Automotive Artificial Intelligence Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

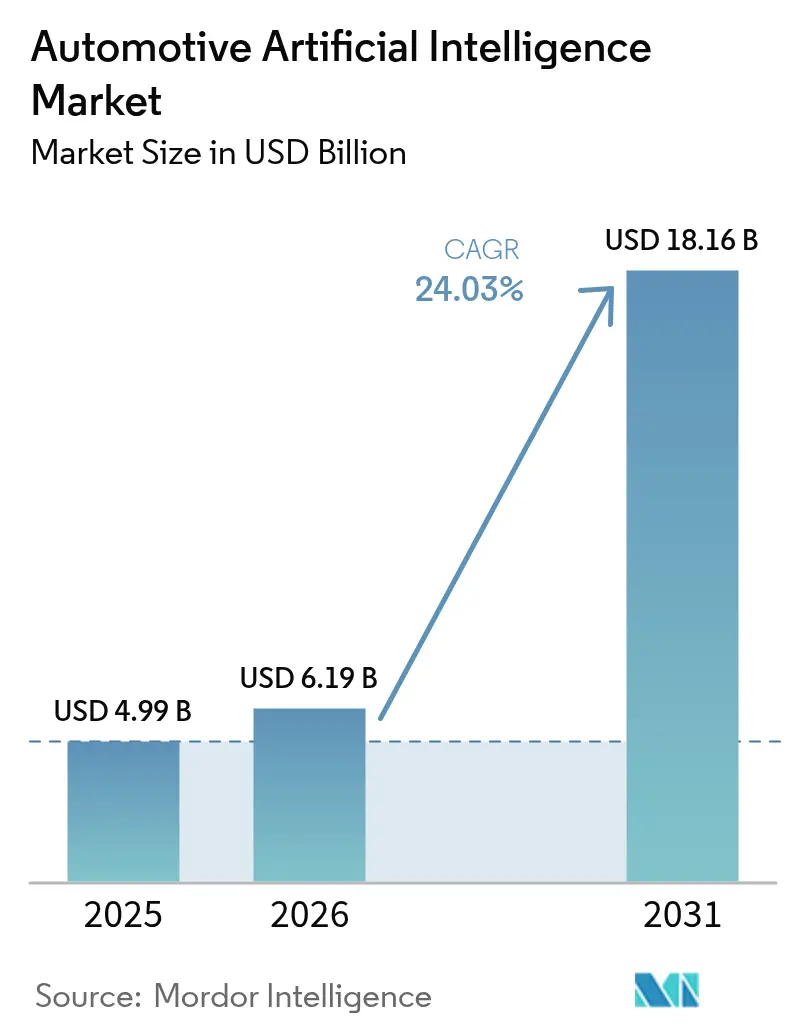

| Market Size (2026) | USD 6.19 Billion |

| Market Size (2031) | USD 18.16 Billion |

| Growth Rate (2026 - 2031) | 24.03% CAGR |

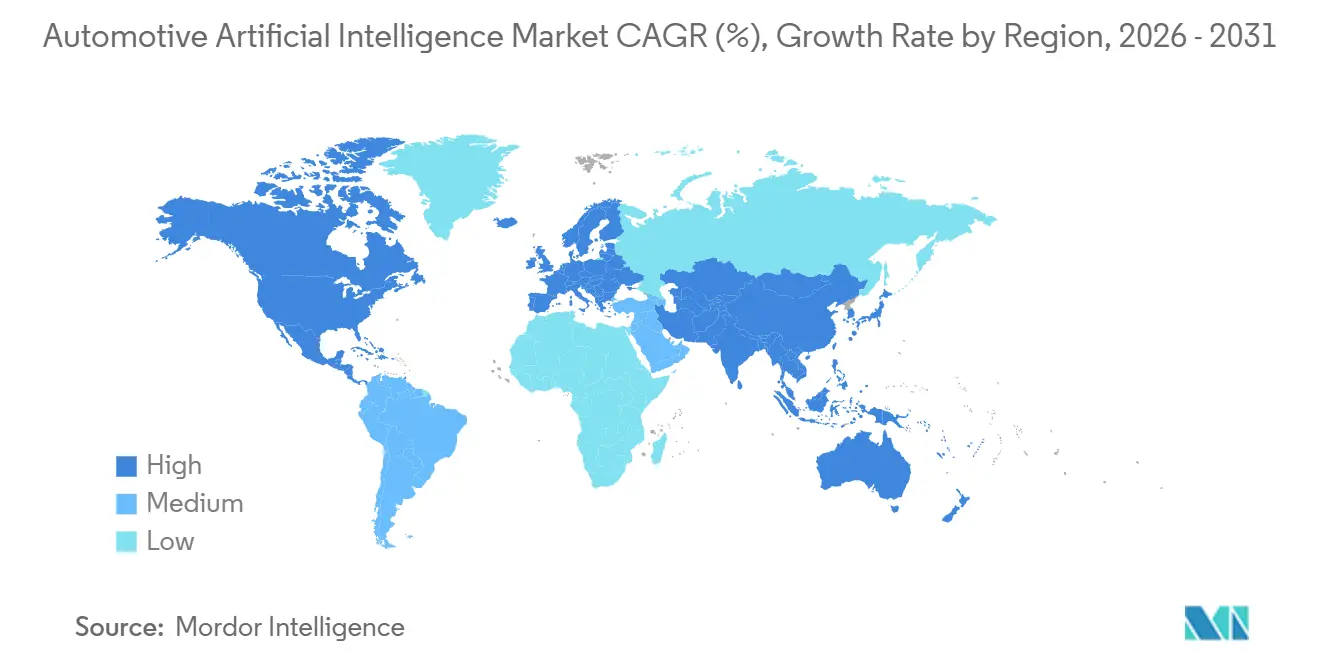

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

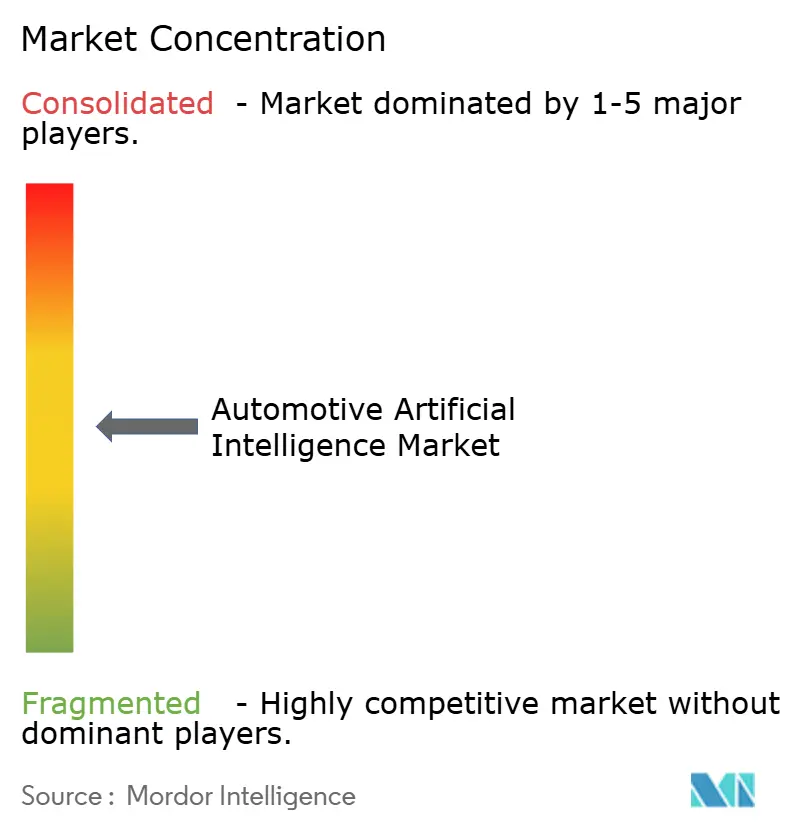

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Artificial Intelligence Market Analysis by Mordor Intelligence

The Automotive Artificial Intelligence Market size was valued at USD 4.99 billion in 2025 and is estimated to grow from USD 6.19 billion in 2026 to reach USD 18.16 billion by 2031, at a CAGR of 24.03% during the forecast period (2026-2031). Automakers are increasingly unlocking revenue by pushing software features to vehicles already on the road, moving away from a sole reliance on new-car sales. In recent years, software has become a significant contributor to global revenue. However, as chip costs decline, hardware accelerators are finding their way into mass-market models, leading to a broader adoption of camera, radar, and lidar perception. North America has emerged as a major revenue pool, bolstered by Tesla's extensive fleet of vehicles that continuously upload driving data. Meanwhile, the Asia-Pacific region is gaining momentum, fueled by China's sovereign-AI policies investing heavily in domestic compute infrastructure. Regulatory mandates, like the European Union's General Safety Regulation II and China's C-NCAP protocol, are pushing Level-2 safety functions into every new passenger car. This is compressing design cycles and shifting budgets towards on-device inference. As a result, the competitive landscape is transitioning from a focus on hardware design to monetizing features via over-the-air updates, benefiting vertically integrated players.

Key Report Takeaways

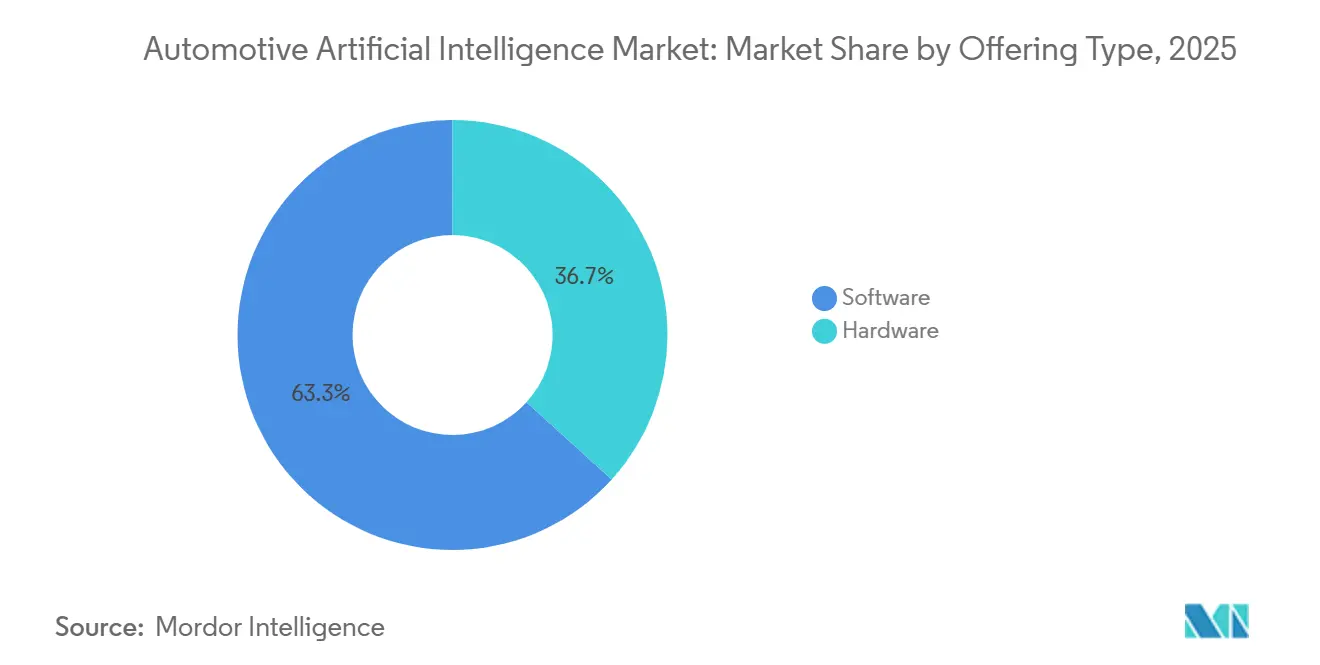

- By offering, software led with 63.28% revenue share in 2025, while hardware is projected to advance at a 24.05% CAGR through 2031.

- By technology, classical machine learning held 43.37% of 2025 revenue, whereas deep learning is set to expand at a 24.07% CAGR through 2031.

- By process, image recognition accounted for 46.14% of 2025 revenue, and data mining is forecast to grow at a 24.13% CAGR to 2031.

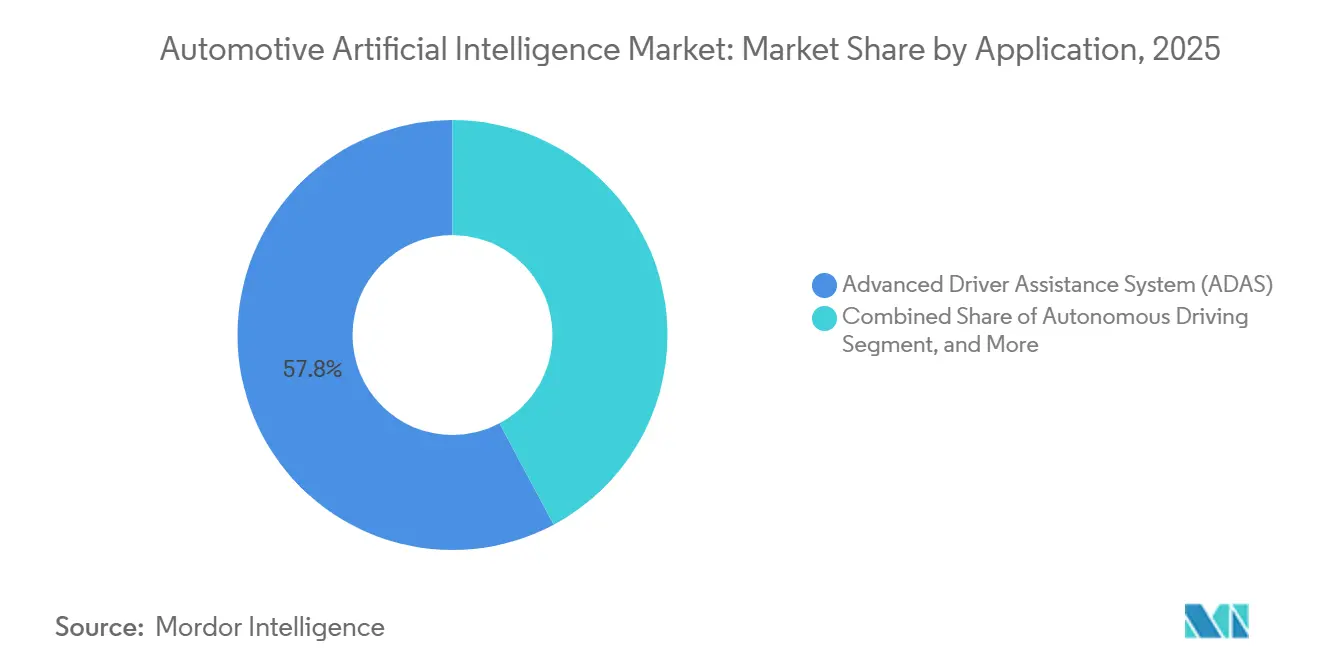

- By application, advanced driver-assistance systems commanded 57.83% of 2025 revenue, while autonomous driving is poised for a 24.11% CAGR over 2026-2031.

- By vehicle type, passenger cars accounted for 68.81% of 2025 revenue, yet light commercial vehicles are expected to grow at a 24.17% CAGR through 2031.

- By geography, North America accounted for 37.16% of 2025 revenue, while Asia-Pacific is projected to post the fastest growth, with a 24.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Artificial Intelligence Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Mandates for Level-2+ ADAS Safety Features | +5.2% | Global, with EU and China leading enforcement | Short term (≤ 2 years) |

| Rapid Decline in AI-compute and TOPS for Automotive SoCs | +4.8% | North America and Asia-Pacific core, spillover to EU | Medium term (2-4 years) |

| Explosion of Over-the-air (OTA) SW Updates Enabling AI Feature Monetization | +4.1% | North America and China, early adoption in premium segments | Medium term (2-4 years) |

| Fleet-learning Architectures Accelerating Perception Model Accuracy | +3.6% | North America and China, limited in EU due to GDPR constraints | Long term (≥ 4 years) |

| Emerging Chiplet-Based ECUs Lowering BOM | +3.1% | Asia-Pacific core, North America following | Medium term (2-4 years) |

| On-device Multimodal Foundation Models Reducing Cloud Dependency | +2.9% | Global, with faster adoption in markets with weak connectivity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates for Level-2+ ADAS Safety Features

Regulators worldwide now view automated braking, lane-keeping, and driver-monitoring as standard equipment rather than premium options. The European Union’s General Safety Regulation II has required these functions on every new passenger car since July 2024, guaranteeing an annual base of almost 18 million units that must integrate AI inference chips. In China, the C-NCAP 2024 protocol awards zero stars to models lacking AI-powered pedestrian detection, effectively barring non-compliant cars from the market. The U.S. National Highway Traffic Safety Administration followed in December 2025 by proposing compulsory automatic emergency braking for all light vehicles from model year 2029. Such mandates shorten the payback period for ADAS investments from 7 years to roughly 3, making AI a board-level priority for automakers.

Rapid Decline in AI-compute and TOPS for Automotive SoCs

The cost per tera-operation has plunged 68% since 2024, due to advanced packaging and chiplet designs. Qualcomm’s Snapdragon Ride Flex launched in March 2025 with 2,000 TOPS at a USD 450 bill of materials cost, yet still meets ISO 26262 ASIL-D requirements [1]“Snapdragon Ride Flex Technical Brief,” Qualcomm, qualcomm.com . Horizon Robotics’ Journey-6 ships at 1,200 TOPS for USD 280, enabling Chinese brands to offer Level-2+ functions in sub-USD 25,000 cars [2]“Journey-6 Product Launch,” Horizon Robotics, horizon.cc . Intel’s Mobileye conceded the trend in September 2025, announcing chiplet adoption for EyeQ Ultra by 2027. As computing becomes commoditized, value shifts to software ecosystems rather than pure silicon design.

Explosion of Over-the-air Software Updates Enabling AI Feature Monetization

Recurring subscriptions now rewrite vehicle economics. Tesla generated USD 1.8 billion from Full Self-Driving subscriptions in 2025 by improving lane-change accuracy each month. General Motors’ OnStar Intelligence, launched mid-2025 at USD 25 per month, attracted 1.2 million subscribers by year-end. Mercedes-Benz began offering U.S. drivers Level-3 Drive Pilot for USD 2,500 annually in January 2026. These services deliver software margins near 70%, pressuring tier-1 suppliers that rely on traditional hardware sales.

Fleet-learning Architectures Accelerating Perception Accuracy

In 2025, Waymo's robotaxis in San Francisco and Phoenix traveled significant distances without a driver, achieving an impressively low disengagement rate. Meanwhile, Tesla's Shadow Mode identified numerous new edge cases from its extensive fleet, integrating these insights into its training for the upcoming software release. China is speeding up this data-sharing cycle, permitting anonymized sensor data sharing among brands. This collaboration enables companies like BYD and Geely to jointly refine their perception models. In contrast, Europe's GDPR regulations hinder similar data pooling efforts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Functional-Safety Regulations Across Jurisdictions | -2.8% | Global, with EU, US, and China enforcing divergent standards | Long term (≥ 4 years) |

| High Validation Cost of AI Models for Edge-case Scenarios | -2.3% | North America and EU, where liability frameworks demand exhaustive testing | Medium term (2-4 years) |

| Persistent Scarcity of Automotive-grade AI Talent | -1.6% | Global, acute in Europe and Japan | Long term (≥ 4 years) |

| Supply-chain Exposure to Advanced-node Foundry Capacity | -1.4% | Global, with dependencies on TSMC and Samsung | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Functional-Safety Regulations Across Jurisdictions

Regulatory fragmentation is driving up costs and delaying product releases. For instance, obtaining ISO 26262 certification for a single ADAS feature requires significant financial investment. Meanwhile, China's GB/T 34590 standard extends timelines due to additional cybersecurity testing. In the U.S., guidance remains optional, in contrast to Euro NCAP's mandate for pedestrian-protection scenarios. As a result of these fragmented regulations, Continental faced substantial expenses in the projected period.

High Validation Cost of AI Models for Rare Edge Cases

Waymo revealed it invested a significant amount to simulate billions of miles for its San Francisco deployment. In 2025, Aurora Innovation, after allocating substantial resources to validation, decided to delay its roll-out. These considerable expenditures not only deter smaller players but also bolster the position of established firms with more robust balance sheets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Dominates, Hardware Accelerates

Software accounted for 63.28% of the share in 2025, driven by monthly feature releases that keep cars current for years after purchase. Meanwhile, Hardware is slated to grow at a 24.05% CAGR because chiplet accelerators lower costs to the point that Level-2 functions can reach sub-USD 25,000 vehicles. The Automotive Artificial Intelligence market size for the hardware segment is forecast to more than triple between 2026 and 2031, underlining a pivotal shift in bill-of-materials priorities.

Over the forecast horizon, automakers bring algorithm design in-house to secure annuity revenue, squeezing legacy tier-1s that once bundled software with cameras and radars. Mercedes-Benz canceled a USD 400 million external contract in January 2025 and set up its own Level-3 code base. Suppliers counter by bundling cloud services: Qualcomm ties every Snapdragon Ride Flex sale to a five-year AWS SageMaker subscription so models can be retrained without swapping chips. NVIDIA’s Drive Orin pushes a 7-billion-parameter vision-language model on the device, cutting cellular data charges that previously eroded lease margins.

By Technology: Deep Learning Surges Past Classical Approaches

Classical machine learning still accounted for 43.37% of the market in 2025, but transformer-based deep learning models are advancing at a 24.07% CAGR. Waymo’s 12-layer transformer stack processed 1.4 GB per second of sensor data, paring disengagements to 0.09 per 1,000 miles. Tesla’s end-to-end neural network in FSD Beta v12 replaced hand-coded rules, boosting recall in construction zones from 89% to 96%. Consequently, the Automotive Artificial Intelligence market share of vendors reliant on classical features shrank eight percentage points last year.

Computer vision accounted for 28% of technology revenue as Euro NCAP and C-NCAP mandate multi-camera arrays in every new vehicle. Natural-language processing reached 12%, reflecting the rise of voice assistants that reduce distractions. Context awareness held 9% but is on a steep incline because predictive cruise control now adjusts speed hundreds of meters ahead of curves, trimming brake wear and raising fuel efficiency. As large multimodal models converge camera, radar, and lidar inputs, software stacks that once resided in separate ECUs are consolidating, simplifying wiring and reducing power consumption.

By Process: Image Recognition Leads, Data Mining Gains Momentum

Image recognition led with 46.14% of 2025 revenue on the back of mandated surround-view cameras. Signal recognition followed at 31%. Data mining, however, is growing fastest at a 24.13% CAGR as automakers monetize the oceans of sensor logs generated each day. Tesla’s Shadow Mode captured 18,000 new edge cases in 2025, condensing development cycles from 18 months to six. The Automotive Artificial Intelligence market size tied to data-mining platforms is therefore on a steeper trajectory than that of pure perception.

Companies now treat raw driving data as an asset class. General Motors started licensing anonymized logs to insurers such as Allstate in 2025, creating USD 120 million in high-margin revenue. Chinese policy supports data pooling across brands, enabling BYD and Geely to improve pedestrian detection by 22% in low-light conditions; Europe’s GDPR blocks such collaborations, placing EU automakers at a disadvantage.

By Application: Autonomous Driving Closes the Gap on ADAS

Advanced driver-assistance systems controlled 57.83% of 2025 revenue because regulators made Level-2 functionality mandatory. Autonomous driving, nevertheless, is the fastest application, expected to grow at a 24.11% CAGR after Waymo’s fleets recorded 2.4 million incident-free driverless miles. Voice and gesture control, now standard, contributed significantly to the revenue in human-machine-interface features. Meanwhile, platforms such as GM's OnStar Intelligence played a key role in driving the share of revenue from predictive maintenance.

Regulatory definitions lag technology. Mercedes-Benz Drive Pilot lets drivers look away at speeds below 40 mph, but it is confined to certain highways. BMW Highway Assistant delivers hands-free travel up to 85 mph but remains classified as Level-2 because driver supervision is required. Predictive maintenance emerges as a lucrative add-on, with Bosch’s diagnostics suite cutting warranty claims 18% for participating automakers. These trends suggest the Automotive Artificial Intelligence market will increasingly revolve around ongoing service revenue rather than one-time option packages.

By Vehicle Type: Light Commercial Fleets Gain Speed

Passenger cars accounted for 68.81% of 2025 revenue, driven by global unit volume and safety mandates. Light commercial vehicles, however, are projected to grow at a 24.17% CAGR, buoyed by fleet operators that can justify AI retrofits through measurable fuel and routing savings. In the mid-2020s, Amazon outfitted a significant number of vans with driver-monitoring cameras, achieving notable reductions in fuel consumption. UPS, on the other hand, reported substantial annual savings from AI-driven route optimization, recovering its investments in a relatively short period. Despite these advancements, heavy commercial vehicles account for only a small share of revenue, primarily due to ongoing challenges in obtaining regulatory clearance for driverless trucking.

While fleets distribute their AI expenditures across numerous vehicles, individual consumers face higher prices. As a result, the competitive landscape is shifting towards subscription bundles, emphasizing a reduced total cost of ownership over mere purchase incentives. With hardware costs declining, the trend indicates that by the decade's close, the Automotive Artificial Intelligence market will pivot more towards vans and mid-duty trucks.

Geography Analysis

North America contributed 37.16% of 2025 revenue, buoyed by Tesla's established presence and Waymo's commercial robotaxis. A forthcoming NHTSA regulation is set to equip millions of U.S. light trucks with automatic braking by the end of the decade, presenting a lucrative opportunity for sensor suppliers. With the majority of its population now covered by 5G, Canada is leveraging low-latency V2X communication to successfully reduce intersection crashes during field trials. However, the fragmented liability statutes across states are hindering the rollout of Level-3 technology.

Asia-Pacific is projected to expand by 24.15%, spurred by China's substantial push into domestic computing to lessen its dependence on imported GPUs [3]“AI Infrastructure Investment Plan,” National Development and Reform Commission (China), ndrc.gov.cn . Horizon Robotics made waves in 2025, shipping a significant number of Journey-6 SoCs and capturing a notable portion of China's ADAS market. In a bid to tackle driver shortages, Japan greenlit Level 4 autonomous buses for several rural routes. Meanwhile, South Korea's Hyundai Mobis is making a significant move with a major investment in an R&D campus focused on transformer-based perception. Despite these advancements, India lags, with federal safety mandates still voluntary. However, Tata Motors has ambitious plans, aiming to equip all cars priced above a certain threshold with Level-2 features starting in the latter part of the decade.

Europe, which contributes a considerable share of 2025 revenue, grapples with slower growth due to data-pooling constraints under GDPR. Mercedes-Benz's Drive Pilot enrolled a modest number of subscribers during its inaugural period. While Germany granted numerous testing permits for autonomous vehicles in 2025, commercial operations remain restricted to geofenced areas. The U.K.'s Automated Vehicles Act has clarified automaker liability, energizing London-based Wayve to secure substantial funding for its embodied-AI platform. In the Middle East and Africa, which together accounted for a small share of revenue, Dubai is ambitiously targeting that 50% of trips be driverless by 2030. Yet challenges such as desert heat and limited HD mapping continue to hinder progress.

Competitive Landscape

The Automotive Artificial Intelligence market is moderately concentrated. The top five players—Tesla, Waymo, NVIDIA, Mobileye, and Horizon Robotics—accounted for nearly half of the projected revenue in the mid-term. Tesla's unique blend of custom silicon, fleet-learning, and direct software billing has enabled it to achieve subscription margins that elude brands dependent on dealers. Waymo's robotaxis operate at a significantly lower cost compared to standard ride-hailing services, underscoring their economic viability in bustling urban centers. NVIDIA's Drive Orin, featuring a highly advanced vision-language model, is strategically placed in vehicles to reduce data fees. However, it faces substantial pricing competition from Qualcomm's Ride Flex.

Chip designers are increasingly integrating software into their offerings to secure consistent revenue streams. Meanwhile, tier-1 companies are acquiring startups to bridge the gap. Qualcomm's acquisition of Arriver resulted in the development of Ride Flex, a comprehensive hardware and middleware solution. In a similar vein, Continental's investment in Recogni was aimed at addressing a silicon shortfall.

Applied Intuition, with significant funding, is positioning itself in the simulation-as-a-service arena, a validation niche underscored by Aurora's decision to halt a major expenditure. Patent filings highlight contrasting strategies: NVIDIA recently secured a substantial number of patents centered on transformer perception, while Mobileye focused on responsibility-sensitive safety with a notable number of patents.

Automotive Artificial Intelligence Industry Leaders

NVIDIA Corporation

Continental AG

Tesla Inc.

Mobileye Vision Technologies Ltd

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Helm.ai, backed by Honda, unveiled a cutting-edge vision system for autonomous vehicles, expanding Honda's perception portfolio and highlighting a closer collaboration between the OEM and the start-up.

- April 2025: BMW announced the integration of Deep Seek AI into future China-market vehicles, underscoring the need for localized intelligent-cabin solutions.

- March 2025: Magna, in collaboration with NVIDIA, is embedding DRIVE Thor into safety systems, covering Levels 2+ to 4.

Global Automotive Artificial Intelligence Market Report Scope

The scope of the report includes Offering (Hardware and Software), Technology (Machine Learning, Deep Learning, and More), Process (Data Mining and More), Application (Autonomous Driving and More), Vehicle Type (Passenger Cars, Light Commercial, and Heavy Commercial), and Geography.

| Hardware |

| Software |

| Machine Learning |

| Deep Learning |

| Computer Vision |

| Natural Language Processing |

| Context Awareness |

| Data Mining |

| Image Recognition |

| Signal Recognition |

| Autonomous Driving |

| Advanced Driver-Assistance Systems (ADAS) |

| Human-Machine Interface |

| Predictive Maintenance & Diagnostics |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Offering | Hardware | |

| Software | ||

| By Technology | Machine Learning | |

| Deep Learning | ||

| Computer Vision | ||

| Natural Language Processing | ||

| Context Awareness | ||

| By Process | Data Mining | |

| Image Recognition | ||

| Signal Recognition | ||

| By Application | Autonomous Driving | |

| Advanced Driver-Assistance Systems (ADAS) | ||

| Human-Machine Interface | ||

| Predictive Maintenance & Diagnostics | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What revenue will software subscriptions contribute by 2031?

Recurring software is forecast to remain above 60% of the overall Automotive Artificial Intelligence market, with hardware gains coming mainly from cheaper chiplets rather than margin expansion.

Which region is growing fastest through 2031?

Asia-Pacific, propelled by China’s sovereign-AI spending, is projected to post a 24.15% CAGR over the period.

How do chiplet architectures change vehicle cost structures?

They cut the bill of materials for high-performance ECUs by as much as 60%, enabling Level-2+ functions in vehicles priced below USD 25,000.

Why are light commercial vehicles adopting AI faster than heavy trucks?

Fleet operators realize immediate fuel and routing savings and face fewer regulatory hurdles than fully driverless long-haul trucks.

What is the primary barrier to global autonomous deployment?

Divergent functional-safety rules across jurisdictions force parallel validation tracks, adding USD 15 million or more per feature and delaying releases.

Page last updated on: