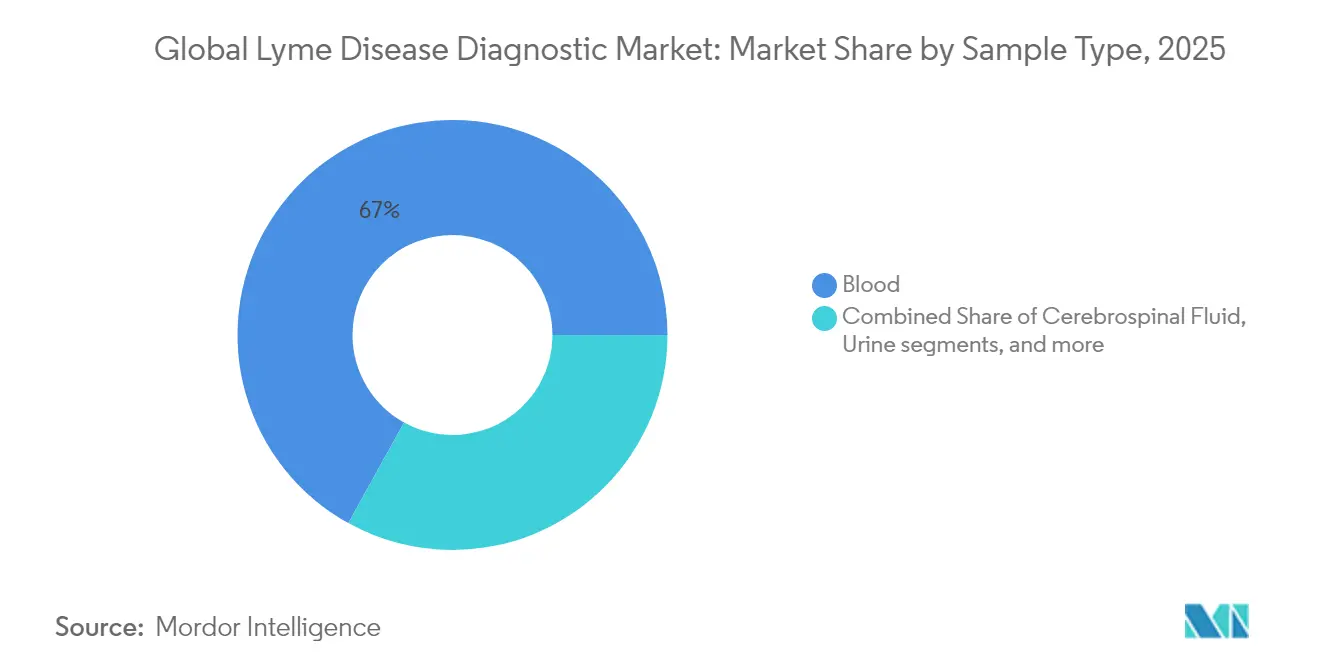

- By sample type, blood/serum accounted for 66.95% of the Lyme disease diagnostics market size in 2025, whereas urine testing will expand at a 7.04% CAGR between 2026-2031.

- By end user, diagnostic laboratories held 38.35% revenue in 2025, yet homecare testing is set to rise at 7.58% CAGR through 2031.

- By geography, North America led with 42.98% revenue share in 2025; Asia-Pacific is poised for the highest 7.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lyme Disease Diagnostic Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-linked tick habitat expansion | +1.2% | Global, temperate regions | Long term (≥ 4 years) |

| Rising adoption of modified two-tier testing | +0.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| FDA approvals of high-sensitivity rapid kits | +0.7% | North America, spill-over to aligned markets | Short term (≤ 2 years) |

| Home-collection kits boosting access | +0.6% | Global, early adoption in developed markets | Medium term (2-4 years) |

| AI-powered digital readers | +0.5% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Growth in point-of-care investments | +0.4% | North America, Latin America, Mediterranean | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Climate-linked Tick Habitat Expansion

Warming winters and longer summers lengthen tick activity seasons and push vectors into higher latitudes, lifting U.S. diagnoses to roughly 476,000 annually and driving test volumes as far south as northern Mexico. Models suggest a 1.5-fold increase in Baltic habitats, alongside a sharp decline in parts of Ukraine, compelling health systems to tailor test menus according to Borrelia species prevalence. Mediterranean and North African nations now report a rise in Borrelia circulation, pressuring suppliers to localize antigen panels for regional strains. Economic projections indicate that a 3 °C temperature rise could swell U.S. healthcare costs to USD 236 million, underlining the persistent demand for accurate early-stage diagnostics.

Rising Adoption of Modified Two-Tier Algorithms (MTTTA)

Clinical laboratories are replacing Western blot confirmation with second-step ELISAs that capture earlier antibody responses, doubling detection sensitivity in some studies without losing specificity. U.S. payers such as Blue Cross NC have started to reimburse MTTTA workflows, easing budget constraints on labs and accelerating uptake. European reference centers are updating guidelines, creating a follow-on effect in emerging Asian laboratories that rely on EU technical standards. Vendors that can bundle first- and second-step kits within a single regulatory filing enjoy stronger purchasing leverage.

FDA Approvals of High-Sensitivity ImmunoBlot & xVFA Rapid Tests

Clearances for 31-antigen ImmunoBlot kits and 20-minute smartphone-interpreted xVFA assays have redefined speed and sensitivity thresholds for Lyme tests. U.S. FDA special controls for nucleic-acid FISH devices signal broader agency willingness to green-light cutting-edge formats, prompting a surge of 510(k) filings in 2024-2025. These authorizations shorten development cycles for rapid point-of-care tools positioned for urgent-care clinics and mobile health units.

Home-Collection Kits Boosting Access & Testing Volumes

FDA-certified fingerstick devices such as the Tasso Remote Kit allow patients to mail blood to specialty labs, sidestepping geography and appointment bottlenecks. Direct-pay models decouple revenue from lagging insurance policies and appeal to Lyme-aware consumers in rural U.S. counties and European tourist corridors. Regulators still require physician oversight for treatment, but early-stage market evidence shows higher completion rates and repeat testing among home users.

Restraints Impact Analysis*

| Restarints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High false-negative rate of legacy ELISA protocols | -0.90% | Global, with highest impact in cost-sensitive markets | Medium term (2-4 years) |

| Reimbursement gaps for multiplex & urine-based assays | -0.60% | North America & EU, expanding to emerging markets | Long term (≥ 4 years) |

| Supply-chain fragility for recombinant antigens | -0.40% | Global, with concentrated impact in specialized manufacturing regions | Short term (≤ 2 years) |

| Physician under-recognition in emerging geographies | -0.30% | APAC, Latin America, MEA regions with limited endemic disease awareness | |

| Source: Mordor Intelligence | |||

High False-Negative Rate of Legacy ELISA Protocols

Traditional two-tier testing can miss up to 50% of early infections, leading clinicians to treat empirically or order repeat tests, raising costs and patient anxiety. France’s SPPT classification illustrates policy acknowledgement of these weaknesses, but many insurers still reimburse only the standard workflow, delaying modern upgrades. False negatives also skew surveillance data, masking actual disease burdens in national registries.

Reimbursement Gaps for Multiplex & Urine-Based Assays

Payers often require multi-year clinical-utility evidence before approving novel multiplex panels, slowing hospital adoption despite laboratory. New York regulators recently declined PCR reimbursement, citing insufficient validation relative to serology. This two-speed payment environment restricts advanced test access to self-pay patients, capping broader market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: ELISA Dominance Faces Multiplex Challenge

ELISA generated 45.98% of 2025 revenue, supported by entrenched reimbursement and automated analyzers across clinical labs, yet its high false-negative profile is sparking migration to multiplex arrays growing at a 6.07% CAGR. Western blot remains integral within legacy algorithms, though the Modified Two-Tier ELISA model is gradually curbing blot demand. PCR and NAAT fill a narrow early-infection niche, while lateral-flow cards suit field medicine despite lower sensitivity levels. The Lyme disease diagnostics market size for multiplex microarrays is anticipated to climb markedly as hospitals adopt one-run co-infection panels that improve workflow efficiency. Adoption is paced by payer acceptance and the need for staff training to interpret expanded antigen signatures.

Clinical experience shows protein microarrays lifting sensitivity from 63% to 100% when up to 400 antigens are screened simultaneously. FDA-cleared ImmunoBlot kits with 31-band profiles are eroding Western blot use by matching specificity while reducing laboratory time. As reimbursement codes catch up, ELISA's hold will loosen, yet budget-constrained regional labs may still cling to legacy platforms until depreciation cycles end.

By Technology: Serology Leadership Challenged by Digital Innovation

Serology commanded 57.12% revenue in 2025, but digital and AI-augmented platforms are sprinting ahead with 6.62% CAGR by automating result reads and cutting interpretation errors. Molecular assays appeal for direct pathogen detection within the first two weeks of infection, though higher costs limit routine use. Point-of-care cartridges are now integrating machine-learning analytics, enabling physicians to obtain 95.5%-accurate results in under 20 minutes without shipping specimens off-site. The Lyme disease diagnostics market is therefore seeing technology lines blur as vendors hybridize serology with digital overlay or bundle molecular confirmatory tests.

Over the forecast, AI-enabled lateral-flow readers that link to electronic records will become standard in urgent-care clinics. Cloud-based calibration data will ensure consistent sensitivity across devices, while labs migrate to automated strip interpretation, reducing manpower costs. As software attains Class II medical-device status, technology suppliers will pivot from pure reagents to integrated diagnostics-as-a-service subscriptions.

By Sample Type: Blood Dominance with Urine Innovation

Blood/serum use accounted for 66.95% of 2025 tests thanks to mature ELISA workflows, but urine assays, projected at 7.04% CAGR, entice clinicians seeking painless, repeatable sampling, especially for pediatric and geriatric cohorts. Cerebrospinal fluid testing remains the gold standard for neuroborreliosis though volumes are modest. Skin and synovial samples cover localized manifestations but require invasive collection. The Lyme disease diagnostics market size for urine testing will hinge on assay sensitivity breakthroughs and payer acknowledgment of clinical utility.

Technical hurdles include low antigen concentrations and sample stability during shipping, yet microfluidic concentration devices and targeted peptide detection are pushing limits downward. Some U.S. labs are piloting urine-PCR for real-time treatment monitoring, appealing to physicians who need early therapeutic feedback. Nevertheless, ambiguous reimbursement policies keep adoption in early-adopter territory.

By End User: Laboratory Dominance Shifts to Homecare Growth

Diagnostic laboratories garnered 38.35% revenue in 2025, benefiting from high test throughput and entrenched referral patterns, but the homecare channel is set to rise at a 7.58% CAGR as patients embrace doorstep sampling kits. Hospitals and physician offices will still manage acute presentations, yet their share may plateau as preventive self-testing becomes routine in endemic counties. Research institutes generate niche demand for experimental methods and trial screening but rely on grant cycles.

Direct-to-consumer platforms offer fixed-price bundles that bypass insurance friction, appealing to patients wary of coverage denials. However, regulators mandate clinician review of positive findings, leading many kit providers to partner with telemedicine groups. Laboratories respond by launching white-label home programs to protect specimen inflows, indicating a gradual convergence of traditional and consumer models within the Lyme disease diagnostics market.

Geography Analysis

North America contributed 42.98% revenue in 2025 as endemic counties expanded westward and northward, with the United States logging about 476,000 annual cases and healthcare costs near USD 1 billion. Canada’s provincial reporting upgrades and Mexico’s emerging tick surveillance reinforce regional growth. FDA rulemaking around laboratory-developed tests introduces near-term compliance costs but longer-term confidence in assay quality.

Asia-Pacific is the fastest-growing region at 7.18% CAGR to 2031, driven by heightened awareness in China, India, and Japan. Diverse Borrelia species challenge imported assay panels, pushing suppliers to localize antigens and validation studies. Public-health agencies across South Korea and Australia have begun joint training with European laboratories to accelerate expertise transfer. Investment in point-of-care formats fits the region’s dispersed rural populations and infrastructure gaps.

Europe maintains strong volumes thanks to harmonized testing guidelines and high clinician familiarity. Germany and France spearhead research output, while Mediterranean states such as Italy and Spain face rising incidence linked to warmer climates and migrating birds South America and parts of Africa sit in early-stage adoption: Argentina has documented human cases, yet under-diagnosis persists due to limited reagent availability and clinician knowledge.

Competitive Landscape

Market competition is moderate. Abbott, Roche, and DiaSorin leverage turnkey analyzers and global distribution to retain core laboratory accounts, while bioMérieux’s VIDAS Lyme IgG II and IgM II assays show legacy firms still innovating within serology. Smaller disruptors like T2 Biosystems target early infection with direct-detection panels that sidestep antibody lag, offering 30-day post-bite coverage. AI-driven startups integrate cloud analytics with smartphone readers, differentiating on user experience rather than reagent chemistry.

The FDA's new special controls for molecular FISH devices ease entry for nucleic-acid platforms, widening the field for mid-sized entrants, while M&A activity such as Quest Diagnostics' USD 985 million acquisition of LifeLabs expands specimen-collection networks across Canada and the U.S. and pressures regional labs to consolidate. Vendors increasingly bundle test kits with digital interpretation software and telemedicine follow-ups, signaling the convergence of diagnostics and virtual care in the Lyme disease diagnostics market.

Lyme Disease Diagnostic Industry Leaders

T2 Biosystems, Inc

Bio-Rad Laboratories

Oxford Immunotec USA, Inc

ROCHE DIAGNOSTICS INTERNATIONAL LTD

Abbott

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: En Carta Diagnostics SA raised EUR 1.5 million to advance point-of-care molecular kits for early Lyme detection.

- March 2025: Thermo Fisher and Bayer partnered to develop companion diagnostics across infectious diseases.

- January 2025: T2 Biosystems signed a letter of intent with ECO Laboratory to launch the T2Lyme Panel for detection within 30 days post-infection.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global Lyme disease diagnostic market as all in-vitro test kits, instruments, and digital readers sold to detect Borrelia infections in human samples collected in hospitals, independent labs, physician offices, and emerging home-collection channels. Values are expressed at manufacturer selling price, net of rebates, and exclude any therapeutic or vector-control revenues.

Scope exclusion: animal testing products are outside the study.

Segmentation Overview

- By Test Type

- ELISA

- Western Blot

- PCR / NAAT

- Lateral Flow Assay (Rapid)

- ImmunoBlot

- Multiplex Microarray & Others

- By Technology

- Serologic (Antibody-based)

- Molecular

- Point-of-Care Platforms

- Multiplex Diagnostic Platforms

- Digital & AI-augmented Diagnostics

- By Sample Type

- Blood / Serum

- Cerebrospinal Fluid

- Urine

- Skin Biopsy

- Synovial Fluid

- By End User

- Hospitals & Clinics

- Diagnostic Laboratories

- Research Institutes

- Homecare / Direct-to-Consumer

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed infectious-disease clinicians, reference-lab managers, and product managers across North America, Germany, Japan, and Brazil. Conversations validated average test panels per suspected case, rapid kit adoption rates, and typical ASP erosion, enabling us to fine-tune regional coefficients and scenario bounds.

Desk Research

We gathered foundational incidence and testing-volume data from tier-1 public sources such as the US CDC tick-borne disease dashboard, ECDC surveillance reports, PubMed clinical studies, and country customs imports of ELISA and PCR reagents. Trade association briefs from AdvaMed, the German Diagnostics Industry Association, and peer-reviewed articles detailing sensitivity of modified two-tier algorithms further shaped baseline positivity assumptions. Paid intelligence assets, D&B Hoovers for manufacturer sales splits and Dow Jones Factiva for kit pricing moves, helped refine revenue pools. The sources listed illustrate our desk research spectrum; many additional references informed gap checks and clarifications.

Market-Sizing & Forecasting

A top-down construct starts with reported Lyme incidence, adjusts for under-diagnosis multipliers, and converts symptomatic caseloads into test demand through observed testing ratios. Revenue emerges after layering region-specific blended ASPs. Supplier roll-ups and channel checks act as a selective bottom-up sense check, with variances reconciled through weighted averaging. Key variables in the model include tick-habitat expansion indices, updated CDC/ECDC prevalence revisions, rapid-kit reimbursement shifts, average repeat-test frequency per patient, and the share of point-of-care platforms. Forecasts employ multivariate regression linking incidence growth, diagnostic guideline changes, and price learning curves, with coefficients stress-tested by our primary experts.

Data Validation & Update Cycle

Outputs undergo cross-tab checks against customs value trends and quarterly manufacturer disclosures; anomalies trigger analyst re-contact. Mordor refreshes the model annually and issues interim tweaks when guideline revisions or major product launches materially shift assumptions.

Why Our Lyme Disease Diagnostic Baseline Commands Reliability

Published estimates often diverge; definitions, caseload multipliers, and price assumptions seldom align.

Key gap drivers include broader inclusion of therapeutic revenues by some publishers, differing under-reporting multipliers, single-source ASP extrapolations, and longer refresh cadences that miss guideline updates. Areas where Mordor's disciplined scope and yearly re-validation keep numbers grounded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 630 million | Mordor Intelligence | - |

| USD 946 million | Global Consultancy A | Applies uniform 10× under-diagnosis factor and averages public-procurement ASPs only |

| USD 6.7 billion (2024) | Regional Consultancy B | Blends therapeutic and diagnostic revenues and counts veterinary tests |

| USD 9.8 billion (2024) | Trade Journal C | Uses survey-based price points, no incidence cross-check, last update mid-2023 |

Taken together, the comparison shows that Mordor's transparent scope boundaries, incidence-anchored demand build, and yearly review deliver a balanced, traceable baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the current value of the Lyme disease diagnostics market?

The market is valued at USD 663.67 million in 2026 and is forecast to climb to USD 860.82 million by 2031.

Which region holds the largest share of Lyme disease diagnostics revenue?

North America leads with 42.98% market share in 2025 because of long-standing endemicity and mature laboratory infrastructure.

Why are modified two-tier testing algorithms (MTTTA) gaining traction?

MTTTA workflows replace Western blots with second-step ELISAs, doubling early-stage detection sensitivity while keeping specificity high.

How fast is the home-collection testing segment growing?

Homecare and direct-to-consumer testing is projected to expand at a 7.58% CAGR through 2031 as patients seek convenient sampling kits.

What role does climate change play in Lyme disease diagnostics demand?

Warmer winters and longer summers expand tick habitats, driving sustained testing needs in newly affected regions worldwide.

Page last updated on: