Global Procedure Trays Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.96 Billion |

| Market Size (2031) | USD 41.82 Billion |

| Growth Rate (2026 - 2031) | 10.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

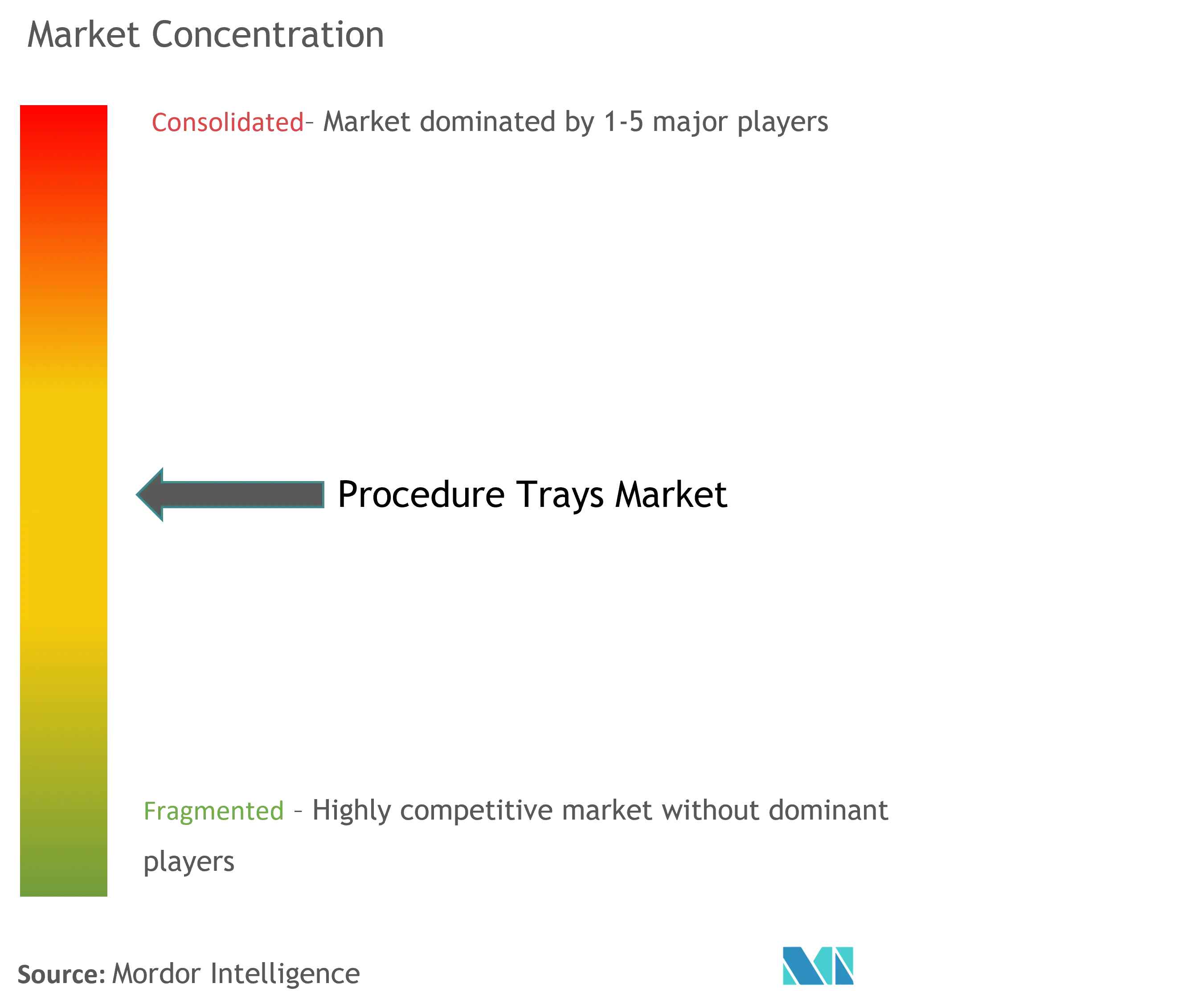

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Procedure Trays Market Analysis by Mordor Intelligence

The procedure trays market size is expected to grow from USD 23.59 billion in 2025 to USD 25.96 billion in 2026 and is forecast to reach USD 41.82 billion by 2031 at 10.03% CAGR over 2026-2031. The projected growth is anchored in health-system priorities to streamline operating room logistics, contain spending, and comply with infection-control standards. Rising minimally invasive and same-day surgery volumes, rapid adoption of vendor-managed inventory programs, and the infusion of AI-enabled configuration software have combined to accelerate uptake of standardized custom procedure trays. Cost pressures have made single-use kits attractive, while sustainability mandates in Europe and tighter ethylene-oxide emissions rules worldwide are pushing suppliers to re-engineer packaging. Intensifying competitive activity—marked by acquisitions, portfolio integration, and investments in digital supply-chain visibility—further underpins the market’s momentum.

Key Report Takeaways

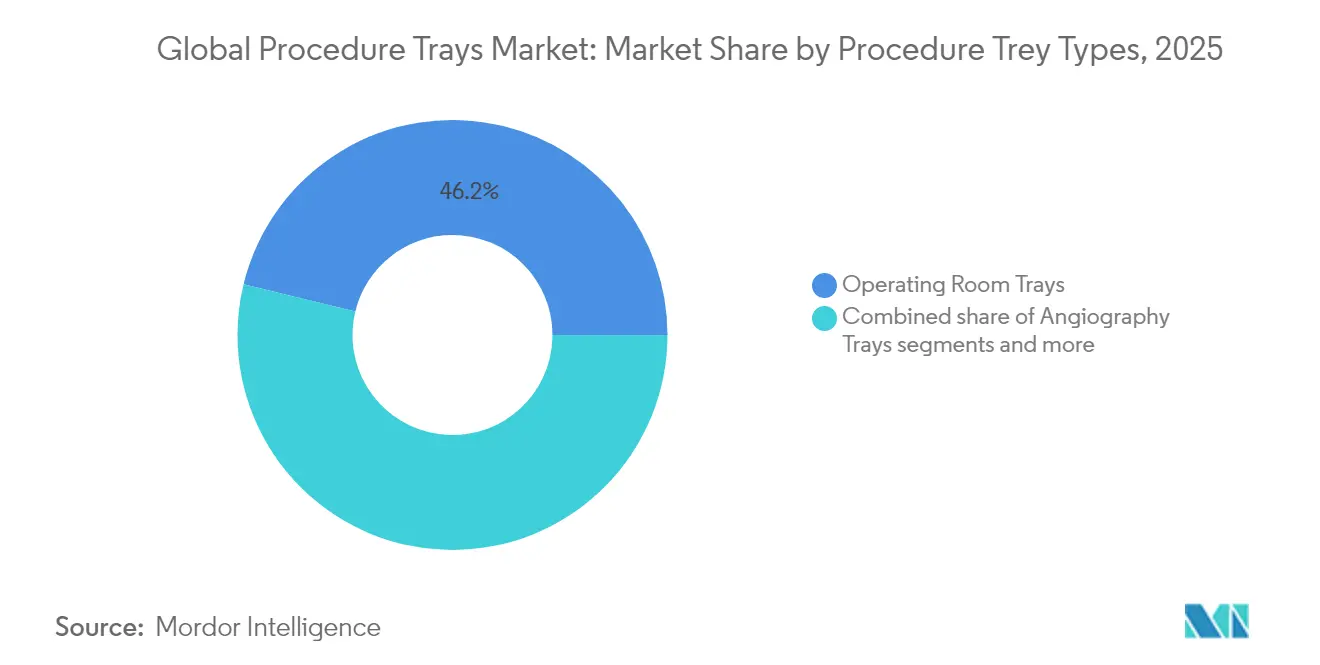

- By procedure tray type, Operating Room Procedure Trays led with 46.21% of procedure trays market share in 2025.

- Anaesthesia Trays are projected to post the highest 10.54% CAGR through 2031 within the procedure trays market size.

- By end user, hospitals accounted for 53.10% of the procedure trays market share in 2025, while ambulatory surgical centers are set to expand at 10.78% CAGR to 2031.

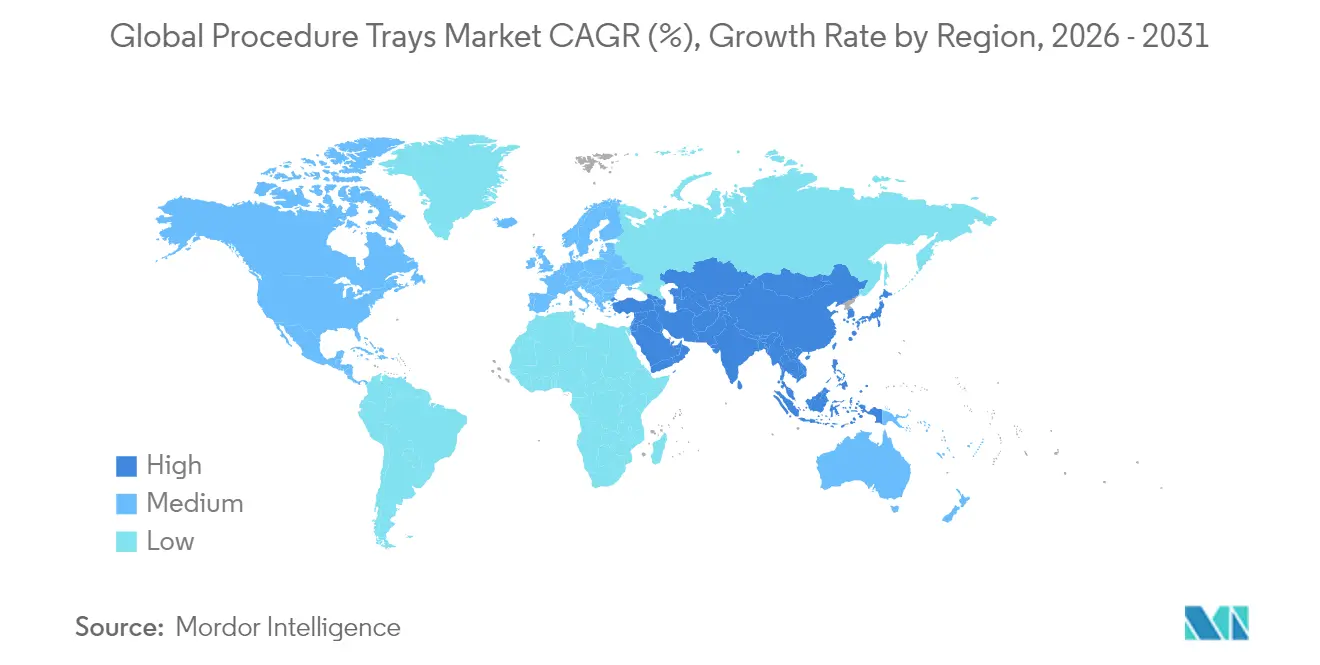

- By geography, North America held 37.95% revenue share in 2025; Asia-Pacific is set to rise at an 11.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Procedure Trays Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in minimally-invasive and day-surgery volumes | +2.1% | Global, with North America & APAC leading adoption | Medium term (2-4 years) |

| Hospital cost-containment push toward single-use CPTs | +1.8% | Global, particularly acute in North America & Europe | Short term (≤ 2 years) |

| Stricter global surgical site-infection (SSI) benchmarks | +1.5% | Global, driven by WHO guidelines and regulatory bodies | Long term (≥ 4 years) |

| Vendor-managed-inventory (VMI) adoption in IDNs | +1.3% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Surge in AI-driven tray-optimization software | +1.0% | North America & Europe early adopters, APAC following | Long term (≥ 4 years) |

| Sustainability mandates favoring life-cycle-assessed kits | +0.8% | Europe leading, North America & APAC adopting gradually | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Minimally Invasive and Day-Surgery Volumes

Ambulatory surgical centers are forecast to boost procedure throughput by 21% between 2024 and 2034, a shift that elevates demand for lighter, single-patient kits designed for fast room turnover[1]Source: StockTitan Market News, “Stryker Completes Acquisition of Inari Medical,” stocktitan.net . CMS has already added 547 new codes to the ASC covered-procedures list for 2026, broadening the clinical scope of outpatient surgery. With ASCs performing operations at 144% lower cost than hospital outpatient departments, payers and patients continue to migrate elective procedures out of inpatient settings. Manufacturers now offer compact procedure trays that preserve sterility yet reduce component counts, cutting setup time and facilitating higher caseloads. The trend is especially beneficial to anaesthesia tray providers because outpatient anesthesia demands purpose-fitted airway, nerve block, and monitoring supplies. Continued growth in endoscopy, arthroscopy, and percutaneous cardiovascular interventions amplifies the requirement for procedure-specific sets.

Hospital Cost-Containment Push Toward Single-Use CPTs

Providers are embracing single-use custom procedure trays as a direct response to rising financial pressure and persistent bottlenecks in sterile processing. Major hospitals discard at least USD 15 million worth of unused surgical supplies each year, with 27% of opened items never touching a patient. Internal Cardinal Health analyses indicate that errors on procedure cards waste 3-5% of annual surgical-supply budgets; for a large facility that is an avoidable cost of more than USD 3 million, while updating just seven procedure cards can save over USD 68,000 per year. Moving to single-use kits eliminates reprocessing expense and lowers contamination risk; hospitals using CensisAI² have processed 20% more trays each month without adding staff. Group purchasing organizations are accelerating adoption by negotiating bulk contracts that make disposable options financially feasible. Artificial-intelligence solutions for OR workflow optimization amplify the benefit: deployments have produced USD 500,000 in annual savings per operating room by improving efficiency and reducing waste. The economic case is strongest in North America, where labor costs are high and regulatory requirements around sterility are stringent.

Stricter Global Surgical Site-Infection Benchmarks

The WHO’s evidence-based SSI guidelines link sterile instrument management to lower infection rates, driving hospitals toward tightly controlled tray assembly and packaging. Healthcare-associated infections add USD 25 billion to USD 45 billion to US expenditure each year. Real-time AI surveillance platforms now track SSI incidence, feeding data back into tray redesign to eliminate contamination vectors. Regulators worldwide are ratcheting up sterilization validation and traceability protocols, so suppliers offering hermetic packaging, RFID labels, and audit-ready documentation gain preference. Providers recognize the downstream savings—fewer readmissions and litigation exposures—outweigh the upfront premium of higher-spec kits.

Vendor-Managed Inventory Adoption in IDNs

Integrated delivery networks partnering on vendor-managed inventory have realized lower cuts in stockholding costs while maintaining service levels. Procedure trays, with predictable consumption curves, fit well within VMI programs that position inventory inside the hospital but on the vendor’s balance sheet. The arrangement releases working capital, standardizes SKUs across campuses, and provides real-time demand data for suppliers. IDNs also expect contingency buffers after pandemic shortages, incentivizing collaborative planning. Vendors able to embed analytics dashboards and automated replenishment engines into hospital ERP systems are differentiating through service rather than price.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price erosion from GPO tenders & bulk buying | -1.9% | Global, most acute in North America | Short term (≤ 2 years) |

| Regulatory scrutiny over plastics waste in OR kits | -1.2% | Europe leading, expanding globally | Medium term (2-4 years) |

| Supply-chain fragility for sterilization capacity | -0.8% | Global, particularly affecting single-source dependencies | Short term (≤ 2 years) |

| Clinician resistance to "one-size-fits-all" custom kits | -0.6% | Global, varying by specialty and institution | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Erosion from GPO Tenders & Bulk Buying

The six largest US GPOs channel nearly 90% of acute-care purchasing, together negotiating over USD 108 billion in volume and forcing double-digit price concessions on high-turn items such as procedure trays. Administrative fees of 1.22%–2.25% diminish manufacturer margins further when tenders cover comprehensive kit portfolios. Value-based contracts now peg price to clinical metrics such as SSI rates or tray-related case delays, transferring outcome risk to suppliers. Smaller vendors struggle to scale tooling changes needed to meet bespoke specs at tendered prices, accelerating consolidation. Inflationary pressure on resin, paper pulp, and labor is unlikely to be fully recouped through GPO negotiations in the near term.

Regulatory Scrutiny Over Plastics Waste in OR Kits

The EU directive mandates that procedure tray packaging be recyclable and carry prescribed recycled content starting 2026, while the US EPA now requires 90% ethylene-oxide emission cuts from sterilizers used on 95% of surgical kits. Compliance forces re-validation of barrier properties whenever materials change, lengthening regulatory cycles and diverting R&D budgets. Hospitals also set voluntary waste-reduction targets, making non-compliant suppliers less competitive in tenders. Although eco-design investments unlock future opportunity, near-term cash flow may tighten as tooling and validation costs rise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Tray Type: Operating Room Dominance Drives Standardization

Operating Room (OR) procedure trays accounted for 46.21% of the custom procedure trays market share in 2025, underscoring their central role in the majority of surgical interventions performed around the world. Their dominance reflects the broad applicability of general surgical procedures and the steady move toward standardized OR protocols that favor pre-assembled configurations. Anaesthesia trays are expanding at a 10.54% CAGR through 2031 as perioperative care grows more complex and more surgeries shift to ambulatory settings, where highly specialized anesthetic management is critical. Angiography trays are benefiting from the rising volume of interventional cardiology procedures; Cardinal Health’s cath-lab and office-based-lab kits illustrate the market’s evolution toward procedure-specific solutions. Ophthalmology trays remain a smaller but steadily growing niche, powered by advances in vitreoretinal instruments and the growing prevalence of age-related ocular disorders that require surgical intervention.

Across the custom procedure trays market, increasing specialization and a sharper focus on clinical outcomes are reshaping demand patterns. A series of workflow studies shows that just 14% of instruments in a typical surgical pan are actually used during a case, revealing substantial opportunities for cost savings through tray optimization. Further, 87% of tray errors stem from lapses in human inspection, driving annual financial losses of USD 6.7 million–9.4 million in lost chargeable OR minutes for large hospitals. A 2024 systematic review reported that revising surgical packs generated 21.8% cost savings and cut waste by 8.06%. Specialty trays outside the major categories, though individually smaller, spur continual innovation as manufacturers develop niche kits to support emerging techniques and subspecialty procedures.

By End User: Hospital Dominance Meets ASC Disruption

Hospitals commanded 53.10% of global revenue in 2025 as they remain the locus for complex surgery, trauma care, and transplantation. In these settings, bulk purchasing through GPOs and vendor-managed inventory programs stabilizes demand and supports recurring tray audits. Yet ambulatory surgical centers are projected to post a 10.78% CAGR, lifting their share of procedure trays market size steadily through 2031. The economic model—lower facility fees and shorter stays—makes pre-sterilized kits indispensable because ASCs lack central sterile departments. With CMS adding hundreds of codes to the ASC roster, spine, cardiac rhythm, and total joint procedures are shifting to outpatient suites, boosting demand for specialty trays configured for smaller workspaces and faster patient turnover.

Clinics and physician offices remain smaller consumers, sourcing minor-procedure sets for dermatology, wound closure, or pain management. However, as reimbursement encourages site-of-service shifts, vendor portfolios that scale from clinic to ASC to hospital stand to capture lifetime customer value. Manufacturers now bundle training and digital preference-card tools to ease transitions, further solidifying relationships across care settings.

Geography Analysis

North America held 37.95% of 2025 revenue thanks to advanced hospital infrastructure, early adoption of AI inventory systems, and mature GPO procurement. Policy frameworks such as the FDA’s Medical Device Single Audit Program accelerate market entry for tray variants, while investment in digital OR integration amplifies demand for RFID-tagged kits. US providers also lead in vendor-managed inventory penetration, creating stickier supplier partnerships and predictable reorder cadence. Canada mirrors US trends although provincial group purchasing has compressed prices, compelling suppliers to demonstrate cost-avoidance value through instrument reduction analytics.

Asia-Pacific is on track for an 11.02% CAGR to 2031, the fastest among all regions. Universal health-insurance expansion and government pushes for domestic manufacturing—exemplified by India’s Production-Linked Incentive scheme—are encouraging local assembly of custom trays, shortening lead times and lowering landed cost. China’s “Buy China” directives prioritize domestically sourced kits for public tenders, spurring joint ventures between global majors and local converters. Procedure-specific sets for endoscopy, laparoscopic gynecology, and orthopedic trauma are gaining traction as tertiary hospitals adopt Western surgical protocols. Uneven sterilization capacity remains a bottleneck, particularly in Southeast Asia, but mobile gamma-irradiation services and shared ethylene-oxide facilities are emerging to bridge the gap.

Europe remains a large yet mature market where sustainability regulation shapes purchasing criteria. The impending EU requirement for recyclable packaging has already prompted many tenders to include environmental scoring. Hospitals in Germany and the Nordics pilot closed-loop recycling of tray wrap, feeding demand for mono-material laminates. Price discipline enforced by statutory insurance keeps overall growth moderate, but high-acuity centers continue to standardize complex cardiac and neuro trays to reduce case variation. Southern Europe lags in adoption owing to fiscal constraints and slower capital-spend cycles.

South America and the Middle East & Africa register mid-single-digit growth as macroeconomic volatility and uneven reimbursement temper expansion. Uptake concentrates in private hospital groups and medical tourism hubs where differentiation hinges on international accreditation and SSI benchmarks. Suppliers focusing on modular tray concepts that can be adapted to locally sourced consumables gain a foothold while circumventing import tariffs.

Competitive Landscape

The field exhibits moderate fragmentation punctuated by consolidation among scale players. Medline’s USD 950 million purchase of Ecolab’s surgical solutions unit in 2024 strengthened its closed-loop value proposition from drapes to sterilization chemicals. Stryker’s USD 4.9 billion acquisition of Inari Medical in 2025[2]Source: ASC Focus Editorial Team, “Annual Report Projects High Growth in ASC Volume,” ascfocus.org broadened its neuro-vascular kit franchise and highlights OEM appetite for procedure-adjacent growth.

Technology capability is the differentiator. Cardinal’s WaveMark analytics, Owens & Minor’s proprietary Kanban replenishment signal growing preference for bundled offerings. Competitive response includes investment in RFID tagging, cloud-based preference-card configurators, and carbon-footprint calculators. Suppliers weak in digital or sustainability credentials risk relegation to price-taker status.

Regional upstarts in India, China, and Mexico court domestic tenders with cost-competitive kits but often lack the clinical training and inventory-management services prized by IDNs. Global incumbents therefore pursue local assembly partnerships to secure price competitiveness while maintaining IP control and quality systems

Global Procedure Trays Industry Leaders

Owens & Minor, Inc

Cardinal Health

Mölnlycke Health Care

Becton, Dickinson, and Company

CPT Medical, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Teleflex completed the EUR 760 million (USD 827 million) purchase of BIOTRONIK’s vascular intervention arm, adding drug-coated balloons and resorbable scaffold R&D pipeline

- February 2025: Stryker closed the USD 4.9 billion Inari Medical acquisition, gaining clot-removal technologies for venous disease

Global Procedure Trays Market Report Scope

As per the scope of the report, procedure trays are the set of all tools and instruments which are being used in surgeries and diagnostic procedures. These trays contain several types of single-use instrument, which minimizes the time and make it convenient for the healthcare professional. The Procedure Trays Market is segmented by Product (Angiography, Operating Room, Ophthalmology), End User (Hospitals, Clinics and Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Operating Room Procedure Trays |

| Angiography Trays |

| Ophthalmology Trays |

| Anaesthesia Trays |

| Other Specialty Trays |

| Hospitals |

| Ambulatory Surgical Centers |

| Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Procedure Tray Type | Operating Room Procedure Trays | |

| Angiography Trays | ||

| Ophthalmology Trays | ||

| Anaesthesia Trays | ||

| Other Specialty Trays | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the procedure trays market in 2026?

The procedure trays market size is valued at USD 25.96 billion in 2026.

What is the expected growth rate for procedure trays through 2031?

Revenue is projected to rise at a 10.03% CAGR, reaching USD 41.82 billion by 2031.

Which procedure tray segment is expanding the fastest?

Anaesthesia trays are forecast to grow at a 10.54% CAGR due to increasing outpatient anesthesia workloads.

Why are ambulatory surgical centers important for tray suppliers?

ASCs rely on ready-to-use sterile kits to keep turnover high and costs low, driving a 10.78% CAGR in tray demand.

How are sustainability regulations affecting tray design?

EU rules require all medical packaging to be recyclable by 2030, prompting suppliers to shift to mono-material, low-carbon wraps.

Page last updated on: