Polyvinylidene Chloride (PVDC) Coated Films Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

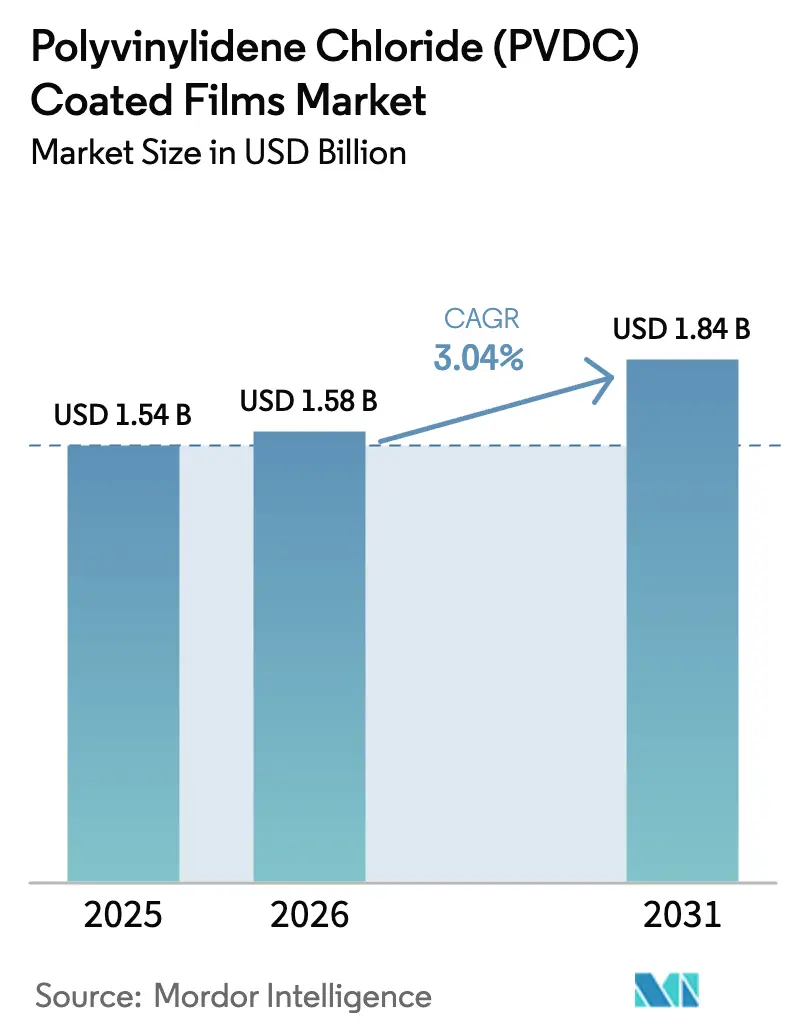

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 1.84 Billion |

| Growth Rate (2026 - 2031) | 3.04% CAGR |

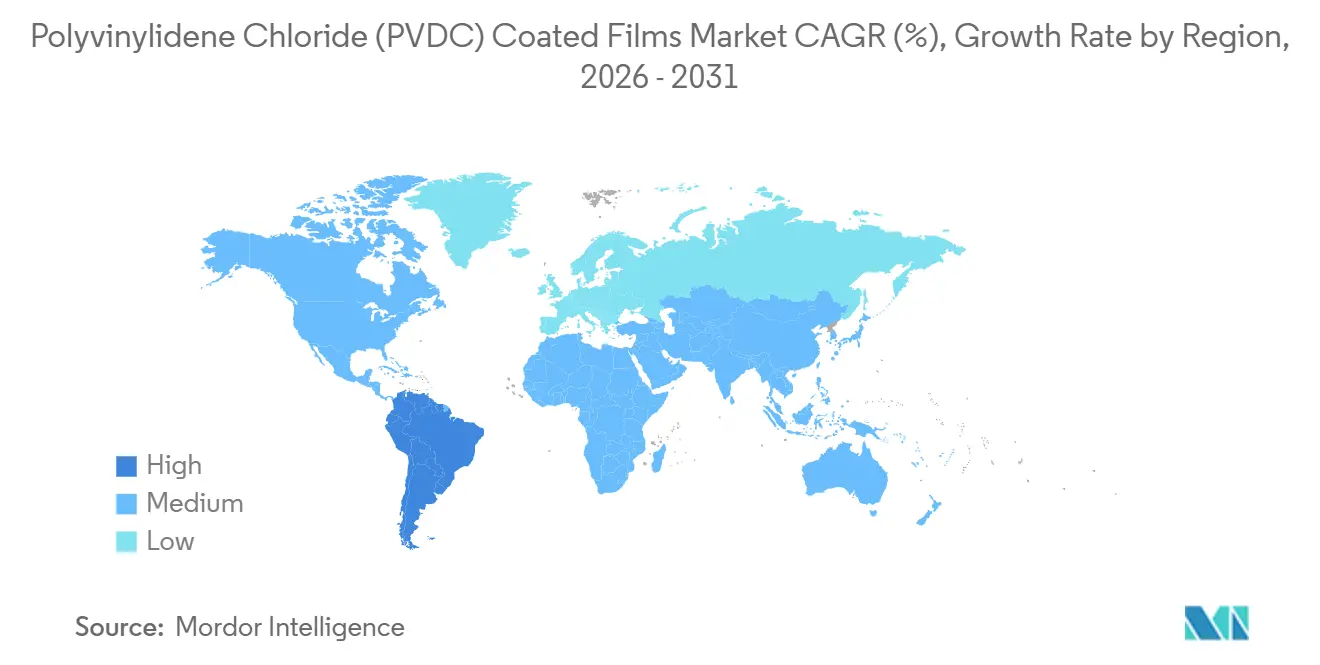

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyvinylidene Chloride (PVDC) Coated Films Market Analysis by Mordor Intelligence

The Polyvinylidene Chloride Coated Films Market size was valued at USD 1.54 billion in 2025 and is estimated to grow from USD 1.58 billion in 2026 to reach USD 1.84 billion by 2031, at a CAGR of 3.04% during the forecast period (2026-2031). This steady climb reflects persistent demand from food brands that require oxygen- and moisture-tight packs for chilled meat, cheese, and ready-to-eat meals, as well as pharmaceutical companies that rely on blister formats to safeguard moisture-sensitive active ingredients. Growth is tempered by expanding adoption of recyclable mono-material EVOH and polyolefin structures that help brand owners satisfy circular-economy targets. Producers are also wrestling with higher vinylidene-chloride (VDC) feedstock costs as European chlor-alkali plants decarbonize, raising the appeal of lighter-coat PVDC grades that reduce resin use. Meanwhile, trial success in mechanically recycling PE/PVDC multilayers suggests that end-of-life objections may soften if waste handlers accept these films into polyethylene streams.

Key Report Takeaways

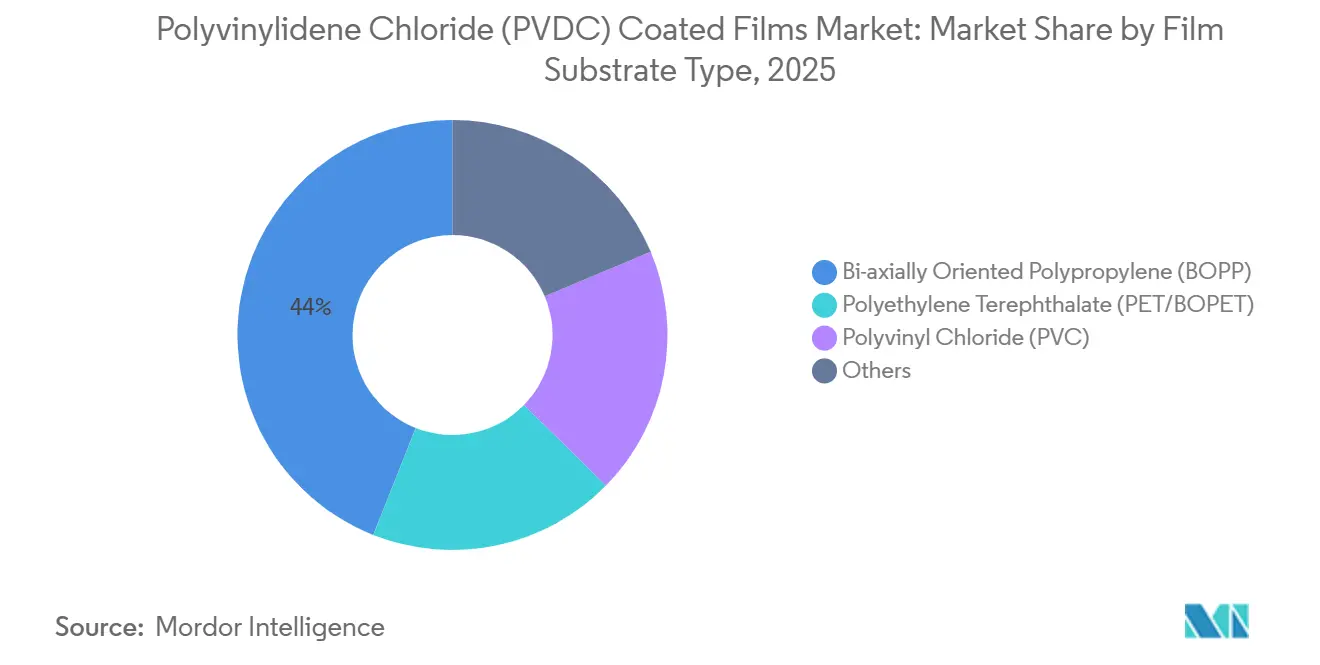

- By film substrate, bi-axially oriented polypropylene (BOPP) led with 44% of the PVDC-coated films market share in 2025. Polyvinyl chloride (PVC) is forecast to expand at a 3.67% CAGR through 2031.

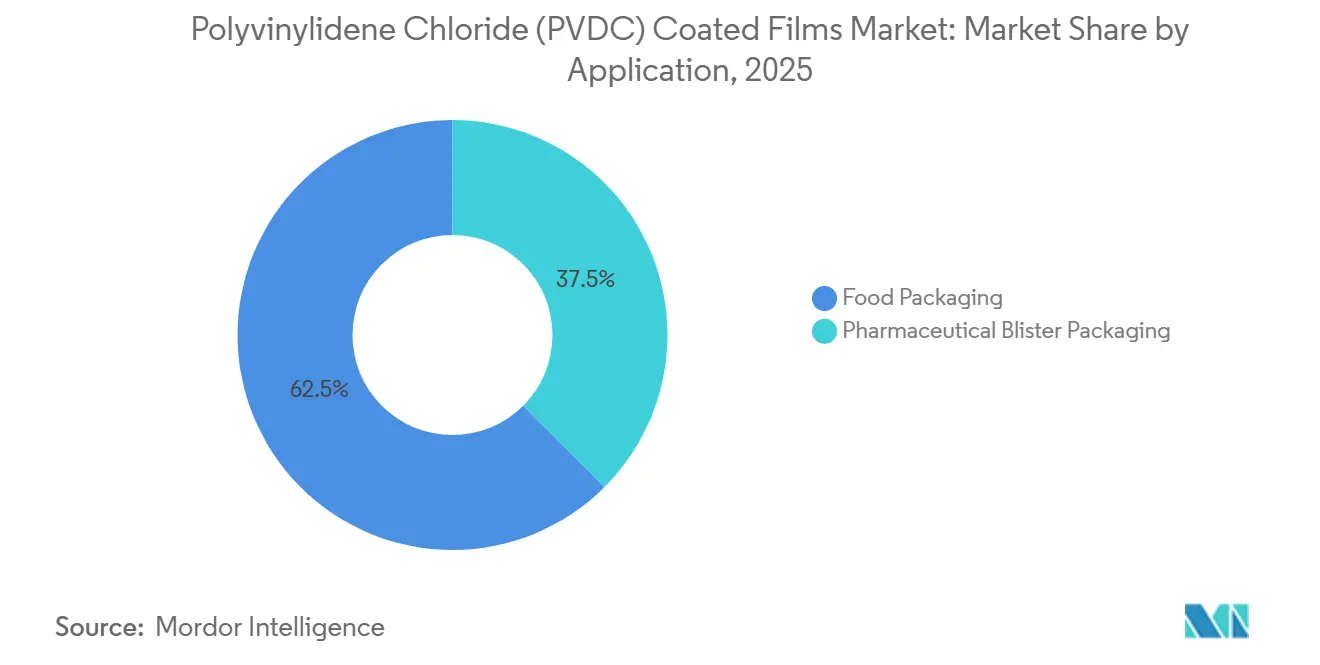

- By application, food packaging accounted for 62.50% of demand in 2025. Pharmaceutical blister packaging is advancing at a 4.38% CAGR through 2031.

- By geography, Asia-Pacific captured 41.38% revenue in 2025, while South America records the fastest regional CAGR of 3.57% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyvinylidene Chloride (PVDC) Coated Films Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processed and Ready-to-Eat Food Boom | +1.2% | Global, with strongest uptake in Asia-Pacific urban centers and North America convenience retail | Medium term (2-4 years) |

| Pharmaceutical Blister‐Pack Adoption Surge | +0.9% | Europe, North America, and India (generic-drug export hubs) | Long term (≥ 4 years) |

| Superior Gas- and Moisture-Barrier Performance | +0.7% | Global, particularly critical in tropical/humid climates (Southeast Asia, South America, Middle East) | Short term (≤ 2 years) |

| Shift to Ultra-Thin (less than 15 µm) PVDC Coatings | +0.5% | Europe and North America, driven by lightweighting mandates and plastic-tax minimization | Medium term (2-4 years) |

| Emergence of PFAS-Free Fluorine-Free PVDC Grades | +0.4% | North America and European Union, in response to FDA and EFSA food-contact restrictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Processed and Ready-to-Eat Food Boom

As urban incomes rise and lifestyles grow busier, there's a heightened demand for portion-controlled, shelf-stable meals. These meals need to remain fresh for an extended period during chilled distribution. PVDC-coated BOPP and PET films facilitate modified-atmosphere packaging, effectively curbing lipid oxidation and microbial spoilage. In response to surging orders from ready-meal brands in India and the Middle East, UFlex is ramping up production of barrier film in Karnataka. Brand owners are now opting for thinner coatings over traditional designs, achieving cost reductions while maintaining shelf life. While compliance with FDA 21 CFR 177.1980 and EU 10/2011 is essential, converters can gain a competitive advantage by certifying pasteurization durability at high temperatures.

Pharmaceutical Blister-Pack Adoption Surge

Producers of generic drugs in India and Eastern Europe are shifting from strip packs to thermoformed PVC/PVDC blisters. This move is to meet the ICH Q1A moisture-barrier criteria for active pharmaceutical ingredients (APIs) like aspirin and antibiotics. PVC laminated with PVDC ensures a longer shelf life even in Zone IVb climates. Despite undergoing a Chapter 11 restructuring, Klöckner Pentaplast is doubling down on investments in pharmaceutical-grade PVC/PVDC. The company is keenly aware of the premium margins associated with ultra-high-barrier grades, which are essential for biologics. The European Medicines Agency's guidance on package-integrity testing has solidified PVDC's significance in the industry. This is especially true given that alternative ceramic-oxide coatings don't have robust long-term field data backing their efficacy.

Superior Gas and Moisture Barrier Performance

PVDC's crystalline VDC-MA structure offers oxygen permeability that's significantly lower than EVOH, especially under high humidity. This advantage is particularly beneficial in regions like Southeast Asia, South America, and the Middle East, where humidity levels frequently surpass 70%. Comparative trials show chilled beef in PVDC-coated BOPP maintains color stability longer than in EVOH laminates under 4 °C storage[1]Syensqo press team, “Syensqo achieves breakthrough in mechanical recycling of PVDC multilayer food packaging,” Syensqo, syensqo.com. High-shrink PVDC grades help sausage casings modulate CO₂ and O₂ exchange, while ultra-low-WVTR formulations protect dried fruit from moisture pickup during monsoon warehousing.

Shift to Ultra-Thin (less than 15 µm) PVDC Coatings

In Europe, plastic-tax penalties and demand-weighted fees in the UK are pushing converters to reduce coat weight. Syensqo’s Diofan Ultra736 is facilitating thinner dry coatings by boosting emulsion solids and minimizing pinhole risks. New lines in Europe are now commonly equipped with inline gravimetric sensors and closed-loop tension control, ensuring coat-weight variations remain within ±3 g/m².

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from EVOH and Metallized Barriers | -0.8% | Europe and North America, where recyclability and RecyClass certification drive material selection | Medium term (2-4 years) |

| End-of-Life/Chlorine-based Recycling Concerns | -0.6% | European Union (PPWR mandates), United Kingdom, and select United States states with advanced EPR frameworks | Long term (≥ 4 years) |

| VDC-Monomer Supply Volatility Amid Chlor-Alkali Decarbonisation | -0.4% | Global, with acute pressure in Europe due to energy-intensive electrolysis and carbon-border-adjustment mechanisms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from EVOH and Metallized Barriers

Nine-layer blown EVOH films commissioned by Coveris in the United Kingdom provide sub-1 cm³/m²/day OTR in dry conditions and can be recycled within polyethylene waste streams[2]Coveris communications, “Coveris announces major investment in technical films capacity,” Coveris, coveris.com. Falling EVOH resin prices and rising VDC costs are shrinking PVDC’s historical cost edge, particularly in dry-goods packaging where absolute humidity is low. Metallized PET and AlOx-coated films additionally appeal to snack-food brands that demand a light barrier, although opacity restricts their use for fresh meat.

End-of-Life / Chlorine-Based Recycling Concerns

PVDC’s chlorine content raises worries about hydrochloric acid release during incineration and contamination of polyolefin recycle streams. The EU Packaging and Packaging Waste Regulation requires practical recyclability by 2030, placing PVDC multilayers under scrutiny. Syensqo’s 2025 mechanical-recycling breakthrough shows PE/PVDC films can be reprocessed at 220 °C without stabilizers, yet municipal acceptance is inconsistent and converters must still pay national plastic taxes in Germany and France.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Film Substrate Type: BOPP Dominance Driven by Cost and Machinability

BOPP claimed a 44% share of the PVDC-coated films market in 2025, reflecting its low resin cost and high run speeds on rotogravure coaters. Many converters adeptly process 20 µm BOPP bases at high speeds, achieving the tensile strength essential for bone-in meat packaging. BOPET, catering to premium trays subjected to mild pasteurization, commands a notable price premium. While PVC holds only a modest volume share, it will log the fastest 3.67% CAGR because of blister demand. The market size for PVDC-coated films linked to polyvinyl chloride is set to rise in the coming years. Additionally, specialty niches like polyamide sausage casings and PLA stand-up pouches contribute to the “others” category.

BOPP’s lead faces challenges from recyclable mono-PP lidding, achieving low OTR without the need for PVDC. Should upcoming scale-up trials prove successful, downgauged mono-PP might threaten BOPP’s market share in PVDC-coated films by decade's end. However, any transition depends on converters confirming barrier stability at high relative humidity, a benchmark currently favoring PVDC structures.

By Application: Food Packaging Volume Versus Pharmaceutical Growth

Food accounted for 62.5% of segment revenue in 2025, with chilled meats leading the charge, necessitating an OTR of less than 5 cm³/m²/day. Retailers appreciate PVDC's clarity, allowing shoppers to verify meat color—an edge that metallized and ceramic-oxide films lack. Yet, with a growing focus on RecyClass certification, dry-goods brands are increasingly leaning towards EVOH.

Pharmaceutical blister packs, while smaller, are rising at a 4.38% CAGR through 2031. The market for PVDC-coated films in blister formats is driven by India's expanding generic-drug exports and the introduction of moisture-sensitive biologics in the United States and Europe. Drug manufacturers, seeking a three-year shelf life, are gravitating towards ultra-high-barrier PVDC grades, which are priced higher than standard laminates, due to their OTR requirement.

Geography Analysis

Asia-Pacific held 41.38% of the PVDC-coated films market revenue in 2025 on the back of India’s and China’s integrated film capacity and strong retail modernization. Jindal Poly Films and Cosmo Films run in-house PVDC coating that lets them tweak barrier properties to local humidity and distribution conditions. Rising blister exports from India to regulated markets further underpin demand.

South America, led by Brazil and Argentina, posts the fastest 3.57% regional CAGR to 2031. As supermarket penetration rises, converters upgrade from waxed wraps to PVDC high-barrier films that extend refrigerated shelf life. Domestic regulations are less stringent on recyclability, giving PVDC a window of opportunity even as European brand owners tighten specifications.

North America balances strong blister-pack growth with early extended-producer-responsibility (EPR) moves in California and Maine that penalize non-recyclable formats. Syensqo’s recycling breakthrough could mitigate these fees if sortation systems accept PE/PVDC multilayers. Europe presents the stiffest challenge: the Packaging and Packaging Waste Regulation demands recyclability at scale by 2030 and levies plastic taxes on non-recyclables. Some municipal systems have begun to trial the Syensqo protocol, but acceptance is far from uniform. The Middle East and Africa remain small yet rising, with Saudi Arabia’s premium dairy segment and South Africa’s pharmaceutical imports driving niche demand.

Competitive Landscape

The polyvinylidene chloride (PVDC) coated films market is moderately fragmented. Regional converters compete by offering substrate variety and short lead times. Many maintain parallel EVOH lines to pivot when VDC pricing spikes. Disruptors push ceramic-oxide-coated PET that matches PVDC’s OTR in dry climates and flows into PET recycle streams, attracting snack and coffee brands focusing on light and oxygen barrier. Yet PVDC retains a defensible niche in humid markets and in medical packs where multi-year barrier data trump recyclability.

Polyvinylidene Chloride (PVDC) Coated Films Industry Leaders

CCL Industries

KUREHA CORPORATION

UNITIKA LTD

Jindal Poly Films Limited

Klöckner Pentaplast

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Syensqo announced successful mechanical-recycling trials for multilayer food films containing Ixan PVDC (structure: PE/EVA/Ixan PVDC/EVA/PE), validated by CSI (IMQ group) under EN 13430.

- March 2025: Pregis expanded EVOH blown-film capacity in Anderson, South Carolina, offering a mono-PE structure to replace metallized or PVDC films.

Global Polyvinylidene Chloride (PVDC) Coated Films Market Report Scope

PVDC-coated films are obtained by coating OPP or other types of base film with a very thin layer of PVDC. It is widely used as a packaging material that provides moisture-proofing and gas-barrier properties in addition to the properties of the base film. Low dependency on the oxygen barrier property on humidity, moisture-barrier property, and excellent aroma-retaining properties further increase its market concentration for the food industry. The polyvinylidene chloride market is segmented by film substrate type, application, and geography. By film substrate type, the market is segmented into bi-axially oriented polypropylene (BOPP), polyethylene terephthalate (PET/BOPET), polyvinyl chloride (PVC), and others. By application, the market is segmented into food packaging and pharmaceutical blister packaging. The report also covers the market size and forecasts for the market in 15 countries across the globe. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Bi-axially Oriented Polypropylene (BOPP) |

| Polyethylene Terephthalate (PET/BOPET) |

| Polyvinyl Chloride (PVC) |

| Others (Polyethylene, polyamide,PLA, Cellulosics etc.) |

| Food Packaging |

| Pharmaceutical Blister Packaging |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Film Substrate Type | Bi-axially Oriented Polypropylene (BOPP) | |

| Polyethylene Terephthalate (PET/BOPET) | ||

| Polyvinyl Chloride (PVC) | ||

| Others (Polyethylene, polyamide,PLA, Cellulosics etc.) | ||

| By Application | Food Packaging | |

| Pharmaceutical Blister Packaging | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the PVDC-coated films market?

It stands at USD 1.58 billion in 2026 and is forecast to reach USD 1.84 billion by 2031, registering a CAGR of 3.04%.

Which end-use segment is growing fastest for PVDC-based films?

Pharmaceutical blister packaging is advancing at a 4.38% CAGR through 2031, outpacing food applications.

Which region adds capacity most aggressively?

Asia-Pacific, led by India and China, continues to commission new PVDC coating lines to meet domestic and export demand.

What technology threatens PVDC in food packs?

Nine-layer EVOH films and ceramic-oxide-coated PET are gaining share where recyclability outweighs absolute barrier strength.

Which substrate currently dominates?

BOPP holds 44% of the global share because of cost advantages and high-speed coatability.

Page last updated on: