Antipsychotic Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

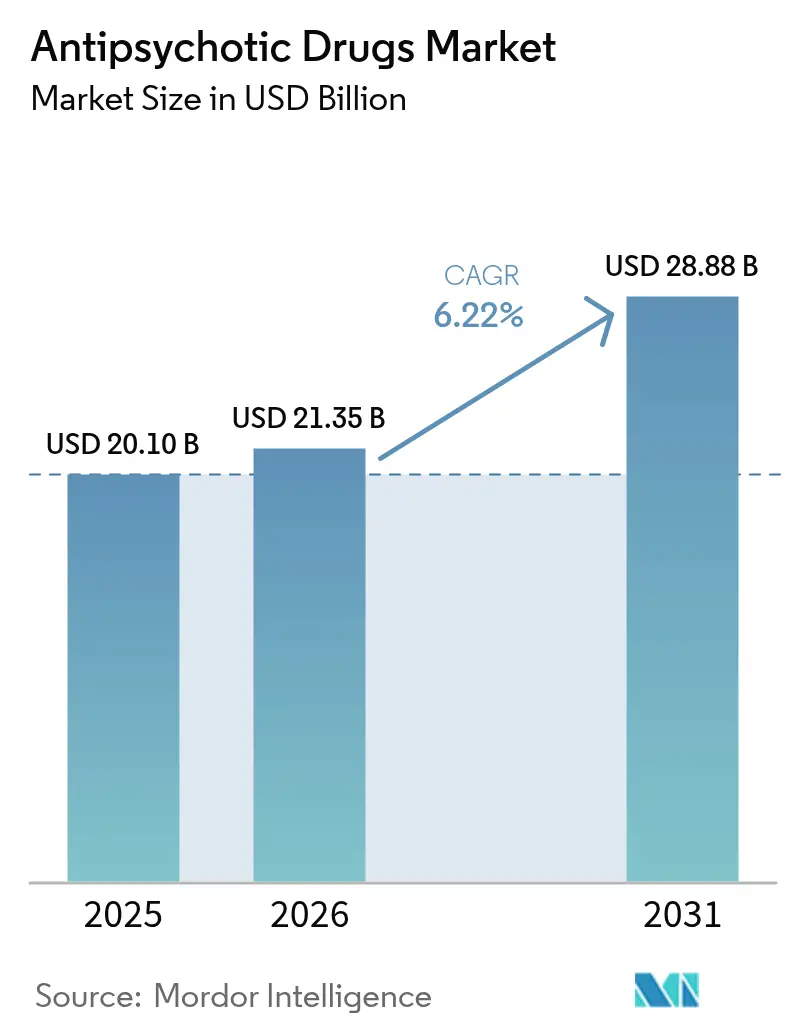

| Market Size (2026) | USD 21.35 Billion |

| Market Size (2031) | USD 28.88 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

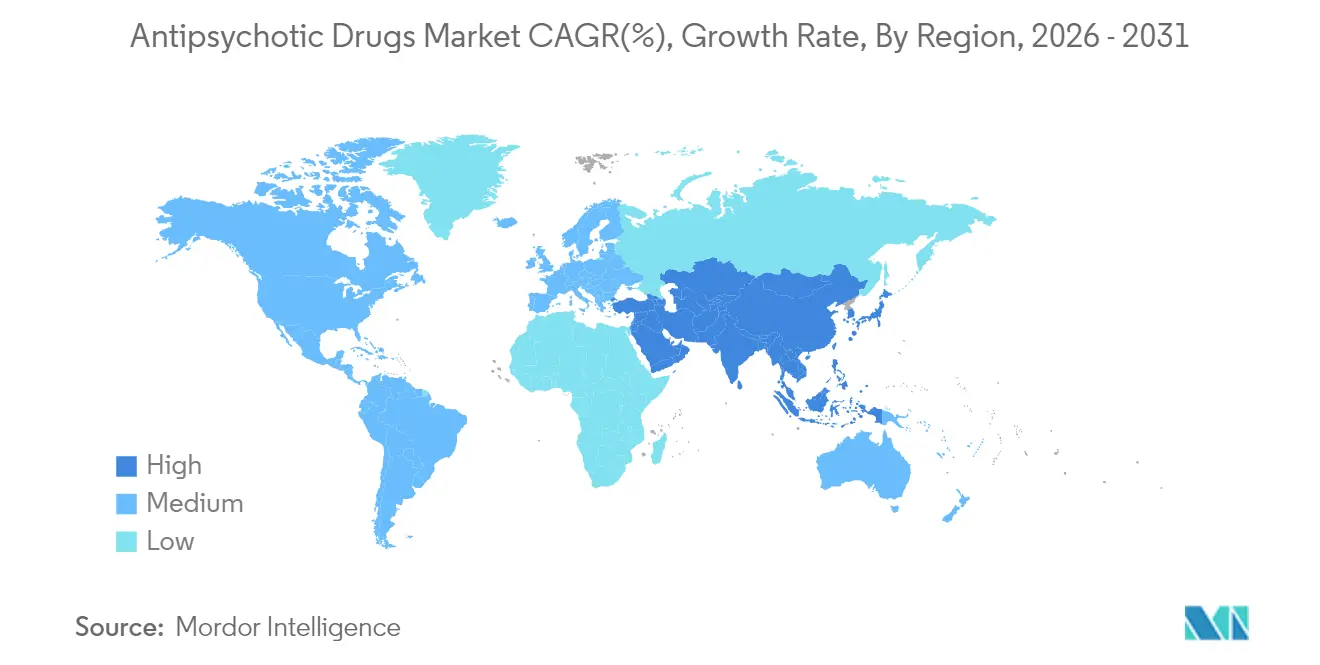

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antipsychotic Drugs Market Analysis by Mordor Intelligence

The Antipsychotic Drugs market size is expected to grow from USD 20.10 billion in 2025 to USD 21.35 billion in 2026 and is forecast to reach USD 28.88 billion by 2031 at 6.22% CAGR over 2026-2031.

Growth rests on three pillars: the steady rise in diagnosed mental-health disorders, brisk uptake of third-generation agents with dopamine-partial-agonist or muscarinic-receptor activity, and sustained public-payer funding that lowers patients’ out-of-pocket costs. Consolidation among innovators is reshaping the competitive arena, with recent high-value acquisitions designed to secure intellectual property and fast-track differentiated assets. In parallel, long-acting injectables gain momentum as real-world evidence confirms superior relapse prevention and cost offsets. Generics, however, intensify price pressure as patents expire on blockbuster atypical molecules, prompting firms to bundle medicines with digital-therapeutic companions that reinforce adherence and extend product lifecycles.

Key Report Takeaways

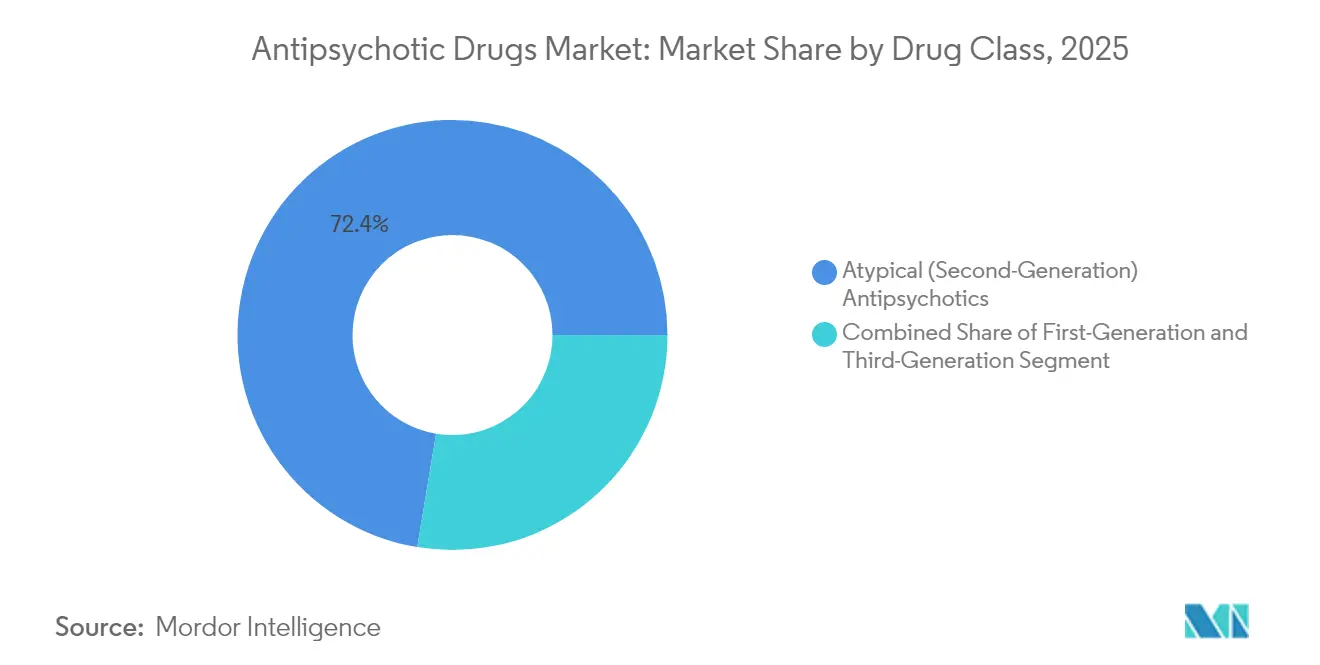

- By drug class, atypical agents led with 72.38% of antipsychotic drugs market share in 2025, while third-generation agents are projected to post the fastest 6.96% CAGR through 2031.

- By therapeutic application, schizophrenia commanded 61.72% of the antipsychotic drugs market size in 2025, whereas bipolar disorder is advancing at an 7.72% CAGR to 2031.

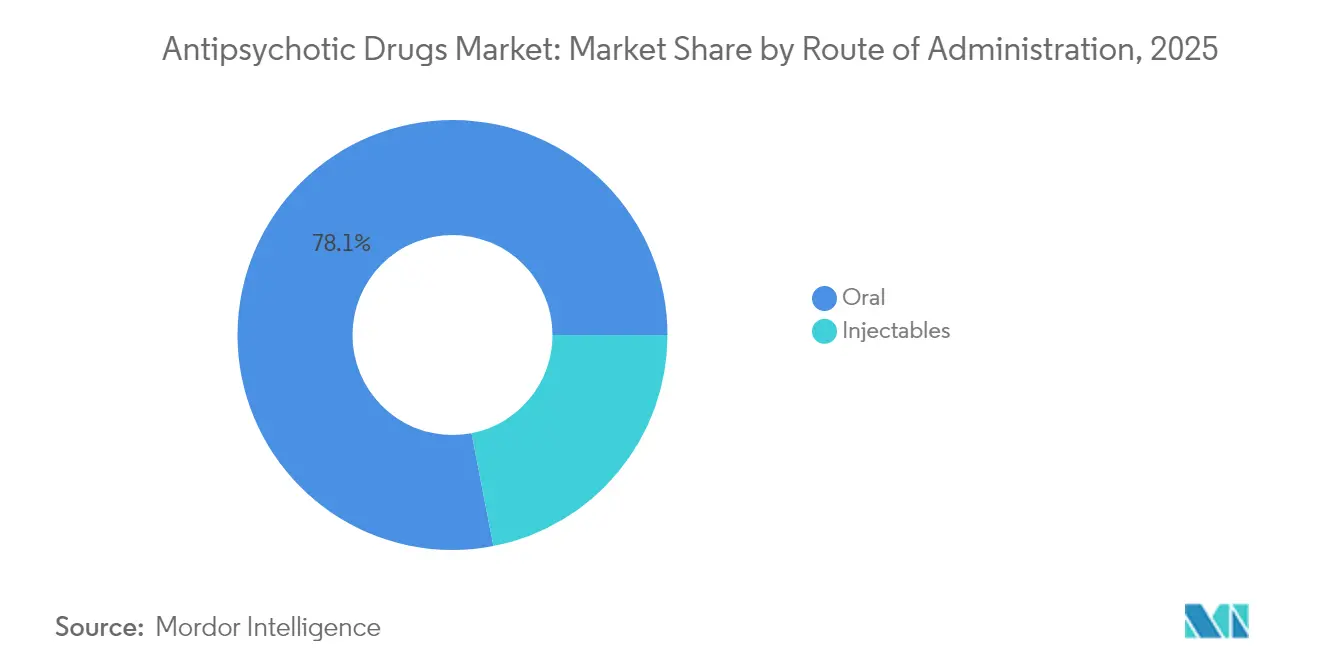

- By route of administration, oral formulations accounted for 78.05% revenue share in 2025; long-acting injectables are set to expand at a 7.55% CAGR between 2026 and 2031.

- By geography, North America contributed 39.22% of the antipsychotic drugs market share in 2025, while the Asia-Pacific region is the fastest-growing, with a 7.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Antipsychotic Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Rising LAI Adoption in Community Mental-Health Programs | +1.0% | Global, strongest in North America & Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| Expanding Early-Psychosis Intervention Centers | +0.7% | North America & Europe lead | Long term (≥4 years) |

| Surge in Medicaid/Medicare Coverage for Third-Generation Agents | +0.9% | Primarily North America | Short term (≤2 years) |

| Increasing Focus of Governments and Health Care Organizations on Mental Health | +1.3% | Global | Medium to Long term (2-4+ years) |

| Digital-Therapeutic Companion Apps Boosting Medication Adherence | +0.5% | North America & Europe lead | Medium term (2-4 years) |

| Robust R&D Pipeline and FDA Approvals for Novel Formulations | +1.2% | Global, with North America & Europe; Asia-Pacific following | Short to Medium term (≤4 years) |

| Source: Mordor Intelligence | |||

Rising LAI Adoption in Community Mental-Health Programs

Long-acting injectable antipsychotics are closing the 50% non-adherence gap that undermines oral therapy. A 2024 Journal of Clinical Psychopharmacology study reported 30-day readmission rates of 1.9% for LAIs versus 8.3% for oral drugs, translating to a 77% reduction in early rehospitalizations. Early initiation of LAIs within 12 months of diagnosis yields annual healthcare savings of USD 7,195 per patient by reducing emergency department utilization. These findings persuade payers to reimburse LAIs earlier in treatment algorithms, accelerating penetration across community clinics.

Expanding Early-Psychosis Intervention Centers

Coordinated Specialty Care programs are scaling rapidly. The National Alliance on Mental Illness estimates that broader roll-out could reach 600,000-800,000 additional patients and generate USD 115-140 billion in system savings over a decade . A 2024 Hong Kong study in JAMA Network Open linked implementation of the EASY Plus model to steep declines in self-harm episodes among adults aged 26-44 years. These centers favor newer agents with balanced efficacy and tolerability profiles, fuelling demand for third-generation options.

Surge in Medicaid/Medicare Coverage for Third-Generation Agents

The 2025 Medicare Advantage and Part D rate notice increases payments by 3.70% and establishes a USD 2,000 out-of-pocket cap, thereby widening access to premium-priced novel antipsychotics.[1]Emily Eisner et al., “Barriers and Facilitators of User Engagement With Digital Mental Health Interventions,” JMIR Mental Health, mental.jmir.orgAll chronic diseases now fall under Medication Therapy Management, ensuring mental-health medicines are actively reviewed and supported. Expanded coverage accelerates uptake of agents such as cariprazine and brexpiprazole, cushioning revenue lost to generic erosion.

Digital-Therapeutic Companion Apps Boosting Medication Adherence

Smartphone-based tools that offer reminders, symptom diaries, and clinician dashboards are proving effective in psychiatric settings. A 2025 JMIR Mental Health synthesis found that alignment with patient needs and human support are key drivers of engagement. [2]Centers for Medicare & Medicaid Services, “CMS Finalizes Payment Updates for 2025 Medicare Advantage and Part D Programs,” cms.gov The FDA granted Breakthrough Device status to a prescription digital therapeutic for schizophrenia in 2024, underscoring regulatory acceptance of software adjuncts. Improved adherence extends medication persistence, enlarging the treated population base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Patent Cliffs of Key Atypical Molecules | -1.7 | Global, with highest impact in North America and Europe | Short term (≤ 2 yrs) |

| Addiction Caused Due to the Antipsychotic Drugs | -1.0 | Global | Long term (≥ 5 yrs) |

| Black-Box Warnings Limiting Pediatric Prescriptions | -0.8 | United States, European Union | Medium term (~ 3-4 yrs) |

| Price-Control Expansion under China's NRDL | -0.6 | China, with spillover effects in Asia-Pacific | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

Patent Cliffs of Key Atypical Molecules

Major brands face imminent loss of exclusivity. Abilify Maintena’s patent expiry in June 2025 threatens 44% of its prescription base. Johnson & Johnson’s Invega Sustenna posted USD 2.9 billion in 2023 U.S. sales, yet generics from Teva and Viatris loom. Price erosion depresses branded revenue and compresses margins across the antipsychotic drugs market.

Addiction Caused Due to the Antipsychotic Drugs

Safety issues curb long-term acceptance. Tardive dyskinesia affects up to 127 per 1,000 users in the United States, impacting roughly 500,000 individuals. A 2024 study in Heart Rhythm linked certain agents to severe QT prolongation in more than 10% of users, raising arrhythmia risk . Such adverse-event profiles restrict prescribing in vulnerable cohorts, tempering overall uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Third-Generation Agents Reshape Treatment Paradigms

Atypical formulations generated the largest antipsychotic drugs market size in 2025, capturing 72.38% revenue on the back of broad indications and payer familiarity. Third-generation agents, though smaller in absolute dollars, are forecast to outpace the overall market with a 6.96% CAGR through 2031. Their dopamine-partial-agonist or dual muscarinic activity mitigates extrapyramidal side effects, a clear advantage that bolsters clinician confidence. Bristol Myers Squibb’s Cobenfy (xanomeline-trospium), the first new mechanistic class in 70 years, underscores this pivot.

Improved metabolic profiles and reduced tardive-dyskinesia risk strengthen payer value propositions. The antipsychotic drugs market size attached to third-generation products is predicted to expand steadily as pipeline entrants such as roluperidone advance toward possible approval. First-generation agents remain useful in acute agitation and resource-strained settings, yet their share declines annually due to tolerability concerns.

By Therapeutic Application: Bipolar Disorder Drives Expansion

Schizophrenia treatment dominated revenue, corresponding to 61.72% of 2025 antipsychotic drugs market share. Bipolar disorder is the fastest-growing use case, with an 7.72% CAGR projected as physicians embrace agents effective across manic and depressive phases. CAPLYTA (lumateperone) earned approval for bipolar I and II depression, prompting Johnson & Johnson's USD 14.6 billion acquisition of Intra-Cellular Therapies to secure the CAPLYTA franchise.

CAPLYTA's pending application in major depressive disorder and REXULTI's 2023 label extension for agitation in Alzheimer's dementia broaden clinical reach. Over the forecast period, the antipsychotic drugs market size linked to dementia-related psychosis is expected to increase as payers recognize the benefits of behavioral-symptom relief.

By Route of Administration: Long-Acting Injectables Gain Momentum

Oral tablets retained the dominant position with 78.05% of total 2025 revenue, favored for chronic maintenance and flexibility. Yet the long-acting-injectable segment is set for a 7.55% CAGR through 2031 as adherence gains and longer dosing intervals improve outcomes. The antipsychotic drugs market size for LAIs will rise further with once-monthly and once-bimonthly formulations such as Rykindo, Uzedy, and Abilify Asimtufii obtaining regulatory clearance.

Phase 3 data for TEV-749, a subcutaneous olanzapine LAI, confirm efficacy and tolerability, signaling near-term expansion avenues. Short-acting injectables will remain niche, reserved for emergency stabilization.

Geography Analysis

North America generated 39.22% of global revenue in 2025, buoyed by early adoption of third-generation agents and payer reforms that cap annual patient out-of-pocket spend at USD 2,000 under Medicare Part D cms.gov. FDA approvals for muscarinic-receptor therapies and once-bimonthly LAIs sustain clinical enthusiasm, while Canada and Mexico add incremental growth through mental-health investment schemes.

Asia-Pacific is the fastest-growing territory at a 7.61% CAGR through 2031. China’s domestic innovators secured the first U.S. nod for a Chinese-developed paliperidone palmitate LAI in 2024, spotlighting the region’s research ascent. Improved insurance penetration and destigmatization campaigns in India and Southeast Asia enlarge the treated population, further propelling the antipsychotic drugs market.

Europe retains solid share anchored by universal health coverage and a regulatory focus on real-world evidence. The 2025 approval of Rxulti for adolescent schizophrenia widens access in a sensitive demographic. Price-volume agreements temper list-price inflation, yet offsetting uptake of novel therapies supports steady value growth. South America and the Middle East & Africa, though smaller, are forecast to out-perform historic averages as governments integrate mental-health services into national benefit packages.

Competitive Landscape

Strategic consolidation defines 2025 deal-flow. Johnson & Johnson purchased Intra-Cellular Therapies for USD 14.6 billion to secure CAPLYTA’s bipolar and schizophrenia franchises. Bristol Myers Squibb acquired Karuna Therapeutics to add KarXT, a muscarinic receptor agonist, underscoring appetite for mechanistic diversity.

Digital innovation introduces new entrants. Boehringer Ingelheim and Click Therapeutics’ investigational prescription digital therapeutic received Breakthrough Device status, marking software’s rise alongside molecules . Terran Biosciences’ TerXT aims to combine prodrugs of xanomeline and trospium in a once-daily oral and LAI formulation, challenging incumbents.

Partnership structures diversify risk. AbbVie’s USD 65 million upfront collaboration with Gilgamesh Pharmaceuticals explores neuroplastogens, with milestones worth up to USD 1.95 billion. Medium-sized players leverage licensing to extend geographic reach without over-stretching capital, preserving pipeline optionality in a competitive, data-driven environment.

Antipsychotic Drugs Industry Leaders

Eli Lily and Company

Johnson and Johnson

Pfizer Inc.

AstraZeneca plc

Otsuka Pharmaceutical Co, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Johnson & Johnson acquired Intra-Cellular Therapies for USD 14.6 billion, adding CAPLYTA to its neuroscience portfolio.

- January 2025: Acadia Pharmaceuticals filed DAYBUE with the European Medicines Agency and outlined Managed Access Programs set for Q2 2025.

- September 2024: FDA cleared Bristol Myers Squibb’s Cobenfy, the first muscarinic-targeting antipsychotic.

- July 2024: Luye Pharma obtained FDA approval for Erzofri, a paliperidone palmitate LAI developed in China.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the antipsychotic drugs market as all prescription pharmaceutical products whose primary indication is the management of psychosis-linked disorders, principally schizophrenia, bipolar disorder-related mania or mixed episodes, and dementia-related psychosis, delivered through oral solids or short- and long-acting injectables and valued at the ex-manufacturer price level.

Scope exclusion: medicines used solely as hypnotics, anxiolytics, or mood stabilizers without formal psychosis labeling are outside the remit of this estimate.

Segmentation Overview

- By Drug Class

- Typical (First-Generation) Antipsychotics

- Atypical (Second-Generation) Antipsychotics

- Dopamine Partial Agonists (Third-Generation)

- By Therapeutic Application

- Schizophrenia

- Bipolar Disorder

- Major Depressive Disorder

- Dementia-Related Psychosis

- Others

- By Route of Administration

- Oral

- Injectables

- Long-Acting Injectables (LAIs)

- Short-Acting Injectables

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured discussions with practicing psychiatrists, hospital pharmacists, payer advisers, and regional key-opinion academics across North America, Europe, and fast-growing Asia-Pacific helped us stress-test prevalence-to-treatment conversion ratios, adherence patterns for LAIs, and likely generic erosion timing. Their insights guided final assumption tuning and scenario weighting.

Desk Research

Mordor analysts began with open-access pillars such as WHO mental-health prevalence files, the UN Population Prospects, OECD health-expenditure dashboards, and national drug-utilization databases (for example, Medicare Part D and EMA EudraVigilance) to benchmark treated-patient pools and therapy shifts.

Clinical-trial registries, recent FDA and EMA approval dossiers, and trade-association bulletins then mapped emerging third-generation assets and long-acting injectable uptake trends.

Paid repositories, D&B Hoovers for company revenue signal checks and Dow Jones Factiva for validated volume-weighted ASP clues, added depth.

This list is illustrative; many additional public and proprietary sources informed data cleaning and gap fills.

Market-Sizing & Forecasting

The model starts with a top-down prevalence-to-treated-cohort build-up by disorder and region; incidence, diagnosis, and treatment-penetration ratios are flexed using historical ICD-coded script volumes.

Supplier roll-ups and sampled ASP × unit checks provide a limited bottom-up cross-reference, and mismatches beyond a certain threshold trigger re-work.

Key fingerprints guiding the base year include a significant share of long-acting injectables in U.S. atypical antipsychotic sales, historical Medicaid script growth rate, average annual generic price deflation, schizophrenia prevalence drift, and FDA new-molecule approvals.

Forecasts use multivariate regression coupled with ARIMA overlays on prevalence and pricing series, allowing rapid scenario swaps when primary experts flag material reimbursement or pipeline surprises.

Data voids, for instance, private-hospital script volumes in India, are bridged with scaled proxy ratios sourced from tertiary interview inputs.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, variance checks against independent prescription audits, and automated outlier flags.

Reports refresh each year; interim flashes are issued when regulatory, supply, or epidemiology shifts would alter the baseline by more than three percent.

Why Mordor's Antipsychotic Drugs Baseline Earns Trust

Published estimates often diverge because research houses pick unequal indication baskets, apply different ASP ladders, or lock forecasts to outdated prevalence files.

Key gap drivers we observe include narrower disorder scope (some omit dementia-related psychosis), single-country ASP sampling without currency-year harmonization, and less frequent model refreshes, which together push totals away from real-world spend levels that our quarterly validations capture.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 20.10 bn (2025) | Mordor Intelligence | - |

| USD 18.32 bn (2025) | Global Consultancy A | excludes third-generation agents and LAIs in Asia |

| USD 19.61 bn (2025) | Regional Consultancy B | conservative ASP set frozen at 2023 exchange rates |

| USD 20.96 bn (2025) | Trade Journal C | prevalence uplift untested against prescription audits |

Taken together, the comparison shows that our disciplined scope choices, blended top-down-bottom-up checks, and annual refresh cadence give decision-makers a transparent, repeatable baseline that neither overstates nor understates real demand.

Key Questions Answered in the Report

What is the current size of the antipsychotic drugs market?

The antipsychotic drugs market generated USD 21.35 billion in 2026 and is expected to reach USD 28.88 billion by 2031.

Which region is growing fastest?

Asia-Pacific is projected to expand at a 7.61% CAGR from 2026 to 2031, the highest regional growth rate in the industry.

Why are long-acting injectable antipsychotics gaining traction?

LAIs cut 30-day readmissions from 8.3% to 1.9%, improve adherence, and deliver annual cost savings of more than USD 7,000 per patient, driving wider adoption among payers and clinicians.

How will patent expiries affect market dynamics?

Loss of exclusivity for blockbuster atypicals such as Abilify Maintena and Invega Sustenna will heighten generic competition, trimming branded revenue and accelerating product bundling with digital supports.

Which therapeutic application is set for the quickest growth?

Bipolar disorder treatment is forecast to post the fastest 7.72% CAGR, supported by expanded labels for newer agents like lumateperone.

Page last updated on: