Antidepressant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

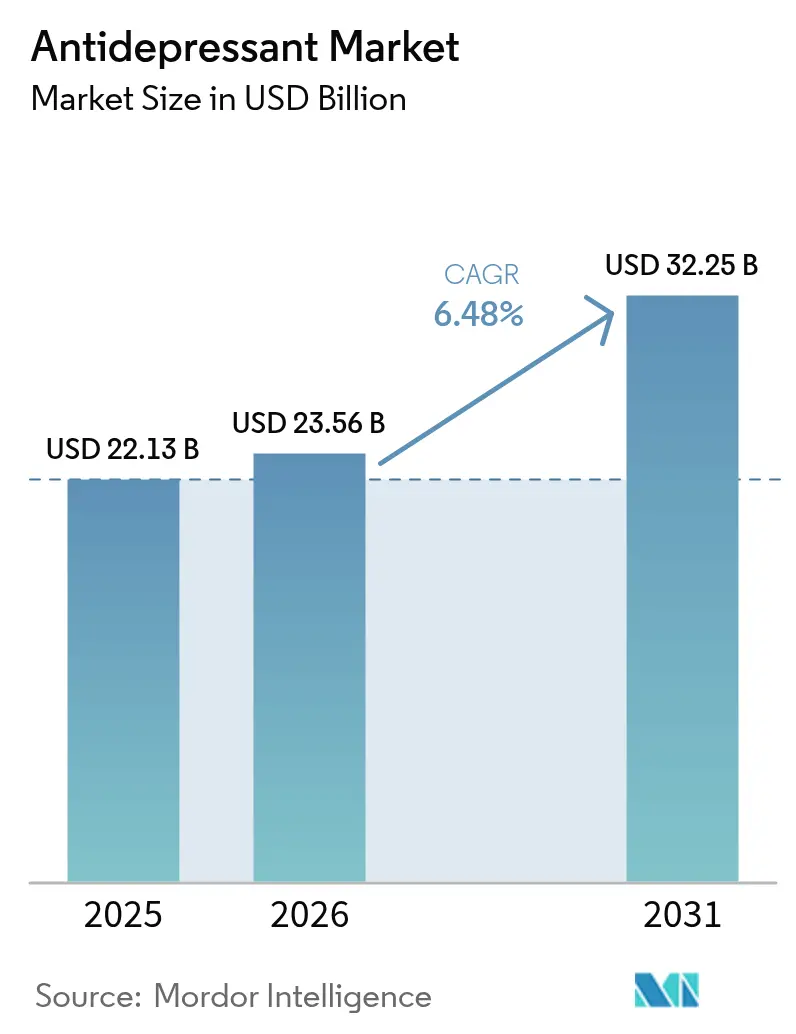

| Market Size (2026) | USD 23.56 Billion |

| Market Size (2031) | USD 32.25 Billion |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

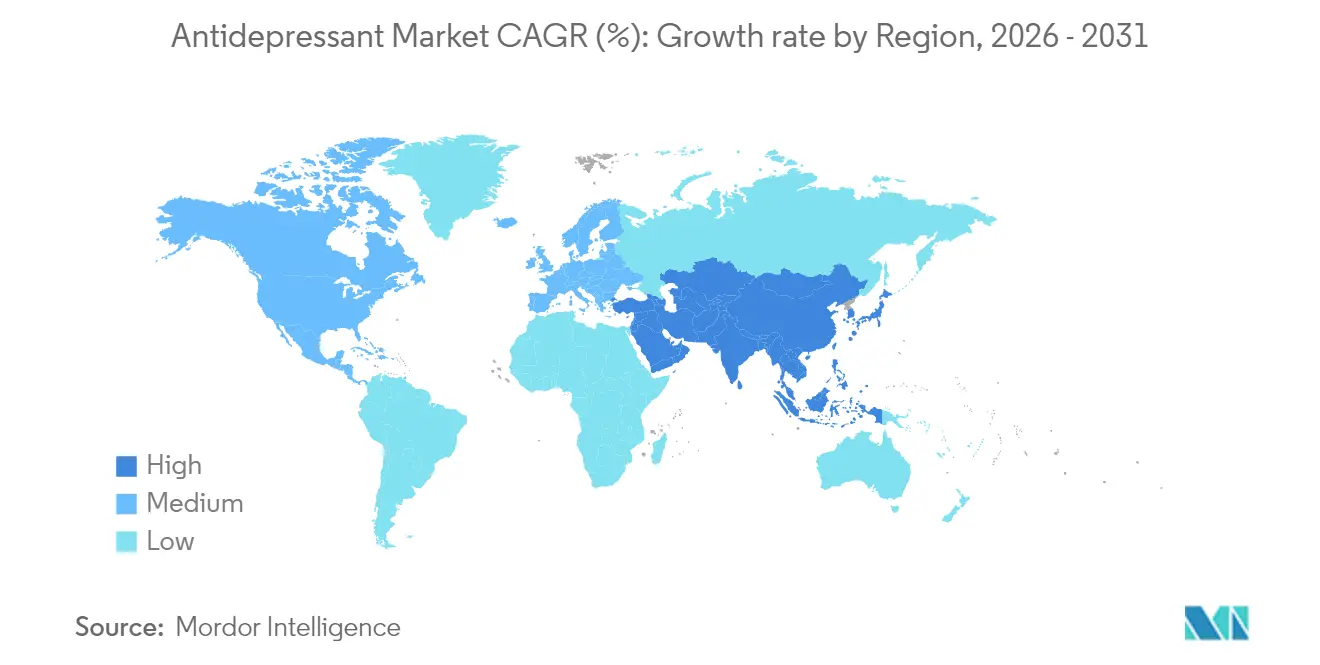

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antidepressant Market Analysis by Mordor Intelligence

The antidepressants market size was valued at USD 22.13 billion in 2025 and estimated to grow from USD 23.56 billion in 2026 to reach USD 32.25 billion by 2031, at a CAGR of 6.48% during the forecast period (2026-2031). Growth rests on rapid-acting glutamatergic medicines that shorten symptom-relief times, AI-enabled precision prescribing, and steady uptake of telehealth-based mental-health services. North America anchors demand, yet Asia-Pacific now dictates the steepest growth curve as stigma recedes and insurance cover widens. Intensifying competitive activity ranges from the USD 14.6 billion Johnson & Johnson-Intra-Cellular Therapies deal to a string of FDA fast-track designations for next-generation agents[1]Source: Johnson & Johnson, “Johnson & Johnson Closes Landmark Intra-Cellular Therapies Acquisition to Solidify Neuroscience Leadership, jnj.com . Regulatory flexibility around novel mechanisms (for example, the FDA’s 2025 esketamine monotherapy clearance) pairs with expanding digital front doors to care, creating sizable entry points for innovators. Patent-expiring brands and ensuing generic erosion temper topline prospects, yet focused lifecycle and combination-therapy tactics cushion revenue gaps. Meanwhile, sustainability mandates on active-pharmaceutical-ingredient (API) discharge tighten cost structures but reward early adopters of green chemistry.

Key Report Takeaways

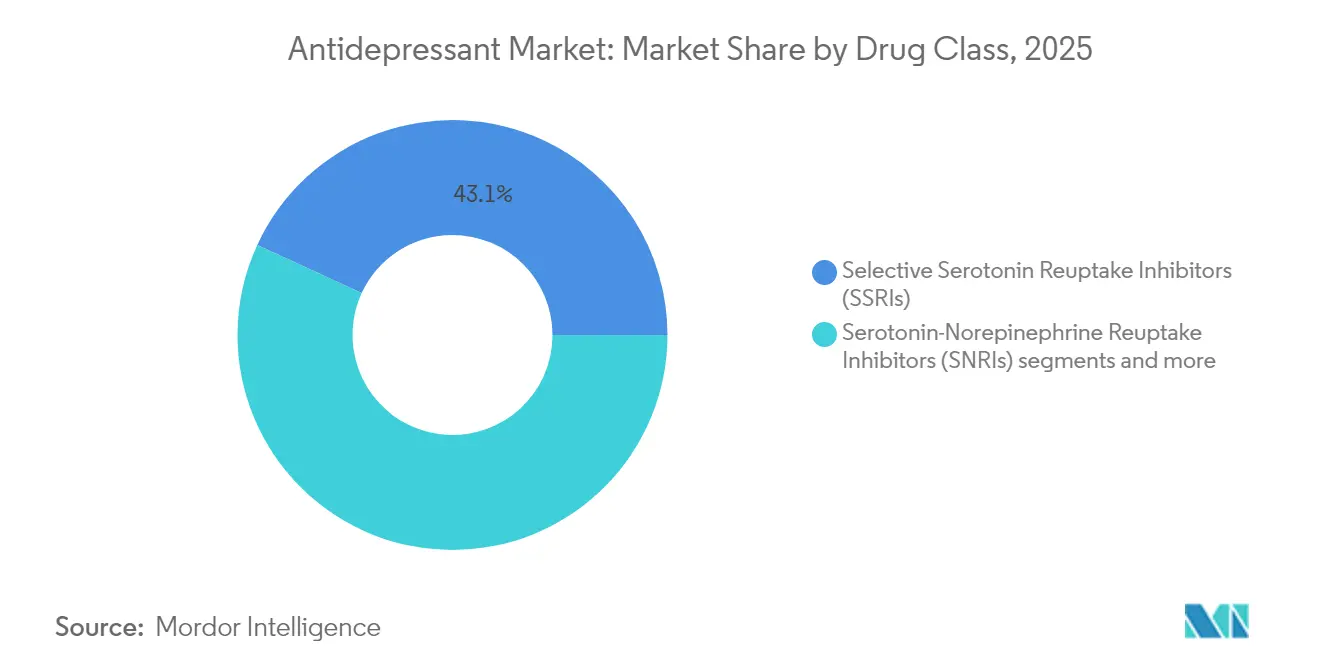

- By drug class, Selective Serotonin Reuptake Inhibitors led with 43.12% of antidepressants market share in 2025, while rapid-acting glutamatergic agents are projected to expand at a 6.78% CAGR through 2031.

- By depressive disorder, Major Depressive Disorder held 36.74% of the antidepressants market size in 2025, whereas postpartum depression is forecast to grow at a 7.03% CAGR to 2031.

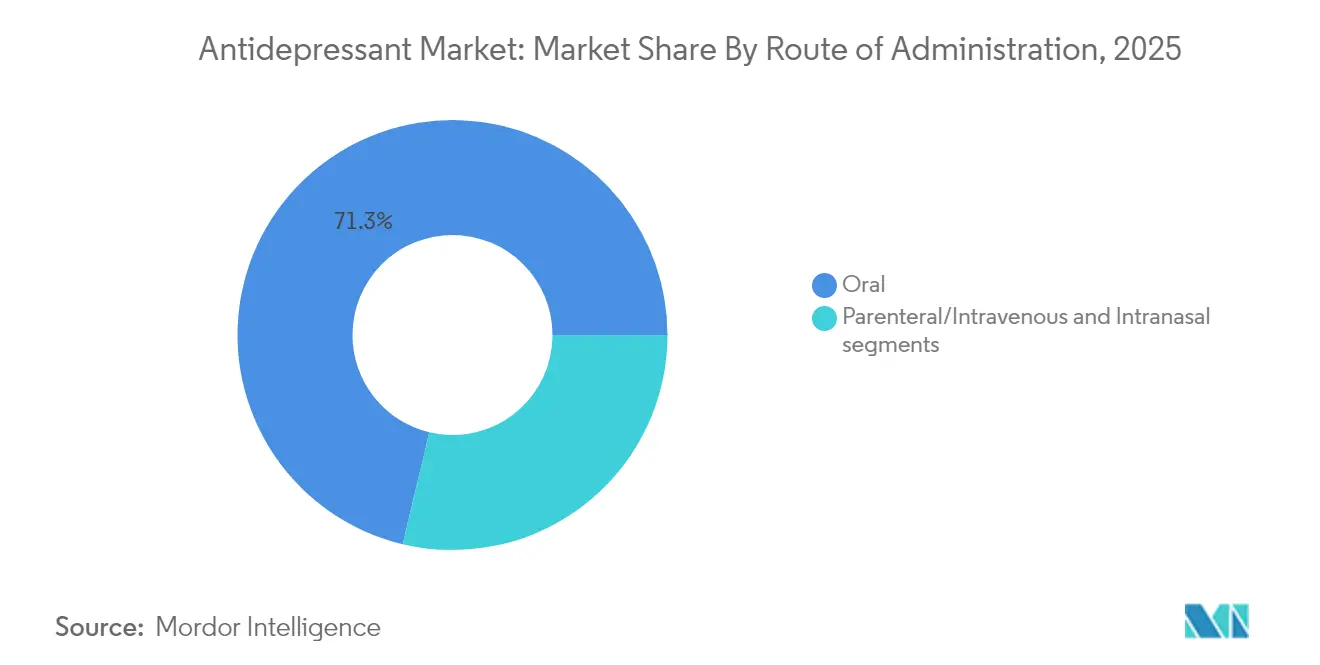

- By route of administration, oral formulations accounted for 71.28% share of the antidepressants market size in 2025, while intranasal delivery is advancing at a 7.66% CAGR through 2031.

- By distribution channel, hospital pharmacies captured 40.12% revenue share in 2025 and online pharmacies are poised to register a 7.36% CAGR over 2026-2031.

- By geography, North America commanded 36.21% of the antidepressants market size in 2025, whereas Asia-Pacific is expanding at an 7.96% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Antidepressant Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of major depressive disorder | +1.2% | Global; highest in North America & Europe | Medium term (2-4 years) |

| Ageing population with higher depression risk | +0.9% | Global; concentrated in developed markets | Long term (≥ 4 years) |

| Frequent launches of next-gen SSRIs/SNRIs | +1.1% | North America, Europe, APAC | Short term (≤ 2 years) |

| Expansion of tele-psychiatry and e-prescriptions | +1.4% | Global; led by North America | Short term (≤ 2 years) |

| Uptake of rapid-acting ketamine/esketamine | +1.6% | North America, Europe, emerging APAC | Medium term (2-4 years) |

| AI-driven precision psychiatry & biomarker diagnostics | +0.8% | North America, Europe, select APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Major Depressive Disorder

Global depression cases climbed to nearly 300 million by 2024, with major depressive disorder representing the largest share. Post-pandemic stress, economic uncertainty, and social isolation have sustained incidence rates, especially among women and older adults. Broader primary-care screening protocols and integrated behavioral-health teams now channel more patients toward evidence-based pharmacotherapy. Insurers increasingly reimburse long-term maintenance regimens, positioning the antidepressants market for continued volume growth. Pharmaceutical pipelines respond with agents promising faster onset and better tolerability, matching evolving clinical expectations.

Ageing Population with Higher Depression Risk

Late-life depression afflicts over 20% of adults older than 50 and far higher proportions in long-term-care settings. Chronic comorbidities complicate choice and dosing of antidepressants, driving R&D toward molecules with minimal drug-interaction potential. Dedicated geriatric trials and formulation tweaks (for example, lower-dose sustained-release tablets) underscore a strategic pivot toward older cohorts. Health-system budgets also face rising indirect costs linked to untreated geriatric depression, spurring earlier pharmacologic intervention.

Frequent Product Launches of Next-Gen SSRIs/SNRIs

Regulators cleared Exxua (gepirone) in 2024, the first 5-HT1A selective agonist for depression [2]Source: U.S. Food and Drug Administration, “Drug Trials Snapshots: Exxua,” U.S. Food and Drug Administration, fda.gov . Ansofaxine, a serotonin-norepinephrine-dopamine reuptake inhibitor, now awaits US authorization after positive Phase III data. These launches target residual challenges of classic SSRIs, chiefly sexual dysfunction and delayed onset. Extended-release and deuterated chemistries heighten metabolic stability, extending once-daily convenience. Aggressive physician-education programs and payer contracting accelerate early market capture.

Expansion of Tele-psychiatry & E-Prescriptions

US claims data show tele-psychiatry visits surging beyond 60% of behavioral-health encounters in 2024. Video consultation normalizes remote mental-health care, collapsing geographic barriers to specialist access. E-prescribing dovetails with digital medication-adherence tools, supporting rapid titration and monitoring. Insurers and state regulators have moved to permanent reimbursement parity for virtual psychiatry, marking a structural channel shift that props up prescription volumes in the antidepressants market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent cliffs & generic erosion | -1.8% | Global; highest in North America & Europe | Short term (≤ 2 years) |

| Adverse-event profile & black-box warnings | -0.9% | Global; regulatory focus in developed markets | Medium term (2-4 years) |

| Shift toward digital therapeutics curbing drug demand | -0.7% | North America, Europe, APAC | Medium term (2-4 years) |

| Regulatory scrutiny on API residues in water bodies | -0.4% | Global; strictest in Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse-Event Profile & Black-Box Warnings

All antidepressants carry FDA black-box warnings about suicidality in patients under 25. High discontinuation rates linked to sexual dysfunction and weight gain spur non-adherence. Innovations like Exxua advertise reduced sexual-side-effect risk, but require electrocardiogram monitoring for QT prolongation, adding complexity. Spravato’s dissociative profile mandates REMS-certified clinics, limiting uptake outside urban areas.

Shift Toward Digital Therapeutics Curbing Drug Demand

Prescription digital therapeutics now deliver guideline-based cognitive-behavioral therapy through smartphones and have secured Center for Medicare & Medicaid Services reimbursement codes. Randomized-controlled trials report comparable efficacy to pharmacotherapy in mild depression. As accountable-care contracts spread, provider systems adopt lower-cost digital first-line options, potentially trimming prescription volumes, especially in maintenance therapy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: SSRIs Remain Cornerstone While Glutamatergic Agents Accelerate Innovation

SSRIs retained a 43.12% antidepressants market share in 2025 owing to decades-long physician familiarity and broad formulary inclusion . Yet the antidepressants market now pivots toward rapid-acting glutamatergic drugs, whose 6.78% CAGR to 2031 will materially enlarge the class footprint. Esketamine’s monotherapy sanction and oral R-ketamine tablets in Phase III exemplify this surge. SNRI incumbents still command meaningful volume, bolstered by dual efficacy in neuropathic pain. Atypicals such as bupropion attract patients seeking weight-neutral or smoking-cessation benefits, cushioning erosion in older tricyclic segments.

Pipeline data confirm a widening mechanistic palette: AMPA-receptor potentiators, neurosteroid agonists, and 5-HT2A psychedelic analogs are each in mid-stage trials. Sustained interest from large-pharma neuroscience franchises coincides with venture-backed biotech exploration, positioning the antidepressants market for successive innovation waves. Brand-lifecycle extensions around SSRIs—including deuterated chemistry and micro-dosing regimens—retain relevance, yet forward-looking strategic capital plows into non-monoaminergic paths promising competitive differentiation.

By Depressive Disorder: MDD Dominates as Postpartum Segment Surges

Major Depressive Disorder held 36.74% of the antidepressants market size in 2025, reflecting its prevalence and strong reimbursement support across health plans. Zurzuvae’s 2024 approval opened a dedicated postpartum-depression submarket projected to climb 7.03% CAGR to 2031. The new once-daily, 14-day neuroactive-steroid course offers relief within 3 days, appealing to new mothers seeking rapid functional restoration. OCD and bipolar-depression niches continue to leverage SSRI and adjunctive antipsychotic use; yet targeted pipeline molecules such as lumateperone aim to sharpen efficacy in symptom clusters like mixed-features depression.

Patient-advocacy campaigns and employer-sponsored maternal-health benefits hasten postpartum-depression diagnosis and treatment specialist referral, cementing long-run volume contributions. Meanwhile, payers increasingly segment formularies by disorder-specific clinical performance, rewarding assets that demonstrate remission within defined timeframes. Hence, manufacturers defending MDD franchises diversify into postpartum or geriatric sub-labels to lock in premium pricing across multiple depressive spectrums, fortifying their stance in the wider antidepressants market.

By Route of Administration: Oral Dominance Faces Intranasal Disruption

Oral tablets and capsules comprised 71.28% of 2025 sales, underscoring entrenched convenience and production economies. Yet intranasal sprays display a 7.66% CAGR, led by esketamine’s clinic-based dosing that bypasses hepatic first-pass metabolism. Parenteral infusions maintain a foothold in tertiary centers, reserved for acute suicidality cases.

Oral-route incumbents counter with extended-release pellets, abuse-deterrent layers, and drug-delivery polymer science to match the rapidity advantages of intranasal modes. Furthermore, AI-supported pharmacokinetic modeling now guides personalized oral dosing schedules that maintain trough serum levels while minimizing peaks driving side effects, thereby fortifying the oral franchise inside the evolving antidepressants market.

By Distribution Channel: Hospital Pharmacies Retain Lead While Online Platforms Surge

Hospital pharmacies controlled 40.12% of revenue in 2025 given the necessity for onsite observation during initiation of agents such as esketamine. Online pharmacies, expanding at 7.36% CAGR, ride the tele-psychiatry wave, offering discreet doorstep delivery that resonates in stigma-sensitive consumer cohorts. Retail chains continue to furnish high-volume SSRI refills, but they are digitizing refill-reminder apps and click-and-collect services to compete.

State policy shifts granting pharmacists provider status allow medication-therapy-management billing, turning retail outlets into community mental-health nodes. Hospital systems meanwhile integrate e-prescribing portals that link directly to their own outpatient pharmacies, solidifying capture of discharge scripts. The channel contest therefore drives service innovation and embedded digital tooling, both of which evolve the broader antidepressants market buying experience.

Geography Analysis

North America held 36.21% of global revenues in 2025 thanks to high per-capita spend, broad insurance coverage, and rapid adoption of accelerated-approval drugs. US FDA policy that balances expedited pathways with stringent post-marketing surveillance anchors the region’s innovation status. Canada’s centralized formularies speed nationwide uptake once Health Canada clears a new agent. Mexico’s Seguro Popular expansion pulls more patients into formal care, lifting generic-SSRI volumes.

Asia-Pacific records the swiftest trajectory at an 7.96% CAGR as urbanization and mental-health literacy grow. China’s 2024 inclusion of toludesvenlafaxine in the National Reimbursement Drug List validated government commitment to psychiatric care funding. India’s domestic-manufacturing push lowers generic costs, widening rural access. Japan’s super-aged demographics and universal health insurance sustain high per-patient drug utilization despite cost-containment efforts. South Korea leverages advanced digital-health infrastructure to integrate mood-tracking wearables with prescription management, illustrating the tech-enabled future of antidepressant care.

Europe shows stable expansion as the European Medicines Agency’s centralized marketing authorization streamlines cross-border launches, while national health-technology-assessment bodies enforce cost-effectiveness hurdles. Germany leads digital-therapeutics reimbursement under its DiGA program, creating complementary or substitutive pressure on drug use. Stringent EU environmental standards on pharmaceutical effluent impose incremental compliance costs, nudging manufacturers toward closed-loop water-recycling plants. Central-Eastern Europe’s rising income levels support branded-generic penetration, though capacity constraints in outpatient psychiatry remain a growth obstacle.

Competitive Landscape

The antidepressants market presents moderate concentration: the top five pharma firms account for about half of branded sales, while generics introduce fragmentation in mature molecules. Johnson & Johnson’s acquisition of Intra-Cellular Therapies in January 2025 installed CAPLYTA as a keystone asset for expansion into MDD, projected at USD 5 billion peak sales. Sage Therapeutics and Biogen co-commercialize zuranolone, tapping women-focused marketing channels and specialty-pharmacy logistics to overcome a USD 16,000 course cost.

AbbVie’s prospective USD 2 billion licensing pact with Gilgamesh marks a big-pharma leap into psychedelic-derived assets, foreshadowing portfolio diversification away from monoamine reuptake inhibition. Lundbeck exits its co-promotion duties on Trintellix, reallocating capital toward Rexulti lifecycle updates and four novel Phase III candidates slated for 2026 readouts fiercepharma.com. Generic entrants—including Zydus Cadila’s vortioxetine—rapidly shave price premiums, but novel-mechanism brands shield value through orphan-like positioning and REMS distribution.

Digital-therapeutics producers, often venture-backed, increasingly partner with drug makers to bundle apps that improve adherence and collect real-world outcomes. Amazon-backed telehealth platforms now offer subscription mental-health bundles integrating e-prescribing and wearable-data dashboards, challenging traditional sales funnels. Success will hinge on synchronized drug-device co-development that proves additive clinical benefit, thereby securing reimbursement.

Antidepressant Industry Leaders

GlaxoSmithKline PLC

Sanofi

AstraZeneca

Eli Lilly and Company

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Johnson & Johnson closed its USD 14.6 billion buyout of Intra-Cellular Therapies, gaining CAPLYTA for bipolar depression and planned MDD expansion.

- March 2025: PharmaTher received a June 2025 FDA goal date for ketamine NDA aimed at easing US supply shortages.

- January 2025: FDA cleared esketamine (Spravato) for standalone use in treatment-resistant depression, the first rapid-acting monotherapy approval.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global antidepressants market as the annual prescription-based sales value of pharmacotherapies indicated for major depressive disorder, dysthymia, anxiety-related conditions (OCD, GAD, panic disorder), chronic and neuropathic pain, captured across all drug classes: SSRIs, SNRIs, TCAs, MAOIs, NMDA receptor antagonists, monoamine modulators, atypical antipsychotic add-ons, and emerging psychedelic compounds. Value is recorded in USD at distributor purchase price and includes branded and generic products dispensed through retail, hospital, and online pharmacies.

Scope Exclusions: Over-the-counter mood supplements, mood stabilizers used mainly for bipolar disorder, and device-based neuromodulation therapies lie outside this estimate.

Segmentation Overview

- By Drug Class (Value)

- NMDA Receptor Antagonists

- Atypical Antipsychotic Augmentation

- Monoamine Modulators (SSRI/SNRI, MAOI, TCA)

- Psychedelics & Novel Compounds

- Others

- By End User (Value)

- Hospitals

- Specialty Clinics

- Homecare & Telepsychiatry

- Research & Academic Centers

- By Distribution Channel (Value)

- Retail Pharmacies

- Hospital Pharmacies

- Online Pharmacies

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with psychiatrists, psychiatric pharmacists, reimbursement advisers, and active-ingredient suppliers across North America, Europe, China, India, and Brazil. Their insights on prescription persistence, off-label use, and likely price erosion enabled us to sharpen input ranges and resolve data gaps before final triangulation.

Desk Research

Mordor analysts first synthesize open datasets from authorities such as the World Health Organization, the US Food & Drug Administration Orange Book, the European Medicines Agency, national prescription audits (e.g., NHS Digital), customs trade dashboards, and peer-reviewed epidemiology journals. Company 10-Ks, investor presentations, patent registries accessed through Questel, and revenue splits from D&B Hoovers supply brand-level anchors and pricing context. Numerous other publicly available and paid sources were also reviewed to cross-check figures and clarify assumptions.

Market-Sizing & Forecasting

Our model begins with a top-down reconstruction of patient pools: diagnosed prevalence multiplied by treatment penetration, average daily dose, and yearly adherence, which is matched to ex-manufacturer revenue reported in audited filings. These results are then cross-checked through sampled average-selling-price-by-volume roll-ups for key molecules. Variables such as generic penetration, patent-expiry timelines, per-capita mental-health spend, reimbursement shifts, and launch probability for pipeline drugs feed a multivariate regression combined with scenario analysis. Limited bottom-up supplier roll-ups are used only to adjust material outliers.

Data Validation & Update Cycle

Mordor analysts compare model outputs with independent prescription audits and historic sales curves; any variance beyond preset thresholds triggers expert re-contact and assumption review before sign-off. Reports refresh every twelve months, with interim updates issued when major approvals, safety withdrawals, or macro shocks alter market fundamentals.

Why Mordor's Antidepressant Baseline Commands Reliability

Published estimates often vary because each publisher chooses its own drug basket, pricing point, and refresh cadence. By selecting a clinically consistent scope, capturing sales across all channels, and recalibrating every year, we offer decision-makers a balanced baseline they can trace and reproduce.

Key gap drivers include whether rapid-acting glutamatergic agents and augmentation therapies are counted, the choice of ex-factory versus pharmacy sell-out pricing, currency conversion years, and the treatment of sudden patent cliffs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 22.13 B (2025) | Mordor Intelligence | |

| USD 18.70 B (2024) | Global Consultancy A | Older base year, narrower drug basket, ex-factory prices only |

| USD 20.11 B (2025) | Industry Association B | Omits NMDA and psychedelic agents, applies rolling three-year average that smooths growth |

| USD 17.90 B (2025) | Trade Journal C | Uses retail consumption values yet excludes hospital channel sales |

These comparisons show that while others provide useful snapshots, Mordor's step-wise reconstruction, cross-channel coverage, and timely refresh make our baseline the most transparent and dependable foundation for strategic planning.

Key Questions Answered in the Report

What is the current size of the antidepressants market?

The antidepressants market reached USD 23.56 billion in 2026 and is forecast to hit USD 32.25 billion by 2031.

Which region leads global sales?

North America held 36.21% of 2025 revenue, driven by high per-capita spending and rapid uptake of innovative drugs.

What drug class is growing fastest?

Glutamatergic agents, including esketamine and oral ketamine candidates, are projected to grow at a 6.78% CAGR through 2031.

How large is the postpartum-depression therapy opportunity?

Postpartum depression therapies are expected to post a 7.03% CAGR, propelled by zuranolone’s launch targeting around 500,000 US women annually.

Will tele-psychiatry affect prescription volumes?

Yes. Tele-psychiatry already accounts for more than 60% of behavioral-health visits in the United States, expanding prescription reach and fueling online-pharmacy growth.

What are the main threats to branded antidepressant revenues?

Patent expirations leading to lower-priced generics, boxed-warning-related adherence issues, and the rise of reimbursed digital therapeutics all exert downward pressure on brand sales.

Page last updated on: