Automotive Digital Cockpit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

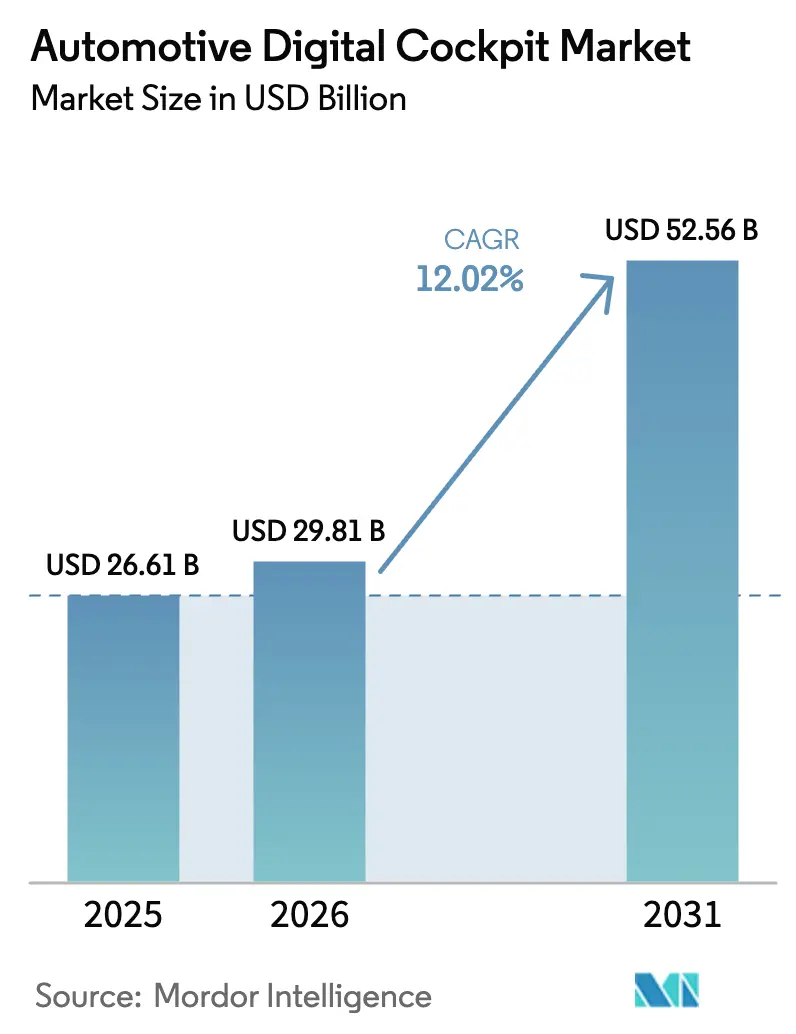

| Market Size (2026) | USD 29.81 Billion |

| Market Size (2031) | USD 52.56 Billion |

| Growth Rate (2026 - 2031) | 12.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Digital Cockpit Market Analysis by Mordor Intelligence

Automotive digital cockpit market size in 2026 is estimated at USD 29.81 billion, growing from 2025 value of USD 26.61 billion with 2031 projections showing USD 52.56 billion, growing at 12.02% CAGR over 2026-2031. The market’s growth is anchored in the automotive shift toward software-defined vehicles, tightening safety mandates, and mounting consumer expectations for seamless in-car connectivity. Carmakers are merging infotainment, driver-assistance, and vehicle controls into domain controller platforms that lower the bill of materials cost while supporting over-the-air upgrades. Battery-electric architectures accelerate adoption by supplying the power and network bandwidth needed for high-resolution displays and AI functions. Competitive intensity is rising as semiconductor vendors, display specialists, and traditional Tier-1s all vie to supply next-generation cockpits, prompting automakers to favor long-term platform agreements that assure cybersecurity compliance and functional-safety certification.

Key Report Takeaways

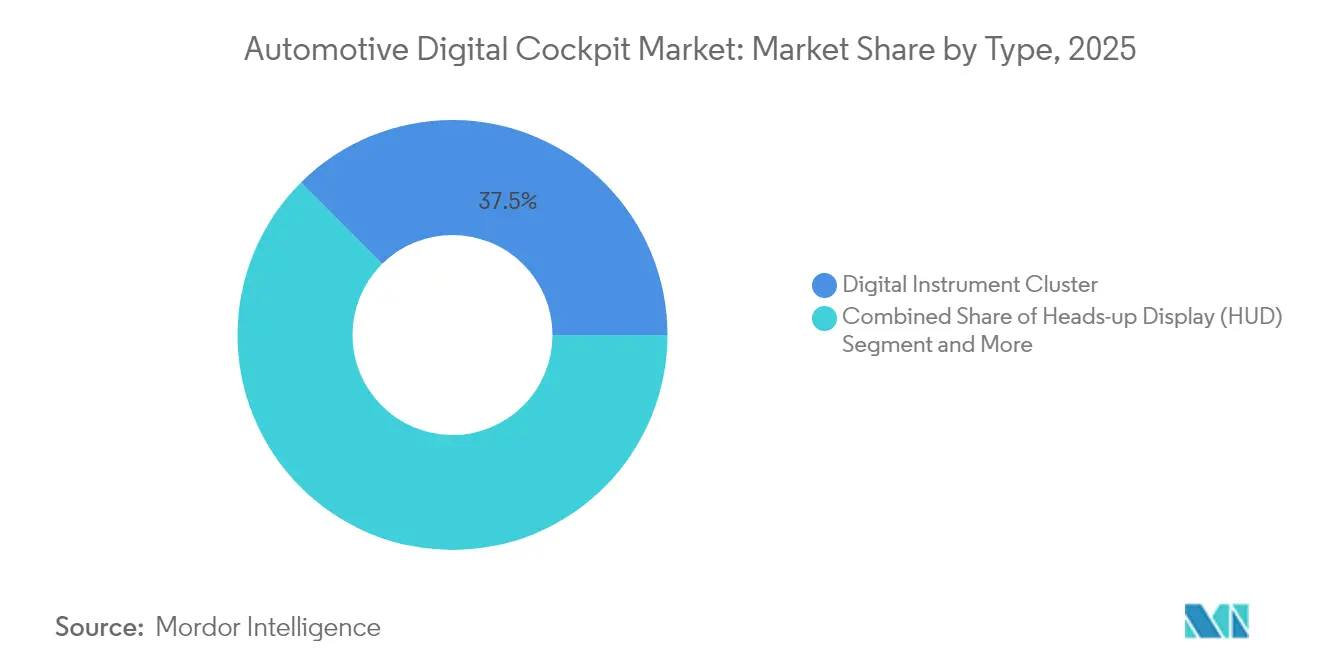

- By type, digital instrument clusters led the automotive digital cockpit market share by 37.45% in 2025, while heads-up displays are set to expand at an 18.05% CAGR to 2031.

- By vehicle type, passenger cars accounted for 68.89% of the automotive digital cockpit market size in 2025; light commercial vehicles show the fastest growth at 14.33% CAGR through 2031.

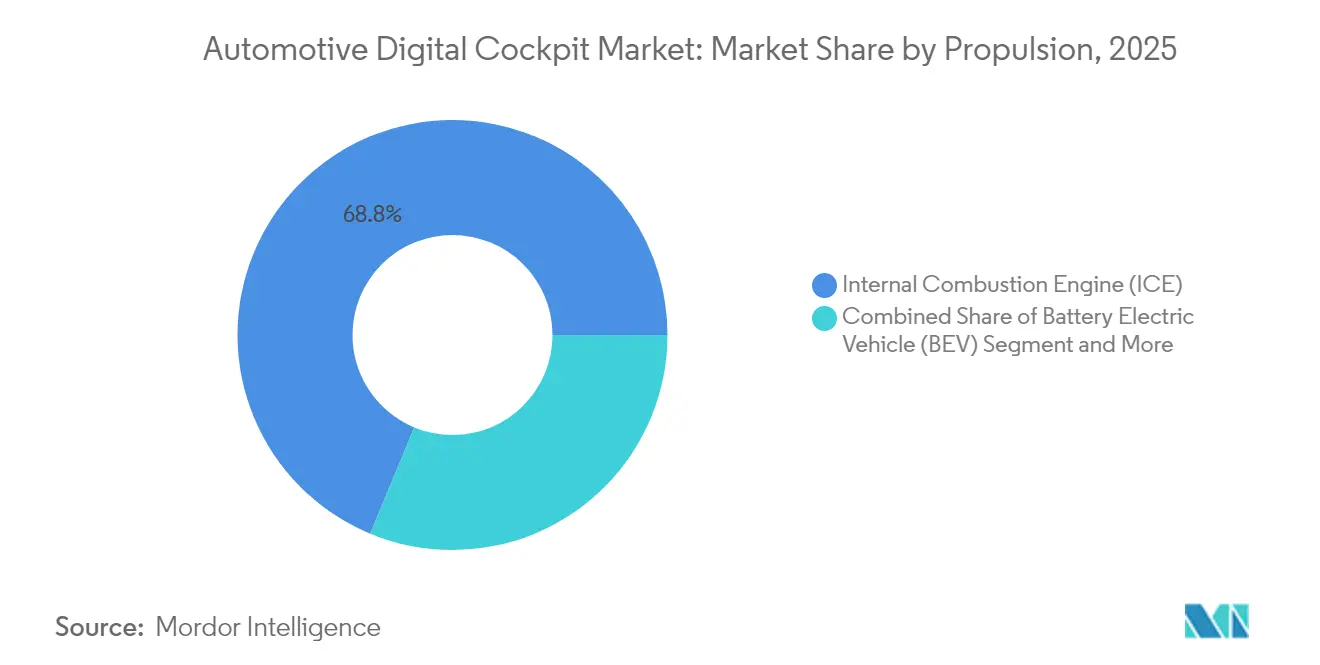

- By propulsion, ICE vehicles captured 68.75% of the automotive digital cockpit market size in 2025, while battery electric vehicles (BEVs) are advancing at an 18.05% CAGR to 2031.

- By sales channel, the OEM-fitted segment held 91.25% of the automotive digital cockpit market's revenue share in 2025, outpacing aftermarket solutions with a 13.58% CAGR.

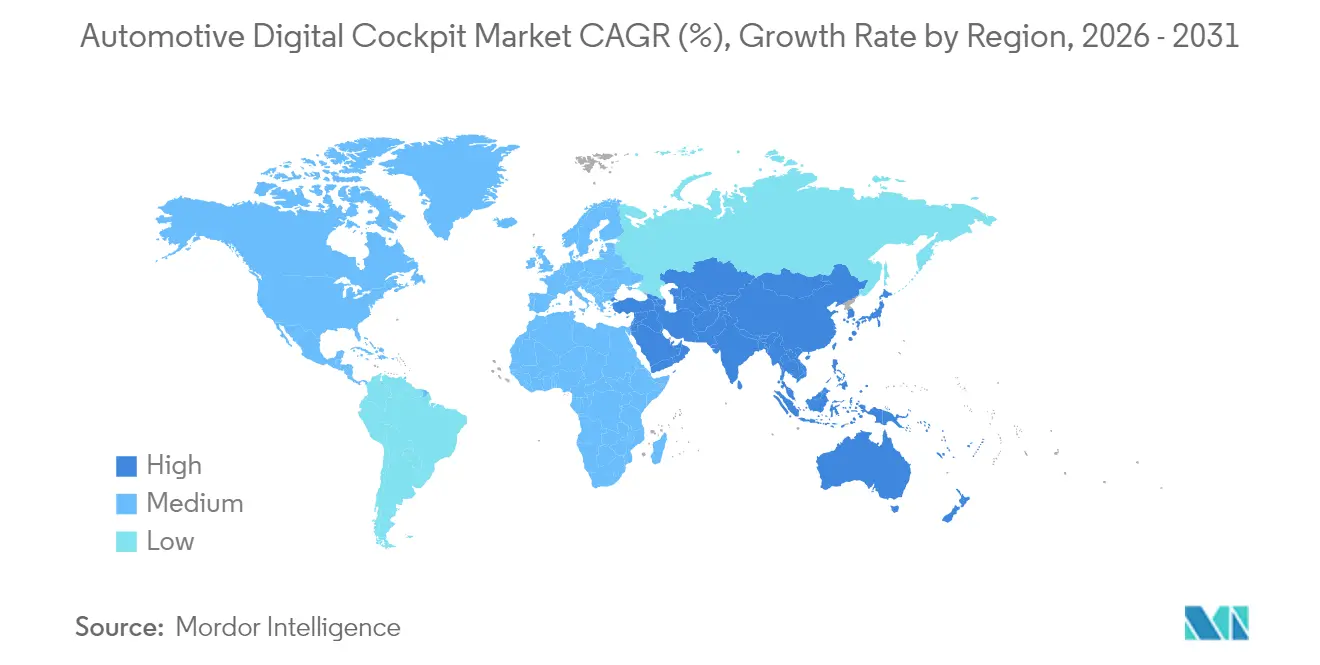

- By region, Asia-Pacific commanded 39.42% of the automotive digital cockpit market share in 2025 and is projected to grow at a 14.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Digital Cockpit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Immersive Infotainment Demand | +3.2% | Global, with premium adoption in North America and Europe | Medium term (2-4 years) |

| Mandatory ADAS and Safety Regulations | +2.8% | Global, led by EU GSR II and NHTSA requirements | Short term (≤ 2 years) |

| EV Software-Defined Cockpits | +2.1% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Centralized Domain Controllers | +1.8% | Global, with early adoption in premium segments | Medium term (2-4 years) |

| In-car Subscription Revenue | +1.4% | North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| Android Automotive Adoption | +0.9% | Global, with accelerated adoption in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Consumer Appetite for Immersive Infotainment

Carmakers are designing cabins around multi-screen layouts and AI voice assistants that mimic smartphone experiences. TCL CSOT’s panoramic HUD and 32:9 center displays preview the next design language, while Honda’s forthcoming ASIMO OS embeds machine-learning personalization. Content partnerships, such as Visteon–TuneIn, add streaming media to the dashboard. Premium brands further reinforce the trend. For instance, Audi’s A6 Sportback e-tron combines an 11.9-inch virtual cluster with a 14.5-inch OLED touch screen for vivid graphics.

Mandatory ADAS and Safety Regulations

Regulatory mandates are catalyzing the integration of advanced driver assistance systems with digital cockpit platforms, creating synergies that enhance both safety and user experience while reducing system complexity. EU General Safety Regulation II updates require mandatory advanced driver-assistance features in all passenger vehicles, all of which must present intuitive, real-time alerts. Qualcomm and Bosch responded with a mixed-criticality computer that hosts infotainment and ADAS workloads on one SoC, reducing latency and wiring. This convergence is further accelerated by functional safety standards like ISO 26262 ASIL-B compliance requirements, which are driving innovation in display technologies and LED driver architectures.

EV Platforms Favoring Software-Defined Cockpits

Electric vehicles provide centralized power and Ethernet backbones that consolidate more than 50 ECUs into a few domain controllers, a shift Intel claims cuts wiring length by 60% while freeing energy for high-bandwidth displays. Stellantis projects software revenue to reach EUR 20 billion by 2030 on the back of cockpit-based digital services. Chinese OEMs are further amplifying the trend by leveraging software-defined cockpits to differentiate their offerings.

Centralized Domain Controllers Slashing BOM Cost

Moving infotainment, ADAS, and cluster rendering onto a single board lowers component count, validation cycles, and long-term maintenance. The cost benefits extend beyond hardware to software development and maintenance, as centralized platforms enable shared computing resources and simplified over-the-air update mechanisms. Infineon and MediaTek’s entry-level reference design meets ASIL-B and demonstrates how mass-market vehicles gain access to multi-display packages while shaving up-front cost.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System Cost | -2.1% | Global, with acute impact on emerging markets | Short term (≤ 2 years) |

| Cybersecurity and Data-Privacy Risk | -1.8% | North America and EU, expanding globally | Medium term (2-4 years) |

| Advanced-Node SoC Shortages | -1.6% | Global, with critical impact on premium segments | Short term (≤ 2 years) |

| Driver-Distraction Regulations | -1.2% | EU and North America, with regulatory spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront System and Validation Cost

Achieving ISO 26262 ASIL-B for cockpit displays demands redundant power rails, fault-injection testing, and exhaustive software audits, all of which inflate non-recurring engineering spend. HARMAN alone employs more than 500 engineers on cockpit programs, underscoring the labor intensity. Smaller OEMs delay rollouts, and some legacy models were withdrawn in Europe when new cybersecurity rules took effect in 2024.

Escalating Vehicle-Cybersecurity and Data-Privacy Liabilities

UN ECE R155/R156 rules and equivalent EU statutes oblige automakers to patch vulnerabilities for at least 10 years, raising recurring costs. BlackBerry’s expanded tie-up with Marelli shows the move toward hardened micro-kernels and intrusion-detection gateways inside the cockpit. Data-privacy provisions now require on-screen consent flows and localized cloud storage, adding software complexity but opening service revenue for compliance tools.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Multi-Screen Integration Drives Premium Adoption

In 2025, digital instrument clusters commanded a 37.45% of the automotive digital cockpit market share, serving as the primary interface for speed, range, and ADAS alerts. Heads-up displays, however, are setting the pace with an 18.05% CAGR, pushed by OEM demand for augmented-reality overlays that keep drivers’ eyes forward. The digital cockpit market is also shifting toward panoramic CIDs, passenger-indulgent PIDs, and camera-based driver-monitoring modules that help satisfy Euro NCAP driver-attention ratings.

Center stack screens now stretch beyond 15 inches, enabled by higher pixel densities and low-power LTPO backplanes that limit heat. Envisics’ second-generation holographic HUD debuted in GM’s 2024 Cadillac Lyriq, highlighting cross-segment trickle-down of once-premium tech. TCL CSOT’s 32:9 combo display merges cluster and infotainment on a single surface, heralding further component consolidation. Growing demand for immersive experiences guarantees that multi-display packages remain a growth lever for the digital cockpit market.

By Vehicle Type: Commercial Segments Accelerate Digitalization

In 2025, passenger cars led the automotive digital cockpit market, securing a 68.89% share and witnessing a 13.92% annual growth. Consumers now expect the same cloud-linked services in a compact hatchback that they once saw only in luxury sedans, forcing volume brands to stretch cockpit feature lists. Digital cockpit market adoption in light commercial vehicles is quickening as fleets seek telematics integration that pairs route planning with driver-condition monitoring.

Medium and heavy trucks increasingly require electronic logging devices, and domain-controller cockpits satisfy this mandate while supporting predictive maintenance analytics. BYD’s roll-out of 21 models with self-developed cockpit chips demonstrates how cost-optimized designs are scaling into workhorse vans and pickups. This divergence means light commercial vehicles may outpace passenger cars in incremental unit growth, even though the latter still dominate the digital cockpit market size.

By Propulsion: Electric Platforms Enable Advanced Integration

In 2025, internal-combustion vehicles commanded a dominant 68.75% share of the automotive digital cockpit market. Yet, many new ICE models now arrive with over-the-air-ready domain controllers to future-proof cabin electronics. Battery-electric vehicles are projected to register the fastest growth rate of 18.05% through 2031 as flat-floor architectures make room for larger displays and zonal power distribution. EV platforms supply stable 48-V or high-voltage rails that simplify active-matrix mini-LED backlighting and GPU-rich compute clusters.

Hybrids act as a bridge, sharing EV conveniences like plug-in firmware upgrades while leveraging existing 12-V harnesses. The shift toward electrification accelerates cockpit innovation, as automakers leverage the clean-sheet design opportunities presented by EV platforms to implement next-generation cockpit architectures that would be difficult to retrofit into conventional vehicles.

By Sales Channel: OEM Integration Dominates Market Strategy

In 2025, OEM-installed systems dominated the automotive digital cockpit market with a 91.25% share and are projected to grow at a 13.58% CAGR due to their alignment with vehicle-wide E/E architecture. Automakers validate cybersecurity, functional safety, and user-interface consistency before a model ever leaves the plant, eliminating many integration pitfalls seen in retrofits.

Aftermarket demand persists, served by niche upgrade specialists offering 12.3-inch TFT clusters for recent pickups or luxury SUVs. Yet rising encryption of in-vehicle networks and central-compute architectures mean retrofit options are shrinking. Consequently, future digital cockpit market volume will remain OEM-centric, with aftermarket channels focusing on accessories rather than full domain-controller replacements.

Geography Analysis

In 2025, the Asia-Pacific region dominated the digital cockpit market, accounting for 39.42% of global revenues. Projections indicate a robust growth rate of 14.44% CAGR for the region, extending through 2031. China’s EV boom, propelled by aggressive subsidies and local component ecosystems, has turned domestic brands into cockpit technology exporters; Volkswagen, GM, and Nissan have licensed Chinese HMI stacks for local-market variants. Japan reinforces the region’s software push: DENSO plans to quadruple software revenue to JPY 800 billion by 2035, and Toyota’s Arene OS aims to deliver cross-model cabin experiences.

Europe is projected to maintain a medium pace, driven by the continent’s leadership in premium marques that anchor cockpit R&D budgets. EU General Safety Regulation II forces the adoption of smart clusters capable of presenting mandatory warnings. Yet compliance costs remain high; several low-volume models exited production in 2024 after cybersecurity rules took effect. German OEMs counter by concentrating resources on digital-first platforms such as BMW’s NEUE KLASSE, which prioritizes user-centric HUDs over analog gauges.

North America is expected to deliver a steady 8.94% CAGR. The region’s large SUV and pickup segments demand high-brightness displays visible under direct sunlight, spurring innovation in optical bonding and anti-reflective coatings. NHTSA’s broadened NCAP adds blind-spot, lane-keep, and pedestrian braking criteria, effectively mandating advanced HMIs. Meanwhile, Stellantis’ USD-denominated software revenue goals illustrate how cockpit-tied digital services can become a core margin contributor.

Competitive Landscape

Market concentration is moderate, with the top five suppliers holding around half of the combined share, leaving white-space for specialized display, OS, and cybersecurity entrants. Continental, Bosch and DENSO are the top performers, while technology companies like Qualcomm are rapidly gaining ground through semiconductor platforms that enable next-generation cockpit functionality.

Strategic alliances define the field. Bosch and Qualcomm unveiled a scalable central computer that merges infotainment and ADAS, allowing automakers to tier features via software licenses. Continental plans to spin off its Automotive Technologies unit, freeing capital to intensify investment in immersive HMIs and secure-by-design software.

Furthermore, HARMAN maintains a 500-engineer cockpit practice and recently became an Android Auto certification partner, ensuring rapid integration of Google apps. Patent filings focus on augmented-reality visualization and haptic feedback, as illustrated by a keyboard-driven tactile interface patent that could migrate from consumer electronics to vehicles. The convergence of software, silicon, and optics positions digitally fluent suppliers to capture disproportionate value in the evolving digital cockpit market.

Automotive Digital Cockpit Industry Leaders

Robert Bosch GmbH

Continental AG

DENSO Corporation

Visteon Corporation

Harman International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: VIA optronics partnered with Autolink Information Technology to deliver touch-sensor display assemblies optimized for European cockpits.

- January 2025: QNX introduced QNX Cabin, a cloud-native development suite that lets distributed teams co-create cockpit applications in real time.

- January 2025: TCL CSOT revealed a 3D AR-HUD, panoramic HUD with ambient-light sensing, and dual-display 32:9 CID-PID panel at CES 2025.

- January 2025: Panasonic Automotive Systems and Qualcomm expanded their cooperation to embed generative-AI voice agents and rich multimedia into Snapdragon Cockpit Elite-based systems, which are slated for 2026 model-year launches.

Global Automotive Digital Cockpit Market Report Scope

The digital cockpit market refers to the integration of advanced digital technologies and features into the automotive cockpit or interior space. It includes digital displays, infotainment systems, connectivity features, advanced driver assistance systems (ADAS), and other digital components that enhance the driving experience and provide a range of functionalities.

The automotive digital cockpit market is segmented by equipment type, vehicle type, and geography. By equipment type, the market is segmented by heads-up displays, camera-based driving monitoring systems, and digital instrument clusters. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By geography, the market is segmented by North America, Europe, Asia-Pacific, and the rest of the world.

The report offers market size and forecast in value (USD) for the above segments.

| Heads-up Display (HUD) |

| Digital Instrument Cluster |

| Center Stack Display |

| Advanced Driver-Monitoring Camera |

| Telematics/Connectivity Control Unit |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Hybrid and Plug-in Hybrid (HEV/PHEV) |

| OEM-fitted |

| Aftermarket Retro-fit |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Morocco | |

| South Africa | |

| Rest of the Middle East and Africa |

| By Type | Heads-up Display (HUD) | |

| Digital Instrument Cluster | ||

| Center Stack Display | ||

| Advanced Driver-Monitoring Camera | ||

| Telematics/Connectivity Control Unit | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Hybrid and Plug-in Hybrid (HEV/PHEV) | ||

| By Sales Channel | OEM-fitted | |

| Aftermarket Retro-fit | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Morocco | ||

| South Africa | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the digital cockpit market?

The market generated USD 29.81 billion in 2026 and is on course to approach USD 52.56 billion by 2031 at a 12.02% CAGR.

Which region leads global demand for digital cockpits?

Asia-Pacific holds 39.42% of global revenue owing to China’s rapid EV adoption and local suppliers’ competitive pricing.

Why are battery-electric vehicles critical to cockpit growth?

EV platforms supply centralized power and zonal wiring that simplify high-performance computing and multi-screen integration, propelling an 18.05% CAGR for BEV cockpit sales.

How are safety regulations influencing cockpit design?

EU GSR II and NHTSA NCAP updates require real-time ADAS alerts, pushing automakers toward domain-controller cockpits that combine safety and infotainment on unified displays.

What challenges could slow digital cockpit adoption?

High up-front validation costs and growing cybersecurity liabilities can delay rollouts, especially for smaller OEMs and cost-sensitive vehicle segments.

Page last updated on: