Benzodiazepine Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.81 Billion |

| Market Size (2031) | USD 3.22 Billion |

| Growth Rate (2026 - 2031) | 2.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

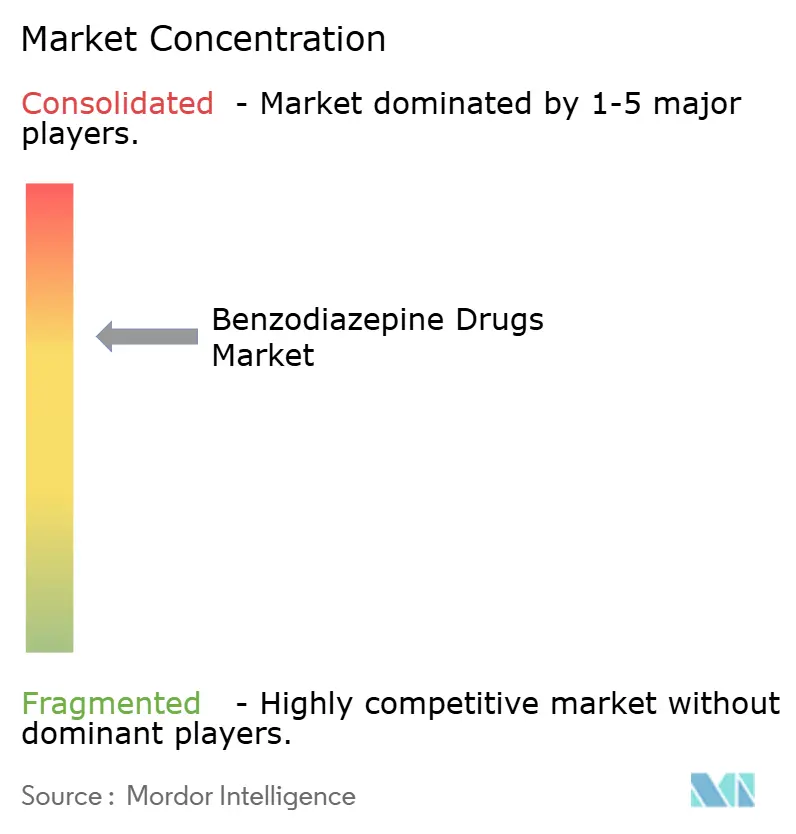

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benzodiazepine Drugs Market Analysis by Mordor Intelligence

benzodiazepine drugs market size in 2026 is estimated at USD 2.81 billion, growing from 2025 value of USD 2.73 billion with 2031 projections showing USD 3.22 billion, growing at 2.79% CAGR over 2026-2031. Demand stays resilient because anxiety prevalence remains high, hospital protocols still favor rapid-acting sedatives, and regulators now allow controlled telemedicine prescribing. Growth also stems from expanding intranasal and pediatric indications, wider generic uptake in emerging economies, and steady uptake in alcohol-withdrawal protocols. Counterbalancing forces include stringent monitoring rules, recurring API shortages, and substitution by non-benzodiazepine anxiolytics, yet the net effect keeps the benzodiazepine drugs market on a measured upward path.

Key Report Takeaways

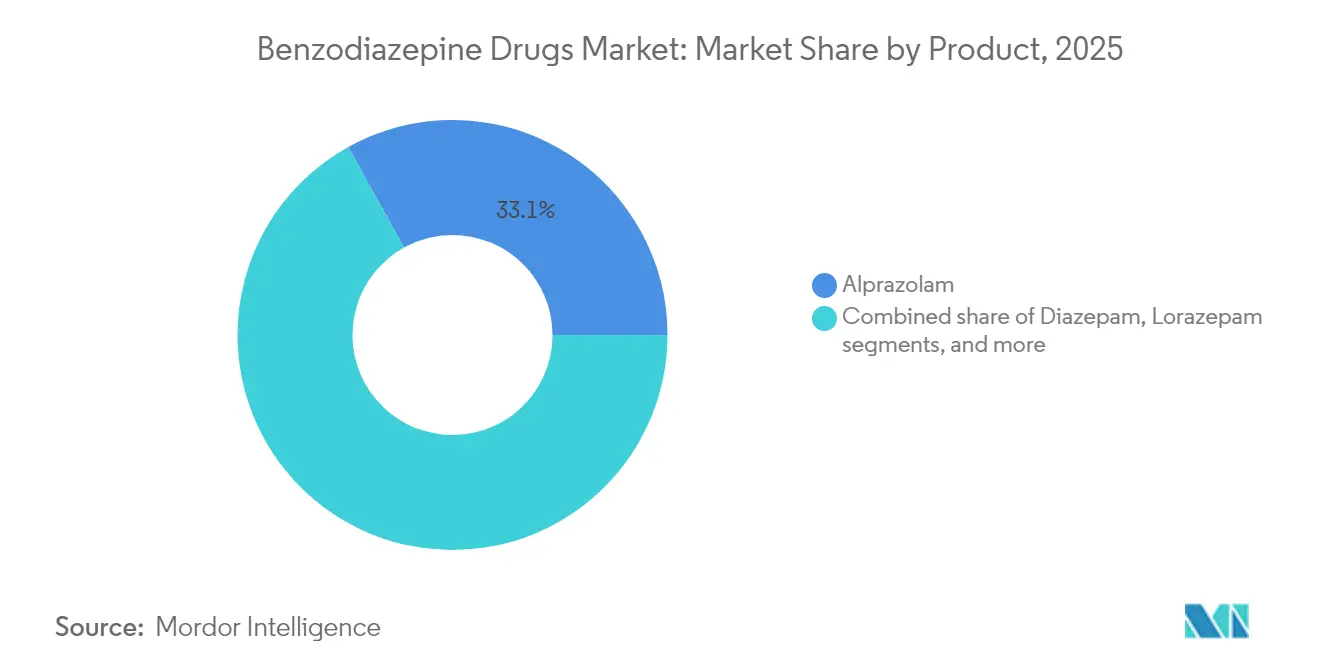

- By product, alprazolam led with a 33.05% revenue share in 2025, while diazepam is projected to post the fastest 4.16% CAGR through 2031.

- By application, anxiety disorders accounted for 54.10% of the benzodiazepine drugs market size in 2025; alcohol-withdrawal therapy is set to grow at a 3.58% CAGR.

- By time of action, short-acting agents captured 47.40% of the benzodiazepine drugs market share in 2025; ultra-short options are poised to register a 4.21% CAGR.

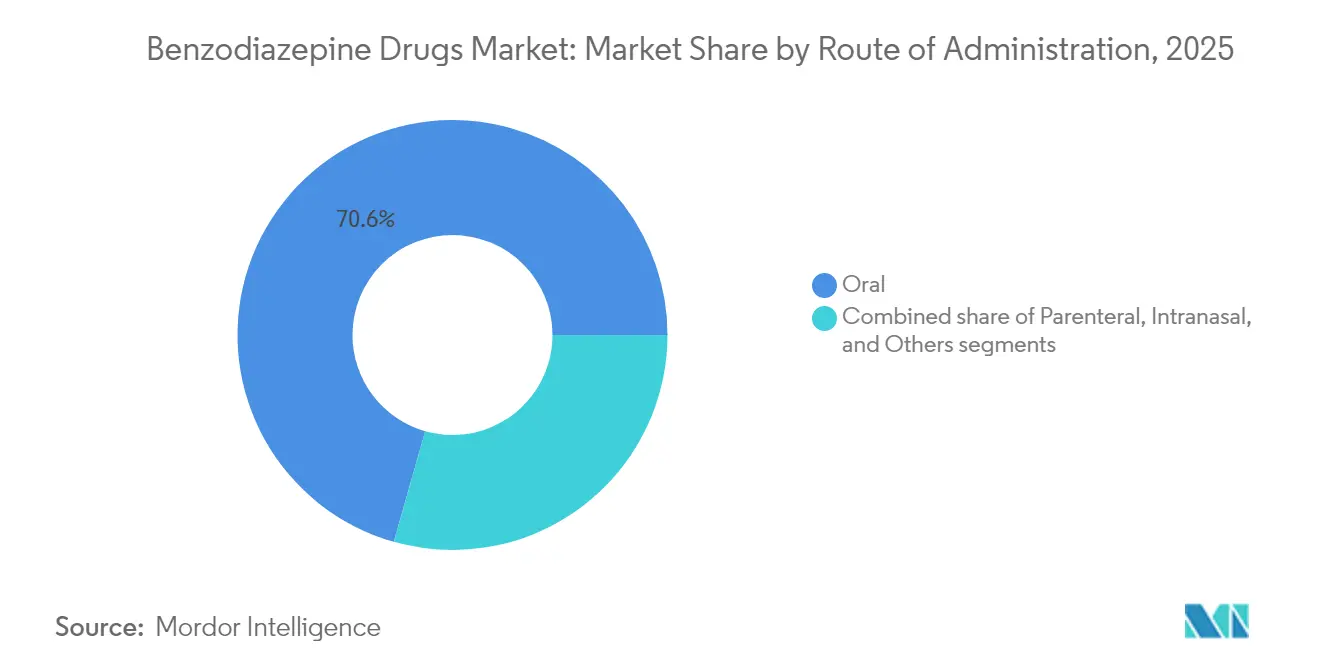

- By route of administration, oral forms held 70.60% share, whereas intranasal products are expanding at a 3.74% CAGR.

- By distribution channel, hospital pharmacies dominated with a 51.30% share in 2025; online pharmacies show the fastest 3.83% CAGR.

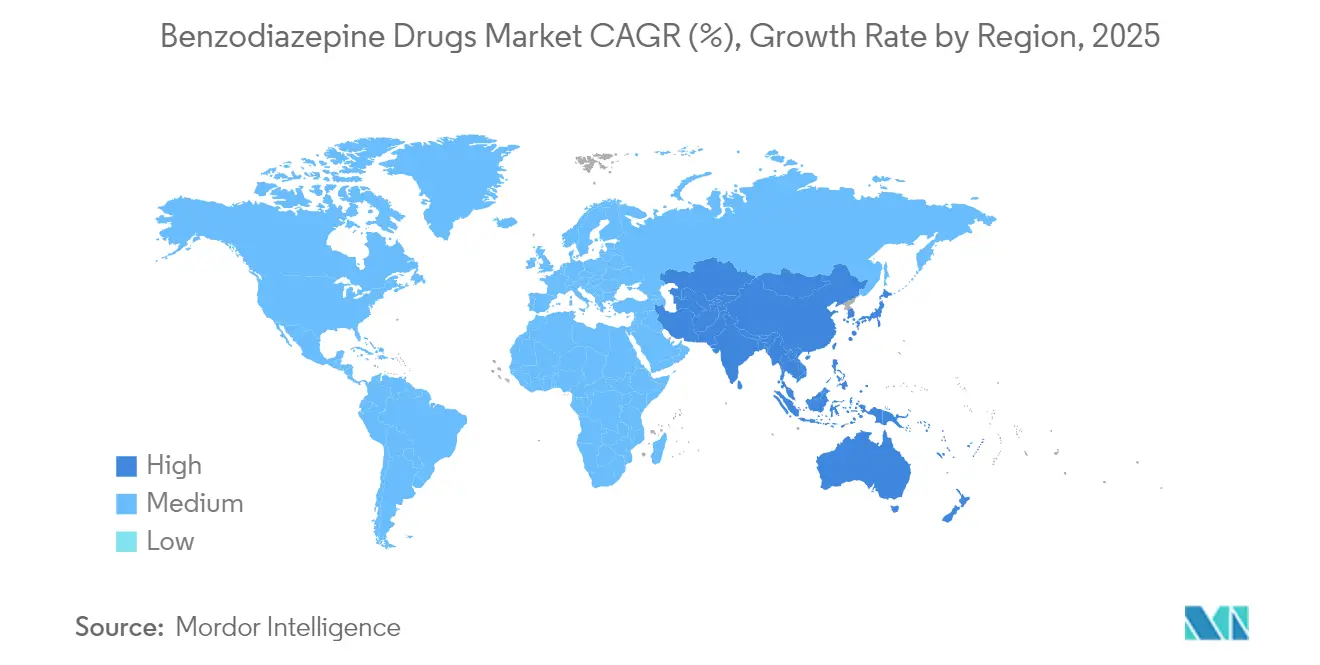

- North America represented 40.10% of revenue in 2025; Asia-Pacific is the quickest-growing region at a 3.25% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Benzodiazepine Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of anxiety & panic disorders | +0.8% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Ageing population with multiple comorbidities | +0.6% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Increasing insomnia linked to digital-lifestyle fatigue | +0.5% | North America & EU, emerging in urban APAC | Medium term (2-4 years) |

| Growing adoption of low-cost generics | +0.4% | APAC core, spill-over to Latin America | Short term (≤ 2 years) |

| Expansion of palliative-care protocols using benzodiazepines | +0.3% | Global, early gains in developed healthcare systems | Long term (≥ 4 years) |

| Shortages of alternative anti-anxiety APIs driving formulary substitution | +0.2% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Anxiety & Panic Disorders

Global anxiety incidence keeps climbing, especially in BRICS economies. U.S. data showed 18.2% of adults screened positive for anxiety symptoms in 2025, up from pre-pandemic baselines. This epidemiological pressure sustains prescriptions even as guidelines tighten. Reproductive-age women report higher medication adherence, amplifying script volumes. Telehealth now broadens reach, notably after the DEA allowed Schedule III-V benzodiazepine e-prescribing under special registration rules. Professional bodies nevertheless push gradual tapering[1]American Society of Addiction Medicine Staff, “Benzodiazepine Tapering,” asam.org for long-term users, underscoring the balancing act between need and safety.

Ageing Population with Multiple Comorbidities

Aging societies contribute a steady patient pool with anxiety, insomnia and seizure comorbidity. A 2024 seven-nation survey[2]Teodora Babici, “Prevalence and Patterns of Benzodiazepine Use in Older Europeans,” BMC Geriatrics, biomedcentral.com found 14.9% benzodiazepine use among Europeans aged 65+, peaking at 35.5% in Croatia. Prescribers prefer longer-acting diazepam for simplified dosing yet must monitor fall and cognition risks. Health agencies promote deprescribing campaigns, but the clinical reality of complex multimorbidity keeps benzodiazepines in geriatric toolkits.

Increasing Insomnia Linked to Digital-Lifestyle Fatigue

Remote work and device overuse disrupt circadian rhythms. Novel partial modulators such as dimdazenil promise fewer cognitive effects, signaling industry innovation toward safer sleep aids. Younger adults now drive short-acting demand, but regulators first recommend behavioral therapy, placing a ceiling on volume growth.

Growing Adoption of Low-Cost Generics

Patent expiries and new capacity spur generic substitution. A Brazilian primary-care audit recorded 29.1% prolonged use, often at supra-guideline doses, spotlighting both affordability and misuse risk. Established generic firms with stringent quality systems gain share as intermittent shortages hit smaller rivals.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High risk of dependence, abuse & diversion | -0.9% | Global, most severe in North America | Medium term (2-4 years) |

| Intensifying regulatory scrutiny & up-scheduling initiatives | -0.7% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Emergence of non-benzo anxiolytics (e.g., Z-drugs, CBD-based) | -0.5% | North America & EU, early adoption in urban centers | Medium term (2-4 years) |

| API supply-chain vulnerabilities (China–India chokepoints) | -0.3% | Global, concentrated impact on generic manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Risk of Dependence, Abuse & Diversion

Designer analogues fuel overdose deaths, with 141 fatalities linked in the last one and a half decades. Scottish prison screens frequently detect etizolam, illustrating illicit penetration. Young adult prescribing has crept upward since 2008, diverging from the overall decline, driving regulators to intensify monitoring. The UK has already proposed Class C controls on fifteen novel agents.

Intensifying Regulatory Scrutiny & Up-Scheduling Initiatives

New DEA telemedicine rules introduce multi-tier registration and mandatory PDMP checks. China shifted midazolam to Category I in July 2024, adding license hurdles and full-chain traceability. In Europe, the EMA lorazepam Macure referral showcased the bloc’s willingness to harmonize labelling when member states disagree. Smaller firms face rising compliance costs, potentially thinning supplier pools.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Alprazolam Dominance Faces Diazepam Renaissance

In 2025, alprazolam generated 33.05% of revenue, anchoring the benzodiazepine drugs market size. Demand stems from frontline anxiety protocols and prescriber familiarity. The benzodiazepine drugs market size for diazepam is projected to rise at a 4.16% CAGR, fueled by seizure, alcohol-withdrawal, and pediatric nasal-spray extensions. Diazepam was again the most widely traded psychotropic agent, reported by 158 nations. Supply interruptions hit clonazepam and lorazepam during 2024, exposing how concentrated manufacturing magnifies the risk of shortage.

Innovators now pursue delivery upgrades. In April 2025, the FDA cleared diazepam nasal spray for children down to age 2, stretching exclusivity for Neurelis. Such milestones signal an era where differentiated formats rather than new molecules sustain margins within the benzodiazepine drugs market.

By Application: Anxiety Disorders Drive Volume While Alcohol Withdrawal Shows Promise

Anxiety disorders accounted for 54.10% of the benzodiazepine drugs market share in 2025, a position underpinned by persistently high symptom prevalence. Alcohol-withdrawal management, though smaller, will exhibit a 3.58% CAGR through 2031, aided by detox program growth and evidence favoring benzodiazepines for seizure prophylaxis.

Intranasal diazepam and midazolam have improved emergency seizure care response times. Insomnia scripts remain controlled as payers push non-drug therapies, yet technology-induced sleep disruption keeps a niche need alive. Muscle spasm relief and pre-operative sedation add incremental volumes.

By Time of Action: Short-Acting Formulations Lead Despite Ultra-Short Innovation

Short-acting agents held 47.40% of 2025 revenue, reflecting clinician desire for quick onset and lower accumulation. The benzodiazepine drugs market size tied to ultra-short molecules is forecast to grow at 4.21% CAGR, enabled by inhalable or vaporised technologies.

Staccato alprazolam reached peak plasma in 2 minutes versus 45 minutes orally, underscoring the clinical appeal of rapid delivery. Intermediate and long-acting options still serve elderly cohorts needing sustained coverage with fewer doses.

By Route of Administration: Oral Dominance Challenged by Intranasal Innovation

Oral tablets and capsules retained 70.60% of the benzodiazepine drugs market size in 2025, a function of ease, cost, and entrenched habits. Intranasal formats are expanding at 3.74% CAGR as they offer non-invasive, fast brain availability and bypass the hepatic first pass.

Supply shocks in injectable lorazepam after Akorn’s exit highlighted parenteral fragility. Academic work on nose-to-brain transfer confirms robust seizure mitigation in animal models for intranasal benzodiazepines. Sublingual and rectal forms stay niche for special-needs users.

By Distribution Channel: Hospital Pharmacies Lead While Online Growth Accelerates

Hospital pharmacies dispensed 51.30% of sales in 2025. Institutional controls, EHR linkage and formulary oversight keep this channel central. Retail outlets occupy a steady second position but face tighter audit trails.

Online pharmacies, aided by telepsychiatry, will post a 3.83% CAGR. A recent survey valued the global e-pharmacy space at USD 353.9 billion by 2032. DEA’s new telehealth framework tightens safeguards, yet patients still value discretion and convenience when sourcing controlled drugs

Geography Analysis

North America generated 40.10% of 2025 revenue and will grow at 2.32% CAGR. Anxiety prevalence of 18.2% in U.S. adults underscores continuing demand. Supply disruptions in clonazepam and lorazepam during 2024 revealed manufacturing concentration risks, while three-tier DEA rules now govern tele-prescribing.

Europe advances at 2.70% CAGR to 2031. Elderly prescription prevalence reaches 35.5% in Croatia, 33.5% in Spain, highlighting intra-region variance. EMA’s centralised referrals, such as for lorazepam Macure, harmonise safety messaging and ensure cross-border consistency. Surveillance of 36 new designer analogues keeps regulatory vigilance high.

Asia-Pacific records the fastest 3.25% CAGR. India saw a 113.30% surge in anxiety cases over three decades. China’s Category I reclassification of midazolam raises compliance stakes. Japan could soon launch the first locally approved diazepam nasal spray following Aculys Pharma’s orphan-drug submission. Markets in the Middle East & Africa and South America grow at roughly 2.9% under improved mental-health recognition and broader health-system funding.

Competitive Landscape

The benzodiazepine drugs market remains moderately consolidated. Leading manufacturers integrate API production, formulation and distribution to buffer cost shocks. Repeated shortages in 2024 shifted share toward firms that sustained supply.

Differentiation now pivots to abuse-deterrent designs and alternative delivery. Valtoco’s expanded paediatric nod in April 2025 exemplifies how targeted indications widen the addressable base. Patents on device-drug combinations protect price premia even as molecule patents lapse.

Smaller entrants face sizable regulatory and capital hurdles, especially after new telemedicine and up-scheduling rules. White-space opportunities lie in paediatric, intranasal and ultra-short action niches, yet require strong regulatory expertise to navigate complex, multi-jurisdiction oversight.

Benzodiazepine Drugs Industry Leaders

Bausch Health Companies Inc.

F. Hoffmann-La Roche AG

Pfizer Inc.

Teva Pharmaceutical Industries Ltd.

Viatris Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The US FDA broadened diazepam nasal spray (Valtoco) use to children aged 2-5, strengthening Neurelis’s paediatric seizure franchise.

- January 2025: The US DEA issued three telemedicine rules that enable Schedule III-V benzodiazepine e-prescribing under special registration, with mandatory PDMP checks.

- September 2024: Aculys Pharma submitted a Japanese NDA for diazepam nasal spray, the country’s first intranasal antiepileptic candidate.

- June 2024: The EMA completed its lorazepam Macure review, recommending status-epilepticus label updates and paediatric excipient warnings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the benzodiazepine drugs market covers every prescription-only benzodiazepine molecule approved for human use, irrespective of strength, dosage form, or indication, and tracks manufacturer-level revenues converted to United States dollars. These molecules are primarily dispensed for anxiety disorders, insomnia, seizure control, alcohol-withdrawal management, and procedural sedation across all major care settings.

Scope exclusion: Illicit designer analogs, veterinary tranquilizers, and hospital compounding of bulk diazepam are not counted.

Segmentation Overview

- By Product

- Alprazolam

- Diazepam

- Lorazepam

- Clonazepam

- Temazepam

- Others

- By Application

- Anxiety Disorders

- Seizures

- Insomnia

- Alcohol Withdrawal

- Other Applications

- By Time of Action

- Ultra-short Acting

- Short Acting

- Intermediate Acting

- Long Acting

- By Route of Administration

- Oral

- Parenteral

- Intranasal

- Others

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with psychiatrists, neurologists, hospital pharmacists, and generic-drug distributors spanning North America, Europe, and Asia-Pacific supply real-world insights on prescription duration, generic penetration, and anticipated guideline changes. Online surveys of insomnia patients in key countries validate refill frequency and channel preference, closing data gaps revealed during desk work.

Desk Research

Our analysts begin with publicly available pillars such as the US National Institute of Mental Health prescription audit tables, WHO mental-health prevalence dashboards, DEA controlled-substance quota files, and EMA/FDA approval archives, which clarify molecule availability and scheduling nuances. Trade statistics from UN Comtrade, anxiety-drug expenditure series released by national health ministries, and scholarly meta-analyses on benzodiazepine utilization trends provide volume and prevalence anchors. Paid data services, notably D&B Hoovers for company revenue splits and Dow Jones Factiva for regulatory event timelines, enrich the desk review. The sources cited are illustrative; many additional public and subscription assets inform interim checks.

Market-Sizing & Forecasting

A top-down model converts country-level prescription counts and standard-of-care prevalence into unit demand, which is then multiplied by weighted average selling prices to yield baseline value. Bottom-up roll-ups of leading supplier revenues plus sampled hospital purchase invoices act as reasonableness checks before totals are reconciled. Key variables include diagnosed anxiety prevalence, per-patient daily dose, generic share drift, unit ASP trajectories, regulatory deprescribing targets, and geriatrics share of population. Five-year forecasts apply multivariate regression with scenario analysis layered over ARIMA trend curves, and assumptions are stress-tested with our primary experts. Data gaps in bottom-up granularity are bridged by interpolation from nearest proxy nations and validated against shipment growth signals.

Data Validation & Update Cycle

Outputs undergo variance screens versus historic trends, peer values, and sentinel national statistics; anomalies trigger a second analyst review before sign-off. The model is refreshed annually, with ad-hoc updates after material events such as major label expansions or scheduling changes, ensuring clients always receive the latest view.

Why Mordor's Benzodiazepine Drugs Baseline Commands Reliability

Published market values often diverge because firms choose differing molecule baskets, starting years, and price erosion curves.

Key gap drivers include inclusion of veterinary sedatives, older base-year anchoring, or aggressive ASP decline assumptions that are not cross-checked with current reimbursement files.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.73 B (2025) | Mordor Intelligence | - |

| USD 2.80 B (2023) | Global Consultancy A | Counts veterinary and research-grade compounds |

| USD 3.36 B (2025) | Industry Association B | Bundles injectable anesthesia sub-segment and herbal OTC anxiolytics |

| USD 2.96 B (2021) | Regional Consultancy C | Uses older base year and assumes uniform 5 % annual ASP decline |

These comparisons show that Mordor's disciplined scope selection, current-year anchoring, and dual-path validation deliver a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How are new telemedicine regulations influencing benzodiazepine access in the United States?

The DEA’s special-registration framework now lets physicians prescribe Schedule III-V benzodiazepines via video visits, expanding patient reach but adding strict PDMP look-ups that limit potential misuse.

Which benzodiazepine delivery formats are gaining the most traction among clinicians?

Intranasal sprays and other rapid-acting, device-based formulations are increasingly favored because they provide faster symptom control and incorporate features that deter diversion.

What supply-chain vulnerabilities should executives monitor for benzodiazepine products?

Dependence on a small group of API plants in China and India makes the market prone to shortages when factories face regulatory, quality or logistics disruptions.

How is regulatory up-scheduling outside the United States affecting global distribution strategies?

Countries such as China have moved certain molecules into stricter psychotropic categories, compelling manufacturers to secure additional licences and implement end-to-end traceability before shipping product.

Why are abuse-deterrent technologies becoming a key competitive differentiator?

Devices and formulations that minimize tampering not only meet tightening safety expectations but also enable premium pricing and longer periods of brand protection despite heavy generic penetration.

Page last updated on: