Quantum Key Distribution Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

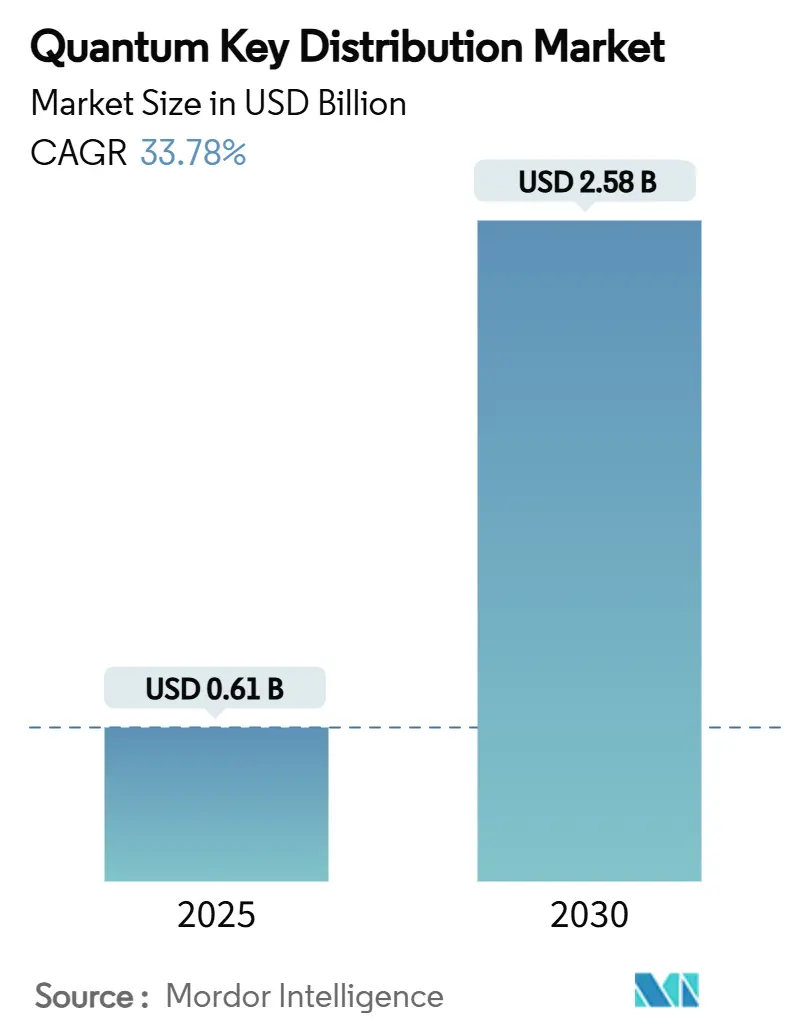

| Market Size (2025) | USD 0.61 Billion |

| Market Size (2030) | USD 2.58 Billion |

| Growth Rate (2025 - 2030) | 33.78% CAGR |

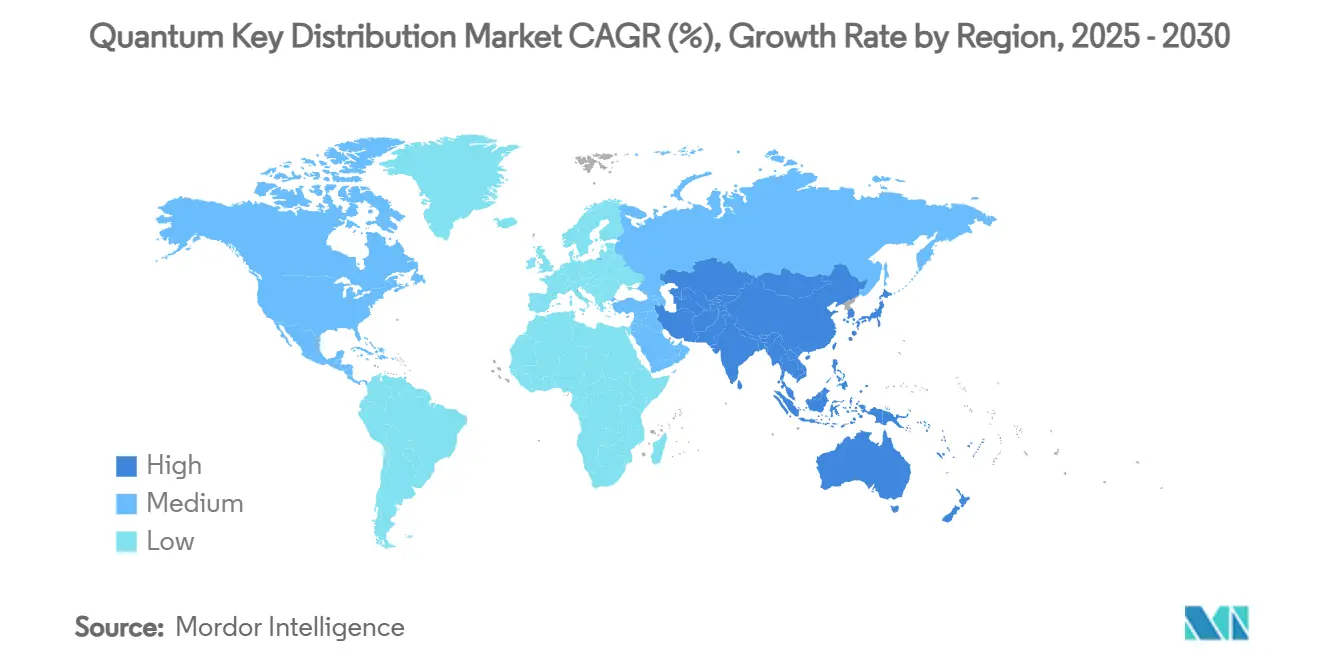

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

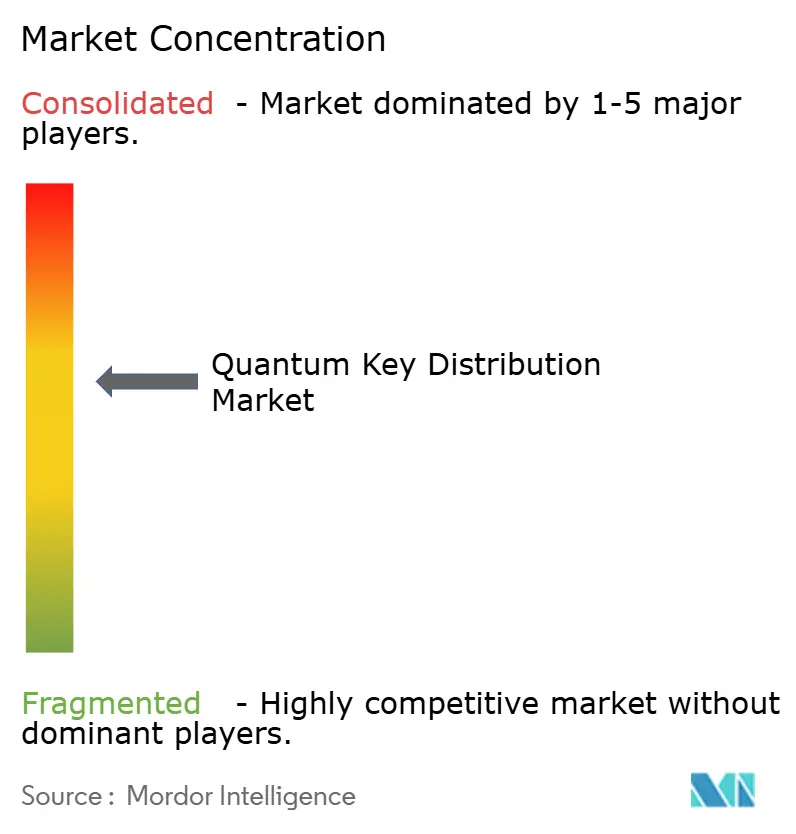

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Quantum Key Distribution Market Analysis by Mordor Intelligence

The global Quantum Key Distribution market size stands at USD 0.61 billion in 2025 and is projected to climb to USD 2.58 billion by 2030, advancing at a 33.78% CAGR. This steep trajectory is underpinned by mounting cyber-security urgency ahead of the anticipated “Q-Day,” accelerated national R&D programs, and the convergence of telecom and satellite infrastructure that expands deployment options. Governments are translating strategic security concerns into funded projects, while financial institutions and data-center operators race to harden networks against harvest-now-decrypt-later threats. Vendor consolidation demonstrates a maturing ecosystem in which established quantum specialists merge with platform players to simplify enterprise adoption. Simultaneously, standards initiatives such as NIST’s post-quantum cryptography timeline spur global compliance spending, creating a virtuous cycle of investment and innovation.

Key Report Takeaways

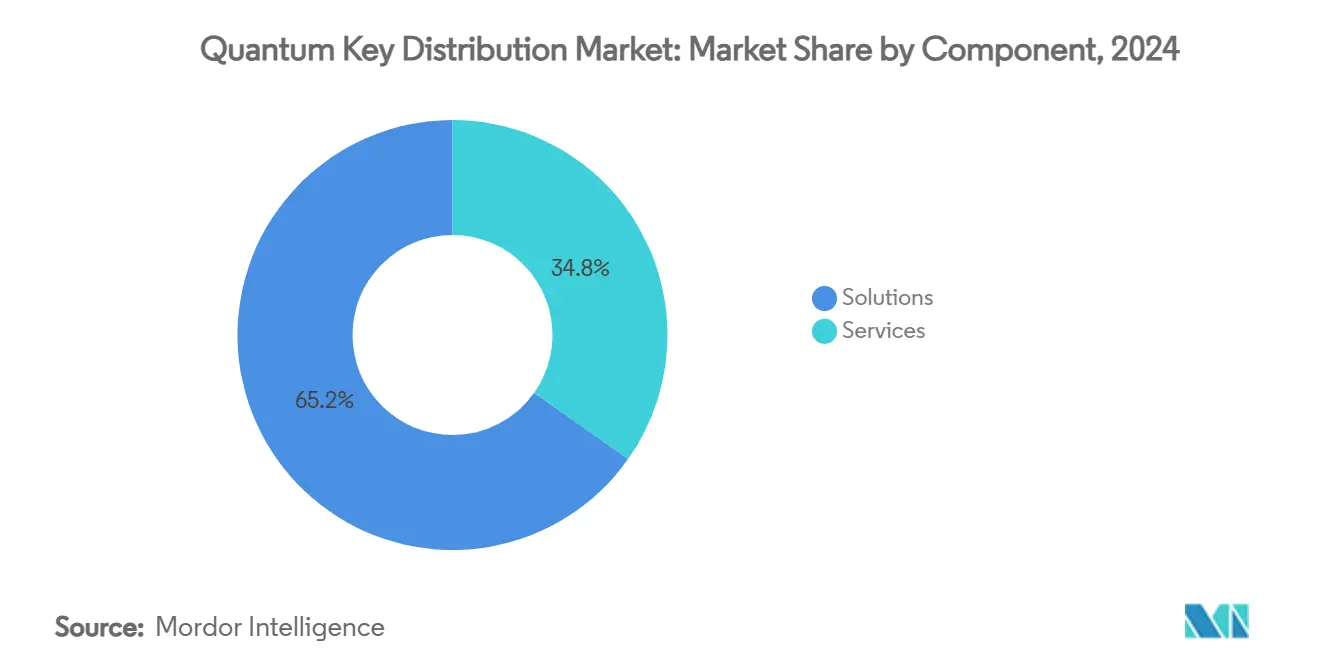

- By component, Solutions captured 65.21% of the Quantum Key Distribution market share in 2024; Services are forecast to expand at a 34.32% CAGR through 2030.

- By deployment mode, fiber-based terrestrial systems accounted for 58.06% of the Quantum Key Distribution market size in 2024 while satellite QKD is advancing at a 35.86% CAGR to 2030.

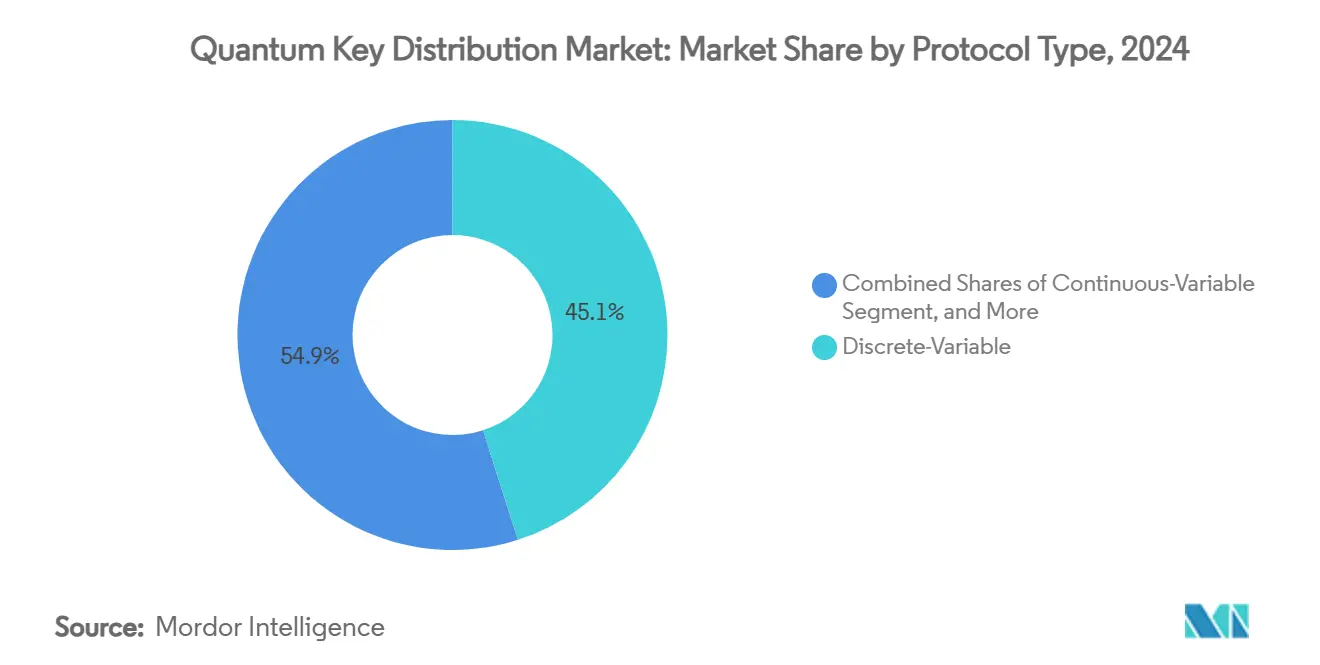

- By protocol type, BB84/SARG04 implementations led with a 45.07% share in 2024; continuous-variable systems are projected to grow at a 36.41% CAGR over the forecast horizon.

- By end-user industry, Government and Defense held 35.23% revenue share in 2024, whereas Data Centers and Cloud Providers register the fastest CAGR at 35.27% through 2030.

- By geography, Asia-Pacific commanded 32.56% of revenue in 2024 and is poised for a 38.36% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Quantum Key Distribution Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing cyber-security urgency ahead of "Q-Day" | +8.2% | Global, with priority in North America & Europe | Short term (≤ 2 years) |

| Large-scale public R&D programmes for national quantum networks | +6.8% | APAC core, spill-over to Europe & North America | Medium term (2-4 years) |

| Telecom operators integrating QKD into existing fiber backbones | +5.4% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Low-earth-orbit satellite constellations enabling global QKD coverage | +4.9% | Global, with initial focus on intercontinental links | Long term (≥ 4 years) |

| Hyperscale data-center interconnects adopting QKD for crypto-agility | +3.7% | North America & APAC, expanding to Europe | Short term (≤ 2 years) |

| Procurement rules mandating quantum-safe communications in critical infrastructure | +4.8% | Europe & North America, spreading to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Cyber-security Urgency Ahead of “Q-Day”

NIST’s 2024 roadmap mandates U.S. federal agencies complete migration away from RSA and ECDSA by 2035, triggering parallel transition plans across defense primes, utilities, and telecom carriers.[1]National Institute of Standards and Technology, “NIST Releases First 3 Finalized Post-Quantum Encryption Standards,” nist.gov HSBC’s quantum-secured foreign-exchange pilot illustrates financial-sector leadership, safeguarding EUR 30 million (USD 32.5 million) transactions against quantum attacks.[2]HSBC, “HSBC Pioneers Quantum Protection for AI-Powered FX Trading,” hsbc.com Heightened awareness of harvest-now-decrypt-later tactics pushes enterprises to deploy quantum-safe channels in parallel with post-quantum cryptography, accelerating demand for the Quantum Key Distribution market.

Large-scale Public R&D Programs for National Quantum Networks

China’s backbone links 16 cities across 12,000 km, validating hybrid QKD and post-quantum cryptography at operational scale.[3]China Daily, “China Telecom Pushes Boundaries in Quantum Technologies,” chinadaily.com.cn Europe’s four-year NOSTRADAMUS project under EuroQCI readies test infrastructure for 2026, while Germany’s proposed QTF-Backbone adds a dedicated fiber grid for secure quantum signals. These publicly funded build-outs reduce commercial risk, seed supplier ecosystems, and create reference architectures that private firms can replicate.

Telecom Operators Integrating QKD into Existing Fiber Backbones

BT’s metro pilot in London simultaneously transmits classical data and quantum keys over a single fiber, proving service-provider feasibility at thousands of keys per second. In March 2025, KDDI and Toshiba multiplexed 33.4 Tbps of data with quantum keys over 80 km, tripling capacity of earlier approaches. Such demonstrations enable carriers to monetize premium “quantum-secure” connectivity without new fiber builds, propelling service uptake.

Low-earth-orbit Satellite Constellations Enabling Global QKD Coverage

China’s Jinan-1 microsatellite achieved 13,000 km key exchanges, confirming economical small-sat platforms for intercontinental links. Thales-Hispasat’s EUR 103.5 million (USD 113.6 million) QKD-GEO program extends coverage from geostationary orbit, merging satellite and terrestrial networks into hybrid global architectures. Leveraging free-space optics and adaptive wavelength selection enhances link uptime and secure key rates, broadening the addressable Quantum Key Distribution market.

Restraints Impact Analysis of Quantum Key Distribution Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX/OPEX of QKD hardware and key-management systems | -7.4% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Photon-loss and distance limits without mature quantum repeaters | -5.7% | Global, affecting long-distance applications | Long term (≥ 4 years) |

| Lack of interoperability/standards across multi-vendor QKD gear | -4.7% | Global, with emphasis on Europe & North America | Medium term (2-4 years) |

| Absence of widely deployed quantum-safe authentication to complement QKD | -3.7% | Global, priority in enterprise and government sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX/OPEX of QKD Hardware and Key-management Systems

Precision components such as single-photon detectors remain costly, limiting uptake among price-sensitive sectors. Key-management appliances require specialized staff and 24×7 monitoring to maintain certification, challenging mid-size enterprises that lack quantum skill sets. Although prices decline with volume, immediate budget constraints temper near-term Quantum Key Distribution market growth.

Photon-loss and Distance Limits Without Mature Quantum Repeaters

Commercial QKD links plateau near 150 km in fiber owing to attenuation, and long-haul solutions default to trusted nodes that introduce operational complexity. Cryogenic rare-earth repeaters show promise yet remain in research labs, keeping fully trustless continent-scale networks several years away. Investment decisions thus weigh cost against partial security benefits, slowing deployments across sparsely populated geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Quantum Key Distribution Market Segment Analysis

By Component:

Services Growth Accelerates Integration DemandSolutions dominated revenue with 65.21% share in 2024, reflecting established hardware and software stacks delivered by incumbent vendors. The Services segment, however, is forecast to surge at 34.32% CAGR as enterprises seek design, certification, and managed operations expertise. Professional services orchestrate hybrid classical-quantum architectures, addressing skills shortages while ensuring compliance with evolving standards. Telecom operators bundle managed key distribution into existing network-operations centers, translating capital outlays into recurring service revenue. This consultancy-driven uptake underpins sustained expansion of the Quantum Key Distribution market.

Second-generation offerings emphasize automation, policy orchestration, and seamless integration with security-information event-management (SIEM) tools. Toshiba’s service platform delivers secret bit rates of 300 kb/s with failure probabilities below 10^-10, illustrating how tightly coupled software and hardware services reduce total cost of ownership. As enterprises consider full-stack quantum-safe frameworks, demand shifts from discrete products toward turnkey life-cycle services, reinforcing the Services growth narrative within the Quantum Key Distribution industry.

By Deployment Mode:

Satellite QKD Challenges Fiber DominanceFiber systems retained 58.06% revenue in 2024, buoyed by existing metropolitan infrastructure, predictable attenuation, and well-understood maintenance procedures. Yet satellite networks exhibit 35.86% CAGR through 2030, catalyzed by LEO constellations and impending GEO demonstrators that bypass terrestrial constraints. Hybrid architectures blend fiber core, free-space urban links, and satellite backbones, offering resilient, geography-agnostic coverage and elevating total Quantum Key Distribution market size.

Technology advances broaden satellite viability. Adaptive wavelength routing mitigates atmospheric loss, while intelligent beam steering trims quantum-bit-error rates from 2.5% to 0.7% and boosts secure key throughput above 30 kb/s. Governments favor satellite QKD for diplomatic connectivity, and global banks eye it for cross-border settlement channels. As satellite capacity scales, the competitive gap with fiber narrows, intensifying rivalry and spurring cross-sector partnerships.

By Protocol Type:

Continuous-Variable Gains Telecom CompatibilityDiscrete-variable schemes (BB84/SARG04) held 45.07% of 2024 revenue owing to deep academic vetting and clear security proofs. Still, continuous-variable (CV) systems register the fastest 36.41% CAGR, leveraging standard optical coherent detection that aligns with telco equipment. CV-QKD eliminates costly single-photon detectors, reducing capex and easing integration into dense-wavelength-division multiplexing (DWDM) backbones. Integrated photonic CV chips have demonstrated gigabit-scale key rates over 10 km links, underscoring commercial readiness.

Discrete-modulated CV-QKD improves robustness under channel noise, while polar-code reconciliation shrinks overhead. Entanglement-based E91 protocols remain niche, valued for foundational research and provable security but hampered by operational complexity. Vendors now ship multi-protocol transceivers, allowing customers to toggle between DV and CV modes, a flexibility that amplifies total Quantum Key Distribution market share across diversified use cases.

By End-user Industry:

Data Centers Drive Enterprise AdoptionGovernment and Defense retained the leading 35.23% share in 2024, propelled by national-security mandates and classified-network requirements. Yet the Data Centers and Cloud Providers segment edges ahead in growth at 35.27% CAGR as hyperscalers fortify intra-cluster traffic. Feasibility studies outline modular QKD deployment topologies that blend dark fiber and integrated photonics for high-density racks.

BFSI institutions expedite rollouts to shield high-value transactions; HSBC’s FX pilot proved live trading compatibility. Healthcare applications secure genomic and clinical-trial repositories, aligning with privacy regulations. Industrial enterprises explore QKD-protected SCADA links to mitigate operational-technology breaches. Each vertical adds incremental demand, pushing the Quantum Key Distribution market toward enterprise mainstream.

Geography Analysis

APAC Quantum Key Distribution Market

Asia-Pacific accounted for 32.56% of the Quantum Key Distribution market in 2024 and is projected to expand at a 38.36% CAGR. China’s USD 15 billion state investment created the world’s largest operational quantum network spanning 12,000 km, a live showcase of hybrid QKD-post-quantum cryptography architecture. Japan advances crypto-agile transport capable of seamless algorithm switching, while Singapore’s NQSN+ funnels SGD 100 million (USD 73.6 million) into industry pilots. These orchestrated programs nurture supplier ecosystems and accelerate commercialization.

North America and Oceania Quantum Key Distribution Market

North America prioritizes standards and regulatory certainty. NIST’s timeline compels federal agencies to complete a phased migration by 2035, fostering an ecosystem of vendors aligned to rigorous certification. Private capital flows reinforce public spending; PSiQuantum’s USD 620 million collaboration with Australia anchors cross-border talent and IP exchange that ultimately bolsters regional deployments. Industry-funded testbeds validate inter-vender interoperability, easing procurement risk for critical-infrastructure operators.

Europe Quantum Key Distribution Market

Europe adopts a coordinated infrastructure stance. The EuroQCI aims for contiguous national backbones, bolstered by Thales-Hispasat’s GEO satellite program that offers continent-scale coverage. Germany’s planned QTF-Backbone positions the country for technological sovereignty and serves as a blueprint for neighboring nations. Interoperability pilots across BT, Orange, and Deutsche Telekom generate best-practice blueprints, lowering barriers for broader adoption and enlarging the Quantum Key Distribution market size across the continent.

Competitive Landscape

The Quantum Key Distribution market shows moderate concentration as incumbents pursue scale through acquisitions while niche entrants target specialized competencies. IonQ’s USD 250 million purchase of ID Quantique, followed by deals for Qubitekk and Capella Space, forms the largest integrated quantum-networking platform, spanning terrestrial and satellite domains. Toshiba strengthens service orchestration, integrating high-speed QKD with key-management platforms for turnkey deployment. QuantumCTek, SK Telecom, and Quantum Xchange pursue strategic alliances that couple national telecom infrastructure with indigenous QKD hardware.

Differentiation pivots from isolated performance metrics to end-to-end operational reliability, API-based integration, and managed offerings. Vendors able to deliver plug-and-play modules that seamlessly connect to SIEM and zero-trust architectures secure premium margins. Standardization bodies such as ITU-T FG-QIT4N accelerate baseline compatibility, placing pressure on proprietary protocols while enlarging the addressable Quantum Key Distribution industry footprint.

White-space opportunities persist in quantum-safe authentication schemes, quantum-secure multi-party computation, and vertical solutions tailored to regulated industries. As the ecosystem coalesces around common interfaces, the competition shifts toward value-added analytics, service-level guarantees, and global coverage footprints that blend fiber, free-space, and satellite links.

Quantum Key Distribution Industry Leaders

ID Quantique SA

Toshiba Digital Solutions Corporation

QuantumCTek Co., Ltd.

SK Telecom Co., Ltd.

QuintessenceLabs Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Quantum Key Distribution Market Companies Covered in this Report

- ID Quantique SA

- Toshiba Digital Solutions Corporation

- QuantumCTek Co., Ltd.

- SK Telecom Co., Ltd.

- QuintessenceLabs Pty Ltd.

- Quantum Xchange Inc.

- Qasky (Anhui Qasky Quantum Technology Co., Ltd.)

- MagiQ Technologies Inc.

- NEC Corporation

- KETS Quantum Security Ltd.

- Qnu Labs

- LuxQuanta Technologies S.L

- ThinkQuantum S.r.l

- IonQ

- KEEQuant GmbH

- SpeQtral Pte Ltd

- QEYnet Inc

- Kloch

- HEQA Security

- Quantum Telecommunication Italy

Recent Industry Developments in Quantum Key Distribution Market

- March 2025: KDDI Research and Toshiba multiplexed 33.4 Tbps of data and quantum keys over 80 km single fiber, tripling conventional capacity and paving the way for practical inter-data-center QKD integration.

- February 2025: IonQ acquired ID Quantique for USD 250 million, integrating quantum computing and quantum-safe networking to deliver a unified platform targeting enterprise scalability.

- January 2025: Thales Alenia Space and Hispasat launched the EUR 103.5 million (USD 113.6 million) QKD-GEO program, developing the first geostationary QKD payload to extend secure links worldwide.

- January 2025: NTT Communications demonstrated a quantum-secure transport system that switches cryptographic suites without service interruption, advancing crypto-agile network operations.

Global Quantum Key Distribution Market Report Scope

Segmentation Overview

| Solutions |

| Services |

| Fiber-based Terrestrial QKD |

| Free-Space / Satellite QKD |

| Trusted-Node Metropolitan Networks |

| Discrete-Variable |

| Continuous-Variable |

| Entanglement-based |

| Government and Defense |

| BFSI (Banking, Financial Services and Insurance) |

| Telecommunications Service Providers |

| Data Centers and Cloud Providers |

| Healthcare and Life Sciences |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Turkey | ||

| Saudi Arabia | ||

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment Mode | Fiber-based Terrestrial QKD | ||

| Free-Space / Satellite QKD | |||

| Trusted-Node Metropolitan Networks | |||

| By Protocol Type | Discrete-Variable | ||

| Continuous-Variable | |||

| Entanglement-based | |||

| By End-user Industry | Government and Defense | ||

| BFSI (Banking, Financial Services and Insurance) | |||

| Telecommunications Service Providers | |||

| Data Centers and Cloud Providers | |||

| Healthcare and Life Sciences | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Turkey | |||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Quantum Key Distribution market in 2030?

The market is forecast to reach USD 2.58 billion by 2030, rising from USD 0.61 billion in 2025.

Why is Quantum Key Distribution gaining traction before quantum computers reach full scale?

Organizations face harvest-now-decrypt-later threats and must comply with mandates such as NIST’s migration timeline, prompting early adoption of quantum-safe channels.

Which region currently leads in Quantum Key Distribution deployments?

Asia-Pacific leads with 32.56% revenue share in 2024, driven by large-scale Chinese and Japanese projects and Singapore’s funding incentives.

How fast is the Services segment of Quantum Key Distribution expanding?

Services are projected to grow at a 34.32% CAGR through 2030 as enterprises seek integration and managed security expertise.

What technology advancements make satellite QKD commercially viable?

LEO constellations, adaptive wavelength routing, and GEO payloads improve link stability and key rates, enabling global coverage beyond fiber constraints.

Which end-user industry is the fastest growing adopter of Quantum Key Distribution?

Data Centers and Cloud Providers segment shows the highest CAGR at 35.27% through 2030, reflecting hyperscale demand for quantum-safe interconnects.

Page last updated on: