Schizophrenia Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.45 Billion |

| Market Size (2031) | USD 14.51 Billion |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Schizophrenia Drugs Market Analysis by Mordor Intelligence

The global schizophrenia drugs market size in 2026 is estimated at USD 12.45 billion, growing from 2025 value of USD 12.07 billion with 2031 projections showing USD 14.51 billion, growing at 3.11% CAGR over 2026-2031. Behind this steady headline figure, the schizophrenia drugs market is rapidly evolving as muscarinic agonists, glutamate modulators, and dopamine partial agonists compete with decades-old dopamine-antagonist therapies. Long-acting injectables (LAIs) are growing at 8% CAGR as health systems seek to counter 50% non-adherence rates, while Asia-Pacific’s 8.5% CAGR underscores widening diagnosis and insurance coverage. Portfolio realignment is accelerating: Bristol Myers Squibb acquired Karuna Therapeutics for USD 14 billion to secure KarXT, and Johnson & Johnson followed with a USD 14.6 billion purchase of Intra-Cellular Therapies to add lumateperone, signaling that differentiated mechanisms now dictate competitive advantage. Heightened payer focus on outcomes is also lifting demand for formulations that cut hospitalization, a trend favoring LAIs and third-generation agents.

Key Report Takeaways

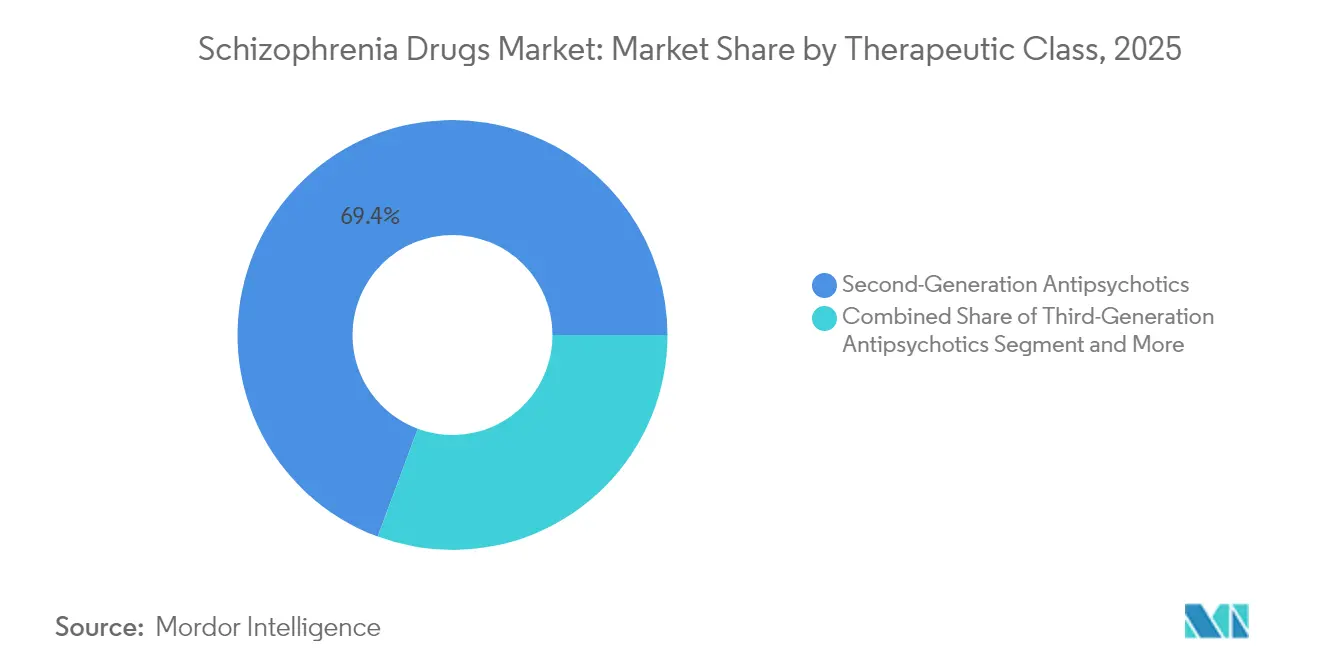

- By therapeutic class, second-generation antipsychotics held 69.35% of the schizophrenia drugs market share in 2025, while third-generation agents are advancing at a 7.18% CAGR through 2031.

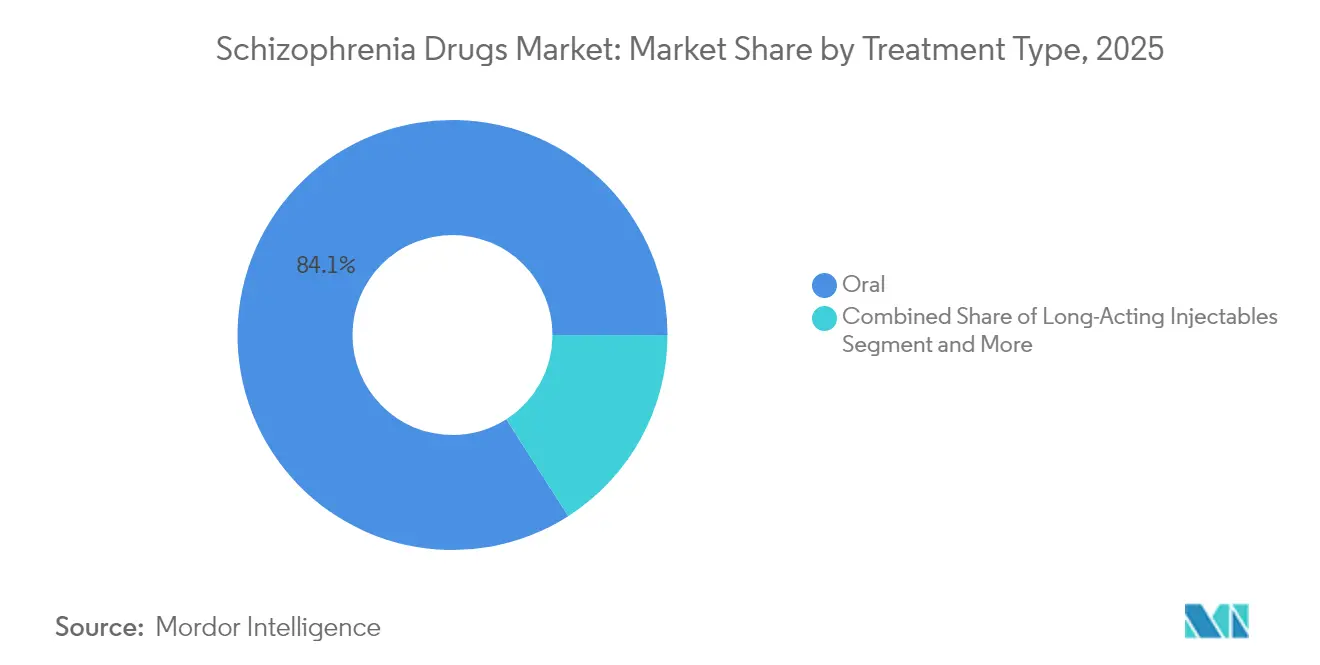

- By treatment type, oral products commanded 84.05% share of the schizophrenia drugs market size in 2025, whereas long-acting injectables are expanding at an 7.72% CAGR over 2026-2031.

- By distribution channel, retail pharmacies accounted for 54.72% of the market size in 2025; online pharmacies to grow at a 8.82% CAGR between 2026-2031.

- By drug mechanism of action, dopamine-serotonin antagonists led with 79.35% revenue share in 2025; dopamine D2/D3 partial agonists grow at a 6.55% CAGR through 2031.

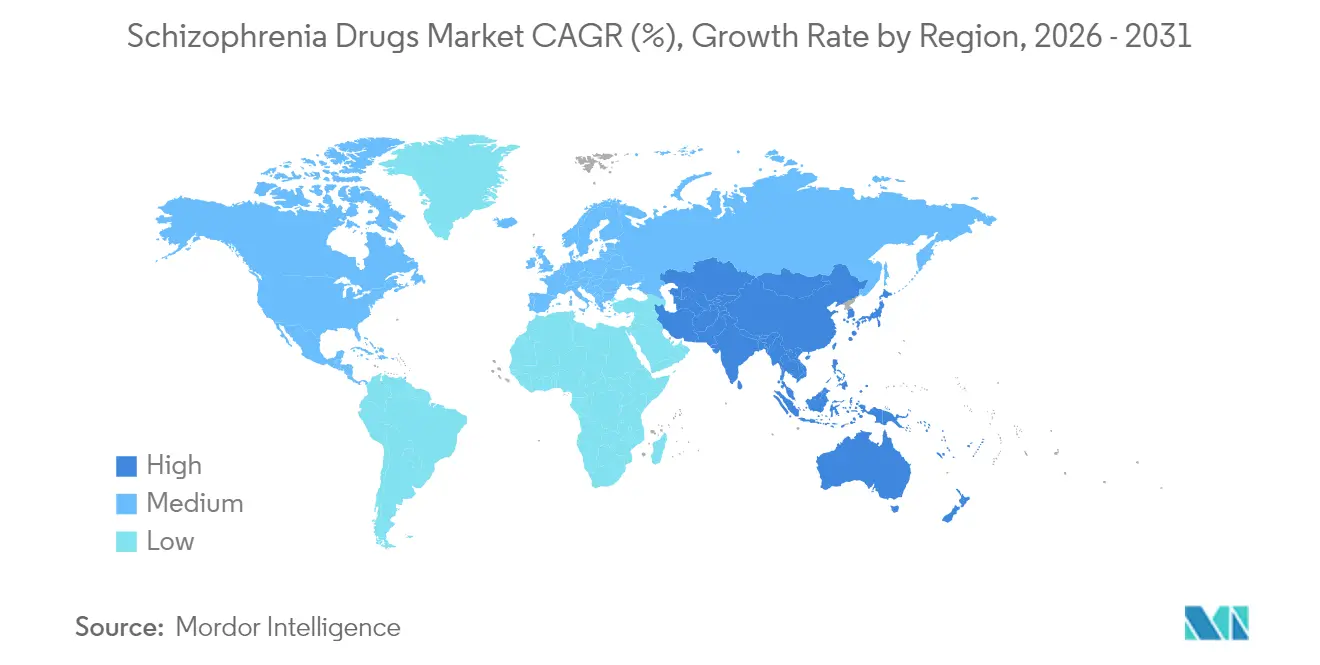

- By geography, North America led with 45.05% revenue in 2025; Asia-Pacific is projected to post the fastest 8.17% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Schizophrenia Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global Prevalence & Earlier Diagnosis of Schizophrenia | +1.2% | Global, with concentration in Asia-Pacific | Medium term (2-4 years) |

| Rising Adoption of Long-Acting Injectable Formulations for Improved Adherence | +0.9% | North America & Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Launch of Novel Third-Generation & Multi-Target Agents Expanding Treatment Options | +0.7% | North America, followed by Europe & Japan | Medium term (2-4 years) |

| Expansion of Mental-Health Insurance Coverage & Government Funding Worldwide | +0.5% | North America, Europe, developed Asia-Pacific | Medium term (2-4 years) |

| Affordable Generics & Public Procurement Programs Enhancing Access in Emerging Markets | +0.4% | Emerging markets in Asia-Pacific, Latin America, MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Global Prevalence & Earlier Diagnosis of Schizophrenia

Global prevalence has climbed to 24 million in 2025, and improved screening in primary care means more patients enter treatment earlier. Early intervention programs now stretch from Japan’s nationwide EIP network to pilot schemes in Chile, shortening the prodromal phase and enlarging the treated population. The economic burden reached USD 343.2 billion in the United States in 2024, intensifying payer appetite for drugs that cut relapse-driven hospital stays. Academic centers in Australia and Singapore are sharing longitudinal data sets that aid biomarker discovery, a move that may soon refine segment-specific prescribing. Taken together, rising prevalence and proactive diagnosis underpin volume growth for the schizophrenia drugs market.

Rising Adoption of Long-Acting Injectable Formulations for Improved Adherence

Up to half of patients discontinue oral therapy within one year, yet LAIs slash treatment-failure risk by 26-45% and materially lower rehospitalization. Payers now reimburse paliperidone every three months and olanzapine once monthly at parity with oral regimens, bolstering uptake in U.S. and German outpatient clinics. Chinese guidelines added LAIs to first-episode care pathways in 2025, cementing Asia-Pacific demand. R&D momentum is shifting to subcutaneous depots; Teva’s TEV-749 delivered >92% patient satisfaction in Phase 3, indicating convenience can translate into sustained adherence. The cumulative effect of these developments is a steady expansion of LAI penetration within the schizophrenia drugs market.

Launch of Novel Third-Generation & Multi-Target Agents Expanding Treatment Options

FDA approval of xanomeline-trospium in September 2024 ushered in the first muscarinic-based antipsychotic class, marking a pivotal moment after 35 years of dopamine complacency[1]FDA, “FDA Approves Drug With New Mechanism of Action for Treatment of Schizophrenia,” fda.gov. Muscarinic agonists, TAAR-1 agonists, and glutamatergic modulators now populate the most diversified pipeline in decades. Brexpiprazole and cariprazine already show superior efficacy for negative symptoms while mitigating weight gain, and early Phase 2 data for evenamide signal promise in treatment-resistant subgroups. Investors funneled more than USD 3 billion into late-stage trials during 2024-2025, catalyzing broader therapeutic choice and invigorating competition in the schizophrenia drugs market.

Expansion of Mental-Health Insurance Coverage & Government Funding Worldwide

The U.S. Medicare Payment Advisory Commission moved to abolish the 190-day inpatient cap, extending psychiatric coverage for severe schizophrenia cases. New Jersey mandated inpatient reimbursement parity for LAIs, a template other states are studying. Japan’s 2025 mental-health law broadened reimbursement for community-based care, including home LAI administration. In Europe, the EU4Health program earmarked EUR 825 million for digital mental-health initiatives, indirectly supporting tele-psychiatry prescriptions. Collectively, these policy moves enlarge payor budgets, creating fertile ground for premium-priced innovations in the schizophrenia drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Safety Concerns (Metabolic, Cardiovascular, Neurological) Limiting Long-Term Use | -0.8% | Global | Long term (≥ 4 years) |

| High Stigma & Low Treatment-Seeking Behavior Curtailing Uptake | -0.6% | Global, particularly severe in emerging markets | Long term (≥ 4 years) |

| Complex Regulatory & Reimbursement Pathways Delaying Launch of Novel Therapies | -0.4% | Global, with varying impact by region | Medium term (2-4 years) |

| Patent Expiries Triggering Price Erosion & Revenue Decline for Innovator Brands | -0.3% | Global, with higher impact in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Safety Concerns (Metabolic, Cardiovascular, Neurological) Limiting Long-Term Use

Up to 60% of patients on second-generation drugs develop weight gain or glucose abnormalities that double cardiovascular mortality versus the general population[2]Christoph Correll, “Metabolic Risk With Antipsychotics,” mdpi.com. Fear of tardive dyskinesia and metabolic syndrome drives frequent switching, eroding persistence rates. While third-generation molecules reduce metabolic load, clinicians still monitor QT prolongation and akathisia, complicating long-term adherence plans. These unresolved safety issues dampen uptake of chronic therapy across the schizophrenia drugs market.

High Stigma & Low Treatment-Seeking Behavior Curtailing Uptake

Stigma delays care in over 70% of cases across low-income regions; cultural norms label schizophrenia as spiritual affliction, steering families to traditional healers first. Even in the U.S., patients reporting high internalized stigma exhibit 40% higher non-adherence, shrinking real-world demand. Reluctance to disclose illness hampers employer-sponsored insurance enrollment, especially among gig-economy workers. The result is an under-penetrated treated population that suppresses revenue potential for the schizophrenia drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Class: Shift Toward Third-Generation Agents Broadens Choice

Second-generation medicines captured 69.35% of schizophrenia drugs market share in 2025 on the back of proven efficacy. However, third-generation therapies recorded the fastest 7.18% CAGR and are projected to carve deeper inroads as favorable metabolic profiles resonate with payers and physicians. The schizophrenia drugs market size attributable to third-generation products could top USD 3.15 billion by 2031 if current uptake trends hold. First-generation drugs still serve cost-constrained settings but gradually relinquish volume amid side-effect worries.

Developers now pursue muscarinic, TAAR-1, and glutamatergic avenues, fragmenting the once-stable class landscape. As biomarkers emerge, prescribers anticipate algorithm-guided selection, accelerating mechanism-specific growth nodes inside the schizophrenia drugs market.

By Drug Mechanism of Action: Receptor Diversity Enables Personalized Prescribing

Dopamine-serotonin antagonists once monopolized treatment, yet their dominance fell below 79.35% of 2025 revenue as partial agonists and novel modulators gained share. Cariprazine’s D3 preference enhances negative-symptom relief, while NMDA modulators offer hope for cognitive deficits. The schizophrenia drugs market size linked to dopamine D2/D3 partial agonists is forecast to rise at 6.55% CAGR through 2031.

Regulators now encourage mechanism-rich pipelines, expediting fast-track designations for first-in-class agents. Greater heterogeneity boosts the likelihood that prescribers tailor regimens to symptom clusters, fostering nuanced competition within the schizophrenia drugs market.

By Treatment Type: Long-Acting Injectables Cement Growth Trajectory

Oral tablets dominated 84.05% revenue in 2025, yet LAIs are set to expand share as subcutaneous products lower administration barriers. LAI revenue in the schizophrenia drugs market size is expected to approach USD 3.62 billion by 2031, driven by payer recognition of their relapse-prevention economics. Short-acting injectables and transdermal options fill niche needs such as acute agitation or needle-averse patients.

Manufacturers emphasize real-world evidence: three-monthly paliperidone cut Medicare hospital days by 32%, and six-monthly formulations are in Phase 2. These data support broader guidelines recommending LAIs after first relapse, potentially accelerating their diffusion across the schizophrenia drugs market.

By Distribution Channel: Digital Commerce Reshapes Access Pathways

Retail pharmacies held 54.72% share, yet online channels grew 8.82% CAGR as tele-psychiatry prescriptions surged. China’s “Internet+” pharmacies dispensed 38% more antipsychotic packs in 2024, and U.S. mail-order volumes rose 22%. Hospital pharmacies preserve importance for LAI initiation but ceded routine refills to community outlets.

FTC scrutiny of PBMs may realign rebate flows, affecting net prices across the schizophrenia drugs market. Meanwhile, Amazon’s RxPass and CVS Health’s digital clinic integrate mental-health consultations, signaling that distribution competition now hinges on platform reach and patient engagement.

Geography Analysis

North America accounted for 45.05% of schizophrenia drugs market revenue in 2025, anchored by high diagnosis, robust insurance, and early adoption of novel agents. The region also fields the majority of pivotal trials, reinforcing first-to-market advantages. However, specialty drug inflation outpaced wage growth, prompting payers to tighten prior-authorizations that could temper future volume growth.

Asia-Pacific posted the fastest 8.17% CAGR and is projected to lift its share to 27.35% by 2031. Drivers include rising disposable income, government insurance expansion, and early-intervention programs in Japan and South Korea. China’s bulk-procurement policy slashed prices, enabling provincial roll-outs of LAIs in 2025. Strategic deals, such as Newron’s evenamide licenses for Japan and Korea, illustrate how localization accelerates penetration in the schizophrenia drugs market.

Europe retained substantial volume on the back of universal coverage and integrated care models. Germany led LAI adoption, while Spain’s digital prescription initiative cut refill gaps by 18%. The continent also houses several manufacturing sites for active pharmaceutical ingredients, offering supply-chain resilience that can buffer price shocks within the schizophrenia drugs market.

Competitive Landscape

The schizophrenia drugs market displays moderate concentration: the top companies controls the significant market revenue. Johnson & Johnson, Eli Lilly, and Alkermes plc anchor the leaderboard through Invega, Zyprexa, and Cobenfy, respectively. Recent M&A reshaped the field: Bristol Myers Squibb’s USD 14 billion buyout of Karuna Therapeutics secured KarXT, and Johnson & Johnson’s USD 14.6 billion acquisition of Intra-Cellular Therapies brought CAPLYTA into its neuroscience stable[3]Synapse, “Wave of Mergers and Acquisitions,” synapse.patsnap.com.

Pipeline diversity fuels rivalry. Teva is advancing TEV-749, while Neurocrine’s TAAR-1 agonist NBI-1117568 posted positive Phase 2 data. Small-cap firms like Newron target add-on strategies, positioning evenamide for resistant cases. Generic makers, including Sunshine Biopharma, launched lurasidone generics in 2025, intensifying price pressure on mature brands. Strategic differentiation now hinges on clinical outcomes, dosing convenience, and safety profiles.

Regional entrants add complexity: Zai Lab filed a KarXT NDA in China, aiming to leverage rapid NRDL inclusion. Japanese firms, backed by the Pharmaceuticals and Medical Devices Agency’s Sakigake pathway, seek accelerated domestic approvals. Competitive dynamics therefore balance global scale with localized execution inside the schizophrenia drugs market.

Schizophrenia Drugs Industry Leaders

Eli Lilly and Company

Alkermes PLC

Johnson & Johnson (Janssen)

AbbVie Inc. (Allergan)

Otsuka Pharmaceutical Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Newron Pharmaceuticals began the ENIGMA-TRS Phase 3 program for evenamide in greater than 1,000 treatment-resistant patients.

- March 2025: Teva Pharmaceuticals reported positive SOLARIS Phase 3 results for once-monthly subcutaneous TEV-749 (olanzapine) with 92% patient satisfaction.

Global Schizophrenia Drugs Market Report Scope

As per the scope of the report, Schizophrenia is characterized by delusions, hallucinations, and other cognitive difficulties, which can often be a lifelong struggle. It is a chronic and severe mental disorder that affects how a person thinks, feels, and behaves. People with schizophrenia may seem like they have lost touch with reality. Although schizophrenia is not as common as other mental disorders, the symptoms can be disabling. The schizophrenia drugs market is segmented by therapeutic class (second-generation antipsychotics, third-generation antipsychotics, and other therapeutic classes), treatment (oral and injectables), and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Second-Generation (Atypical) Antipsychotics |

| Third-Generation (D2/D3 Partial Agonists) |

| First-Generation (Typical) Antipsychotics |

| Other Therapeutic Classes |

| Dopamine-Serotonin Antagonists |

| Dopamine D2/D3 Partial Agonists |

| NMDA-Receptor Modulators |

| Novel Multi-Target Modulators |

| Oral (Tablets, Capsules, Solutions) |

| Long-Acting Injectables (Depot) |

| Short-Acting Injectables |

| Transdermal Patch |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapeutic Class | Second-Generation (Atypical) Antipsychotics | |

| Third-Generation (D2/D3 Partial Agonists) | ||

| First-Generation (Typical) Antipsychotics | ||

| Other Therapeutic Classes | ||

| By Drug Mechanism of Action | Dopamine-Serotonin Antagonists | |

| Dopamine D2/D3 Partial Agonists | ||

| NMDA-Receptor Modulators | ||

| Novel Multi-Target Modulators | ||

| By Treatment Type | Oral (Tablets, Capsules, Solutions) | |

| Long-Acting Injectables (Depot) | ||

| Short-Acting Injectables | ||

| Transdermal Patch | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the schizophrenia drugs market?

It is USD 12.45 billion in 2026 and is projected to reach USD 14.51 billion by 2031.

Which region is growing fastest for schizophrenia treatment sales?

Asia-Pacific is expanding at an 8.17% CAGR through 2031 due to broader insurance coverage and rising diagnosis.

Why are long-acting injectables gaining traction?

LAIs cut treatment-failure risk by up to 45% and reduce hospitalizations, improving adherence and payer economics.

What makes third-generation antipsychotics different?

They offer improved metabolic profiles and better control of negative symptoms compared with older dopamine antagonists.

How concentrated is competition in this therapeutic area?

The top five firms hold roughly 62% of revenue, reflecting moderate concentration that is declining as new entrants appear.

Page last updated on: