Psychedelic Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

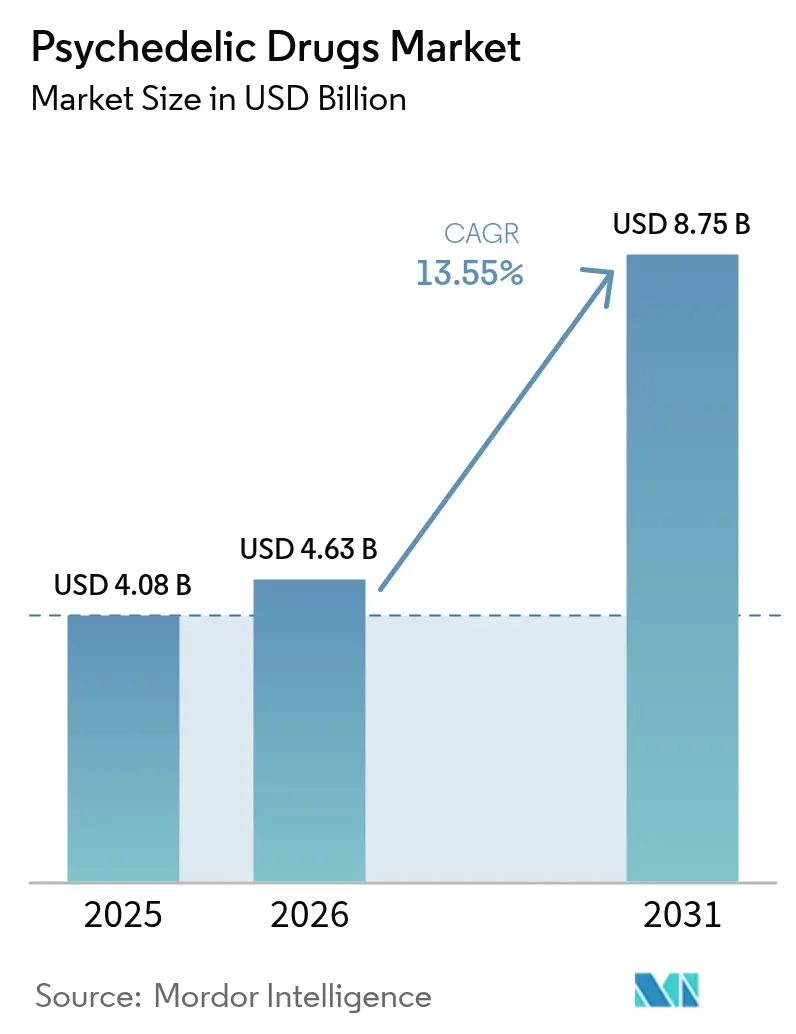

| Market Size (2026) | USD 4.63 Billion |

| Market Size (2031) | USD 8.75 Billion |

| Growth Rate (2026 - 2031) | 13.55% CAGR |

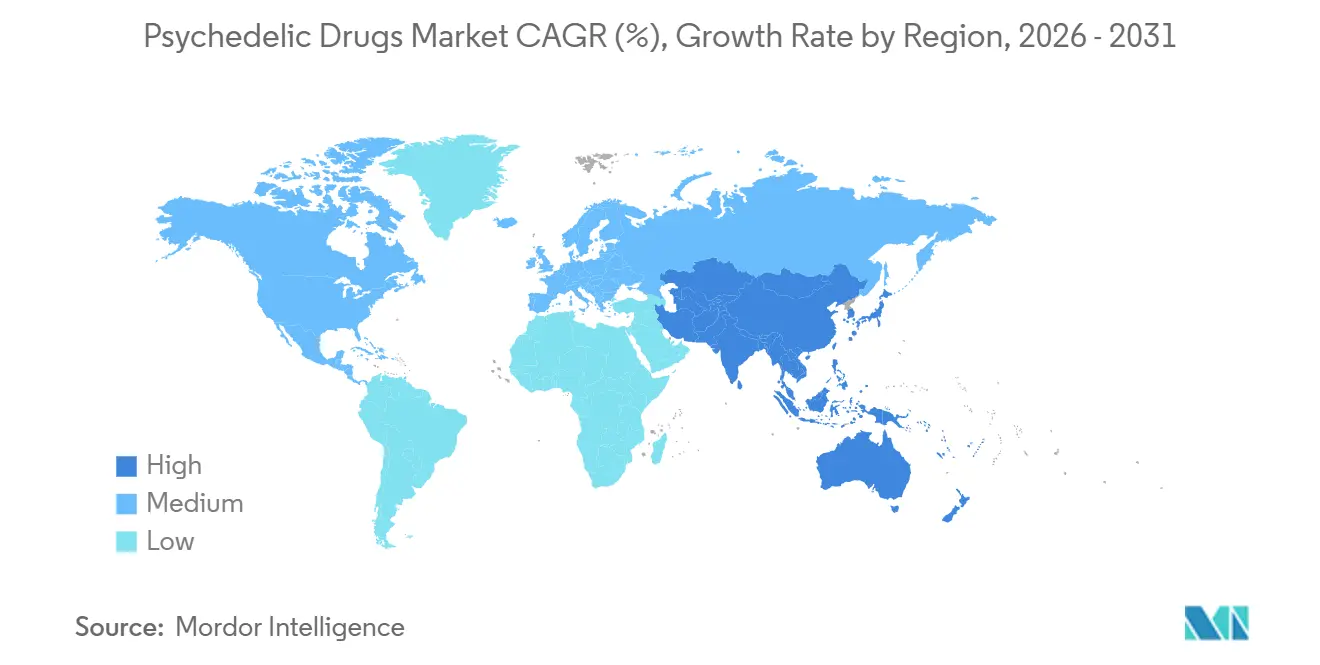

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Psychedelic Drugs Market Analysis by Mordor Intelligence

The psychedelic drugs market size was valued at USD 4.08 billion in 2025 and estimated to grow from USD 4.63 billion in 2026 to reach USD 8.75 billion by 2031, at a CAGR of 13.55% during the forecast period (2026-2031). The forecast implies that the psychedelic drugs industry will roughly double in absolute value within five years as the pipeline of late-stage assets advances, investors are recalibrating their risk–reward view of novel neuro-psychiatric treatments. The pipeline is enriched by a growing number of next-generation molecules that seek to retain therapeutic power while reducing hallucinogenic intensity, hinting at a future where psychedelic therapy becomes a routine medical option. Internal estimates suggest that every 1% improvement in global treatment-resistant depression outcomes could unlock up to USD 1 billion in annual incremental prescription revenue, reinforcing why established pharmaceutical companies are now entering partnership deals. An emerging consensus is that the next adoption wave will be led by formal reimbursement decisions rather than headline-grabbing clinical breakthroughs.

Key Report Takeaways

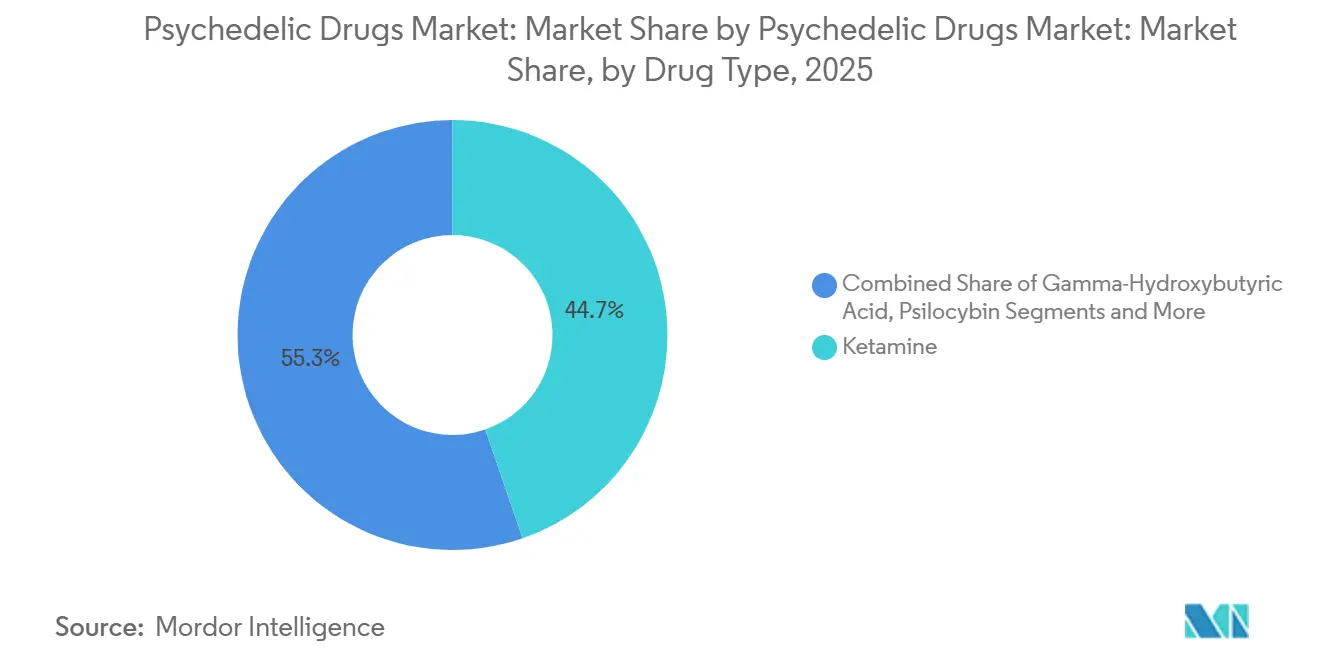

- By drug type, ketamine held 44.70% of the psychedelic drugs market share in 2025, while psilocybin is projected to advance at an 17.85% growth rate through 2031.

- By source, synthetic compounds accounted for 63.80% of revenue in 2025, whereas naturally derived psychedelics are set to grow at a 14.2% rate over the forecast horizon.

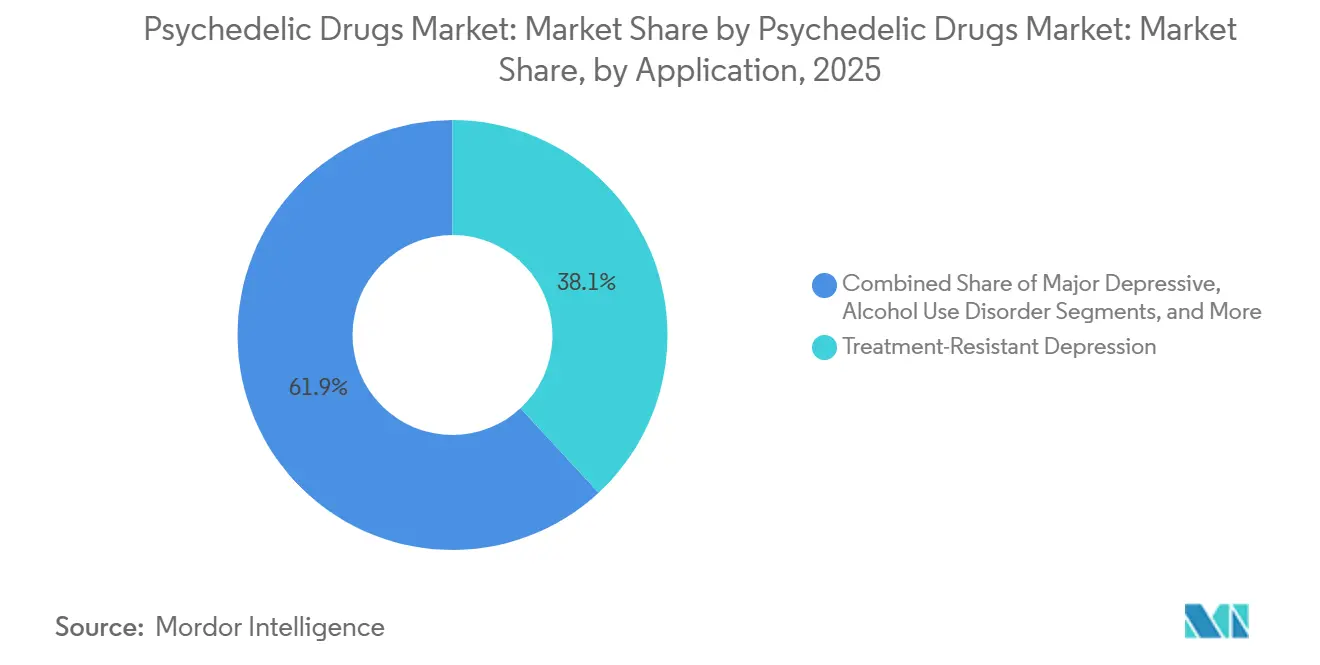

- By application, treatment-resistant depression captured a 38.10% share in 2025, and post-traumatic stress disorder therapies are forecast to rise at a 16.75% growth rate through 2031.

- By route of administration, oral formats led with a 55.20% share in 2025; intranasal products are expected to grow the fastest at 18.6% up to 2031.

- By distribution channel, hospital pharmacies managed 59.90% of 2025 sales, while online and telehealth platforms are projected to expand at a 21.4% growth rate by 2031.

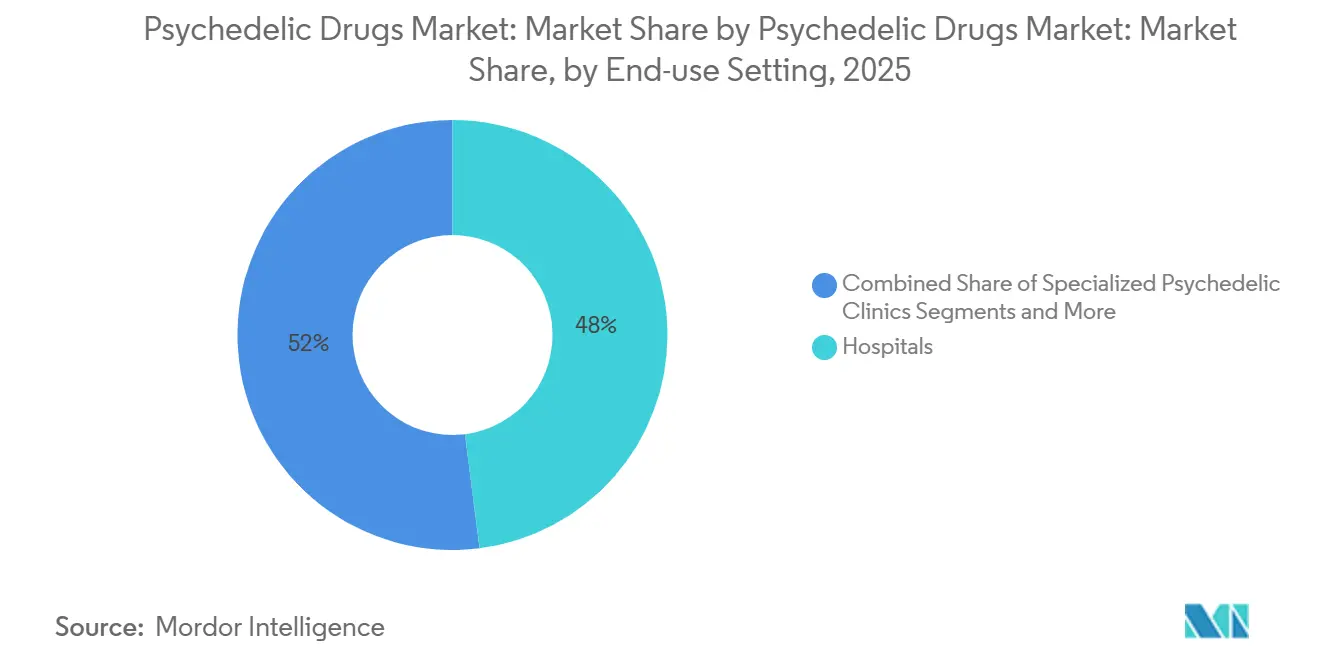

- By end-use setting, hospitals represented 48.00% of demand in 2025, and specialized psychedelic clinics are anticipated to grow at a 19.95% rate during the forecast period.

- By geography, North America commanded a 51.60% share in 2025; Asia-Pacific is on course for the quickest regional expansion with a 14.75% growth rate to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Psychedelic Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global prevalence of mental-health disorders and unmet therapeutic needs | +1.5% | Global | Medium term (~3-4 yrs) |

| Progressive regulatory shifts toward medicalization and de-scheduling of psychedelics | +1.2% | North America & Australia | Medium term (~3-4 yrs) |

| Escalating institutional & strategic investment fuelling R&D and commercial infrastructure | +0.8% | North America & EU | Short term (≤2 yrs) |

| Expansion of health-care delivery models enabling psychedelic-assisted therapy (clinics & tele) | +0.6% | Global | Medium term (~3-4 yrs) |

| Strategic pharma-biotech alliances targeting novel psychedelics | +0.5% | North America & EU | Short term (≤2 yrs) |

| Liberalization of controlled-substance laws and expansion of ketamine clinic networks | +0.4% | North America; early adopters in APAC | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

Rising Global Prevalence of Mental-Health Disorders and Unmet Therapeutic Needs

The escalating incidence of treatment-resistant depression and anxiety is expanding the psychedelic drugs market size by increasing the addressable patient pool. Phase 2 studies showing 75 % remission with psilocybin after two doses have amplified clinician interest because durable responses can lower total therapy hours per year. Health systems facing psychiatrist shortages are inferring that high-impact, low-frequency interventions could relieve bottlenecks in outpatient care. As awareness rises, patient advocacy groups are urging payers to reassess cost-effectiveness models that rely on long-term antidepressant adherence.

Progressive Regulatory Shifts Toward Medicalization and De-Scheduling of Psychedelics

More explicit FDA[1]U.S. Food and Drug Administration, “Psychedelic Drugs: Considerations for Clinical Investigations,” U.S. Food and Drug Administration, fda.govguidance on clinical trial design and breakthrough designations is shortening development timelines, directly influencing psychedelic drugs market share capture by late-stage sponsors. Oregon and Colorado have issued licenses for supervised psilocybin services, creating data sets that federal agencies can review, which may speed national rescheduling. The inference here is that localized policy experiments are effectively functioning as phase 4 safety studies, giving regulators empirical assurance before national roll-outs. Australia’s precedent supports global policy diffusion because it shows that medicalized use can coexist with stringent supply-chain controls.

Escalating Institutional and Strategic Investment Fueling R&D and Commercial Infrastructure

Capital inflows, illustrated by USD 296 million raised in 2023, allow small biotechs to fund multi-center trials in parallel rather than sequentially. AbbVie’s USD 2 billion neuroplastogen alliance signals that big-pharma due diligence thresholds have been met, which encourages additional strategic investors. A new inference is that deal structures increasingly include joint commercialization options for co-developed clinics, implying that drug makers plan to influence delivery networks, not just molecule discovery. Traditional banks that once excluded Schedule I assets from portfolios now field specialist analyst coverage, reflecting growing institutional confidence.

Expansion of Health-Care Delivery Models Enabling Psychedelic-Assisted Therapy

Purpose-built clinics are proliferating, with a 20% annual opening rate, and are differentiating themselves through aesthetics and integration coaching services. Tele-health platforms extend reach by conducting pre-screening and post-integration remotely, which reduces on-site visit frequency and patient travel costs. An emergent inference is that hybrid care models will determine whether the psychedelic drugs industry growth remains urban-centric or spreads to underserved rural areas. Partnerships such as Compass Pathways and Mindful Health Solutions suggest that pharma companies see treatment ecosystem design as a risk-mitigation tool for regulators concerned about safety.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited insurance coverage and reimbursement pathways | -1.0% | North America & EU | Short term (≤2 yrs) |

| Persisting societal stigma and patient acceptance barriers | -0.7% | APAC core, spill-over to MEA | Long term (≥5 yrs) |

| Adverse-event management requiring certified psychotherapists | -0.5% | Global | Medium term (~3-4 yrs) |

| High assisted-therapy session costs hindering payer reimbursement | -0.4% | North America & EU | Medium term (~3-4 yrs) |

| Source: Mordor Intelligence | |||

Limited Insurance Coverage and Reimbursement Pathways

The absence of standard payer codes keeps patient out-of-pocket costs high and may delay widespread uptake. Yet, it also incentivizes providers to experiment with bundled-payment models that package drug, therapy, and follow-up. Early health economic analyses indicate that two psilocybin sessions can offset a year’s worth of antidepressant spend, a data point that resonates with cost-containment committees. The inference is that once a single large public insurer covers a psychedelic intervention, private insurers will quickly follow to avoid the perception of denying effective care. Jurisdictional variability, however, means sponsors must prepare country-specific pharmacoeconomic dossiers.

Persisting Societal Stigma and Patient Acceptance Barriers

Schedule I classification reinforces public skepticism, and some clinicians fear reputational damage from association with hallucinogens. Education campaigns led by research hospitals are reframing psychedelics as neuro-plasticity modulators rather than recreational substances, reshaping discourse. A fresh inference is that testimonials from military veterans successfully treated for PTSD create persuasive narratives that bridge scientific data and public empathy. United Nations concerns about premature commercialization highlight the need for evidence-based marketing codes to avoid backlash.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Ketamine hold Majority of the Market Share

Ketamine holds 44.70% psychedelic drugs market share in 2025. Novel oral extended-release tablets are reducing dissociation events, which supports broader psychiatric adoption. A logical inference is that dosing convenience will pivot ketamine toward maintenance therapy regimes, increasing repeat-prescription revenue streams. Psilocybin, growing at 17.85% annually, benefits from double breakthrough therapy designations, positioning it as the fastest mover in the psychedelic drugs industry pipeline.

Psilocybin’s synthetic analogs aim to shorten hallucinogenic duration, enabling community clinic roll-out without overnight stays. MDMA’s pending PTSD approval could shift payer focus from depression to trauma care, diversifying the revenue mix. The segment’s competitive pressure is steering smaller developers toward ultra-rare indications to secure orphan designation advantages. As new chemical entities emerge, drug-type diversification reduces reliance on single-asset success and strengthens overall market resilience.

By Source: Synthetic Compounds Command Significant Share

Synthetic compounds command 63.80% psychedelic drugs market size in 2025 because GMP manufacturing underpins regulatory acceptance. The inference is that batch consistency reduces the risk of trial delays due to product variability, an often-overlooked cost driver. Growing consumer trust in “natural” mental health aids, however, lifts demand for botanically derived psilocybin, granting that niche a 14.2% growth rate.

Semi-synthetic hybrids are capitalizing on the authenticity narrative while retaining patent life, creating a bridge between pharmaceutical rigor and consumer perception. Extraction-purification advances now yield micro-crystalline psilocin with impurity profiles that satisfy pharmacopeia standards, blurring the old natural-versus-synthetic divide. A strategic inference is that IP filings around purification technology could become as valuable as those for new molecules, a trend mirrored in cannabis markets.

By Application: Treatment-resistant Depression Dominates the Market

Treatment-resistant depression accounts for 38.10% psychedelic drugs market share in 2025 and remains the anchor indication for most late-stage assets. Superior remission durability means mental-health providers can reallocate therapist hours to other conditions, improving clinic economics. PTSD, advancing at a 16.75% CAGR, is poised for acceleration if MDMA secures FDA approval, because the veteran care population provides an organized patient funnel.

Substance-use disorder trials aim to leverage psychedelics’ ability to reset reward pathways, an approach supported by early data on alcohol-use remission. An inference is that success in addiction treatment could prompt cross-referral from rehabilitation centers, integrating psychedelics into mainstream recovery protocols. Combination therapy studies that pair psychedelics with cognitive behavioral therapy may further elevate efficacy, enhancing payer appeal.

By Route of Administration: Oral hold Majority of the Market

Oral formulations hold 55.20% psychedelic drugs market share in 2025 due to patient familiarity and scalable manufacturing. Extended-release tablets reduce clinic time, hinting that partial home-use protocols could emerge once safety data mature. Intranasal products grow at 18.6% yearly, driven by esketamine’s commercial performance, and offer a near-immediate onset, which is attractive for acute suicidal ideation cases.

The pending Phase 2b results for intranasal mebufotenin Benzoate could validate rapid-acting short-duration psychedelics, widening the pool of ambulatory settings. Sublingual films are in pre-clinical stages and promise improved bioavailability without needles, suggesting that route-of-administration innovation is key to patient segmentation strategies.

By Distribution Channel: Hospital Control the Majority of the Market

Hospital pharmacies control 59.90% of the psychedelic drugs market size in 2025 because current protocols demand controlled-environment dispensing. This dominance ensures robust chain-of-custody compliance, a priority for regulators tracking diversion risks. Online and tele-health channels grow at 21.4% as digital triage streamlines referrals, hinting at eventual share erosion for hospital channels.

Pharmacy benefit managers are evaluating psychedelics as specialty drugs, which could shift distribution toward accredited specialty pharmacies. An inference is that supply-chain traceability technology developed for opioids may be repurposed for psychedelics, satisfying oversight needs while enabling mail-order fulfillment for certain formulations.

By End-Use Setting: Hospital attain the Significant Market Share

Hospitals hold 48.00% of the psychedelic drugs market share in 2025, offering a built-in emergency response, which reassures hesitant regulators. Clinic networks dedicated to psychedelic therapy expand at 19.95% per year and use spa-like environments to enhance patient comfort, an approach that appears to improve session completion rates.

Research institutes remain indispensable for protocol refinement and therapist training, solidifying academic-commercial linkages that accelerate knowledge transfer. A forward-looking inference is that home-care administration will emerge for non-hallucinogenic psychoplastogens, marking a step change in scalability once first-in-class approvals arrive.

Geography Analysis

North America, with a 51.60% psychedelic drugs market share in 2025, combines progressive state policy, substantial venture capital, and premier academic centers. Massachusetts’ creation of a Natural Psychedelic Substances Commission, funded via a 15% sales tax, exemplifies how states monetize and regulate simultaneously. Johns Hopkins secured USD 55 million in philanthropy to expand psilocybin programs, illustrating that non-dilutive funding is abundant for high-profile research. The region also houses most specialty clinic chains, yielding dense referral networks that drive patient throughput. A strategic inference is that this density will support outcome-based reimbursement pilots because large patient volumes yield statistically robust data.

Europe ranks second by revenue, paced by the United Kingdom’s Clerkenwell Health facility, the continent’s first commercial psychedelic trials hub. Germany’s pharmaceutical ecosystem gives local firms an edge in GMP manufacturing of psychedelic APIs, while Switzerland leverages historical expertise in psychedelic chemistry to attract cross-border trials. The European Medicines Agency has signaled its willingness to engage in adaptive trial designs, creating alignment with smaller biotech budgets. An inference is that pan-European clinical trial networks could accelerate data collection by harmonizing ethics approvals, countering the perception of a slow regulatory environment.

Asia-Pacific grows at 14.75% CAGR, led by Australia’s federal rescheduling decision that entrenches its role as regional trailblazer. High treatment costs in early clinics demonstrate that affluent patients will self-fund, hinting that private-pay demand can bootstrap clinical infrastructure before insurance arrives. China’s emerging psychedelic retreat market blends traditional medicine concepts with modern mindfulness, suggesting cultural adaptation pathways distinct from Western medical models. Japan monitors developments but continues to fund basic research under its state mental-health initiative, laying the groundwork for future clinical translation. The inference is that Asia-Pacific growth will hinge on a mix of medical tourism and gradual domestic liberalization, a pattern earlier seen in cannabis markets.

Competitive Landscape

The psychedelic drugs industry consists of a two-tier structure: large pharmaceutical incumbents holding commercial products and a swarm of venture-backed biotechs advancing novel assets. Johnson & Johnson’s Janssen division anchors the market with Spravato, which delivered USD 689 million in revenue in 2023, proving that payer acceptance can follow strong safety monitoring protocols. The blockbuster trajectory of an intranasal esketamine reinforces investor conviction that psychedelics can meet traditional commercial benchmarks. An inference is that financial analysts now model psychedelic assets with risk-adjusted sales curves comparable to oncology agents at similar stages.

Strategic collaborations dominate growth strategy, as illustrated by AbbVie’s USD 2 billion neuroplastogen deal with Gilgamesh, which front-loads development risk onto the biotech while giving AbbVie future commercial rights. The emphasis on non-hallucinogenic psychoplastogens reflects a push to simplify care delivery, thereby widening the payor base beyond supervised clinic settings. Smaller companies, like Delix Therapeutics, target patent-protected analogs with rapid onset and short duration, carving defensible niches. An inference here is that intellectual property wars may shift from molecule claims to method-of-use and digital-protocol patents as clinical practice evolves.

Service providers such as Field Trip Health, Mindbloom, and Numinus extend the competitive arena beyond molecules, integrating therapy protocols, digital tracking, and real-world data capture. These platforms feed anonymized outcomes back to drug developers, accelerating iterative protocol refinement. An unspoken advantage is that ownership of longitudinal patient data could position service firms as indispensable partners once payers demand evidence of cost-effectiveness. As a result, competitive advantage is migrating toward those who control both the drug asset and the experience layer.

Psychedelic Drugs Industry Leaders

Johnson & Johnson

Jazz Pharmaceuticals

COMPASS Pathways

MindMed Inc.

Cybin Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Colorado licensed its first psilocybin healing center. The facility now operates under the state’s Natural Medicine Health Act and sets transparent pricing for supervised psilocybin services.

- May 2024: AbbVie and Gilgamesh Pharmaceuticals announced a USD 2 billion collaboration aimed at non-hallucinogenic neuroplastogens. The partnership combines AbbVie’s commercialization muscle with Gilgamesh’s discovery platform.

- March 2024: Cybin secured FDA Breakthrough Therapy Designation for CYB003 in Major Depressive Disorder. The decision followed Phase 2 data indicating 75% remission after two doses.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the psychedelic drugs market as the regulated and investigational sale of hallucinogenic pharmaceuticals, including ketamine, psilocybin, LSD, MDMA, DMT, ibogaine, mescaline, and GHB, formulated for mental health, pain, or neurologic indications and supplied through licensed medical channels or clinical trial programs.

Scope Exclusion: Recreational or illicit sales, smart-shop botanicals, and non-psychoactive placebo kits fall outside this study.

Segmentation Overview

- By Drug Type

- Gamma-Hydroxybutyric Acid (GHB)

- Ketamine

- Psilocybin

- Lysergic Acid Diethylamide (LSD)

- 3,4-Methylenedioxymethamphetamine (MDMA)

- Dimethyltryptamine (DMT)

- Ibogaine

- Mescaline

- Other Drug Types

- By Source

- Naturally-Derived

- Synthetic

- By Application

- Treatment-Resistant Depression

- Major Depressive Disorder

- Post-Traumatic Stress Disorder (PTSD)

- Substance & Opiate Addiction

- Anxiety & Panic Disorders

- Narcolepsy & Sleep Disorders

- Alcohol Use Disorder

- Other Applications

- By Route of Administration

- Oral

- Intranasal

- Intravenous

- Sublingual / Buccal

- Transdermal & Others

- By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online & Telehealth Platforms

- Other Distribution Channels

- By End-use Setting

- Specialized Psychedelic Clinics

- Hospitals

- Research & Academic Institutes

- Homecare Settings

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing psychiatrists, hospital pharmacy managers, CRO executives, and reimbursement advisors across North America, Europe, Asia-Pacific, and LATAM. These discussions verified pricing spreads, dose frequencies, and off-label penetration, and helped us refine uptake curves for novel agents.

Desk Research

Our desk work starts with clinical trial repositories such as ClinicalTrials.gov and EudraCT, which reveal pipeline attrition rates and enrollment volumes that feed incidence-to-treatment ratios. We then gather prevalence data and prescription cost benchmarks from the World Health Organization, U.S. National Institute of Mental Health, Eurostat, and Japan's MHLW. Trade associations, such as the American Psychiatric Association and the European College of Neuropsychopharmacology, provide dosing guidelines that anchor average treatment cost estimates. Company 10-Ks, investor decks, and FDA advisory transcripts clarify launch timelines and initial list prices. Finally, proprietary databases (D&B Hoovers and Dow Jones Factiva) supply audited revenue trails for listed manufacturers. The sources named are illustrative; many additional references were reviewed to cross-check facts and fill gaps.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort build establishes the demand pool, which is then stress tested through selective bottom-up supplier roll-ups of ketamine clinic volumes and compassionate use shipments. Key model drivers include diagnosed cases of treatment-resistant depression, average annual cost per psychedelic session, regulatory approval cadence, reimbursement coverage ratios, and clinic capacity additions. A multivariate regression links these variables to historical sales, while ARIMA smoothing handles short data runs. Where country-level unit data are missing, we interpolate using mental health expenditure per capita and adjust with primary source insights.

Data Validation & Update Cycle

Outputs pass a three-layer analyst review, variance checks against external sales trackers, and scenario reruns when pivotal events (e.g. FDA priority review) occur. The dataset refreshes yearly, with interim updates for material approvals.

Why Mordor's Psychedelic Drugs Baseline Commands Reliability

Published estimates often diverge because firms pick different drug baskets, pricing anchors, and refresh cadences.

Key gap drivers include some studies that fold in over-the-counter botanicals or illicit channels, others that rely solely on manufacturer revenue without adjusting for off-label clinic mark-ups, and a few that apply uniform global ASPs that ignore reimbursement caps in emerging markets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.08 B (2025) | Mordor Intelligence | - |

| USD 3.31 B (2024) | Global Consultancy A | Excludes MDMA pipeline and clinic mark-ups |

| USD 3.88 B (2025) | Trade Publication B | Counts only synthetic molecules; omits natural psilocybin programs |

| USD 5.56 B (2024) | Industry Association C | Includes recreational sales estimates and broad mental health supplements |

These comparisons show that Mordor's clear scope boundaries, dual-track modeling, and annual audit yield a balanced, reproducible baseline that decision makers can trust.

Key Questions Answered in the Report

What is the current psychedelic drugs market size?

The psychedelic drugs market size stands at USD 4.63 billion in 2026.

How fast is the psychedelic drugs industry expected to grow?

It is forecast to reach USD 8.75 billion by 2031, representing a 13.55% CAGR.

Which drug type dominates the psychedelic drugs market?

Ketamine accounts for 44.70% market share, supported by FDA-approved uses for treatment-resistant depression.

Which region holds the highest psychedelic drugs market share?

North America leads with 51.60% market share due to favorable state regulations and extensive research infrastructure.

Which region has the biggest share in Psychedelic Drugs Market?

In 2025, the North America accounts for the largest market share in Psychedelic Drugs Market.

Why is psilocybin considered the fastest-growing psychedelic segment?

Breakthrough therapy designations and positive remission data for depression are accelerating psilocybin’s clinical adoption.

What are the main barriers to wider psychedelic therapy adoption?

Key obstacles include uncertain reimbursement pathways, societal stigma, and the need for specialized delivery infrastructure.

Page last updated on: